Is there a Business Case for Microinsurance? · PDF fileIs there a Business Case for...

19

Is there a Business Case for Microinsurance? Synthesizing 3 years of learning Richard Koven Business Case Project Manager The MILK Project March 2014

Transcript of Is there a Business Case for Microinsurance? · PDF fileIs there a Business Case for...

Is there a Business Case for Microinsurance?

Synthesizing 3 years of learning Richard Koven Business Case Project Manager The MILK Project March 2014

“There is a business case when the investment of capital and other resources in microinsurance are justified over time such that the benefits, costs and risks balance out to create a commercial rationale for an insurer, distributor, and intermediary to enter and sustain a position in microinsurance”

Is it profitable?

India Health

Philippines Life

Colombia Life

Kenya Health

Global Intermediaries

…looking at 5 year financial results including covered lives, premium earned claims, distribution and administrative expenses and profits

As of 2012, these firms covered 48 million people with USD 276 Million earned premium

MILK studied 20 firms intensively

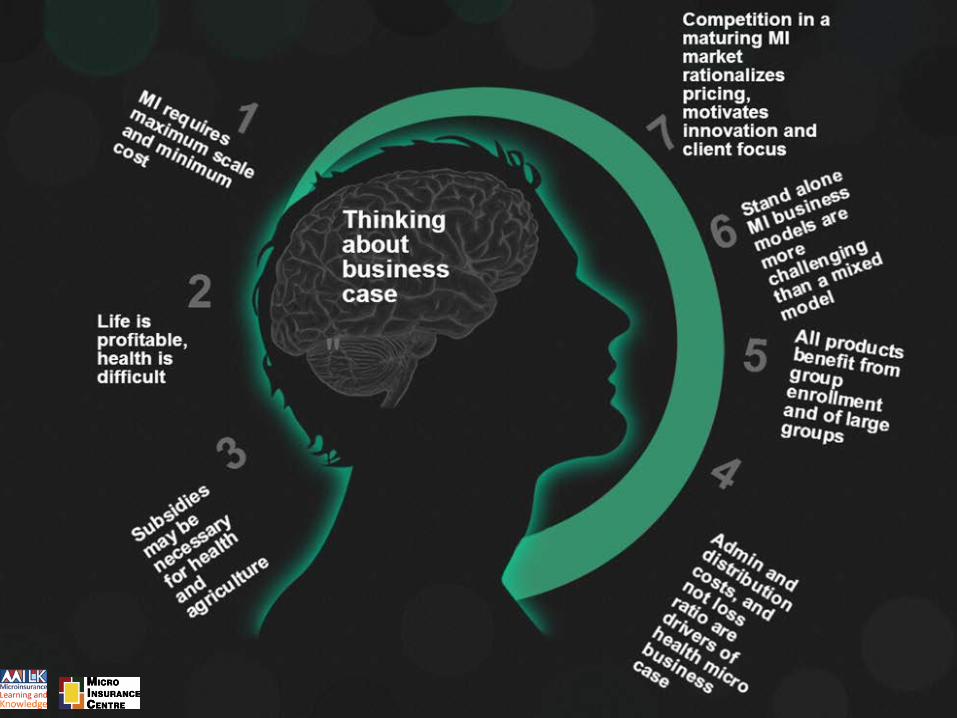

Competition

Subsidy Business

Model Product Type

Distribution Enrollment

Mode

Scale Program

Age

Eight Drivers of Microinsurance Business Case

…a big slice EU life policy EUR 1,150

…a small slice Colombia micro life EUR 17 Philippines micro life EUR 4

Scale

…a tiny slice Kenya micro health USD 6.18 India micro health USD 3.21

US health plan USD 4,250 …a big slice

Scale

margin

distribution & admin

claims Margin

-18%

Claims

57%

Admin

61%

Scale

The upside down Triangle

MILK Study Composite Private HMIs 2008-2012

microinsurance profitability relies on massive scale at minimal cost

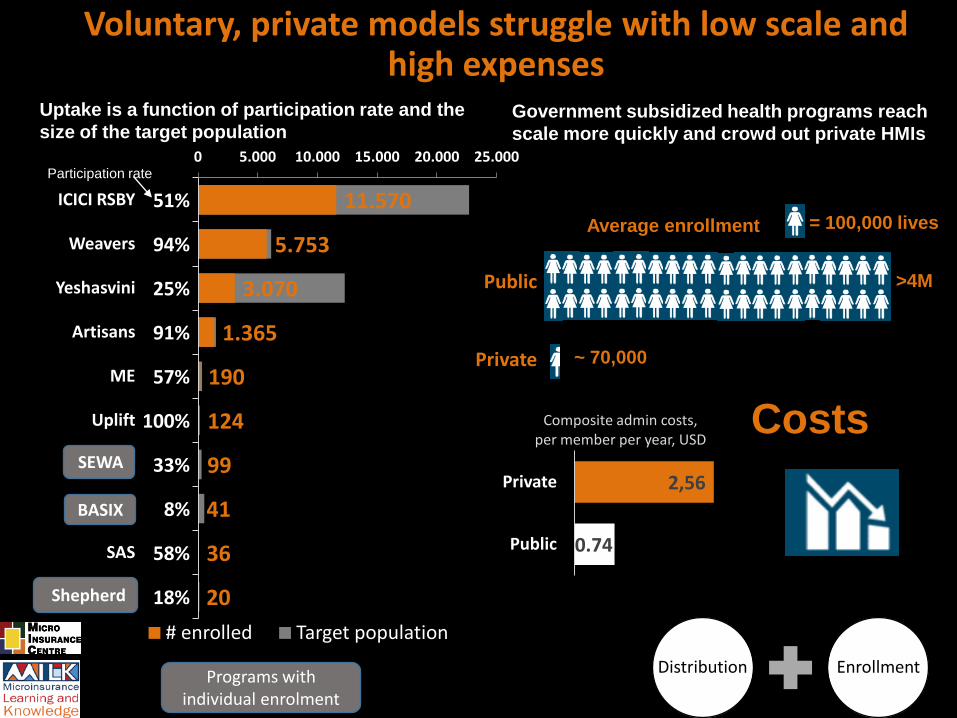

Voluntary, private models struggle with low scale and high expenses

Uptake is a function of participation rate and the size of the target population

Government subsidized health programs reach scale more quickly and crowd out private HMIs

Programs with individual enrolment

Public

Private

= 100,000 lives

>4M

~ 70,000

Average enrollment

0.74

2,56

Public

Private

Composite admin costs, per member per year, USD

Costs

20

36

41

99

124

190

1.365

3.070

5.753

11.570

18%

58%

8%

33%

100%

57%

91%

25%

94%

51%

Shepherd

SAS

BASIX

SEWA

Uplift

ME

Artisans

Yeshasvini

Weavers

ICICI RSBY

0 5.000 10.000 15.000 20.000 25.000

# enrolled Target population

SEWA

Shepherd

BASIX

Participation rate

Distribution Enrollment

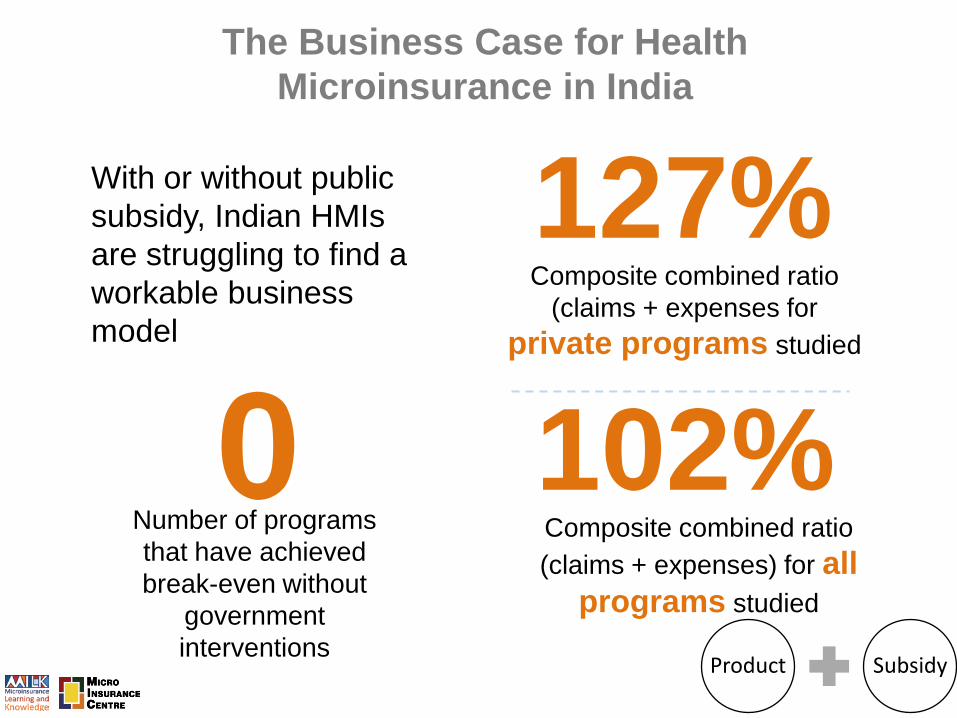

The Business Case for Health Microinsurance in India

With or without public subsidy, Indian HMIs are struggling to find a workable business model

0 Number of programs that have achieved break-even without

government interventions

102% Composite combined ratio (claims + expenses) for all

programs studied

127% Composite combined ratio

(claims + expenses for private programs studied

Product Subsidy

Private HMIs find it difficult to offer attractive products at affordable prices without

subsidy.

Expense ratio and not loss ratio In India is the primary driver of losses and lack of sustainability in private

programs

22%

78%

Public programs

63%

37%

Private programs

Admin Claims

Cost vs. Benefit per Member per Year (USD) Low scale leads to high

expense ratios

0,57

2,30

Premium charged to member

Benefit provided to member (claims)

Public

1,88

0.82

Private

Product Subsidy

Kenya HMI

Expense ratios are lower in Kenya…but premiums for HMIs are higher ; in Kenya subsidy is in the form of

absorbed loss ratio

0

1

2

3

4

5

6

7

8

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

USD

, per

mem

ber

per

year

Public HMIs

Premium Claims Admin

247% Claims

69% Claims

35% Exp.

45% Exp.

Private HMIs Kenya NHIF

Composite 282%

Kenya Composite 114%

2012 Premium, Claims, Expenses & Loss Ratios

NHIF

Private HMIs

3.1 Million

300,000

Covered Lives

Most programs are IP only and the opportunity to employ OP as a compliment to NHIFs IP is missed

Product Subsidy

100% Premiums

46% Claims

2

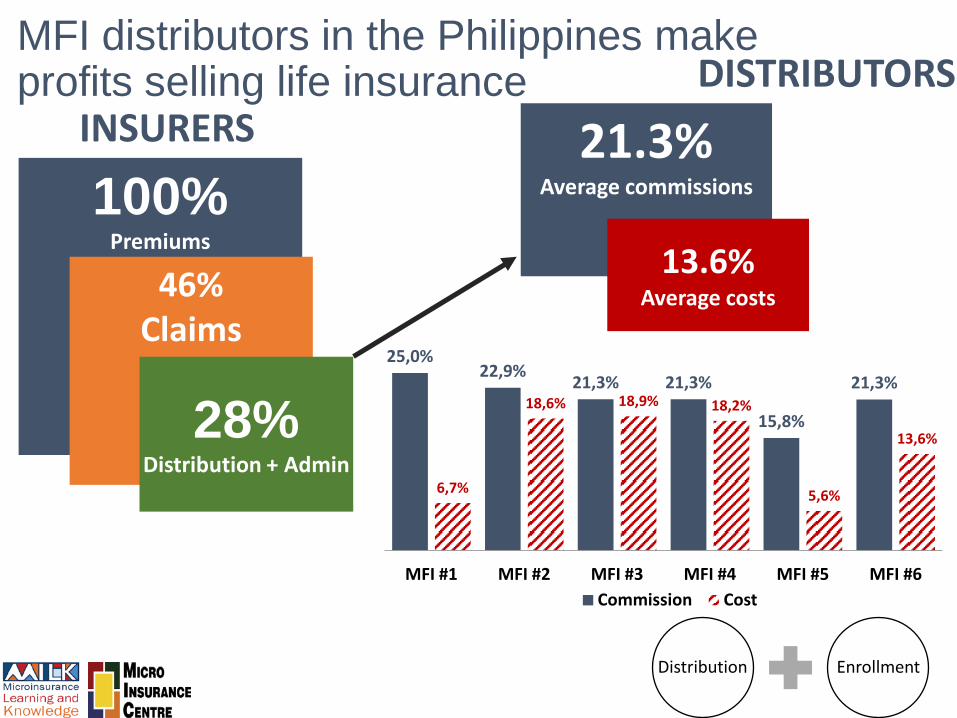

INSURERS DISTRIBUTORS

MFI distributors in the Philippines make profits selling life insurance

21.3% Average commissions

13.6% Average costs

25,0% 22,9%

21,3% 21,3%

15,8%

21,3%

6,7%

18,6% 18,9% 18,2%

5,6%

13,6%

MFI #1 MFI #2 MFI #3 MFI #4 MFI #5 MFI #6 Commission Cost

Distribution Enrollment

28%

Distribution + Admin

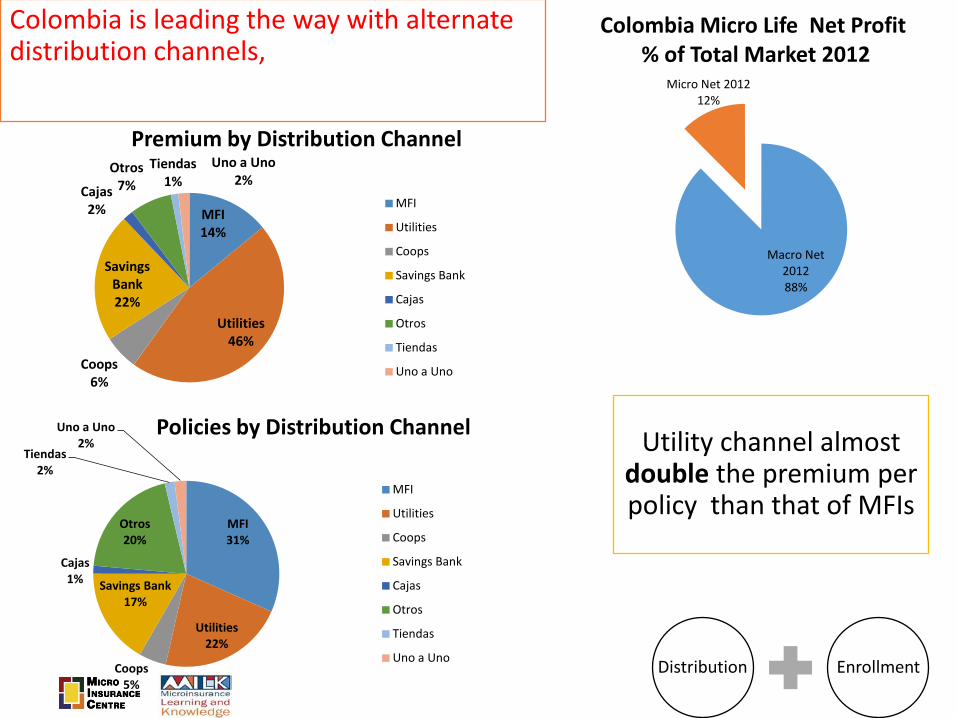

Colombia is leading the way with alternate distribution channels,

Utility channel almost double the premium per policy than that of MFIs

Distribution Enrollment

Macro Net 2012 88%

Micro Net 2012 12%

Colombia Micro Life Net Profit % of Total Market 2012

MFI 31%

Utilities 22%

Coops 5%

Savings Bank 17%

Cajas 1%

Otros 20%

Tiendas 2%

Uno a Uno 2%

Policies by Distribution Channel

MFI

Utilities

Coops

Savings Bank

Cajas

Otros

Tiendas

Uno a Uno

MFI 14%

Utilities 46%

Coops 6%

Savings Bank 22%

Cajas 2%

Otros 7%

Tiendas 1%

Uno a Uno 2%

Premium by Distribution Channel

MFI

Utilities

Coops

Savings Bank

Cajas

Otros

Tiendas

Uno a Uno

140.070

215.106

311.244

523.650

675.864

-168%

-30%

-33% -38%

-300%

-200%

-100%

0%

100%

200%

300%

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

2008 2009 2010 2011 2012

PlaNet Guarantee Covered lives and margin%, 2008-2012

Consolidation

Focus on consulting

484.208 587.692

2.000.347

3.467.008

4.202.597

-414%

-278% -177%

-73% -46%

-500%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400%

500%

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

4.000.000

4.500.000

2008 2009 2010 2011 2012

MicroEnsure Covered lives and margin %, 2008-2012

MNO initiative

Intermediaries are hugely leveraged to scale…they work off a small slice (commissions) of a small slice (micro premiums)

PG & ME have worked thru many strategies seeking scale and profits

Business Model

Health initiative

Intermediaries earn average revenue of just over USD 1.00 per year per life

Business Model

2008 2009 2010 2011 2012 All Years

ME & PG

Aon & Star

1,02 1,39 1,28 1,14 1,08 1,15 1,23 0,79

(5,40) (5,10)

(3,00)

(1,67) (1,49)

(2,34) (2,68)

(0,68)

Consolidated Revenues/Life & Expenses/Life (USD)

ME, PG & Star Micro (2008-2012); Aon Bolivia (2008-2011); AKAM (2008-2010)

Revenue/Life Expense/Life

… stand alones especially challenged. With expenses more than USD 2.50---both must support European based HQ

… when supported by commercial firms, costs are USD 0.68

In the Philippines... Competition rationalizes pricing, motivates innovation and client focus

43%

51% 52%

68% 74%

21%

29%

30%

38%

46%

22%

22% 21%

30% 28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2008 2009 2010 2011 2012

CARD, CLIMBS, PPLIC, TSPI, ME Claims & Expense Ratios 2008-2012

Combined Ratio Loss Ratio Expense Ratio

19.297.246

29.295.106

40.507.200

46.009.490

55.277.723

4.086.864

8.432.904 12.324.769

17.385.456

25.327.765

2008 2009 2010 2011 2012

Gross Premium Claims Expon. (Gross Premium)

Competition

Thank You!

Rick Koven [email protected]

Co-Authors India: Denis Garand, Taara Chandani

Kenya: Joseph Jamwaka, Anne Kamau, Donna Swiderek Philippines: John Wipf

Colombia: Xavier Martin Research Assistance

Emily Zimmerman, Katie Biese, Nick Winkleblack