Comparative Review of Governance Structures for Ecosystem ...

2513095 © Chapman Tripp

Iwi corporate structures and governance

Te Tau Ihu Economic Summit

OCTOBER 2012

Iwi corporate structures and governance 19 OCTOBER 2012 / 2

2513095 © Chapman Tripp

Beyond Treaty settlements

• The Treaty settlement process has been a feature of the New Zealand landscape, in some shape or form, long before the establishment of the Waitangi Tribunal in 1975 – and much has been learnt along the way

• Now, the majority of iwi have either concluded Treaty settlements or are in the process of doing so

• As a result, iwi are now putting in place different structures and strategies to grow their settlement assets

• We recommend structures which build on those currently being implemented and moving away from the largely charitable model implemented as part of earlier settlements

Iwi corporate structures and governance 19 OCTOBER 2012 / 3

2513095 © Chapman Tripp

PSGE structures

• As a pre-condition of settlement, the Crown requires iwi to put in place a post-settlement governance entity (“PSGE”)

• The PSGE must be:

― Representative of the claimant group

― Transparent in its decision-making and dispute resolution procedures

― Accountable to the claimant group

― For the benefit of the members of the claimant group

― Ratified by the claimant group

Iwi corporate structures and governance 19 OCTOBER 2012 / 4

2513095 © Chapman Tripp

Commonly used PSGE structure PSGE

• Receives the settlement assets, and may hold certain cultural redress assets

• Usually a private trust

• May be a registered tax charity

• Trustees are members of the claimant group, and are often all elected at the same time

Asset Holding Company

• Holds and manages the claimant group’s commercial assets (obtained before and through the settlement), and provides funds to the PSGE by way of dividend payments

• Limited liability company, wholly owned by PSGE

• May be a registered tax charity

• Directors are usually appointed by the trustees of the PSGE

• May have a number of subsidiaries

Social Services Provider

• Provides social benefits to members of the claimant group (e.g. education grants, health services)

• The PSGE may also undertake some social functions itself

• Usually a tax charity

• Entities providing social benefits will usually be charitable

PSGE [Usually a tax

charity]

Directors

Asset Holding Company [May be a tax charity]

Trustees

Social Services Trust

[Usually a tax charity]

Elected Trustees

Sometimes a merged entity

Iwi corporate structures and governance 19 OCTOBER 2012 / 5

2513095 © Chapman Tripp

Commonly used PSGE structure

Key Issues:

1. The trustees are often exposed to personal liability

2. Charitable entities are prohibited from making non-charitable distributions; therefore, a charitable structure does not allow for non-charitable distributions/benefits to claimant group members

3. If a charitable trust (in our example structure, the Social Services Trust) receives income derived from business activities, it is prohibited from making charitable distributions to claimant group members living overseas

4. Lack of stability with certain structures due to uncertainty around delegated authority

5. The claimant group may lack the expertise to effectively govern and manage its commercial asset holding company

6. Sudden changes of control, policy and direction

I will address each of these key issues during the course of this presentation, and discuss different structuring options for solving each issue

Iwi corporate structures and governance 19 OCTOBER 2012 / 6

2513095 © Chapman Tripp

Commonly used entities

• We will look at the key characteristics of the

following entities commonly used by iwi in their

post-settlement structures:

1. Trusts

2. Incorporated societies

3. Companies

4. Limited partnerships

Iwi corporate structures and governance 19 OCTOBER 2012 / 7

2513095 © Chapman Tripp

1. Trusts: Key characteristics

Legal personality:

• Not a separate legal entity – cannot contract in its own name or own property

• All trust property vests in the trustees personally, and is held on trust by them for the benefit of the claimant group

• Perpetuity period of 80 years applies (unless the trust is charitable, in which case there is perpetual succession)

Iwi corporate structures and governance 19 OCTOBER 2012 / 8

2513095 © Chapman Tripp

1. Trusts: Key characteristics

Governed by:

• Its trust deed, which is a private document (although PSGE trust deed is normally made available to claimant group members)

• Trustee Act 1956

• If charitable, the trust can be incorporated as a board under the Charitable Trusts Act 1957

• Other rules developed by the courts over time (i.e. equity)

Under each of these governing documents and laws, trustees owe certain fiduciary duties to the beneficiaries of the trust – in this case, to the members of the claimant group

If the trustees fail to discharge any of these duties, they can be personally liable for breach of trust

Iwi corporate structures and governance 19 OCTOBER 2012 / 9

2513095 © Chapman Tripp

1. Trusts

Key Issue 1: Trustees are often exposed to personal liability

• Trustees owe duties to the beneficiaries of the trust (i.e. to the claimant group) personally – this means that they will be personally liable if they fail to discharge, or breach, a duty

• In certain circumstances, the trustees may be indemnified out of the trust fund – however, this does not offer watertight protection

Iwi corporate structures and governance 19 OCTOBER 2012 / 10

2513095 © Chapman Tripp

1. Trusts

Generally two types of entity to choose from:

1. Incorporated society

2. Company

We discuss our recommended option shortly...

Solution: Incorporate an entity to be the corporate trustee of the PSGE trust

PSGE Corporate Trustee

Elected representatives

are directors and shareholders

Trustee

Iwi corporate structures and governance 19 OCTOBER 2012 / 11

2513095 © Chapman Tripp

1. Trusts

Key Issue 2: Charitable entities are prohibited from making non-charitable distributions; therefore, a charitable structure does not allow for non-charitable distributions to

claimant group members

Iwi corporate structures and governance 19 OCTOBER 2012 / 12

2513095 © Chapman Tripp

1. Trusts

Solution:

• The PSGE trust remains a non-charitable entity – this will allow it to make non-charitable distributions to members of the claimant group

• A new charitable trust is created with the Corporate Trustee as the settlor (“Charitable Trust 1”)

• A new entity is created to be the corporate trustee of the new charitable trust (“Corporate Trustee 2”)

Iwi corporate structures and governance 19 OCTOBER 2012 / 13

2513095 © Chapman Tripp

1. Trusts

Key Issue 3: If a charitable trust (in our example structure, the Social Services Trust)

receives income derived from business activities, it is prohibited from making

charitable distributions to claimant group members living overseas

Iwi corporate structures and governance 19 OCTOBER 2012 / 14

2513095 © Chapman Tripp

1. Trusts

Solution:

• Create a second charitable trust which will receive non-business income only (“Charitable Trust 2”) – this will allow it to make charitable distributions overseas

• Corporate Trustee 2 will also be the corporate trustee of Charitable Trust 2

Iwi corporate structures and governance 19 OCTOBER 2012 / 15

2513095 © Chapman Tripp

2. Incorporated societies: Key characteristics Legal personality:

• Is not expressly a separate legal entity, but does possess certain characteristics of a separate legal entity, including:

― Perpetual succession

― Able to sue and be sued

• An incorporated society can own property, but may only enter into contracts as permitted by its rules

• A contract that is ultra vires the rules of the society cannot be enforced by either party

Governed by:

• Incorporated Societies Act 1908

• Its rules, which are publicly available via the Companies Office website

Iwi corporate structures and governance 19 OCTOBER 2012 / 16

2513095 © Chapman Tripp

2. Incorporated societies

Key Issue 4: Lack of stability due to uncertainty around delegated authority

Example: Waikato-Tainui Te Kauhanganui Incorporated

Iwi corporate structures and governance 19 OCTOBER 2012 / 17

2513095 © Chapman Tripp

2. Incorporated societies: Instability?

• Mahuta v Porima (2000): The Queen’s Representative challenged the decision of Te Kaumaarua to enter into an agreement to sell the Auckland Warriors Rugby League Club Ltd; challenge failed

• Porima v Te Kauhanganui o Waikato Inc (2000): Six elected members must have authority to make decisions, even without the requisite quorum as specified in the rules – to do otherwise would “leave a complete void in Tainui’s affairs”

• Mahuta v Porima (2000): Group opposing six elected members of Te Kaumaarua attempted to call a meeting to remove those members; Court ruled the meeting invalidly called

Iwi corporate structures and governance 19 OCTOBER 2012 / 18

2513095 © Chapman Tripp

2. Incorporated societies: Instability?

• Porima v Waikato Raupatu Trustee Company Ltd (2010): Meeting of directors not validly held, and notice of meeting contained insufficient notice of resolution to remove directors and other employees of the company

• Solomon v Waikato Raupatu Trustee Company Ltd (2004): Notice of directors’ meeting contained insufficient notice of proposed disciplinary action against director; purported suspension of that director therefore invalid

• Roa v Morgan (2009): Matters of governance must be decided by Te Kauhanganui, including any decision relating to the structure of the Waikato-Tainui group

Iwi corporate structures and governance 19 OCTOBER 2012 / 19

2513095 © Chapman Tripp

2. Incorporated societies: Instability?

• Martin v Morgan (2011): Application for injunction bought by T Martin to prevent her removal as Chair of Te Kauhanganui; application not granted as unnecessary

• Waikato-Tainui Te Kauhanganui Inc v Martin (2011): Application for injunction bought by Te Kauhanganui on the direction of Te Arataura, to prevent the Chair of Te Kauhanganui from proceeding with the half-yearly general meeting; application granted

• Morgan v Martin (2011): Application bought by T Morgan for declaration that resolution removing him as a member of Te Kauhanganui invalid; application granted

Iwi corporate structures and governance 19 OCTOBER 2012 / 20

2513095 © Chapman Tripp

2. Incorporated societies: Instability?

• Waikato-Tainui Te Kauhanganui Inc v Martin (2012): Application for injunction bought on the direction of Te Arataura to prevent Chair of Te Kauhanganui from proceeding with “induction” meeting; application refused

• Waikato-Tainui Te Kauhanganui Inc v Martin (2012): Application for injunction bought on the direction of Te Arataura to prevent meeting, at which it was proposed that new members of Te Arataura be elected under the new rules; application refused

• Takerei v Roa (2012): Application for declaration as to validity of Hiiona Marae elections, bought by the Chair of Te Kauhanganui (and others); application granted

Iwi corporate structures and governance 19 OCTOBER 2012 / 21

2513095 © Chapman Tripp

2. Incorporated societies

Solution: Do not use an incorporated society within the PSGE structure. We recommend using a company as the corporate trustee of

the PSGE trust

• Lack of legal authority and precedent relating to incorporated societies makes it an unstable structure

• Companies are more recognised

Iwi corporate structures and governance 19 OCTOBER 2012 / 22

2513095 © Chapman Tripp

3. Companies: Key characteristics

Legal personality:

• Separate legal entity – can contract in its own name, and own property

• Perpetual succession

Governed by:

• Companies Act 1993

• Constitution (if it decides to adopt one), which is publicly available via the Companies Office website

Iwi corporate structures and governance 19 OCTOBER 2012 / 23

2513095 © Chapman Tripp

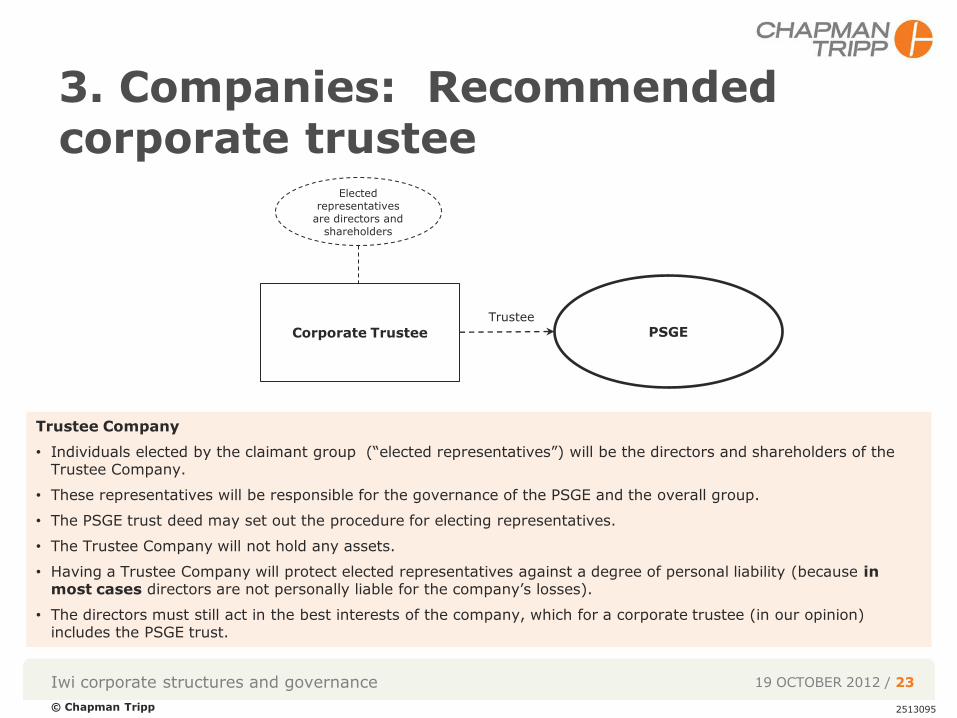

3. Companies: Recommended corporate trustee

PSGE Corporate Trustee

Elected representatives

are directors and shareholders

Trustee

Trustee Company

• Individuals elected by the claimant group (“elected representatives”) will be the directors and shareholders of the Trustee Company.

• These representatives will be responsible for the governance of the PSGE and the overall group.

• The PSGE trust deed may set out the procedure for electing representatives.

• The Trustee Company will not hold any assets.

• Having a Trustee Company will protect elected representatives against a degree of personal liability (because in most cases directors are not personally liable for the company’s losses).

• The directors must still act in the best interests of the company, which for a corporate trustee (in our opinion) includes the PSGE trust.

Iwi corporate structures and governance 19 OCTOBER 2012 / 24

2513095 © Chapman Tripp

4. Limited Partnerships

• An internationally recognised vehicle

• Since its introduction into New Zealand in 2008, the limited partnership structure has been readily adopted and utilised by the funds industry, with millions of dollars tied up in funds investments

• My colleague, Te Aopare Dewes, went through the key characteristics of a limited partnership, so I won’t go through them again – in short...

Iwi corporate structures and governance 19 OCTOBER 2012 / 25

2513095 © Chapman Tripp

4. Limited Partnerships

Key characteristics:

• General Partner: responsible for managing the day-to-day affairs of the limited partnership (we recommend using a company as the general partner to further limit liability)

• Limited Partners: contribute funds to the limited partnership, and receive “partnership shares” in return. Limited Partners are prohibited from taking part in the management of the limited partnership (we recommend that Limited Partners have the power to appoint directors to the board of the General Partner, effectively ensuring that the Limited Partners do have a say in the running of the limited partnership)

• Separate legal person, so able to contract in its own name and own property

• Governed by the Limited Partnerships Act 2008 and the limited partnership agreement, which is a private document

• Look-through for tax

Iwi corporate structures and governance 19 OCTOBER 2012 / 26

2513095 © Chapman Tripp

4. Limited Partnerships

Key Issue 5: The claimant group may lack the expertise to effectively govern and manage its

commercial asset holding company

Iwi corporate structures and governance 19 OCTOBER 2012 / 27

2513095 © Chapman Tripp

4. Limited Partnerships

Solution:

• Use subsidiary limited partnerships to carry out any commercial operations

• The trust deed of the PSGE should provide that all board members must possess the particular skills required to effectively operate a commercial business

Iwi corporate structures and governance 19 OCTOBER 2012 / 28

2513095 © Chapman Tripp

Final key issue

Key Issue 6: Sudden changes of control, policy and direction

Iwi corporate structures and governance 19 OCTOBER 2012 / 29

2513095 © Chapman Tripp

Final key issue

Solution:

• Stagger the elections of board members, to ensure continuity from one election to the next

Iwi corporate structures and governance 19 OCTOBER 2012 / 30

2513095 © Chapman Tripp

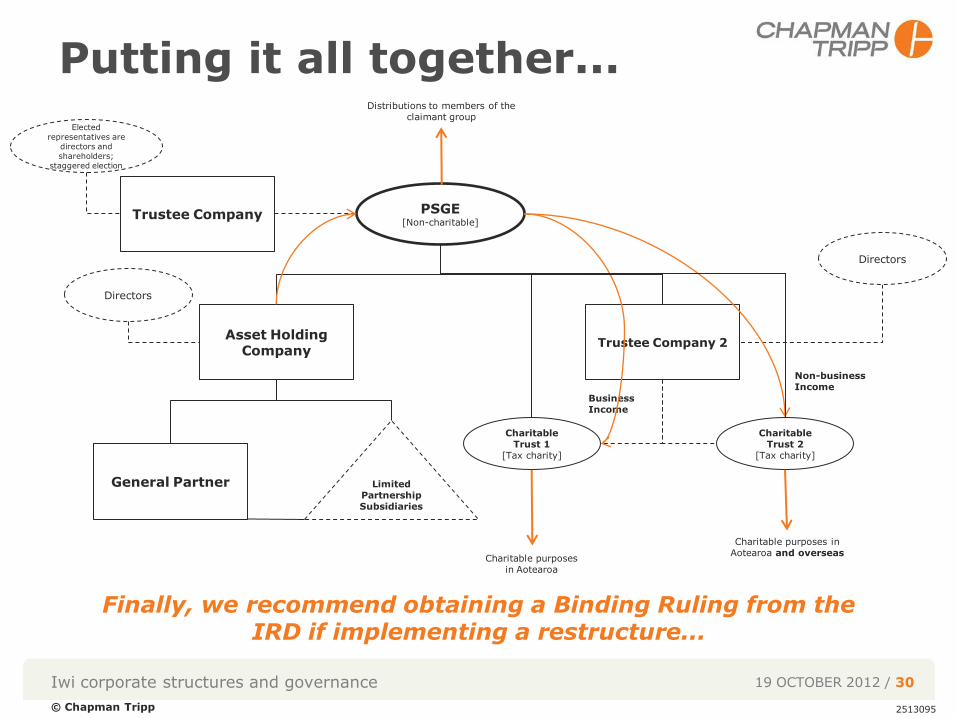

Putting it all together...

Elected representatives are

directors and shareholders;

staggered election

PSGE [Non-charitable]

Trustee Company

Charitable Trust 1

[Tax charity]

Charitable purposes in Aotearoa

Charitable purposes in Aotearoa and overseas

Charitable Trust 2

[Tax charity]

Business Income

Non-business Income

Asset Holding Company

Trustee Company 2

Distributions to members of the claimant group

Directors

Directors

Limited Partnership Subsidiaries

General Partner

Finally, we recommend obtaining a Binding Ruling from the IRD if implementing a restructure...

Iwi corporate structures and governance 19 OCTOBER 2012 / 31

2513095 © Chapman Tripp

Questions

Iwi corporate structures and governance 19 OCTOBER 2012 / 32

2513095 © Chapman Tripp

Contact