IRS Collection Division Representation All audio is streamed through your computer speakers. There...

26

IRS Collection Division Representation • All audio is streamed through your computer speakers. • There will be several attendance verification questions during the LIVE webinar that must be answered via the online quiz at the conclusion to qualify for CPE. • For the archived/recorded version of this webinar, there are also 3 review questions per hour and the link to the attendance verification quiz is a final exam on the topics covered during the presentation. • Please note: You will not hear any sound until the webinar begins. 1

-

Upload

tabitha-blair -

Category

Documents

-

view

216 -

download

0

Transcript of IRS Collection Division Representation All audio is streamed through your computer speakers. There...

IRS Collection Division Representation

• All audio is streamed through your computer speakers. • There will be several attendance verification questions during the

LIVE webinar that must be answered via the online quiz at the conclusion to qualify for CPE.

• For the archived/recorded version of this webinar, there are also 3 review questions per hour and the link to the attendance verification quiz is a final exam on the topics covered during the presentation.

• Please note: You will not hear any sound until the webinar begins.

1

2

IRS COLLECTION

Robert E. McKenzieArnstein & Lehr LLPChicago312.876.6927

Learning Objectives

• Determine the IRS notice procedure for delinquent taxes

• Identify the taxpayers rights to appeal collection due process notices from the IRS

• Determine the criteria for a streamlined installment agreement

• Identify the process for negotiating an installment agreement for larger tax liabilities

3

4

MCKENZIE’S PRIME DIRECTIVE

•GET THE FEE FIRST!!

Collection

5

2009 2010 2011 2012 2013

Levies 3,478,181 3,606,818 3,748,884 2,961,162 1,855,095

Liens 965,618 1,096,376 1,042,230 707,768 602,005

Seizures 581 605 776 733 547

6

IRS Notice Procedure

• First notice CP-14• CP-501• CP-503• CP-504• First 4 notice spaced 5 weeks apart• Letter 1058, CP-90

7

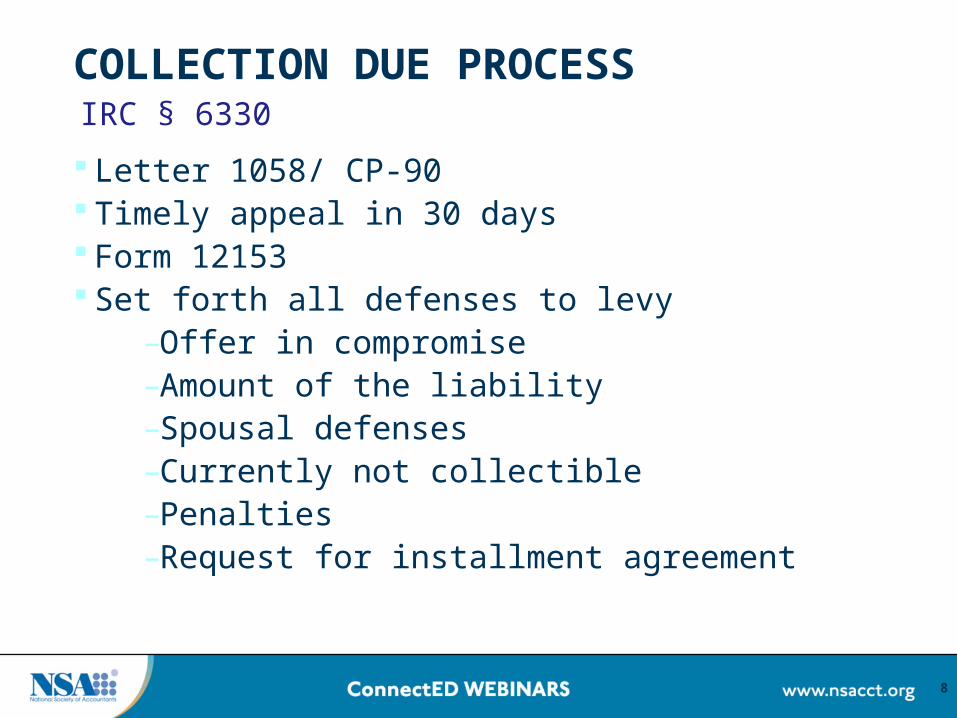

COLLECTION DUE PROCESS

Letter 1058/ CP-90 Timely appeal in 30 days Form 12153 Set forth all defenses to levy

–Offer in compromise–Amount of the liability–Spousal defenses–Currently not collectible–Penalties–Request for installment agreement

8

IRC § 6330

Extensions of Time to Pay

• Up to 120 days• Form 433 D is not to be used. ‑• The IRS will not file a lien.• No Notices of Intent to Levy, Notice of Hearing

(LT 11 or Letter 1058DO) or levies during granted extension periods, unless collection is in jeopardy or at risk.

9

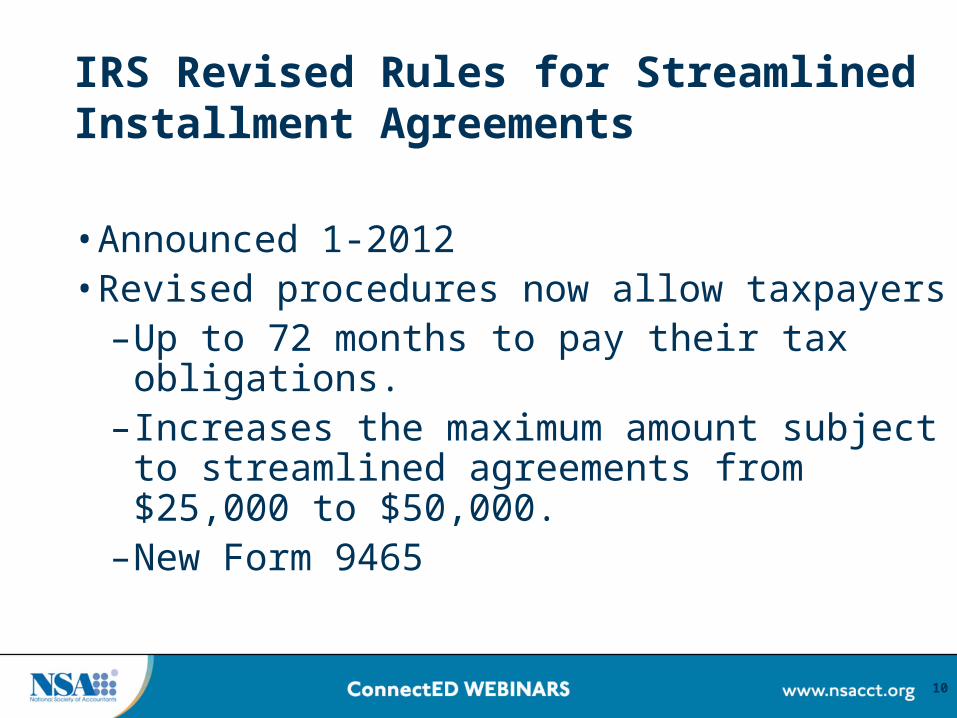

IRS Revised Rules for Streamlined Installment Agreements

• Announced 1-2012• Revised procedures now allow taxpayers

– Up to 72 months to pay their tax obligations. – Increases the maximum amount subject to

streamlined agreements from $25,000 to $50,000.– New Form 9465

10

OPA

• Online Payment Agreement• https://sa2.www4.irs.gov/irfof/lang/en/eiapoalogin.jsp

11

Review Questions for Self Study CPE:

Now’s the time to answer the review questions 1-3.Click here:http://www.proprofs.com/quiz-school/story.php?title=ODEyMTY2K6R4

*Once all questions are complete please submit and close quiz window.

12

New Collection Procedures

• Announced on 2-24-11• Increasing the dollar threshold when liens are generally issued,

resulting in fewer tax liens.• Easier for taxpayers to obtain lien withdrawals after paying a

tax bill.• Withdrawing liens in most cases where a taxpayer enters into

a Direct Debit Installment Agreement $25K or less.• Creating easier access to IAs for more struggling small

businesses now can do streamlined up to $25 K for 24 months• Expanding a streamlined Offer in Compromise program to

cover more taxpayers less than $25K and less than $100K income

13

Installment Agreements

•Greater than $50,000– Must submit form 433A for individuals– Must also submit form 433B for self employed– Subject to allowable expense standards– Must stay current

14

Allowable Expenses

• Allowable ExpensesA. National StandardsB. Medical expensesC. Regional Standards D. Local Standards E. Necessary for production of income or health

& welfare of the family

15

Food Clothing & Misc.

16

Out-of-Pocket Medical

17

Transportation

18

19

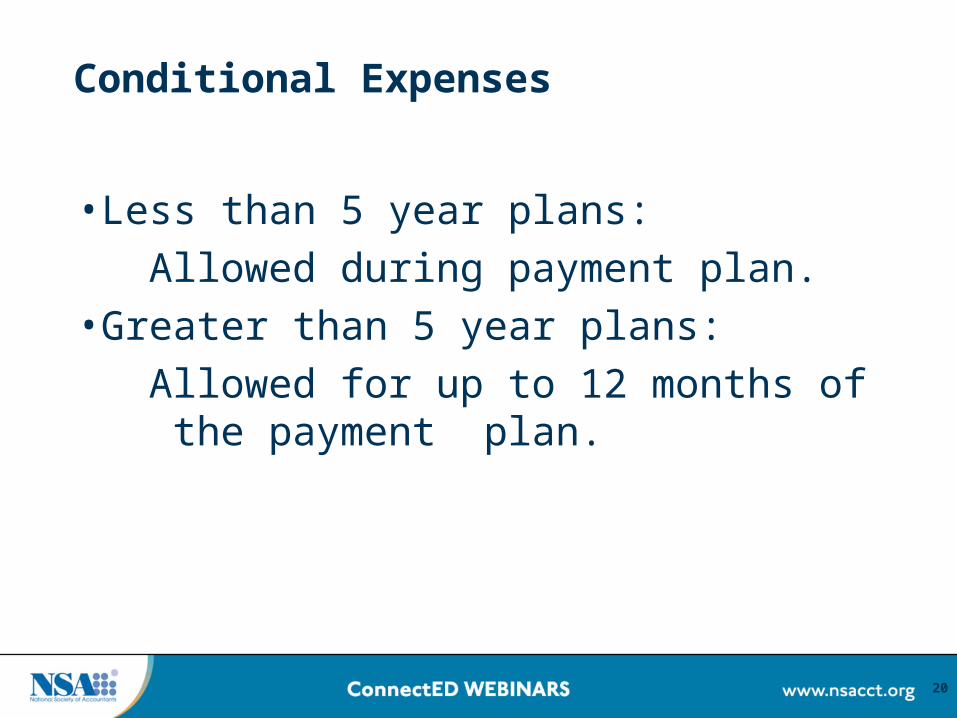

Conditional Expenses

•Less than 5 year plans:Allowed during payment plan.

•Greater than 5 year plans:Allowed for up to 12 months of the payment

plan.

20

Preparing Form 433A

• PGs. 35-40• Assets• Budget

21

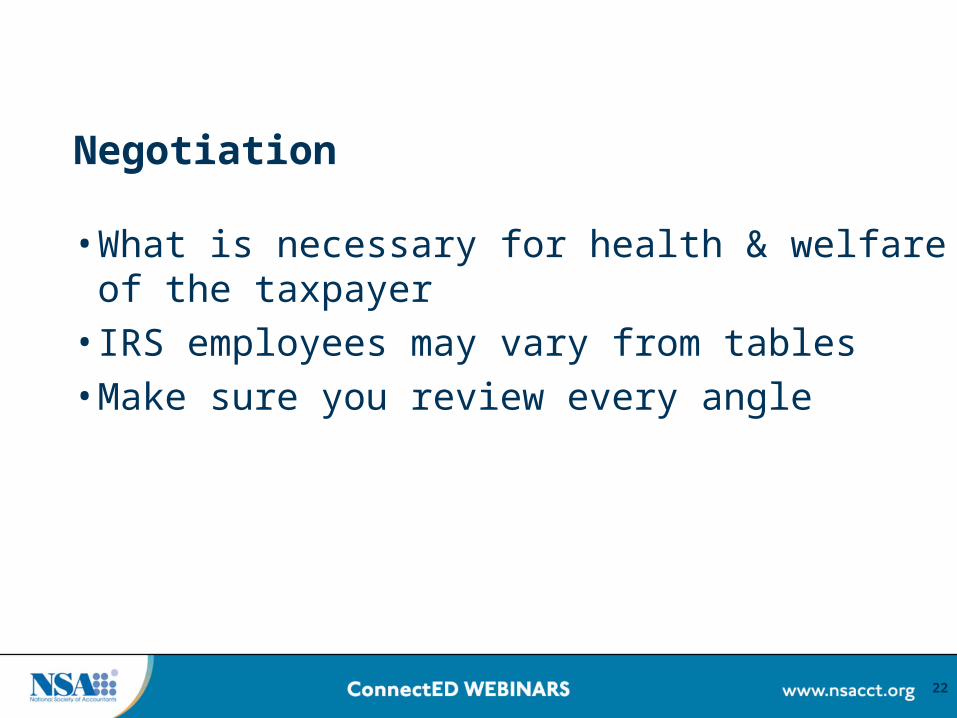

Negotiation

• What is necessary for health & welfare of the taxpayer• IRS employees may vary from tables• Make sure you review every angle

22

With Whom Do You Negotiate?

•Practitioner Priority Service 1-866-860-4259•ACS•(CSR's): at a Field Assistance Office •Revenue officers

23

Review Questions for Self Study CPE:

Now’s the time to answer the review questions 4-6.Click here:http://www.proprofs.com/quiz-school/story.php?title=ODEyMTY2K6R4

*Once all questions are complete please submit and close quiz window.

24

HAVE A LESS HAVE A LESS TAXING YEAR!!!!!TAXING YEAR!!!!!

Thank You!!Thank You!!

25

Thank you for participating in this webinar.Below is the link to the online survey and CPE quiz:

http://webinars.nsacct.org/postevent.php?id=13530Use your password for this webinar that is in your email confirmation.

You must complete this survey and the quiz or final exam (for the recorded version) to qualify to receive CPE credit.

National Society of Accountants1010 North Fairfax Street

Alexandria, VA 22314-1574Phone: (800) 966-6679

26