Investor Presentationinvestor.pttgcgroup.com/misc/PRESN/2014078-pttgc... · Continues to Strive for...

46

Investor Presentation NDR in Hong Kong with SCBS / GS 7-8 July 2014

Transcript of Investor Presentationinvestor.pttgcgroup.com/misc/PRESN/2014078-pttgc... · Continues to Strive for...

Investor Presentation

NDR in Hong Kong with SCBS / GS 7-8 July 2014

Disclaimer

This presentation includes forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. This presentation contains a number of forward-looking statements including, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. PTTGC has based these forward-looking statements on its views with respect to future events and financial performance. Actual financial performance of the entities described herein could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements. Forward-looking statements represent estimates and assumptions only as of the date that they were made. The information contained in this presentation is subject to change without notice and PTTGC does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

2

Agenda

3

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

• Thailand’s largest ethane-base cracker with integrated aromatics and refining businesses • Highly competitive cost structure with pricing arrangement for gas feedstock based upon

equitable return on investment for both PTT and PTTGC • Fully integrated petrochemical and refinery operations with diversified product portfolio

covering full hydrocarbon chain • Strong footprint in fast growing regions with 5 operating countries worldwide • Committed to operational excellence targeting best in class/ first quartile business

efficiency • PTT’s Chemical Flagship

Prof

ile Incorporated on October 19, 2011 from the amalgamation of PTTAR and PTTCH

Total petrochemical capacity: 8.75 MTA

Total distillation capacity: 280 KBD

Number of employees: 3,660 persons

2013 Sales : $17.9 bn; EBITDA: $1.8bn

Asset size: $13.7 bn (as of 31/12/2013)

Foreign Limit <= 37%

Dividend Policy >=30%

Top

5 Sh

areh

olde

rs

1. PTT 48.89% 2. NVDR 9.05% 3. STATE STREET BANK EUROPE LIMITED 2.84% 4. STATE STREET BANK AND TRUST COMPANY 1.92% 5. HMC POLYMERS COMPANY LIMITED 1.85% as of Mar 6, 14

Overview of PTTGC

4

Flexible Feedstock and Secured Product Offtake

Flexible Feedstock and By-Product Enhancement

PTTGC's refinery (145 KBD) is one of the most complex refineries in Thailand, with Nelson Index of 10.17 and refining capacity accounting for 13% of country’s total capacity

Value enhancement from by-product exchange among Olefins, Aromatics and Refinery units highlights operational integration and efficiency:

- CR from Aromatics units sent to Refinery to produce middle distillate

- Pygas from Olefins unit sent to Aromatics for BTX - Offgas from Refinery sent to Cracker for olefins

products

Feedstock Supply Product Marketing

Refinery

Aromatics

Olefins / Polymers

Others

Condensate

Crude Oil

Others

Ethane, Propane, LPG

C5-C9

C10-C25

C2-C4

Olefins

100% Polymers (1)

46%

54%

Feedstock Supply Commercial Agreements Product Marketing Commercial Agreements

Customers

Others

70%

30%

1. PTT owns 50%, PTTGC and IRPC each owns 25% in PTTPM

5

Nameplate Capacity

Refinery: CDU 145 KBD Aromatics (BTX) 2,259 KTA Olefins: Ethylene 2,376 KTA Propylene 512 KTA Polymer: HDPE 800 KTA LDPE 300 KTA LLDPE 400 KTA MEG 395 KTA

Highly Competitive Cost Structure & Performance mainly driven by Olefins and Derivatives

6

94

244

1019 1030 1039 1107

1177 1199 1228

0

200

400

600

800

1000

1200

1400

MDEEthane

NAMEthane

WEPNaphtha

MDENaphtha

NAMNaphtha

MDELPG

NEANaphtha

SEANaphtha

NEA LPG

2013 Global Ethylene Cash Cost by Region USD/Ton

Source: IHS (formerly CMAI) average 2013. PTTGC cash cost takes into account the effect of the renewal of gas price agreement Note: MDE = Middle East, NAM = North America, NEA = Northeast Asia, SEA = Southeast Asia, WEP = Western Europe. MDE cash costs are average values of Iran and Saudi Arabia.

48%

20%

21% 5%

5% 1%

Adj. EBITDA Breakdown

16%

16%

56%

3% 3% 5%

Typical Revenue Breakdown

% Adj. EBITDA Margin

3 8

27

5 7 10

2

10

27

8 2

10

Refinery Aromatics Olefins andDerivatives

Green HVS PTTGC

2012 2013

s

s

Natural Gas

Crude Palm Oil

Crude

Condensate

Cracker

Aromatics Plants

Refinery

Ethylene

HDPE

LLDPE

LDPE

MEG

Propylene

Oleochemicals

Paraxylene

Benzene

PTAPET Fiber / Resin

EO

Ethanolamine

Ethoxylate

Cyclohexane

CumenePhenol

Acetone

EB / SM

PS

BPA

Methyl Ester( B - 100 )

PC

Caprolactam Nylon 6

Fatty Alcohol

MMA PMMA

Epoxy Resins

ABS

SBR

PP

PTT Phenol

Petroleum Products- LPG- Reformate- Light Naptha- Jet Fuel- Diesel- Fuel Oil

Reformate , Heavy

Naphtha

Pygas

Condensate Residue ,

Hydrogen

Light Naphtha

C 3 ,C 4

OffGas Mixed C 4 Butadiene

PO

PUTDI / HDI

Toluene

Polyols

Orthoxylene

Cracker Bottom ,

Hydrogen

PA Plasticizer

1. PTTGC does not currently produce these products.

REFINERY & SHARED FACILITIES AROMATICS OLEFINS POLYMERS EO-BASED

PERFORMANCE GREEN CHEMICALS HIGH VOLUME SPECIALTIES

Feedstock Upstream Intermediates Downstream Proximity to Suppliers and Customers

Exchange Stream Products By-Products

Potential Product Opportunities (1)

Fully Integrated Petrochemical and Refinery Operations

with Diversified Product Portfolio

3

7

Agenda

8

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

Strategic Direction

9

GREEN

CORE UPLIFT PROJECTS

1-STEP ADJACENCIES

Operational Excellence

Synergy Excellence

Debottlenecking

Marketing Excellence

NEW GEOGRAPHIES NEW PRODUCTS

ASEAN: Pertamina

CHINA: Sinochem

PC, PU, SBR, Nylon 66

System House

Compounding

Olechemical

PLA

Succinic Acid

PLA/PBS Compound

EXCELLENCE

EXECUTION

EBITDA Uplift

15-30% (2012-2017)

1st Quartile

Performance

ROIC > 14%

Listed in Globally

Sustainability Index

Leverage collaboration with PTT Group Capabilities and Organization enablers Social and environmental sustainability

Continues to Strive for Strong Profitable Growth

~800-900

~620-650

Green

563

Actual2012

Target2017

Target2022

Expected EBITDA BenefitUplift 15-30%

Phase 1 : Foundation for Growth Phase 2: The Growth Mode

Green

HVS

New Global Hub

Debottleneck

Synergy Project Excellence

Operational Excellence Marketing Excellence Capital Expenditure Excellence

We aim to grow ~5 percent p.a. in the next ten years

Sales in THB Bn Based on constant Dubai crude year 2012 at USD 109 per bbl

10

Adjusted Target • Revised Operational Excellence target • Include only projects passed stage gates

* Debottleneck EBITDA uplift includes 1Q/14 BV project starts up 3Q/15 TOCGC Plant Improvement Project 4Q/15 PX Expansion starts up Not Including PTTPE Cracker Debottlenecking and LLDPE Expansion

Original Target

Excellence Programs Update 1Q/14 EBITDA UPLIFT

Core Uplift 1-Step Adjacencies Green Business

Excellence Programs

2014 Target (MUSD)

1Q/14 Actual (MUSD)

Synergy Excellence - Heavy Gas (Offgas) - Pure H2 via PSA - C3/C4 Stream - 3 Streams (Heavy Gasoline, LCB, CB) - Heavy Aromatics

83.0 6.5

Marketing Excellence - Customer Portfolio Management - Product Development - Pricing Excellence

80.0 20.4

Operational Excellence - Total 42 projects in 2014 - 29 Energy Saving Projects - 7 Plant Reliability Projects - 6 Cost Reduction/Optimization

Projects

31.0 6.4

Total 194.0 33.3

(MUSD)

(MUSD)

11

Target COD: 2Q/14

Target COD: 4Q/14

Construction Progress at 98%

Construction Progress at 58%

Phenol 2 Project

TOCGC Plant Improvement Project

Debottlenecking & Expansion

PTTPE Cracker Debottlenecking

PX Expansion

LLDPE Expansion

2013 2015 - 2018 2014 Synergy

Pure H2 via New PSA

Off Gas upgrading at Olefins

Target COD: 3Q/15

Target COD: 4Q/15

Target COD: 3Q/15

BEP

Target : 2016 BEP

Target : 2017

Construction Progress at 34%

Construction Progress at 19%

Construction Progress at 55%

BOD approved Project

BOD approved Project

BOD approve EPC BOD approve EPC

Construction

Construction

Seek for additional and opportunities Synergy Benefits

Note: Progress as of May. 2014

Excellence Programs Updates Execution of Core uplift Projects according to Target

12

Increase Capacity

CAPEX (MUSD)

Expected EBITDA Uplift

(MUSD)

EOE +90 KTA

PX +115 KTA BZ + 35 KTA OX + 20 KTA

Phenol +250 KTA Acetone +155 KTA

12% Olefins Increase

New LLDPE +300 KTA

94.2

128.8

348

285

272

Integrated IRR

17-20%

16

34

IRR 17%

BOD approved EPC + Construction

BOD approved EPC + Construction

BOD approved EPC + Construction

Target COD: 2Q/14

Butadiene +75 KTA Butiene-1 +25 KTA

262 58 BV Project

Construction

Core Uplift 1-Step Adjacencies Green Business

13

PTTPE Cracker Debottlenecking

Existing LLDPE

400 KTA

New LLDPE

300 KTA

Metallocene LLDPE

400 KTA

Convert to

For High Performance Market Stretch film, Agriculture Film, Heavy Duty Bag, etc.

For Conventional Market Packaging Film, Rotomolding, etc.

Ethylene from Existing Contract

which will be Expired

Ethylene

Total 700 KTA Additional Ethane from PTT • 50% Vol. with Existing Pricing

Formula • 50% Vol. with Existing pricing

Formula + 100 $/Ton Additional LPG from PTT • Existing Pricing Formula

PTTPE Cracker Debottlenecking and New LLDPE Plant

Core Uplift 1-Step Adjacencies Green Business

Additional Capacity of PTTPE Cracker

12% Increase Additional Capacity LLDPE 300 KTA

CAPEX 285 MUSD CAPEX 272 MUSD

Integrated IRR- 17-20% Target Completion 2016 Target Completion 2017

Execution > 5 Growth Projects in the next 5 years 1st Screen for Further Feasibility Study

14

PC Compounding

Commodity Compounding

1st Screen for Further Feasibility Study

Not qualify for 1st Screen

New Application Compounding

Using additives and modifiers to result with a particular color, texture, strength, and etc.

Blending two or more types of polymers together

Polymer Compounding

PU Chain System House HDI Derivatives

Bio-plastics Compounding

Ethylene

HDPE

LLDPE

LDPE

MEG

Propylene

Oleochemicals

Paraxylene

Benzene

PTAPolyester Fiber

EOEthanolamine

Ethoxylate

Cyclohexane

Cumene

Phenol

Acetone

EB/SM

PS

BPA

Methyl Ester(B-100)

PC

Caprolactam Nylon 6

Fatty Alcohol

MMA PMMA

Epoxy Resins

ABS

SBR

PET Resin

PTT Phenol

- LPG- Reformate- Light Naptha- Jet Fuel- Diesel- Fuel Oil

Toluene

PO

Mixed C4 Butadiene

Polyols

PP

SystemHouse

HDI

TDI

PU

HDMA

Orthoxylene PA

Plasticizer

PLA Plant PLA

Succinic Acid Plant Succinic Acid

Petroleum Products

Nylon 6,6Adipic AcidPhenol

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

Business Direction

Compounding Strategy Serving the Customers’ Needs

15

Global Compounding Market (2012)

Compound 18,900 KTA

Global Compounded Market

(Auto + E&E)

Commodity Compounding

Using additives and modifiers to result with a particular color, texture, strength, and etc.

1. Seeking Business Partner by JV/Acquisition

2. Market Back Development

3. Compounding

• PC, ABS, PC/ABS Nylon 6 Nylon 66, PE, PP, PS, PPE, PPS, PVC, PBT/PET

Forward Integration Extreme

Temperature Plastics

High Temperature Plastics

Engineering Plastics

Commodity Plastics

AMORPHOUS SEMI-CYRSTALLINE

Thermoplastic Portfolio

New Application Compounding

Blending two or more types of polymers together

Compounding Polymer Producers Customers

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

1. Seeking for Business Partner by JV/Acquisition

2. In-house R&D development

Value Chain Forward Integration

Backward Integration

∼5-15% ∼8-30% ∼6-15%

Backward Integration

EBITDA Margin

Vencorex Business Directions Focusing its activities toward specialty Isocyanates

16

Isocyanate

HDI

TDI

MDI

Transaction: • Investment transaction completed on May 31, 2012 • 51% stake – Investment capital to ₤121 million Objective: • To step into HVS (PU Chain) by using the technology and

knowhow (TDI & HDI) from Vencorex • Maintain existing business and expand business in Asia • Forward integration into downstream

51% 49%

Business Directions

1. Expand and enhance HDI Business

2. Continue R&D for TDI and HDI Process Improvement

3. Utilizing TDI technology in Asia where demand is growing

4. Stop TDI Production in France from maturing market

5. Seek for Business Partner of Isocyanates & PU to expand the Business in Asia

Rationale of Investment

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

Polyols Propylene Oxide (PO)

Toluene

Benzene

Propylene

Butadiene

Propylene

HMDA

1

2

JV / Acquisition

JV / Acquisition

Bio-Polyols

Polyols

Formulation

Polyurethane Flexible & Rigid Foam (69%)

Polyurethane Coating and Paint (16%)

Polyurethane Elastomers and Others (15%)

Polyurethane

System House

3

Seeking for JV/Acquisition

General Information of Indonesia

New Geographies : Capturing Asian Demand JV with Pertamina

17

Signed HOA JV Manufacturing

2013 2015 - 2018 2014

COD New Cracker + Downstream Petrochemical

Target: 2018

Distribution of PTTGC’s products in Indonesia

Finalize Site Location and Setup JV Company

Signed JV Marketing & Trading

Incorporation Marketing and Trading JV Target July’14

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

Competitive advantage over size and vicinity

World-scale integrated petrochemical complex covering upstream to downstream

Pave a way towards HVS product offering

Estimated investment of USD 4-5 bn

Expected COD 2018

Polymers and Other HVS

Pertamina is Indonesia’s largest corporation, active in all segments of the energy value chain

Capital: Jakarta

Major City: Jakarta, Bandung, Surabaya, Medan

Surface Area: 1,904,443 sq km

Geography: Archipelagic

Language: Bahasa Indonesia (official) and English

Religion: Islamic, Buddhism, Hinduism

Population: 237 million (2012)

Labor Force: 120 million (2012)

Unemployment rate: 6.7% (2012)

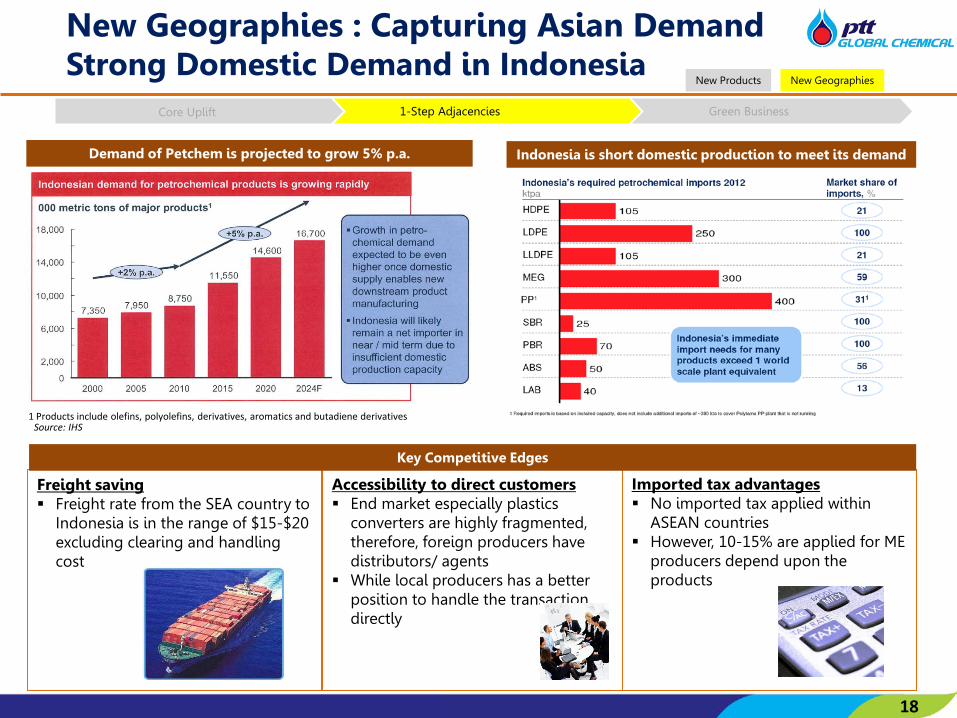

Freight saving Freight rate from the SEA country to

Indonesia is in the range of $15-$20 excluding clearing and handling cost

Accessibility to direct customers End market especially plastics

converters are highly fragmented, therefore, foreign producers have distributors/ agents

While local producers has a better position to handle the transaction directly

New Geographies : Capturing Asian Demand Strong Domestic Demand in Indonesia

18

Imported tax advantages No imported tax applied within

ASEAN countries However, 10-15% are applied for ME

producers depend upon the products

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

Key Competitive Edges

1 Products include olefins, polyolefins, derivatives, aromatics and butadiene derivatives Source: IHS

Demand of Petchem is projected to grow 5% p.a. Indonesia is short domestic production to meet its demand

New Geographies : Capturing Asian Demand

19

2013 2015 - 2018 2014

Study for Backward

Integration

Cooperation on Trading activities in China

Study of possible of downstream Petrochemical

Core Uplift 1-Step Adjacencies Green Business

New Geographies New Products

To secure access to China downstream market Signed MoU to jointly explore potential collaboration e.g., PU and

PC chains and Bio-based chemicals Strengthen sales & market in China

Sinochem Corporation is a Chinese conglomerate primarily engaged in the production and trading of chemicals and fertilizer and exploration and production of oil.

Transformation of Myriant to PTTGC’s Biotechnology R&D Center

20

Transforming into World Class Biotechnology R&D Center

R&D Technology and Knowhow Transfer

Products in the Pipeline Progress

14 KTA Semi-Commercial Plant in operation at Lake Providence, Louisiana

R&D Phase I: Lab-level Economics

Licensed to Purac, business partner in Spain, and is producing at commercial scale.

R&D Phase I: Lab-level Economics

Applications

From R&D Products

Applications Market

Butanediol (BDO) (SAC)

Core Uplift 1-Step Adjacencies Green Business

Green Business Roadmap

Succinic Acid(SAC)

Butanediol (BDO)

Poly butylene Succinate (PBS)

PLA/PBSCompound

Lactic Acid(HLA)

Poly Lactic Acid(PLA)

Acrylic Acid

Corn/Sugars

CellulosicFeedstock Polyacrylic

Acid/Acrylic ester

PLA Resin

Muconic Acid Adipic Acid

• Located in Boston, Massachusetts which fully equipped with R&D Resources and Facilities

CAPEX to Support Growth Approved and Uncommitted CAPEX Plan for year 2013 - 2017

21

5 Years Investment CAPEX

193 246 247 256 234 234

175 59 35

325 410

103

3 0 0

19 49

46

95

15 25

26

25

32

4

738

790

463

357

249 260

545 544

216

101 15 25

2013A 2014 2015 2016 2017 2018

Green1-stepCore upliftPhenolAnnual MaintenanceTotalTotal Growth Project

Approved CAPEX Plan 2014 -2018 Unit: USD mn

*

* Including the 40% acquisition of Phenol and Phenol 2 Project

Agenda

22

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

1Q/14 Business Highlights Performance Soften from Weak Aromatics Market and Key Performance Plant Shutdowns

(Unit: Million Baht) 1Q/13 4Q/13 1Q/14 Change YoY

Change QoQ

Sale Revenue 141,309 154,599 146,366 +4% -5%

EBITDA 16,419 14,089 10,999 -33% -22%

EBITDA Margin (%) 12% 9% 8% -35% -18%

Net Profit 12,075 7,421 6,296 -48% -15%

Earnings Per Share (Baht/share) 2.68 1.65 1.40 -48% -15%

Adjusted EBITDA 17,062 12,763 11,574 -32% -9%

Adjusted EBITDA Margin (%) 12% 8% 8% -35% -4%

23

Business Environment and Operations Recap

24

Dubai crude reduced from average at 106.8 $/BBL in 4Q/13 to average 104.5 $/BBL in 1Q/14 from higher non-OPEC supply despite the unrests in oil producing countries. Therefore, contributing to Stock loss (Net NRV) of 575 MB

FX Gain amounting to 602 MB, from Baht appreciation from end 4Q/13 at 32.95 Baht/USD to end 1Q/14 at 32.58 Baht/USD

Aromatics price dropped while Olefins and Refinery improved

Diesel-Dubai 17.8 USD/BBL -9% YoY 0% QoQ FO – Dubai -8.5 USD/BBL -15% YoY +19% QoQ PX-Cond 387 USD/Ton -42% YoY -23% QoQ BZ-Cond 380 USD/Ton -12% YoY +10% QoQ HDPE 1,554 USD/Ton +5% YoY +1% QoQ MEG 1,182 USD/Ton -8% YoY -2% QoQ

Overall utilization rate of major businesses

*Source: BOT Selling Rate

109.1

105.5

116.1

106.4 106.3 107.5 108.2

100.8

106.3 106.8 104.5

90

95

100

105

110

115

120

Average Dubai Crude Price USD/BBL

Average and Closing FX : THB/USD*

1Q/13 4Q/13 1Q/14YoY

% + /(-)QoQ

% + /(-)Refinery CDU Utilization (%)

101 103 101 +0 -2

Aromatics BTX Utilization (%)

92 93 91 -1 -2

Olefins Utilization (%)

97 93 77 -20 -16

Polymers Utilization (%)

109 111 99 -10 -12

EO Based MEG Utilization (%)

97 86 65 -32 -21

Green ME Utilization (%)

101 137 111 +10 -26

FA Utilization (%) 132 125 113 -19 -12Phenol Phenol Utilization (%) 126 130 78 -48 -52

31.2 30.9 31.1 31.5 31.5 30.8 29.9 30.0 31.6 31.8 32.8

30.99

31.97

30.97 30.78

29.45

31.27 31.53

32.95 32.58

2012 2013 1Q/12 2Q/12 3Q/12 4Q/12 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Average FX Closing FX

Overview of Business Units’ Performance Drop in Olefins and Derivatives’ Margin

25

47%

20%

21%

6% 6% 0% 19%

8%

65%

3% 2% 3%

146,366 MB

11,574 MB

Adjusted EBITDA Sales Revenue

1Q/2014

% EBITDA Margin 1Q/2013 4Q/2013 1Q/2014 Business Unit :

Refinery 3 3 3 Aromatics 14 5 3 Olefins and Derivative 30 24 24 Green 8 10 4 HVS 4 1 3

Average 12 8 8

Change in Olefins and Derivatives adj. EBITDA

Unit: MB

EBITDA margin

1Q/2013 1Q/2014 30% 24%

YOY Volume +/- %

Olefins -33% PE -5%

MEG -15%

YOY Price +/- %

Ethylene 3% HDPE 5% MEG -8%

9,574 9,334

7,744 7,382 7,301 7,301 7,547 7,547

240

1,589

362 81 360 114

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

Strong Financial Position

26

Key Financial Ratios

As of Mar. 31, 2014 As of Dec. 31, 2013

THB 432 Bn THB 432 Bn

Cash + ST Investment

CA

PPE

Non CA

Share holders’ Equity

IBD

Liab.

Statements of Financial Position Interest Rate Currencies

64 % Fixed 52 % THB

36 % Float 48 % USD & Others

Loan Type

• Cost of long term debts ~ 4.79% (Include W/H Tax)

• Average loan life after refinancing - 4.88 Years

Treasury policy Net IBD to Equity ratio of ≤ 0.7x Net IBD to EBITDA ratio of ≤ 2.4x

THB 119 Bn

THB Bn

* After Refinance

41 41

231 231

116 112

44 48

245 251

120 119

67 62

15.36

8.94 9.86 14.93 14.43

7.83 11.76

0.68

32.63

0.28

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

PTTGC PPCL Others

1.30 1.34

0.31 0.28

0.0x0.3x0.6x0.9x1.2x1.5x

31 Dec. 13 31 Mar. 14

Net IBD / EBITDANet IBD/Equity

14.44%

11.51% 9.42% 7.97%

5%

10%

15%

20%

31 Dec. 13 31 Mar. 14

ROE ROA

Maturity of Financial Debt* as at Mar. 31, 2014 Key Financial Ratios

Agenda

27

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

2014 Market Outlook

28

Crude

IEA forecasted demand of crude increase 1.3 mbd supported by gradual economic recovery led by Europe and the US.

Expects Dubai price to maintain around 104.2 USD/bbl for year 2014

Increase in supply from US shale gas, while sanction measure in Iran and Libya ease. Net crude supply additional of 1.4 mbd, pressuring crude price.

Aromatics

BZ spread will maintain from last year despite higher capacity addition.

PX spread soften from addition supply while demand laggard.

Ethylene, Polyethylene, and MEG

Ethylene price should maintain at a high level from short of supply

Polyethylene price will remain at high level in 2014 from constant demand for commodity plastics.

MEG’s margin is expecting to improve in 2H/2014 due to many plants in Asia and ME will shutdown for annual maintenance

Conclusion Year of Excellence Execution

29

• Expect an uptrend of Petrochemical industry, especially for Olefins & Olefins Derivatives

• Expect better Plant Utilization Rate for the rest of the year, especially for Olefins and Olefins derivatives from increasing gas supply from PTT

• Focus on Excellence Execution • Operational and Marketing Excellence

• Synergy Projects

• Debottlenecking/Expansion Projects • TOCGC Plant Improvement Project • PX Expansion • Phenol 2 • PTTPE Cracker Debottlenecking • LLDPE Expansion

• To Finalize Site Location and Setup JV Company with Pertamina

• Strengthen cooperation between PTTGC and Sinochem

Agenda

30

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

1Q/2014 Performance by Business Unit

Market outlook Detail

Refinery Performance Improved Mkt GRM

31

ULG

95

- D

B

JET

- D

B

Die

sel

- D

B

FO -

DB

14.4 13.7 18.4

14.6 12.4 9.2 14.6

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

17.8 17.5 20.3

15.3 17.0 17.3 17.0

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

19.1 17.9

19.6

16.8 17.3 17.7 17.8

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

-3.4 -8.1 -7.4

-3.7

-10.7 -10.5

-8.5

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Petroleum Product Spread (USD/BBL)

+58% QoQ -21% YoY

-2% QoQ -16% YoY

0% QoQ -9% YoY

+19% QoQ -15% YoY 4.71 3.52 4.37

2.38 3.48 3.42 4.48

(0.30)

0.84

(0.91)

(2.45)

4.21

1.11

(0.69)

0.35 0.78 0.27 1.23

0.98

0.78 0.33

4.76 5.14 3.73

1.16

8.67

5.31 4.12

(10.00) (8.00) (6.00) (4.00) (2.00) - 2.00 4.00 6.00 8.00

(4.00)

(2.00)

-

2.00

4.00

6.00

8.00

10.00

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Market GRM Stock Gain/(Loss) Net NRV

Hedging Gain/(Loss) Accounting GRM

Gross Refinery Margin (USD/BBL)

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Market GRM 4.71 3.52 4.37 2.38 3.48 3.42 4.48

GRM on CRS 2.97 2.87 3.08 2.38 2.90 2.98 2.85

GRM on CDU 5.84 4.37 5.50 2.73 4.31 4.31 5.52

Total Intake (KBD)

100% 91% 101% 63% 98% 103% 101%

Sales Volume (KBD)

-9% QoQ -3% YoY

CDU U-Rate

7% 8% 9% 5% 9% 8% 5% 13% 14% 15% 13% 15% 13% 14%

55% 51% 50% 54% 52% 49% 52%

9% 12% 11% 10% 12% 15% 13% 16% 14% 14% 16% 12% 15% 16%

194 166 180 111 176 196 185

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Naphtha + Ref.

Jet

Diesel

Fuel Oil

Others

-5% QoQ +3% YoY

Note: In 2Q/13, Refinery had Planned Turnaround of 38 days

145.9 132.4 146.3 91.8

142.4 149.1 146.5

51.0 54.7 57.8

36.0

55.5 69.4 52.5

196.9 187.1 204.1

127.8

197.8 218.4 198.9

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Crude Condenstate Residue & Others

946 922 948 871

930 937 917

1,484 1,479 1,618

1,409 1,440 1,440

1,304 1,207

1,301 1,379

1,286 1,258 1,283

1,297

800

1000

1200

1400

1600

1800

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Condensate Erawan PX FECP BZ Spot Korea

Aromatics Performance Soften PX hitting hard on Aromatic Business

Pri

ces

PX

FEC

P -

Co

nd

B

Z S

po

t -

Co

nd

Aromatics Products Prices and Spread (USD/Ton)

-23% QoQ -42% YoY

+10% QoQ -12% YoY

539 557 669

539 510 502 387

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

261 380 430 415

328 346 380

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

257 297 394

325 260 222

166

(1.58) (0.19)

-

(0.81)

- -

-

12.57 17.47

(1.45) (45.97)

84.10

26.94

(7.90)

268 314

393

278

344

249

158

(100)

-

100

200

300

400

(100)

-

100

200

300

400

500

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Market P2F Hedging Gain/(Loss)Stock Gain/(Loss) Net NRV Accounting P2F

Products to Feed Margin (USD/Ton BTX)

14% 10% 13% 12% 11% 6% 12%

26% 28% 26% 26% 31% 30% 25%

37% 38% 39% 36% 37% 39% 38%

24% 23% 22% 26% 22% 24% 24%

3,262 3,346 824 810 876 836 806

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

BZ Group

PX Group

NaphthaGroupOther By-Products

BTX U-Rate and Sales Volume (KTons)

86% 90%

92% 84% 91% 93% 91% BTX U-Rate

32

Olefins and Derivatives Performance Strong HDPE Price but impact from shutdown and soften MEG

Pri

ces

MEG

AC

P –

0.6

5Eth

ylen

e H

DP

E -

Nap

hth

a

Olefins Derivatives Prices and Spread (USD/Ton)

-13% QoQ -35% YoY

+5% QoQ +19% YoY

Adjusted EBITDA Margin

U-Rate (%)

436 566 521 585 568 590 620

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

379 323

-

375 351 284 281 245

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14HDPE (FILM) SEA 1,380 1,488 1,482 1,443 1,489 1,536 1,554LLDPE CFR SEA 1,354 1,487 1,477 1,433 1,490 1,549 1,560LDPE CFR SE Asia 1,362 1,534 1,459 1,444 1,569 1,664 1,639MEG ACP 1,179 1,202 1,282 1,173 1,143 1,208 1,182Naphtha MOPJ 943 921 961 858 920 946 935

1,380 1,488 1,482 1,443 1,489

1,536 1,554

1,179 1,202 1,282

1,173 1,143 1,208 1,182

943 921 961 858 920 946 935 700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

HDPE (FILM) SEA LLDPE CFR SEA LDPE CFR SE Asia

MEG ACP Naphtha MOPJ

87% 90% 88% 90% 96% 88% 86%

13% 10% 12% 10% 4% 12% 14%

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Gas Naphtha

27% 27% 30% 28% 26% 24% 24%

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

GAS : NAPHTHA

+1% QoQ +5% YoY

33

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14Olefins 88% 90% 97% 93% 75% 93% 77%HDPE 99% 106% 109% 96% 106% 113% 93%LLDPE 100% 103% 113% 72% 113% 114% 99%LDPE 88% 76% 101% 99% 5% 101% 115%MEG 88% 94% 97% 100% 92% 86% 65%

Sales Volume (KTons)

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14Olefins 748 756 200 218 147 190 134 HDPE 778 834 216 193 208 217 202 LLDPE 396 397 102 70 119 107 98 LDPE 273 218 75 71 25 47 72 MEG 249 372 83 104 95 89 71 Total 2,445 2,577 676 657 594 650 578

Phenol and BPA Performance U-rate Drop from Planned Shutdown

Pri

ces

BP

A-P

hen

ol

Ph

eno

l-B

Z

Phenol/ BPA Prices and Spread (USD/Ton) U-Rate and Sales Volume (KTons)

Phenol 119% 126% 126% 127% 124% 130% 78%

BPA 74% 100% 64% 116% 116% 104% 70%

1,207 1,301

1,379 1,286 1,258 1,283 1,297

1,445 1,416 1,523

1,402 1,352 1,387 1,424

1,678 1,708

1,880

1,719 1,630 1,605 1,610

800

1000

1200

1400

1600

1800

2000

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Benzene Phenol BPAU-Rate

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14 Phenol (CMP) 1,445 1,416 1,523 1,402 1,352 1,387 1,424 BPA (CMP) 1,678 1,708 1,880 1,719 1,630 1,605 1,638 Benzene 1,207 1,301 1,379 1,286 1,258 1,283 1,297

34

Sales Volume (Kton)

238

115 145 116 94 104 126

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

233 292

356 317 277 218 214

2012 2013 1Q/13 2Q/13 3Q/13 4Q/13 1Q/14

Income Statement Soften from Lower Olefins U-Rate and PX Spreads

35

Note: Adjusted EBITDA = EBITDA – Stock Gain/(Loss) &NRV

MB % MB % MB % MB % MB %1 Sales Revenue 141,309 100 154,599 100 146,366 100 5,057 4 (8,233) (5)2 Feedstock Cost (112,119) (79) (128,428) (83) (121,151) (83) 8,805 8 (7,277) (6)3 Product to Feed Margin 29,190 21 26,172 17 25,215 17 (3,748) (13) (957) (4)4 Variable Cost (6,903) (5) (7,407) (5) (7,416) (5) 628 9 (38) (1)5 Fixed Cost (4,128) (3) (4,785) (3) (4,633) (3) 618 15 (106) (2)6 Stock Gain/(Loss) & NRV (643) 0 1,326 1 (575) (0) 68 11 (1,901) (143)7 Gain/(Loss) Hedging Commodity 148 0 499 0 194 0 47 32 (305) (61)8 Other Income 1,324 1 1,660 1 1,318 1 (6) 0 (342) (21)9 SG&A (2,569) (2) (3,375) (2) (3,104) (2) 535 21 (271) (8)

10 EBITDA 16,419 12 14,089 9 10,999 8 (5,420) (33) (3,090) (22)11 Depreciation & Amortization (3,952) (3) (4,381) (3) (4,202) (3) 250 6 (179) (4)12 EBIT 12,467 9 9,708 6 6,797 5 (5,670) (45) (2,911) (30)13 Financing Expenses (1,115) (1) (1,146) (1) (1,141) (1) 26 2 (5) 0 14 FX Gain/(Loss) 1,986 1 (794) (1) 602 0 (1,384) (70) 1,396 176 15 Shares of gain/(loss) (18) 0 16 0 240 0 258 1,433 224 1,442 16 Corporate Income Tax (1,220) (1) (557) (0) (373) (0) (847) (69) (184) (33)17 Net Profit After Income Tax 12,100 9 7,227 5 6,126 4 (5,974) (49) (1,101) (15)

Portion of Net Profit: 18 Shareholders 12,075 9 7,421 5 6,296 4 (5,779) (48) (1,125) (15)19 Minorities 25 0 (194) (0) (170) (0) (195) (780) 24 12

20 Adjusted EBITDA 17,062 12 12,763 8 11,574 8 (5,488) (32) (1,189) (9)

4Q/131Q/2013 1Q/14 Change YoY Change QoQ

Agenda

36

PTTGC’s Business Overview 1

Strategy and Execution 2

Operating Results 3

Market Outlook 4

Appendix 5

1Q/2014 Performance by Business Unit

Market outlook Detail

Crude Oil – More Growing Supply Winds Prices Down Slightly

• Global geopolitics e.g. Ukraine, Iran, Libya • China’s economic growth • Potentially weak currencies in Emerging

Market countries that may affect oil demand • Potential impact of US crude oil export on

global crude flows • Renewables energy e.g. significant drop in

solar pricing

IEA Maintains Oil Demand Forecast Global Oil Supply Keeps Growing

Crude Oil Price Tends to be Bearish Factors to be Watched

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 2015

OtherAsia

China ME LatinAmerica

Africa US andCanada

FSU EU Oceanea

Source: IEA

2013 2014 2015

Source: PIRA

Non OPEC

OPEC

GDP Growth (%) 2013 2014

U.S. 1.9 2.8

Euro -0.5 1.2

China 7.7 7.5

World 3.0 3.6

• A gradual economic recovery led by U.S.

• 2014 Oil Demand Growth = 1.3 MBD • U.S. and Canada crude

production increase 1.3 MBD in 2014-15 each

• Iraq, Iran and Libya will raise production 0.9 MBD in 2015

• Saudi Arabia has to cut production more 0.5 MBD in 2015 to make balance

0.38 MBD 0.35

0.24 0.18 0.17

0.09 0.07 (0.05) (0.14)

108.2

100.8

106.3 106.8

104.5 104.2 103.8 104.2

101.0

UNIT: USD/BBL

UNIT: MBD

61.2

30.8 30.8 31.0

62.6

64.3

Source: PRISM (Apr 2014)

Average 2013 2014 2015

Dubai 105.5 104.2 101.0

37

Refinery – Better-than-Expected Margin This Year due to Capacity Shutdowns and Delays

Capacity Additions Shift to 2015 Mid Dist. Lead Global Demand Growth

2014 Crack Spreads Improve Factors to be Watched

• China’s economic growth • Potentially weak currencies in Emerging

Market countries that may affect oil demand • Alternative fuel e.g. CNG, bio-fuel • More stringent environmental regulation e.g.

clean fuel policy

Source: PRISM (Apr 2014)

-200

-100

0

100

200

300

400

500

2012 2013 2014 2015

Gasoline

Jet/Kero

Diesel

Fuel Oil

Source: JBC

UNIT: KBD

-12-8-4048

12162024

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14

Diesel

Gasoiline

Fuel Oil GRM 2013 (A) = $6.7/bbl GRM 2014 (F) = $7.1/bbl

UNIT: USD/BBL

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

2012 2013 2014 2015 2016

Source: JBC

38

• 750 KBD capacity shutdown in Japan (420) and Australia (330) in 2014-15

• 760 KBD expansion in China shifted to 2015

Source: JBC

Demand Growth

UNIT: KBD

PX Demand/Supply Balance

BZ Demand from U.S. Supports Margin

60%65%70%75%80%85%90%

0.01.02.03.04.05.06.0

2012 2013 2014 2015 2016

Capacity Addition

Demand Growth

Aromatics – Competitiveness is Crucial for Survival

BZ Demand/Supply Balance

Global PX Cash Cost Curve

UNIT: MT Operating Rate Asian O/R

Global O/R

39

Source: IHS

Source: IHS Source: IHS

10%20%30%40%50%60%70%80%

-0.50.00.51.01.52.02.53.0

2012 2013 2014 2015 2016

Capacity Addition

Demand Growth

UNIT: MT Operating Rate Asian O/R

Global O/R

Asian Demand Grows Much Faster High Operating Rate in Asia

Global Ethylene Cash Cost Curve Ethylene Cash Margin is Rising

Ethylene – Firm Asian Demand Supports Profitability

40

Source: IHS

New Asian Capacity from PDH & CTO China Becomes More Self-sufficient

But China Relies on Propane Import China PDH is Higher Cash Cost

Propylene – New Capacity from On-purpose but We Can Compete

Average Demand Growth 4 MT pa.

41

Source: IHS

Source: IHS

China PDH

• Add value to mixed C4 • Save cost of purchasing butene-1 • Provide flexibility to maximize butadiene or

butene-1

Mobility Drives Demand Growth BD Demand/Supply Balance

China’s Importing is Still Growing BD Project Increases Value and Flexibility

Butadiene – Value Added to Mixed C4 with More Flexibility

58%

62%

66%

70%

74%

78%

82%

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

2012 2013 2014 2015 2016 2017 2018

America Europe Middle EastChina Other Asia Demand Growth

UNIT: MT Operating Rate

Global O/R

42

Source: IHS

Source: IHS Naphtha Mixed C4

Butadiene

Butene-1

Max BD Mode BD 75 KTA B-1 20 KTA

Max B-1 Mode BD 45 KTA B-1 40 KTA

China Dominates MEG Demand in 2013

High Operating Rate at 89%

MEG – High Operating Rate from Unreliable Coal-based Plants

43

New Capacity Comes from Coal-based

Source: IHS

Source: IHS

Expecting Low O/R from Coal-based MEG

Margin will Return H2/14 Onwards

• Quality getting better but still not accepted by polyester fiber

• Unproven logistics capability – Can they deliver on-spec on time?

%

0.00.51.01.52.02.53.0

2013 2014

Capacity Addition

Demand Growth

0.00.51.01.52.02.53.0

2013 2014

Capacity Addition

Demand Growth

0.00.51.01.52.02.53.0

2013 2014

Capacity Addition

Demand Growth

44

PE – Demand/Supply Balance with Economic Recovery Makes Margin Improved

Global PE Margins are on the Rise

2013 2014

LLDPE Demand/Supply and Spread

UNIT: MT

Spread LLDPE – MOPJ (USD/MT)

2013 2014

LDPE Demand/Supply and Spread

UNIT: MT

Spread LDPE – MOPJ (USD/MT)

2013 2014

HDPE Demand/Supply and Spread

UNIT: MT

Spread HDPE – MOPJ (USD/MT)

Source: IHS

566 625

613 686

565 637

2.17 1.70

1.54 1.40 0.57 0.59

BPA Demand/Supply Balance

UNIT: MT Operating Rate

Phenol Demand/Supply Balance

This Will Make Acetone Price High

Phenol/BPA – Acetone Will Be Great Contributor to Phenol Chain

20%30%40%50%60%70%80%90%

0.00.20.40.60.81.01.2

2012 2013 2014 2015 2016

Other Asia

China

UNIT: MT Operating Rate

Global O/R

Demand Growth

20%30%40%50%60%70%80%90%

0.00.10.20.30.40.50.6

2012 2013 2014 2015 2016

Other Asia

China

Global O/R

Demand Growth

45

Low O/R Makes Acetone Tight Supply

46

For further information & enquiries, please contact our Investor Relations Team at [email protected]

Thank You

1 Thitipong Jurapornsiridee VP - Corporate Finance & IR [email protected] +662-265-85742 Puvadol Vasudhara IR Manager [email protected] +662-140-87123 Panugorn Puengpradit IR Analyst [email protected] +662-140-87144 Prang Chudasring IR Analyst [email protected] +662-265-83275 Supika Charudhanes IR Analyst [email protected] +662-265-85336 Chutima Jarikasem IR Coordinator [email protected] +662-140-8713