Issues in Valuation E-Business Valuation. AGENDA 1.DCF Method and Forecasting 2.Valuation of...

32

Issues in Valuation E-Business Valuation

-

date post

21-Dec-2015 -

Category

Documents

-

view

234 -

download

2

Transcript of Issues in Valuation E-Business Valuation. AGENDA 1.DCF Method and Forecasting 2.Valuation of...

Issues in Valuation

E-Business Valuation

AGENDA

1. DCF Method and Forecasting2. Valuation of Dot.coms

– Introduction– DCF Method– McKinsey Method: DCF starting from the

future– The PEG ratio– The Price-to-Sales Ratio– Other multiples

Consistency(or 2 out of 3 ain’t bad)

• To conduct a DCF there are three layers of assumptions that you need to make:– Growth in revenues– Investment Rates– Financing

• You only need to determine two of these. The third one is then given.

Example 1

• If a firm has a target capital structure. – Financing then determines the investment

policy. You just need to forecast how well the firm will invest (NOPLAT → g) to complete your valuation model.

– Examples include firms in emerging markets, which are financially constrained.

Example 2

• Suppose the investment policy is constrained by competition.– In mature industries such as tobacco and

steel growth opportunities are not available. – This fixes growth in revenues and investment

rates.

• Only need to determine the firm’s financial policy (dividends, repurchases, equity & debt issues).

Paper and PencilBack of the Envelope Forecasting

Year 2000 Forecast 2001

Assumptions

Income Statement Description Value

Sales 1000 % of Sales (t-1) 1+0.07

COGS % of Sales (t) 0.7

Gross Profit Arithmetic

Interest % of Debt (t) 0.1

Taxable Income Arithmetic

Taxes% of Taxable Income 0.53

Net Income Arithmetic

Dividends % of Net Income 0.6

Retained Earnings Arithmetic

Balance Sheet

Current Assets % of Sales (t) 0.15

Fixed Assets % of Sales (t) 0.7

Total Assets Arithmetic

Current Liabilities % of Sales (t) 0.07

Debt (PLUG)

Equity

Stock 400 Constant 400

Accumulated Earnings 100 Arithmetic

Total Liabilities Arithmetic

Paper and Pencil Continued

Pro FormaAssumptions

Sales growth 7%

Initial sales 1,000

FA_Sales 70%

CA_Sales 15%

CL_Sales 7%

COGS_Sales 70%

Interest 10%

Dividend Payout 60%

Tax rate 53%

Forecasts

Year 0 1 2 3 4 5

Income Statement

Sales 1,070 1,145 1,225 1,311 1,403

COGS 749 801 858 918 982

Gross Profit 321 343 368 393 421

Interest 28 28 28 28 27

Taxable Income 293 316 340 366 393

Taxes 155 167 180 194 209

Net Income 138 148 160 172 185

Dividends 83 89 96 103 111

Retained Earnings 55 59 64 69 74

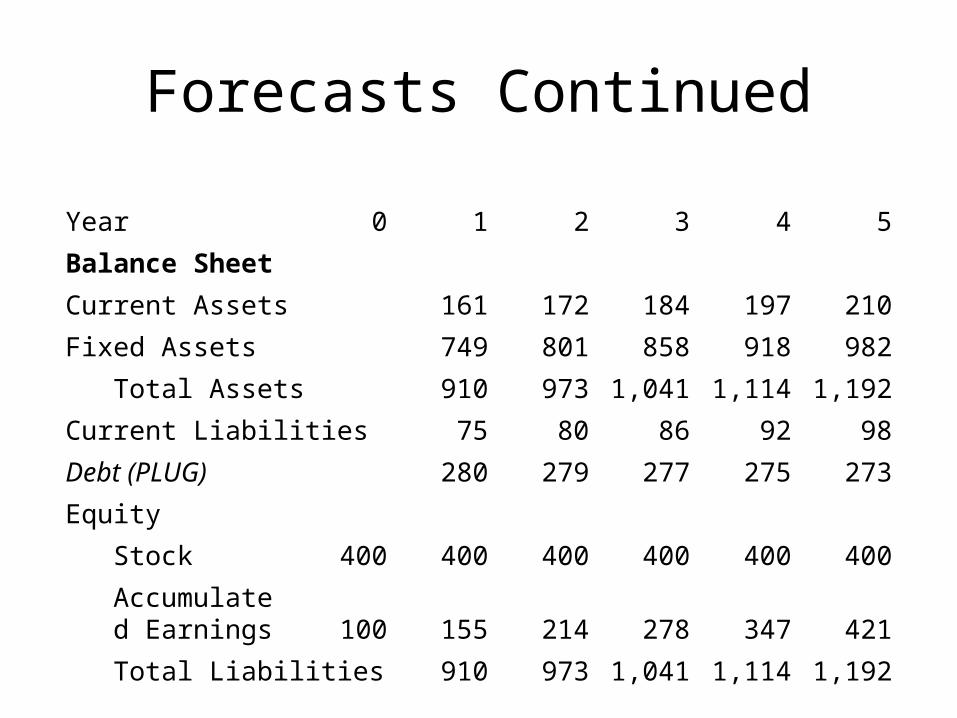

Forecasts Continued

Year 0 1 2 3 4 5

Balance Sheet

Current Assets 161 172 184 197 210

Fixed Assets 749 801 858 918 982

Total Assets 910 973 1,041 1,114 1,192

Current Liabilities 75 80 86 92 98

Debt (PLUG) 280 279 277 275 273

Equity

Stock 400 400 400 400 400 400

Accumulated Earnings 100 155 214 278 347 421

Total Liabilities 910 973 1,041 1,114 1,192

Valuation of Dot.coms

• Valuation of Internet companies has been a hotly discussed topic.

• Most Internet companies have a limited history and have been losing money.

• Yet, share prices of Internet companies are (still) extremely high compared to their financial performance.

Relative ValuesThen: December 2000

• AOL (TWX) $132B > Procter & Gamble (PG) $122B• Schwab (SCH) $43B > Merrill Lynch (MER) $29B• Yahoo (YHOO) $40B > New York Times (NYT) $6B• eBay (EBAY) $23B > Sotheby’s (BID) $2B• Priceline.com (PCLN) $23B > US Airways (UAIR) $5B• Amazon (AMZN) $22B > Barnes & Noble (BKS) $2B

And Now: August 2004• AOL (TWX) $77B < Procter & Gamble (PG) $139B• Schwab (SCH) $12B < Merrill Lynch (MER) $47B• Yahoo (YHOO) $38B > New York Times (NYT) $6B• eBay (EBAY) $50B > Sotheby’s (BID) $1B• Priceline.com (PCLN) $.7B > US Airways (UAIR) $.16B• Amazon (AMZN) $15B > Barnes & Noble (BKS) $2B

.Com Values – Give Up Now?

• There are several features of internet firms that make their valuation a very, very difficult task. – Is it still worth trying?– No choice, every day the market has to take its best guess as to

each firm’s value. Just learn to deal with it.– You get points not for being 100% right, just being right over

50% of the time!

• Three years ago, everybody expected the internet consulting business to surge.– 2000 year-end forecasts estimated the demand for internet

consulting to grow a 50-60% per year, resulting in a market for these services at 60-70 billion in the year 2003!

– Good example of forecasts gone wild.

Forecasts with Negative Earnings

• Current earnings growth rates cannot be used in valuation. What do you do now?

• Use analyst estimates of future earnings. But how did they get their estimates?

• Use your own judgment regarding future costs, and revenues.– Dot com firms typically have large fixed costs and relative to traditional

firms lower marginal costs. – A typical forecast will keep the fixed and marginal costs fairly constant

from year to year. – To get the future earnings you now only need to project out sales

growth. Not easy, but at least you now have a baseline to work with.• The Going Concern Assumption

– Many Dot.coms have failed in the last several years.– Before you assume a terminal value with an infinite life, ask yourself

whether or not you believe the probability that the firm will survive is one? If not remember to adjust you expected cash flows for the probability the firm will go out of business.

Other Hurdles

• Absence of Historical Data– Cannot estimate betas based on historical information

about stock prices.– I would use an asset beta of one. On average it

should be right!

• Absence of Comparable Firms– Cannot value the company based on multiples.– But, you can get a handle on things by looking at a

related industry. For example Priceline is a travel company. What is the beta for firms in the overall travel and tourism industry?

Amazon.comComparison Data

Profitability Company Industry1 Market2

Gross Profit Margin 23.69% 54.25% 49.37%

Pre-Tax Profit Margin 4.61% 1.17% 8.79%

Net Profit Margin 4.61% -1.92% 5.59%

Return on Equity -- -- 11.20%

Return on Assets 14.60% -1.30% 1.90%

Return on Invested Capital 28.40% -1.80% 5.50%

Amazon.com

Valuation Company Industry1 Market2

Price/Sales Ratio 2.62 4.81 1.23

Price/Earnings Ratio 58.45 -- 40.67

Price/Book Ratio -- 5.73 2.47

Price/Cash Flow Ratio 55.11 91.42 10.82

Amazon.comOperations Company Industry1 Market2

Days of Sales Outstanding 7.54 38.78 49.12

Inventory Turnover 19.8 25.3 8.4

Days Cost of Goods Sold in Inventory 18 14 43

Asset Turnover 3.4 0.7 0.4

Net Receivables Turnover Flow 57.1 10.5 8.2

Effective Tax Rate 0.00% -- 33.60%

Amazon.com

Financial Company Industry1 Market2

Current Ratio 1.7 2.42 1.41

Quick Ratio 1.4 2.2 1

Leverage Ratio -- 1.73 5.87

Total Debt/Equity -- 0.24 1.38

Interest Coverage 3.4 2 2.7

Amazon.com

Per Share Data ($) Company Industry1 Market2

Revenue Per Share 14.74 3.61 21.85

Fully Diluted Earnings Per Share

0.66 -0.13 0.66from Total Operations

Dividends Per Share 0 0.01 0.33

Cash Flow Per Share 0.7 0.19 2.48

Working Capital Per Share 1.59 1.59 -0.18

Long-Term Debt Per Share 4.33 0.67 11.33

Book Value Per Share -1.94 3.03 10.87

Total Assets Per Share 4.64 5.24 63.82

Amazon.com

Growth Company Industry1 Market2

12-Mo. Revenue Growth 34.40% 20.60% 15.90%

12-Mo. Net Income Growth -- -- 201.90%

12-Mo. EPS Growth -- -- 61.00%

12-Mo. Dividend Growth -- -83.30% -25.00%

36-Mo. Revenue Growth 22.60% -2.40% 4.40%

36-Mo. Net Income Growth -- -- 11.40%

36-Mo. EPS Growth -- -- -8.40%

36-Mo. Dividend Growth -- -- -9.10%

1Industry: Internet Software & Svcs2 Public companies trading on the New York Stock Exchange, the American Stock Exchange, and the NASDAQ National Market.

Data from Hoover’s Online.

DCF Applied to Internet Firms• At the time of the valuation we might expect an Internet firm to lose

money for at least 5-10 years.– Will it run out of cash first?

• Since this is close to the forecast horizon in the DCF method, all the value creation takes place in the continuation period.

• In this sense, DCF is not different from multiples valuation.• The following are some suggestions to cope with these difficulties:

– Lengthen the projection period from 5 to 10-15 years before assuming constant growth.

– Use a multiple stage model and apply different growth rates and discount rates as the return and risk profile of internet companies change over time,

– Use techniques such as scenario analysis to reduce the risk of assuming one outcome, which may turn to be way off.

McKinsey Approach: DCF starting From the future

• This method consists of estimating the key value drivers once a sustainable growth state has been reached.

• The difficult part involves a thorough analysis of the economic environment.– Competition– Industry position

• The previous analysis would yield a forecast of free cash flows for something like ten years from now.

• Next link the present to the future in a consistent way such as linear growth.

• The discount rates may vary in different subperiods.• Uncertainty may be resolved by means of scenario

analysis

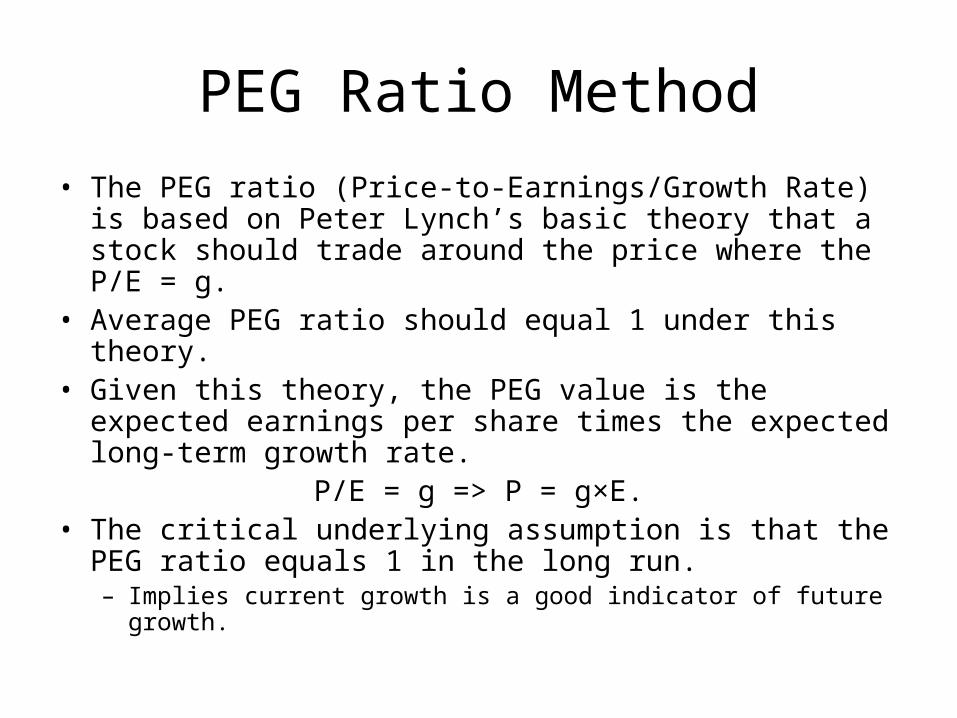

PEG Ratio Method

• The PEG ratio (Price-to-Earnings/Growth Rate) is based on Peter Lynch’s basic theory that a stock should trade around the price where the P/E = g.

• Average PEG ratio should equal 1 under this theory.• Given this theory, the PEG value is the expected

earnings per share times the expected long-term growth rate.

P/E = g => P = g×E.• The critical underlying assumption is that the PEG ratio

equals 1 in the long run.– Implies current growth is a good indicator of future growth.

PEG: The Good and Bad• The Good

– If all firms within a sector have similar growth rates and market risk, a strategy of picking the lowest PE ratio stock in each sector will yield undervalued stocks.

– Portfolio managers and analysts sometimes compare PE ratios to the expected growth rate to identify under and overvalued stocks.

• Firms with PE ratios less than their expected growth rate are viewed as undervalued.

• The Bad– There is no general basis for believing that a firm is undervalued just

because it has a PE ratio less than expected growth.– This relationship may be consistent with a fairly valued or even an

overvalued firm, if interest rates are high, or if a firm has a high market risk.

– As interest rates decrease (increase), fewer (more) stocks will emerge as undervalued using this approach.

PEG: Application• The PEG ratio is the ratio of P/E to expected growth in earnings per• share.

PEG = PE / Expected Growth Rate in Earnings.• Check to make sure the earnings and growth rate used to compute

the PEG ratio are:– From the same initial year.– Calculated over the same period (2 years, 5 years).– Derive from the same source (analyst projections, consensus

estimates).• Are the earnings used to compute the PE ratio consistent with the

growth rate estimate?– No double counting. If the estimate of growth in earnings per share is

from the current year, it would be a mistake to use forward EPS in computing PE.

– Double counting puts the growth rate in twice. Once in the PEG and a second time in the projected earning’s boost .

PEG and Fundamentals• Remember that High risk companies will trade at much lower PEG

ratios than low risk companies with the same expected growth rate.– A company that looks to be the most under valued on a PEG ratio basis

may just be the riskiest firm in the sector.• Companies that can attain growth more efficiently by investing less

in better return projects will have higher PEG ratios than companies that grow at the same rate less efficiently.– Companies that look cheap on a PEG ratio basis may be companies

with high reinvestment rates and poor project returns.• Companies with very low or very high growth rates will tend to have

higher PEG ratios than firms with average growth rates. This bias is more pronounced for low growth stocks.– PEG ratios do not neutralize the growth effect.

Price to Sales• Unlike price-earnings and price-book value ratios, which can

become negative and not meaningful, the price-sales multiple is available even for the most troubled firms.

• Unlike earnings and book value, which are heavily influenced by accounting decisions on depreciation, inventory and extraordinary charges, revenue is relatively difficult to manipulate.

• Price-sales multiples are not as volatile as price-earnings multiples, and hence may be more reliable for use in valuation.

• Over time, studies have shown that companies revert to a "normal," or average, PSR applicable to the industry in which they operate.– Big supermarkets, courtesy of their low margins and competitive

environment, usually trade on a PSR of about 0.5

Calculation• The PS ratio equals the equity value divided by

the firm's sales. You can either use total values or per share values. Either will give you the same answer as the units cancel.

• For Amazon (8/6/2004):• Revenues per share $14.74• Stock Price 35.90• PS Current 2.44 = 35.90/14.74• PS Current (Industry) 4.81

EPS = .

S

Other Multiples

• Basically these are ratios based on measures of web traffic:– Price/Customer or User.– Hit ratios/Click-through ratios (i.e. price/hits etc).– Price/”growth flow” (growth flow = earnings with R&D

added back in).

Sources:

www.mediametrix.com

www.internet.com