Ironshore Inc. Consolidated Financial Statements … 2015 GROUP PUBLIC... · We have audited the...

39

Ironshore Inc. Consolidated Financial Statements December 31, 2015

Transcript of Ironshore Inc. Consolidated Financial Statements … 2015 GROUP PUBLIC... · We have audited the...

Ironshore Inc.

Consolidated Financial Statements

December 31, 2015

A member firm of Ernst & Young Global Limited

Ernst & Young LLP 5 Times Square New York, NY 10036-6530

Tel: +1 212 773 3000 Fax: +1 212 773 6350 ey.com

1

Report of Independent Auditors

The Board of Directors and Shareholders Ironshore Inc.

We have audited the accompanying consolidated financial statements of Ironshore Inc., which comprise the consolidated balance sheets as of December 31, 2015 and 2014, and the related consolidated statements of operations and comprehensive income, changes in shareholders’ equity, and cash flows for the years then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

A member firm of Ernst & Young Global Limited

2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Ironshore Inc. as of December 31, 2015 and 2014, and the results of their operations and their cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

March 10, 2016

See accompanying notes to the consolidated financial statements.

3

Ironshore Inc.

Consolidated Balance Sheets

As of December 31, 2015 and 2014 (Expressed in thousands of U.S. dollars, except share data)

2015 2014

ASSETS

Fixed maturity securities, at fair value (amortized cost: 2015 - $4,451,226;

2014 - $4,031,724) $4,425,968 $4,044,195

Equity securities, at fair value (cost: 2015 - $202,014; 2014 - $209,265) 200,724 207,090

Short term investments, at cost which approximates fair value 3,979 40,877

Other investments 90,866 61,089

Total investments 4,721,537 4,353,251

Cash and cash equivalents 381,604 328,797

Accrued investment income 21,057 19,351

Premiums receivable 494,834 514,035

Reinsurance recoverable on unpaid losses 776,787 693,298

Reinsurance recoverable on paid losses 59,034 66,397

Deferred acquisition costs 106,939 125,098

Prepaid reinsurance premiums 372,612 305,647

Goodwill and other intangible assets 76,226 79,354

Deferred tax asset 37,228 12,191

Receivable for securities sold 9,179 17,904

Other assets 193,036 184,592

Total assets $7,250,073 $6,699,915

LIABILITIES

Reserve for losses and loss adjustment expenses $3,197,541 $2,838,158

Unearned premiums 1,304,591 1,310,908

Insurance and reinsurance balances payable 228,243 240,594

Payable for securities purchased 21,761 11,388

Other liabilities 183,383 111,477

Debt obligations 347,992 347,629

Total liabilities 5,283,511 4,860,154

COMMITMENTS AND CONTINGENCIES

SHAREHOLDERS' EQUITY

Common shares, 400,000,000 authorized, par value $0.01 per share

(2015: 140,657,340; 2014: 136,625,637), shares issued and outstanding 1,407 1,366

Additional paid-in capital 1,431,794 1,364,762

Accumulated other comprehensive loss (6,149) (8,074)

Retained earnings 539,510 481,707

TOTAL SHAREHOLDERS' EQUITY 1,966,562 1,839,761

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $7,250,073 $6,699,915

See accompanying notes to the consolidated financial statements.

4

Ironshore Inc.

Consolidated Statements of Operations and Comprehensive Income

For the years ended December 31, 2015 and 2014 (Expressed in thousands of U.S. dollars, except share data)

2015 2014

REVENUES

Gross premiums written $2,163,852 $2,210,554

Reinsurance premiums ceded (684,028) (591,374)

Net premiums written 1,479,824 1,619,180

Change in unearned premiums 63,427 (92,184)

Net premiums earned 1,543,251 1,526,996

Net investment income 113,300 97,043

Net realized and unrealized gains (losses) on investments (48,351) 28,039

Net foreign exchange losses (11,054) (5,283)

Other income 50,413 33,566

Total revenues 1,647,559 1,680,361

EXPENSES

Losses and loss adjustment expenses 1,010,218 1,077,274

Acquisition expenses 210,053 214,708

General and administrative expenses 322,728 279,101

Non-recurring transaction expenses 39,529 -

Interest expense 22,169 21,906

Total expenses 1,604,697 1,592,989

Income before tax benefit (expense) 42,862 87,372

Income tax benefit (expense) 14,941 (2,906)

Net income 57,803 84,466

Net loss attributable to non-controlling interest - (11)

Net income attributable to Ironshore Inc. $57,803 $84,477

COMPREHENSIVE INCOME

Net income $57,803 $84,466

Other comprehensive income, before tax

Equity gains from foreign currency translation 3,851 6,909

Losses on intra-entity foreign currency transactions (1,926) (4,662)

Other comprehensive income, before tax 1,925 2,247

Income tax on other comprehensive income - -

Other comprehensive income, net of tax 1,925 2,247

Comprehensive income 59,728 86,713

Comprehensive loss attributable to non-controlling interests - (11)

Comprehensive income attributable to Ironshore Inc. $59,728 $86,724

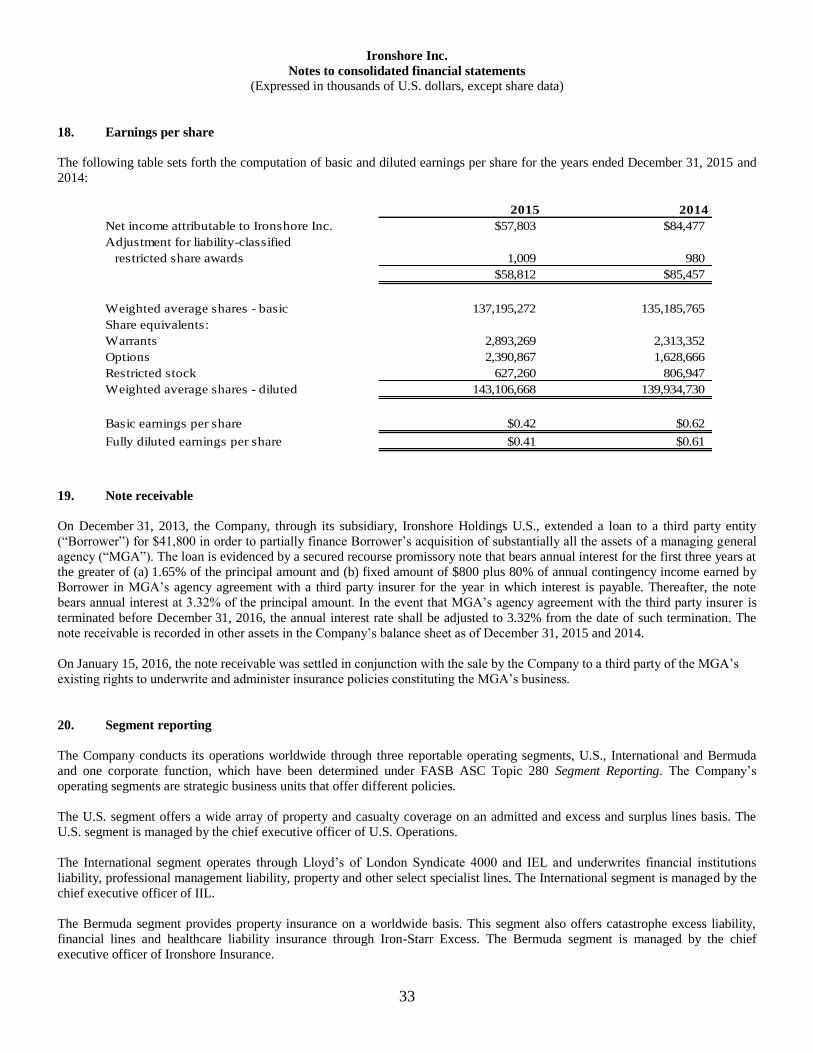

Earnings per share:

Weighted average common shares outstanding - Basic 137,195,272 135,185,765

Weighted average common shares outstanding - Diluted 143,106,668 139,934,730

Net income (loss) per common share outstanding - Basic $0.42 $0.62

Net income (loss) per common share outstanding - Diluted $0.41 $0.61

See accompanying notes to the consolidated financial statements.

5

Ironshore Inc.

Consolidated Statements of Changes in Shareholders’ Equity

For the years ended December 31, 2015 and 2014 (Expressed in thousands of U.S. dollars)

2015 2014

COMMON SHARES

Balances as of beginning of year $1,366 $1,362

Issuance of shares, net of forfeitures 377 8

Repurchase of shares (336) (4)

Balance as of end of year 1,407 1,366

ADDITIONAL PAID-IN CAPITAL

Balance as of beginning of year 1,364,762 1,354,164

Issuance of shares, net of forfeitures 466,387 2,590

Repurchase of shares (469,813) (5,189)

Contribution of additional paid-in capital 36,947 -

Stock compensation expense 19,450 7,927

Tax benefit on stock compensation expense 8,088 722

Modification of liability awards to equity 5,973 5,897

Purchase of non-controlling interest - (1,349)

Balance as of end of year 1,431,794 1,364,762

ACCUMULATED OTHER COMPREHENSIVE LOSS

Balance as of beginning of year (8,074) (10,321)

Equity gains from foreign currency translation 3,851 6,909

Losses on intra-entity foreign currency transactions (1,926) (4,662)

Balance as of end of year (6,149) (8,074)

RETAINED EARNINGS

Balance as of beginning of year 481,707 397,230

Net income attributable to Ironshore Inc. 57,803 84,477

Balance as of end of year 539,510 481,707

TOTAL IRONSHORE INC. SHAREHOLDERS' EQUITY 1,966,562 1,839,761

NON-CONTROLLING INTEREST

Balance as of beginning of year - 3,909

Net loss attributable to non-controlling interest - (11)

Purchase of non-controlling interest - (3,898)

Balance as of end of year - -

TOTAL SHAREHOLDERS' EQUITY $1,966,562 $1,839,761

See accompanying notes to the consolidated financial statements.

6

Ironshore Inc.

Consolidated Statements of Cash Flows

For the years ended December 31, 2015 and 2014 (Expressed in thousands of U.S. dollars)

2015 2014

CASH FLOWS PROVIDED BY OPERATING ACTIVITIES:

Net income $57,803 $84,466

ADJUSTMENTS TO RECONCILE NET INCOME TO NET CASH

PROVIDED BY OPERATING ACTIVITIES:

Amortization and depreciation 7,906 10,478

Stock compensation expense 22,953 11,866

Amortization of fixed maturity securities 23,444 19,724

Net realized and unrealized (gains) losses on investments 48,351 (28,039)

Deferred tax benefit (25,065) (7,931)

CHANGES IN OPERATING ASSETS AND LIABILITIES:

Accrued investment income (1,765) (1,031)

Premiums receivable 13,138 (60,928)

Reinsurance recoverable on unpaid losses (88,342) (109,272)

Reinsurance recoverable on paid losses 6,551 (5,993)

Deferred acquisition costs 16,027 (2,683)

Prepaid reinsurance premiums (68,945) (33,088)

Other assets 2,018 5,370

Reserve for losses and loss adjustment expenses 381,347 681,891

Unearned premiums 4,691 116,772

Insurance and reinsurance balances payable (8,461) 59,492

Other liabilities 48,699 15,499

Net cash provided by operating activities 440,350 756,593

CASH FLOWS USED IN INVESTING ACTIVITIES:

Purchases of fixed maturity securities (3,974,331) (3,723,875)

Purchases of short term investments (22,055) (278,929)

Purchases of equity securities (134,894) (347,221)

Purchases of other investments (83,236) (58,497)

Proceeds from sales of fixed maturity securities 3,086,889 2,654,490

Proceeds from maturity of fixed maturity securities 430,589 401,470

Proceeds from sales of short term investments 58,956 283,885

Proceeds from sales of equity securities 135,978 278,630

Proceeds from sales of other investments 61,724 1,726

Purchases of fixed assets (9,890) (9,368)

Issuance of note receivable - (3,741)

Net cash used in investing activities (450,270) (801,430)

See accompanying notes to the consolidated financial statements.

7

Ironshore Inc.

Consolidated Statements of Cash Flows

For the years ended December 31, 2015 and 2014 (Expressed in thousands of U.S. dollars)

2015 2014

CASH FLOWS PROVIDED BY FINANCING ACTIVITIES:

Proceeds from issuance of common shares 466,764 2,600

Repurchase of shares (470,149) (5,156)

Contribution of additional paid-in capital 36,965 -

Contribution of deferred merger consideration 35,413 -

Issuance of debt - 100,000

Purchase of non-controlling interest - (5,247)

Net cash provided by financing activities 68,993 92,197

Net increase in cash and cash equivalents 59,073 47,360

Cash and cash equivalents as of beginning of year 328,797 286,700

Effect of exchange rates on cash and cash equivalents (6,266) (5,263)

CASH AND CASH EQUIVALENTS AS OF END OF YEAR $381,604 $328,797

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION:

Income taxes paid $20,639 $12,578

Interest paid $21,631 $21,393

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

8

1. Nature of the business

Ironshore Inc. (“Ironshore”), a Cayman Islands corporation, through its subsidiaries (collectively referred to as the “Company”)

provides specialty commercial property and casualty coverage for risks located throughout the world.

The Company’s principal operating subsidiary, Ironshore Insurance Ltd. (“Ironshore Insurance”), is registered as a Class 4 insurer

under The Insurance Act 1978 in Bermuda, related regulations and amendments thereto (the “Bermuda Insurance Act”). Ironshore

Insurance writes primarily property catastrophe and property all-risks coverage for small to mid-sized commercial risks. Ironshore

Insurance includes Ironshore Insurance Ltd, Singapore Branch, which is registered as a direct insurer to carry on general insurance

in Singapore effective January 26, 2012, and Ironshore Insurance Ltd., Canada Branch, which writes property and casualty

insurance for Canadian-domiciled risks effective March 29, 2014.

The Company’s U.S. platform consists of Ironshore Holdings (U.S.) Inc. (“Ironshore Holdings U.S.”), a Delaware corporation, and

its principal subsidiaries Ironshore Indemnity Inc., (“Ironshore Indemnity”), a Minnesota domiciled insurer, and Ironshore

Specialty Insurance Company (“Ironshore Specialty”), an Arizona domiciled insurer (collectively referred to as the “U.S.

companies”). The U.S. companies serve the property and specialty casualty insurance market sectors. The U.S. companies also

insure all classes of aviation and aerospace risks worldwide through an agreement with Starr Aviation Agency, Inc.

The Company’s International platform includes Ironshore International Ltd. (“IIL”) and a subsidiary company, Ironshore

Corporate Capital Ltd. (“ICCL”), both of which were incorporated in England and Wales. The International platform also includes

Pembroke JV Limited (“PJV”), its principal subsidiary, Pembroke Managing Agency Limited (“PMA”), and Ironshore Europe

Limited (“IEL”), an Irish corporation. PMA operates within the Lloyd’s of London (“Lloyd’s”) insurance market through

Syndicate 4000 and underwrites a portfolio of specialist lines products including financial institutions, professional liability,

marine and other select specialist lines. IEL commenced underwriting a diverse range of specialty lines in 2011.

Iron-Starr Excess Agency Ltd (“Iron-Starr Excess” or the “Agency”) acts as a specialty lines insurance and reinsurance managing

general agency in the offering, issuance and administration of insurance policies written on an equal subscription basis by

Ironshore Insurance and Starr Insurance and Reinsurance Limited (“SIRL”). In July 2014, Iron-Starr Excess added Hamilton Re, a

Bermuda-based property and casualty reinsurer, as subscribing insurer in order to increase capacity for full suites of products being

offered. Iron-Starr Excess writes financial lines, healthcare and catastrophic excess casualty insurance products, targeting Fortune

2000 and other clients purchasing catastrophe excess coverage.

2. Significant accounting policies

Basis of presentation These consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the

United States of America (“U.S. GAAP”) and include the financial statements of Ironshore and its wholly owned and majority

owned subsidiaries. All significant inter-company balances and transactions have been eliminated in consolidation. Certain prior

year amounts have been reclassified to conform to the current year presentation.

Use of estimates in financial statements

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions

that affect the reported and disclosed amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the

date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results

could differ materially from those estimates. The major estimates reflected in the Company’s consolidated financial statements

include, but are not limited to, the reserves for losses and loss adjustment expenses, reinsurance recoverable balances including

allowances for reinsurance recoverables deemed uncollectible, estimates of written and earned premium, the fair value of

investments, recoverability of intangible assets and the net deferred tax asset or liability.

Premiums and related expenses

Premiums. Direct insurance and assumed facultative reinsurance premiums are recognized as earned on a pro rata basis over the

applicable policy or contract periods. For assumed treaty reinsurance written on a losses occurring basis, premiums written are

earned on a pro rata basis over the risk period. For assumed treaty reinsurance written on a risks attaching basis, premiums written

are earned on a pro rata basis over the periods of the underlying policies. Premiums may include estimates based on information

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

9

received from brokers, ceding insurers and insureds, and any subsequent differences from such estimates are recorded in the period

in which they are determined. In each case, the portions of the premiums written applicable to the unexpired terms are recorded as

unearned premiums.

Assumed retroactive loss portfolio transfer (“LPT”) contracts in which the insured loss events occurred prior to the inception of the

contract are evaluated to determine whether they meet the established criteria for reinsurance accounting. If reinsurance accounting

is appropriate, premiums written are fully earned and corresponding losses and loss adjustment expenses recognized at the

inception of the contract. The contracts can cause significant variances in gross premiums written, net premiums written, net

premiums earned, and net incurred losses in the years in which they are written. Reinsurance contracts sold not meeting the

established criteria for reinsurance accounting are recorded using the deposit method.

A premium deficiency reserve is established when expected claim payments or incurred losses, loss adjustment expenses and

administrative expenses exceed the premiums to be earned over the remaining contract period. For the purposes of determining

whether a premium deficiency reserve exists contracts are grouped in a manner consistent with how policies are marketed,

serviced and measured. Anticipated investment income is utilized as a factor in the premium deficiency reserve calculation.

Acquisition expenses Acquisition expenses are costs that vary with, and are directly related to, the production of new and renewal business, and consist

principally of commissions and brokerage expenses. The Company does not capitalize internal costs associated with the

production of new business. Acquisition expenses are shown net of commissions on reinsurance ceded. These costs are deferred

and amortized over the periods in which the related premiums are earned. Deferred acquisition costs are limited to their estimated

realizable value based on the related unearned premiums. Anticipated loss and loss adjustment expenses based on historical and

current experience and anticipated investment income related to those premiums are considered in determining the recoverability

of deferred acquisition costs. Acquisition expenses also include profit commission. Profit commissions are recognized when

earned.

Reserve for losses and loss adjustment expenses

The reserve for losses and loss adjustment expenses includes reserves for unpaid reported losses and for losses incurred but not

reported. The reserve for unpaid reported losses and loss expenses is established by management based on reports from loss

adjusters, ceding companies and insureds and represents the estimated ultimate cost of events or conditions that have been reported

to, or specifically identified, by the Company. The reserve for incurred but not reported losses and loss adjustment expenses is

established by management based on actuarially determined estimates of ultimate losses and loss expenses. Inherent in the estimate

of ultimate losses and loss expenses are expected trends in claim severity and frequency and other factors which vary significantly

as claims are settled. Accordingly, ultimate losses and loss expenses may differ materially from the amounts recorded in the

consolidated financial statements. These estimates are reviewed regularly and, as experience develops and new information

becomes known, the reserves are adjusted as necessary. Such adjustments, if any, are recorded in earnings in the periods in which

they become known and are accounted for as changes in estimates.

Ceded Reinsurance In the normal course of business, the Company may seek to mitigate underwriting risk that could cause unfavorable results by

reinsuring certain amounts of risk with reinsurers. Reinsurance does not relieve the Company of its primary obligation to the

insured. The accounting for reinsurance ceded depends on the method of reinsurance. If the policy is on a losses occurring basis,

reinsurance premiums ceded and associated commissions are expensed on a pro rata basis over the period reinsurance coverage is

provided. If the policy is on a risk attaching basis, reinsurance premiums ceded and associated commissions are expensed in line

with gross premiums earned to which the risk attaching policy relates. Prepaid reinsurance premiums represent the portion of

premiums ceded on the unexpired terms of the policies purchased. Reinsurance commissions that will be earned in the future are

deferred and recorded as deferred acquisition costs on the balance sheets.

Reinsurance recoverable is presented on the balance sheets net of any reserves for uncollectible reinsurance. The method of

determining the reinsurance recoverable on unpaid losses and loss adjustment expenses involves actuarial estimates in a manner

consistent with the determination of unpaid losses and loss adjustment expenses.

Ceded reinstatement premiums are estimated after the occurrence of a significant loss and are recorded in accordance with the

contract terms based upon the ultimate loss estimates associated with each contract. Ceded reinstatement premiums are earned over

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

10

the remaining contract period. Ceded reinstatement premiums earned were $5,905 and $8,296 for the years ended December 31,

2015 and 2014, respectively.

Certain ceded reinsurance contracts do not transfer underwriting risk and are accounted for using the deposit method of

accounting. Fees are accounted for as income based on the terms of the contract. A deposit asset is recorded at the inception of the

contract based on the consideration transferred. Corresponding changes in the amount of the deposit asset reflecting actual and

expected future loss payments are recorded as a credit or charge to interest income.

Investments The Company’s investments in fixed maturity and equity securities are classified as trading and are carried at fair value, with

related unrealized gains and losses recorded in net realized and unrealized gains (losses) on investments included in the statement

of operations and comprehensive income. The Company believes that accounting for its investments as trading with all changes in

fair value included in income reduces an element of management judgment as the Company is not required to perform an analysis

of its investments for other-than-temporary impairment.

Fair values of the Company’s fixed maturity and equity securities are based on quoted market prices or, when such prices are not

available, by reference to broker or underwriter bid indications and/or internal pricing valuation techniques. Investment

transactions are recorded on a trade date basis with balances pending settlement recorded as receivable for investments sold or

payable for investments purchased.

For mortgage-backed and other asset-backed debt securities, fair value includes estimates regarding prepayment assumptions,

which are based on current market conditions. Amortized cost in relation to these securities is calculated using a constant effective

yield based on anticipated prepayments and estimated economic lives of the securities. When actual prepayments differ

significantly from anticipated prepayments, the effective yield is recalculated to reflect actual payments to date. Changes in

estimated yield are recorded on a retrospective basis, which results in future cash flows being used to determine current book

value.

Realized gains and losses on sales of investments are determined on the average cost basis.

Net investment income includes interest income on fixed maturity securities, recorded when earned, dividend income on equity

investments, recorded when declared and the amortization of premiums and discounts on investments. The amortization of

premium and accretion of discount is computed using the effective interest rate method. Net investment income is recorded net of

investment expenses.

Short term investments Short term investments, which are managed as part of the Company’s investment portfolio, have an original maturity of one year

or less when purchased, and are carried at cost which approximates fair value.

Other investments

Other investments include investments in promissory notes and investments in closed-end limited partnerships that invest

primarily in commercial real estate debt in North America and Europe. It also includes investment in a Cayman-island registered

partnership fund that primarily invests in portfolio companies in China, Hong Kong, Macau and/or Taiwan. Investments in

promissory notes are carried at cost with interest income recorded in net investment income. Investments in closed-end limited

partnerships and Cayman-island registered fund are carried at fair value, with related unrealized gains and losses recorded in net

realized and unrealized gains (losses) on investments included in the statement of operations and comprehensive income.

Cash and cash equivalents The Company considers all investments with an original maturity of ninety days or less as cash equivalents.

Other Assets Investments in which the Company had significant influence over the operating and financial policies of the investee are classified

as other assets and are accounted for under the equity method of accounting. Under this method, the Company records its

proportionate share of income or loss from such investments in its results for the period and includes these investments in other

assets in its consolidated financial statements.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

11

Also included in other assets are depreciable long-lived assets such as information technology equipment, software, leasehold

improvements, furniture and fixtures that are carried at cost less accumulated depreciation and are depreciated on a straight-line

basis over their estimated useful lives taking into account residual value. The estimated useful lives (i.e. information technology

equipment—3 years; software—3 to 5 years; leasehold improvements—shorter of their useful life or remaining life of the lease;

furniture and fixtures—5 years) is based on the period over which the Company expects to generate net cash inflows from the use

of these assets. The depreciable long-lived assets are subject to impairment testing whenever events or changes in circumstances

indicate that their carrying amount may not be recoverable.

Insurance and reinsurance balances payable Insurance and reinsurance balances payable principally represents ceded premiums payable and profit commissions payable to

third party reinsurance companies or program administrators. Also included within this line item are amounts related to the

Company’s insurance business principally related to return premiums, which arise when an insurance contract is cancelled and the

Company is required to return some or all of the premium received to the insured.

Business combinations, goodwill and other intangible assets The Company accounts for business combinations in accordance with FASB ASC Topic 805 Business Combinations, and

goodwill and other intangible assets that arise from business combinations in accordance with FASB ASC Topic 350 Intangibles—

Goodwill and Other. A purchase price that is in excess of the fair value of the net assets acquired arising from a business

combination is recorded as goodwill, and is not amortized. Other intangible assets with a finite life are amortized over the

estimated useful life of the asset. Other intangible assets with an indefinite useful life are not amortized.

Goodwill and other indefinite life intangible assets are tested for impairment at least annually. The Company first assesses

qualitative factors in determining whether it is necessary to perform the two-step quantitative goodwill impairment test. Only if

management determines that it is more likely than not that the fair value of a reporting unit is less than its carrying amount based

on qualitative factors, would it be required to then perform the two-step quantitative goodwill impairment test detailed below.

The first step identifies potential impairments by comparing the fair value of the reporting unit to its book value, including

intangibles. If the fair value of the reporting unit exceeds the carrying amount, the intangible is not impaired and the second step is

not required. If the carrying value is in excess of the fair value, the second step computes the possible impairment loss by

comparing the implied fair value of the intangible with the carrying amount. If the implied fair value of the intangible is less than

the carrying amount, the intangible is written down to its fair value with a corresponding expense being charged to earnings.

The Company considers the recoverability of its intangible assets whenever a change in circumstances arises and in the event that

an impairment exists, any excess unamortized balances are recorded in earnings.

Non-controlling interest The Company accounts for non-controlling interest in accordance with FASB ASC Topic 805 Business Combinations which

establishes accounting and reporting standards that require that ownership interests in subsidiaries held by other parties be

presented in the consolidated statement of shareholders’ equity separately from the parent’s equity and the consolidated net income

attributable to non-controlling interest be presented on the face of the consolidated statements of operations and comprehensive

income. The guidance also requires that changes in a parent’s ownership interest while the parent retains controlling financial

interest in its subsidiary be accounted for consistently. Disclosures in financial statements are required to identify and distinguish

between the interests of the parent and non-controlling owners. On July 1, 2014, the Company purchased the remaining 40%

interest in Wright & Co. from the non-controlling shareholders for cash of $5,247, increasing its ownership interest from 60% to

100%.

Foreign exchange The Company’s reporting currency is the United States Dollar (U.S. dollars). Monetary assets and liabilities denominated in

currencies other than the entities’ functional currencies are revalued at the exchange rates in effect as of the balance sheet date with

the resulting foreign exchange gains and losses included in earnings as net foreign exchange gains (losses). Revenues and expenses

denominated in currencies other than the entities’ functional currencies are remeasured at the average rate for the period. The

financial statements of each of the Company’s subsidiaries are initially measured using the entity’s functional currency, which is

determined based on its operating environment and its underlying cash flows. For entities with a functional currency other than

U.S. dollars, foreign currency assets and liabilities are translated into U.S. dollars using the period end rates of exchange, while

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

12

statements of operations are translated at average rates of exchange for the period. The resulting cumulative translation adjustment

is recorded in accumulated other comprehensive income as a separate component of shareholders’ equity.

Stock based compensation The Company accounts for its stock compensation plans in accordance with the fair value recognition provisions of FASB ASC

Topic 718 Compensation—Stock Compensation, which requires the Company to measure the cost of services received from

employees, directors and eligible consultants in exchange for an award of equity instruments based on the estimated fair value of

the award on the date of grant for equity-classified awards. The cost of these services is recognized as compensation expense over

the requisite service period and is included in earnings. The Company measures liability-classified awards based on the fair value

remeasured at each reporting period until the date of settlement. The compensation cost related to liability-classified awards

includes a change in the fair value of the liability instrument at each reporting period.

Earnings per share Basic earnings per ordinary share are calculated by dividing net income available to ordinary shareholders by the weighted average

number of ordinary shares outstanding. Diluted earnings per ordinary share are based on the weighted average number of ordinary

shares, warrants, restricted stock and options outstanding, except the effects of the warrants, restricted stock and options that are

anti-dilutive.

Taxation Income taxes have been provided in accordance with the provisions of FASB ASC Topic 740 Income Taxes on those operations

which are subject to income taxes. Deferred tax assets and liabilities result from temporary differences between the amounts

recorded in the consolidated financial statements and the tax basis of the Company’s assets and liabilities. The effect on deferred

tax assets and liabilities of a change in tax rates is recognized in earnings in the period that includes the enactment date. A

valuation allowance against deferred tax assets is recorded if it is more likely than not that all, or some portion, of the benefits

related to deferred tax assets will not be realized.

The Company reflects tax positions in accordance FASB ASC Topic 740, Income Taxes. Such tax positions are, based solely on

their technical merits, more likely than not to be sustained upon examination by taxing authorities and reflect the largest amount of

benefit, determined on a cumulative probability basis that is more likely than not to be realized upon settlement with the applicable

taxing authority with full knowledge of all relevant information.

Recent accounting pronouncement

Amendments to Fair Value Disclosures

In May 2015, the FASB issued Accounting Standards Update 2015-07 “Disclosure for Investments in Certain Entities That

Calculate Net Asset Value per Share (or Its Equivalent)” which removes the requirement to categorize within the fair value

hierarchy all investments for which fair value is measured using the net asset value per share practical expedient. However, the

reporting entity is still required to disclose information that will help users understand the nature and risk of these investments.

This update is effective for public business entities for fiscal years beginning after December 15, 2015 and after December 15, 2016

for all other entities. The amendments should be applied retrospectively for all periods presented. Earlier application is permitted.

The Company adopted this pronouncement starting for the period ended June 30, 2015 and it had no material impact on the

consolidated financial statements.

Amendments to the Consolidation Standard

In February 2015, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update No. 2015-2,

Consolidation – Amendments to the Consolidation Analysis, which amends the current consolidation guidance. The main

provisions of these amendments may affect consolidation conclusion and include, among others, the following key items:

elimination of three of the six conditions for evaluating whether a fee paid to a decision maker or a service provider

represents a variable interest;

exclusion of some fee arrangements paid to a decision maker on determining primary beneficiary; and

reduction in the application of related party guidance on determining primary beneficiary.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

13

This update will be effective for public business entities with annual periods beginning after December 15, 2015 and December 15,

2016 for all other entities. Earlier application is allowed. The Company believes that this guidance has no impact on the

consolidated financial statements.

Elimination of Extraordinary Item Concept

In January 2015, the FASB issued Accounting Standard Update No. 2015-01, Income Statement – Extraordinary and Unusual

Items which eliminates the concept of extraordinary items. Preparers and their auditors will no longer need to evaluate whether

unusual and/or infrequent items are treated properly. Presentation and disclosure guidance for items that are unusual in nature or

infrequent in occurrence will be expanded to include items that have both characteristics. This update will be effective for interim

and annual periods beginning after December 15, 2015. Earlier application is allowed. The Company believes that this guidance

will have no impact on the consolidated financial statements.

Simplifying the Presentation of Debt Issuance Costs

In April 2015, the FASB issued Accounting Standards Update 2015-03 Simplifying the Presentation of Debt Issuance Costs

requiring entities to present debt issuance costs related to a recognized liability in the balance sheet as a direct reduction from that

liability rather than as an asset. This will align the presentation of debt issuance costs with that of debt discounts and premiums. The

guidance is effective for non-public business entities for fiscal years beginning after December 15, 2015 and interim periods within

fiscal years beginning after December 15, 2016. Earlier application is permitted. The Company believes that this guidance will not

have a material impact on the consolidated financial statements.

Disclosures about Short Duration Insurance Contracts

In May 2015, the FASB issued Accounting Standards Update 2015-09 Disclosures about Short Duration Insurance Contracts

requiring insurers to make additional disclosures about short-duration contracts (typically a year or less). The disclosures focus on

the liability for unpaid claims and claim adjustment expenses. Insurers are required to provide tables showing incurred and paid

claims development information by accident year for the number of years claim typically remain outstanding (but not more than 10

years). Insurers will also have to provide a reconciliation of this information to the statement of financial position. For accident

years included in the development tables, insurers will have to disclose the total of incurred-but-not-reported liabilities and

expected development on reported claims plus claims frequency information unless impracticable, and the historical average annual

percent of payout incurred claims. These disclosures will be required to be aggregated or disaggregated so that useful information is

not obscured. The guidance is effective for non-public business entities for fiscal years beginning after December 15, 2016 and

interim periods the following year. Earlier application is permitted. The Company believes that this guidance has no impact on the

consolidated financial statements as it is a change in disclosure only.

Simplifying the Accounting for Measurement Period Adjustments

In September 2015, The FASB issued Accounting Standards Update 2015-16 Simplifying the Accounting for Measurement Period

Adjustments eliminating the requirement that an acquirer in a business combination account for adjustments it makes to the

provisional amounts it records for assets and liabilities retrospectively. An acquirer must recognize these measurement-period

adjustments during the period in which it determines their amounts, including the effect on earnings of any amounts they would

have recorded in previous periods if the accounting had been completed at the acquisition date. The guidance is effective for non-

public business entities for fiscal years beginning after December 15, 2016 and interim periods with fiscal years beginning after

December 15, 2017. Earlier application is permitted. The Company believes that this guidance will not have a material impact on

the consolidated financial statements.

3. Fosun Equity Investment and Ironshore Tender Offer

On August 17, 2014, the Company entered into a definitive equity purchase agreement (the “Equity Purchase Agreement”) with

Fosun International Limited (“Fosun”) and Mettlesome Investment Limited, a wholly owned subsidiary of Fosun (“Mettlesome”),

pursuant to which the Company agreed to sell to Mettlesome 20% of Ironshore’s total outstanding ordinary shares on a fully

diluted basis (the “Fosun Equity Investment”). The Fosun Equity Investment was consummated on February 12, 2015 and,

pursuant to the terms of the Equity Purchase Agreement, the Company initially issued to Mettlesome 27,980,743 ordinary shares

for a cash purchase price of $456,804. The purchase price and number of shares issued were subject to certain post-closing

adjustments under the Equity Purchase Agreement.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

14

In November 2014, the Company launched a tender offer (the “Ironshore Tender Offer”) to repurchase securities representing 20%

of Ironshore’s total outstanding ordinary shares on a fully diluted basis. Following closing of the Fosun Equity Investment, the

Company consummated the Ironshore Tender Offer, repurchasing 27,687,491 ordinary shares (including shares underlying options

and Class B warrants exercised in connection with the tender offer) at approximately $16.3256 per share and 1,921,040 Class A

warrants at approximately $6.3256 per warrant. All of the proceeds from the Fosun Equity Investment, together with the exercise

price payable to the Company upon the exercise of options and Class B warrants described above, were used to pay the tender

offer consideration. The securities repurchased by the Company pursuant to the Ironshore Tender Offer were cancelled and retired.

The number of securities repurchased by the Company and the aggregate tender offer consideration are subject to adjustment based

on the post-closing adjustments pursuant to the Equity Purchase Agreement.

On March 6, 2015, in conjunction with the initial post-closing adjustment pursuant to the Equity Purchase Agreement, the

Company issued 97,296 additional shares to Mettlesome and received a cash purchase price adjustment of $9,776.

The post-closing adjustments under the Equity Purchase Agreement and the related post-closing share adjustments pursuant to the

Ironshore Tender Offer were finalized in the second fiscal quarter of 2015. Costs incurred associated with the Fosun Equity

Investment are recorded in non-recurring transaction expenses in the consolidated statement of operations and comprehensive

income.

Effective upon closing of the Fosun Equity Investment, the Company’s memorandum of association was amended to increase the

authorized capital of the Company from 200,000,000 ordinary shares to 400,000,000 shares, par value of $0.01 each, which may

be ordinary shares or preferred shares.

4. Merger with Fosun

On May 1, 2015, the Company entered into a definitive merger agreement (the “Merger Agreement”) with Fosun International

Limited (“Fosun”), Mettlesome Investments (Cayman) III Limited (“Purchaser”), Mettlesome Investment 2, a wholly-owned

subsidiary of Purchaser (“Merger Sub”) and IS Equityholder Rep, LLC, solely in its capacity as the representative of the

equityholders of the Company (“Equityholder Representative”), pursuant to which the parties agreed that Fosun would acquire

indirectly the remaining interest in the Company that Fosun did not already beneficially own (the “Fosun Acquisition”). On

November 20, 2015, the Fosun Acquisition was effected by the merger of Merger Sub with and into the Company, with the

Company surviving the merger and becoming a wholly owned indirect subsidiary of Fosun. The aggregate consideration paid by

Purchaser was $2,042,936, which was allocated ratably among the holders of shares, restricted share units, warrants and options of

the Company (taking into consideration the exercise prices of warrants and options), after deduction of (a) the portion of

transaction expenses incurred by the Company payable out of the merger consideration, (b) transaction expenses incurred by the

Equityholder Representative prior to the Closing, (c) $2,500 to fund an escrow account against which indemnity claims may be

made by the Purchaser and (d) $750 to fund potential expenses incurred by the Equityholder Representative after the closing.

Payments for certain equity held by certain employees of the Company were funded into separate escrow accounts for the benefit

of such employees, and payments out of such escrow accounts will be made to such employees on a deferred basis, in each case,

pursuant to arrangements contemplated by the Merger Agreement. The deferred consideration payable was $48,498 and is

recorded in the consolidated balance sheet in the following line items: cash of $48,498, other liabilities of $35,413, and additional

paid in capital of $13,085. Costs incurred associated with the merger of $22,110 are recorded in non-recurring transaction expenses in the consolidated

statement of operations and comprehensive income. Fosun reimbursed the Company for these expenses and the reimbursement is

recorded as additional paid in capital in the balance sheet. Non-recurring transaction expenses also include costs incurred of

$7,615 associated with the Fosun Equity Investment (refer to Note 3) and $9,804 due to the accelerated vesting of certain share

based compensation awards pursuant to the Merger Agreement.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

15

5. Investment in Joint Ventures

Ironshore Holdings U.S. formed IDP Holdings LLC (“IDP”) as a joint venture with The Distinguished Programs Group LLC

(“DPG”).

On November 1, 2012, IDP entered into an Asset and Membership Interest Purchase Agreement with National Specialty

Underwriters, Inc. and certain of its subsidiaries (collectively, “NSU”) pursuant to which IDP purchased NSU’s hospitality and

casualty insurance programs business and related claims administration business for cash and a promissory note issued by IDP.

Ironshore Holdings U.S. made a cash equity investment of $4,844 and advanced a loan of $10,088 to IDP, which equity

investment and loan, together with a cash equity investment by DPG, were used to finance the purchase from NSU. In April 2014,

Ironshore Holdings U.S. made an additional cash equity investment of $1,250 and advanced a loan of $2,500 to IDP, which equity

investment and loan, together with a cash equity investment by DPG were used to repay the promissory note issued by IDP in

connection with the NSU transaction. Further, on September 1, 2014, IDP entered into an asset purchase agreement with DPG

pursuant to which IDP purchased certain new hospitality program business from DPG for cash. Ironshore Holdings U.S. made an

additional cash equity investment of $620 and advanced a loan of $1,241 to IDP, which equity investment and loan, together with

a cash equity investment by DPG were used to finance such purchase from DPG. Each loan from Ironshore Holdings U.S. to IDP

bears interest at a rate of prime plus 4% per annum subject to a minimum interest rate of 6% per annum and a maximum interest

rate of 12% per annum. The loans were secured by a pledge of substantially all of the assets of IDP. All profits and losses of

operations are shared equally between Ironshore Holdings U.S. and DPG.

On October 26, 2015, Ironshore Holdings U.S. sold its ownership interest in IDP to DPG for $10,893 resulting in a gain of $5,330

recognized in other income. In addition, the aggregate promissory note value of $13,828 and accrued interest outstanding up to the

October 26, 2015 were settled by DPG.

6. Goodwill and other intangible assets

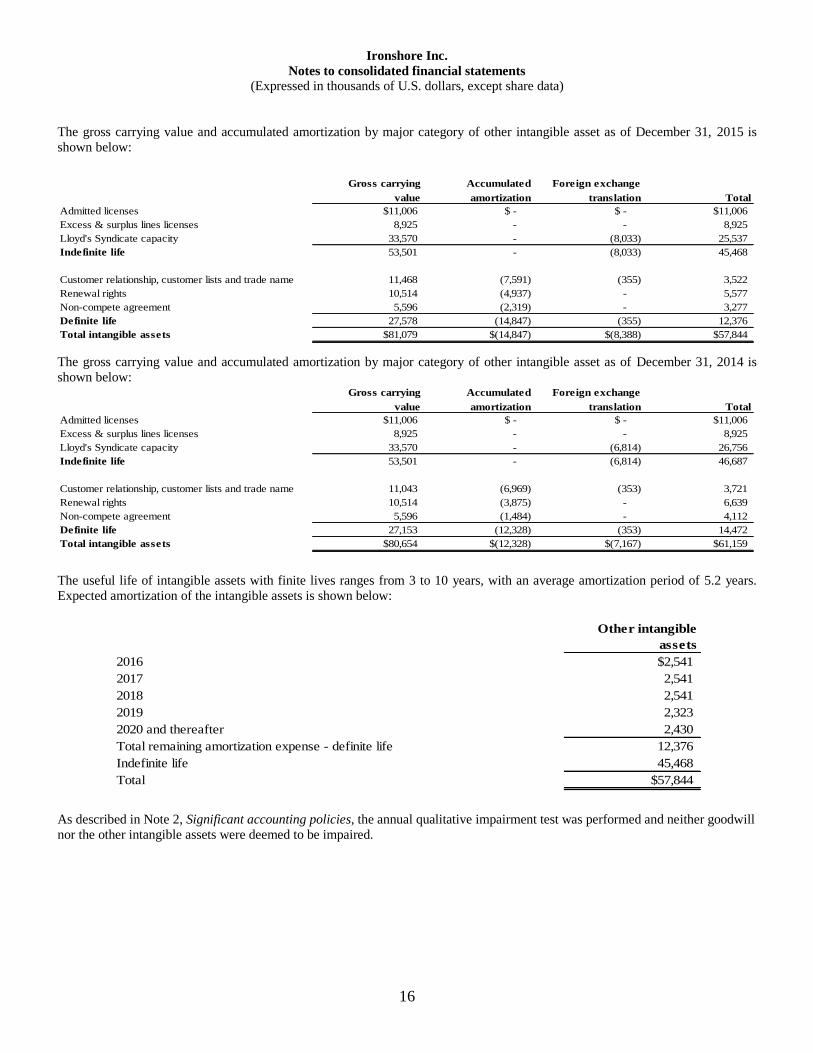

Goodwill and other intangibles as of December 31, 2015 and 2014 are as follows:

Goodwill & other

Goodwill intangible assets

Gross Gross Amortization

Foreign

Exchange Total Total

Balance as of January 1, 2014 $17,804 $80,425 $(9,944) $(5,727) $64,754 $82,558

Reclassification (b) 391 (391) - - (391) -

Acquired during 2014 - 620 - - 620 620

Amortization - - (2,384) - (2,384) (2,384)

Foreign exchange translation (a) - - - (1,440) (1,440) (1,440)

Balance as of December 31, 2014 18,195 80,654 (12,328) (7,167) 61,159 79,354

Acquired during 2015 187 425 - - 425 612

Amortization - - (2,519) - (2,519) (2,519)

Foreign exchange translation (a) - - - (1,221) (1,221) (1,221)

Balance as of December 31, 2015 $18,382 $81,079 $(14,847) $(8,388) $57,844 $76,226

Other intangible assets

(a) Represents foreign exchange translation on Lloyd’s Syndicate capacity.

(b) Represents adjustment related to the acquisition of ERR acquisition.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

16

The gross carrying value and accumulated amortization by major category of other intangible asset as of December 31, 2015 is

shown below:

Gross carrying Accumulated Foreign exchange

value amortization translation Total

Admitted licenses $11,006 $ - $ - $11,006

Excess & surplus lines licenses 8,925 - - 8,925

Lloyd's Syndicate capacity 33,570 - (8,033) 25,537

Indefinite life 53,501 - (8,033) 45,468

Customer relationship, customer lists and trade name 11,468 (7,591) (355) 3,522

Renewal rights 10,514 (4,937) - 5,577

Non-compete agreement 5,596 (2,319) - 3,277

Definite life 27,578 (14,847) (355) 12,376

Total intangible assets $81,079 $(14,847) $(8,388) $57,844

The gross carrying value and accumulated amortization by major category of other intangible asset as of December 31, 2014 is

shown below: Gross carrying Accumulated Foreign exchange

value amortization translation Total

Admitted licenses $11,006 $ - $ - $11,006

Excess & surplus lines licenses 8,925 - - 8,925

Lloyd's Syndicate capacity 33,570 - (6,814) 26,756

Indefinite life 53,501 - (6,814) 46,687

Customer relationship, customer lists and trade name 11,043 (6,969) (353) 3,721

Renewal rights 10,514 (3,875) - 6,639

Non-compete agreement 5,596 (1,484) - 4,112

Definite life 27,153 (12,328) (353) 14,472

Total intangible assets $80,654 $(12,328) $(7,167) $61,159

The useful life of intangible assets with finite lives ranges from 3 to 10 years, with an average amortization period of 5.2 years.

Expected amortization of the intangible assets is shown below:

Other intangible

assets

2016 $2,541

2017 2,541

2018 2,541

2019 2,323

2020 and thereafter 2,430

Total remaining amortization expense - definite life 12,376

Indefinite life 45,468

Total $57,844

As described in Note 2, Significant accounting policies, the annual qualitative impairment test was performed and neither goodwill

nor the other intangible assets were deemed to be impaired.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

17

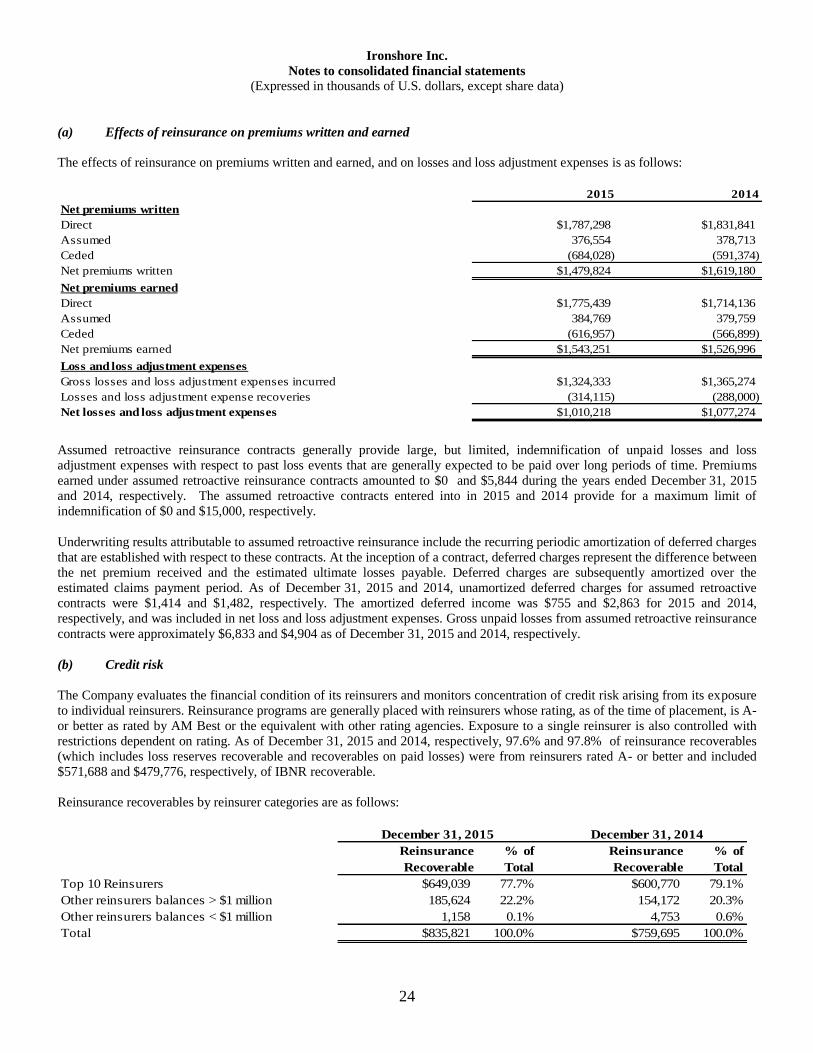

7. Investments

The amortized cost, gross unrealized gains and losses and fair value of investments as of December 31, 2015 are as follows:

Amortized Unrealized Unrealized Fair

cost gains losses value

U.S. government and government agency securities $484,524 $164 $(1,240) $483,448

Non-U.S. government and government agency securities 121,800 1,040 (4,191) 118,649

Municipal securities 90,898 845 (182) 91,561

Corporate securities 1,589,575 7,030 (12,815) 1,583,790

Bank loans 456,803 1,656 (10,055) 448,404

U.S. asset-backed securities 610,907 293 (5,588) 605,612

U.S. mortgage-backed securities 1,096,719 6,009 (8,224) 1,094,504

Total fixed maturity securities 4,451,226 17,037 (42,295) 4,425,968

Equity securities 202,014 10,547 (11,837) 200,724

Short term investments 3,979 - - 3,979

4,657,219 $27,584 $(54,132) $4,630,671

The amortized cost, gross unrealized gains and losses and fair value of investments as of December 31, 2014 are as follows:

Amortized Unrealized Unrealized Fair

cost gains losses value

U.S. government and government agency securities $359,877 $764 $(370) $360,271

Non-U.S. government and government agency securities 107,536 1,663 (1,122) 108,077

Municipal securities 88,020 1,344 (179) 89,185

Corporate securities 1,325,037 15,915 (8,015) 1,332,937

Bank loans 435,697 1,489 (6,811) 430,375

U.S. asset-backed securities 635,540 1,562 (3,459) 633,643

U.S. mortgage-backed securities 1,080,017 12,379 (2,689) 1,089,707

Total fixed maturity securities 4,031,724 35,116 (22,645) 4,044,195

Equity securities 209,265 5,527 (7,702) 207,090

Short term investments 40,877 - - 40,877

$4,281,866 $40,643 $(30,347) $4,292,162

Included in the tables above are fixed maturity securities with a fair value of $16,585 and $25,483 which are on deposit with U.S.

insurance regulators as of December 31, 2015 and 2014, respectively, to meet certain statutory requirements. The Company also

maintains fixed maturity securities and cash amounting to $1,981,393 and $1,545,000 in trust accounts as collateral under the

terms of certain insurance and reinsurance transactions as of December 31, 2015 and 2014, respectively.

As of December 31, 2015 and 2014, the Company maintained a trust account of $28,265 and $18,101, respectively, composed of

cash and fixed maturity securities to meet certain Canadian insurance regulatory requirements for Ironshore Insurance Ltd. -

Canada Branch.

On December 1, 2009, the Company entered into a $50,000 standby letter of credit facility provided by Citibank Europe plc. As of

December 31, 2015 and 2014, $49,701 and $37,254 respectively, of letters of credit were issued and outstanding under this

facility, for which $63,754 and $43,929, respectively, of fixed maturity securities were pledged as collateral.

The Company operates in the Lloyd’s market through its corporate member ICCL, which represents its participation in Syndicate

4000. Lloyd’s sets capital requirements for corporate members annually based on the Syndicates’ business plans, rating and

reserving environment together with input arising from Lloyd’s discussions with regulatory and rating agencies. Such capital, or

Funds at Lloyd’s (“FAL”), may be satisfied by cash, certain investments and undrawn letters of credit provided by approved

banks. As of December 31, 2015 and 2014, fixed maturity securities with a fair value of $322,003 and $277,571; equity securities

with a fair value of $51,698 and $55,783; and short term investments and cash equivalents with a fair value of $1,521 and $9,929,

respectively, were restricted to satisfy ICCL’s FAL requirements.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

18

The following represents an analysis of net realized gains (losses) on the sale of investments for the years ended:

Realized Realized Net realized

gains losses gains (losses)

Fixed maturity securities $11,451 $(18,250) $(6,799)

Equity securities 2,805 (5,106) (2,301)

Short term investments 602 (719) (117)

$14,858 $(24,075) $(9,217)

Year ended December 31, 2015

Realized Realized Net realized

gains losses gains (losses)

Fixed maturity securities $14,263 $(10,951) $ 3,312

Equity securities 19,639 (4,290) 15,349

Short term investments 664 (707) (43)

$34,566 $(15,948) $ 18,618

Year ended December 31, 2014

The amortized cost and fair value amounts for fixed maturity securities held as of December 31, 2015 are shown by contractual

maturity below. Actual maturity may differ from contractual maturity because certain borrowers may have the right to call or

prepay certain obligations with or without call or prepayment penalties.

Amortized cost Fair value

Due in one year or less $119,186 $119,256

Due after one year through five years 2,159,334 2,152,723

Due after five years through ten years 391,047 384,267

Due after ten years 51,160 46,731

U.S. asset-backed securities 610,907 605,612

U.S. mortgage-backed securities 1,096,719 1,094,504

U.S. government sponsored enterprises 22,873 22,875

Total fixed maturity securities $4,451,226 $4,425,968

December 31, 2015

The following table sets forth certain information regarding the investment ratings of the Company’s fixed maturity investment

portfolio as of December 31, 2015. Investment ratings are as designated by Standard & Poor’s Ratings Group or Moody’s

Investors Service.

S&P Equivalent Rating (a) Amortized cost Fair value

AAA $825,850 $821,953

AA 1,620,810 1,619,238

A 901,539 901,138

BBB 553,388 546,168

Below BBB 361,437 349,357

Not rated 188,202 188,114

Total fixed maturity securities $4,451,226 $4,425,968

December 31, 2015

(a) Carried at the lower of Standard & Poor’s or Moody’s rating, presented in Standard & Poor’s equivalent rating

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

19

Net investment income is derived from the following sources:

For the years ended December 31 2015 2014

Fixed maturity securities $109,241 $95,864

Equity securities 6,566 6,302

Other investments 6,210 2,124

Cash and cash equivalents 850 686

Short term investments 10 8

Total gross investment income 122,877 104,984

Investment expenses (9,577) (7,941)

Net investment income $113,300 $97,043

8. Fair value measurement

U.S. GAAP establishes a framework for measuring fair value using a hierarchy of fair value measurements that distinguishes market

data between observable independent market inputs and unobservable market assumptions and requires additional disclosures about

such fair value measurements. Financial assets and liabilities are classified in their entirety based on the lowest level of input that is

significant to the fair value measurement. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for

identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

The three levels of the fair value hierarchy are described further below:

Level 1: Quoted prices in active markets for identical assets/liabilities (unadjusted);

Level 2: Indirect observable inputs including quoted prices for similar assets/liabilities (adjusted) and market corroborated inputs;

Level 3: Unobservable inputs which reflect the underlying entity’s interpretation of risk assumptions used by market participants.

The Company receives assistance with its investment accounting function from an independent service provider. This service

provider as well as the Company’s investment managers uses several pricing services and brokers to assist with the determination of

the fair value of the Company’s investment portfolio.

The Company does not typically adjust prices obtained from pricing services. In accordance with accounting guidance regarding fair

value measurements, the Company’s service providers maximize the use of observable inputs ensuring that unobservable inputs are

used only when observable inputs are not available.

The following table presents the Company’s investments that are measured at fair value on a recurring basis as well as the carrying

amount of these investments as of December 31, 2015 by level within the fair value hierarchy:

Quoted Prices in Significant

Active Markets Other Significant

for Identical Observable Unobservable

Assets Inputs Inputs

2015 (Level 1) (Level 2) (Level 3) Total

U.S. government and government agency securities $460,573 $22,875 - $483,448

Non-U.S. government and government agency securities - 118,649 - 118,649

Municipal securities - 91,561 - 91,561

Corporate securities - 1,582,790 1,000 1,583,790

Bank loans - 226,342 222,062 448,404

U.S. asset-backed securities - 575,575 30,037 605,612

U.S. mortgage-backed securities - 1,089,388 5,116 1,094,504

Total fixed maturity securities 460,573 3,707,180 258,215 4,425,968

Equity securities 194,876 5,848 - 200,724

Short term investments - 3,979 - 3,979

$655,449 $3,717,007 $258,215 $4,630,671

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

20

The following table presents the Company's investments that are measured at fair value on a recurring basis as well as the carrying

amount of these investments as of December 31, 2014 by level within the fair value hierarchy:

Quoted Prices in Significant

Active Markets Other Significant

for Identical Observable Unobservable

Assets Inputs Inputs

2014 (Level 1) (Level 2) (Level 3) Total

U.S. government and government agency securities $283,252 $77,019 - $360,271

Non-U.S. government and government agency securities - 108,077 - 108,077

Municipal securities - 89,185 - 89,185

Corporate securities - 1,331,957 980 1,332,937

Bank loans - 188,998 241,377 430,375

U.S. asset-backed securities - 629,027 4,616 633,643

U.S. mortgage-backed securities - 1,081,844 7,863 1,089,707

Total fixed maturity securities 283,252 3,506,107 254,836 4,044,195

Equity securities 172,992 33,873 225 207,090

Short term investments - 40,877 - 40,877

$456,244 $3,580,857 $255,061 $4,292,162

A description of the valuation techniques and inputs used to determine fair values of investments carried at fair value, as well as the

classification of each investment type in the fair value hierarchy is detailed below.

The Company’s investments classified as Level 1 include U.S. government and government agency securities and equity securities

for which fair value is based on quoted market prices in active markets which is defined by the Company’s pricing service as a

security that has traded in the previous seven days.

The Company’s Level 2 securities primarily consist of securities that are valued using models or other valuation techniques. These

models are industry standard models that take into account various assumptions including time value, yield curve, prepayments

speeds, default rates, loss severity, current market and contractual prices for the underlying securities as well as other economic data.

The majority of these assumptions are observable in the marketplace and this category includes some U.S. and Non-U.S.

government and government agency securities, municipal securities, corporate securities, bank loans, U.S. asset-backed securities,

U.S. mortgage-backed securities, equity securities and short term investments.

The Company’s investments classified as Level 3 consist of bank loans, certain corporate securities, U.S. asset and mortgage-backed

securities and equity securities. Level 3 securities are valued using non-binding broker quotes and other third party pricing sources,

without modification. Consequently, the information about significant unobservable inputs used in the fair value measurement as

required by U.S. GAAP are not disclosed.

The Company’s other investments include investments in closed-end limited partnerships that invest primarily in private commercial

real estate debt in North America and Europe (“Real Estate Debt Funds”). In May, 2015, the Company also invested in a limited

partnership fund registered in Cayman Islands called China Momentum Fund, L.P. (CMF). The fair value of these investments is

estimated using the net asset value (NAV) as provided by the general partners or investment managers. As the NAV obtained from

the general partners or investment managers lags by one quarter as of the measurement date, the Company considers any adjustment

to the most recent NAV such as capital calls, distributions, redemptions and all other information available to the Company.

The Real Estate Debt Funds invest principally in senior and subordinated instruments, including mortgages, B-notes and mezzanine,

senior and bridge loans related to real estate-related assets. These investments are not allowed to be redeemed, transferred or resold

and have an estimated term of 3 to 7 years. CMF invests primarily in portfolio of companies engaged in consumer, financial or

industrial undertakings domiciled in China, Hong Kong, Macau and/or Taiwan. The investment period for CMF commenced on

August 15, 2013 and with an estimated term of 10 years unless sooner dissolved. As of December 31, 2015 and 2014, Real Estate

Debt Funds and CMF had a balance of $87,366 and $43,760, respectively, recorded as other investments in the consolidated balance

sheets.

There have been no significant changes in the Company’s use of valuation techniques or related inputs nor have there been any

transfers between Level 1 and Level 2 during the years ended December 31, 2015 and 2014, respectively. The transfers from Level 2

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

21

to Level 3 during the years ended December 31, 2015 and 2014 reflect low level of trading activity in certain fixed maturity

securities while the transfers of fixed maturity securities from Level 3 to Level 2 that occurred during the same periods reflect higher

reliance on observable inputs. The Company’s policy is to recognize transfers in and out of the fair value hierarchy measurement

levels as of the date of the actual transfer.

As of December 31, 2015 and 2014, the Company’s Level 3 investments represented 5.6% and 5.9% of its total investments

measured at fair value, respectively.

Level 3 Gains and Losses

The table below presents assets that are measured at fair value on a recurring basis as of December 31, 2015 using significant

Level 3 inputs:

U.S. asset- U.S. mortgage-

Equity Corporate backed backed

Year ended December 31, 2015 Bank loans securities securities securities securities Total

Balance at beginning of year $241,377 $225 $980 $4,616 $7,863 $255,061

Realized gains (losses) (1,198) (7) - - 130 (1,075)

Unrealized gains (losses) 459 15 17 (212) (127) 152

Purchases 75,442 - - 22,065 6,018 103,525

Sales (75,744) (233) 1 (772) (8,755) (85,503)

Amortization 837 - 2 11 (13) 837

Transfer into Level 3 4,609 - - 8,708 - 13,317

Transfer out of Level 3 (23,720) - - (4,379) - (28,099)

Balance at end of the year $222,062 $0 $1,000 $30,037 $5,116 $258,215

The table below presents assets that are measured at fair value on a recurring basis as of December 31, 2014 using significant

Level 3 inputs:

U.S. asset- U.S. mortgage-

Equity Corporate backed backed

Year ended December 31, 2014 Bank loans securities securities securities securities Total

Balance at beginning of the period $132,831 - $77 $50,571 $3,567 $187,046

Realized gains 26 - 4 - - 30

Unrealized gains (losses) (2,593) (15) (2) (14) 86 (2,538)

Purchases 174,926 240 980 4,629 6,180 186,955

Sales (71,796) - (79) - (1,099) (72,974)

Amortization 698 - - 1 12 711

Transfer into Level 3 25,018 - - - - 25,018

Transfer out of Level 3 (17,733) - - (50,571) (883) (69,187)

Balance at end of the year $241,377 $225 $980 $4,616 $7,863 $255,061

Change in unrealized loss for the year included in earnings for assets held at the end of December 31, 2015 and 2014 amounted to

$669 and $1,795, respectively.

Financial Instruments not Carried at Fair Value

U.S. GAAP requires that entities disclose the fair value of all of their financial instruments whether or not carried at fair value in

the financial statements.

On May 4, 2010, the Company issued $250,000 of Senior Notes bearing an annual interest rate of 8.5%, payable semi -annually in

arrears on May 15 and November 15 of each year, beginning November 15, 2010. As of December 31, 2015 and December 31,

2014, the fair value of the Senior Notes was $287,500 (carrying value – $247,992) and $300,948 (carrying value - $247,629),

respectively. The fair value is determined using a non-binding broker quote which is considered Level 3 in the fair value hierarchy.

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

22

Consequently, the information about significant unobservable inputs used in the fair value measurement as required by U.S. GAAP

is not disclosed.

As of December 31, 2015, the Company has an outstanding loan of $100,000 owed to Federal Home Loan Bank Boston (“FHLB”)

(see Note 14). As of December 31, 2015, the carrying value of the short-term loan of $100,000 approximates fair value and is

classified as Level 2 in the fair value hierarchy.

9. Reserves for losses and loss adjustment expenses

Reserves for losses and loss adjustment expenses are based in part upon the estimation of case reserves reported from brokers,

insureds and ceding companies. The Company also uses statistical and actuarial methods to estimate ultimate expected losses and

loss adjustment expenses. The period of time from the occurrence of a loss, the reporting of a loss to the Company and the

settlement of the Company’s liability may be several months or years. During this period, additional facts and trends may be

revealed. As these factors become apparent, case reserves will be adjusted, sometimes requiring an increase or decrease in the

overall reserves of the Company, and at other times requiring a reallocation of incurred but not reported reserves to specific case

reserves. These estimates are reviewed regularly, and such adjustments, if any, are recorded in earnings in the period in which they

become known. While management believes that it has made a reasonable estimate of ultimate losses, there can be no assurances

that ultimate losses and loss expenses will not exceed the total reserves.

The following table represents the activity in the reserve for losses and loss adjustment expenses for the years ended December 31,

2015 and 2014, respectively:

2015 2014

Gross reserves for losses and loss adjustment expenses, beginning of year $2,838,158 $2,181,812

Less reinsurance recoverable balances, beginning of year 693,298 601,352

Net reserves for losses and loss adjustment expenses, beginning of year 2,144,860 1,580,460

Increase (decrease) in net losses and loss adjustment expenses incurred in

respect of loses occurring in:

Current year 1,000,318 1,024,508

Prior years 9,900 52,766

Total incurred losses and loss adjustment expenses 1,010,218 1,077,274

Less net losses and loss adjustment expenses paid in respect of losses

occurring in:

Current year 130,449 146,129

Prior years 586,252 358,467

Total net paid losses 716,701 504,596

Net foreign currency gain on reserve for losses and loss adjustment expenses (17,623) (8,278)

Net reserve for losses and loss adjustment expenses, end of year 2,420,754 2,144,860

Plus reinsurance recoverable balances, end of year 776,787 693,298

Gross reserve for losses and loss adjustment expenses, end of year $3,197,541 $2,838,158

The underlying reasons for prior year unfavorable development of $9,900 for the year ended December 31, 2015 included:

Net unfavorable loss reserve development for our U.S. segment of $7,800, of which $13,200 was recognized in our

IronPro line of business, primarily on the 2013 and 2014 accident years, and $12,800 in our aviation line of business,

primarily on the 2013 and 2014 accident years, due to higher than expected reported claim activity. This was partially

offset by favorable loss reserve development due to better than expected reported claim activity in the following lines of

business and accident years: $11,300 in our U.S. property line of business (2013 and 2014 accident years) and $10,400 in

our environmental line of business (2012 and 2013 accident years); and

Ironshore Inc.

Notes to consolidated financial statements (Expressed in thousands of U.S. dollars, except share data)

23

Net unfavorable loss reserve development for our Bermuda segment of $1,400, of which was $6,200 was recognized in

our Bermuda property line of business, primarily on the 2013 and 2014 accident years, due to higher than expected

reported claim activity. This was partially offset by favorable development due to better than expected reported claim

activity of $4,700 in our Corporate Deals line of business, primarily on the 2013 and 2014 accident years.

The underlying reasons for prior year unfavorable development of $52,766 for the year ended December 31, 2014 included:

Net unfavorable loss reserve development for our U.S. segment of $43,700, of which $74,700 was recognized in our

casualty line of business, primarily on the 2009 to 2013 accident years, due to higher than expected reported claim

activity. This was partially offset by favorable loss reserve development due to better than expected reported claim

activity in the following lines of business and accident years: $11,600 in our U.S. property line of business (2011 to 2013

accident years), $9,700 in our political risk line of business (2011 to 2013 accident years), $4,000 in our IronPro line of

business (2009 and 2010 accident years), and $3,200 in our IronHealth line of business (2011 accident year); and

Net unfavorable loss reserve development for our International segment of $9,400, of which $14,000 was recognized in

our marine line of business due to higher than expected reported claim activity, primarily on the 2010 to 2012 accident

years. This was partially offset by favorable loss reserve development due to better than expected reported claim activity

of $4,700 in our liability line of business primarily on the 2009 and 2011 accident years.

The Company has written an increasing volume of casualty business in recent years which adds significant variability to

management’s estimates because of the longer tail nature of the risks.

As of December 31, 2015 and 2014, reinsurance recoverable and reserve for losses and loss adjustment expenses include amounts

of $25,506 and $18,784, respectively, related to the pre-acquisition business of Ironshore Indemnity and Ironshore Specialty that