issue 22 - EPRA

44

ISSUE 22 EPRA NEWS - ISSUE 22 GUEST EDITOR Mark Cooper % CALM BEFORE THE STORM FEATURES % INTERVIEW WITH GUILLAUME POITRINAL % REAL PROPERTY INVESTMENT LAW IN NEW EUROPE % ISLAMIC REITS % MANY OPPORTUNITIES ABROAD FOR INVESTORS MARKET FOCUS % GLOBAL LISTED PROPERTY UNIVERSE % MARKET OVERVIEW – FIRST QUARTER 2007 % EUROPEAN ANALYST COVERAGE % CITYCON: AN EXPANDING RETAIL PROPERTY EXPERT

Transcript of issue 22 - EPRA

i ss u e 22

EPRA

NEW

S -

ISSU

E 22

guest editor Mark Cooper% Calm before the storm

features

% IntervIew wIth GuIllaume PoItrInal% real ProPerty Investment law In new euroPe% IslamIC reIts% many oPPortunItIes abroad for Investors

market focus

% Global lIsted ProPerty unIverse% market overvIew – fIrst Quarter 2007% euroPean analyst CoveraGe% CItyCon: an exPandInG retaIl ProPerty exPert

As at 16 June 2007

EPRA MEMBERSAustrAliA

•OrchardFundsManagement

•Univ.ofWesternSydney,PropertyResearchCentre

•ValadPropertyGroup

•VanguardInvestmentsAustralia

AustriA

•CAImmobilienAnlagen

•conwertImmobilienInvest

•Immoeast

•ImmofinanzImmobilienAnlagen

•MeinlEuropeanLand

•Warimipex

Belgium

•Befimmo

•Cofinimmo

•LeasinvestRealEstate

•Petercam

•SolvayBusinessSchool

CAnAdA

•OxfordPropertiesGroup

•Presima(CDPCapital)

FinlAnd

•Citycon

•CREFCenterforRealEstateInvestment&Finance/Hanken

•KTIFinland

•Sponda

FrAnCe

•AcantheDeveloppement

•Affine

•AXAREIMFrance

•BNPParibas

•E.M.G.P.

•FoncièredesRégions

•FoncièreParisFrance

•Gecina

•Klépierre

•Mercialys

•OrcoPropertyGroup

•Silic

•SociétédelaTourEiffel

•SociétéFoncièreLyonnaise

•SociétéGénérale

•Unibail

•UniversitéParisDauphine

germAny

•AlstriaOffice

•BeitenBurkhardt

•ColoniaRealEstate

•DBRealEstateInvestment

•DeutscheEuroshop

•DeutscheWohnen

•DICAsset

•EurocastleInvestment

•GBWAGBayerischeWohnungs-Aktiengesellschaft

•Heitman

•HSHNordbank

•HypoVereinsbank

•IRE|BSImmobilienakademie

•IVGImmobilien

•PATRIZIAImmobilien

•Rothschild

•SEBAssetManagement

•TAGTegernsee

•Viterra

•Vivacon

•WestLB

greeCe

•BabisVovos–International

ConstructionGroup

•EurobankPropertiesREIC

•LamdaDevelopment

Hong Kong

•HongkongLand

•UniversityofHongKong,Dept.ofRealEstate&Construction

isrAel

•Gazit-Globe

itAly

•Aedes

•BeniStabili

•IGD

•Pirelli&C.RealEstate

•Risanamento

netHerlAnds

•ABN-AMROAssetManagement

•ABPInvestments

•AMBPropertyEurope

•AmsterdamSchoolofRealEstate

•BPFBouwinvest

•CBRichardEllis

•CITCO

•CliffordChance

•CordaresRealEstate

•Corio

•DeloitteRealEstate

•DoctorsPensionFunds

•Ernst&YoungEuropeanRealEstateGroup

•EurocommercialProperties

•FortisInvestmentManagement

•Kempen&Co

•KPMGAccountants

•LaSalleInvestmentManagement

•Loyens&Loeff

•MNServices

•NIBCBank

•NieuweSteenInvestments

•PGGM

•PhilipsPensionFund

•PricewaterhouseCoopers

•ProLogis

•RedevcoEuropeServices

•RodamcoEurope

•SpazioInvestment

•SPFBeheer

•UniversityofMaastricht

•VastNedGroup

•Wereldhave

norwAy

•NorwegianProperty

russiA

•EasternPropertyHoldings

•SistemaHals

singApore

•GICRealEstate

•KeppelLand

•NationalUniversityofSingapore,Dept.ofRealEstate

spAin

•InmobiliariaColonial

•Metrovacesa

•ParquesolInmobiliariayProectos

•RentaCorporaciónRealEstate

•ReyalUrbis

•TESTA(GrupoSacyrVallehermoso)

sweden

•Castellum

switzerlAnd

•AllrealHolding

•CUREM

•PSPSwissProperty

•Sal.OppenheimRealEstate

•SwissPrimeSite

•ZüblinImmobilienHolding

united ArAB emirAtes

•AbuDhabiInvestmentAuthority

united Kingdom

•AllcoFinance

•AMPCaptialReddingInvestors

•AssetValueInvestors

•BarclaysGlobalInvestors

•BDOStoyHayward

•BigYellowGroup

•BerwinLeightonPaisner

•BritishLand

•Brixton

•CambridgePlaceIM

•Capital&Regional

•CassBusinessSchool

•Citigroup

•CreditSuisseFirstBoston

•DerwentLondon

•DeutscheBank

•DTZInternational

•EuroHypo

•GoldmanSachs

•GraingerTrust

•Hammerson

•HelicalBar

•HendersonGlobalInvestors

•HinesEurope

•HSBCBank

•InvistaFoundationProperty

•JPMorgan

•JPMorganCazenove

•LandSecurities

•LehmanBrothers

•LibertyInternational

•Linklaters

•Lovells

•M3CapitalPartners

•MapeleyEstates

•MerrillLynch

•MorganStanley

•MorleyFundManagement

•Moody’sInvestorsService

•NabarroNathanson

•PrincipalGlobalInvestors

•QuintainEstates&Development

•Safestore

•Schroders

•Shaftesbury

•SEGRO

•SpeymillGroup

•StandardLifeInvestments

•ThamesRiverCapital

•UBSInvestmentBank

•UKBalancedPropertyTrust

•UKCommercialPropertyTrust

•UniversityofCambridge,Dept.ofRealEstate

•UniversityofReading,CentreforRealEstateResearch

•WarburgPincus

•WestfieldGroup

•WorkspaceGroup

usA

•Archstone-Smith

•AEWCapitalManagement

•CherokeeINvestementServices

•Cohen&SteersCapitalMgmt

•CornerstoneRealEstateAdvisors

•EuropeanInvestors

•FidelityMgmt&Research

•ForumPartnersIM

•FranklinTempletonInvestments

•GEMRealtyCapital

•INGClarionRealEstateSecurities

•KensingtonInvestmentGroup

•MercuryPartners

•MITCenterforRealEstate

•TheOhioStateUniversity

•TabernaRealtyFinanceTrust

•RealFoundations

•RussellInvestmentGroup

•SimonPropertyGroup

•SNLFinancial

•TheTuckermanGroup

•TheWhartonSchool,Zell-LurieRealEstateCenter,

Univ.ofPennsylvania

July 2007, issue 22

GUEST EDITORCalm before the storm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

NEWSIn the news . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

FEATURESInterview with Guillaume Poitrinal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

The status of Real Property Investment Law in New Europe . . . . . . . . . . 10

Islamic REITs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

G-REITs without residential real estate:

many opportunities abroad for investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

MARKET FOCUSREITs within the context of the Global Listed Property Universe . . . . . . 16

EPRA Sees Global Real Estate Coalition Emerging

Over Accounting Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Market Overview – First Quarter 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Unibail . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

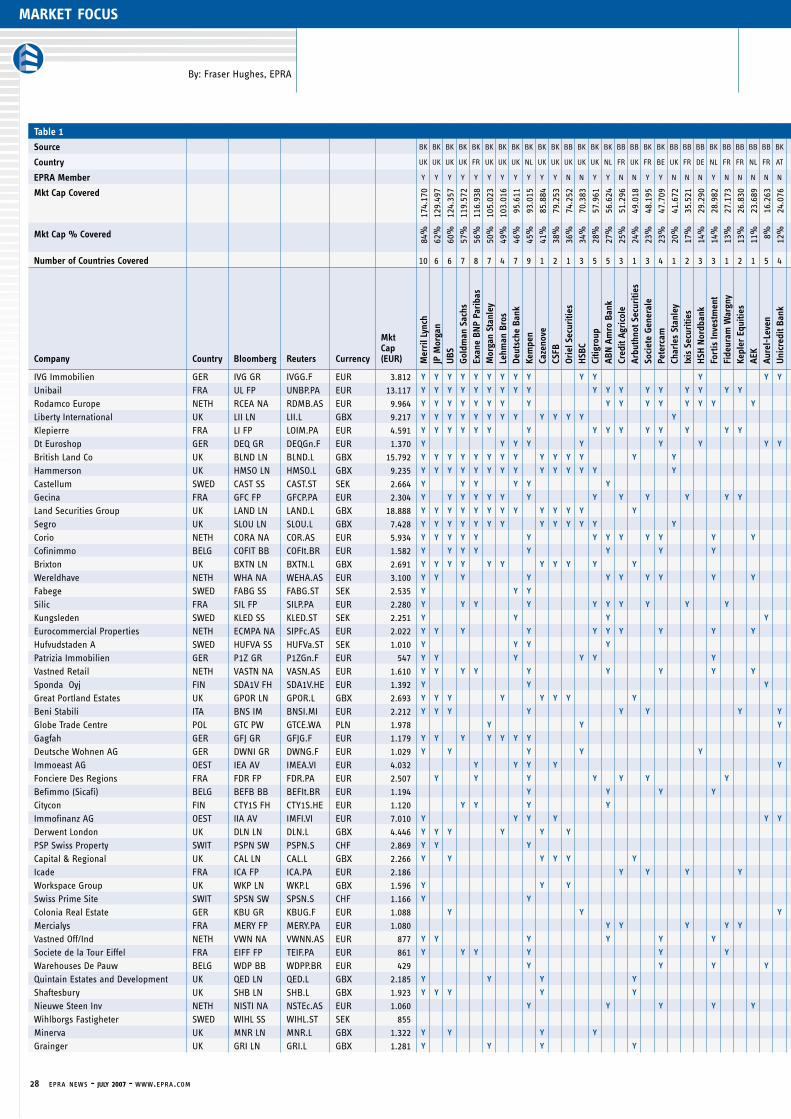

European Analyst Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Citycon - An Expanding Retail Property Expert . . . . . . . . . . . . . . . . . . . . . . . . . . .32

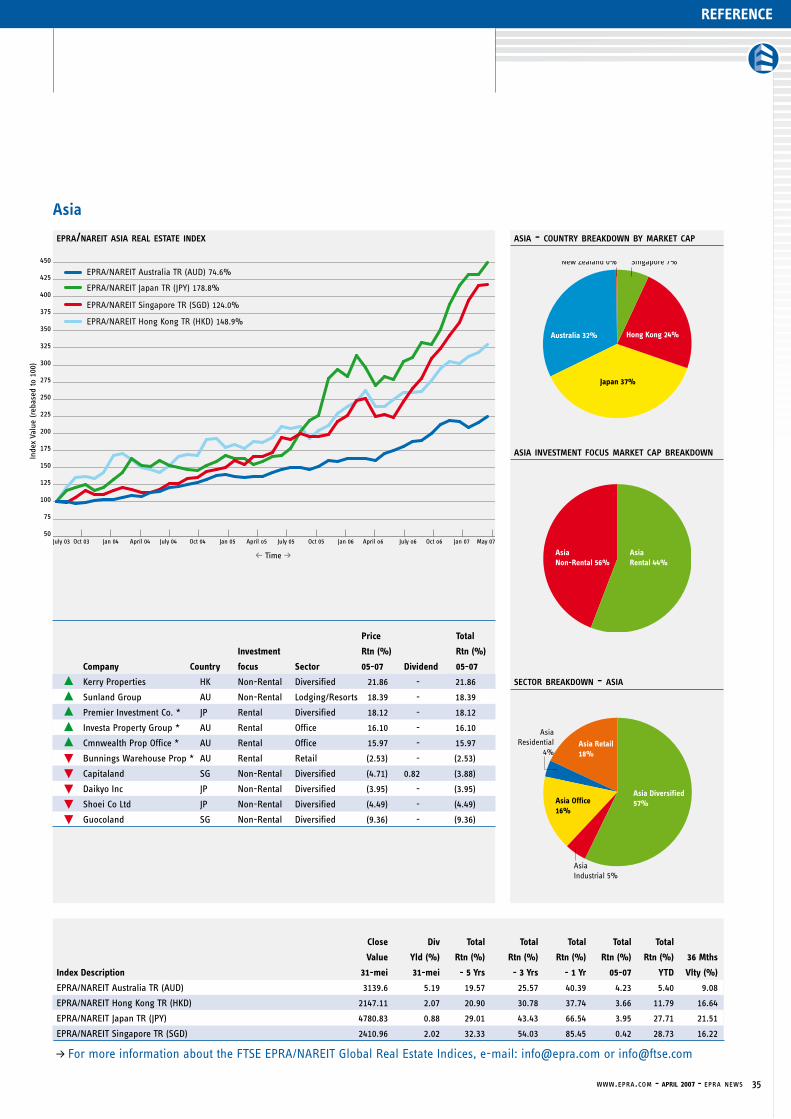

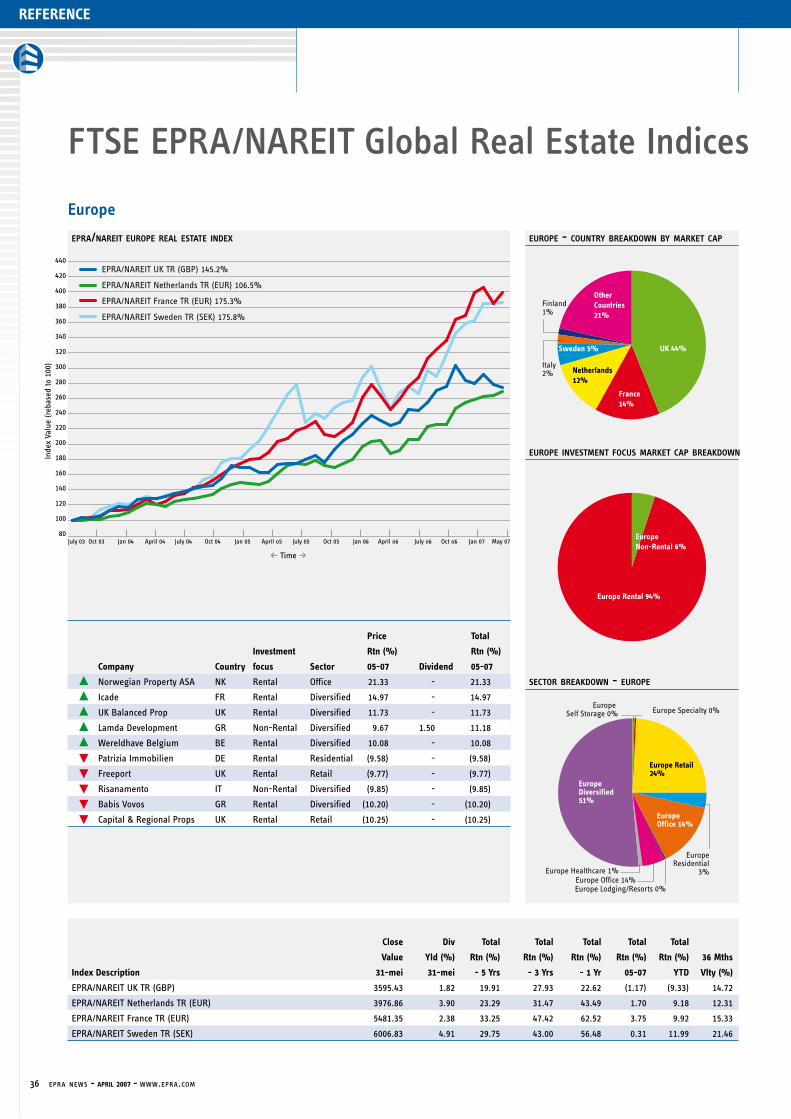

REFERENCEFTSE EPRA/NAREIT Global Real Estate Indices . . . . . . . . . . . . . . . . . . . . . . . . . 34

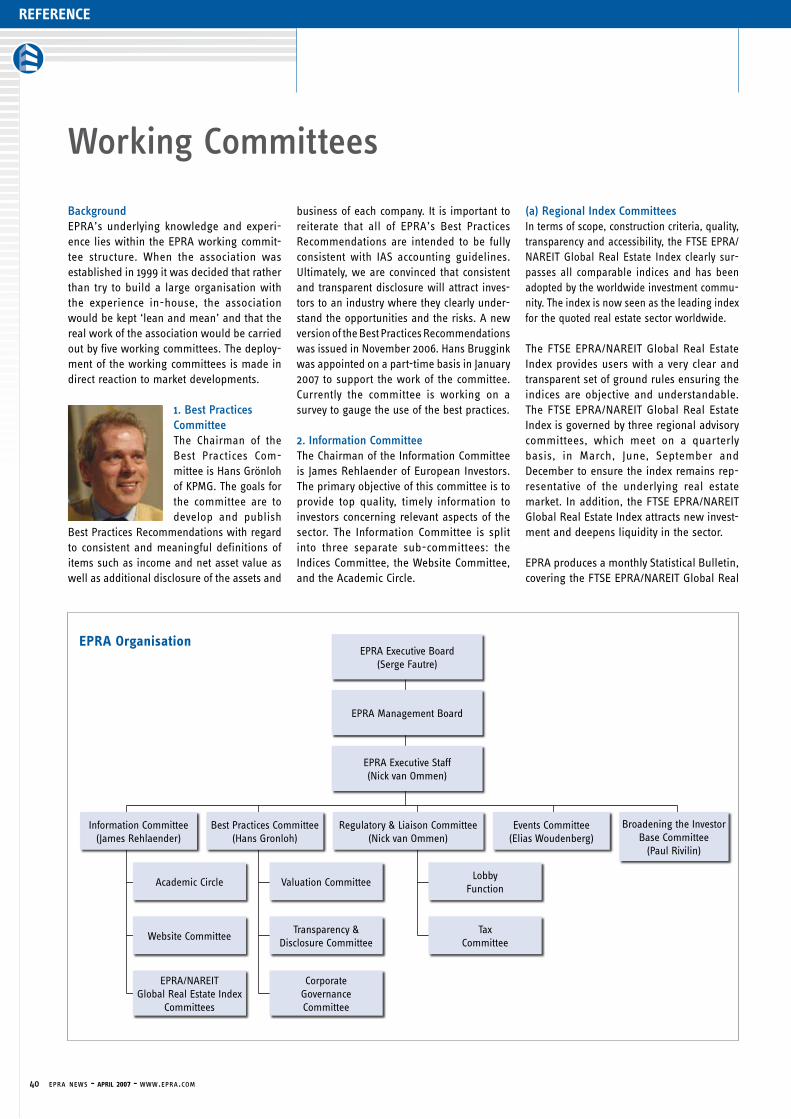

Working Committees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Annual Conference 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

CONTENTSCREDITS

GUEST EDITORMark Cooper, Europroperty

ARTICLE CREDITSMarcus Cieleback, EurohypoCharles Cruden & Jacques de Servigny, Gide Loyrette NovelGerard de Gunzburg, M3 Capital PartnersMike Grupe, NAREITSteve Hays, Bellier FinancialHanna Jaakkola, CityconHarm Meijer & Osmaan Malik, JPMorganAlex Moss, AME CapitalAtasya Osmadi, University of Western SydneyGuilaume Poitrinal, UnibailSandra Steel, FTSE

DESIGN & LAYOUTLen Shape – info@lenshape .nl Marek Maakt – mm@marekmaakt .nl

PRINTINGSmiet-Offset BV, Den Haag

FROM EPRA

Welcome to the 22nd edition of EPRA News

We are in the thick of our preparations for the

8th annual conference on 6 & 7 September

2007 in the Hotel Grande Bretgne, Athens,

Greece . We have now closed the opportunity

to sponsor the conference . We closed sponsor-

ship at eight headline and 24 standard spon-

sors . Unfortunately, anyone wishing to sponsor,

must now wait for the 2008 conference in

Dublin . A full list of sponsors can be found

in the conference section of the newsletter,

under the ‘Reference’ section . In addition, as

most people are aware, we limit the delegate

number to 250 . We are rapidly approaching

80% of this capacity, and the Grande Bretgne

is fully booked . This incredible level of support

clearly means that the conference is clearly well

respected in the industry and members appre-

ciate the work we are doing of their behalf .

As always, we would like to encourage members

to get involved with the publication and come

forward with suggestions for contributions and

articles . We must ensure the newsletter is both

topical and interesting for the reader .

Please send your comments and suggestions

to: info@epra .com

� epra news - july 2007 - www.epra.com

EuroProperty is Europe’s leading commercial

real estate investment magazine. Published

twice a month, it focuses on cross-border busi-

ness, tracking deals, M&A activity and fund

launches across Europe.

Mark Cooper is group editor of EuroProperty.

Prior to this he spend a year as editor of IPE

Real Estate magazine. He has eight years

experience in real estate journalism, starting

his career with the Estates Gazette in the UK.

’ ContactMark Cooper

Group Editor

EuroProperty

Tel: +44 (0)20 7911 1845

Mob: +44 (0) 7795 657 066

Fax: +44 (0)20 7911 1900

1 Procter Street

London WC1V 6EU

Mark CooperGroup editor of

EuroProperty

Are we to see a wave of private equity takeovers in the European listed prop-

erty sector, following a couple of years of take-private transactions in the US? Or more mega-mergers such as the swallowing of Rodamco Europe by Unibail?

Prior to the introduction of the UK REIT, many commentators predicted a rush of mergers as the new REITs jostled to find their place in the market, to achieve signifi-cant scale and to attract international share-holders. Overall, there has been rather less M&A activity in the European market than might have been expected. In fact, European real estate stocks have performed pretty sluggishly since the start of the year, pro-ducing a -0.79% return in the year to May – surely not the sign that the market is expecting a wave of takeovers.

Since the flurry of activity in the SIIC sector a few years ago and in Spain, there has been fairly little activity other than Derwent Valley’s acquisition of London Merchant Securities and the Unibail/Rodamco Europe deal. Since then Foncière des Régions has announced its intention to merge with Beni Stabili, so we may be seeing the start of a trend.

However, compared with the massive priva-tisation drive in the US, where the take-pri-vates of Equity Office Properties and Archstone-Smith alone took more than $50bn of property out of the public markets, there has been almost nothing in Europe. This seems rather odd, especially as the growth prospects in continental Europe are much stronger than in the US. The big private equity players involved in REIT take-privates in the US all have very significant operations in Europe. And they all have plenty of cash to play with.

One reason why private equity players are not taking on big M&A deals may also explain why European companies are not getting involved in consolidation. A significant amount of attention and capital has been turned towards the east and the developing markets of eastern Europe and Russia.

Rather than looking for western European companies to buy, players like Morgan Stanley are investing in ventures in Russia and the east. Similarly, companies which have raised significant chunks of equity, such as Immoeast and Meinl European Land, have been raising it to expand eastwards.

It may also be that European REITs and other listed property companies are just too expen-sive. US REITs and their portfolios tend to be higher yielding than European companies. The most attractive continental European REITs tend to trade at a premium to net asset value so there’s little chance of picking them up on the cheap, although finance costs on the continent are still low to enable highly-geared players to leverage the stuffing out of a portfolio. However, that they are not doing it suggests they are cautious on the pros-pects of value growth in core European markets.

However, a company with a strong develop-ment pipeline could be worth buying in to as standing investments could be sold into a still-hot market in order to focus on the added value development business. Analysts canvassed by EuroProperty for a recent article said the strength of Hammerson’s development pipeline is one of the reasons it has been the most talked-about takeover target. The only question is whether its board and shareholders would let it go at a price to suit a private equity buyer.

The other UK majors have generally been trading at a discount to net asset value of at least 10%, which could offer opportunities. However, it’s fairly unlikely that any buyer could pick these companies up even at net asset value. Derwent Valley bought London Merchant Securities for a 30% premium to net asset value so it’s pretty clear there’s nothing going cheap. Nonetheless, most of the analysts EuroProperty spoke to still reckon a private equity buyout of a UK major is likely this year.

The full price Derwent paid was a reflection of how important London Merchant Securities was to its plans to become a significant

Calm before the storm

By: Mark Cooper

guest editor

www.epra.com - july 2007 - epra news �

guest editor

Calm before the storm

central London REIT. And it is this desire to create sector-dominating businesses which will drive merger activity in the European listed sector in the next few years.

The pace of this activity will inevitably be fairly slow as the companies involved are large and bids take time to assemble. However, there is a real opportunity for com-panies with big ambitions in the region to position themselves for the long term.

From a pricing point of view, it’s probably the wrong time to start buying, but from a strategy point of view, it’s unlikely to be better. Sentiment is good and shareholders will be happy to sanction big plans. Continental European players have a big advantage here: their ratings are higher and they have access to cheaper debt. Picking up their peers on either side of the Channel could be relatively straightforward.

But what about the UK majors? They have been the most significant companies in the European sector but, apart from Hammerson and SEGRO, have little presence outside the UK. The recent sluggish performance of the UK market may protect some of them, but also prevent them from expanding on the continent. There’s no reason of course why a UK company shouldn’t remain a UK company,

but if it does it won’t be a major in the future. They’ll be more like those US REITs which specialise in the West Coast or other regions. In an increasingly integrated Europe, the future giants will be sector specialists with cross-border presence.

This will not just be scale for the sake of it, but the scale to service global occupiers, the country diversification to offset cycles and most importantly, the room to grow and develop as Europe grows and develops.

Unibail has made a strong start with the Rodamco acquisition – it now has a significant retail weighting and a genuinely pan-European business. It would make sense to develop the business in that direction. However, Foncière des Régions remains very diversified – a col-lection of different businesses. The US experi-ence would suggest that this will change and non-core business lines like residential and hotels must eventually be spun off.

While the management teams of sector-diversified companies generally tend to press the benefits of the current way of things, such as the ability to ride the downturn in one sector by focusing on another, the evi-dence is that shareholders – particularly big REIT funds – like sector specialisation. And it is these shareholders who will take the

market forward across the world. Mini-con-glomerates will not survive in property. On the other hand, a company like Derwent London can remain as a significant niche player with scale in its specialist market.

But what about Land Securities or British Land. Both companies have done well in recent times, but it seems inevitable that they will be broken up into their distinct business lines. In fact, it would make sense for them to swap their diverse business lines, so Land Securities would take on British Land’s retail assets while BL swallow LandSec’s office business.

But if either company wants to be a truly sig-nificant European player in the future, it will have to cross the channel in a significant way. This might seem difficult and expensive, but if LandSec sold off its office assets and Trillium, for example, it would have a pretty significant cash pile for buying businesses in continental Europe. However, that’s a pretty serious step for management to take; it is more likely that LandSec and companies like it will carry on as they are until shareholder pressure breaks them up.

Those companies with a significant foothold outside their domestic market, however, have a real chance to be the big names of the future. $

The Chicago skyline, home to Blackstone’s newly acquired Equity Office empire.

� epra news - july 2007 - www.epra.com

news

In the news

EPRA’s Travels

Nick and Fraser traveled to the NAREIT Investor conference in New York at the

beginning of June and following this Nick flew alone to Montreal to speak to Canadian investors. The amount of interest generated by North American investors for global listed real estate continues to be strong. Nick also made trips to the OECD meeting in Sydney in

FTSE EPRA/NAREIT Developments

There are a number of recent developments with FTSE EPRA/NAREIT. Please see below:

• The Launch of FTSE EPRA NAREIT Europe REIT index (scheduled for June 25th): Created in response to market demand, the FTSE EPRA/NAREIT Europe REITs and Non-REITs indices will enhance the FTSE EPRA/NAREIT index series, and reflect all of Europe’s developed markets. These real time indices, will be calculated on a daily basis, every 15 seconds and will be of interest to institutional investors in real estate securities who want to differenti-ate between Europe REITs and Europe Non-REITs.

• BGI Launched iShares FTSE EPRA/NAREIT UK Property Fund (Listed on LSE) on 20 March 2007.

• The FTSE EPRA/NAREIT Capped indices were launched on 20 June to enhance the EPRA/NAREIT product range, and to create new indices which meet the UCITs III requirements (no weightings above 10%). $

EPRA Membership hits 201

Membership numbers continue to rise. Since the last edition in March we have

welcomed nine new members from nine dif-ferent countries. New members for this period are: Alstria Office (Austria), Cornerstone (United States), Eurobank Properties (Greece), Fonciere Paris France (France), GBWAG (Germany), Norwegian Properties (Norway), Orchard Fund Management (Australia), Parquesol (Spain) and University of Maastricht (Netherlands). A full membership list is located on page 2 of the newsletter. $

ing carbon footprint in 2007. To round things off, Fraser spoke at the IPF property course in London on two separate occasions in April and June. $

eprA has appointed philip Charls (58), currently general manager of the dutch Chamber of Commerce for Belgium and luxembourg, as its new Chief executive officer, with effect from october 1st, 2007.

He succeeds Nick van Ommen (60) who has led EPRA as Chief Executive Officer since May 2000, following the association’s inception in October 1999.

“I am delighted at Philip’s appointment and confident he will build on EPRA’s success in the future, due to his broad managerial and financial market experience, and through working closely with the association’s com-mittees,“ Van Ommen said.

April to discuss international tax issues, the BPF REIT conference in London, and he gave presentations at the Vienna real estate exhi-bition and the Milan real estate conference in May. In June he attended the Morgan Stanley conference in London and scheduled two days of one-on-ones. I am afraid Al Gore would be horrified at Nick’s rapidly expand-

“The tax harmonisation of Real Estate Investment Trusts (REITs) between the U.S. and Europe, the planned launch of deriva-tives on the FTSE/EPRA NAREIT real estate indices this year, and the expansion of coop-eration with our partner associations -- NAREIT in the U.S. and APREA in Asia, are just some of the key areas we are working on,” he added.

Philip Charls has held his position at the Dutch Chamber of Commerce since 2001 and prior to that was Chief Executive Officer of RVS-Insurance Belgium, part of the ING Group, for seven years.“I’m looking forward to joining such an internationally diverse and dynamic organi-sation as EPRA, operating in one of the most

exciting investment sectors, as the growth in real estate stocks around the world has been phenomenal in recent years. I trust the team will meet to the expectations set by the industry for the coming years,” Charls said. $

EPRA appoints Philip Charls as new Chief Executive Officer

Philip Charls

www.epra.com - july 2007 - epra news �

Michael R. Grupe is executive vice president for

Research and Investor Outreach at The National

Association of Real Estate Investment Trusts

(NAREIT). NAREIT is the trade association for

real estate investment trusts (REITs) and pub-

licly traded real estate companies with an

interest in the U.S. property and investment

markets. At NAREIT, he directs all research and

investor outreach activities related to industry

information, the analysis of industry perfor-

mance, the design and implementation of

membership surveys, communication with

investors, the media, policymakers and the

public, and support for the association’s Policy

& Politics agenda. He also acts as liaison to the

press on technical issues involving REIT indus-

try experience and practice.

Michael earned his Ph.D. degree in business-

statistics from The University of Wisconsin. He

is a member of the Urban Land Institute, the

American Real Estate Society and the Advisory

Board of the Real Estate Research Institute.

’ ContactNational Association of Real Estate Investment

Trusts

1875 Eye Street NW, Suite 600

Washington, DC 20006-5413

Tel: 202-739-9400 or 800-3-NAREIT

E-mail: [email protected]

Michael R. GrupeExecutive Vice President,

Research and Investor

Outreach

The National Association

of Real Estate Investment

Trusts

news

Ibbotson explored optimal global real estate allocations by creating and comparing the

performance of optimal portfolios based on two different methodologies: one that con-structed portfolio performance using histori-cal investment returns for various asset classes, and another that projected future portfolio performance using forward-looking, expected investment returns.

Ibbotson’s historical analysis of data for the period 1990-2005 showed the addition of global real estate allocations improved returns of global portfolios, with nearly all of that increase coming from U.S. real estate investment, according to Thomas Idzorek, Ibbotson Associates’ Vice President of Research and Product Development, and co-author of the study.

“The forward-looking analysis indicated that North American real estate should continue to be approximately half of the total real estate allocation in an optimized global portfolio and serve as a core component of the global market portfolio,” Idzorek said. “As compared with the optimized portfolio based on histori-cal data, future allocations to European and Asian real estate should increase. The forward-looking optimizations include significant allo-cations to Asian and European real estate. As always, the key is diversification.”

Real Estate Boosts Historical Portfolio ReturnsIbbotson created its historical models by charting risks and returns for various asset classes for the 1990-2005 period and con-structing optimized portfolios of moderate risk (defined by a volatility level of 10 percent) with and without global listed real estate. The real estate asset class was represented by the FTSE EPRA/NAREIT Global Real Estate Index, with its North American, European

and Asian sub indices. The researchers found that the optimized real estate allocations by region placed the bulk of investment in North America, because of its superior returns and lower volatility, with little allocation to Europe and none to Asia.

Modeling the FutureThe future performance of global real estate, however, is unlikely to be the same as that of the past. Consequently, Ibbotson constructed estimates of future investment returns for each asset class by blending historical returns with expected future returns. Importantly, the future return calculations took into con-sideration the historical levels of risk (volatil-ity) and correlation for each asset class and geographic region, based on the assumption that, over time, higher levels of risk will be commensurate with higher returns.

In Ibbotson’s unconstrained, forward-looking optimizations, allocations to global real estate range from 15 to 24 percent at the moderate-risk level (10 percent volatility). The allocations, however, were diversified among the world’s real estate markets.

“Approximately half of the real estate alloca-tion – 12.1 percent of the total portfolio – still went to North America,” said NAREIT Executive Vice President of Research and Investor Outreach Michael Grupe. “However, one-third of the forward-looking real estate allocation – 7.8 percent of the total portfolio – went to Europe, and 3.4 percent of the total portfolio went to Asian real estate.”

Additionally, Ibbotson’s forward-looking expected returns are more conservative when compared with historical investment performance. Including global real estate,

Ibbotson projected a 9.60 percent average total return for the optimal forward-looking portfolio, down from the 10.98 percent average annual return of the optimal his-torical portfolio.

“Ibbotson’s forward-looking results point to the growing importance of the European and Asian real estate markets for global investors – but also to the continuing importance of the North American market and the overall importance of real estate investment in a globally allocated longterm portfolio,” Grupe said. “However, they also may indicate that, going forward, investors may be required to assume more risk to achieve returns compa-rable to historical ones.” $ Ibbotson Report available from:www.epra.com

WASHINGTON, DC—At $4.6 trillion, income-producing commercial real estate – indirect and direct – is a major component of the global investment universe, and investors increasingly are globalizing their real estate allocations. The spread of the REIT approach to real estate invest-ment makes it easy and efficient for investors around the world to invest in other regions. At a time when many investors are diversifying abroad, the findings of a new Ibbotson Associates study, commissioned by NAREIT, serve as a reminder that a global real estate investment port-folio should be anchored with a significant allocation to North American real estate.

Ibbotson study underscoresImportance of real estate in global investment portfolios

Portfolio Optimization Study Points to Continuing Importance of North AmericanReal Estate Market; Growing Roles for Europe and Asia

� epra news - july 2007 - www.epra.com

features

FH: How and why did you decide get into real estate?GP: I entered the real estate market in 1995. After a few years with Morgan Stanley M&A department, Leon Bressler offered me an opportunity to join Unibail to head up the corporate development activities. I did not know anything about the sector, but I liked the CEO, the team and the company.

FH: Leon Bressler is a tough act to follow, how do you think you are doing? GP: Leon and I have worked together very closely for 12 years. In this context, this suc-cession is a continuation more than anything else. I accepted the job because I strongly believe in the future of the company, based on its backbone of advanced skills, unique positioning and development outlook.

FH: The Rodamco/Unibail deal means that you will lead the largest company in Europe. Did you envisage this when you took over?GP: Size is not the prime objective of the transaction. The prime objective is to deliver shareholder value based on the cross-fertil-ization of the knowledge and strengths of both companies. Unibail is primarily a devel-oper, in addition to an active property manager. However, Unibail is only active in France. On the other hand, Rodamco is a successful international investor: it has gath-ered a fantastic portfolio of large and unique shopping centres in the major European cities. Putting the two companies together - deploying an active management and devel-opment strategy on every asset should create outstanding value.

FH: For how long was the deal brewing?GP: Like any transaction that has a strong industrial sense, the idea of this combination has been “on and off” over the past decade. The pending evolution of the Dutch BI law and the support of a number of large share-holders make the transaction easier to implement today that it was in the past.

FH: How important was it for Unibail to diversify outside of the Paris/French market?GP: The idea for Unibail is not to diversify its holdings, but to create value. This combina-tion should create value, primarily on an

asset by asset basis. To achieve this objective, we will mobilise Unibail’s practice in large shopping centre management and develop-ment, which we started to built-up some 30 years ago. Moreover, the size of the com-bined entity will help us generate additional revenues. Our 95 shopping centres will be a very exciting development platform for any new or active retailer wishing to penetrate the European market. The flow of some 700 million visits per annum to our sites will be marketed to advertisers and any other players that want to get access to a large number of qualified customers.

FH: What synergies do you see and where will you need to make improvements in the Rodamco portfolio?GP: Our objective is to jointly build up one the best integrated operator-developer-investor companies in Europe, active in a selected number of underlying property markets, holding a major position in the large shopping centre segment. Historically, Rodamco has primarily focused on invest-ment, as opposed to management and development. As a result, we see many opportunities embedded into Rodamco current portfolio. In addition, there is many things to be carried out regarding Unibail’s assets. The new organization, relying on 5 strong local headquarters and one focused international headquarter, is designed to deliver this value creation.

FH: How do you see the future of your offices and Convention & Exhibition businesses?GP: The Paris office market is the most attrac-tive and robust office market in continental Europe and still has strong growth potential driven by the on-going market recovery and a high demand coupled with limited supply for prime office assets. Unibail’s outstanding development projects will foster further value creation, particularly in La Défense. The office business remains a major part of Unibail’s development, allowing the company to seize relevant opportunities on the European market.

Unibail will leverage its leadership in the French Convention & Exhibition market where it owns prime assets in Paris and La Défense. Furthermore, the merger project

Interview with Guillaume Poitrinal

Guillaume Poitrinal was appointed Chairman

& Chief Executive Officer in June 2006.

Aged 39 and father of three, Guillaume

Poitrinal joined Unibail in 1995 as a Project

Manager at the office of the Chief Executive. He

was promoted successively to Head of Corporate

Development and Planning, Chief Financial

Officer, Executive Vice President in charge of

Finance and the Office Division, and then

Managing Director in charge of all Divisions

and of Finance. Guillaume has been CEO since

April 2005.

Over the last ten years, in his different roles,

Guillaume Poitrinal has played a key part in

major external growth and development,

which are focal points of the Group’s history.

He has also been responsible for all operations

in the capital markets over this period.

Before joining Unibail, he spent three years in

mergers and acquisitions and corporate

finance departments at Morgan Stanley in

London and then in Paris. He is a graduate of

HEC Business School.

’ Contact Unibail

5 boulevard Malesherbes

75802 Paris Cedex 08

France

Tel: +33 53 437 437

www.unibail.com

Guillaume PoitrinalChairman & Chief

Executive Officer

By: Fraser Hughes

www.epra.com - july 2007 - epra news �

About Unibail/Rodamco EuropeCreating the pan-European commercial property leader

The no.1 commercial property company in Europe

• The no.1 portfolio of prime shopping centres with 10 out of the top 25 in Continental Europe

• A total combined property value of €21.7 billion and a presence in 14 European countries

A unique pan-European vision for value creation

• Combination of two industry success stories

• Implementing a single pan-European marketing and retail management strategy

• Sharing best practices and complementary skills in investment and retail management

• Leveraging Rodamco’s pan-European network and Unibail’s proven development skills

The no.1 commercial property developer in Europe

• At the forefront of retail innovation

• Acceleration of development opportunities across Europe

Further value creation opportunities in Paris Office market and Convention & Exhibition

Strong financial profile

Support from Rodamco and Unibail Management and Supervisory Boards

Support from Rodomco’s largest shareholder

features

with CCIP will create the European leader in the sector, with a growth potential from a unique portfolio of prime and complemen-tary assets, and open the door to new exten-sion opportunities. The merger should also accelerate the growth of the sector in France.

FH: Some analysts have expressed concerns that the enlarged group will be too big to outperform. How do you react to this?GP: Guess what....this is a question that we have fielded for the past 6 or 8 years regard-ing Unibail as a sole entity! In fact, there is only one way to make sure that a small or a large company outperforms: it must ensure that each underlying asset itself is outper-forming. If an asset is not positioned to deliver superior growth, the company should dispose of it. With this discipline, and a con-trolled number of assets, there is no reason why size should be an issue. Moreover, in the large shopping centres segment, size gives you a better access to new and existing retailers, to development and extension opportunities and to additional revenues. Size also allows you to develop advanced marketing skills and innovative ideas that can be deployed on the entire portfolio, sub-sequently resulting in a more attractive overall retail product.

FH: Name the three big challenges for the merged group in the short term.GP: The first challenge is obviously about organization. We expect to have the full new organization, including people and key pro-cesses, in place within three months. It does not appear to be too difficult given the quasi absence of overlap between the two busi-ness models.

The second challenge is to put all the assets “in motion”, with a real strategic value cre-ation vision for the next 5 years. To achieve this, many areas of expertise can be put in force, including leasing, marketing, refur-bishment and extensions.

The third challenge is to consolidate our development pipeline. We will start with 1.5 million m² of existing projects scheduled for delivery over the next 5 years. Beyond that, we believe that we can further rein-force our leadership in large shopping centre developments. There are still many opportunities in this segment, including the so-called “mature” western Europe markets.

FH: When you look at other property companies in the Europe, who do you most admire and why?GP: With the expansion of the REIT regimes throughout Europe, there is now a number of highly interesting investment opportuni-ties for investors - the investment choices are really there. My personal preference would go to focused, skilled, self managed compa-nies with a completely aligned interest between the investors and the executive team.

FH: Looking back, do you have any regrets?GP: No.

FH: What do you do in your spare time?GP: Nothing exceptional: family, music and sport. $

FH: On the whole, how do you feel the market has reacted to the Rodamco deal?GP: The share price has suffered somewhat since the announcement. One of the reasons for this is the significant market correction of the sector as a whole. Unibail, has under-performed the EPRA Europe Index by some 5 to 6%, which, I would argue is minimal for a change of this size.

FH: You are one of the youngest CEOs in the industry, with many years ahead of you. How do you expect the European landscape to develop over the next 10 years?GP: I am quite confident for those companies that have decided to focus on very strong market positions coupled with defined expertise. Value creation in the future will be primarily derived from operational skills. Finance will no longer be sufficient. Unibail-Rodamco is well positioned to fully benefit from this trend.

Interview with Guillaume Poitrinal

10 epra news - july 2007 - www.epra.com

features

The status of real property investment law in new Europe

Jacques de ServignyPartner

Jacques de Servigny is partner in charge of the

Budapest office of Gide Loyrette Nouel. He was

admitted to the Paris Bar in 1990. He has a DESS

(Master’s degree) in international tax law,

University of Paris XII (1989). He graduated from

HEC, Paris (1989). He has a DEA (Master’s degree)

in intellectual property (1987) and a Maitrise in

private law, University of Paris (1986).

’ Contact Office BudapestPhone: +36 1 411 7400

Fax: +36 1 411 7440

E-mail: [email protected]

Charles Scott CrudenSenior Associate

Charles Cruden is a senior associate in the Budapest

office of Gide Loyrette Nouel and a member of the

International Real Estate Practice Group. He has

practised real property investment law in Central

and Eastern Europe for over 5 years. He qualified

as a solicitor in 2001. He has a diploma in legal

practice, Exeter University (1999), a diploma in law,

Exeter University (1998), a M.A in history, Cambridge

University (2001) and a B.A. in history, Cambridge

University (1996).

’ Contact GLN Budapest Direct Phone: +36 1 411 7418

Phone: +36 1 411 7400

Fax: +36 1 411 7440

E-mail: [email protected]

“Perceived risk” is hindering the devel-opment of some New European prop-

erty markets. We have been advising inves-tors, banks and developers in New Europe since 1991. In general the legal frameworks of Bulgaria, Croatia, Czech Republic, Hungary, Montenegro, Romania, Russia, Serbia, Slovakia, Turkey and Ukraine permit institu-tional real estate investment. A short over-view of CEE countries highlighting specific juridical matters is produced in the following text.1

BulgariaThe Bulgarian commercial real estate market began in 2005. We are slightly concerned that the Bulgarian Law of Restitution is open to abuse. However, the restitution issue will eventually tail off due to a statute of limita-tion. An interesting twist is that a privatised state company may use the Law to claim the restitution of property that was nationalised from the company that was the predecessor of the state company that was privatised.

CroatiaThe implementation of the Croatian Construction Act 2003 will facilitate develop-ment in Croatia. The Lease and Sale of Business Premises Act 2004 and the Obligations Act 2005 have created a clear framework for commercial leases. The Financial Leasing Act 2006 creates the pos-sibility to financially lease real property.

Czech RepublicThe Czech Republic has a well established real property investment market. The early reorganization of the Czech cadastre in 1993 has facilitated the development of the market. The Building Act 2006, which entered into force on 1st January 2007, aims at improving the co-operation between the administra-tions involved in the authorisation process.

The Czech Commercial Leases Act 1990 created uncertainty as to whether the tenant had a pre-emption right if the landlord sold the property. In 2005 the legislator removed the ambiguity: a tenant does not have a stat-utory pre-emption right.

HungaryHungary is an often used jurisdiction in international real estate tax structures. Hungary benefits for an extensive network of double taxation treaties. The possibility of being able to obtain binding rulings from the tax authority greatly facilitates the cer-tainty of the Hungarian aspects of interna-tional tax structures.

MontenegroThe adoption by Montenegro of the EURO as its national currency has stabilized its economy. Like Bulgaria, Montenegro is tack-ling the past expropriation of real property without the payment of fair compensation. The Restitution Act 2004 enables former owners to seek restitution or reimburse-ment. The Act provides for a 10 year period in which to bring claims. We recommend a careful title due diligence to ascertain the risk of restitution claims.

PolandPoland has the most significant real property investment market in New Europe. In the coming years Russia, Ukraine and Turkey will be strong contenders. The perpetual usufruct is a form of title specific to the Polish legal system. It is commonly used in relation to real property held in full ownership by the State Treasury or local authorities. The per-petual usufruct is an ownership right for a limited duration in return for an annual fee. Local authorities are entitled to modify the annual fee each year. Sometimes adjust-ments lead to major disputes.

Capital is flooding into real estate investments. Private equity firms and pension funds are increasing their real estate allocations. Many sovereign funds are yet to make their first investments in New Europe. We are also seeing the first securitizations of New European properties. The weight of capital has changed investment profiles. The sheer weight of capital is having a positive effect in opening up new real estate markets and creating alternative asset classes across New Europe.

By: Jacques de Servigny and Charles Cruden

www.epra.com - july 2007 - epra news 11

features

RomaniaRomania has a dynamic real estate invest-ment market. Romanian law specifies that any deed pursuant to which a transfer of ownership takes place must be executed in notarised form under the pain of nullity. Deeds must be registered with the local bureau of the Office for Cadastral Works and Real Property Publicity in order to become binding against third parties.

RussiaIn some regions of Russia (including Moscow) the easiest way to obtain a development site is to lease it. However, the purchase of land is also possible in Moscow and is more advisable. As a rule a site is leased to an investor for 1 to 3 years (for the period of the design works and construction) and then a period such period is prolonged to 49 years after the building is constructed. We note that the owner of the building has an exclu-sive right to renew an agreement for the lease of a site underlying a building.

SerbiaIn Serbia real property investment is primar-ily focused on Belgrade. Unlike Bulgaria and Montenegro the law regulating full-scale restitution is yet to be enacted (possibly in 2007). Instead, persons have been granted usage rights over land owned prior to nation-alisation, while the State remains the actual

owner. The uncertainty of restitution is not preventing real estate investments; rather prudent investors are spending more on title due diligence to ascertain the risk.

SlovakiaSlovakia joined the EU on 1st May along with the Czech Republic, Hungary and Poland. However, the Slovak real property investment market did not receive as much investor atten-tion as the markets of the Czech Republic, Hungary or Poland. Slovakia responded quickly by abolishing transfer tax from 1st January 2005. Therefore, the sale of real prop-erty is not subject to transfer tax. This had a positive effect with investors and real estate investment in Slovakia has since quickened. Unfortunately, other countries in New Europe have not followed Slovakia’s lead and abol-ished transfer tax on real property.

TurkeyCo-ownership of real property is common in Turkey. It is also common for commercial property such as shopping malls to be co-owned in Turkey. Co-ownership reflects Turkish customs regarding the inheritance of land. In Istanbul the co-ownership of land has had an impact on the development of the real property investment market. If co-owners cannot agree on the use, sale or pos-session of the property, they may have to go to the court to resolve the matter in a parti-

tion action. As co-ownership is solved, Turkey will become an important real property investment market in the region.

UkraineSome investments in Ukraine have required innovative holding structures. The number of developers with track records in investment grade real estate is increasing. There were some exciting challenges as we implemented a western acquisition structure in the Ukraine. We used the laws of France and the laws of Ukraine to create a contractual framework that gave our client the comfort it needed to proceed with an acquisition.

Team approachA team approach is important to the success of any real estate transaction. Often commer-cial property investments require lawyers, accountants, tax advisers, valuers, environ-ment consultants and technical experts to perform due diligence. When different teams work together the investment process is facilitated. A due diligence that identifies the key risks and provides solutions will help any transaction to succeed. $

1 Jacques de Servigny and Charles Cruden are among the authors of “Real Property Investment Law” a set of 12 New European country reports published with REP Real Estate Publishers. Full reports available from Europe Real Estate (REP Real Estate Publishers): www.europe-re.com

The status of real property investment law in new Europe

The Kemlin, an old face in developing Moscow.

12 epra news - july 2007 - www.epra.com

features

Atasya Osmadi is a PhD student from Malaysia;

now at the University of Western Sydney doing her

research on REITs in Malaysia. She is also a lecturer

at Universiti Sains Malaysia, Penang.

Atasya OsmadiLecturer

Islamic REITs

LPTs have proven to be a very successful property investment vehicle in Australia, as well as REITs in the US. Recent years has also seen substantial growth in REITs around the world; particularly in Asia (Japan, Singapore, Hong Kong, South Korea) and in Europe (France, UK, Germany), with over US$600 billion in the global REIT markets. One unique development in this area is the establishment of the world’s first Islamic REITs in Malaysia, which include the principles of Sharia finance.

• Banks and Financial Institutions with riba (interest) base services.

In a situation where the property has tenants operating haram activities, the fund manager needs to perform some additional compliance assessments before acquiring the property for an Islamic REIT. They need to ensure that the total rental ratio from haram activities to the total turnover of the Islamic REIT in the current financial year should not exceed 20 percent. If it does exceed 20 percent, the SAC will advise against investing in such a property. The fund manager needs to be well-versed in differenti-ating halal and haram activities. In addition, the manager of an Islamic REIT has to ensure that all forms of investment, deposit and financing instruments comply with the Sharia principles. One of the key difference of Islamic financing system is they do not charge and pay interest.

The Islamic financial system is viewed to be advantageous to both sides of the capital provider and client as to embrace the concept of value-adding partnership, and profit and risk sharing. A few of the general Islamic finance laws that need to be followed includes the debt and cash money should not form 50% of the existing assets and debt to equity ratio of the company should not be more than 30:70%. Besides that, it has to use Islamic insurance to insure its property. However, conventional insurance is accept-able if Islamic insurance is unavailable. An Islamic REIT is also encouraged to partici-pate in forward sales or purchases of cur-rency with Islamic financial institutions. However, if the Islamic REIT deals with con-ventional financial institutions, it is permit-ted to participate in the conventional forward sales or purchases of currency. Figure 1 high-lights the differences between Islamic REITs and conventional REITs.

An Islamic REIT is also not permitted to own a property in which all the tenants operate only haram activities. It cannot be put into an Islamic REIT, even if the total rental complies with the 20% benchmark. In the case of accepting new tenants, tenants who operate fully haram activ-ities will not be allowed. By taking these factors into account, it is seen to be advantageous, as it encourages production of lawful commodi-ties and services and thus promotes ethical business and ethical investing.

By: Atasya Osmadi

Graeme Newell is professor of property investment

at the University of Western Sydney. He is actively

involved in property research and was strong links

to the property industry, both in Australia and inter-

nationally. Professor Newell is a member of the

EPRA Academic Circle and has previously prepared

research reports for EPRA on the diversification ben-

efits of European property stocks in portfolios.

The University of Western Sydney (UWS) has been

offering property degree programs for over 30

years. Over 500 students are currently doing prop-

erty programs at UWS. Many UWS property gradu-

ates are now leaders in the Australian property

industry, as well as internationally.

Graeme NewellProfessor of property

investment at the

University of Western

Sydney

With over US$600 billion in Islamic finance funds, Malaysia has a signifi-

cant role in Islamic finance; in particular, Malaysia is the world’s biggest issuer of Islamic debt, ahead of Bahrain, accounting for US$32 billion, or 60 per cent of all Islamic debt globally. Internationally, Malaysia dom-inates the Islamic bond market by account-ing for 84% of the total value of Islamic bonds issued globally. 85% of equity stocks traded on Bursa Malaysia are Sharia compli-ant. Although Islamic REITs are in the process of being established, Islamic funds have been well established, with a few of the major Islamic finance and property funds including Dubai Islamic Bank, Kuwait Finance House and Gulf Finance House.

Islamic REITs An Islamic REIT is a form of ethical invest-ment. Every single property transaction will be examined by the Sharia Advisory Council (SAC) of the Securities Commission (SC) to ensure full compliance with Islamic principles. The Islamic REIT guideline which compli-ments the existing Malaysian REIT guidelines allows Muslims to enjoy the benefits of con-ventional REITs, while being Sharia-compli-ant. This is seen to be more advantageous.

According to the guidelines, an Islamic REIT is permitted to own or purchase property in which the tenants operate mixed activities which are halal (permitted) and haram (not permitted), but with restrictions. Activities that are classified as haram as decided by the SAC are:

• Manufacturing or sale of haram products (i.e pork products, tobacco, alcoholic liquor, arms and ammunitions).

• Entertainment activities- cinema, pornog-raphy and any other obscene materials, hotels and resorts.

• Gambling.

• Conventional insurance companies.

• Stockbroking or share trading in non-Sharia compliant securities.

www.epra.com - july 2007 - epra news 13

features

Property Investment OpportunitiesIn the world of globalisation, there is a need for a global property investment strategy. These days, conventional foreign banks are adopting the concept of Islamic finance and offering a range of Islamic financial products (i.e. HSBC, Citibank, UBS). This indicates new expertise and new ideas locally and interna-tionally. This is an opportunity to join in the growth in this sector as Middle Eastern inves-tors are looking for safer places to invest their money which also offers superior return, as well as meeting the requirements of Sharia finance. Although the market for Islamic REITs is still small, there is plenty of room for further development. Support for this product is growing as Muslims become more concerned over the matter of a true Islamic regulation

and more investors are aware that they get better advantage with Islamic products. There is a promising global future for Islamic REITs as Dubai is also considering an Islamic REIT structure while Amanah Raya Bhd (the first Malaysian Government firm to form a REIT) plans to list its second real estate investment trust (REIT) in Malaysia and in Dubai. Implications for Property Investors in EuropeIn January 2007, REITs were introduced both in UK and Germany, adding to the existing form of REIT-like structures in Belgium, France and the Netherlands. Their entry to the REIT market is significant as it will increase liquidity and transparency to the international REIT market. Importantly, Islamic REITs are also considered to be a

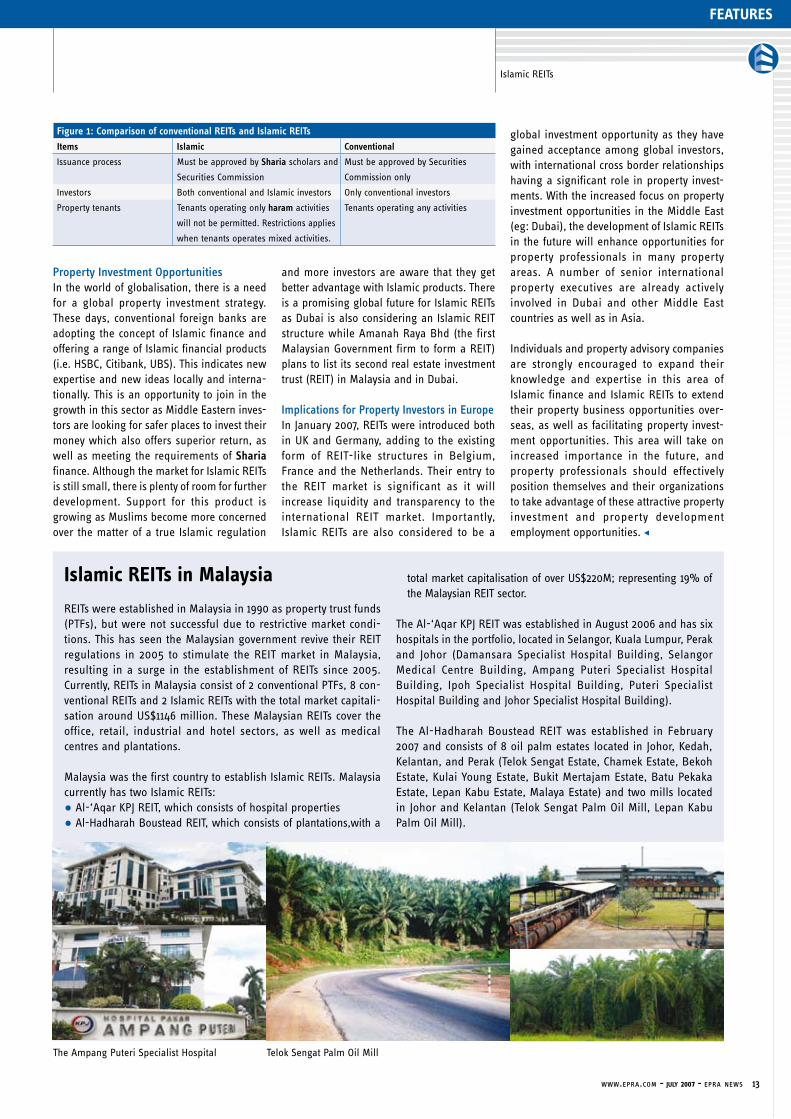

Figure 1: Comparison of conventional REITs and Islamic REITs

Items Islamic Conventional

Issuance process Must be approved by Sharia scholars and

Securities Commission

Must be approved by Securities

Commission only

Investors Both conventional and Islamic investors Only conventional investors

Property tenants Tenants operating only haram activities

will not be permitted. Restrictions applies

when tenants operates mixed activities.

Tenants operating any activities

Islamic REITs

Islamic REITs in Malaysia

REITs were established in Malaysia in 1990 as property trust funds (PTFs), but were not successful due to restrictive market condi-tions. This has seen the Malaysian government revive their REIT regulations in 2005 to stimulate the REIT market in Malaysia, resulting in a surge in the establishment of REITs since 2005. Currently, REITs in Malaysia consist of 2 conventional PTFs, 8 con-ventional REITs and 2 Islamic REITs with the total market capitali-sation around US$1146 million. These Malaysian REITs cover the office, retail, industrial and hotel sectors, as well as medical centres and plantations.

Malaysia was the first country to establish Islamic REITs. Malaysia currently has two Islamic REITs:

• Al-‘Aqar KPJ REIT, which consists of hospital properties

• Al-Hadharah Boustead REIT, which consists of plantations,with a

total market capitalisation of over US$220M; representing 19% of the Malaysian REIT sector.

The Al-‘Aqar KPJ REIT was established in August 2006 and has six hospitals in the portfolio, located in Selangor, Kuala Lumpur, Perak and Johor (Damansara Specialist Hospital Building, Selangor Medical Centre Building, Ampang Puteri Specialist Hospital Building, Ipoh Specialist Hospital Building, Puteri Specialist Hospital Building and Johor Specialist Hospital Building).

The Al-Hadharah Boustead REIT was established in February 2007 and consists of 8 oil palm estates located in Johor, Kedah, Kelantan, and Perak (Telok Sengat Estate, Chamek Estate, Bekoh Estate, Kulai Young Estate, Bukit Mertajam Estate, Batu Pekaka Estate, Lepan Kabu Estate, Malaya Estate) and two mills located in Johor and Kelantan (Telok Sengat Palm Oil Mill, Lepan Kabu Palm Oil Mill).

global investment opportunity as they have gained acceptance among global investors, with international cross border relationships having a significant role in property invest-ments. With the increased focus on property investment opportunities in the Middle East (eg: Dubai), the development of Islamic REITs in the future will enhance opportunities for property professionals in many property areas. A number of senior international property executives are already actively involved in Dubai and other Middle East countries as well as in Asia.

Individuals and property advisory companies are strongly encouraged to expand their knowledge and expertise in this area of Islamic finance and Islamic REITs to extend their property business opportunities over-seas, as well as facilitating property invest-ment opportunities. This area will take on increased importance in the future, and property professionals should effectively position themselves and their organizations to take advantage of these attractive property investment and property development employment opportunities. $

The Ampang Puteri Specialist Hospital Telok Sengat Palm Oil Mill

14 epra news - july 2007 - www.epra.com

features

The REIT Act does, however, come with a significant limitation with regard to

investment opportunities: the G-REIT may not or only to a limited extent invest in German residential property portfolios. This was a political compromise which makes little sense from an economic point of view. Analysis of the 15 largest stocks of the DIMAX in terms of market capitalisation shows that 9 of these companies hold considerable resi-dential property portfolios or focus entirely on residential real estate. So what alterna-tives exist for residential real estate investors if they cannot incorporate their portfolios into a G-REIT?

The existing stock corporations with large residential portfolios already demonstrate that there is a route to the stock market without incorporating German residential

Real Estate Investment Trusts (REITs) worldwide and their implementation

Source: Eurohypo RAC Research Source: Eurohypo RAC Research, Ellwanger & Geiger

DIMAX - top 15 in terms of market capitalisation

(as at 31.12.2006)

Market capitalisation in m EUR

% Gagfah 5,386

IVG Immobilien AG 3,775

% Patrizia Immobilien AG 1,069

% Deutsche Wohnen AG 1,030

Deutsche Euroshop AG 968

DIC Asset AG 874

% DIBAG Industriebau AG 612

% Colonia Real Estate AG 583

% GAG Gemeinnütz. AG f. Wohnungsbau Köln 562

% Vivacon AG 520

% GBWAG Bayerische Wohnungs-AG 458

% GBH Grundstücks- und Baugesellschaft AG 375

TAG Tegernsee AG 304

DGAG Deutsche Grundvermögen AG 289

Hamborner AG 263

% = AGs with large residential portfolios

By: Dr. Marcus Cieleback

Following often intense discussions between proponents and opposers of REITs, which almost led to a coalition row, the lower and upper houses of German government approved the law on the creation of German real estate stock corporations with listed shareholdings (REIT Act) at the end of March. For investors this has created a new possibility of indirect real estate investment, which fulfils international requirements in terms of fungibility and transparency and which has existed internationally for many years. This has taken the professionalisation of the German real estate market to a new level, which will be felt by all market participants. With their specific risk/return profile, G-REITs offer attractive entry and exit opportunities into and out of the real estate asset category, and not just for internationally active investors.

G-REITs without residential real estate: many opportunities abroad for investors

portfolios into the REIT Act. The high level of interest in easily tradable indirect real estate participations in German residential portfo-lios can be satisfied in other ways. Gagfah is an example of how a “quasi REIT” can be created with German residential property using a foreign holding. Other ways of satis-fying investor interest are listing on foreign stock exchanges via, for example, a SIIC (Société d’Investissements Immobiliers Cotées = French REIT, e.g. Fonciere des Regions) or on the alternative investment market in London (e.g. Puma Brandenburg). These vehicles represent an increasingly sig-nificant channel for the gathering pace of the secondary sales of residential portfolios.

The secondary sales show further ways of disposing of residential portfolios, for example, participation of professional, long-

term focussed asset managers or the creation of closed funds or special funds (e.g. LB Wohn-Invest, DCM GmbH & Co. Wohn-immobilien-Fonds 2 Berlin KG, ZBI 1 - 3). Tenant privatisation is also possible, but only sensible for sub-portfolios. Ultimately a mix of these strategies is possible or waiting until a residential G-REIT is introduced since incorporation of residential real estate makes sense in the long term from an economic point of view. The inverted route, which involves buying further portfolios to create a critical mass to enable a stock market flota-tion in Germany or abroad, is another pos-sible way. The latter currently appears to be the likely solution.

The analysis shows that German residen-tial portfolios can be traded in various ways, mostly in a highly liquid manner, even without the G-REIT. The current market capitalisation of the DIMAX is also dominated by companies with consider-able residential real estate portfolios. In the end, the exclusion of residential port-folios from the REIT Act has resulted in foreign holding structures or listing on foreign stock exchanges being significantly more attractive to investors. This can not be a long-term solution for the German capital market. $

www.epra.com - july 2007 - epra news 15

features

Since 2005 Dr. Marcus Cieleback is heading the

Research department in the Real Estate Appraisal &

Consulting division of Eurohypo AG. He studied eco-

nomics at the University in Freiburg and completed

his doctorate at the University of Bayreuth in 2001 in

the area of real estate finance. A year later he joined

MEAG, the asset management company Munich Re

Group. At MEAG, Dr. Cieleback was responsible for

the strategic real estate market analysis and com-

parative asset class studies. His focus at Eurohypo

includes the risk-based analysis and comparison of

global real estate markets and the development of

econometric models for forecasting the risks and

returns of the global markets. He is a frequent

speaker at international conferences and a pub-

lished author in various international magazines.

’ Contact EUROHYPO AG

Head of Research

Real Estate Appraisal & Consulting

Helfmann-Park 5, 65760 Eschborn

E-mail: [email protected]

Tel: +49 (0) 69 - 2548 - 21533

Fax: +49 (0) 69 - 2548 - 81533

Dr. Marcus CielebackHead of Research

G-REITs without residential real estate:

many opportunities abroad for investors

Trading of residential portfolios

1999

Source: AME Capital / Bloomberg

400000

350000

300000

250000

200000

150000

100000

50000

02000 2001 2002 2003 2004 2005 1st half 2006

Initial sales fo 800 units or more

Second sales of 800 units or more

Examples of investments in German residential portfolios by opportunistic investors and their exits

Notable primary portfolios /

companies

Company /

entity new

Investor Exit

Gagfah

Nileg

WOBA Dresden

Gagfah Fortress Listing via Luxembourg holding

Wohnungsbau Hoechst

and others

Deutsche Wohnen

AG

Deutsche Bank Listing

Viterra

Eisenbahnerwohnungen

RWE

BIG Heimbau AG

Deutsche

Annington

Terra Firma ? - speculation of a listing

WBG Jade and others WBG Jade and

others

Deutsche Bank/

Cerberus

Sale to Babcock & Brown / GPT

Group

ThyssenKrupp Immeo Wohnen Morgan Stanley/

Cerberus

Sale

(Fonciere des Regions) to Foncière

Développement Logement

Kieler Wohnungsbau

Gladbacher ABG

and others

Vitus Gruppe Blackstone Majority sale to a consortium

led by Deutsche Bank (including

Round Hill Capital and Morley Fund

Management)

DGAG DGAG B&L Immobilien/

HSH Nordbank

Majority sale to Pirelli Real Estate

GSW GSW Cerberus / Goldman

Sachs

?

BauBecon Holding BauBecon

Holding

Cerberus ?

GEHAG GEHAG Oaktree Capital

Management

?

Source: Eurohypo RAC Research

About EUROHYPO AGEurohypo AG is Europe’s leading spe-cialised bank for real estate and public sector financing. The bank is a member of the Commerzbank group.

Eurohypo has an excellent position in the global market: The Bank is a real estate finance providers with a pan-European presence, an established unit in the USA and the leader in European real estate investment banking. The bank also establishes its corporate finance business in asia.

16 epra news - july 2007 - www.epra.com

0

200

400

600

800

1000

Chart 1: Comparison of REIT and PropCo structures by market capitalization – May 2007

market focus

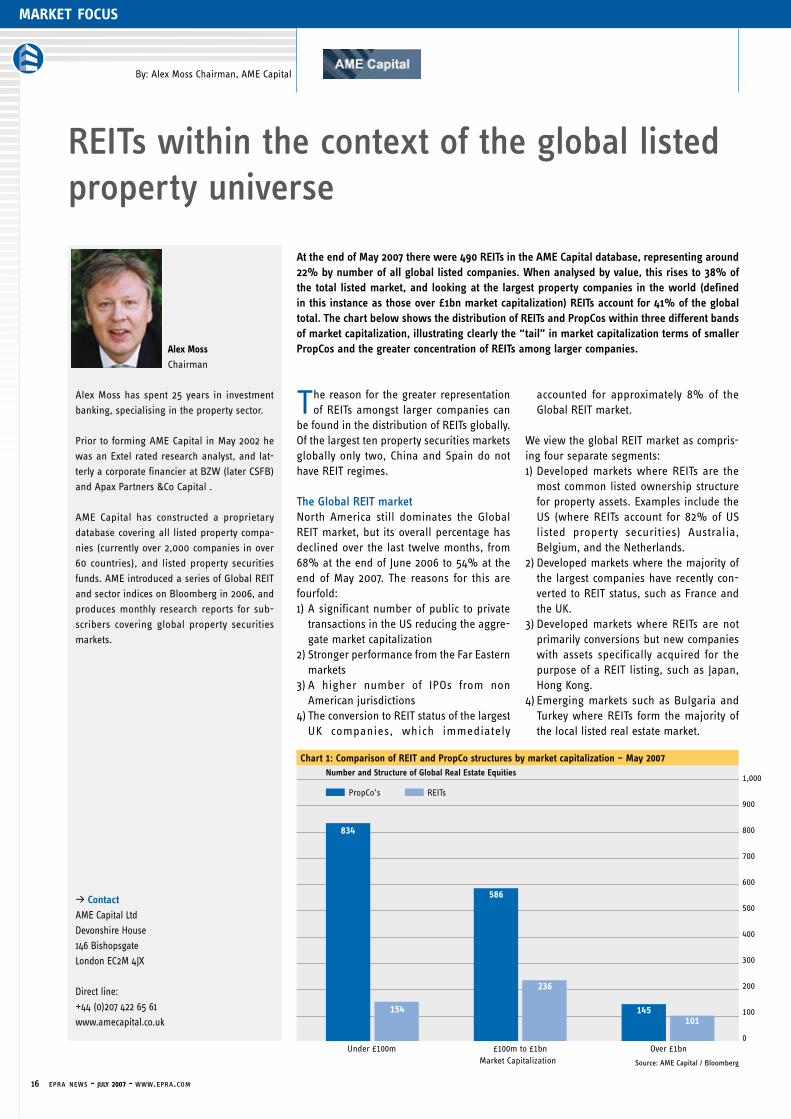

The reason for the greater representation of REITs amongst larger companies can

be found in the distribution of REITs globally. Of the largest ten property securities markets globally only two, China and Spain do not have REIT regimes.

The Global REIT marketNorth America still dominates the Global REIT market, but its overall percentage has declined over the last twelve months, from 68% at the end of June 2006 to 54% at the end of May 2007. The reasons for this are fourfold:1) A significant number of public to private

transactions in the US reducing the aggre-gate market capitalization

2) Stronger performance from the Far Eastern markets

3) A higher number of IPOs from non American jurisdictions

4) The conversion to REIT status of the largest UK companies, which immediately

accounted for approximately 8% of the Global REIT market.

We view the global REIT market as compris-ing four separate segments:1) Developed markets where REITs are the

most common listed ownership structure for property assets. Examples include the US (where REITs account for 82% of US listed property securities) Australia, Belgium, and the Netherlands.

2) Developed markets where the majority of the largest companies have recently con-verted to REIT status, such as France and the UK.

3) Developed markets where REITs are not primarily conversions but new companies with assets specifically acquired for the purpose of a REIT listing, such as Japan, Hong Kong.

4) Emerging markets such as Bulgaria and Turkey where REITs form the majority of the local listed real estate market.

At the end of May 2007 there were 490 REITs in the AME Capital database, representing around 22% by number of all global listed companies. When analysed by value, this rises to 38% of the total listed market, and looking at the largest property companies in the world (defined in this instance as those over £1bn market capitalization) REITs account for 41% of the global total. The chart below shows the distribution of REITs and PropCos within three different bands of market capitalization, illustrating clearly the “tail” in market capitalization terms of smaller PropCos and the greater concentration of REITs among larger companies.

Alex Moss has spent 25 years in investment

banking, specialising in the property sector.

Prior to forming AME Capital in May 2002 he

was an Extel rated research analyst, and lat-

terly a corporate financier at BZW (later CSFB)

and Apax Partners &Co Capital .

AME Capital has constructed a proprietary

database covering all listed property compa-

nies (currently over 2,000 companies in over

60 countries), and listed property securities

funds. AME introduced a series of Global REIT

and sector indices on Bloomberg in 2006, and

produces monthly research reports for sub-

scribers covering global property securities

markets.

’ Contact AME Capital Ltd

Devonshire House

146 Bishopsgate

London EC2M 4JX

Direct line:

+44 (0)207 422 65 61

www.amecapital.co.uk

Alex MossChairman

By: Alex Moss Chairman, AME Capital

REITs within the context of the global listed property universe

Number and Structure of Global Real Estate Equities

Under £100m

1,000

900

800

700

600

500

400

300

200

100

0£100m to £1bn Over £1bn

PropCo’s REITs

Market Capitalization

834

586

154

236

145101

Source: AME Capital / Bloomberg

www.epra.com - july 2007 - epra news 17

Chart 2: Largest property securities markets by country - May 2007

market focus

Future MarketsLooking at the structure of the existing listed property securities markets in the Germany and Italy it would appear rea-sonable to assume that their REIT markets will come to be dominated as much by IPOs as conversions of existing listed companies. Further field there are a number of countries where REIT-type legislation has been passed but there are no listed REITs, such as Brazil, Israel and Mexico. In addition a number of emerg-ing markets are considering passing REIT – like legislation such as China, India, and the Philippines. %

REITs within the context of the global listed

property universe

Table 1: Global REIT Markets ranked by size May 2007

Listing Country Number of Companies

Market cap < £100m

Market cap £100m to

£1bn

Market cap > £1bn Sector Mkt cap £

% of Global Listed Real Estate

Equity mkt

% of Global REIT mkt

% of Local Listed Real Estate mkt

AMERICAS 217 52 107 58 227,295,795,807 20.77% 54.32%

AMERICAS DEVELOPED 217 52 107 58 227,295,795,807 20.77% 54.32%

US 184 39 91 54 213,161,891,100 19.48% 50.94% 82.22%

Canada 33 13 16 4 14,133,904,707 1.29% 3.38% 38.24%

FAR EAST 100 34 55 11 44,131,085,321 4.03% 10.55%

FAR EAST DEVELOPED 63 5 47 11 41,670,503,920 3.81% 9.96%

Japan 41 4 30 7 27,901,152,940 2.55% 6.67% 23.87%

Singapore 16 1 12 3 9,438,870,530 0.86% 2.26% 19.85%

Hong Kong 6 0 5 1 4,330,480,451 0.40% 1.03% 2.91%

FAR EAST EMERGING 37 29 8 0 2,460,581,400 0.22% 0.59%

Taiwan 7 2 5 0 909,904,901 0.08% 0.22% 15.09%

Malaysia 13 12 1 0 702,189,598 0.06% 0.17% 8.26%

South Korea 10 9 1 0 520,103,542 0.05% 0.12% 93.49%

Thailand 7 6 1 0 328,383,360 0.03% 0.08% 8.14%

EUROPE 99 45 35 19 85,667,584,452 7.83% 20.47%

EUROPE DEVELOPED 67 16 32 19 84,194,854,083 7.69% 20.12%

UK 14 0 7 7 35,457,662,000 3.24% 8.47% 47.28%

France 30 10 13 7 31,058,560,977 2.84% 7.42% 69.14%

Netherlands 9 2 3 4 14,109,065,270 1.29% 3.37% 75.69%

Belgium 14 4 9 1 3,569,565,835 0.33% 0.85% 82.11%

EUROPE EMERGING 32 29 3 0 1,472,730,369 0.13% 0.35%

Turkey 11 9 2 0 940,551,316 0.09% 0.22% 99.18%

Greece 2 1 1 0 373,431,814 0.03% 0.09% 17.22%

Bulgaria 19 19 0 0 158,747,239 0.01% 0.04% 92.33%

OCEANIA 69 22 34 13 59,934,650,941 5.48% 14.32%

OCEANIA DEVELOPED 69 22 34 13 59,934,650,941 5.48% 14.32%

Australia 61 19 29 13 58,385,635,580 5.34% 13.95% 84.88%

New Zealand 8 3 5 0 1,549,015,361 0.14% 0.37% 91.23%

AFRICA 5 0 5 0 1,444,061,549 0.13% 0.35%

AFRICA EMERGING 5 0 5 0 1,444,061,549 0.13% 0.35%

South Africa 5 0 5 0 1,444,061,549 0.13% 0.35% 26.60%

GLOBAL REIT 490 153 236 101 418,473,178,069 38.24% 100.00%

GLOBAL DEVELOPED 416 95 220 101 413,095,804,751 37.75% 98.72%

GLOBAL EMERGING 74 58 16 0 5,377,373,318 0.49% 1.28%

300

250

200

150

100

50

0

US Hong Kong Japan UK Australia China Singapore France Canada Spain

25%

20%

15%

10%

5%

0%

Mar

ket

Capi

taliz

atio

n £b

n

% o

f Glo

bal M

arke

t

Source: AME Capital / Bloomberg

Source: AME Capital / Bloomberg

18 epra news - july 2007 - www.epra.com

0

10

20

30

40

50

60

70

Chart 3: Global REIT market performance 12 months to May 2007

70

60

50

40

30

20

10

0

-4 -3 -2 -1 0 1 2

Chart 4: Global REIT market performance 12 months to May 2007

-4 -3 -2 -1 0 1 2

market focus

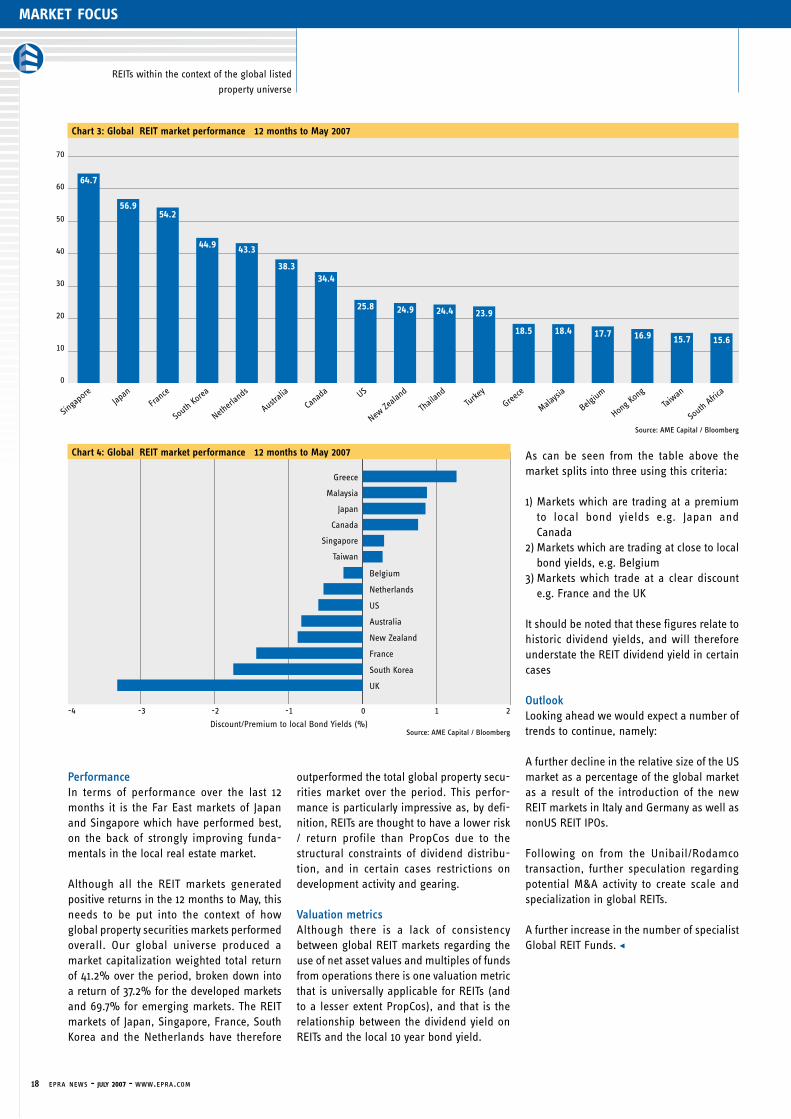

PerformanceIn terms of performance over the last 12 months it is the Far East markets of Japan and Singapore which have performed best, on the back of strongly improving funda-mentals in the local real estate market.

Although all the REIT markets generated positive returns in the 12 months to May, this needs to be put into the context of how global property securities markets performed overall. Our global universe produced a market capitalization weighted total return of 41.2% over the period, broken down into a return of 37.2% for the developed markets and 69.7% for emerging markets. The REIT markets of Japan, Singapore, France, South Korea and the Netherlands have therefore

outperformed the total global property secu-rities market over the period. This perfor-mance is particularly impressive as, by defi-nition, REITs are thought to have a lower risk / return profile than PropCos due to the structural constraints of dividend distribu-tion, and in certain cases restrictions on development activity and gearing.

Valuation metricsAlthough there is a lack of consistency between global REIT markets regarding the use of net asset values and multiples of funds from operations there is one valuation metric that is universally applicable for REITs (and to a lesser extent PropCos), and that is the relationship between the dividend yield on REITs and the local 10 year bond yield.

As can be seen from the table above the market splits into three using this criteria:

1) Markets which are trading at a premium to local bond yields e.g. Japan and Canada

2) Markets which are trading at close to local bond yields, e.g. Belgium

3) Markets which trade at a clear discount e.g. France and the UK

It should be noted that these figures relate to historic dividend yields, and will therefore understate the REIT dividend yield in certain cases

OutlookLooking ahead we would expect a number of trends to continue, namely:

A further decline in the relative size of the US market as a percentage of the global market as a result of the introduction of the new REIT markets in Italy and Germany as well as nonUS REIT IPOs.

Following on from the Unibail/Rodamco transaction, further speculation regarding potential M&A activity to create scale and specialization in global REITs.

A further increase in the number of specialist Global REIT Funds. $

Source: AME Capital / Bloomberg

Source: AME Capital / Bloomberg

Singa

poreJap

anFra

nce

South Ko

rea

Netherl

ands

Australi

a

Canad

a US

New Ze

aland

Thail

and

Turke

y

Greece

Malaysi

a

Belgium

Hong Ko

ng

Taiw

an

South Afric

a

64.7

56.954.2

44.9 43.3

38.334.4

25.8 24.9 24.4 23.9

18.5 18.4 17.7 16.9 15.7 15.6

Belgium

Netherlands

US

Australia

New Zealand

France

South Korea

UK

Greece

Malaysia

Japan

Canada

Singapore

Taiwan

REITs within the context of the global listed

property universe

Discount/Premium to local Bond Yields (%)

www.epra.com - july 2007 - epra news 19

market focus

“The project being managed jointly

by the U.S. Financial Accounting Standards Board (FASB) and the London-based Interna-t i ona l Account ing Standards Boards (IASB) has profound implica-tions for the listed real