Issues on Mvat Audit 81 Questions Nov 2013

65

C.A. DILIP PHADKE FCA 1 I S SUES O N VAT AUDI T PUNE BRANCH OFWIRC OF ICAI ON 10 th November 2013 C A DIL I P P H A DKE B.COM.,LL.B.,F.C.A. C HARTERED AC C O UN TAN T email: [email protected] T e l: 9 3 222 3 1414

-

Upload

pcbhandari -

Category

Documents

-

view

225 -

download

0

Transcript of Issues on Mvat Audit 81 Questions Nov 2013

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 1/65

C.A. DILIP PHADKE FCA 1

ISSUES ON VAT AUDIT

PUNE BRANCHOFWIRC OF ICAI

ON 10th November 2013

CA DILIP PHADKE

B.COM.,LL.B.,F.C.A.CHARTERED ACCOUNTANT

email: [email protected] Tel: 9322231414

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 2/65

C.A. DILIP PHADKE FCA 2

Q.1 One dealer had opted for composi tion scheme for retailer forfinancial year 2011-12. For f inancial year 2012-13, if he wants to

change to normal VAT system, whether he is supposed to declare

stock on 31-03-12 for claiming VAT input for 1-04-2012 onwards?

ISSUES UNDER MVAT AUDIT

Ans. There is no need to declare stock as on 31-03-2012 for a dealeropt ing out of composition for the year 2011-12. On the purchase

held in stock as on 31-03-2012 he is not eligible to input tax

credit . For purchases after 1-4-2012 only, he wil l get the input

tax credit. As it is presumed that on total purchases of 11-12

setoff already claimed during the year 11-12 only.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 3/65

C.A. DILIP PHADKE FCA 3

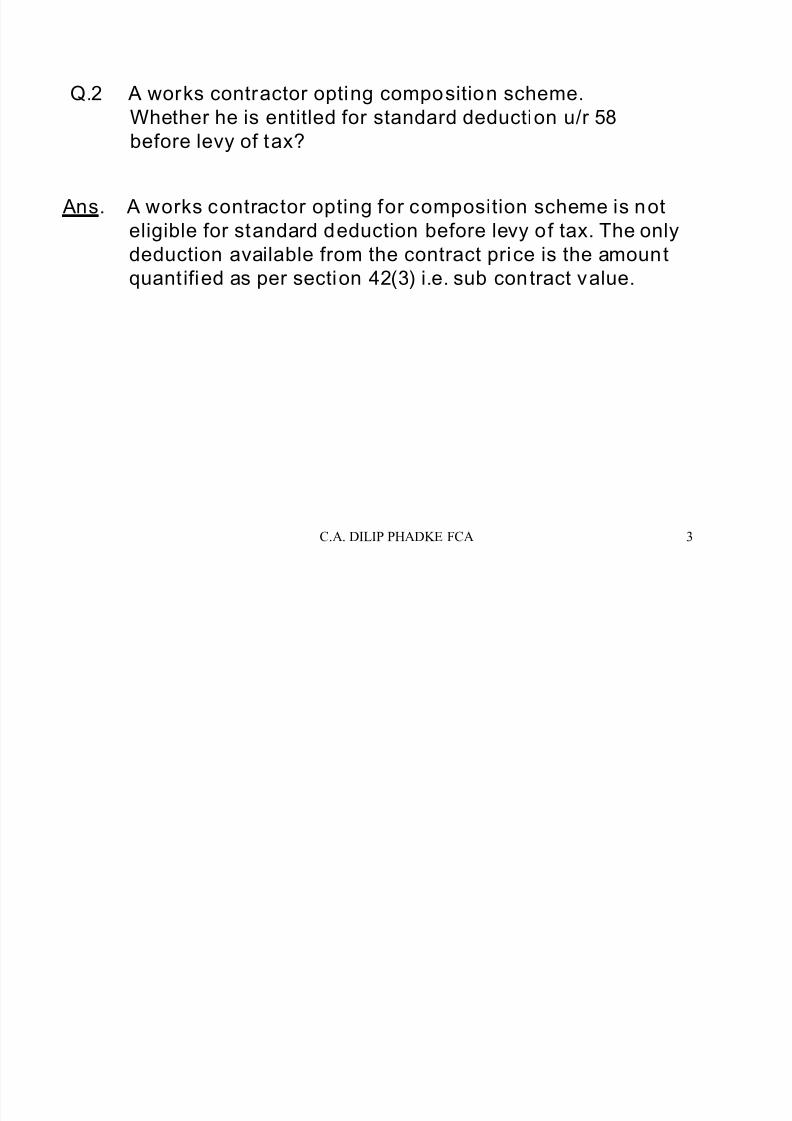

Q.2 A works contractor opting composition scheme.

Whether he is entitled for standard deduction u/r 58

before levy of tax?

Ans. A works contractor opting for composition scheme is not

eligible for standard deduction before levy of tax. The only

deduction available from the contract price is the amount

quantified as per section 42(3) i.e. sub contract value.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 4/65

C.A. DILIP PHADKE FCA 4

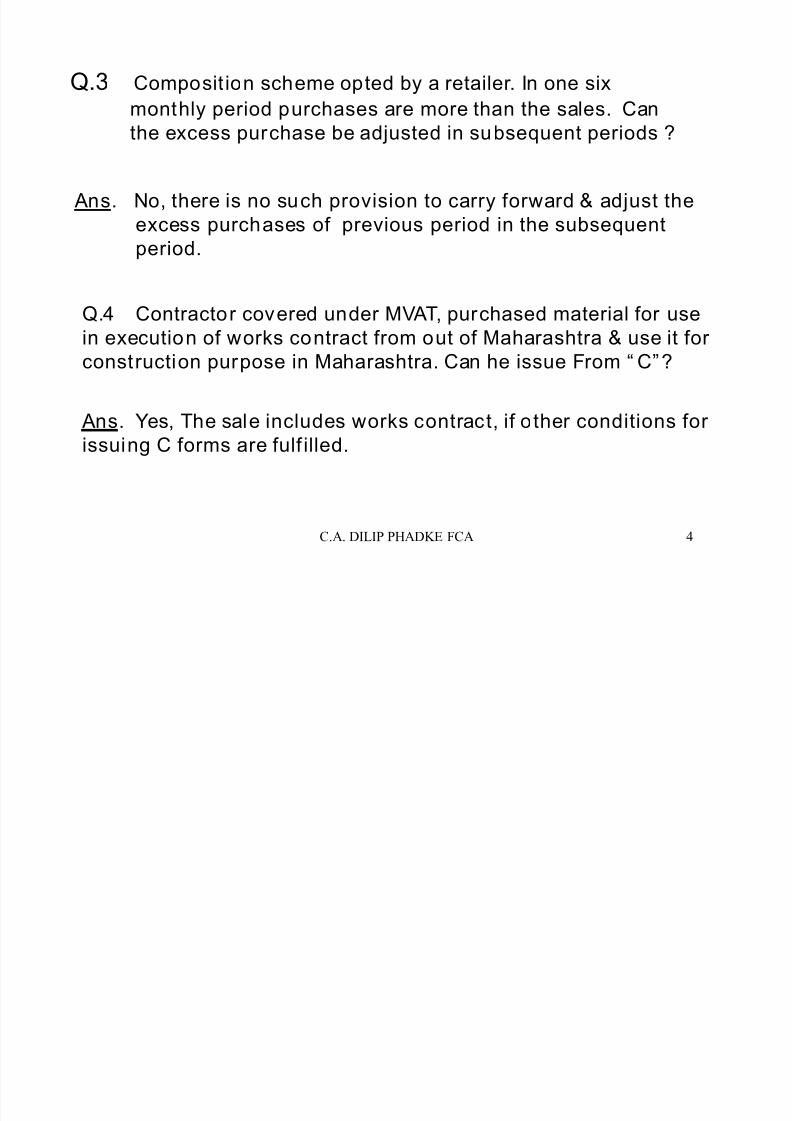

Q.3 Composit ion scheme opted by a retailer. In one six

monthly period purchases are more than the sales. Can

the excess purchase be adjusted in subsequent periods ?

Ans. No, there is no such provision to carry forward & adjust the

excess purchases of previous period in the subsequent

period.

Q.4 Contractor covered under MVAT, purchased material for use

in execution of works contract from out of Maharashtra & use it for

construction purpose in Maharashtra. Can he issue From “ C”?

Ans. Yes, The sale includes works contract, if other conditions forissuing C forms are fulf illed.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 5/65

C.A. DILIP PHADKE FCA 5

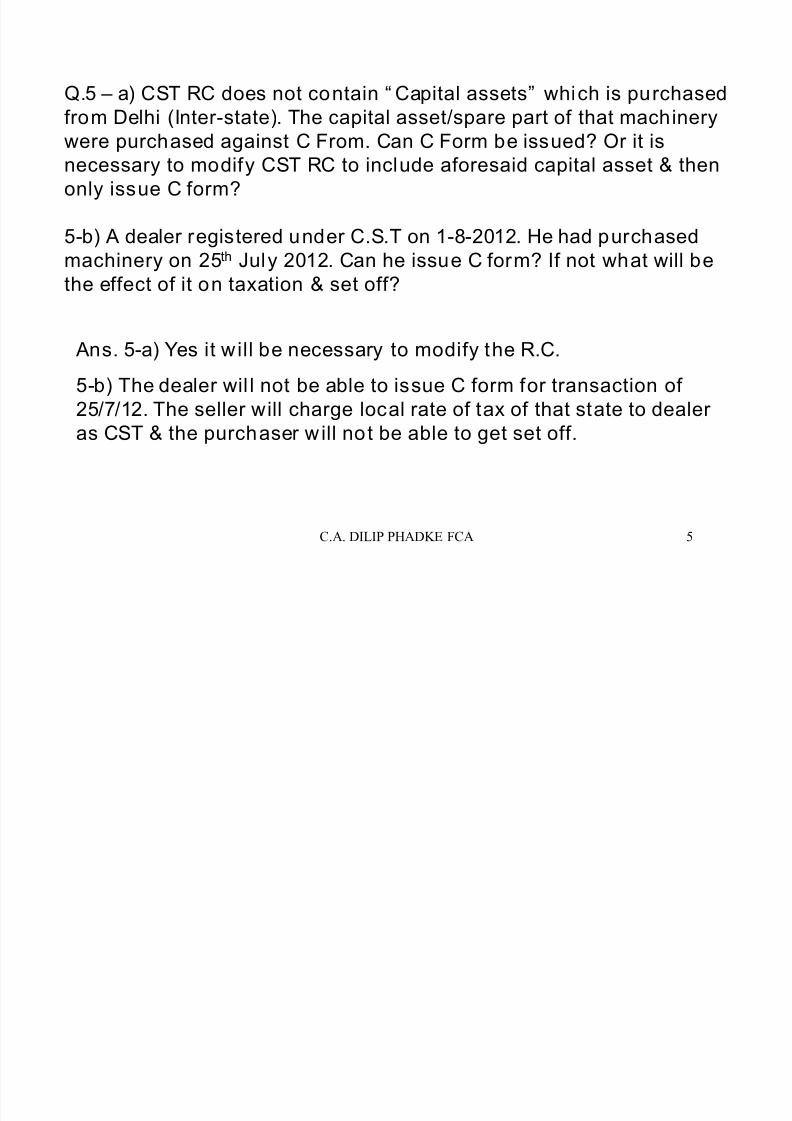

Q.5 – a) CST RC does not contain “ Capital assets” which is purchased

from Delhi (Inter-state). The capital asset/spare part of that machinery

were purchased against C From. Can C Form be issued? Or it isnecessary to modify CST RC to include aforesaid capital asset & then

only issue C form?

5-b) A dealer registered under C.S.T on 1-8-2012. He had purchased

machinery on 25th July 2012. Can he issue C form? If not what will be

the effect of it on taxation & set off?

Ans. 5-a) Yes it will be necessary to modify the R.C.

5-b) The dealer wil l not be able to issue C form for transaction of

25/7/12. The seller will charge local rate of tax of that state to dealeras CST & the purchaser will not be able to get set off.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 6/65

C.A. DILIP PHADKE FCA 6

Q.6 A specific order was placed with the branch. Accordingly, the

goods were transferred from Head Office situated in other

State. Whether claim of branch transfer be allowed or not . If

not, Whether the issuance of “ C” Form by the branch instead

of Form “ F” will be sufficient for such a ‘sales’?

Ans No, the good transferred against specific order placed with

the branch will be treated as inter-state sales in the hand of

H.O. . In such case ‘F’ Form issued by branch will not be of

any use. In order to avail benefit of concessional rate of tax ;

i.e., @ 2%, ‘C’ Form from the purchaser (not from branch) will

be necessary.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 7/65

C.A. DILIP PHADKE FCA 7

Q.7 A dealer in Mumbai SEEPZ sends the goods to duty free shop

at Airport at Mumbai, Chennai & Delhi. After a month, the shop

send the unsold goods back to the dealer & the dealer raisesthe invoice on shop for the goods sold from shops. However,

no VAT is charged. The duty free shop maintain the details

regarding passengers & their flight numbers to whom the

goods are sold. Whether VAT/CST is to be charged for the

sales to such shop? If yes, whether shop can issue “ H” Form

as sale is made only when a passenger buys it f rom duty freeshop & treated as export by the shop?

Ans. 1) The duty f ree shop are not consignment agent of

the unit. Therefore, sale by a dealers in Mumbai SEEPZ to

duty free shop at Mumbai will be local sale & wil l be coveredby MVAT Act,2002. Attention is invited to Notif ication No.

VAT/1505/CR-126/TAXATION-1 dt. 1-4-2005. The liability of

VAT to be determined in accordance with th is notification

otherwise VAT is payable.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 8/65

C.A. DILIP PHADKE FCA 8

3) Duty free shops cannot issue Form ‘H’ to the dealer in SEEPZ

as there was no advance order with such shops. Thus

purchases by duty free shop will not be covered by Section

5(3) of the CST Act, 1956.

2) Sale by a dealer in Mumbai SEEPZ to duty free shop Kolkata

& Chennai will be inter-state sale & wi ll be governed by CST

Act,1956.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 9/65

C.A. DILIP PHADKE FCA 9

Q.8 Dealer has opted for Composit ion scheme in the year 2009-10.

On 01-12-2009 he has contravened one of the conditions of

Composition scheme. Whether benefit of Composition schemebe withdrawn and from what Date?

Ans. According to me , for the first six months he will be eligible

for Composition scheme and from 1/10/2009, it w ill be withdrawnand liable to discharge the liabili ty under normal provisions of

VAT.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 10/65

C.A. DILIP PHADKE FCA 10

Q.9 When OMS sales goods are returned, it has to be claimed in the

same year of sale. Whereas under VAT regime the dealer can claim the

goods returned in the months when he passes the entry in the booksof account on the base of Dr. /Cr. Note received. What will be the stand

taken by the auditor while f inalizing the audit report.?

Ans. As per BASF case the goods return are to reverted back

to the month in which they were sold. As per circular 26 T of

2006 pt. 20 of Commissioner the same has to treated as per the

provisions of M.V.A.T. act. Sec. 63. (goods returned wi thin six

months in the period in which dr. or cr. Note is entered in

books.)

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 11/65

C.A. DILIP PHADKE FCA 11

Q.10 Can Refund at the end of the year be adjusted in the

subsequent year?

Ans. Yes the definition tax is changed & it includes wct

composition.

Q.11 Whether the composition sum paid under works contracts is

eligible for set off?

Ans : Yes if refund is below five lacks

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 12/65

C.A. DILIP PHADKE FCA 12

Q.12 Gold/Bul lion purchase-VAT paid @ 1%.Part of the Jewellery

made is transferred against “ F” Form. How much retentionis to be done out of 1% VAT (Input Credit ) for such

transfers?

Ans. As per Rule 53 of MVAT Act, When goods are being transferred

to the branch retention would be 4%, but however the rate of tax of

items which is being transferred is less than 4% it will such ratewhich is less. In the given case tax rate is 1% then the retention

would be 1% only.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 13/65

C.A. DILIP PHADKE FCA 13

Q.13 Set-off is already claimed on purchase of raw mater ial in the

return for the month of December 2009. Subsequently, thematerial is destroyed. Thereafter, in the month of February 2010,

insurance claim is admit ted. Whether the amount of insurance

claim received is taxable? Whether the set-off al ready claimed

needs to be reversed and paid to the Government?

Ans. The set off is available on date of purchase. The goods are

not sold if they destroyed and claim is received therefore there wil l

not be any tax payable. There is no provis ion for reversal of set off

u/r 53 or 54 if goods are destroyed and business is continued.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 14/65

C.A. DILIP PHADKE FCA 14

Q.14 In on going contract, where dealer’s liabili ty under

the old Works Contract Tax Act is nil, If in the current

year liabili ty under MVAT is also nil in such case, can a

dealer claim set-off on purchases made during current

year?

Ans. Yes the set off w ill be available on purchases not used in on

going contract.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 15/65

C.A. DILIP PHADKE FCA 15

Q.15 No set-off is available on Stock of discontinued business.

What wil l happen if dealer change commodity of business by

discontinuing old commodity business under same name &

constitution?

Ans. The set-off w ill be available on stock of commodity

because business is continued under same name & Vat no.Further if stock wil l be sold it w ill be liable for VAT. If business

is totally discontinued then on stock (on the date of closure of

business) set-off is to be reversed as per provisions of rule

53(5).

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 16/65

C.A. DILIP PHADKE FCA 16

Q.16 A company having business of development of Computer

Software. Whether set-off on computer is available or not ?

Ans.. Set-off on computer can be claimed if i t is capitalized as

Office Equipment subject to reduction of 3% u/r 53(7A). However, in

computer software development business, computers are plant &

machinery for production/ development of software . Therefore ,the

set-off can be claimed.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 17/65

C.A. DILIP PHADKE FCA 17

Q.17 A dealer took registration late after he crossed the required

turnover. What will be the set-of position for the period when he

actual ly crossed the required turnover and the date he got registrat ion(URD Period)? What is the remedy to the dealer? What are the chances

that he will get administrat ive relief?

Ans. If the dealer has got the registration in the sameaccounting year and the goods are unsold at time of

registration he will get the set of f of goods/capital asset. If

dealer has already sold the goods he will have to apply for

administrative relief for charging tax on sale and set off on the

goods sold.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 18/65

C.A. DILIP PHADKE FCA 18

Q.18 The dealer sells an item “ X” . Subsequent to the sale , the

goods are not found as per specification .The dealer has agreed to

take back goods partially after six months & offer some discount onthe goods retained by the customer .For goods returned & reduction

in price credit note is issued showing value of goods returned &

additional discount of fered .Can dealer claim the discount of fered

by reducing i t from the sales turnover in the period in which the

discount is offered?

Ans. Since part of goods are rejected & received back by the

dealer, there is no sale by dealer qua that quantity ,thus provisions

for claiming goods returned are not applicable and rule 63(4) wil l

not be appl icable & dealer wil l not be liable to pay VAT on that part

of goods received back. For rebate/discount of fered on quantityretained, this is a case of re- determination of sales value .Therefore,

the amount would be deductible in the month in which such credit

note is issued as per provisions of rule 63(6).

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 19/65

C.A. DILIP PHADKE FCA 19

Q.19 In case of Works Contract if Contractor haspurchased machinery in the year 2009-10 and used for On

Going Contract as well new Contracts undertaken during

the year 2009-10,Whether Set off on VAT paid on such

Machinery be denied since it is used for On Going

contract?

Ans. Set off will be available irrespect ive of where the machinery

is used. In case of material s/o is available on material used in

contracts other than on going contracts.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 20/65

C.A. DILIP PHADKE FCA 20

Q.20 What are the provisions o MVAT Act vis-à-vis Freight Charges

charged to customers either by way of Separate Debit Note or shown

separately in Bi ll. Whether it forms part of Sales Price for VAT?

Ans. Yes, it is part of Sale Price. u/s 2(25) sales price include amount

charged for anything done before delivery of the material is

complete. Since in most of such cases freight is charged before

delivery. However, if delivery of goods is already given then it may

not be includable in sale price.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 21/65

C.A. DILIP PHADKE FCA 21

Q.21 How to give effect for Debit Note/Credit Note for tax

dif ference i.e. where the dealer has charged 12.5% instead of 4% &

subsequently given CN for 8.5%? What if CN was given in

subsequent f inancial year?

Ans. Sect ion 63(6) provides that i f credit notes (CN) & debit notes

(DN) are issued for variation in sales price or purchase price that the

effect for such variation & tax thereon should be given in the return

in the period in which the appropriate entries for debit notes & creditnotes are taken in books of accounts. In the present case sales

price or purchase price is not varied but amount of tax is varied

therefore effect of such DN & CN should be given by revising the

returns for the period in which sales was made for which such DN &

CN are issued .If such DN & CN are issued in subsequent f inancial

year then also effect need to be given in the month in which sale

was made .The VAT Auditor may make appropriate observations at

para 5 in form 704 Part 1.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 22/65

C.A. DILIP PHADKE FCA 22

Q.22 Under old Works Contract Tax Act prov isions there was a

deduction/exemption provided for in respect of state Government

Contracts. What are the provision in respect of such stateGovernment Contracts under MVAT Act, 2002 of new contracts &

existing old contracts?

Ans. For on going contract deduction is continued.

For new contract there is no such deduction.

Q23 What are the contractee obl igations to deduct TDS on contract?

Ans. : The contractee shall a) If the contract value exceeds f ive

lacks deduct tax @ 2% from amount payable to reg. contractors &

5% from unreg. Contractors. No T.D.S to be made on payment to

sub contractors. b) pay tds. amount online before 21st of nextmonth in treasury by chalan MTR-6 c) Issue certi ficate in form No.

402 to the contractor for T.D.S. d) keep record of tds & cert. in

form No. 404 e) file return of tds. in form No. 424

ELECTRONICALLY within three months from end of the year.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 23/65

C.A. DILIP PHADKE FCA 23

Ans. The liability for TDS is to be determined on the basis of

amount payable in the year .If amount payable to the contractorfor all contracts in a year is Rs.5 Lacs or more then only

provisions of WCT TDS are appl icable .Since in the given case

the amount paid and payable to the contractor exceeds Rs. 5

Lacs, TDS provision will be attracted.

Q.24 If Private Ltd Co. Registered dealer in Mumbai having addit ional

place of business in Nashik g ives a construction contract to the

contractor for consideration of more than 5 lakhs. The contract isawarded in 2010-11. The work is completed in two years 2011-12 & 2012-

13. In each year amount payable is less than five lacks. Whether T.D.S.

on W.C. IS APPLICABLE?

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 24/65

C.A. DILIP PHADKE FCA 24

Q.25 A dealer is a Hotelier. He is holding l iquor license &

also entitlement certificate for food manufactured. Liquor

sales Rs.10 Lacs. Food sales Rs.20 Lacs. Is he liable toaudit?

Ans. If for one business provisions of Sec 61 are

attracted then audit is required for all businesses of the

dealer. Hence dealer is liable for VAT audit of food salesalso.

Q.26 Can VAT auditor revise audit report?

Ans. There is no such provision but in following cases it

might be necessary to revise the audit report :

1) Revision of final a/c after submission of vat auditreport.

2) Change of law with retrospective effect.

3) Change in interpretation because of notification or

judicial pronouncement

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 25/65

C.A. DILIP PHADKE FCA 25

Q.27 Jewelers registered under M.V.A.T. He has export

turnover in crores. His total purchases mainly in cash in

small amounts but may be more than Rs. 10,000/- vendorsidentity not known. How to report?

Ans. As there is no set off avai lable it is not necessary to

report in para 3, In Annex J - Sec.2. It will be shown as

purchase from non tin holders.

Q.28 Total turnover of sales Rs. 50 lacks and purchases 48

lacks in a year. Survey under I.T. act conducted. Excess

stock of 15 lacks admitted by dealer. Whether liable for

M.V.A.T. audit? Ans. Yes

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 26/65

C.A. DILIP PHADKE FCA 26

Q.29 How to find out reduction of set off under rule 53 –

2) Tax free goods. 3) Branch trf.

Ans. You have to refer to rule 53 sub rule 9 (a) fordefinition of corresponding goods used in tax free

goods and branch transfer

Q. 30 work is to be done in SEZ in Gujarat by work

contractor in Mumbai. He appoints subcontractor fromSurat. What wil l be the tax to be charged and forms to

be exchanged?

Ans. If the Surat contractor is labour contractor and

material is sent from Maharashtra ‘I’ form can be given

and there will not be any tax. If Surat contractor

purchases material from Gujrat and uses it in contract

there will be no interstate movement and ‘I’ from cannot

be issued.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 27/65

C.A. DILIP PHADKE FCA 27

Q.31 Failure to get audit done u/s 61 of MVAT - sales 250

crores Purchases 300 crores. What is quantum of

penalty?

Ans. As per the new amendment ,where a dealer has not furnished

a copy of audit report or knowingly furnish incomplete report w ithin

a specified time , then after hearing the dealer the Commissioner

may impose on him , in addition to any tax payable , a sum by way of

penalty equals to 1/10 % of total sales . The penalty is levied at 10paise per 100 rupees of sales . The maximum limit of 1 lack is

removed. On turnover of 250 crores sales where the report is not

filed in time the penalty works out to Rs. 25 lacks. The levy of penalty

is never mandatory . Refer to Supreme Court in case of Hindustan

Steels Ltd .25 STC 211 (SC) & Supertron Ltd. (B.H.C.) decided on 13-

12-2012.

The grace period of one month provided in prov ision to sub-section

(2) continues.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 28/65

C.A. DILIP PHADKE FCA 28

Ans.. For 6(2) transaction form is C & EI. As there is preexisting order it can not be done. The I form can not be

issued as the order is placed on dealer of Maharashtra

from SEZ of same state.

Q.32 Supply is to be made by Mumbai Dealer to SEZ in

Maharashtra. The dealer sends the material to his consignee

at Indore to supply the material. Can this be treated as 6(2)

TRANSACTIONS under C.S.T? Can consignee supply the

material against I form?

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 29/65

C.A. DILIP PHADKE FCA 29

Q. 33. How the entry is made in Annexure A & B when payment

for whole yr or period more than applicable return period is

made in single challan?

Q. 34. Is interest on late payment is calculated automatically in

Annexure A & B?

Ans: Tax paid with challan is to be co related with return

period. Split the challan amount to different return

periods in applicable cases. The notice in form No. 213

will be received for mismatch of amt. as per return &

Chalan.

Ans: Yes, it calculated automatically after pressing“ Validate” button of these annexure. Int. is automatically

calculated for revised returns also & if amt. payable in revised

return is reduced still interest will be calculated on amt. paid.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 30/65

C.A. DILIP PHADKE FCA 30

Q. 35. Where to show sales on which no tax is collected

separately & sale to non tin holders in Annexure J-1?

Q. 36. What is the treatment to the dealer having multi-stateactivities?

Ans: It should be entered in Row 5002 in Annexure

J_Sec 1 where space is provided for sales where tax is

not col lected separately.

Ans: If the dealer has multi state activi ties then Trial

Balance in relation to the business Activities in

Maharashtra is not required to be attached.

as per instruction no.27 dealer is required to submit

i) A statement of submission of audit report duly signed by

the Dealer. ii) A duly signed copy of Acknowledgement

generated after uploading of audit report in form 704.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 31/65

C.A. DILIP PHADKE FCA 31

Q. 37. Is it necessary to fill entire row in applicable Schedules

and Annexure?

Q. 38. What is last date of tax payment required to befilled in column d of Annexure A & B especially when due

date is public holiday?

Ans: Due date of tax payment is 21/30 days from the end

of the return period (excepting the due dates those fall onholidays). As provision of electronic payment is there now

you can make payment on holidays also.

Ans: In all the Schedules and Annexure it is mandatoryto fi ll applicable rows completely i. e. if one cell in a row

is fil led then it is mandatory to fil l all the cells in that row

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 32/65

C.A. DILIP PHADKE FCA 32

Ans: Negative certification by the Auditor, if any is

to be incorporated with reasons, at Sr. No. a to p, in

Para 3 of Part 1 and should correspond to the

relevant certificates which are mentioned at 2(B)(a)to 2(B)(p) of Part 1. Further only 500 characters

can be written in one row. Further, the auditor’s

remarks are to be included at Para 5 of Part 1 and

qualification having the impact on the tax liability,wherever applicable, shall be stated in brief.

Q. 39. What is to be written in Sr. No. a to p, in Para

3 of Part I?

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 33/65

C.A. DILIP PHADKE FCA 33

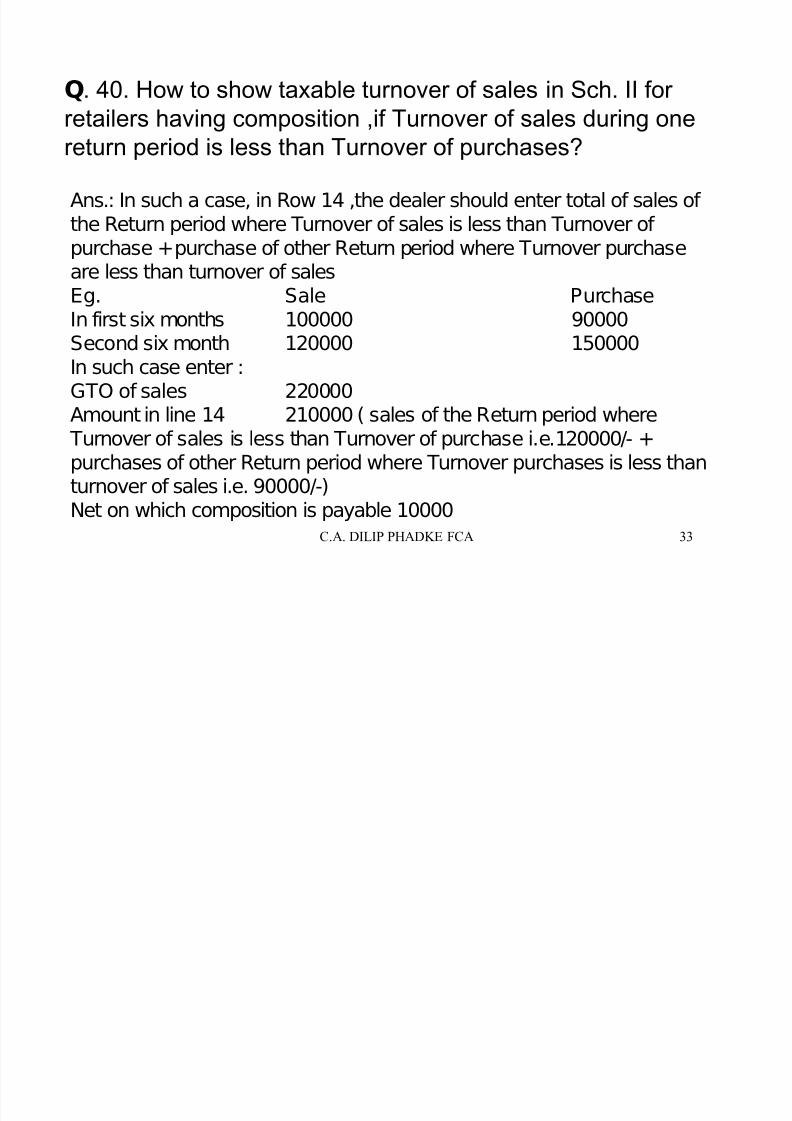

Q. 40. How to show taxable turnover of sales in Sch. II for

retailers having composition ,if Turnover of sales during one

return period is less than Turnover of purchases?

Ans.: In such a case, in Row 14 ,the dealer should enter total of sales ofthe Return period where Turnover of sales is less than Turnover ofpurchase + purchase of other Return period where Turnover purchase

are less than turnover of salesEg. Sale PurchaseIn first six months 100000 90000Second six month 120000 150000In such case enter :GTO of sales 220000

Amount in line 14 210000 ( sales of the Return period where Turnover of sales is less than Turnover of purchase i.e.120000/- +purchases of other Return period where Turnover purchases is less thanturnover of sales i.e. 90000/-)Net on which composition is payable 10000

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 34/65

C.A. DILIP PHADKE FCA 34

Q. 41. In transaction u/s 6(2) under the CST Act , declaration in

Form-C is received but Form-E1/ E2 for the same transaction not

received. In Annexure I, which details are to be written ?

Ans: In this situation, select Form-E1/E2 in column 4, write

details pertaining to purchases in columns 1 to 3, write details

of sales in the column no. 5, 6, 7 & 8 and write rate of tax as

applicable in column 9.

Q. 42. In transaction u/s 6(2) under the CST Act, declaration in

Form-E1/E2 received but declaration in Form-C for the same

transaction not received. In Annexure I, which details are to be

written?

Ans: In this situation, write details of sales in the entire row after

selecting Form C in column 4 and write rate of tax as applicable

in column 9.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 35/65

C.A. DILIP PHADKE FCA 35

Q. 43. In transaction u/s 6(2) under the CST Act, I have not

received declaration in Form – C & E1/E2 of the transaction. In

Annexure I, which details are to be written?

Ans. Enter transaction related to Form E1/E2 in one row and

corresponding transaction related to Form ‘C’ in the next row

below. Select Form-C in column 4, enter details of sales in the

entire row and in column 9, write rate of tax as applicable. In the

next row, enter details of form E1/E2. Select Form-E1/E2 incolumn 4, write details pertaining to purchases in column 1 to 3,

write details of sales in column 5 & 6, and put zero in column 7 to

9.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 36/65

C.A. DILIP PHADKE FCA 36

Q44 Sales promotional items are purchased on C form Whether

there is any contravention?

Ans.: If the goods purchased are used as per Sec. 8(3)of C.S.T.

then there is no contravention. If these items are given free it

needs to be established that the price of these items given free

was included in the sale price of goods sold. Further if any sale

price is realized from these items the tax at rate applicable tothese items will be payable.

Q 45 : How to treat the O.M.S. purchase/ sales & returns while

issuing C forms and shown in audit report?

Ans.: The C form should be issued for net amount. In sec. G of

form 704 it is clearly stated that the amt. should be net of returns

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 37/65

C.A. DILIP PHADKE FCA 37

Q46: Diamond Dealer HO in MH, Factory in Guj, rough

diamond purc and polished in Guj and sent to HO with proper

delivery notes, what should be the treatment?

Ans.: 1. HO should issue Form F to Guj Branch.

2. Include the value of such diamonds in GTO of purchases

3. Show the amount at deduction under clause 3(h) ofSchedule 1 and in Annexure J-Sec 6.

4. Show it reconciliation of purchases in Annexure K.

5. The value of the goods will be sale value at branch

reducing the local taxes, transportation & c & f charges.

6. The auditor should disclose the method adopted and

qualify if not consistent.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 38/65

C.A. DILIP PHADKE FCA 38

Q47 : Mumbai H.O. purchases diamonds and send it to Gujrat Br.

For processing and receives them back within 60 days and sales

the same. What should be the procedure followed? Ans.: The H.O. as well as Gujrat branch will have to issue F form

(Ref. Trade cir. No. 2 T dt. 11-1-2010). If the diamonds sent are

purchased locally the reduction of set off will not be applicable as

they are received back in 60days as per proviso. to rule 53 (3)

Q48: Dealer in Nerul dispatches goods to Delhi as per the

specifications of Nagpur Dealer. Can this transaction be 6(2)

transaction in the hands of Nagpur dealer?

Ans: After the judgment of SC in A & G Project in 2009 such

transaction can not be treated as Sales in Transit Tr. Falling u/s6(2) of CST Act.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 39/65

C.A. DILIP PHADKE FCA 39

Q49 : What are provisions for filing of Revised Returns?

Ans:

1. Dealer can file revised returns upto 9 months from the end ofrelevant F.Y.

2. The dealer can file revised return within 30 days from the end of

due date of filing of Audit Report if any discrepancies found by the

Auditor.

Q.50 Computer purchased for Jewellery designing. Can set off be

claim?

Ans: It is necessary that it should not be treated as office eq. in

books of accounts but should be treated as machinery then it canbe claimed.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 40/65

C.A. DILIP PHADKE FCA 40

Q 51 : An item of 12.5% is purchased from trader. The bill shows

Rs. 1,00,000/- Net plus Tax of Rs. 3,750/-. How to show Set off in

Sch I of Audit Report?

Ans: In clause 4 where the rate wise tax break up to be given

show Rs. 30,000/- as net and Rs. 3,750/- as Tax amount. The Diff

of Rs. 70,000/- should be shown in clause 3 k(computation of

purchases not eligible for set off) as deduction as other allowablededuction.

Q52 : Material of 12.5% rate is purchased for Rs. 1,00,000/- + Rs.

3,750/- now is to be sold for Rs. 1,20,000/- how much tax to be

charged?

Ans: It is purch of material mfg by PSI. The original tax free

amount will be Rs. 70,000/- now tax should be charged on Rs.

50,000/- The bill will be Rs. 1,20,000/- + Rs. 6,250/-

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 41/65

C.A. DILIP PHADKE FCA 41

Q53 : Invoice of March 2010 recd in May 2010 after filing return

for March, What should be treatment?

Ans: If the purchase is recognized in March, the return filed for

March will have to be revised by claiming refund. But if it is

recognized as per chronological method in May then set off can

be claimed in May.

Q54: What will be the rate of Tax if JCB is given on lease locally /

OMS?

Ans: Tax rate will be 12.5% applicable to JCB. In case of OMS

Transaction it will be depend of availability of C Form i.e. 2% or12.5%

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 42/65

C.A. DILIP PHADKE FCA 42

Q 55: The purchaser has paid to the selling dealer amount of Tax

Invoice but it is established that the seller has not deposited the

amount into Govt. Treasury, can set off be claim?

Ans: No. As per Section 48 (5) no set off is available if the same is

not received by the Govt.

Q56. How to treat WCT TDS certificates received / not received?

Ans: Details of TDS Certificate to be entered in Annexure C of

Form 704. But while claiming credit in Schedule III Total Amount of

TDS whether certificate recd or not to be shown in clause 9A(f)

Row 125 any other credits – please specify.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 43/65

C.A. DILIP PHADKE FCA 43

Q 57 : Gas / Oil Co. purchases pipes for moment of gas/oil which

are embedded into ground / building for transmission, Whether set

off will be allowed?

Ans:If pipe lines becomes plant and machinery, the set off will be

available on such purchases. But if It is treated as immovable

property, then no set off will available as per Rule 54. The same is

the case for Electricity Distribution Co. / Telephone Transmission

Co. etc.Q 58 : If in the Balance Sheet while the asset was being

constructed was shown as Capital WIP, Whether set off will be

available?

Ans: As per Section 2(5) capital assets means as defined in Sec2(14) of IT Act means property of any kind held by the assessee.

Hence Set off is allowed.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 44/65

C.A. DILIP PHADKE FCA 44

Q 59: Whether Service Tax and VAT both are chargeable for a

sale transaction, How is the VAT Liability Determined in

Following Case?Sales Value Before Tax Rs. 100/-, Service Tax 10%, VAT @

12.5%. On Which Amount VAT is to be calculated?

Ans : The Supreme Court in case of M/s. Bharat Sanchar

Nigam Ltd. (145 STC 91) held that the State can levy tax onthe sale Element only, if there is a discernible sale and only to

extent relatable to such sale. Thus, it appears that issue

needs to be decided on facts of each case after applying

principles laid down by the Supreme Court. The Definition of

sale price in Section 2(25) does not include Service Tax.Hence, VAT in the Above example will be chargeable on the

amount excluding service Tax.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 45/65

C.A. DILIP PHADKE FCA 45

Q 60: Main Contractor Got a Contract of Rs. 1 Crore. The Same

Contract was Sub-Contracted @95%, whether Main Contractor is

Liable to undertake MVAT Audit?

Ans: Yes. The amount payable to sub-contractor is to be deducted

from the sale price as per Rule 58. Thus, Turnover of Sale will be

only 5 Lakhs for the payment of tax & not for calculating t/o.

Q 61: Computer is Installed in a office and used by the two

Associated Concerns. Both are Registered Dealers.The Concern

owning the Computer raises debit note on other concern for

some charges at the year end. Whether the same is liable to tax?

Ans: It will have to be decided as to whether there is transfer of right to use the computer, if the control, custody & possession of

computer is transferred to associate concern, then there would be

a transfer of right to use and the consideration will be liable to tax.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 46/65

C.A. DILIP PHADKE FCA 46

Q 62: Purchases are made from outside Maharashtra and

delivered outside Maharashtra. The Sale bill is made in

Maharashtra; Whether Such Turnover is to be included in

Turnover?

Ans: Such Turnover need not be Included in Maharashtra, except

when the goods are purchased against ‘C’ Form which was

obtained from the Sales Tax authority of Maharashtra.

Q 63: Whether pure art work or design charges as per the

specification of the Customer without written agreement and

passed on to the customer on CD media is Liable to VAT on Not?

What will be position if designs are being passed on by E-mail?

Ans: Since in the transaction there is no sale of goods it will notattract VAT irrespective of media by which the same is transferred;

(i.e., on C.D. or by e-mail). However if the design is registered

under the Design Act 1911, then it would be sale of goods under

Entry C-39 and will be liable to Tax.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 47/65

C.A. DILIP PHADKE FCA 47

Q 64: Dealer engaged in manufacturing & sale of diamonds. If the

Dealer sells scrap of old machinery etc. Does the Dealer have to

charge VAT on such Sale and at what Rate?

Ans: Yes, at the rate of 5% being scrap of iron and steel

Q 65: In case of work Contract whether work done by

unregistered sub-contractor will be available as deduction? Please

explain the calculation of Tax Liability in the case of workcontractor under Regular Method?

Ans: Work done by unregistered sub-contractor is not available as

deduction. (ii) To work out the liability for tax under regular

method, from the total contract price, admissible deductions u/r 58

be claimed to determine taxable turnover. By applying theapplicable rate to taxable turnover, the tax liability can be worked

out.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 48/65

C.A. DILIP PHADKE FCA 48

Q 66: Is TDS under MVAT different than what is deducted under

the Income Tax Act? Who is Liable to deduct the Tax and in which

circumstances?

Ans: TDS under MVAT is different and is in addition to tax

deducted under the Income Tax Act 1961. Under the MVAT Act,

Notified Employers [Ref: Notifications VAT – 1505/CR-

123/taxation 1 dt. 1-4-2005 and JC(HQ)1/VAT/2005-97 dt. 29-8-

2005) have to deduct the tax. In case the amount payable in ayear exceeds Rs. 5 lakhs, then only provision of TDS is

applicable.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 49/65

C.A. DILIP PHADKE FCA 49

Q 67: In Works Contracts like construction of road, R.A. bills are raised at the

end of the month. These bills are certified by an independent agency which

may take 15 days or even 2 months in some cases. Thereafter, the payment is

released, which may take further time and usually tax is deducted at the time of

payment and paid in the subsequent month. Suppose bill is raised in March,

gets certified and in April,Tax deducted and paid in May. What Turnover figures

are to be given and in which month? When Credit for TDS is to be Taken?

Ans: It depends upon the method followed for revenue recognition in the books

of the contractor. If he records the sales as and when the R.A. Bill is raised say

in the month of March, Sale is to be offered for taxation. Any adjustment in such

value, as and when recorded, will be reflected in the tax period in which such

adjustment is made in books. However, where revenue is recorded only based

on passing of bill, it will be sale of the month in which such sale is booked. A

stand can be taken by the contractor that till the time work is not certified sale

is not concluded. Receipts of Payment are immaterial for determiningconcluded sale. The credit of TDS may be taken in the period in which the

corresponding sale is recorded as per section 31(9). After amendment of

section 31(4) w.e.f. 1-4-2005, it is possible to take the credit for TDS in the

period in which the certificate for payment is furnished. In that case credit of

TDS will have to be taken in the month in which employer had issued

certificate.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 50/65

C.A. DILIP PHADKE FCA 50

Q 68: How does turnover discount (TOD) affect purchases for

the purposes of audit? For example, sales 59,50,000,

Purchases 60,10,000 TOD 2% = Rs. 1,20,000. Net Purchase as

per profit and loss A/c is 58,90,000. As TOD is known at theyear end, it is not deducted in regular return filed.

Ans: The Definition of the terms ‘turnover of sales’ and ‘turnover of

purchases’ are discussed as per the MVAT Act. The TOD is

deductible from purchases. GTO of Purchases will be determinedas Rs. 58,90,000. Thus the dealer is not liable to VAT Audit.

However, care be taken to include other purchases like purchases

debited to P&L A/c, Assets etc, and then GTO of purchases be

determined. If such GTO exceeds Rs. 60 Lakhs, then dealer is

liable to VAT Audit.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 51/65

C.A. DILIP PHADKE FCA 51

Q 69: M/s. X is a metal testing lab. For this, it purchases films,

chemicals, etc. The Turnover of such purchases exceeds 60

Lakhs. Whether M/s. X is required to get registration & the

accounts audited under the MVAT Act?

Ans: M/s. X is not liable to get registered under the MVAT Act.

Under the MVAT Act Liability is required to be determined with

reference to sales. Since, M/s. X is not ‘a dealer liable to pay tax’

Section 61 is not attracted. However, if ‘X’ is already registered thehe will have to get his accounts audited.

Q 70: During the year 2012-13, Sale is Rs. 59,06,000. Car Sale

Rs. 1,00,000/- Is it necessary to carry out MVAT Audit?

Ans: Gross Turnover of sales includes sale of car. Thus GTO ofSales exceeds Rs. 60 Lakhs. Hence, it is necessary to carry out

MVAT Audit.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 52/65

C.A. DILIP PHADKE FCA 52

Q 71: Dealer is a Government Works Contractor. No Bills issued

by the Dealer. Work Measurement and value entered by the

Government engineer in measurement book (MB), which is in the

custody of the Government Dealer. No copy of MB is availablewith the Dealer. Dealer gets Cheque (Net Amount after retention

money, IT – TDS, WCT – TDS) or ECS. Dealer works out the

turnover on the basis of the terms of payment particulars and TDS

certificates (IT & WCT) at year end. How to verify turnover? What

Observations or remarks to be mentioned?

Ans: The facts mentioned above are to be disclosed in the audit

report. The Turnover can be verified based on the payment

Particulars, TDS Certificates and Payments Received, Terms of

Contract etc., and the basis of computation of turnover be

mentioned in the audit report in Cl. d & e of para 3 & para 5 of

part 1.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 53/65

C.A. DILIP PHADKE FCA 53

Q 72: Dealer has no sales but done only construction of building

& installation of machinery in a particular year. The Value of

Purchases of all such capital WIP exceeds 60 Lakhs. Whether

liable to get his accounts audited to submit report? If so to which

authority the audit report should be submitted. Please Elaborate.

Ans: Since the dealer is not liable to pay tax , Section 61 of the

MVAT Act is not applicable. If he wants set off he shall take

registration & file audit report.

Q 73: A Works Contractor opting for composition scheme paying

tax on entire contract amount which exceeds Rs. 60 Lakhs.

Whether Liable to audit?

Ans: Yes. The Turnover of Sales for the purpose of VAT Audit is

60 lacks. The taxable t/o to be determined after applying the

deductions prescribed in rule 58(1).

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 54/65

C.A. DILIP PHADKE FCA 54

Q74: How an employer of a contractor not reg. under MVAT,

but liable to deduct and pay the T.D.S. do the same?

Ans: The Categories of Employers liable to deduct the tax are:1) Central & State Government

2) All Industrial, Commercial or Trading Undertakings

3) Registered Companies

4) Local authorities

5) Co-operative Societies Incl. Housing Soc.6) Registered Dealers of MVAT.

7) Insurance, Finance & Banks

8) Trusts

No TDS shall be made from Sub- contractor Payment.

The TDS shall be made if the amount paid or payable exceedsRs. 5 Lakhs per Annum. In Case of a Co-op Society, if the

value of Contracts awarded is Rs. 10 lakhs or more in the

previous year. The rate of TDS is 2% in case of a contractor

who is registered & 5% in other cases.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 55/65

C.A. DILIP PHADKE FCA 55

Out of above, many employers will be unregistered &

have to pay the TDS and file return in Form No. 405.

They have to approach the Dy. Comm. Of S.T., Business Audit (2) for Mumbai & STO, Returns Branch, in Other

Places with D.D. for the Full Amount of TDS &

Photocopy of PAN Card. The D.D. should be in favour of

“ Bk of Mah.” and in other Places “SBI A/c MVAT’. The

said officer will give a duly signed and serially numberedreceipt for receiving the amount & ack. For having

received return in Form 405/424. The D.D. will be

deposited by the designated officer in Challans in form 6

& after the payments are Realised, send a copy of thechallan to the Employer. The Date of Submission shall

be the date of filing the return & making the payment.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 56/65

C.A. DILIP PHADKE FCA 56

Q.75: What are the changes made in new audit reportversion 2.0.0?

1a) In letter of submission Dealer is expected to give

details of VAT/CST paid based on his acceptance of

VAT Auditor’s Recommendations.

1b) Now there is no necessity for any “Enclosures” in

Letter of Submission as well as in Part-I. As per

instruction no.27 dealer is required to submiti) A statement of submission of audit report duly signed

by the Dealer.

ii) A duly signed copy of Acknowledgement generated

after uploading of audit report in form 704.2) Now the auditor has not to attach financial statements

with annexure with tax audit report but has to certify at

Sr.No.1A that he has taken them on record.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 57/65

C.A. DILIP PHADKE FCA 57

3) In serial no. 1(B) & 1(c) the words “And annexed here with”

are removed.

4) In table-1, serial no.5(a)(ii) return in form 424 is inserted

along with form 405.5) In table-1, serial no. 2(B)(b) the selection of schedules and

annex. as applicable to the dealer, annexure J-3 and j-4 have

been removed.

6) In table-1, certificates at serial no.2(B) clause (c) & (d)

are clubbed as cl. (c).

7) Clause (d) newly introduced as “on the basis of an

information available on the website of department the period

under audit involves no issue in case of this dealer in which a

decision against the State Government or the Commissioner

was delivered by the Tribunal and the Reference and/or

Appeal therein is pending before appropriate forum except

detailed in table 7 herein below, if applicable.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 58/65

C.A. DILIP PHADKE FCA 58

8) Under clause 7 below Table-5 a table has also been

inserted wherein details of references/appeals have been

filed by the State Government or the Commissioner in case of

similar issue is involved in the case of dealer under Auditwhere a decision against State Government or the

Commissioner was given by the Tribunal and the

references/appeals are pending before the appropriate forum

as listed on MAHAVAT Website have to be furnished in the

said clause.9) Certain changes are made in schedule I, III,IV & V because

of insertion of sec. 6A & 6B w.e.f. 1/5/2012 for charging & set

off of purchase tax on cotton or oil seeds. The provision is

made for calculation of purchase tax & its set off.

Now set off will be available on urd purchases also on whichpurchase tax is paid hence in wording change is made where

ever necessary. e.g.

In Sr. no. 3 cl.-O,& Sr. No – 5 cl. (a) the words “from

registered dealer” are removed.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 59/65

C.A. DILIP PHADKE FCA 59

In annex. E instead of heading “Computation of Set-off claim

on the basis of tax paid Purchases effected from Registered

Dealers” it has been replaced with “Computation of Set-off claim on the basis of Tax Paid Purchases”.

10) In annex E sec.-2 New row No.12 has been inserted to

incorporate purchase of taxable goods from registered dealer on

which set-off is not claimed.

11) In annex E sec.-4 for calculating reduction u/r-53 additional

rows are provided for natural gas & D schedule goods.

12) In annex E sec.-5 New row has been provided for details of

total tax paid purchases effected from reg. dealers on which s/o

is calculated and allowed u/r. 52A and 55B along with Rule 52.

13) Annex. G(cert. recd), I (Cert. not recd), J-1(Sales) & J-2

(Purchases): Rows are inserted up to 5000 in place of 1000

14) Annexure J3 & J4: Both the annexure have been removed

in new form 704

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 60/65

C.A. DILIP PHADKE FCA 60

Q.76: Precautions for preparing Annexures of new audit report?

Ans: 1) Put Due Date as 21 or 30 as applicable in Annexure

A&B.2) Annex E – Sec 1 Qty. in liters of petroleumproducts in col.C to be given only in respect of Rs.1/- per liter paid onpurchases by Mfg. co. and not any other product purchasedbypetrol pumps.

3) In Annex. G you have to enter descending order amount of declaration recd. and not invoice value as given in theheading.4) In all the annexure the amt.s are to be given in descendingorders Vat amount. Prepare annex. in excel sheet and paste

it at the end after all entries are arranged in descendingorder. It is difficult to make changes after trf. of data.5) Sales & purchase returns should be shown either by – signin annex. J -1 & J -2 resp. or show net fig. of sale or purchase.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 61/65

Precaution for clause D Para - 3

clause d has been inserted by virtue of sec. 23(8). If

ref./appeals are filed by the State Govt. or the Comm. beforeappropriate forum it is the Assessing officer who must be

aware about the same. The VAT Auditor is supposed to

certify of ref./appeals filed by the State Govt. or Comm. in

respect of similar matter pertaining to dealer. Nearly 900

ref./appeals have been filed before appropriate forum aslisted on MAHAVAT Website. VAT Auditor must go

through all these before certification which is practically not

possible and feasible. The said list of ref./appeals is also

updated on regular basis, which auditor will keep track of thesame while signing VAT Audit Report. Govt. should require

Auditor to certify only if ref./appeals filed in respect of

auditee only and not in general.C.A. DILIP PHADKE FCA 61

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 62/65

C.A. DILIP PHADKE FCA 62

Q. 77: What should be given in Para 3 when it starts with Out of

the aforesaid certificates; the following certificates are negative for

the reasons given hereunder:-

Ans.: Though the wording used is ‘negative’, in my opinion, anyreservation / limiting responsibility statement (which although maynot necessarily mean total negation) that auditor desires to makein respect of any part of report upto Para 3 should be made under

Para 3. In case of clause d as the web site is up dated every day itwill be necessary to mention that ref./appeals up to …. Date aretaken in to consideration.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 63/65

C.A. DILIP PHADKE FCA 63

Q. 78: What should be given in Para 5 when it starts withQualifications or remarks hav ing impact on the tax liability

Ans.: Only those qualifications / remarks that are sure to haveimpact on tax liability should be given here. Limiting responsibilitystatements should not be given under Para 5. The question iswherever the auditor has already computed and reporteddifferential in schedules and report; whether the same againneeds to be reported here. In my opinion single liner in Para 5should cover the issue effectively.

There will be many cases where qualifications will warrantreporting both under Para 3 and Para 5.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 64/65

C.A. DILIP PHADKE FCA 64

As per instruction No. 10. Where dealer is

required to maintain the records about the sales,

purchases, Imports and Exports under Central Excise Act, 1944, the Customs Act, 1962 or under

the State Excise Act in such cases the Auditor

should invariably correlate the details of sales,

purchases, Imports and Exports disclosed under

the said Acts and disclosed under MVAT Act,

2002. Any material difference noticed should be

reported at Para 5 of Part-1 accordingly.

7/27/2019 Issues on Mvat Audit 81 Questions Nov 2013

http://slidepdf.com/reader/full/issues-on-mvat-audit-81-questions-nov-2013 65/65

C.A. DILIP PHADKE FCA 65

![Guide to MVAT[1]](https://static.fdocuments.in/doc/165x107/5532a99c550346c3558b46e6/guide-to-mvat1.jpg)