IPO Readiness - Britcham Brasil PR meetings and marketing roadshow 1 week - All documents completed...

22

IPO Readiness Sao Paulo, May 5 th 2009 Sao Paulo, May 5 2009

Transcript of IPO Readiness - Britcham Brasil PR meetings and marketing roadshow 1 week - All documents completed...

IPO ReadinessSao Paulo, May 5th 2009Sao Paulo, May 5th 2009

Access to global institutional investor base

Domestic

market

US Regional institutional

Middle East US

Asia Eastern Europe

2

Global institutional investor base

US institutional investors

Regional institutional and retail investors

Asia Eastern Europe

Europe UK

London Stock Exchange - key statistics

Total companiesDomestic: 2,345International: 618

Market capitalisation Main Market: UK listed: US$1,732bnInternational listed: US$2,090bn

3

Source: London Stock Exchange statistics – March 2009

Used currency exchange as of 14/04/09: GBP/USD 1.48

International listed: US$2,090bnAIM: US$57bn

Turnover value (Jan-Dec 2008) Main Market: 4,587bnAIM: US$73bn

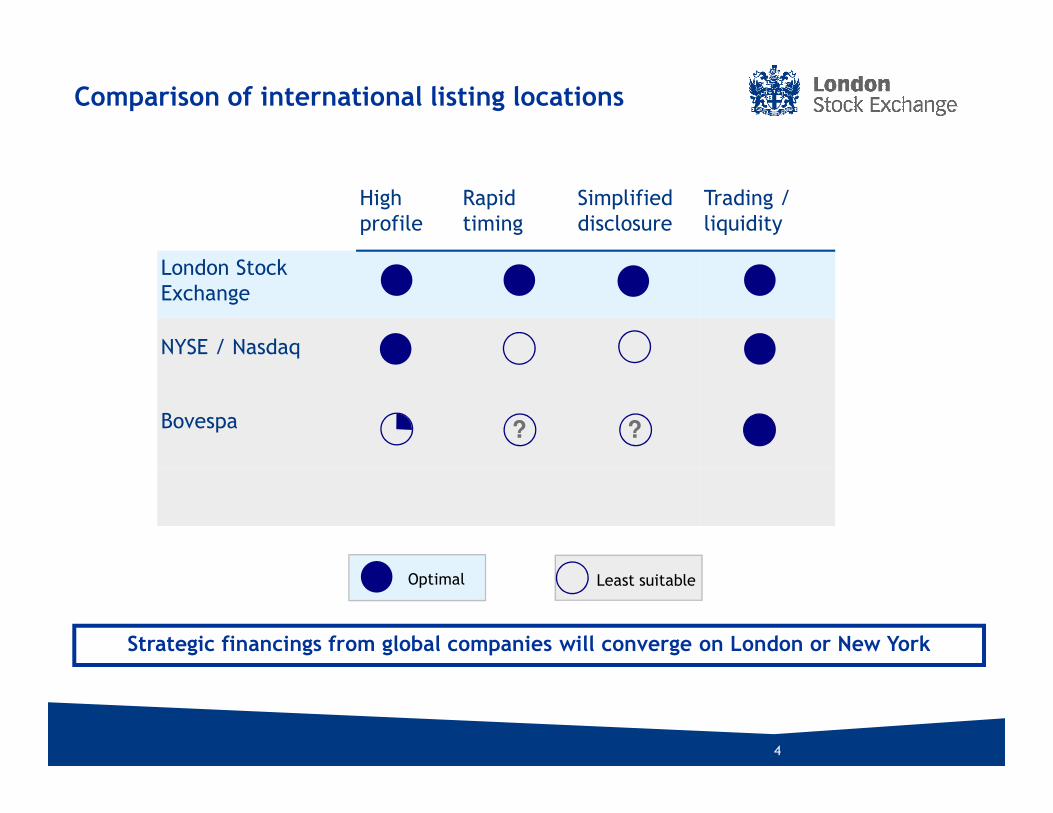

Comparison of international listing locations

High profile

Rapid timing

Simplified disclosure

Trading / liquidity

London Stock Exchange

NYSE / Nasdaq

4

Optimal Least suitable

Bovespa

Strategic financings from global companies will converge on London or New York

? ?

An intelligent approach to regulation

Balance Competing Needs

Companies Investors

Minimise bureaucracyand cost

Maximise protection

5

Needs

US

UKRanked first in corporate governance standards by GMI, Deminor and Davis Global Advisors

Increased cost of compliance and risk premium (Financial Executive & Korn Ferry Surveys)

Principles based -“comply or explain”

Rules based -prescriptive and expensive

Main features

Setting the standard for excellence Where ideas take off

Highest standards of regulation

Investable indices

Different entry requirements

Flexible regulatory regime

6

Investable indices

Largest institutional investor base

Deepest capital pool

Most liquid trading platforms

Enhanced profile and status

Flexible regulatory regime

Specialist small-cap institutional & retail investor base

Bespoke indices

Preparing for the IPO

� Pre-IPO preparation

� Timetable

� Costs

� Alternative sources of finance

� Timing is key

8

� Pricing your IPO

� Following the IPO

� Choosing your advisers

� Role of the NOMAD

� Continuing obligations

Pre-IPO preparation

■ Start early!

- Appoint the right team to manage the process

■ Get your house in order

- Develop robust business plan, be clear about your objectives

- Review internal controls and financial reporting

- Consider ownership and tax issues

- Complete any planned strategic initiatives

- Adopt best-practice corporate governance standards (eg Combined Code)

9

■ Talk to your existing advisers

- Identify issues early on

- Think about advisers you will need to appoint

- Understand the IPO process and manage expectations

■ Other considerations

- Pre-IPO fundraising?

An IPO is not just a transaction, but an opportunity to transform your business

Timetable

Typical time frame to flotation on AIM is 3 to 4 months from the appointment of the advisory team

Weeks before Admission

12 – 16 weeks

- Appoint and instruct advisers

- Agree timetable to Admission

- Initiate due diligence (Long Form and Working Capital Reports, Legal Due Diligence)

6 – 8 weeks

- Review any problem areas that have arisen

- First draft Admission Document

10

- First draft Admission Document

- First draft other required documents

2 – 4 weeks

- Drafting meetings

- Complete due diligence

- PR meetings and marketing roadshow

1 week

- All documents completed and approved

- Pricing and allocation

Costs

■ The main cost of an IPO is commission on money raised (typically 4% - 6%)

■ Ongoing costs of listing on AIM (excluding accounting and legal) approx USD150,000 p.a.

■ Small fundraisings and more complex IPOs are proportionally more expensive

■ While listing can be expensive, the benefits to a company, its employees and shareholders should outweigh the costs

■ Fees may form part of the adviser selection process but should not be the dominant consideration – simply opting for the lowest fees may compromise the success of the IPO

11

consideration – simply opting for the lowest fees may compromise the success of the IPO

Consider all options before going down IPO route

■ An IPO can bring significant benefits to a company

- Access to capital at relatively low cost

- Opportunity to realise value for shareholders and employees

- Enhanced corporate profile

■ But the benefits are not without cost

12

■ But the benefits are not without cost

- Ongoing compliance requirements

- Dilution of control

- Pressure of life in the public eye – the market can be unforgiving

- Management inflexibility and short-term decision making

The attractions of an IPO are not without cost. Management must consider all options to ensure

that an IPO is right for the company

Alternative sources of finance

■ Private placing

Pros

- Relatively quick process

- Fewer disclosure, due diligence or regulatory requirements

- Selective institutional investors or HNWI

■ Private equity or venture capital

Cons

- Investor pool may be limited and lower funds raised

- Less competitive pricing – illiquidity discount

- Likely to IPO anyway to provide exit route

Alternatives depend on stage in the development cycle and company objectives:

13

Pros

- Availability of further finance

- Provision of management expertise

- Likely to support a MBO or MBI

■ Debt financing

Pros

- Flexible structures e.g. PIK, mezzanine

- Optimise capital structure to enhance ROCE

- Less dilution

Cons

- Dilution of control

- Require exit route (IPO or sale)

- Cost – target IRR 30%

Cons

- Increased gearing - risky if interest rates are rising

- Restrictive covenants

- May be difficult in current market

Timing is key

■ State of the market

- Beyond the control of the company

- Success at IPO is highly dependent on investor sentiment

- Windows of opportunity brief in volatile markets

- Be ready!

■ Performance of the business

- Largely under the control of the company

- Track record of earnings pointing to a growth trend, opportunities, execution?

Visibility of future earnings?

14

- Visibility of future earnings?

■ Company strategy

- Investors are looking for a clear strategy and medium term growth prospects

- Can the company deliver?

■ IPO’s are time consuming and distracting so ensure business is not damaged by the process

Better to be ready early – be prepared for the window of opportunity

Pricing your IPO – A Technical Starting Point

• Initial valuation based on the following:

• Peer group analysis

• Precedent transactions (IPO & M&A)

• Discounted cashflow

•Sum of the parts

Initial Valuation Range Three phased marketing and price

discovery approach

Not a simple process:

• What is the peer group? Direct comparables are rare

• Which ratios? Which industry? Blended multiples?

•Environment – tax, structures

• Subjective and objective measures

•The bookbuilding process

15

Optional

Pre-Marketing

Orders &

Bookbuild

PRICE

discovery approach

Phase I – Educate potential investors

Phase II – Target and contact interested investors

Phase III – Company management roadshow

Pricing your IPO – Supply and Demand

• Pricing driven by far more than simply a desktop valuation

• Pricing ultimately driven by supply of and demand for available shares

- Supply

• Funding needs of the company

• Selling shareholders

16

• Demand

• Oversubscribed issue

• Better price although an uplift in pricing best achieved if issue marketed with arange rather than fixed price

• Undersubscribed offer

• A cut in the price often required to meet minimum increase fundraise requirement

Strike a balance to ensure fair pricing

Pricing your IPO – Factors Affecting Price

•Fund Factors

– Availability of funds (redemptions / need to sell)

– The psychology of the fund manager is key. Ultimatelyhe / she will invariably seek the lowest entry price

– Balance of sector / country / exchange risk

•Technical Factors

– Perceived after-market liquidity

Macro factors

� Market conditions

� Economic sentiment

Company factors

� Credibility of story / management

� Track record

� Management remuneration arrangements

17

Need to understand various factors affecting your ultimate valuation

– Perceived after-market liquidity

• price of pre-IPO rounds

• which market?

� Management remuneration arrangements

� Risk

Following the IPO

– An IPO is a beginning not a end

• A strongly rising share price post-IPO offers opportunities

• A declining share price restricts and frustrates

– Role of the equity research analyst key

• In UK, an IPO is accompanied by pre IPO research

• Use the research as a medium to sell your story

• Resist the urge to overstate projected financial performance

–Profits warnings early in a company’s public life can be disastrous

18

–Profits warnings early in a company’s public life can be disastrous

• Under-promise and over-perform

– Unless you are selling shares in an IPO, the downside from over-pricing an issue will vastly outweigh the damage caused by under-pricing it

Choosing your advisers

– Your advisers play a central role in your company’s IPO - and beyond

– Key advisers:

- NOMAD/Sponsor and Broker

- Lawyers

- Reporting Accountants

– Key questions to bear in mind when appointing your advisers:

19

– Key questions to bear in mind when appointing your advisers:

- Do they understand my business?

- Do they have experience with companies in the same sector?

- Do they share my vision for the company and understand where I want to take it?

- Do they have a proven track record of getting the deal done?

Role of the Nominated Adviser (NOMAD)

– AIM is an ‘exchange regulated’ market

- The NOMAD plays a crucial role in upholding regulatory requirements

- AIM has rules for Companies as well as for NOMADS

– NOMAD’s role is to advise company’s board regarding their responsibilities/obligations to their shareholders, investors and London Stock Exchange

- Assess a company’s suitability and appropriateness for admission to AIM

- Perform due diligence on company and its management

- Project-manage IPO

20

- Project-manage IPO

- Assist a company to meet its continuing obligations once admitted

– Choose a NOMAD with relevant transaction and sector experience

– NOMAD may also act as broker to an company on AIM

– All companies listed on AIM must retain a NOMAD at all times

Indicative Timetable

Month 1 Month 2 Month 3 Month 4

Financial due diligence, long form and short form reports

GENERAL

ACCOUNTANTS

Agree capital and group

structure requirements

and board structure considered

including non-executive search

Agree

shareholder

objectives

Draft Memorandum

andUndertake verification exercise

Tax planning

commencesWorking capital report

Dealings

commence

Final

-Long form report

-Short form report

-Working capital report

Final verification

Analysis of share optionSchemes and remunerationpackages

Submission of tax clearance

Discussions with existing shareholders

Preparation Long Form and Working Capital

Reports

Draft Memorandum

and Undertake verification exercise

Agree

shareholder

objectives

Agree capital and group

structure requirements

and board structure considered

including non-executive search

Tax planning

commences

Analysis of share optionSchemes and remunerationpackages

Working capital report

21

LEGAL

DOCUMENTATION

MARKETING

DISTRIBUTION Preliminarypricing

Legal Due Diligence including competent person’s

report if applicable

and

Articles of Association

Drafting /Placing

Agreement, Board

Minutes and other legal

documents

Undertake verification exercise

Prepare pricing model

Institutional

meetings

arrangedPreparation of institutional presentation

Prospectus

issued

Final verification

notes issued

Pricing

Sharesplaced

Brokers research issued

Impact DayRoadshow

and one to one

presentations

Final version of

legal reports

AppointLegalAdviser

Analysts visitcompany

Appoint PRconsultants

and

Articles of Association

Undertake verification exercise

Prospectus cover and other design

Pathfinderissued

Drafting of Prospectus

Resolve any preliminaryRegulatoryissues

Prospectus cover and other design

Contact

Graham Dallas

Head of business development – Americas

+44 (0)20 7797 4055

22

Anne Moulier

Business Development Manager – Americas

+44 (0) 20 7797 4584

Website: www.londonstockexchange.com