ISEN 315 Spring 2011 Dr. Gary Gaukler. Demand Uncertainty How do we come up with our random variable...

20

ISEN 315 Spring 2011 Dr. Gary Gaukler

-

Upload

hilary-peters -

Category

Documents

-

view

216 -

download

1

Transcript of ISEN 315 Spring 2011 Dr. Gary Gaukler. Demand Uncertainty How do we come up with our random variable...

ISEN 315Spring 2011

Dr. Gary Gaukler

Demand Uncertainty

How do we come up with our random variable of demand?

Recall naïve method:

Demand Uncertainty

Demand Uncertainty and Forecasting

Using the standard deviation of forecast error:

Lot Size Reorder Point Systems

Assumptions– Inventory levels are reviewed continuously (the

level of on-hand inventory is known at all times)– Demand is random but the mean and variance of

demand are constant. (stationary demand)– There is a positive leadtime, τ. This is the time that

elapses from the time an order is placed until it arrives.

– The costs are: • Set-up each time an order is placed at $K per order• Unit order cost at $c for each unit ordered• Holding at $h per unit held per unit time ( i. e., per year)• Penalty cost of $p per unit of unsatisfied demand

The Inventory Control Policy

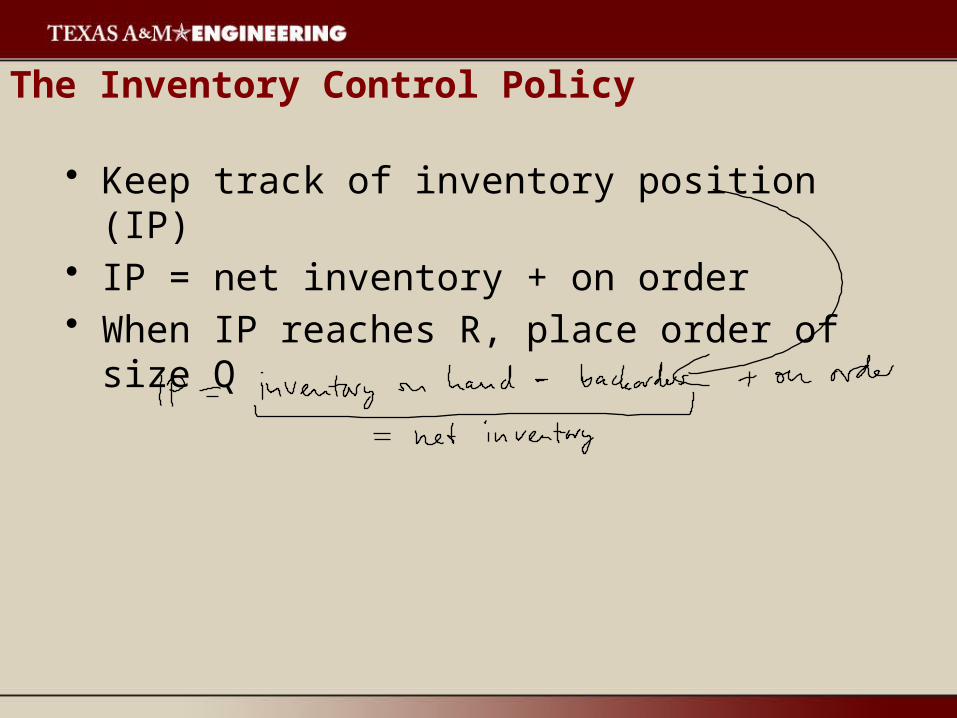

• Keep track of inventory position (IP)• IP = net inventory + on order• When IP reaches R, place order of size Q

Inventory Levels

Describing Demand

• The response time of the system in this case is the time that elapses from the point an order is placed until it arrives. – The uncertainty that must be protected against is

the uncertainty of demand during the lead time. • Assume that D represents the demand during

the lead time and has probability distribution F(t).

• Although the theory applies to any form of F(t), we assume that it follows a normal distribution for calculation purposes.

Decision Variables

• Basic EOQ model:– Single decision variable Q

• Q,R model:– Q and R interdependent decision variables.

Essentially, R is chosen to protect against uncertainty of demand during the lead time, and Q is chosen to balance the holding and set-up costs

The Cost Function

Approach:• Obtain an expression of expected cost per cycle, as a

function of Q,R

• Expected annual cost =

The Cost Function

• Holding cost:

• Setup cost:

The Cost Function

• Backorder cost:

• Procurement cost:

The Cost Function

• Expected cost per cycle:

• Expected annual cost:

Derivation of Optimal Parameters

Derivation of Optimal Parameters

Review

Optimal (Q,R):

Solution Procedure

• The optimal solution procedure requires iterating between the two equations for Q and R until convergence occurs (which is generally quite fast).

• A cost effective approximation is to set Q=EOQ and find R from the second equation.

• In this class, we will use the approximation.

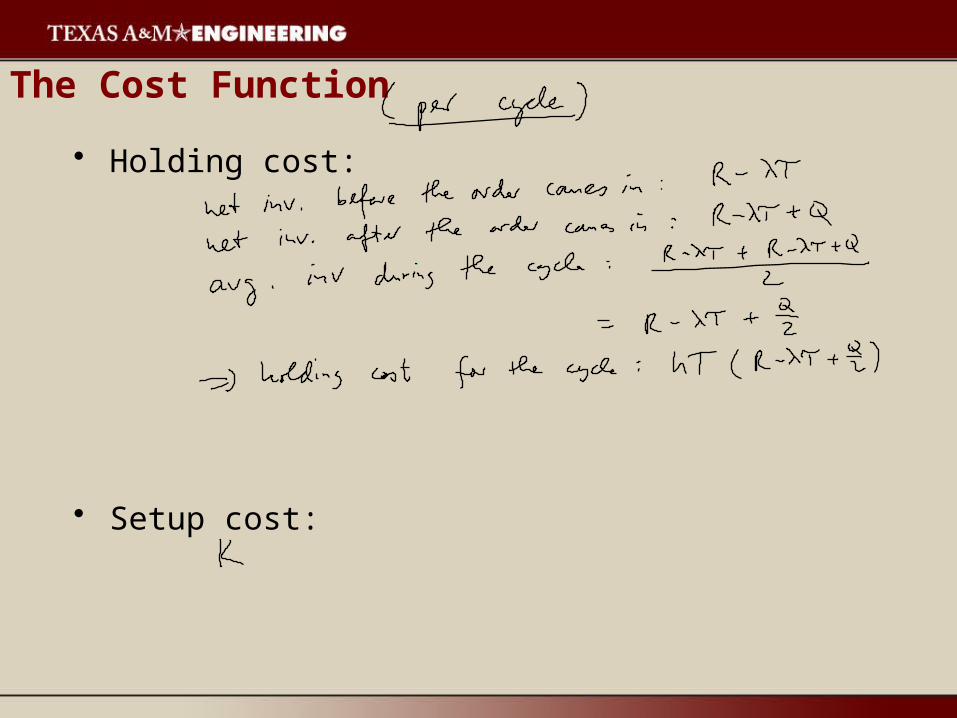

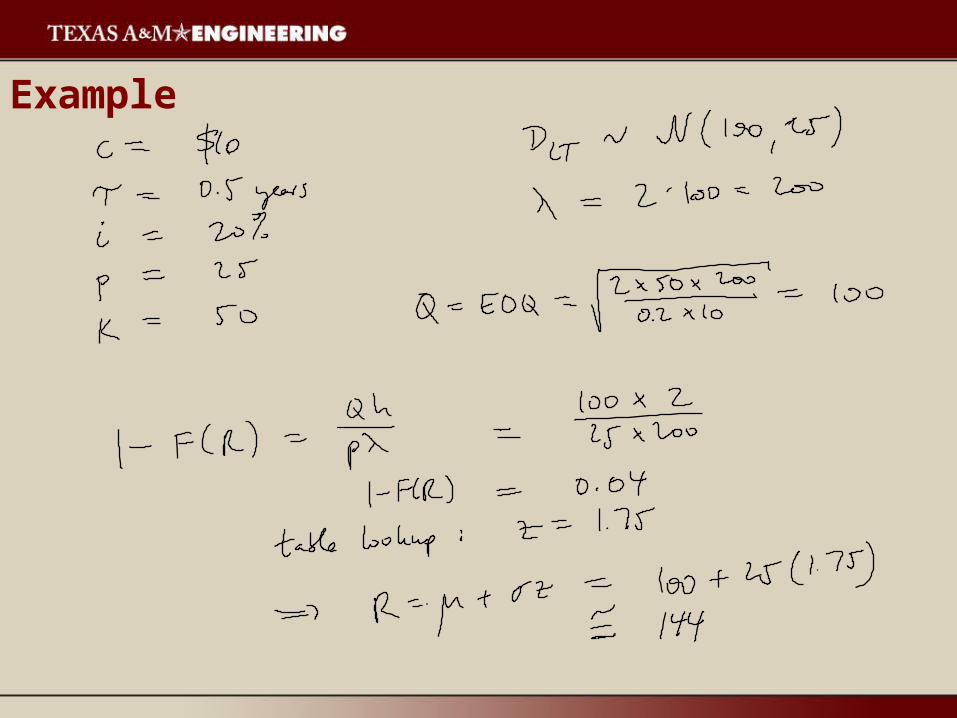

Example• Selling mustard jars• Jars cost $10, replenishment lead time 6 months• Holding cost 20% per year• Loss-of-goodwill cost $25 per jar• Order setup $50• Lead time demand N(100, 25)

Example

Example

![INTERNATIONAL ISEN SPIRITUAL EMERGENCE NETWORK · 2017. 5. 9. · ISEN SPIRITUAL EMERGENCE NETWORK . Title: SpiritualCrisisNetworkFLY-Folded [27381] Author: WensumPrint Created Date:](https://static.fdocuments.in/doc/165x107/60dc55f4ce3a8f4b09262226/international-isen-spiritual-emergence-2017-5-9-isen-spiritual-emergence-network.jpg)