Optimize Your Data Protection Investment for Bottom Line Results.

Upload

is-yatirimCategory

view

189download

2

PERFORMANCE & FINANCIAL RESULTS – 9M12 19 November 2012

Performance & Financial

Results – 9M12

1

About Us

Turkish Capital Markets

Our Performance

Financial Results

Expectations

2 About Us

İş Bank & İş Bank Group Companies

72%

Free Float 28%

Shareholder Structure Subsidiaries*

• Brokerage & Trading

• Investment Advisory

• Asset Management

• Corporate Finance

• Research

Business Lines

Credit Rating

‘AAA(tur)’ The first investment house that has a

credit rating in Turkey

Corporate Governance Rating

‘AAA (Trk)/Distinctive’ The only investment house

that has a corporate governance rating in Turkey

Awards

Euromoney

2011&2010 Best Investment Bank in Turkey

2009 Best M&A House in Turkey

2008&2007 Best Equity House in Turkey

EMEA Finance

2011 Best Investment Bank / Best Broker in Turkey

2010 Best Investment Bank in Turkey

FT/Mergermarket

2010 Financial Advisor of the Year in Turkey

IS Private Equity: (Share: 29.1%) ISGSY Turkey’s largest Private Equity company and listed since 2004; 22.87% IRR

(Internal Rate of Return) on USD basis from 9 exits

IS Investment Trust (Share: 26.5%) ISYAT

Turkey’s leading Investment Trust; listed since 1996, represents more than one third of the sector with its TL 275mn portfolio

IS Asset Management: (Share: 70.0%)

Turkey’s leading portfolio management company managing mainly IS Group funds, represents more than 20% of the fund market with its TL11.9bn AuM

Maxis Securities: (Share: 100.0%) London headquartered B Group capital markets licensed subsidiary

IS Investment Gulf: (Share: 100.0%)

Established in Dubai to focus on corporate finance, mainly M&A activities

Camiş Online: (Share: 99.8%)

Turkey’s one of the long-established brokerage houses

Efes NPL Asset Management: (Share: 74.0%) Aims to manage mainly banks’ NPLs

* Current structure

Performance & Financial

Results – 9M12

3

About Us

Turkish Capital Markets

Our Performance

Financial Results

Expectations

Turkish Capital Markets Trading Volume* 4

Equity Market (In TL Billion)

1.137

891

0

200

400

600

800

1000

1200

1400

2011/9 2012/9

670 592

0

100

200

300

400

500

600

700

800

900

2011/9 2012/9

* Market transactions by members

Source: ISE

Derivatives Market (In TL Billion)

Derivative market was negatively affected by the poor

volume of the equity market

Trading volume of the equity market decreased 22% with

respect to the same period of 2011 in parallel with the

global markets’ performance

Source: TurkDEX

Turkish Capital Markets Trading Volume* 5

Bills & Bonds Market (In TL Billion)

793

542

0

200

400

600

800

1000

2011/9 2012/9

4,6 4,2

0

1

2

3

4

5

6

2011/9 2012/9

(9)%

* Market transactions by members

Securities L/B Market (In TL Billion)

Lower interest rates caused 32% decrease at fixed income market when compared to same period of 2011; deposit banks’

bond IPOs also had a negative effect as they are mostly held till the maturity

Source: ISE Source: Settlement Bank

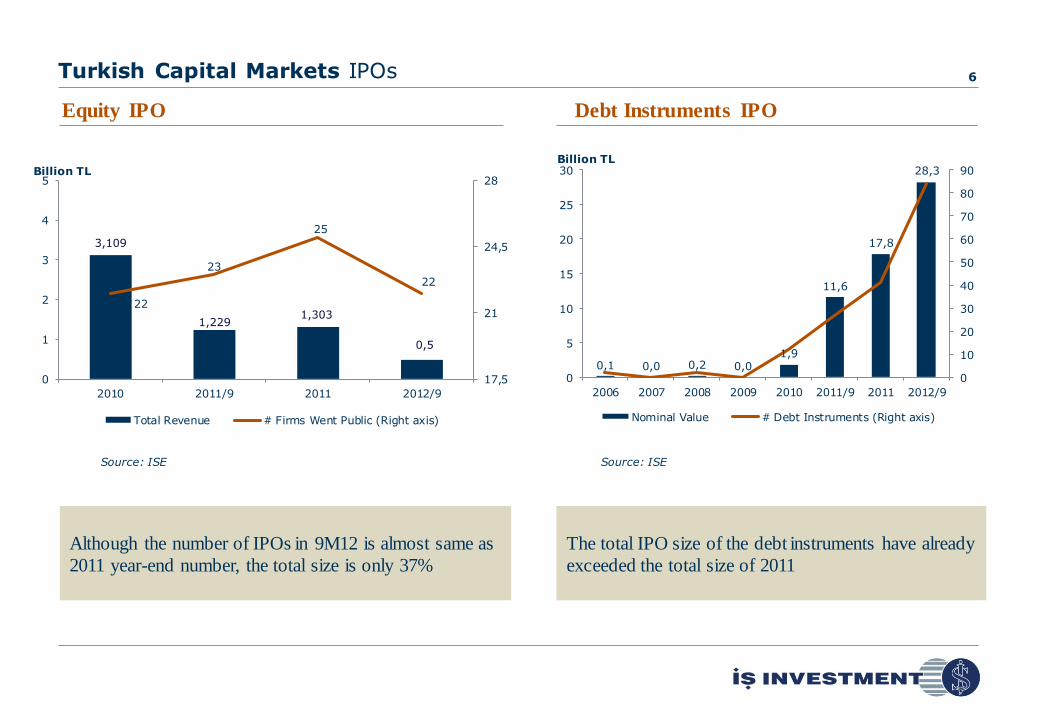

The total IPO size of the debt instruments have already

exceeded the total size of 2011

Turkish Capital Markets IPOs 6

Debt Instruments IPO Equity IPO

Source: ISE Source: ISE

Although the number of IPOs in 9M12 is almost same as

2011 year-end number, the total size is only 37%

0,1 0,0 0,2 0,0 1,9

11,6

17,8

28,3

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011/9 2011 2012/9

Billion TL

Nominal Value # Debt Instruments (Right axis)

22

23

25

22

17,5

21

24,5

28

0

1

2

3

4

5

2010 2011/9 2011 2012/9

Billion TL

Total Revenue # Firms Went Public (Right axis)

0,5

1,303 1,229

3,109

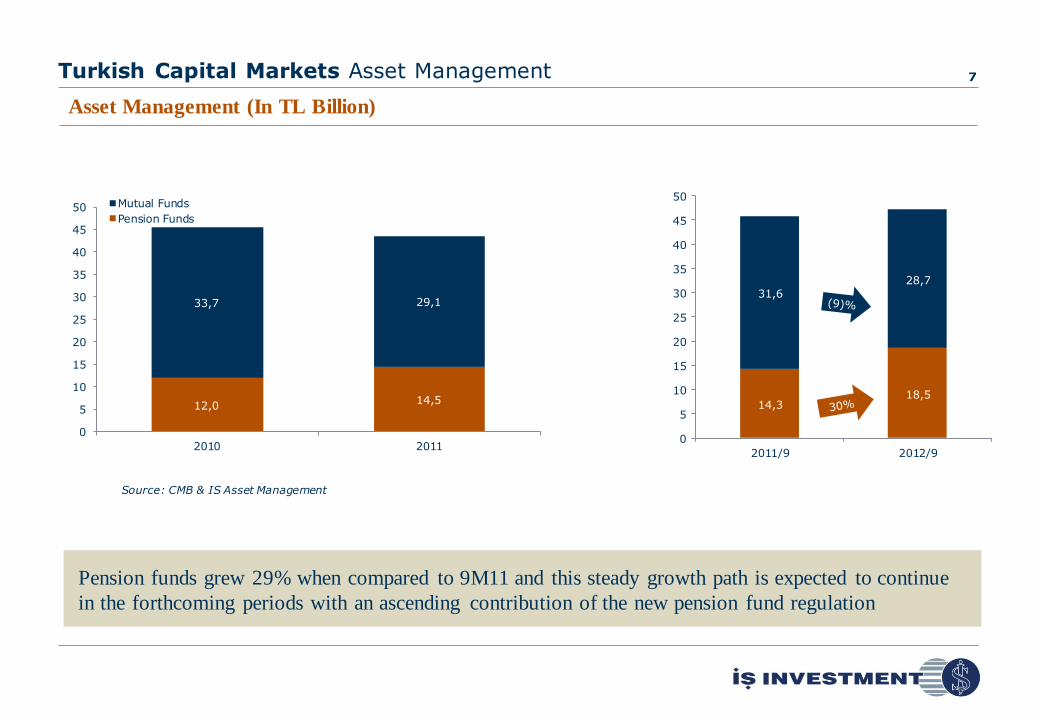

Turkish Capital Markets Asset Management 7

Source: CMB & IS Asset Management

Asset Management (In TL Billion)

14,3 18,5

31,6

28,7

0

5

10

15

20

25

30

35

40

45

50

2011/9 2012/9

Pension funds grew 29% when compared to 9M11 and this steady growth path is expected to continue

in the forthcoming periods with an ascending contribution of the new pension fund regulation

12,0 14,5

33,7 29,1

0

5

10

15

20

25

30

35

40

45

50

2010 2011

Mutual Funds

Pension Funds

Performance & Financial

Results – 9M12

8

About Us

Turkish Capital Markets

Our Performance

Financial Results

Expectations

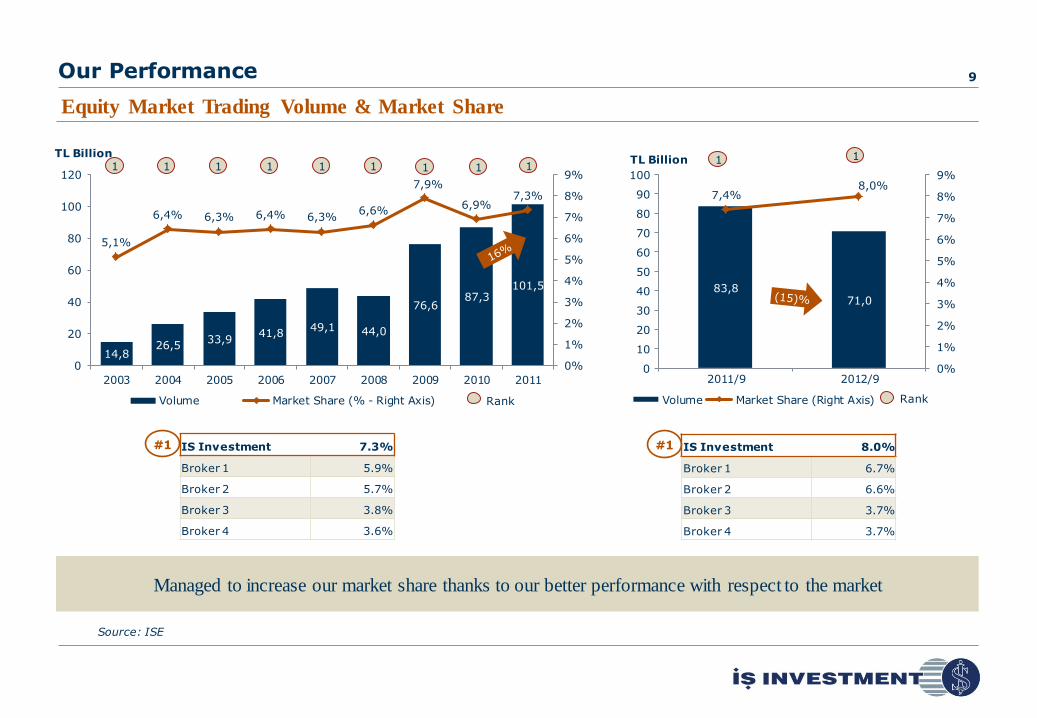

Our Performance 9

Source: ISE

IS Investment 8.0%

Broker 1 6.7%

Broker 2 6.6%

Broker 3 3.7%

Broker 4 3.7%

#1

83,8 71,0

7,4% 8,0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

10

20

30

40

50

60

70

80

90

100

2011/9 2012/9

TL Billion

Volume Market Share (Right Axis)

1 1

Rank

Managed to increase our market share thanks to our better performance with respect to the market

Equity Market Trading Volume & Market Share

14,8 26,5

33,9 41,8

49,1 44,0

76,6 87,3

101,5

5,1%

6,4% 6,3% 6,4% 6,3% 6,6%

7,9%

6,9% 7,3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008 2009 2010 2011

TL Billion

Volume Market Share (% - Right Axis) Rank

1 1 1 1 1 1 1 1 1

IS Investment 7.3%

Broker 1 5.9%

Broker 2 5.7%

Broker 3 3.8%

Broker 4 3.6%

#1

Our Performance 10

Source: TurkDEX

IS Investment 14.8%

Broker 1 9.2%

Broker 2 5.6%

Broker 3 5.4%

Broker 4 4.4%

#1

82,9 87,8

12,4%

14,8%

0%

3%

6%

9%

12%

15%

0

20

40

60

80

100

120

2011/9 2012/9

TL Billion

Volume Market Share (Right Axis) Rank

1 1

As the largest player of the market, we increased our trading volume by 6% with a market share of 14,8%

whereas the market contracted by 12%

Derivatives Market Trading Volume & Market Share

1,5 9,0

40,0

56,9

88,4

99,3

111,1

25,2% 25,3%

16,9%

13,7%

13,2% 11,5%

12,6%

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011

TL Billion

Volume Market Share (% - Right Axis) Rank

1 1 1 1 1 1 1

IS Investment 12.6%

Broker 1 6.3%

Broker 2 6.1%

Broker 3 4.2%

Broker 4 4.1%

#1

Our Performance 11

*Among Brokerage Houses

Source: ISE

11,2

8,6

10,7%

12,2%

0%

2%

4%

6%

8%

10%

12%

14%

0

2

4

6

8

10

12

2011/9 2012/9

TL Billion

Volume Market Share (Right Axis)

1 3

Rank

Our trading volume increased Q-o-Q in 2012 gradually but decreased Y-o-Y

Bills & Bonds Market Trading Volume and Market Share*

19,8

14,2 16,6 17,3

26,9

12,6

13,1% 11,8%

14,1% 12,9%

20,0%

10,2%

0%

5%

10%

15%

20%

25%

0

5

10

15

20

25

30

35

40

2006 2007 2008 2009 2010 2011

TL Billion

Volume Market Share (% - Right Axis) Rank

2 3 2 1 2 3

Our Performance 12

We completed 18 corporate bond IPOs with a market share of 25% in the first 9 months of the year

Corporate Bonds IPO - Size and Market Share

Source: ISE

1,5

7,9

12,7

21,3

0,4

3,7

5,1

7,0

0

5

10

15

20

25

30

2010 2011/9 2011 2012/9

TL Billion

IS Investment

Other

25%

32%

29%

25%

Our Performance 13

Source: ISE Settlement and Custody Bank Inc. & IS Investment

1.090

1.395

23,6%

33,0%

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

0

200

400

600

800

1000

1200

1400

1600

2011/9 2012/9

TL Million

Volume Market Share (Right axis)

We continue to be the most active institution in the market

Securities Lending/Borrowing Market

64 324

719

1.555 1.421 1.340

4,1%

11,5%

26,9%

37,9%

24,3% 24,9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2006 2007 2008 2009 2010 2011

TL Million

Volume Market Share (% - Right axis) Rank

8 2 1 1 1 1

Our Performance 14

164,1

140,0

0

20

40

60

80

100

120

140

160

2011/9 2012/9

TL Million

Source: IS Investment, TSPAKB

Our equity margin trading size, which decreased just because of the lower trading volume of equity market,

still represents 17% of the market

Equity Margin Trading

45 34 64 60

139

492

254

468

736

826

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011

TL Million

IS Investment

Total Market

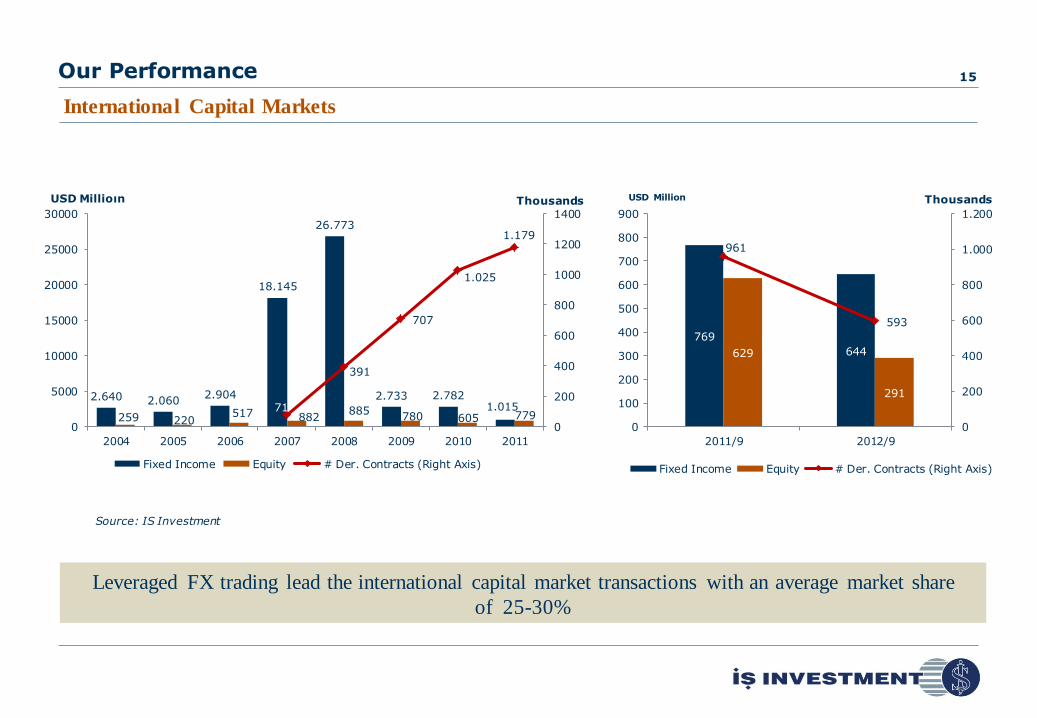

Our Performance 15

International Capital Markets

769

644 629

291

961

593

0

200

400

600

800

1.000

1.200

0

100

200

300

400

500

600

700

800

900

2011/9 2012/9

Thousands USD Million

Fixed Income Equity # Der. Contracts (Right Axis)

Source: IS Investment

2.640 2.060 2.904

18.145

26.773

2.733 2.782 1.015

259 220 517 882

885 780 605 779

71

391

707

1.025

1.179

0

200

400

600

800

1000

1200

1400

0

5000

10000

15000

20000

25000

30000

2004 2005 2006 2007 2008 2009 2010 2011

Thousands USD Millioın

Fixed Income Equity # Der. Contracts (Right Axis)

Leveraged FX trading lead the international capital market transactions with an average market share

of 25-30%

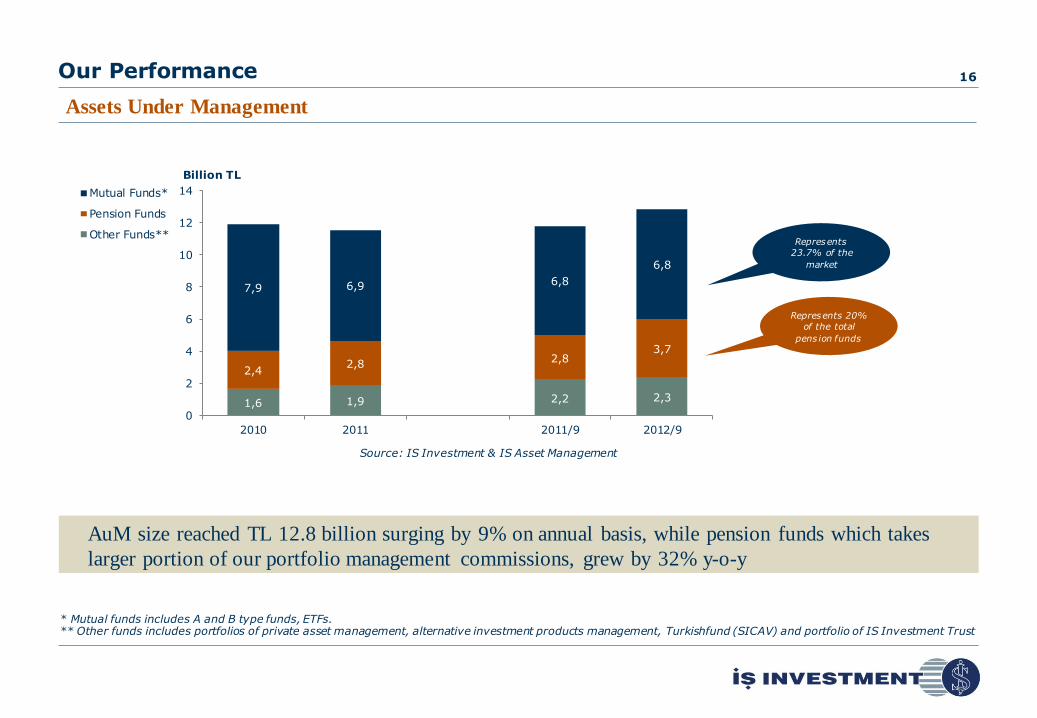

1,6 1,9 2,2 2,3

2,4 2,8

2,8 3,7

7,9 6,9 6,8

6,8

0

2

4

6

8

10

12

14

2010 2011 2011/9 2012/9

Billion TL

Mutual Funds*

Pension Funds

Other Funds**

Our Performance

AuM size reached TL 12.8 billion surging by 9% on annual basis, while pension funds which takes

larger portion of our portfolio management commissions, grew by 32% y-o-y

16

Source: IS Investment & IS Asset Management

Assets Under Management

* Mutual funds includes A and B type funds, ETFs. ** Other funds includes portfolios of private asset management, alternative investment products management, Turkishfund (SICAV) and portfolio of IS Investment Trust

Represents

23.7% of the

market

Represents 20%

of the total

pens ion funds

Performance & Financial

Results – 9M12

17

About Us

Turkish Capital Markets

Our Performance

Financial Results

Expectations

Financial Results Consolidated 18

IS Investment - Consolidated

TL (000) 9M11 9M12 YoY (%)

Total Assets 3,647,176 3,643,744 -

Shareholders' Equity 391,887 440,790 12

Net Profit 42,671 52,802 24

1.241

1.569

2.539 2.686

3.063

3.644

244 268 329 375 400 441

38,4 45,9 67,5 64,2 52,4 62,5*

19,4% 17,9%

22,5%

18,2%

13,5%

15,0%

0%

4%

8%

12%

16%

20%

24%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2007 2008 2009 2010 2011 2012/9

ROAE TL Million

Total Assets Shareholders' Equity Net Profit ROAE

Despite the poor trading volumes in the market especially in the 3rd quarter of 2012, we managed to increase our 9M12

net profit 24% with respect to the same period of 2011

* Income trailing (last 4 quarters’ net income)

24,5

38,4 36,8

45,9

55,4

67,5

46,0

64,2

42,7

52,4 52,8

?

0

10

20

30

40

50

60

70

TL Million

Financial Results Consolidated Net Profit 19

In the first 9 months of the year, we achieved to reach 2011 full-year net profit

2007 2008 2009 2010 2011 2012

9M

Full Year

Net Profit in TL 9M11 9M12 YoY (%)

IS Investment Only 36,837,252 44,041,171 20

IS Investment Trust (548,955) 9,540,834 NA

IS Private Equity 10,809,180 9,365,437 (13)

Other Subsidiaries

(Mainly IS Asset Management) 3,694,729 3,649,016 (1)

Elimination Adjustments* (8,121,012) (13,794,692) 70

Consolidated Net Profit 42,671,194 52,801,766 24

Financial Results Consolidation Effect 20

* Dividend and revenue elimination with subsidiaries

Consolidated Net Profit = [IS Investment Solo Net Profit + Contributions from Subsidiaries] – Elimination Adjustments

Contributions from Subsidiaries

Elimination Adjustments

IS Investment Solo Net Profit

Consolidated Net Profit

Interest and Trading Income

50%

Commission Income

50%

Interest and Trading Income

56% Commission

Income 44%

Financial Results Breakdown of Operating Revenues 21

Breakdown of Revenues

(TL 000) 9M11 9M12 YoY (%)

Interest and Trading Income* 84,000 121,541 45

Commission Revenues** 83,229 94,746 14

Total Operating Revenues 167,229 216,287 29

Operating Revenues – 9M11 Operating Revenues – 9M12

TL 167.2mn TL 216.3mn

Despite the volatile environment, our operating revenues kept increasing thanks to our

diversified revenue structure

* Considerable contribution from our subsidiaries to the interest & trading income ** Client based leveraged FX trading revenues, which is added to the commission revenues, can be seen under interest & derivative income at footnote 27.

Brokerage 72%

Corporate Finance

6%

Asset Management

21%

Other Commissions

1%

Brokerage 75% Corporate

Finance 6%

Asset Management

18%

Other Commissions

1%

Financial Results Breakdown of Commissions 22

Commission Revenues

(TL 000) 9M11 9M12 YoY (%)

Brokerage* 59,720 70,579 18

Corporate Finance 5,250 5,669 8

Asset Management 17,419 17,492 -

Other Commissions 840 1,007 20

Total 83,229 94,746 14

TL 83.2mn TL 94.7mn

Commission Income – 9M11 Commission Income – 9M12

Despite the unfavourable market conditions, brokerage revenues performed well owing to be active in

both domestic and international markets

* Leveraged FX trading revenues are added to the brokerage income

Other Exp. 2%

Marketing Exp. 17%

Adm. Exp. 81%

Other Exp. 2%

Marketing Exp. 15%

Adm. Exp. 83%

Financial Results Breakdown of Operating Expenses 23

Operating Expenses

(TL 000) 9M11 9M12 YoY (%)

Marketing, Sales and Distribution Expenses 16,588 22,552 36

General Administrative Expenses 88,487 108,936 23

Other Operating Expenses 1,764 2,255 28

Total 106,839 133,744 25

TL 106.8mn TL 133.7mn

Operating Expenses – 9M11 Operating Expenses – 9M12

Financial Results Price Performance 24

ISMEN Mcap

ISMEN increased 497% since the beginning of 2009

beating ISE 100 by 120%, while increased 40% year to

date

325

100

353

522

361

486

0

100

200

300

400

500

600

TL Millions

ISMEN Price Performance

ISMEN was selected to

• ISE Dividend Index (XTMTU)

• ISE Dividend 25 Index (XTM25)

• ISE Corporate Governance Index (XKURY)

0

100

200

300

400

500

600

700

ISMEN

ISE 100

Performance & Financial

Results – 9M12

25

About Us

Turkish Capital Markets

Our Performance

Financial Results

Expectations

Expectations 26

Corporate finance

Equity:

– We have mandates still watching a recovery in the stock markets both in domestic and global.

Corporate Bonds:

– After a significant performance in 2011, we have a number of mandates from various sectors with different size in 2012.

– IS Bank (TL 7.8bn), ING Bank (TL 450mn), IS Leasing (TL 100mn), IS Investment (TL 200mn), Alternatifbank (TL 150mn),

Creditwest (TL 50mn), Koç Fiat (TL 50mn), Boyner Holding (TL 100mn).

– We have new mandates.

Actively intermediating leveraged FX trading with a remarkable market share of 26-30%.

TradeMaster has been upgraded – investors are able to make leveraged FX trading via TM FX 24-hour/ 5 business day.

Prime brokerage service is still going up; new funds are in the pipeline.

New products: Single stock futures and options are going to be traded on the ISE.

New capital market law is expected to be approved by the Parliament till the end of the year.

IS Asset Management is estimated to benefit from new pension fund regulation which will be in force as of 2013.

Positive contribution from subsidiaries is expected to continue in the last quarter.

Investor Relations 27

Mr. Mert Erdoğmuş

Deputy CEO

Phone : +90 0212 350 24 12

Fax : +90 0212 350 20 01

E-mail : [email protected]

Mr. Ozan Altan

Head of IR

Phone : +90 0212 350 28 72

Fax : +90 0212 350 20 01

E-mail : [email protected]

The Investor Relations Department is responsible for the timely

communication of necessary, accurate, complete,

comprehensible and easily accessible information and

explanations, which are not considered to be trade secrets to its

shareholders and stakeholders.

http://www.isinvestment.com/wwa_ir_new.aspx

Mr. Alper Alkan

Associate

Phone : +90 0212 350 25 22

Fax : +90 0212 350 20 01

E-mail : [email protected]

Disclaimer

The information in this report is prepared by “IS YATIRIM MENKUL DEGERLER A.S.” (IS Investment) and it is not to be construed as

an offer or solicitation for the purchase or sale of any financial instrument or the provision of an offer to provide investment services.

Information, opinions and comments contained in this material are not under the scope of investment advisory services. Investment

advisory services are given according to the investment advisory contract, signed between the intermediary institutions, portfolio

management companies, investment banks and the clients. Opinions and comments contained in this report reflect the personal views of

the analysts who supplied them. The investments discussed or recommended in this report may involve significant risk, may be illiquid

and may not be suitable for all investors. Therefore, making decisions with respect to the information in this report cause inappropriate

results.

All prices, data and other information are not warranted as to completeness or accuracy and are subject to change without notice. Any

form of reproduction, dissemination, copying, disclosure, modification, distribution and/or publication of this report is strictly prohibited.

The information presented in this report has been obtained from sources believed to be reliable. IS Investment cannot be held responsible

for any errors or omissions or for results obtained from the use of such information.

28

IS Investment 29

HEAD

OFFICE

İş Kuleleri Kule-2 Kat:12

34330 4 . Levent İstanbul

T : 0212 350 20 00

F: 0212 350 20 01

ADANA

BRANCH

Ç ınarlı Mah. Turhan C emal Beriker Bulvarı

LEVENT

BRANCH

İş Kuleleri Kule-2 Kat:4

No:31 Kat:9 Seyhan A DANA, TURKEY 34330 4 . Levent İSTANBUL, TURKEY

T: +90 322 355 97 00 T : +90 212 350 29 00

F: +90 322 355 97 01 F: +90 212 350 29 01

AKARETLER

BRANCH

Süleyman Seba C ad. No:44 B1 Blok D:10

MASLAK

BRANCH

Büyükdere C ad. Nurol P laza No: 257

34357 A karetler İSTANBUL, TURKEY 34398 Maslak İSTANBUL, TURKEY

T : 0212 326 87 00 T : +90 212 367 85 00

F: 0212 326 86 87 F: +90 212 367 85 01

ANKARA

BRANCH

Tahran C ad. No: 3/8

YENİKOY

BRANCH

Köybaş ı Cad. İskele Çıkmazı No:6

06700 Kavaklıdere A NKARA, TURKEY 34464 Yeniköy İSTANBUL, TURKEY

T: +90 312 455 26 50 T : +90 212 363 01 00

F: +90 312 466 60 62 F: +90 212 363 01 01

BURSA

BRANCH

A tatürk Cad. Nalbantoğlu Mah. No:71/3

YEŞİLKÖY

BRANCH

Havalimanı Kavşağı EGS Business Park

16010 Osmangazi BURSA, TURKEY B3 Blok No:470

T : +90 266 294 80 00 34149 Yeşilköy İSTANBUL, TURKEY

F: +90 266 294 80 01 T : +90 212 463 20 00

F: +90 212 463 20 01

İZMİR

BRANCH

A kdeniz C ad. No:14 Birsel İş Merkezi D:501

SUADİYE

REP. OFFICE

Bağdat C ad. Kılıçoğlu Apt. No:451 Kat:1 D:4

35210 A lsancak İZMİR, TURKEY 34740 Suadiye İSTANBUL, TURKEY

T: +90 232 488 90 00 T : +90 216 665 46 00

F: +90 232 488 90 01 F: +90 216 665 46 01

KALAMIŞ

BRANCH

Fener Kalamış C ad. T ibaş Belvü Sitesi A 2 Blok D:3

ALMAATY

REP. OFFICE

2nd Floor , Block A 2 Samal Towers 97,

34726 Fenerbahçe İSTANBUL, TURKEY Zholdasbekov St, 050051 ALMAATA KAZAKİSTAN

T : +90 216 542 72 00 T : +7 727 334 05 08

F: +90 216 414 57 57 F: +7 727 334 05 09

SUBSIDIARY

MAXIS SECURITIES LTD

SUBSIDIARY

IS INVESTMENT GULF LIMITED

8 P rinces Street Dubai International Financial Centre

London EC 2R 8HL UNITED KINGDOM The Gate Village, Building 04, Lev el 1, Units 7 & 8

T : +44207 397 1431 PO Box 482079 Dubai, UAE

T: (+971) 555777726

PERFORMANCE & FINANCIAL RESULTS – 9M12 19 November 2012

![ANNUAL REPORT FISCAL YEAR 2017 ... › en › annual_report_fiscal_year_2017.pdf9 Chapter 1 Investment Results in Fiscal 2017 1 Investment Results [1] Rate of investment return / Amount](https://static.fdocuments.in/doc/165x107/5f284231338517462470380a/annual-report-fiscal-year-2017-a-en-a-annualreportfiscalyear2017pdf.jpg)