INVESTORS CALL PRESENTATION - Roustroust.com/uploads/investor-relations/2014 Q4 and FY...

57

INVESTORS CALL PRESENTATION ROUST CORPORATION GROUP (FORMER CEDC GROUP) FULL YEAR ENDED 31 DECEMBER, 2014 Investor Relations contact: [email protected]

Transcript of INVESTORS CALL PRESENTATION - Roustroust.com/uploads/investor-relations/2014 Q4 and FY...

INVESTORS CALLPRESENTATIONROUST CORPORATION GROUP (FORMER CEDC GROUP)

FULL YEAR ENDED 31 DECEMBER, 2014

Investor Relations contact:

FORWARD LOOKING STATEMENTS

© ROUST | CONFIDENTIAL INFORMATION 2

This presentation contains forward-looking statements based on ourexpectations and assumptions as of March 27, 2015. All forward-lookingstatements are expressly qualified in their entirety by the following cautionarystatements. Forward-looking statements involve known and unknown risks anduncertainties that may cause actual results, performance or events to differmaterially from those expressed or implied by the forward-looking statements.Forward-looking statements are not guarantees of future performance and unduereliance should not be placed on them.

Additional risk factors that may affect future results are contained in our Form10-K for the year ended December 31, 2014 and in our quarterly and currentreports. These risk factors expressly qualify all forward-looking statementscontained in this presentation and should be considered by the reader. Weundertake no obligation to publicly update or revise any forward-lookingstatements or to make any other forward-looking statements, whether as a resultof new information, future events or otherwise.

EXPLANATORY NOTE

On November 24, 2014 by filing of a certificate of amendment with the Secretary of State of the State of Delaware, CEDC changed its name from “Central European Distribution Corporation” to “Roust Corporation”.

On June 30, 2014 ROUST CORPORATION GROUP („ROUST”) acquired Roust Inc. from Roust Trading Limited ("RTL"), pursuant to a SPA, dated May 26, 2014.

Roust Inc. is a leading distributor of premium alcohol brands in Russia including Russian Standard Vodka, Gancia, Remy, Jägermeister and Concha Y Toro. The Roust Inc. transaction is accretive to our earnings and cash flows when measured under the Notes against the twelve month period ended March 31, 2014.

RTL is the sole shareholder of Roust Inc. and ROUST, therefore for accounting purposes, the acquisition was accounted for under the “as if pooling-of-interest” method of accounting applicable to the transfer of assets or exchange of equity interests between entities under common control. The Company has a retained deficit due to the requirement to charge the acquisition price of Roust Inc. directly to equity. The Company received an fairness opinion from a U.S. investment bank as the basis of the $250M purchase price.

As a result of acquisition under common control ROUST is recasting its historical financial statements for the year ended December 31, 2013, published on March 19, 2014.

In accordance with Accounting Standard Codification Topic 805-50, common control of Roust Inc. and ROUST is deemed to have existed since June 5, 2013, the date that RTL acquired ROUST. As a result, the subsequent transfer of the assets and liabilities was accounted for “as if pooling-of-interest” at Roust Inc. historical cost at June 5, 2013, including necessary consolidation adjustments. Accordingly, the consolidated financial statements of ROUST beginning as of June 5, 2013 have been recast to include Roust Inc. balance sheet, results of operations and cash flows.

As a result of the application of the accounting guidelines summarized above, the presentation of ROUST historical financial information herein is not consistent with certain historical financial information as previously reported. As discussed further in Note 4 in the 10-K, the presentation of certain previously reported amounts included herein has been recast to conform to the current presentation.

© ROUST | CONFIDENTIAL INFORMATION 3

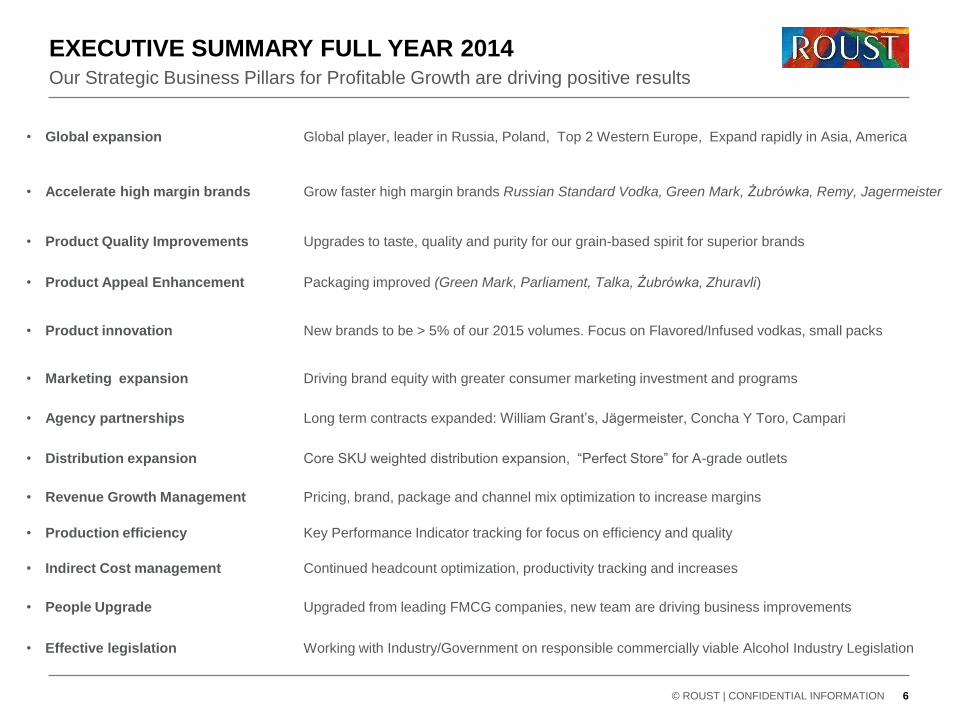

EXECUTIVE SUMMARY FULL YEAR 2014

• Roust now one of the largest global alcohol companies selling 300Million litres per year, expanding

rapidly globally, leading in Russia, Poland, Hungary, Russia’s largest vodka exporter

• Our Strategy is working to drive business improvements and strong financial results:

a) Our Pro Forma Underlying EBITDA reached $122.8M, $+15M vs 2013

b) Global revenue per case and margin growths continue from ‘Revenue Growth Management’

c) Innovation accelerates: further focus on the very profitable vodka flavors and small packs

• Outstanding Polish business performance – Roust is now the Market leader in volume and value!

• The Russian economy/currency has negative impact; Roust performs solidly staying market leader

a) Roust Inc. – integration progressing and succeeding with healthy EBITDA

b) Excise increases in 2014 in Russia and Poland led to category decline, but our core brand share is increasing

c) No excise increase in Russia/Poland 2015; expecting volume growth in 2015

• Strong International growth in markets such as Germany, UK, France, Baltics, Japan, Australia

• Excellent performance in Hungary with record market share and profit growth

• Ukraine business remains stable and under control, no material losses

• Significantly more potential in the business for growth and cost optimization

© ROUST | CONFIDENTIAL INFORMATION 4

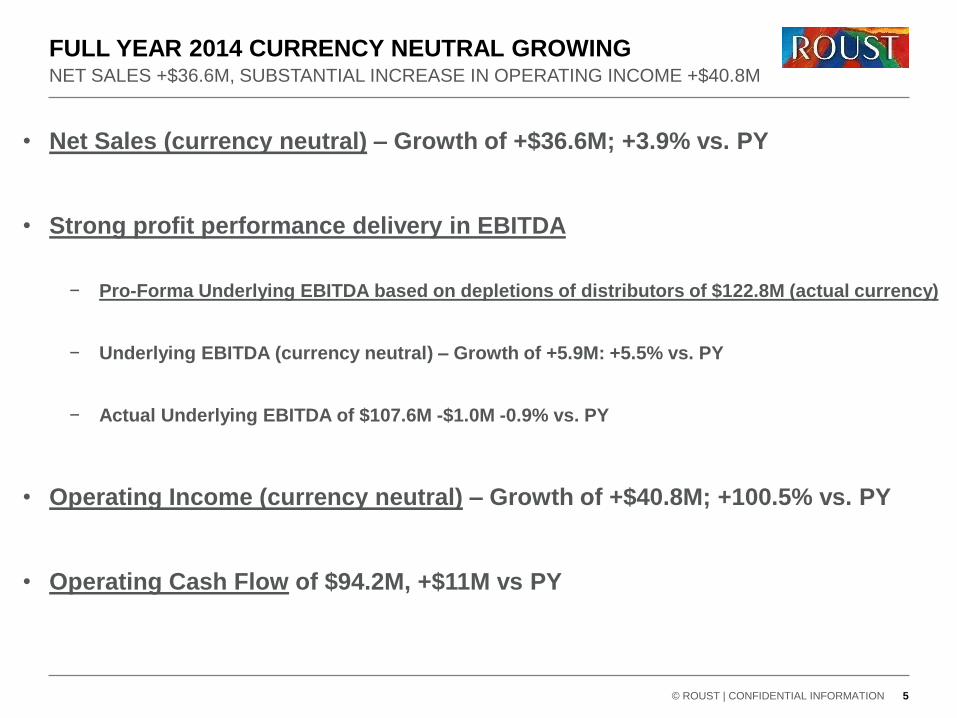

FULL YEAR 2014 CURRENCY NEUTRAL GROWING

© ROUST | CONFIDENTIAL INFORMATION 5

NET SALES +$36.6M, SUBSTANTIAL INCREASE IN OPERATING INCOME +$40.8M

• Net Sales (currency neutral) – Growth of +$36.6M; +3.9% vs. PY

• Strong profit performance delivery in EBITDA

− Pro-Forma Underlying EBITDA based on depletions of distributors of $122.8M (actual currency)

− Underlying EBITDA (currency neutral) – Growth of +5.9M: +5.5% vs. PY

− Actual Underlying EBITDA of $107.6M -$1.0M -0.9% vs. PY

• Operating Income (currency neutral) – Growth of +$40.8M; +100.5% vs. PY

• Operating Cash Flow of $94.2M, +$11M vs PY

© ROUST | CONFIDENTIAL INFORMATION 6

Our Strategic Business Pillars for Profitable Growth are driving positive results

EXECUTIVE SUMMARY FULL YEAR 2014

• Global expansion Global player, leader in Russia, Poland, Top 2 Western Europe, Expand rapidly in Asia, America

• Accelerate high margin brands Grow faster high margin brands Russian Standard Vodka, Green Mark, Żubrówka, Remy, Jagermeister

• Product Quality Improvements Upgrades to taste, quality and purity for our grain-based spirit for superior brands

• Product Appeal Enhancement Packaging improved (Green Mark, Parliament, Talka, Żubrówka, Zhuravli)

• Product innovation New brands to be > 5% of our 2015 volumes. Focus on Flavored/Infused vodkas, small packs

• Marketing expansion Driving brand equity with greater consumer marketing investment and programs

• Agency partnerships Long term contracts expanded: William Grant’s, Jägermeister, Concha Y Toro, Campari

• Distribution expansion Core SKU weighted distribution expansion, “Perfect Store” for A-grade outlets

• Revenue Growth Management Pricing, brand, package and channel mix optimization to increase margins

• Production efficiency Key Performance Indicator tracking for focus on efficiency and quality

• Indirect Cost management Continued headcount optimization, productivity tracking and increases

• People Upgrade Upgraded from leading FMCG companies, new team are driving business improvements

• Effective legislation Working with Industry/Government on responsible commercially viable Alcohol Industry Legislation

BREAKING NEWS: MARKET LEADERSHIP IN POLAND!

• NUMBER 1 Vodka Player in Poland in terms of volume & value share!

− In January 2015 we became TOP VODKA PLAYER in POLAND with 33.6% volume market share

− Further strengthening leader’s position with 35.3% share in February 2015

Volume market share, +4.0 pp.* above our main competitor Stock Spirits

In February we became the value share market leader with 34.2% (+2.3 pp* above Stock)

• ŻUBRÓWKA’S SUCCESS!

− 5.2M nine-liter cases sold in 2014

− No 1 among Polish vodkas

− No 7 vodka brand worldwide

− No 40 largest alcohol brand worldwide

• FASTEST GROWING BRAND among

TOP50 alcohol brands worldwide

(29.5% growth year-on-year)!**

© ROUST | CONFIDENTIAL INFORMATION 7

* Nielsen Report for February 2015 ** According to IMPACT magazine, February 2015

GENERAL BUSINESS OVERVIEW

DESPITE RUSSIAN ECONOMY CHALLENGES WE HAVE

SIGNIFICANT POSITIVE NEWS IN RUSSIA

• Positive news

− No excise increases in 2015, 2016 – Vodka shelf price increases likely below inflation

− Roust premium brands Russian Standard Vodka, Remy, Jägermeister continued to

show growth in Q4 2014 despite excise changes

− Industry legislation to reduce and control key chain discounts is progressing quickly

and expected in 2015 – benefits to Roust margins

− The Government has enacted new laws to reduce the black market including

confiscating equipment, greater fines

− Roust has already reduced Russia cost base $20M in the last 18 months

• Economic issues

− U.S. dollar exchange rate has depreciated 77% in 2014

− Consumer goods inflation 2015 forecast at 12 to 15%

− GDP forecast to fall in 2015 by 1.5 to 3%

− Alcohol + vodka market was still declining in 2014

© ROUST | CONFIDENTIAL INFORMATION 9

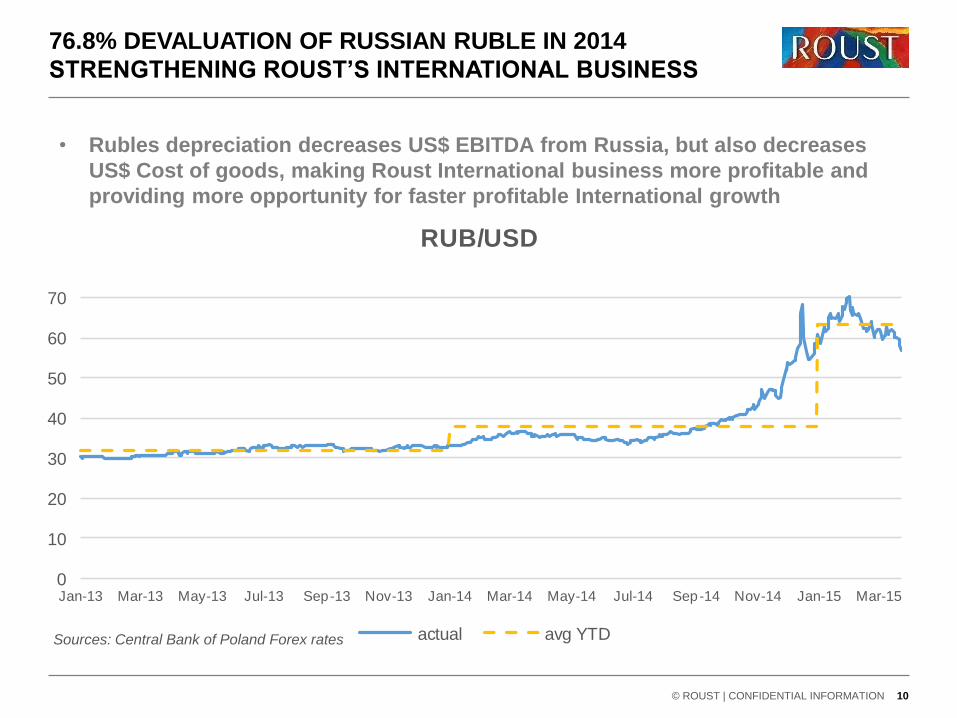

76.8% DEVALUATION OF RUSSIAN RUBLE IN 2014

STRENGTHENING ROUST’S INTERNATIONAL BUSINESS

© ROUST | CONFIDENTIAL INFORMATION 10

Sources: Central Bank of Poland Forex rates

• Rubles depreciation decreases US$ EBITDA from Russia, but also decreases

US$ Cost of goods, making Roust International business more profitable and

providing more opportunity for faster profitable International growth

0

10

20

30

40

50

60

70

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

RUB/USD

actual avg YTD

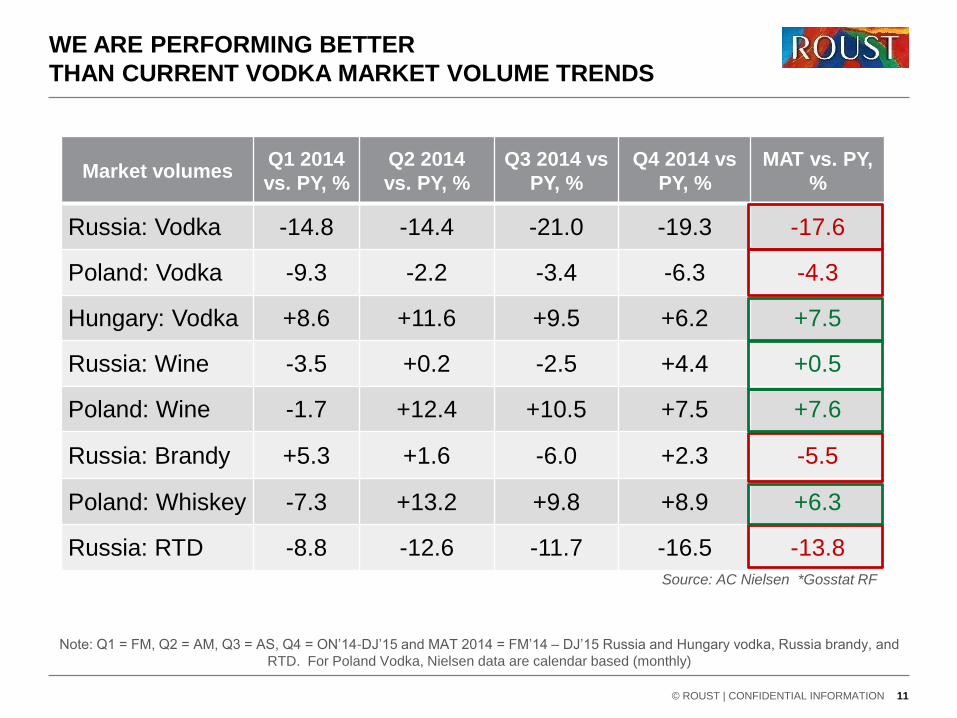

WE ARE PERFORMING BETTER

THAN CURRENT VODKA MARKET VOLUME TRENDS

© ROUST | CONFIDENTIAL INFORMATION 11

Market volumesQ1 2014

vs. PY, %

Q2 2014

vs. PY, %

Q3 2014 vs

PY, %

Q4 2014 vs

PY, %

MAT vs. PY,

%

Russia: Vodka -14.8 -14.4 -21.0 -19.3 -17.6

Poland: Vodka -9.3 -2.2 -3.4 -6.3 -4.3

Hungary: Vodka +8.6 +11.6 +9.5 +6.2 +7.5

Russia: Wine -3.5 +0.2 -2.5 +4.4 +0.5

Poland: Wine -1.7 +12.4 +10.5 +7.5 +7.6

Russia: Brandy +5.3 +1.6 -6.0 +2.3 -5.5

Poland: Whiskey -7.3 +13.2 +9.8 +8.9 +6.3

Russia: RTD -8.8 -12.6 -11.7 -16.5 -13.8

Source: AC Nielsen, *Gosstat RF

Note: Q1 = FM, Q2 = AM, Q3 = AS, Q4 = ON’14-DJ’15 and MAT 2014 = FM’14 – DJ’15 Russia and Hungary vodka, Russia brandy, and

RTD. For Poland Vodka, Nielsen data are calendar based (monthly)

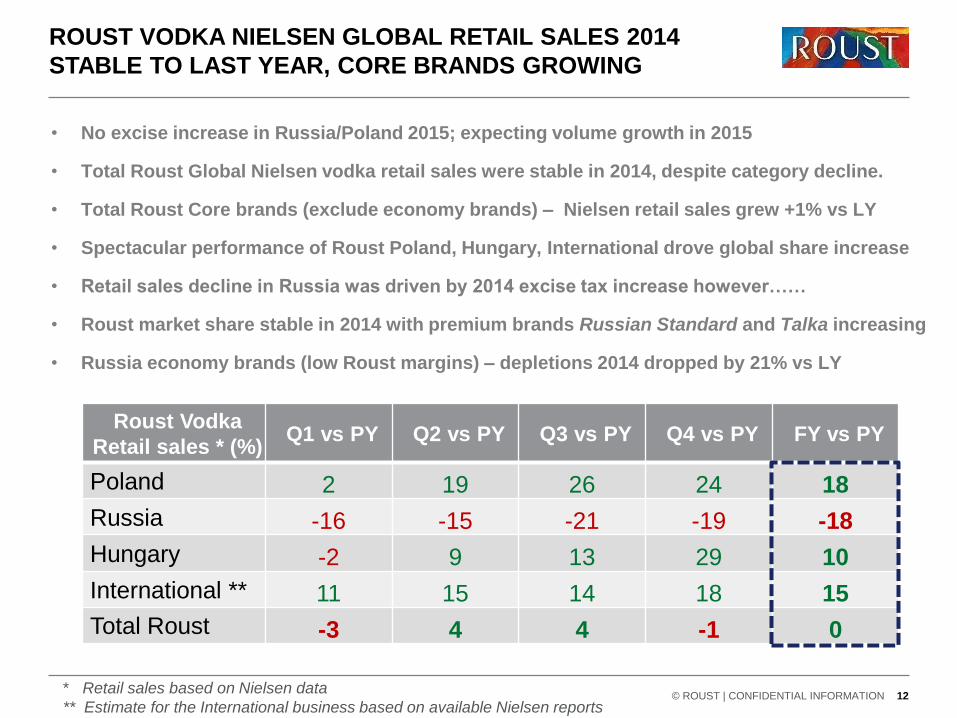

ROUST VODKA NIELSEN GLOBAL RETAIL SALES 2014

STABLE TO LAST YEAR, CORE BRANDS GROWING

© ROUST | CONFIDENTIAL INFORMATION 12

• No excise increase in Russia/Poland 2015; expecting volume growth in 2015

• Total Roust Global Nielsen vodka retail sales were stable in 2014, despite category decline.

• Total Roust Core brands (exclude economy brands) – Nielsen retail sales grew +1% vs LY

• Spectacular performance of Roust Poland, Hungary, International drove global share increase

• Retail sales decline in Russia was driven by 2014 excise tax increase however……

• Roust market share stable in 2014 with premium brands Russian Standard and Talka increasing

• Russia economy brands (low Roust margins) – depletions 2014 dropped by 21% vs LY

Roust Vodka

Retail sales * (%)Q1 vs PY Q2 vs PY Q3 vs PY Q4 vs PY FY vs PY

Poland 2 19 26 24 18

Russia -16 -15 -21 -19 -18

Hungary -2 9 13 29 10

International ** 11 15 14 18 15

Total Roust -3 4 4 -1 0

* Retail sales based on Nielsen data

** Estimate for the International business based on available Nielsen reports

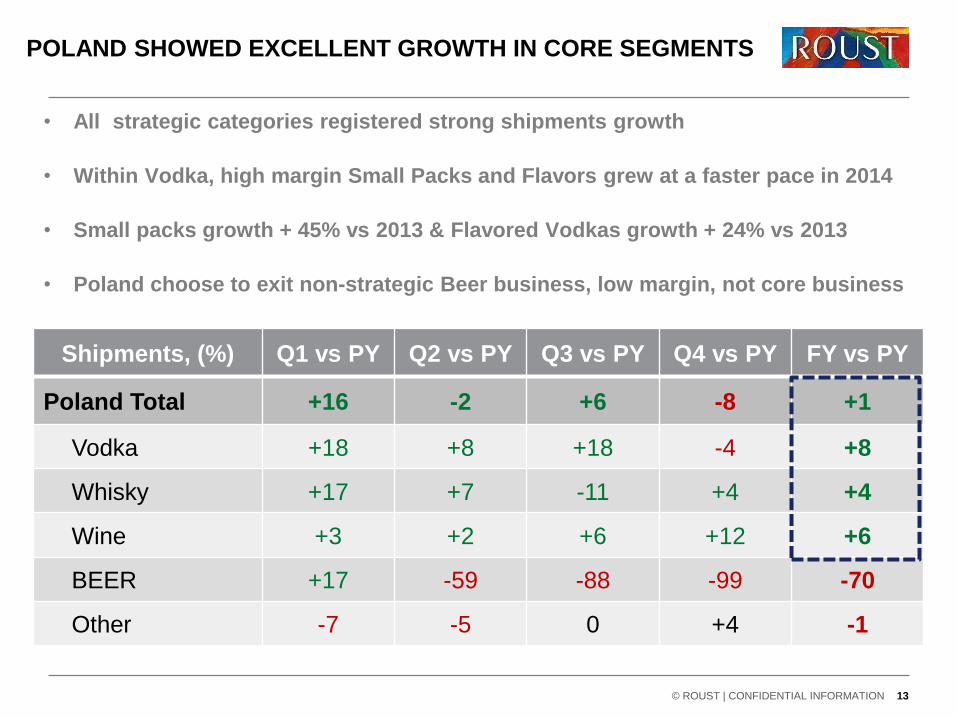

POLAND SHOWED EXCELLENT GROWTH IN CORE SEGMENTS

© ROUST | CONFIDENTIAL INFORMATION 13

Shipments, (%) Q1 vs PY Q2 vs PY Q3 vs PY Q4 vs PY FY vs PY

Poland Total +16 -2 +6 -8 +1

Vodka +18 +8 +18 -4 +8

Whisky +17 +7 -11 +4 +4

Wine +3 +2 +6 +12 +6

BEER +17 -59 -88 -99 -70

Other -7 -5 0 +4 -1

• All strategic categories registered strong shipments growth

• Within Vodka, high margin Small Packs and Flavors grew at a faster pace in 2014

• Small packs growth + 45% vs 2013 & Flavored Vodkas growth + 24% vs 2013

• Poland choose to exit non-strategic Beer business, low margin, not core business

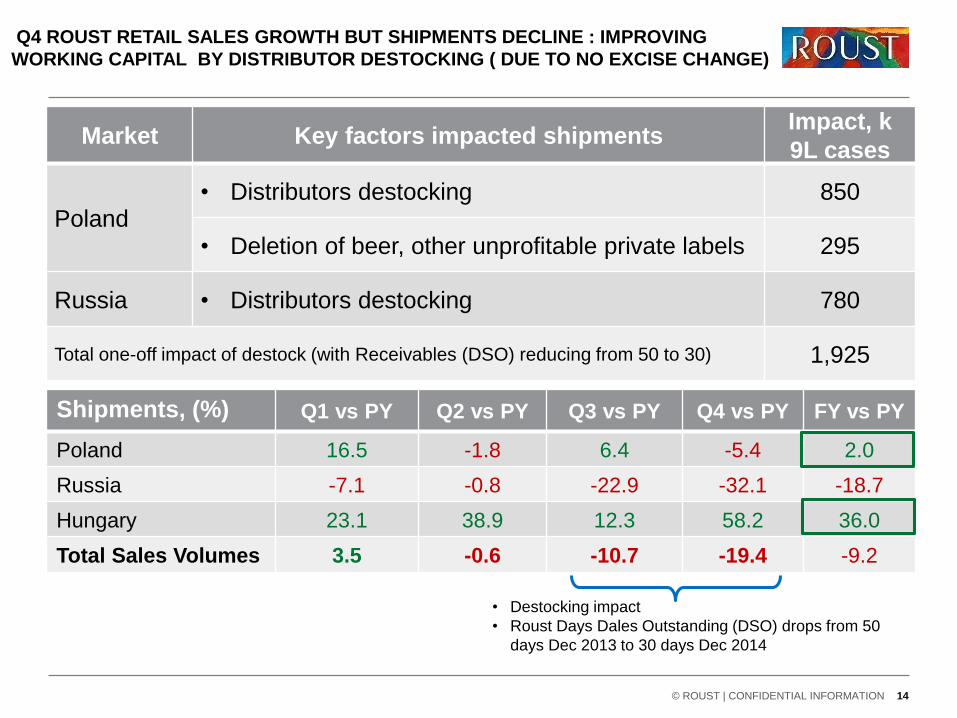

Q4 ROUST RETAIL SALES GROWTH BUT SHIPMENTS DECLINE : IMPROVING

WORKING CAPITAL BY DISTRIBUTOR DESTOCKING ( DUE TO NO EXCISE CHANGE)

© ROUST | CONFIDENTIAL INFORMATION 14

Market Key factors impacted shipmentsImpact, k

9L cases

Poland• Distributors destocking 850

• Deletion of beer, other unprofitable private labels 295

Russia • Distributors destocking 780

Total one-off impact of destock (with Receivables (DSO) reducing from 50 to 30) 1,925

• Destocking impact

• Roust Days Dales Outstanding (DSO) drops from 50

days Dec 2013 to 30 days Dec 2014

Shipments, (%) Q1 vs PY Q2 vs PY Q3 vs PY Q4 vs PY FY vs PY

Poland 16.5 -1.8 6.4 -5.4 2.0

Russia -7.1 -0.8 -22.9 -32.1 -18.7

Hungary 23.1 38.9 12.3 58.2 36.0

Total Sales Volumes 3.5 -0.6 -10.7 -19.4 -9.2

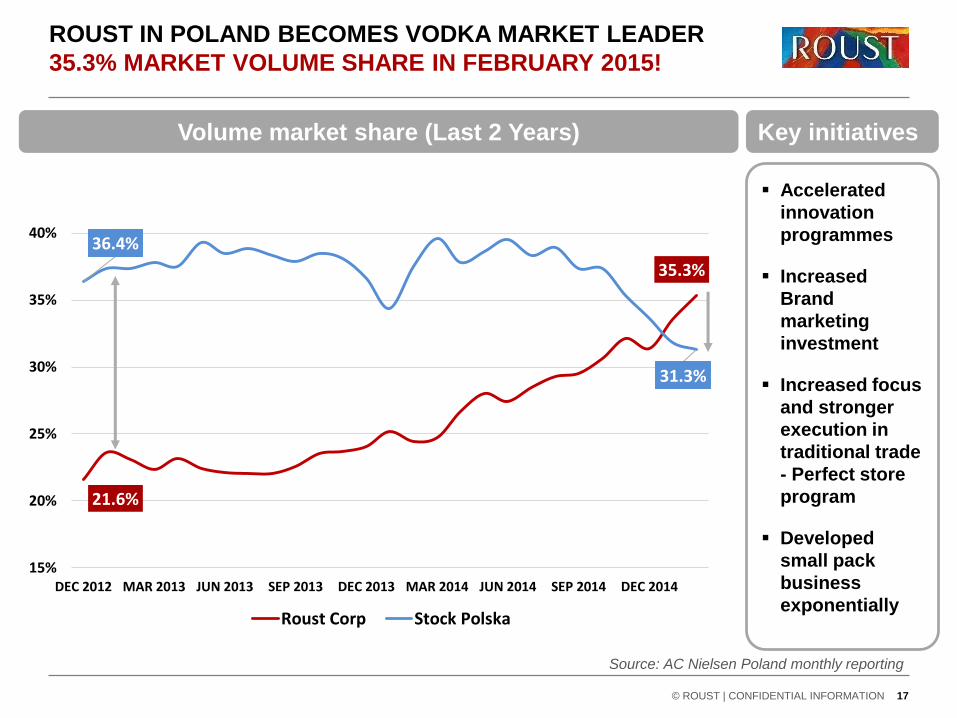

POLAND HIGHLIGHTS

POLAND HIGHLIGHTS: STUNNING SUCCESS 2014

© ROUST | CONFIDENTIAL INFORMATION 16

• Volume and market share growth

− Roust vodka retail volumes +18.0% year-on-year, despite overall vodka market decline of 4.3%

− We became vodka market leader in vodka business (Jan’15) – highest share since 2003!

− Volume market share reached 35.3% (Feb’15), consistent growth since 21.8% (Aug’13)

− Roust Polish business reinforced its position across:

All the retail segments (modern trade, discounters, traditional trade)

All key vodka segments (clear vodka, flavored vodka, small packs, big packs)

− Whisky and table wine – the fastest growing category from in Poland

• Our imported brands success

− Carlo Rossi, number one selling table wine in Poland by value with a 10% market share

− Our whisky volume market shares jumped to 16.5% (+6pp vs. PY), driven mainly by Grant’s

(3rd whisky brand on Polish market) reaching 14.1% (+5.2pp vs. PY).

− New multi-year contracts with Gallo Wines, William Grants (until 2019), Concha Y Toro (until

2020) and Gruppo Campari (through 2016). New contracts for Aperol and Wild Turkey

− Launch of our proprietary sparkling wine brand Gancia

21.6%

35.3%

36.4%

31.3%

15%

20%

25%

30%

35%

40%

DEC 2012 MAR 2013 JUN 2013 SEP 2013 DEC 2013 MAR 2014 JUN 2014 SEP 2014 DEC 2014

Roust Corp Stock Polska

ROUST IN POLAND BECOMES VODKA MARKET LEADER

35.3% MARKET VOLUME SHARE IN FEBRUARY 2015!

© ROUST | CONFIDENTIAL INFORMATION 17

Source: AC Nielsen Poland monthly reporting

Volume market share (Last 2 Years) Key initiatives

Accelerated

innovation

programmes

Increased

Brand

marketing

investment

Increased focus

and stronger

execution in

traditional trade

- Perfect store

program

Developed

small pack

business

exponentially

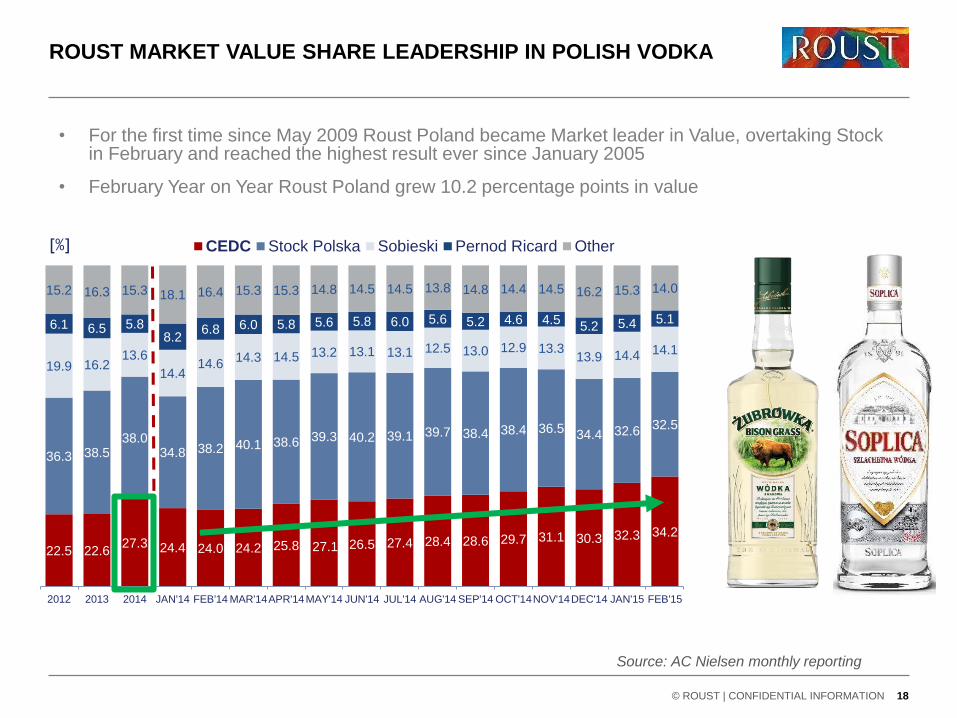

22.5 22.627.3 24.4 24.0 24.2 25.8 27.1 26.5 27.4 28.4 28.6 29.7 31.1 30.3 32.3 34.2

36.3 38.538.0

34.8 38.2 40.1 38.6 39.3 40.2 39.1 39.7 38.4 38.4 36.5 34.4 32.6 32.5

19.9 16.213.6

14.414.6

14.3 14.5 13.2 13.1 13.1 12.5 13.0 12.9 13.313.9 14.4 14.1

6.1 6.5 5.88.2

6.8 6.0 5.8 5.6 5.8 6.0 5.6 5.2 4.6 4.55.2 5.4 5.1

15.2 16.3 15.3 18.1 16.4 15.3 15.3 14.8 14.5 14.5 13.8 14.8 14.4 14.5 16.2 15.3 14.0

2012 2013 2014 JAN'14 FEB'14 MAR'14APR'14 MAY'14 JUN'14 JUL'14 AUG'14 SEP'14 OCT'14NOV'14DEC'14 JAN'15 FEB'15

CEDC Stock Polska Sobieski Pernod Ricard Other

18

ROUST MARKET VALUE SHARE LEADERSHIP IN POLISH VODKA

[%]

Source: AC Nielsen monthly reporting

© ROUST | CONFIDENTIAL INFORMATION

• For the first time since May 2009 Roust Poland became Market leader in Value, overtaking Stock in February and reached the highest result ever since January 2005

• February Year on Year Roust Poland grew 10.2 percentage points in value

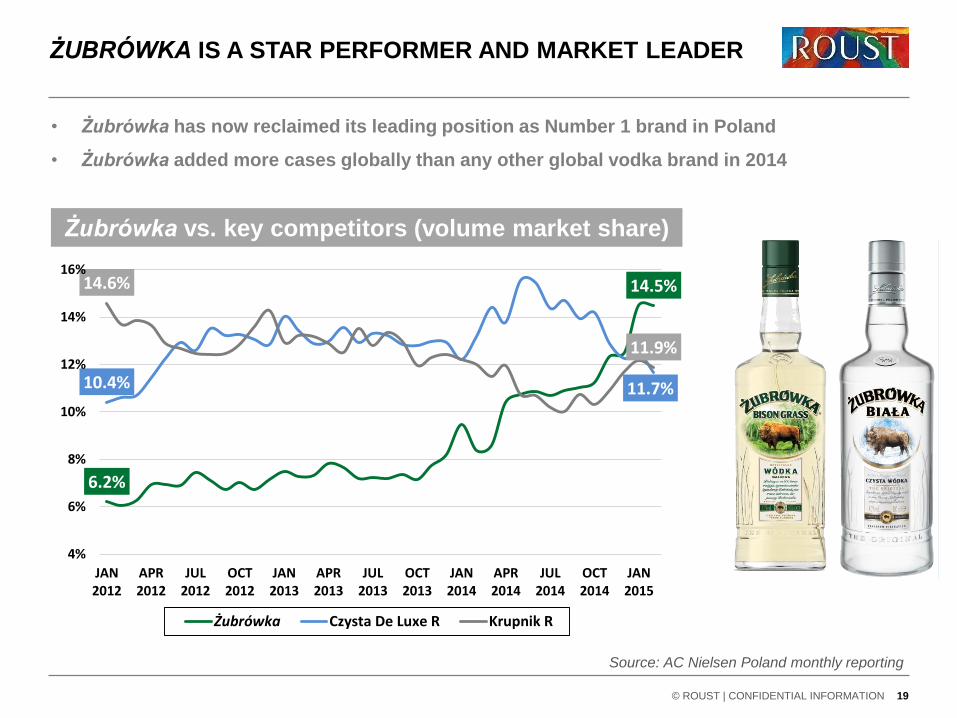

ŻUBRÓWKA IS A STAR PERFORMER AND MARKET LEADER

© ROUST | CONFIDENTIAL INFORMATION 19

Source: AC Nielsen Poland monthly reporting

• Żubrówka has now reclaimed its leading position as Number 1 brand in Poland

• Żubrówka added more cases globally than any other global vodka brand in 2014

Żubrówka vs. key competitors (volume market share)

6.2%

14.5%

10.4% 11.7%

14.6%

11.9%

4%

6%

8%

10%

12%

14%

16%

JAN2012

APR2012

JUL2012

OCT2012

JAN2013

APR2013

JUL2013

OCT2013

JAN2014

APR2014

JUL2014

OCT2014

JAN2015

Żubrówka Czysta De Luxe R Krupnik R

ŻUBRÓWKA, NATURAL INGREDIENTS AND TRADITION

HIGHLIGHTED IN THE UPGRADED LABEL AND BOTTLE

© ROUST | CONFIDENTIAL INFORMATION

20

Brand success

• Żubrówka Biała became market leader in Vodka category with

14.5% of volume Market share (Nielsen Feb 2015)

• Żubrówka Masterbrand 16.2% of volume market share

• Żubrówka became the 7th best selling vodka brand in the world

and the fastest growing vodka brand

Package improvement

• Upgraded Bottle design with adjusted Embossment to underline

bison stamp and polish text

• Upgraded Label design with 3D effect on bison, deeper colors

• Underlined 500 years of Bison Grass tradition, the secret of its taste

Current New

ABSOLWENT REVOLUTIONARY PACKAGING RE-LAUNCH

© ROUST | CONFIDENTIAL INFORMATION 21

Brand success

• One of the most recognizable brand in Poland market

• Awareness above 80%, market leading

• Successfully launched 3 flavors extensions in small

packs growing segments

Package improvement

• Revolutionary packaging with new embossments and

modern see-through label and silver cap

• Refreshed enlarged logotype with deep red colors

• Totally new smooth taste of ‘crystal clear vodka’

Current New

Żubrówka

Złota

Soplica

Plum & Blackcurrant

Absolwent

Grapefruit & Apple Mint; Tangerine

& Wild Strawberry

Żytniówka

POLAND INNOVATION: DRAMATIC ACCELERATION

Soplica

Walnut

© ROUST | CONFIDENTIAL INFORMATION 22

• Roust Poland flavor volume growth +24% vs 2013

• Share increased in flavor segment by 5.2 percentage points (pp) vs 2013

• Still huge potential to growth as gap to Stock is still 24 share points (December 2014)

ACCELERATED PORTFOLIO INNOVATION ON IMPORTS

New launches 2014

GANCIA portfolio

CARLO ROSSI - Sweet

White MoscatoAPEROL WILD TURKEY

© ROUST | CONFIDENTIAL INFORMATION

• Gancia expansion into premium

Sparkling Wines & Vermouth

segments

• Introduction of Wild Turkey into

Premium American Whiskey

segment as a replacement to

Jim Beam

• Continued expansion in sweet

wine segment via Carlo Rossi

sweet white Moscato launch

• Introduction of Aperol to

capitalize on booming in Europe

bitter segment

23

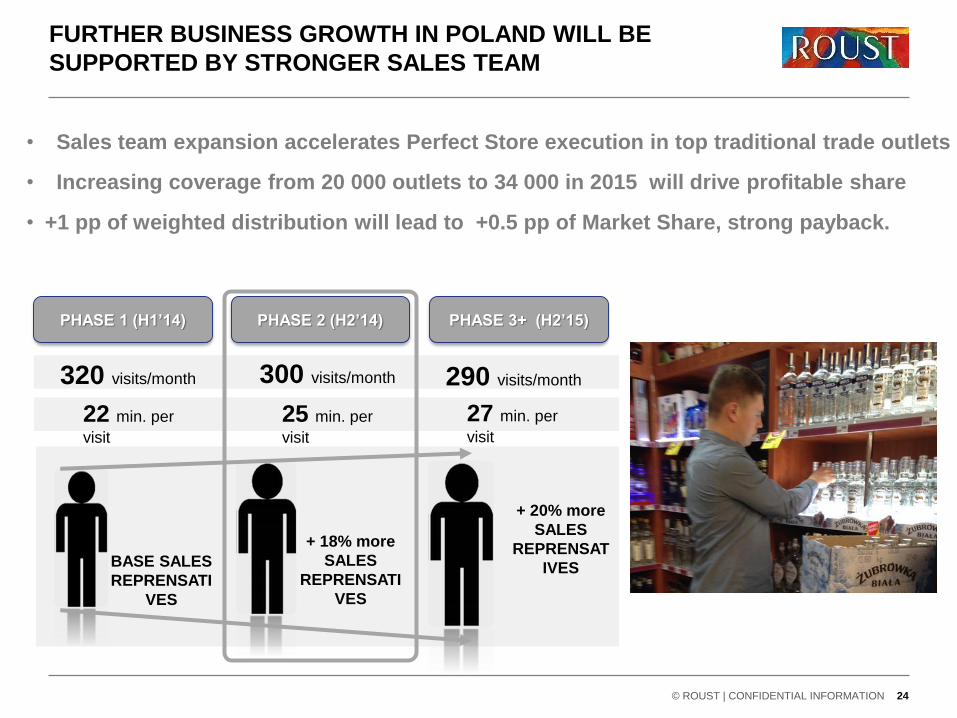

FURTHER BUSINESS GROWTH IN POLAND WILL BE

SUPPORTED BY STRONGER SALES TEAM

PHASE 1 (H1’14)

320 visits/month

22 min. per

visit

BASE SALES

REPRENSATI

VES

PHASE 2 (H2’14)

300 visits/month

25 min. per

visit

PHASE 3+ (H2’15)

290 visits/month

+ 18% more

SALES

REPRENSATI

VES

27 min. per

visit

+ 20% more

SALES

REPRENSAT

IVES

© ROUST | CONFIDENTIAL INFORMATION 24

• Sales team expansion accelerates Perfect Store execution in top traditional trade outlets

• Increasing coverage from 20 000 outlets to 34 000 in 2015 will drive profitable share

• +1 pp of weighted distribution will lead to +0.5 pp of Market Share, strong payback.

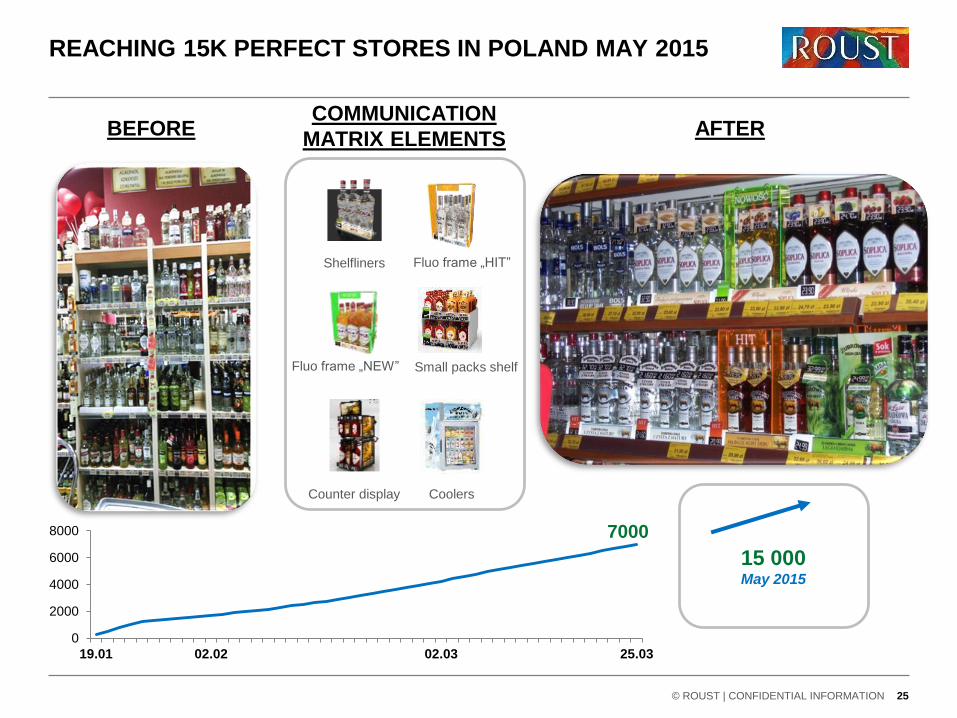

REACHING 15K PERFECT STORES IN POLAND MAY 2015

15 000May 2015

Shelfliners Fluo frame „HIT”

Fluo frame „NEW” Small packs shelf

Counter display Coolers

COMMUNICATION

MATRIX ELEMENTSBEFORE AFTER

© ROUST | CONFIDENTIAL INFORMATION 25

7000

0

2000

4000

6000

8000

19.01 02.02 02.03 25.03

RUSSIA HIGHLIGHTS

RUSSIA HIGHLIGHTS: STABLE MARKET LEADERSHIP,

ROUST SUCCESSFULLY INTEGRATED

• Successful year in Russia given economic and category challenges

– Core brands share increasing, market leadership maintained

– Russian Standard vodka now accelerating

– Much more efficient business structure implemented

– EBITDA for Russia of $50.1M for 2014

• Integration of Roust Inc. with ROUST (former Russian Alcohol) a success

– Roust Inc. acquisition producing synergies across sales and back office structures

Additional efficiencies to be realized in 2015

• Roust Market share stable in total, premium brands share growing

– Nielsen market share: Roust vodka relatively stable market share around 13%

– Government shipments tracking: Roust Russia total vodka share increased

– Roust premium vodka share growing Q4:

Talka +3.7% year-on-year despite shrinking total vodka market (-17.6%)

RSV share growth Q4: 34% in December 2014

– Roust Inc. core agency brands: Remy Martin +9%,ägermeister +8%, Metaxa +15%

– Protected margins Q4 on Agency brands with suppliers support

– Wine business sales showing positive dynamic in 2014 with improved profitability

• Excise tax – no increases in 2015 and 2016

© ROUST | CONFIDENTIAL INFORMATION 27

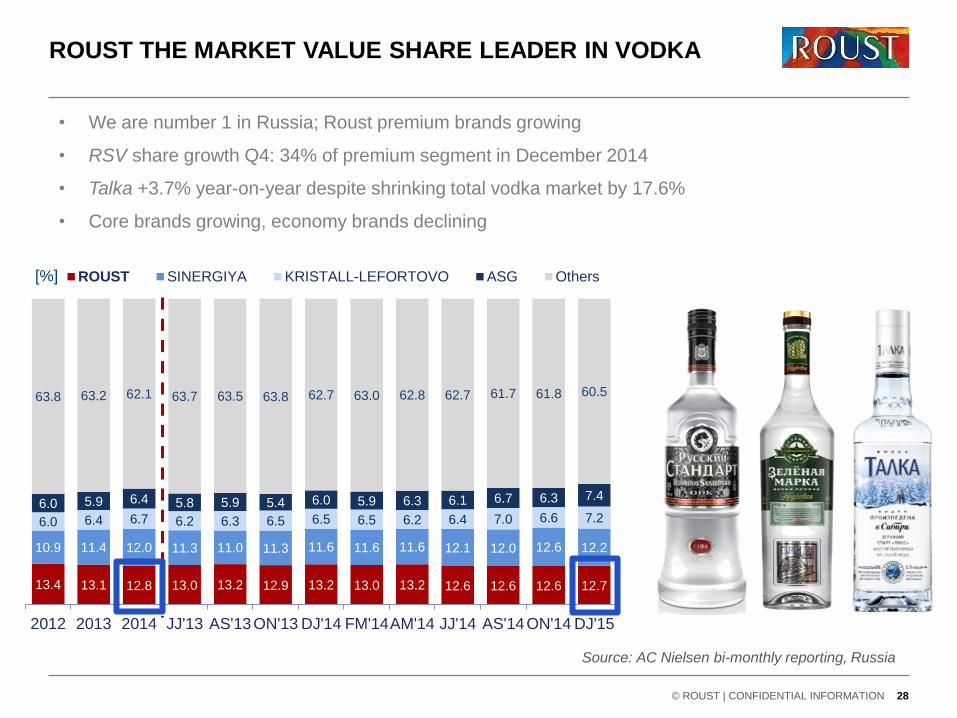

[%]

28

ROUST THE MARKET VALUE SHARE LEADER IN VODKA

13.4 13.1 12.8 13.0 13.2 12.9 13.2 13.0 13.2 12.6 12.6 12.6 12.7

10.9 11.4 12.0 11.3 11.0 11.3 11.6 11.6 11.6 12.1 12.0 12.6 12.2

6.0 6.4 6.7 6.2 6.3 6.5 6.5 6.5 6.2 6.4 7.0 6.6 7.26.0 5.9 6.4 5.8 5.9 5.4 6.0 5.9 6.3 6.1 6.7 6.3 7.4

63.8 63.2 62.1 63.7 63.5 63.8 62.7 63.0 62.8 62.7 61.7 61.8 60.5

2012 2013 2014 JJ'13 AS'13ON'13 DJ'14 FM'14AM'14 JJ'14 AS'14ON'14 DJ'15

ROUST SINERGIYA KRISTALL-LEFORTOVO ASG Others

Source: AC Nielsen bi-monthly reporting, Russia

© ROUST | CONFIDENTIAL INFORMATION

• We are number 1 in Russia; Roust premium brands growing

• RSV share growth Q4: 34% of premium segment in December 2014

• Talka +3.7% year-on-year despite shrinking total vodka market by 17.6%

• Core brands growing, economy brands declining

GREEN MARK REVOLUTIONARY RESTYLING DRIVES APPEAL

29© ROUST | CONFIDENTIAL INFORMATION

Brand success

• 4 million 9l cases in 2014

• 2nd biggest export brand after Russian

Standard vodka

• Market leading brand 2014

Package improvement

• Revolutionary brand restyling will help to

revive the warm and soulful brand feeling

• Unique bottle and labels elements for

counterfeit protection

Current May 2015

© ROUST | CONFIDENTIAL INFORMATION 30

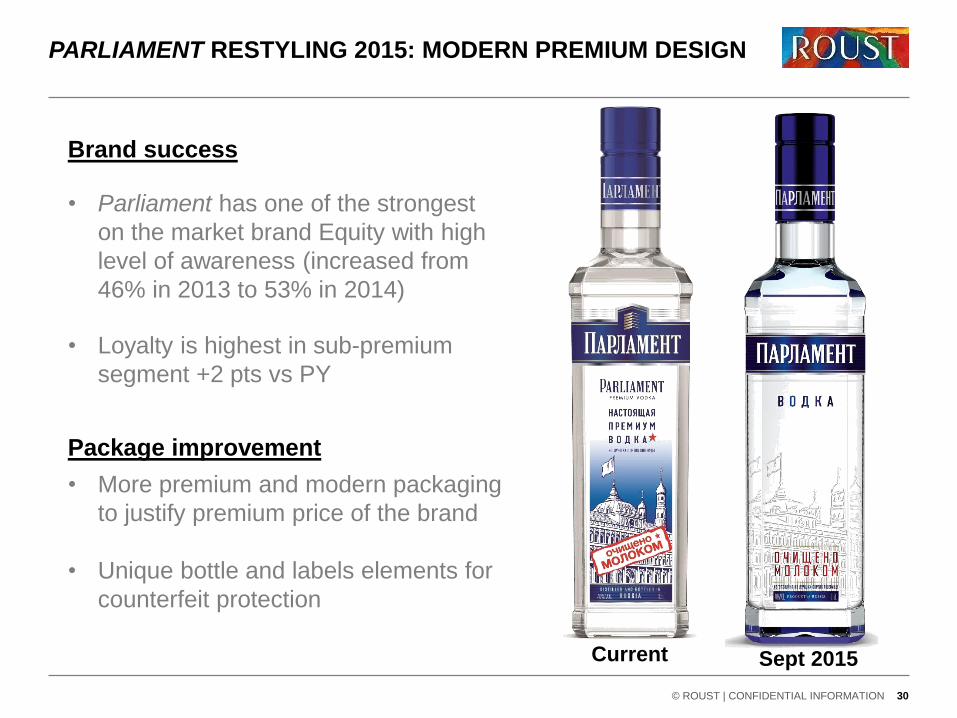

PARLIAMENT RESTYLING 2015: MODERN PREMIUM DESIGN

Brand success

• Parliament has one of the strongest

on the market brand Equity with high

level of awareness (increased from

46% in 2013 to 53% in 2014)

• Loyalty is highest in sub-premium

segment +2 pts vs PY

Package improvement

• More premium and modern packaging

to justify premium price of the brand

• Unique bottle and labels elements for

counterfeit protection

Current Sept 2015

31

Urozhay

Honey

Enlarging the

range with

well-known

taste and

bringing new

consumers

Talka

Siberian Pine

Cedar flavor to

brings to

consumers a

demanded and

popular flavor

RUSSIAN INNOVATION ACCELERATING IN 2014

© ROUST | CONFIDENTIAL INFORMATION

Russian Standard Premium Infusions

• High quality infusions based on natural juice and

Russian Standard vodka

• Allow to enter the traditionally popular infusions

segment in Russia

• Revolutionary product bringing to the market a

premium and high quality product guaranteed by a

strong brand name

Green Mark

Flasks 0.25 & 0.10

To be better

presented in small

packs’ segment that

is increasing

dramatically

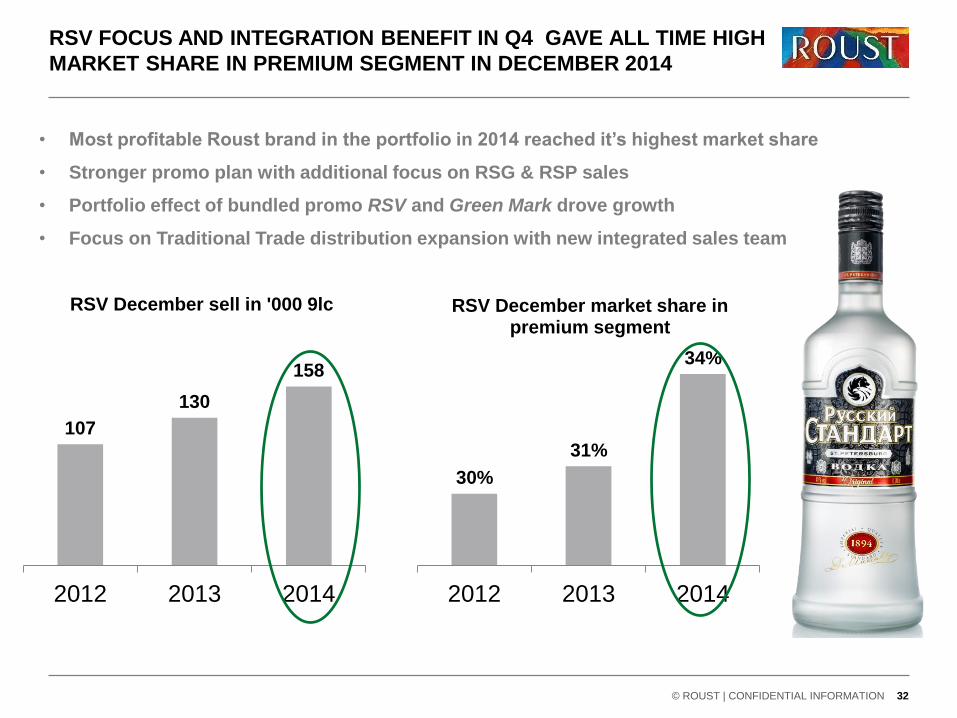

RSV FOCUS AND INTEGRATION BENEFIT IN Q4 GAVE ALL TIME HIGH

MARKET SHARE IN PREMIUM SEGMENT IN DECEMBER 2014

• Most profitable Roust brand in the portfolio in 2014 reached it’s highest market share

• Stronger promo plan with additional focus on RSG & RSP sales

• Portfolio effect of bundled promo RSV and Green Mark drove growth

• Focus on Traditional Trade distribution expansion with new integrated sales team

107

130

158

2012 2013 2014

RSV December sell in '000 9lc

30%

31%

34%

2012 2013 2014

RSV December market share in premium segment

© ROUST | CONFIDENTIAL INFORMATION 32

CORE AGENCY BRANDS GREW STRONGLY IN RUSSIA 2014

© ROUST | CONFIDENTIAL INFORMATION 33

• Remy Martin: +9% vs PY

− Number 2 cognac in Russia

− Share increased in 2014 to 18%

• Jägermeister: +5% vs PY

− 3 years contract signed September 2014

− Brand awareness grew by 12% to 52%

• Metaxa: +15% vs PY

− Distribution expanded in traditional trade by

17,5% after consolidation with Roust Russia

• Jose Cuervo: +41% vs PY

− First year in ROUST portfolio. New listings in

Key accounts, successful launch in Russia

• TOP Wine brands growing:

− Carlo Rossi +59% vs PY

− Concha y Toro +3% vs PY

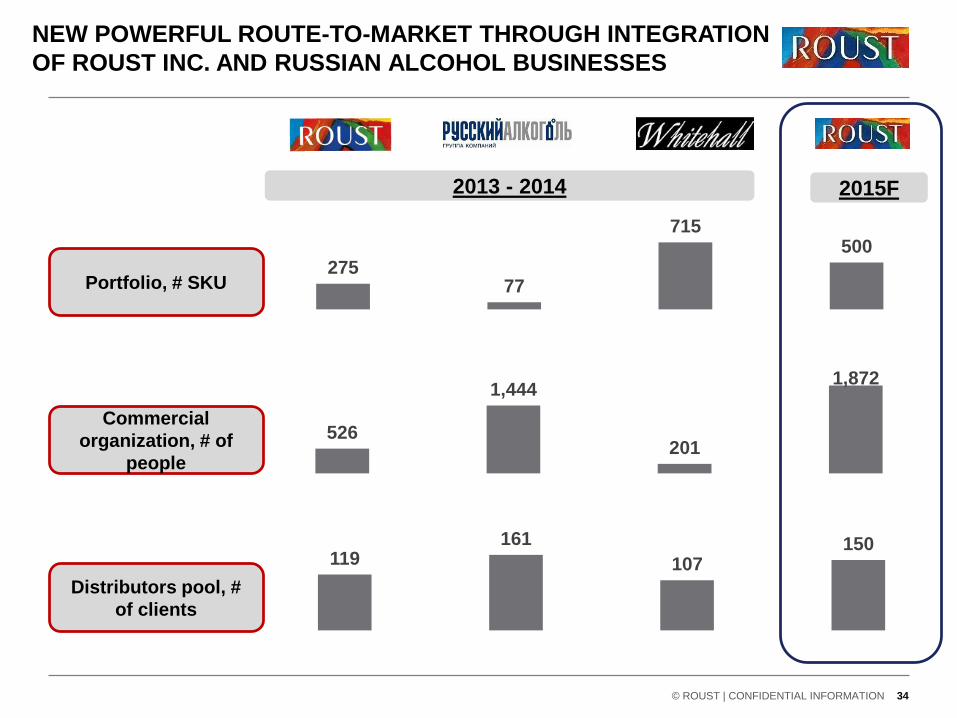

NEW POWERFUL ROUTE-TO-MARKET THROUGH INTEGRATION

OF ROUST INC. AND RUSSIAN ALCOHOL BUSINESSES

Portfolio, # SKU

2015F2013 - 2014

27577

715500

Commercial

organization, # of

people

526

1,444

201

1,872

Distributors pool, #

of clients

119161

107150

© ROUST | CONFIDENTIAL INFORMATION 34

ROUST RUSSIA SALES FORCE IN TRADITIONAL TRADE WILL

INCREASE WEIGHTED DISTRIBUTION AND PERFECT STORES

35

80 shops

Coverage - 45k

215 visits/month

580 Sales

Representatives

300 visits/month

Roust Russia - 2014

100 shops

Coverage - 50k

680 Sales

Representatives

Roust Russia - 2015

© ROUST | CONFIDENTIAL INFORMATION

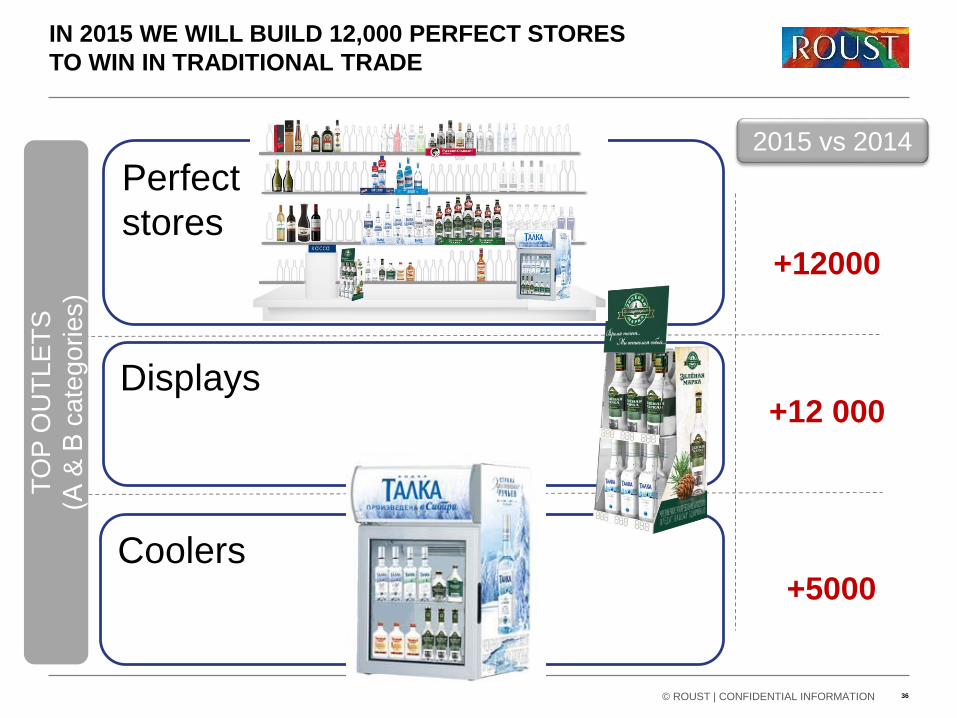

• 12,000 perfects outlets by end 2015 including targeted SKU range, coolers, displays, shelf share

• Increase coverage of traditional trade from 37,000 to 50,000 outlets

• Sales structure focus on Perfect Outlet building & execution: new bonus scheme, 100 new merchandisers

© ROUST | CONFIDENTIAL INFORMATION

IN 2015 WE WILL BUILD 12,000 PERFECT STORES

TO WIN IN TRADITIONAL TRADE

2015 vs 2014

Displays+12 000

+12000

Perfect

stores

TO

P O

UT

LE

TS

(А &

Вca

teg

orie

s)

Coolers+5000

36

INTERNATIONAL HIGHLIGHTS

HUNGARY HIGHLIGHTS: PROFIT GROWTH,

OUTSTANDING MARKET SHARE INCREASES

© ROUST | CONFIDENTIAL INFORMATION 38

• Volume and market share increasing rapidly

− Total volumes year on year increased by +36.0% in 2014 driven mainly by Royal Vodka +50.2%

− Flagship brand Royal Vodka maintains no. 1 position, reaching 56.2% market share in the mainstream vodka

category +3.6%

• Portfolio extension progressing

− Re-launch of key brand Żubrówka Bison Grass in original Polish packaging

Remarkable sales increase of +161% in 2014

− Launch of a new first in the market 0.35l bottle for Royal Vodka (Aug 2014)

− Leveraging ROUST / Russian Standard core brands:

Continued rollout of premium Russian Standard Vodka (launched in 2013)

Gancia sparkling wine (launched April 2014)

• Imported brands growing and contracts extending

− Strong partnerships and contract extensions with Jägermeister and Campari

− New five-year contract with William Grants & Sons.

− Jägermeister +20%; Grant’s Whisky +270% and Metaxa +18%

39

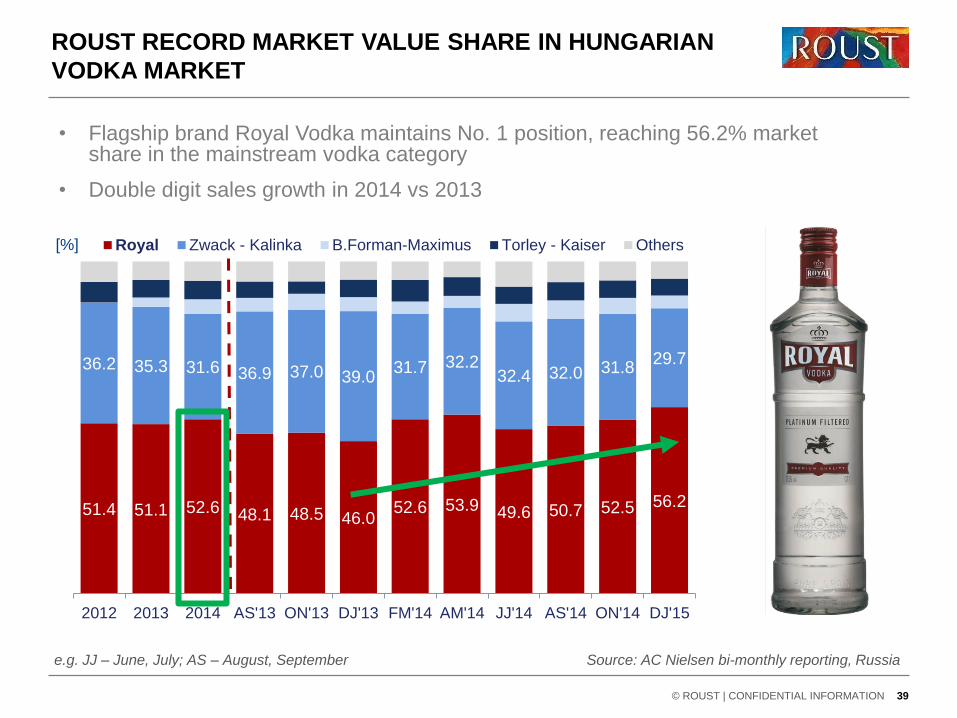

ROUST RECORD MARKET VALUE SHARE IN HUNGARIAN

VODKA MARKET

51.4 51.1 52.6 48.1 48.5 46.052.6 53.9 49.6 50.7 52.5 56.2

36.2 35.3 31.6 36.9 37.0 39.031.7 32.2

32.4 32.0 31.829.7

2012 2013 2014 AS'13 ON'13 DJ'13 FM'14 AM'14 JJ'14 AS'14 ON'14 DJ'15

Royal Zwack - Kalinka B.Forman-Maximus Torley - Kaiser Others[%]

Source: AC Nielsen bi-monthly reporting, Russiae.g. JJ – June, July; AS – August, September

© ROUST | CONFIDENTIAL INFORMATION

• Flagship brand Royal Vodka maintains No. 1 position, reaching 56.2% market share in the mainstream vodka category

• Double digit sales growth in 2014 vs 2013

• UK, Germany, France, Kazakhstan, Baltics, USA, Japan, Australia remain top performers among ROUST’s international markets drove +15% depletions growth vs PY

• We aim for a leading position in all of the top ten vodka countries in the world, and currently hold significant shares in seven of these ten countries.

• Our key goals are:

− Become the number 1 vodka player in the European Union

− Continued market share growth in Kazakhstan / CIS

− Build our business in USA

− Explosive growth in Asia and Africa

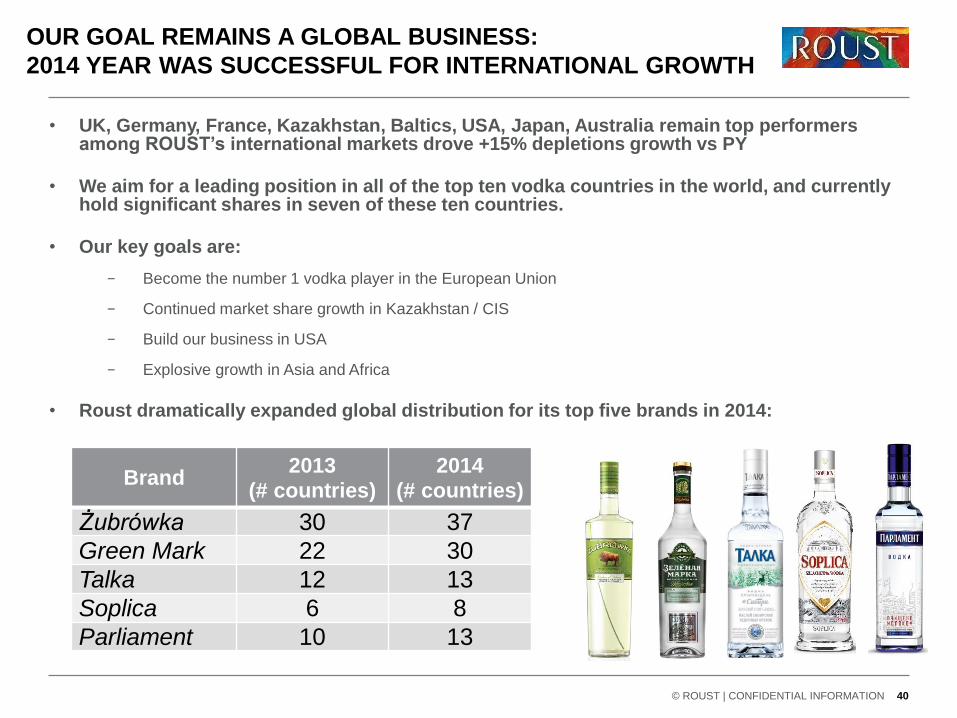

• Roust dramatically expanded global distribution for its top five brands in 2014:

40

OUR GOAL REMAINS A GLOBAL BUSINESS:

2014 YEAR WAS SUCCESSFUL FOR INTERNATIONAL GROWTH

Brand2013

(# countries)

2014

(# countries)

Żubrówka 30 37

Green Mark 22 30

Talka 12 13

Soplica 6 8

Parliament 10 13

© ROUST | CONFIDENTIAL INFORMATION

1. Roust/RSV portfolio grew +21% in 2014 to 1,013k cases

• UK is a strategically important export market for the Company, and in 2014 finished

with Green Mark growing volume +77% vs 2013, and Żubrówka with volume

growing +39% vs 2013, vs total UK vodka market only growing at +2%

2. 2014 saw Green Mark become the 4th largest brand in the UK

Grocers:

• Overtaking Absolut in the process, driven by over 2k new distribution points, the

introduction of Green Mark 35cl SKU to the UK for the first time and participation as

a lead vodka in the Christmas 2014 key trading period.

3. In 2014 Żubrówka overtook rivals to become the No. 3 Flavored

vodka in UK Off Trade

• Driven by +500 new distribution points and a near doubling of rate of sale during.

4. In 2015 we will see further rapid growth for both brands:

• Green Mark targeting +40% volume growth vs 2014, which will see the brand deliver

over 200k 9L cases. Żubrówka also aiming for +40% growth vs 2014. This compares

total UK Vodka Market growing at only +3%.

41

UNITED KINGDOM – DRAMATIC ACCELERATION

© ROUST | CONFIDENTIAL INFORMATION

42

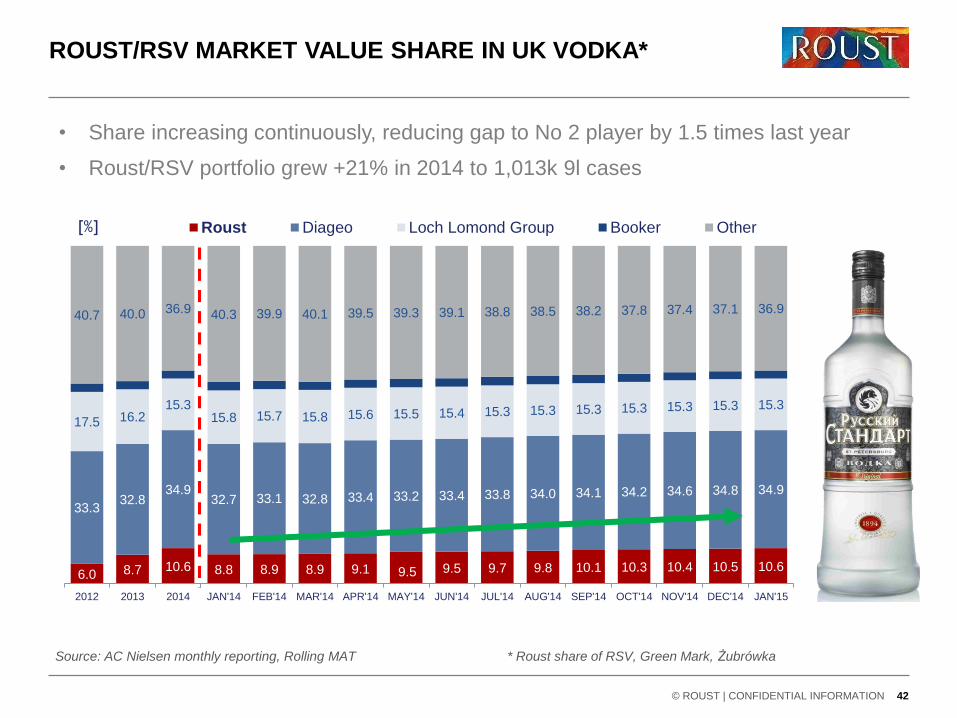

ROUST/RSV MARKET VALUE SHARE IN UK VODKA*

6.0 8.7 10.6 8.8 8.9 8.9 9.1 9.5 9.5 9.7 9.8 10.1 10.3 10.4 10.5 10.6

33.332.8

34.932.7 33.1 32.8 33.4 33.2 33.4 33.8 34.0 34.1 34.2 34.6 34.8 34.9

17.5 16.215.3

15.8 15.7 15.8 15.6 15.5 15.4 15.3 15.3 15.3 15.3 15.3 15.3 15.3

40.7 40.0 36.9 40.3 39.9 40.1 39.5 39.3 39.1 38.8 38.5 38.2 37.8 37.4 37.1 36.9

2012 2013 2014 JAN'14 FEB'14 MAR'14 APR'14 MAY'14 JUN'14 JUL'14 AUG'14 SEP'14 OCT'14 NOV'14 DEC'14 JAN'15

Roust Diageo Loch Lomond Group Booker Other[%]

Source: AC Nielsen monthly reporting, Rolling MAT * Roust share of RSV, Green Mark, Żubrówka

© ROUST | CONFIDENTIAL INFORMATION

• Share increasing continuously, reducing gap to No 2 player by 1.5 times last year

• Roust/RSV portfolio grew +21% in 2014 to 1,013k 9l cases

1. Overall Roust brands for 5.1% share of German vodka market

• Within the Premium sector (>€10) Roust brands account for the largest share,

at 20% share, ahead of Pernod Ricard 19.1% and Diageo 17.5%

2. 2014, the Roust/RSV portfolio grew +52% vs 2013 to 400k 9l cases

3. Green Mark – also significant growth with 43k 9l cases (+265% vs PY)

• Making it a bigger brand in the German market than Finlandia

4. Parliament Vodka achieved 142k 9l cases, +7% vs 2013

5. Yamskaya, exclusive with Aldi – great success with 63k 9l cases

sold in its first year

6. In Q4 2014 we launched Żubrówka into the German market

• We will continue to drive volume growth in 2015, with a plan of over 500k 9l

cases, including the launch of Romanoff vodka in the value sector

43

GERMANY – EXPLOSIVE GROWTH OF FULL PORTFOLIO

© ROUST | CONFIDENTIAL INFORMATION

44

FRANCE IS NOW ACCELERATING AND GROWING SHARE

© ROUST | CONFIDENTIAL INFORMATION

1. Żubrówka is our priority Roust brand focus in France with

strong historical equity and very premium pricing

2. 2014 Performance of Żubrówka kick started growth after

several years decline

• 62k 9l cases depleted in 2014 (+6% v 2013)

• Re-initiated ATL communication (first since 2007) with $820k OOH spend

3. Żubrówka share in 2015 YTD is now 3.3%, up from 2.7%

a year ago.

• Off trade distribution is now 97%, +2% pts versus a year ago, Biała

already 0.5% market share and distribution of 49%

• YTD 2015 shipments +37% vs 2014

4. 2015 Goals for Żubrówka

• Rapidly increase depletions in market to 105k 9l cases (+69% YoY volume

growth, including 30k 9l cases Biała)

• Up-weight advertising for Żubrówka : $1m planned ion 2015 with 2x Outdoor

advertising bursts (+22% YoY media investment increase)

• Grow total brand share to 3.4% and achieve Brand awareness of 48%

FULL YEAR 2014 FINANCIALS

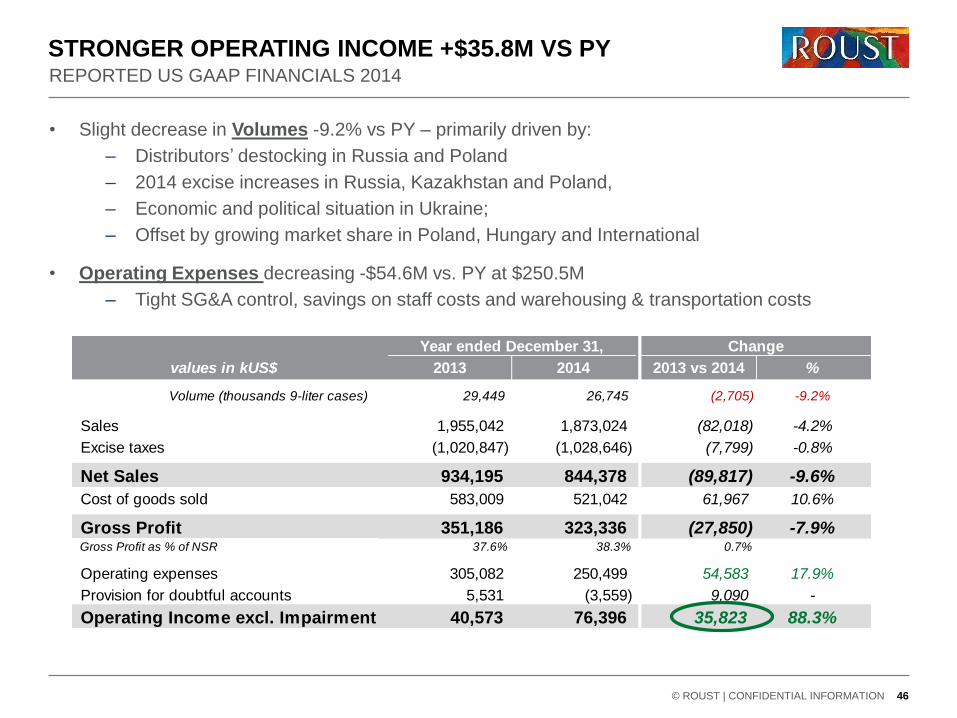

STRONGER OPERATING INCOME +$35.8M VS PY

• Slight decrease in Volumes -9.2% vs PY – primarily driven by:

– Distributors’ destocking in Russia and Poland

– 2014 excise increases in Russia, Kazakhstan and Poland,

– Economic and political situation in Ukraine;

– Offset by growing market share in Poland, Hungary and International

• Operating Expenses decreasing -$54.6M vs. PY at $250.5M

– Tight SG&A control, savings on staff costs and warehousing & transportation costs

© ROUST | CONFIDENTIAL INFORMATION 46

values in kUS$ 2013 2014 2013 vs 2014 %

Volume (thousands 9-liter cases) 29,449 26,745 (2,705) -9.2%

Sales 1,955,042 1,873,024 (82,018) -4.2%

Excise taxes (1,020,847) (1,028,646) (7,799) -0.8%

Net Sales 934,195 844,378 (89,817) -9.6%

Cost of goods sold 583,009 521,042 61,967 10.6%

Gross Profit 351,186 323,336 (27,850) -7.9%Gross Profit as % of NSR 37.6% 38.3% 0.7%

Operating expenses 305,082 250,499 54,583 17.9%

Provision for doubtful accounts 5,531 (3,559) 9,090 -

Operating Income excl. Impairment 40,573 76,396 35,823 88.3%

Year ended December 31, Change

REPORTED US GAAP FINANCIALS 2014

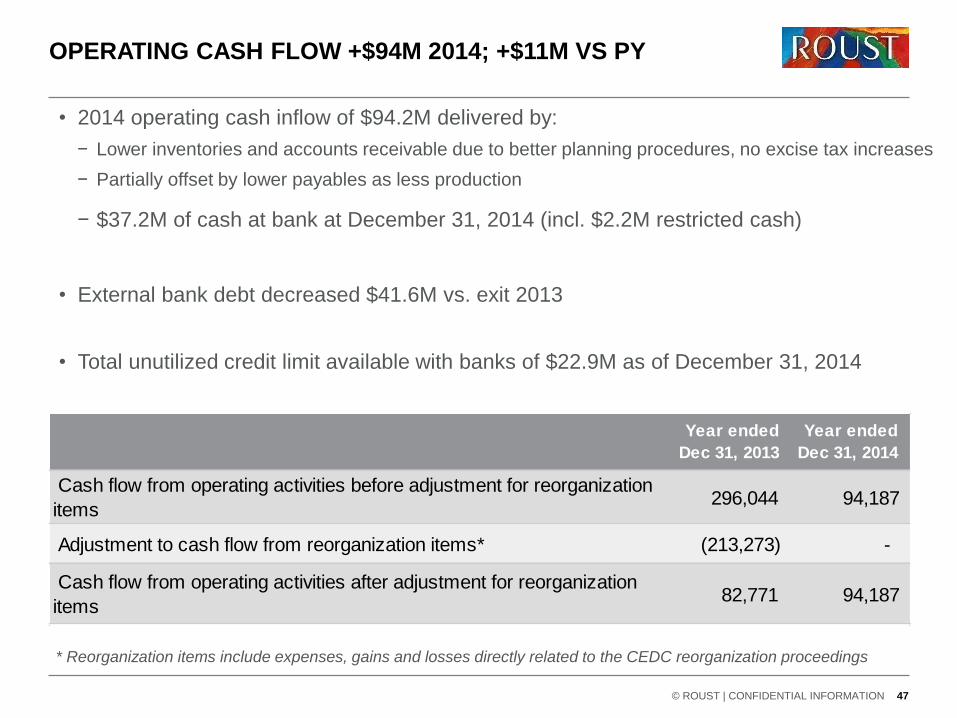

OPERATING CASH FLOW +$94M 2014; +$11M VS PY

© ROUST | CONFIDENTIAL INFORMATION 47

Cash flow from operating activities before adjustment for reorganization

items 296,044 94,187

Adjustment to cash flow from reorganization items* (213,273) -

Cash flow from operating activities after adjustment for reorganization

items 82,771 94,187

Year ended

Dec 31, 2013

Year ended

Dec 31, 2014

• 2014 operating cash inflow of $94.2M delivered by:

− Lower inventories and accounts receivable due to better planning procedures, no excise tax increases

− Partially offset by lower payables as less production

− $37.2M of cash at bank at December 31, 2014 (incl. $2.2M restricted cash)

• External bank debt decreased $41.6M vs. exit 2013

• Total unutilized credit limit available with banks of $22.9M as of December 31, 2014

* Reorganization items include expenses, gains and losses directly related to the CEDC reorganization proceedings

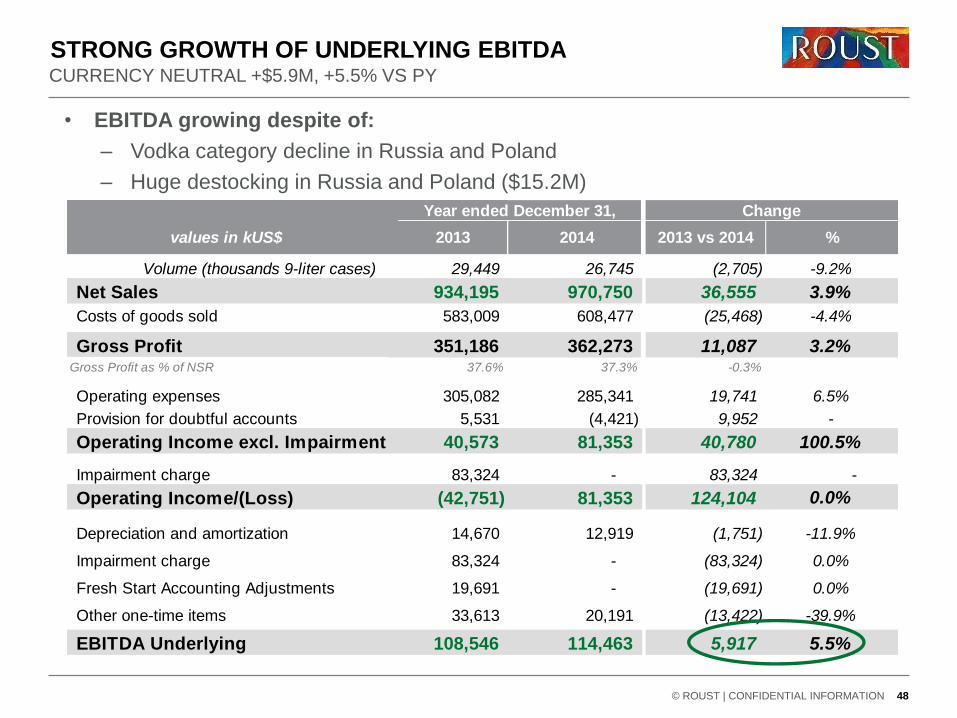

STRONG GROWTH OF UNDERLYING EBITDA

© ROUST | CONFIDENTIAL INFORMATION 48

values in kUS$ 2013 2014 2013 vs 2014 %

Volume (thousands 9-liter cases) 29,449 26,745 (2,705) -9.2%

Net Sales 934,195 970,750 36,555 3.9%

Costs of goods sold 583,009 608,477 (25,468) -4.4%

Gross Profit 351,186 362,273 11,087 3.2%Gross Profit as % of NSR 37.6% 37.3% -0.3%

Operating expenses 305,082 285,341 19,741 6.5%

Provision for doubtful accounts 5,531 (4,421) 9,952 -

Operating Income excl. Impairment 40,573 81,353 40,780 100.5%

Impairment charge 83,324 - 83,324 -

Operating Income/(Loss) (42,751) 81,353 124,104 0.0%

Depreciation and amortization 14,670 12,919 (1,751) -11.9%- -

Impairment charge 83,324 - (83,324) 0.0%-

Fresh Start Accounting Adjustments 19,691 - (19,691) 0.0%-

Other one-time items 33,613 20,191 (13,422) -39.9%

EBITDA Underlying 108,546 114,463 5,917 5.5%

Year ended December 31, Change

• EBITDA growing despite of:

– Vodka category decline in Russia and Poland

– Huge destocking in Russia and Poland ($15.2M)

CURRENCY NEUTRAL +$5.9M, +5.5% VS PY

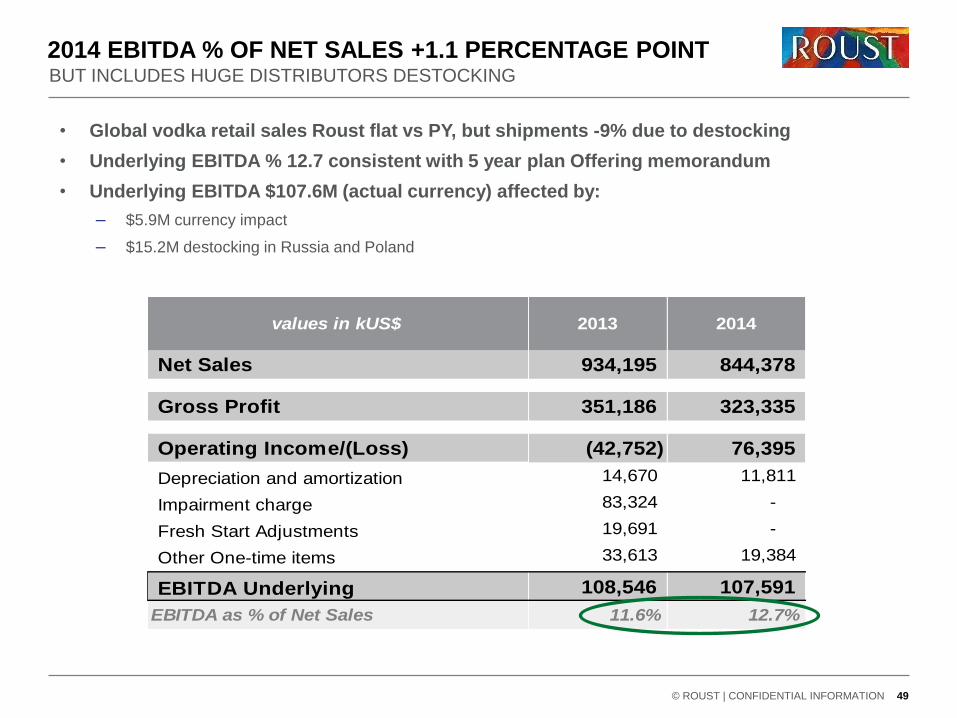

2014 EBITDA % OF NET SALES +1.1 PERCENTAGE POINT

© ROUST | CONFIDENTIAL INFORMATION 49

• Global vodka retail sales Roust flat vs PY, but shipments -9% due to destocking

• Underlying EBITDA % 12.7 consistent with 5 year plan Offering memorandum

• Underlying EBITDA $107.6M (actual currency) affected by:

– $5.9M currency impact

– $15.2M destocking in Russia and Poland

Net Sales 934,195 844,378

Gross Profit 351,186 323,335

Operating Income/(Loss) (42,752) 76,395

Depreciation and amortization 14,670 11,811

Impairment charge 83,324 -

Fresh Start Adjustments 19,691 -

Other One-time items 33,613 19,384

EBITDA Underlying 108,546 107,591

EBITDA as % of Net Sales 11.6% 12.7%

values in kUS$ 2013 2014

BUT INCLUDES HUGE DISTRIBUTORS DESTOCKING

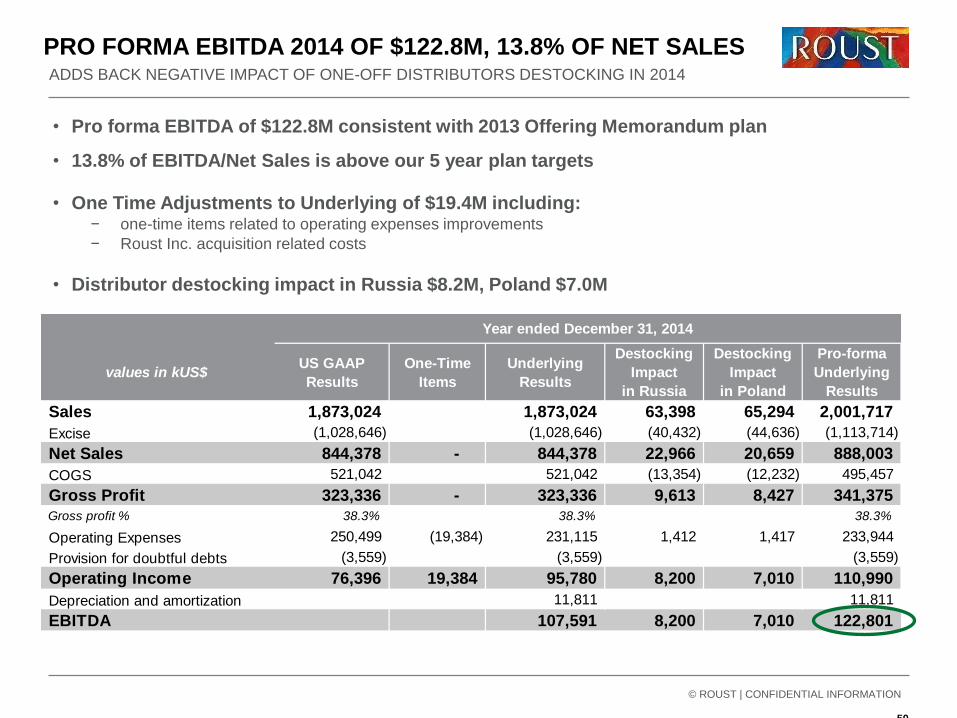

PRO FORMA EBITDA 2014 OF $122.8M, 13.8% OF NET SALES

© ROUST | CONFIDENTIAL INFORMATION

50

• Pro forma EBITDA of $122.8M consistent with 2013 Offering Memorandum plan

• 13.8% of EBITDA/Net Sales is above our 5 year plan targets

• One Time Adjustments to Underlying of $19.4M including:− one-time items related to operating expenses improvements

− Roust Inc. acquisition related costs

• Distributor destocking impact in Russia $8.2M, Poland $7.0M

values in kUS$US GAAP

Results

One-Time

Items

Underlying

Results

Destocking

Impact

in Russia

Destocking

Impact

in Poland

Pro-forma

Underlying

Results

Sales 1,873,024 1,873,024 63,398 65,294 2,001,717

Excise (1,028,646) (1,028,646) (40,432) (44,636) (1,113,714)

Net Sales 844,378 - 844,378 22,966 20,659 888,003

COGS 521,042 521,042 (13,354) (12,232) 495,457

Gross Profit 323,336 - 323,336 9,613 8,427 341,375

Gross profit % 38.3% 38.3% 38.3%

Operating Expenses 250,499 (19,384) 231,115 1,412 1,417 233,944

Provision for doubtful debts (3,559) (3,559) (3,559)

Operating Income 76,396 19,384 95,780 8,200 7,010 110,990

Depreciation and amortization 11,811 11,811

EBITDA 107,591 8,200 7,010 122,801

Year ended December 31, 2014

ADDS BACK NEGATIVE IMPACT OF ONE-OFF DISTRIBUTORS DESTOCKING IN 2014

MAJOR COSTS FAVORABLE

© ROUST | CONFIDENTIAL INFORMATION 51

• Spirit prices costs slightly reduced for total ROUST:

− Poland year 2014 vs year 2013 decreased by10.9%

− Russia year 2014 vs year 2013 stable in rubles but decreased in US dollars

− Our decreasing Russia COGS allows us to accelerate the profitability of Roust International

and size of the International business

• Operating expenses as a % of Net Sales declined from 32.7% to 29.7%

• Favorable cost reduction in almost all categories despite Roust acquisition

− Savings on staff costs - headcount optimization, integration of businesses in Russia

− Warehousing and transportation: lower costs of storage of inventories consigned to others

− Administration expenses: high costs related to restructuring in 2013

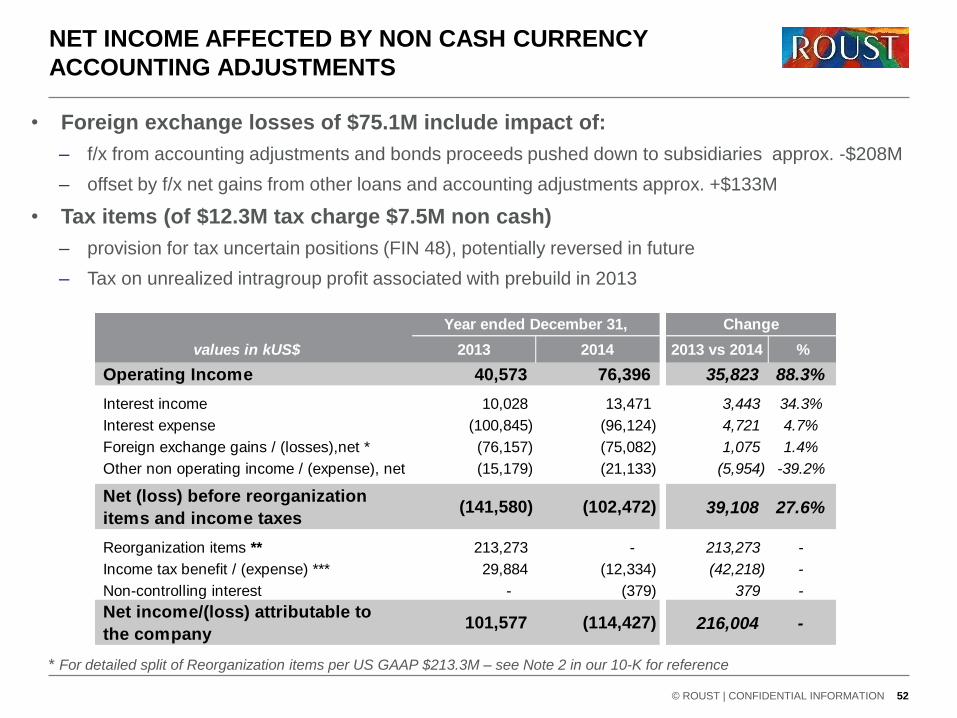

NET INCOME AFFECTED BY NON CASH CURRENCY

ACCOUNTING ADJUSTMENTS

© ROUST | CONFIDENTIAL INFORMATION 52

values in kUS$ 2013 2014 2013 vs 2014 %

Operating Income 40,573 76,396 35,823 88.3%

Interest income 10,028 13,471 3,443 34.3%

Interest expense (100,845) (96,124) 4,721 4.7%

Foreign exchange gains / (losses),net * (76,157) (75,082) 1,075 1.4%

Other non operating income / (expense), net (15,179) (21,133) (5,954) -39.2%

Net (loss) before reorganization

items and income taxes(141,580) (102,472) 39,108 27.6%

Reorganization items ** 213,273 - 213,273 -

Income tax benefit / (expense) *** 29,884 (12,334) (42,218) -

Non-controlling interest - (379) 379 -

Net income/(loss) attributable to

the company101,577 (114,427) 216,004 -

Year ended December 31, Change

* For detailed split of Reorganization items per US GAAP $213.3M – see Note 2 in our 10-K for reference

• Foreign exchange losses of $75.1M include impact of:

– f/x from accounting adjustments and bonds proceeds pushed down to subsidiaries approx. -$208M

– offset by f/x net gains from other loans and accounting adjustments approx. +$133M

• Tax items (of $12.3M tax charge $7.5M non cash)

– provision for tax uncertain positions (FIN 48), potentially reversed in future

– Tax on unrealized intragroup profit associated with prebuild in 2013

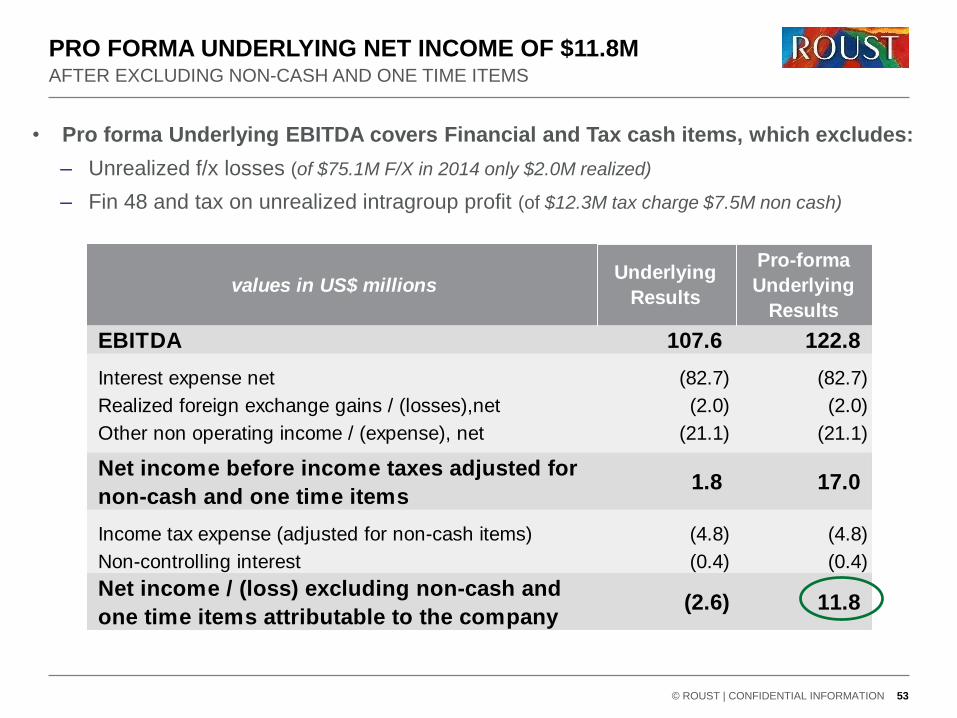

EBITDA 107.6 122.8

Interest expense net (82.7) (82.7)

Realized foreign exchange gains / (losses),net (2.0) (2.0)

Other non operating income / (expense), net (21.1) (21.1)

Net income before income taxes adjusted for

non-cash and one time items1.8 17.0

Income tax expense (adjusted for non-cash items) (4.8) (4.8)

Non-controlling interest (0.4) (0.4)

Net income / (loss) excluding non-cash and

one time items attributable to the company(2.6) 11.8

Underlying

Resultsvalues in US$ millions

Pro-forma

Underlying

Results

© ROUST | CONFIDENTIAL INFORMATION 53

• Pro forma Underlying EBITDA covers Financial and Tax cash items, which excludes:

– Unrealized f/x losses (of $75.1M F/X in 2014 only $2.0M realized)

– Fin 48 and tax on unrealized intragroup profit (of $12.3M tax charge $7.5M non cash)

PRO FORMA UNDERLYING NET INCOME OF $11.8MAFTER EXCLUDING NON-CASH AND ONE TIME ITEMS

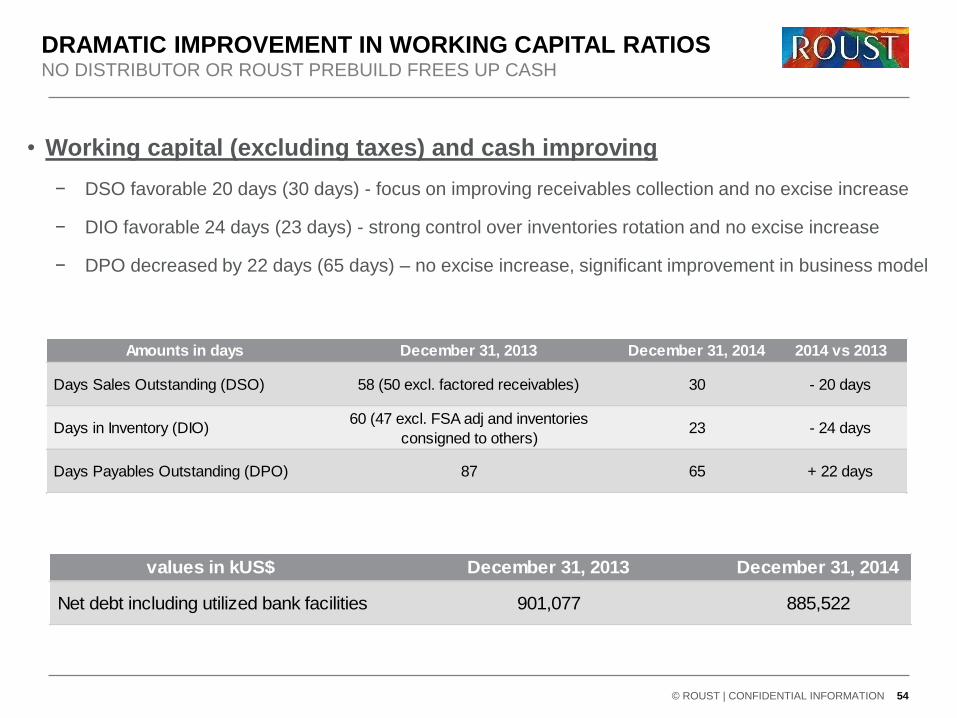

DRAMATIC IMPROVEMENT IN WORKING CAPITAL RATIOSNO DISTRIBUTOR OR ROUST PREBUILD FREES UP CASH

© ROUST | CONFIDENTIAL INFORMATION 54

values in kUS$ December 31, 2013 December 31, 2014

Net debt including utilized bank facilities 901,077 885,522

• Working capital (excluding taxes) and cash improving

− DSO favorable 20 days (30 days) - focus on improving receivables collection and no excise increase

− DIO favorable 24 days (23 days) - strong control over inventories rotation and no excise increase

− DPO decreased by 22 days (65 days) – no excise increase, significant improvement in business model

Amounts in days December 31, 2013 December 31, 2014 2014 vs 2013

Days Sales Outstanding (DSO) 58 (50 excl. factored receivables) 30 - 20 days

Days in Inventory (DIO) 60 (47 excl. FSA adj and inventories

consigned to others)23 - 24 days

Days Payables Outstanding (DPO) 87 65 + 22 days

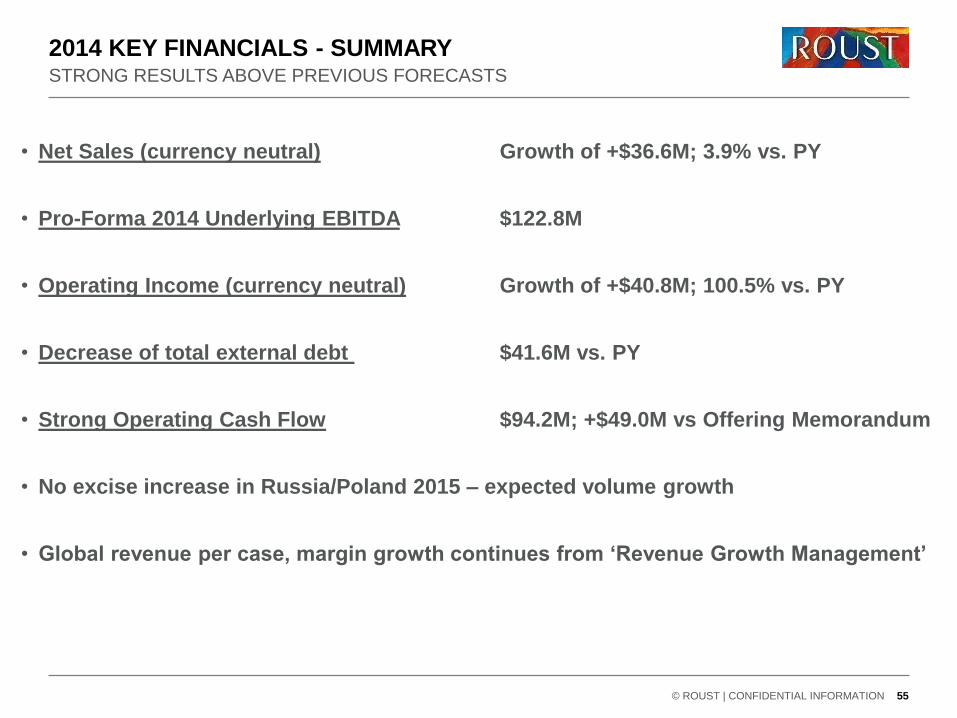

2014 KEY FINANCIALS - SUMMARY

© ROUST | CONFIDENTIAL INFORMATION 55

STRONG RESULTS ABOVE PREVIOUS FORECASTS

• Net Sales (currency neutral) Growth of +$36.6M; 3.9% vs. PY

• Pro-Forma 2014 Underlying EBITDA $122.8M

• Operating Income (currency neutral) Growth of +$40.8M; 100.5% vs. PY

• Decrease of total external debt $41.6M vs. PY

• Strong Operating Cash Flow $94.2M; +$49.0M vs Offering Memorandum

• No excise increase in Russia/Poland 2015 – expected volume growth

• Global revenue per case, margin growth continues from ‘Revenue Growth Management’

IN 2015 …

• Globalization continues: We will continue to expand our leadership in Russia, Poland

and Hungary, grow exponentially our successful Western Europe business, and rapidly

expand our Asian and American business. The lower ruble will help us profitably

accelerate our International business. The focus is on Green Mark and Żubrówka core

brands expansion.

• Renovation of core brands: By Q3 2015 we will have launched new superior

packaging for Green Mark, Parliament and Absolwent.

• Optimized portfolio: We have refocused on our critical and high opportunity SKU’s in

the last 18 months reducing from approximately 1,000 to 500 SKU’s. Given our biggest

SKUs still have large growth opportunity we will further reduce by at least 100 SKUs.

• Strong new product innovation: The successful innovation pipeline in our Polish

business will continue, and we will accelerate innovation in our Russia business with the

aim that 5% of our revenue in 2015 comes from new brands, flavors and packaging.

• Revenue Growth Management continues: Our Revenue Growth Management focus

will continue to increase our margins. We expect real price increases above inflation,

growth in high margin brands, channels, packs. In Russia we are also working with

Industry and the Government on new Retail discounts legislation that will be favorable

for our margins later in 2015.

© ROUST | CONFIDENTIAL INFORMATION 56

IN 2015 …

• Integration completion in Russia: Whilst 80% of our Integration is completed in

Russia, we still have remaining opportunities in Moscow and St. Petersburg sales

teams, Logistics platform and Head-office efficiency, estimated up to $5M in 2015.

• Perfect Outlet expansion: We will continue to expand our core brand weighted

distribution as we have successfully in Poland, Hungary, UK, Germany and France. In

Russia we will begin in Q2 the implementation of our Perfect store program driving

quality shelf presence and activation, which has been a huge success in Poland.

• Focus on quality continues: We have put tremendous work into upgrading the quality

of our product with new audit processes, equipment upgrade and consumer testing.

• Select Capital expenditure: We have large production capability and capacity,

meaning minimal capital expenditure to grow our business. We will however spend

above $10M on capital expenditures in 2015 to launch new products, expand small

package capacity and upgrade quality.

• Expand Agency partner business: We aim to expand selectively our portfolio, e.g. the

recent addition of the strong Bushmills whiskey brand in Russia, and further extent our

successful contracts with key global partners.

• Effective Industry legislation: We will continue to work actively with Industry and

Government to provide commercially effective but responsible legislation, push

programs to limit the black market, and partner with Government more effective retail

discounts legislation.

© ROUST | CONFIDENTIAL INFORMATION 57