Ivan Rodionov Creation of the Venture Capital Industry in Russia Arlington November 24, 2008 Venture...

37

Ivan Rodionov Creation of the Venture Capital Industry in Russia Arlington November 24, 2008 Venture Innovation Fund

-

Upload

lesley-nash -

Category

Documents

-

view

222 -

download

0

Transcript of Ivan Rodionov Creation of the Venture Capital Industry in Russia Arlington November 24, 2008 Venture...

Ivan Rodionov

Creation of the Venture Capital Industry in Russia

ArlingtonNovember 24, 2008

Venture Innovation Fund

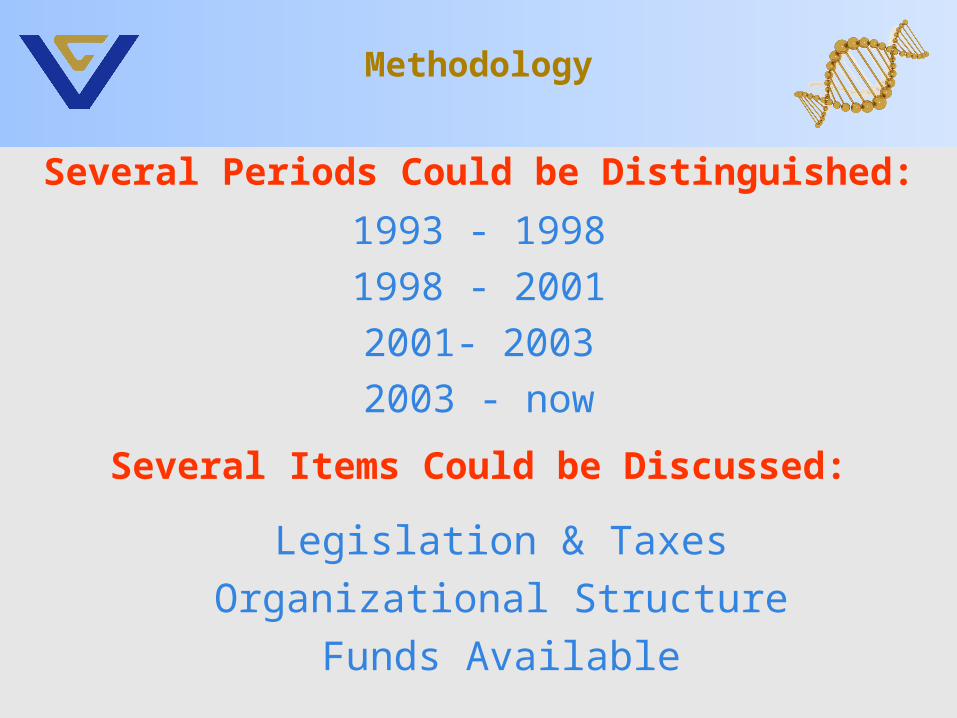

Methodology

Several Periods Could be Distinguished:

1993 - 1998

1998 - 2001

2001- 2003

2003 - now

Several Items Could be Discussed:

Legislation & Taxes

Organizational Structure

Funds Available

Legislation & Taxes

Fiscal Instruments:

• Corporations’ R&D funds as 1.5% of their turnover are profit tax-free, (1992)

• Expenses of Federal R&D foundations are profit and VAT tax-free (1994)

• Corporations’ R&D expenses are profit tax-free (2007)

• Patenting expenses are tax-free (2007)

Before the History

Government funds issuing grants to support R&D

Russian Fund for Basic Researches – RFFI(still operates now)

Russian Fund for Technology Development – RFTI

(still operates now)

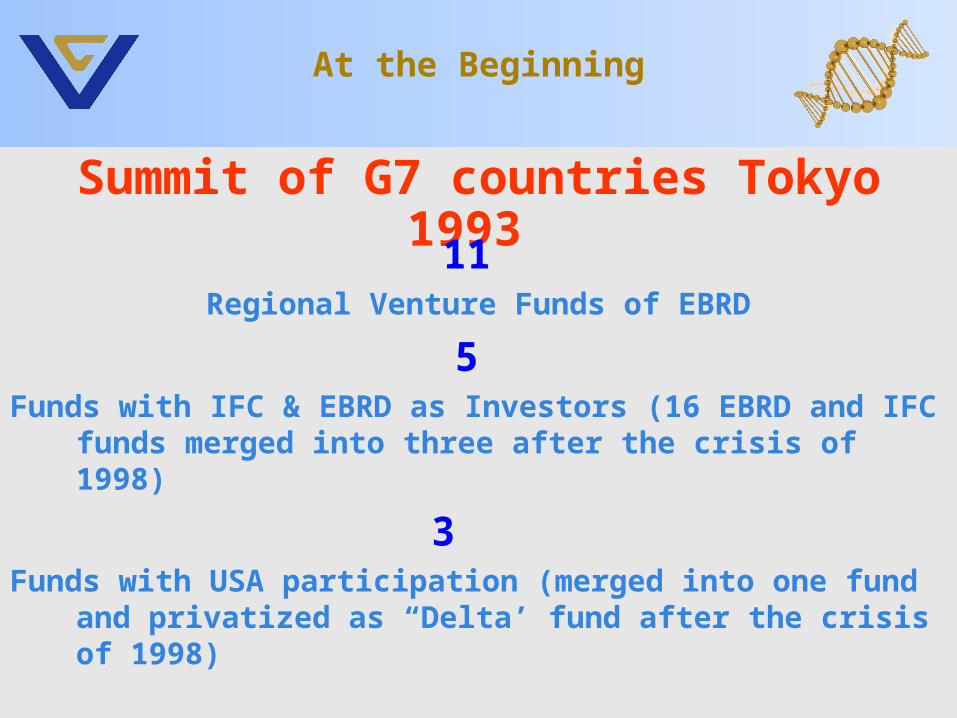

At the Beginning

Summit of G7 countries Tokyo 1993

11 Regional Venture Funds of EBRD

5 Funds with IFC & EBRD as Investors (16 EBRD and IFC funds

merged into three after the crisis of 1998)

3 Funds with USA participation (merged into one fund and

privatized as “Delta’ fund after the crisis of 1998)

• Market Economy Just Started

• Lack of Understanding of Russian realities by the Fund Managers (Russian Economy Crisis)

• Weakness of Fund Managers Community (funds in many regions and managers from different countries)

First Stage1993 - 1998

Main Problems

FASIE - Federal Foundation for Assistance to Small Innovative Enterprises (Bortnik fund) established in 1994 with $50 million

Establishing of FASIE

Main tools to assist:Spin off – START - 3 year project, 30.000 US$ for Phase I, 150.000 – for

Phase II, 50/50 co-financing

Licensing – TEMP - 3 year project, up to 500.000 US$, 30/70 co-financing

from Universities

Knowledge – PUSC - 1 - 2 year project, up to 500.000 US$, 30/70 co-financing

Transfer Partnership

Self - UMNIK (SMART) - nominee should be up to 28 years old, idea should be his

development (her) own, good science behind idea is important criteria, “entrepreneur nature” of nominee is important,

Commercialization is within 5 – 7 years, no need to organize enterprise for first two years

FASIE

• Applications - more than 15000 / Contracts - more than 4000

• Average turnover per SIE - US$ 500 thousands

• Average growth - 20% per year

• Number of commercialized patents - more than 1500

• Number of issued patents - more than 1000

• Companies with turnover

– more than US$ 1mln - about 100– more than US$ 5 mln - dozens– more than US$ 30 mln - 3

Some FASIE’s results (13 years):

Creation of RVCA1997

RVCA MISSION

Promotion of Establishing and Development of the Venture Industry in Russia

RVCA GOAL

Lobbying of the Interest of Venture Capital Community (including Private Equity Investments)

• Formation of Favorable Entrepreneurial Climate in the Country

• Information Support for the Venture Community (Industry Analysis)

• Creation of Communication point for the Companies and Investors

• Training of Qualified Specialists for Venture Capital Industry

RVCA Main Tasks

• Reduction of Competition from Western Piers

• Strengthening of Competitive Advantages of the Venture Capital because of the Crisis of Bank Systems and Lack of Long-Term Debt

• Loosening Bureaucratic Pressure Against Investors

• Growing Activity of Innovative Sector

Second Stage1998 - 2001

New Realities of Russia Economy

Government Fund of Funds Venture Capital Funds

Private and Institutional Investors…

…Investment Potential Growth

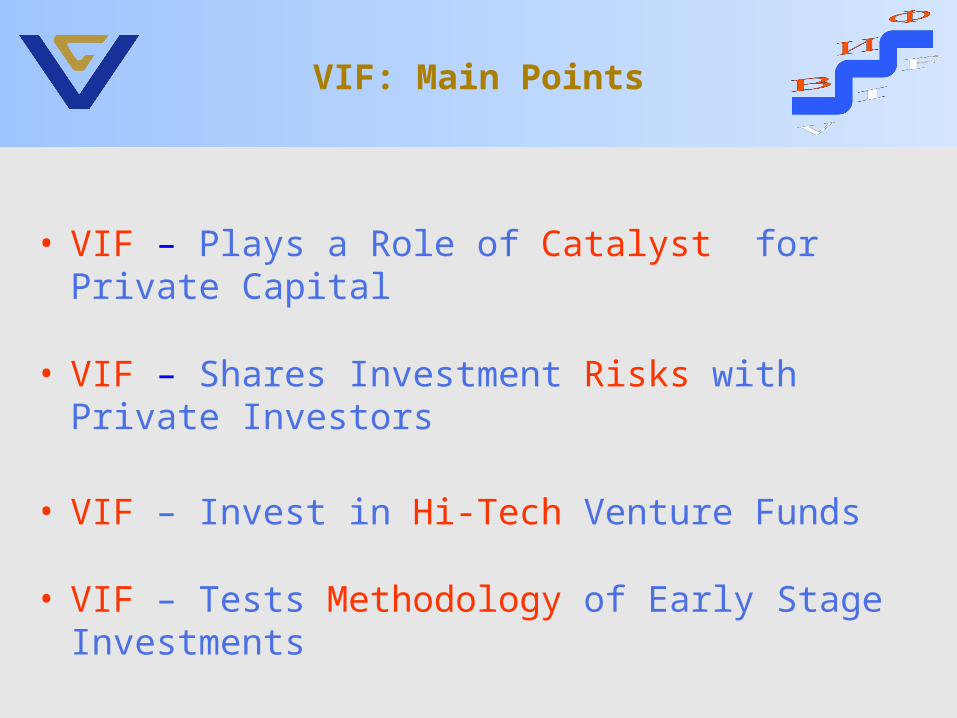

Creation of Venture Innovation Fund (VIF)

• VIF – Plays a Role of Catalyst for Private Capital

• VIF – Shares Investment Risks with Private Investors

• VIF – Invest in Hi-Tech Venture Funds

• VIF – Tests Methodology of Early Stage Investments

VIF: Main Points

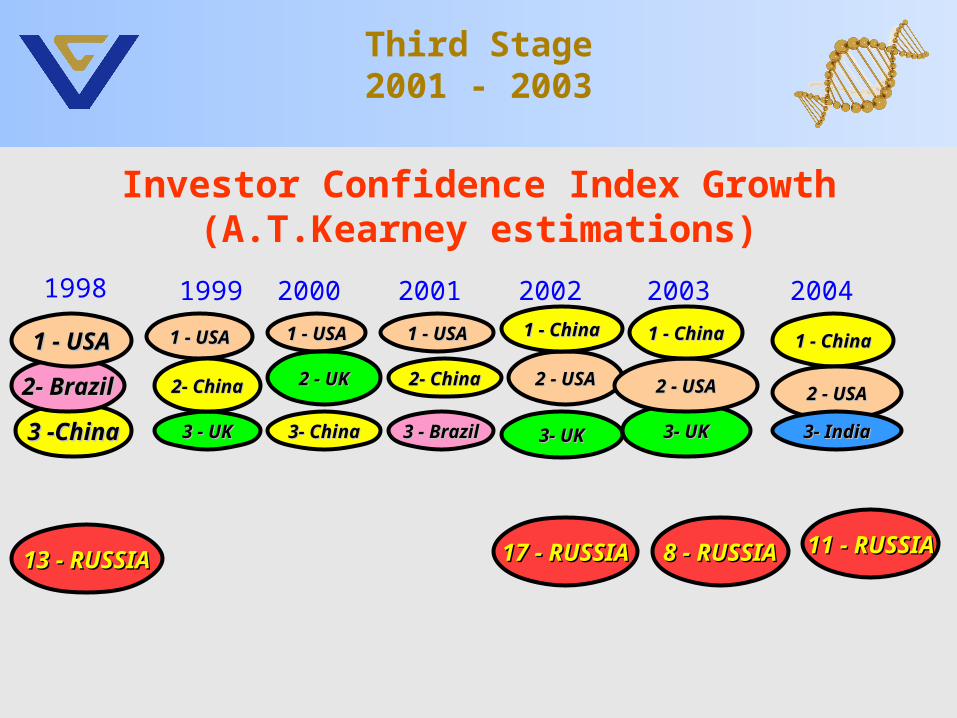

3 -3 -ChinaChina

2- 2- BrazilBrazil

Investor Confidence Index Growth(A.T.Kearney estimations)

Third Stage2001 - 2003

3- 3- UKUK

1998

1 - 1 - USAUSA

13 - 13 - RUSSIARUSSIA

1999

2000

2001 2002

1 - 1 - USAUSA

3 - 3 - UKUK

2- 2- ChinaChina 2 - 2 - USAUSA

17 - 17 - RUSSIARUSSIA

1 - 1 - ChinaChina1 - 1 - USAUSA

2 - 2 - UKUK

1 - 1 - USAUSA

3 - 3 - BrazilBrazil

2003

8 - 8 - RUSSIARUSSIA

3- 3- ChinaChina

2- 2- ChinaChina

3- 3- UKUK

2 - 2 - USAUSA

1 - 1 - ChinaChina

1111 - - RUSSIARUSSIA

2004

1 - 1 - ChinaChina

2 - 2 - USAUSA

3- 3- IndiaIndia

Entrepreneurship Support Infrastructure

State

Fun

ds

Technoparks

UBAR

RV

CRV

Fs

CТ

Т

ITC

Коaching Centers

Incubators

EVCA Course

Infr

astr

uctu

re

Educational

Financial

SME

VIF

RVCA

• Promotion of Creation and Development of SMEs in Hi-Tech with Venture Investments

• Attraction of Russian Money in Russia Venture Industry

• Promotion of Liquidity of Venture Investment Including Development of Securities Markets

• Creation of Institutes to Promote PE Investments in Innovation Companies

• Support of Better Understanding in Russian Society of SMEs Role in Economy Development

Entrepreneurship Support Goals

Targets of Venture Forum & Fair

Funds for the Innovation Companies and Early Stage

Investments in most Promising Technological Industries

Local Capital to Russian Hi-Tech

Foreign Capital to Russian Venture Industry

To Stimulate Inflow of:

Participants of Venture Forums & Fairs

250300

350

450530

630

720800

40 60100 120 130 150

190 210

28 46 54 51 73 75 105 120

0

100

200

300

400

500

600

700

800

900

1 VFF2000

2 VVF2001

3 VVF2002

4 VVF2003

5 VVF2004

6 VVF2005

7 VVF2006

8 VVF2007

Participants

incl. Investors

incl. SMEs

Companies by Industry at the Venture Fairs

Other10%

Biotechnology9%

Computer related

7%

Medical9%

Industrial equipment

29%

Communi-cations

9%

Consumer market related

5%

Chemical & materials

13%

Electronics related

9%

- Innovative Mega Projects started in 2003 with $130 mln continued

- National nanotechnology corporation charted (2007), $5 bln

- Support of infrastructure development – 35 ITC, 200 of TT offices

- $130 mln for business incubators and “compensations” schemes

- Special economic zones under creation from 20044 R&D zones – Moscow (Zelenograd), Dubna, St. Petersburg and Tomsk2 Industrial zones – Lipeck and Elabuga

- Reginal venture funds managed by professional private management teams under creation from 2005 (each has $10-30 mln composed of 25% federal budget + 25% local budget + 50% private funds)

THE GOVERNMENT’S POLICY

Russian Venture CompanyHow it operates

Russian Venture Company

Privately Managed Venture Funds

Venture fund

VC

FUND OFFUNDS LEVEL

VENTUREFUNDS LEVEL

START-UPLEVEL

Å

Nanotechnologies

Alternativeenergy

Medicaltechnologies

BiotechnologiesTelecommunications

Information technologies

Microelectronics

Venture fund

VC Venture fund

VC

Venture fund

VC Venture fund

VC Venture fund

VC

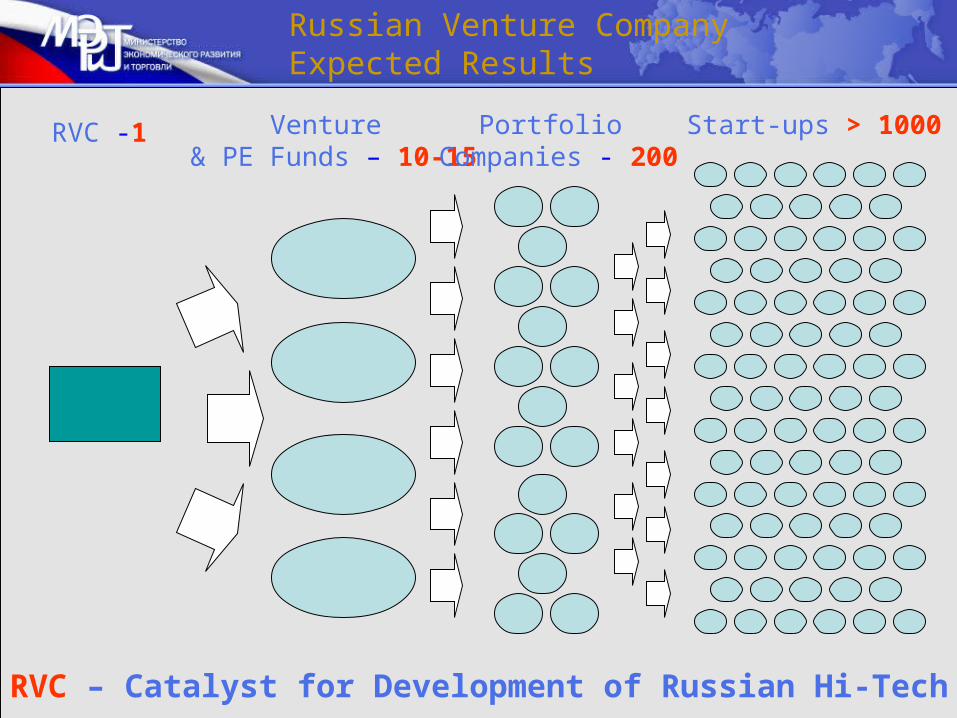

Russian Venture Company Expected Results

RVC – Catalyst for Development of Russian Hi-Tech

RVC -1 Venture & PE Funds – 10-15

Portfolio Companies - 200

Start-ups > 1000

Investment Attractiveness of Russia in 1998-2007

11ChinaChina

1313 RUSSIARUSSIA

22BrazilBrazil

A.T. Kearney Moody’s

CCC

Sovereign Rating of Russia

BBB+

Fitch

CCC

Credit Rating

of Russia

ВВВ+

Standart & Poor’s

CCC

Long-Term Credit Rating of Russia

ВВВ+

FDICI (1998-2005)

22IndiaIndia

3 3 USAUSA

44UKUK

55PolandPoland

66 RUSSIARUSSIA

11 USAUSA

33ChinaChina

SAMPLES TO FOLLOW

SITRA – Finland YOZMA – Israel

THE GOVERNMENT’S POLICY

• Political level (federal and regional) is in a strong favour of knowledge based economy

• Financial and economical policy claimed to be liberal – no any type of activity, including innovation, should have any preferences

• There are no financial incentives for large corporations to become competitive as a result of their innovation policy

• No special tax regime exists to stimulate export of innovative products

• No tax relief for either gain on venture investments or business-angels investments

THE GOVERNMENT’S POLICY - SWOT analysis

• Strengths:

- Almost all known instruments for early stage/expansion financing are now in use

- Some surveys show that about 2.5 mln. persons are acting as business angels (with small money)

- Commercial banks are quite aggressive to attract SME as clients

• Weaknesses:

- The scale of use of all instruments is still too small to influence national economy

- Universities are still considered mostly as places for education not for science and innovation

- Credit interest rates are still too high for innovative business

- Intangible assets are not used as a mortgage

THE GOVERNMENT’S POLICY UP-DATE

Government politics – accent displacement to Hi-Tech

Four «I» Dmitry Medvedev

InstitutesInfrastructureInnovationsInvestment

INFRASTRUCTURE DEVELOPMENT (Special Economic Zones)

Saint-Petersburg

Zelenograd

Dubna

ElabugaLipetck

Tomsk

Moskow

Number of PE & VC Funds in Russia 1994-2007

0

10

20

30

40

50

60

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Ne

w a

nd

liq

uid

ate

d

0

20

40

60

80

100

120

140

160

To

tal

op

era

tin

g

Capitalization of PE & VC Funds in Russia 1994-2007

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Ca

pit

ali

sa

tio

n o

f n

ew

an

d l

iqu

ida

ted

fu

nd

s

0

2000

4000

6000

8000

10000

12000

Ac

cu

mu

late

d C

ap

ita

lis

ati

on

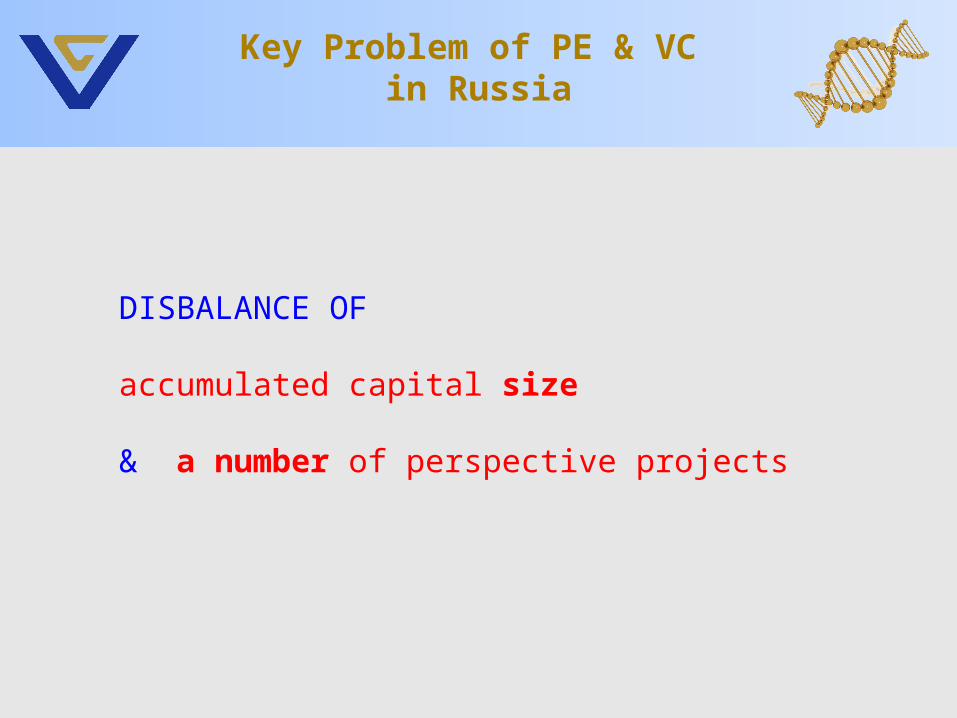

Key Problem of PE & VC in Russia

DISBALANCE OF accumulated capital size

& a number of perspective projects

Sources of Capital 2005 - 2007

Russian 25%

Foreign 75%

Russian 22%

Foreign 78%

Russian SourcesIn 2005 and 2007

Industrial enterprises0%

Banks0%

Government Agencies15%

Institutional Investors49%

Private Persons36%

CorporateInvestors 0%

Private Individuals 36%

Government Agencies 15%

Commercial Banks 0%

InstitutionalInvestors 34%

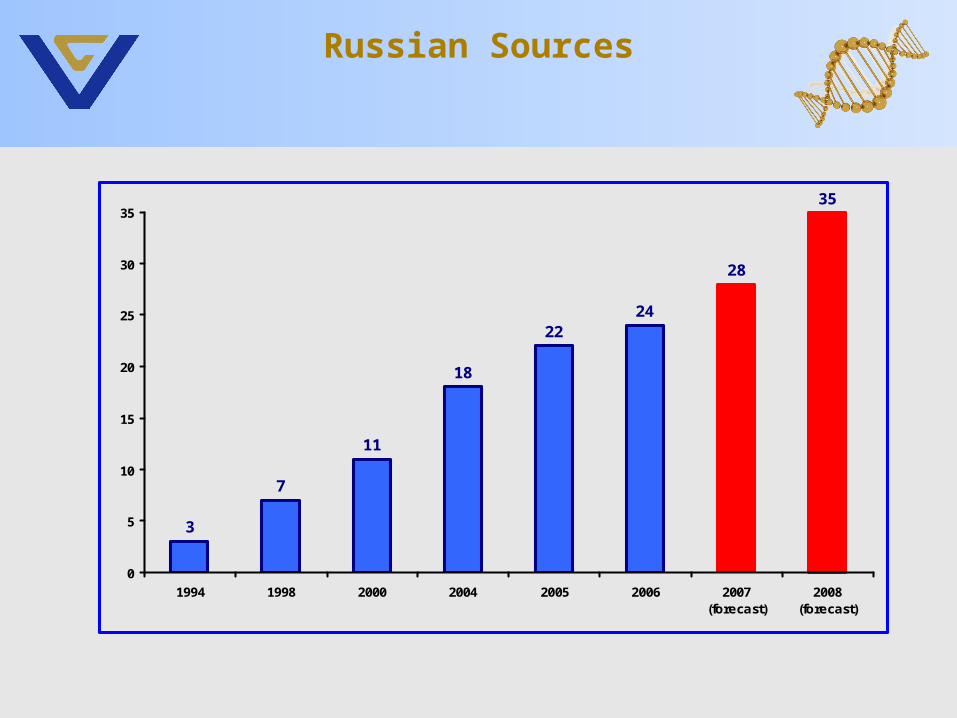

Russian Sources

3

7

11

18

2224

28

35

0

5

10

15

20

25

30

35

1994 1998 2000 2004 2005 2006 2007(forecast)

2008(forecast)

What Has Changed during last 12 years

• Industry has - «Grown-up»

• Fund Managers realized 1-2 full investments cycle

• Market Leaders and Outsiders Clearly Visible

• VC & PE Concept adopted and accepted by business and Government

• Project Quality - Improved

• First Success Stories in Business and Track Records of Management Teams

• Market Infrastructure Emplace:– Better Liquidity in Equity and Debt Markets– More Financial Consultants– Improved Legal Environment

What we Expect in next 5 years?

• Fund Grows at 20% per year to $15-17 bln in 2012

• VC segment aggressive Growth (50-100%) in next 3 years

• More Companies to Invest in

• Number of Management Teams will increase from 50 - in 2007 to 80-100 - in 2012

• Global Players are in coming

• Russian Fund are increase important

• Competition for Deals and People is Growing

• Deals are Large

• Increase Role of Add-Value Strategy

• Strengthening Role of Russian Government as Investor and Regulator

Increasing Role of Innovation Sector!

Venture Innovation Fund (VIF)

tel (812) 326-61-80

www.rvca.ru

Thank You for Attention!