Investor Presentation - Mexichem Statements In addition to historical information, this presentation...

40

Investor Presentation 1 March 2016

Transcript of Investor Presentation - Mexichem Statements In addition to historical information, this presentation...

Investor Presentation

1

March 2016

Forward-Looking Statements

In addition to historical information, this presentation

contains "forward-looking" statements that reflect

management's expectations for the future. The words

“anticipate,” “believe,” “expect,” “hope,” “have the intention

of,” “might,” “plan,” “should” and similar expressions

generally indicate comments on expectations. The final

results may be materially different from current expectations

due to several factors, which include, but are not limited to,

global and local changes in politics, the economy, business,

competition, market and regulatory factors, cyclical trends in

relevant sectors; as well as other factors that are highlighted

under the title “Risk Factors” on the annual report submitted

by Mexichem to the Mexican National Banking and

Securities Commission (CNBV).

The forward-looking statements included herein represent

Mexichem’s views as of the date of this press release.

Mexichem undertakes no obligation to revise or update

publicly any forward-looking statement for any reason unless

required by law.”

Mexichem has implemented a new Code of Ethics that rules

its relationships with its employees, clients, suppliers and

general groups. Mexichem’s Code of Ethics is available for

consulting in the following link:

http://www.mexichem.com/Codigo_de_etica.html.

Additionally, according to the terms contained in the

Securities Exchange Act No 42, Mexichem Audit Committee

established a mechanism of contact, which allows that any

person that knows the unfulfilment of operational and

accounting records guidelines and lack of internal controls of

the Code of Ethics, from the Company itself or from the

subsidiaries that this controls, file a complaint which is

anonymously guaranteed. The whistleblower program is

facilitated by a third party. The telephone number in Mexico

is 01-800-062-12-03.

The website is: http://www.ethic-line.com/mexichem

and contact e-mail is: [email protected].

Mexichem’s Audit Committee will be notified of all complaints

for immediate investigation.

2

Fourth Quarter 2015 represented a strong finish to the year

The Company demonstrated substantial resilience to major headwinds facing global industrials:

Currency Fluctuations

Volatility in Oil Prices

Recent acquisitions: Dura-Line (U.S.) and Vestolit (Germany) performed above projections

Joint Ventures (PMV with PEMEX) and the Ethylene Cracker (with OxyChem) remain on schedule and on budget – bringing Mexichem significant vertical integration

2015 accomplishments set the stage for continued profits in 2016 and beyond

3

Strategic Highlights: 2015

4

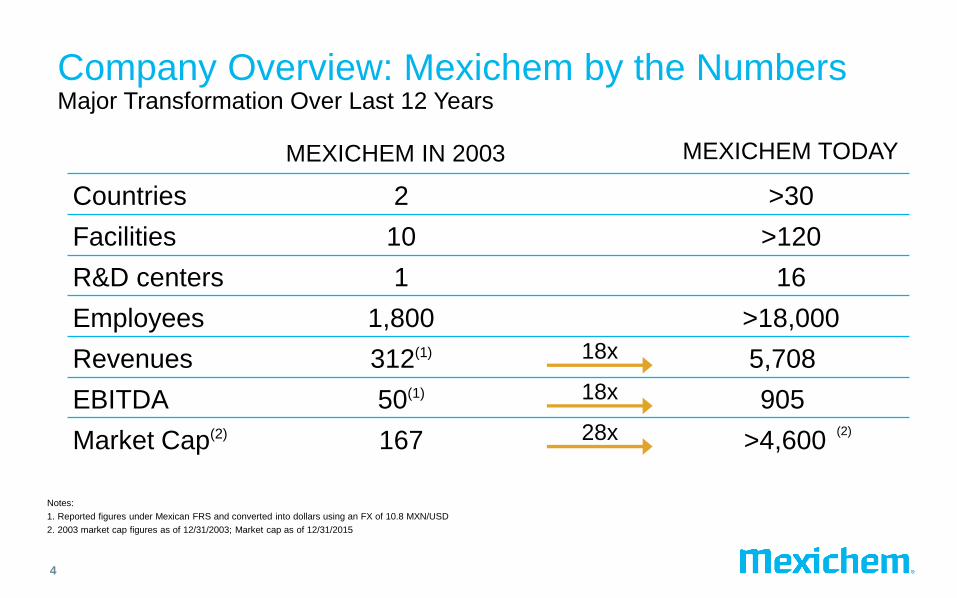

MEXICHEM TODAY

2

10

1

312(1)

167

MEXICHEM IN 2003

>30

>120

16

>4,600

18x

1,800 >18,000

Notes:

1. Reported figures under Mexican FRS and converted into dollars using an FX of 10.8 MXN/USD

2. 2003 market cap figures as of 12/31/2003; Market cap as of 12/31/2015

Company Overview: Mexichem by the Numbers Major Transformation Over Last 12 Years

Countries

Facilities

R&D centers

Employees

Revenues

50(1) 905

5,708

EBITDA

Market Cap(2)

18x

28x (2)

Mexichem at a Glance Global Leader in the Chemicals and Plastics Markets

5

Notes:

Revenues and EBITDA margin correspond to 2015; Figures before intercompany eliminations

Fluent

● Pipes and fittings

● Irrigation systems

● Datacom

Fluor ● Fluorspar

● Hydrofluoric acid

● Refrigerants

● Aluminum fluoride

Joint Venture

with

Joint Venture

with

Fluor

Value Chain

Ehylene

Value Chain

Revenuesl: $608 mm

EBITDA margin: 40%

Revenues: $2,140 mm

EBITDA margin: 15%

Revenues: $3,123 mm

EBITDA margin: 13%

Vinyl ● PVC & Specialty resins

● Compounds & plastifiers

● Derivatives

Mexichem Energy

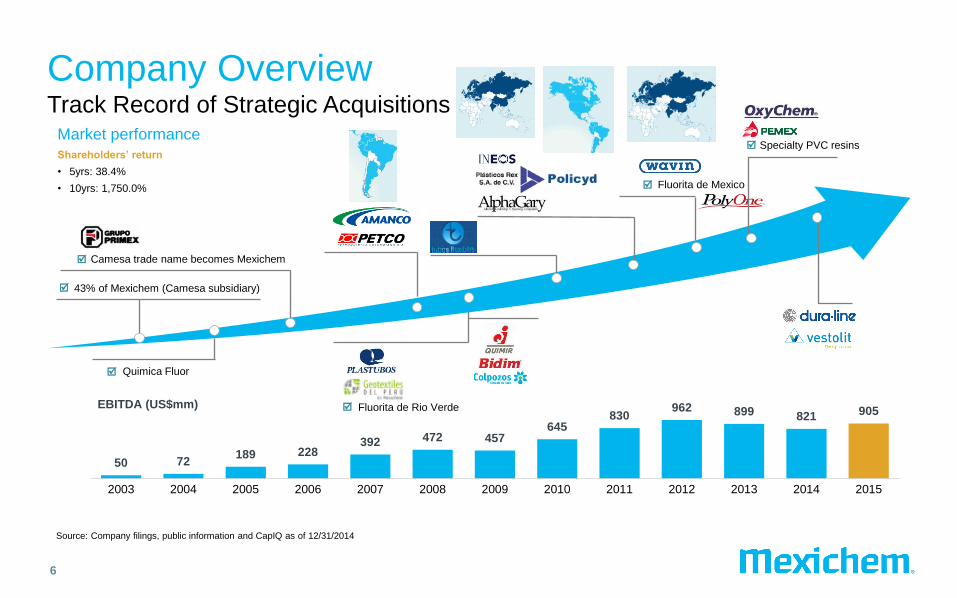

Company Overview Track Record of Strategic Acquisitions

6

50 72 189 228

392 472 457 645

830 962 899 821 905

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Company filings, public information and CapIQ as of 12/31/2014

Fluorita de Rio Verde

Quimica Fluor

43% of Mexichem (Camesa subsidiary)

Camesa trade name becomes Mexichem

EBITDA (US$mm)

Specialty PVC resins

Fluorita de Mexico

Market performance

Shareholders’ return

• 5yrs: 38.4%

• 10yrs: 1,750.0%

7

To Pipes and End-Products From Chemicals

Company Overview: Mexichem by the Numbers Major Transformation Over Last 4 Years

Sales

EBITDA

46% 34% 33% 33% 36%

20%

16% 12% 11% 10%

34% 49% 55% 56% 53%

2011 2012 2013 2014 LTM15

Vinyl Fluor Fluent

2015

38% 31% 33% 26% 35%

39% 36% 27% 31% 27%

29% 34% 42% 44% 45%

2011 2012 2013 2014 2015

Vinyl Fluor Fluent Holding

2015

EBITDA 2011 vs 2015 ($m)

Source: EBITDA as reported 2011 and 2015 figures

$196

$49

$70

$38

$26

$3

$-

$50

$100

$150

$200

$250

$300

$350

2011 2015

FluorDownstream

Brazil

Venezuela

- $202m

% from Mexichem EBITDA 35% 10%

8

Company Overview: Mexichem by the Numbers Mexichem’s EBITDA 2015 is highly affected by $202 million in comparison with 2011 by FX and market conditions on Fluor (downstream), Brazil and Venezuela

Highlights

9

1.

Vertical

Integration:

Ensuring Supply of

raw material +

Building Specialty

Product Portfolio

2.

Margin - Versus

Volume – Driven

3.

Mexichem’s Growth

Model:

Presence by

Industry and

Specific Markets

4.

Strong Financial

Position

5.

Focused

Leadership

Through

Collaboration &

Simplicity

1. Vertical Integration Ensuring Supply to Mitigate Volatility & Increase Cost Competitiveness

10

Ethylene Chain Overview

- One of the largest PVC resin and one of the leading piping player worldwide

1B - Margin/Value Added

1A - Cost and Supply

Salt

Ethane

Chlorine &

Caustic

PVC Resin

Compounds

Mexichem products

+ – VERTICAL INTEGRATION THROUGHOUT THE VALUE CHAIN

VOLATILITY

Ethylene

VCM Fluent

Specialty Resin

On-going joint ventures / announced acquisitions

1.Vertical Integration: Ethylene Ethylene is our Most Important Raw Material

11

1B - Margin/Value Added

1A - Cost and Supply

Ethylene Price Components

Ethane

27%

Others

10% Ethylene Margin

63%

Ethylene Cracker + PMV Joint Venture =

90% of the Vinyl Group’s Ethylene

Supply*

December 2014

December 2015

Others

10%

Ethane

57% Ethylene Margin

34%

Source: Company fillings, *Once PMV and Ethylene cracker are fully operational.

12

Source: IHS Chemical

1B - Margin/Value Added

1A - Cost and Supply

1.Vertical Integration: Ethylene Worldwide Ethylene Cash Costs: Amid Oil Price Declines, North America Is

The Most Profitable Region to Produce Ethylene

1. Building Specialty Products Portfolio Acquisition of Vestolit (in Vinyl)

13

Vestolit Overview

• Europe’s 6th largest PVC manufacturer

‒ Focused on specialty products

• Europe’s only manufacturer of High Impact

Suspension PVC for weather-resistant windows

• Europe’s second-largest producer of paste PVC

for floors and wallpapers, among others

• Total installed PVC capacity is 415 KTon / yr

• Vertical integration from Salt, Chlorine and VCM

through Specialty PVC resin

RATIONALE

• Integrate higher value-added products

• Synergies with PolyOne acquisition and Pemex JV

Salt

Ethane

Chlorine &

Caustic

Ethylene

VCM PVC Resin

Compounds Fluent Specialty

1B – Margin/Value Added

1A – Cost and Supply

14

389 364

280

170 150

130 112

100 100 100 100

Vinnolit Mexichem Solvay TianjinBohai

Chemical

ShenyangChemical

CNSGAnhui Hong

Sifang

KEM ONE Hanwha FPC YidongGroup

TianyeGroup

Source: IHS & Global Paste PVC Resin Industry Report 2014

1. Building Specialty Products Portfolio Specialty PVC Resins Producers Worldwide (Kton)

1B – Margin/Value Added

1A – Cost and Supply

1. Building Specialty Products Portfolio Acquisition of Dura-Line (in Fluent)

15

Dura-Line Overview

• Global leader in high-density polyethylene

(HDPE) conduit, duct and pressure-pipe

solutions

• Applications: telecom / data communications,

energy and infrastructure industries

• Manufacturing facilities: North America (US &

Mexico), India, Oman, Europe, and South Africa

• Benefits from Dura-Line’s product segments and

global footprint:

‒ Technology, market position and blue-chip

customers will allow Mexichem’s expansion

in these segments

‒ Platform for Mexichem’s products in new

geographies

Rationale

• Integrate high value-added polyethylene

products

• Enter growth markets

Salt

Ethane

Chlorine &

Caustic

Ethylene

VCM PVC Resin

Compounds Fluent Specialty

1B – Margin/Value Added

1A – Cost and Supply

Highlights

16

1.

Vertical Integration:

Ensuring Supply +

Building Specialty

Product Portfolio

2.

Margin - Versus

Volume – Driven

3.

Mexichem’s Growth

Model:

Presence by

Industry and

Specific Markets

4.

Strong Financial

Position

5.

Focused

Leadership

Through

Collaboration &

Simplicity

2. Margin Growth vs Volume Growth

17

• In May 2012, Mexichem acquired Wavin

• The leading supplier of pipe systems and solutions in Europe

• Complete portfolio for Above Ground and Below Ground Systems

• Business drivers: energy efficiency, material & resources, climate change

• Successful restructuring of operations in less than two years

‒ Cost rationalization strategy: closed 11 plants to focus on most profitable operations

‒ EBTIDA margin improvement from 2.5% in 2012 to 10% in 2015 (>4.0x increase) amid virtually flat revenue growth

Fluent Europe Revenues in EUR and in USD ($MM)

Fluent Europe EBITDA Margin(1)

(% of Total Revenue)

Note:

1. EBITDA figures exclude restructuring costs and a benefit of US$17MM in 4Q13

1,582 1,544 1,594

1,310 1,232 1,164 1,197 1,180

-

500

1,000

1,500

2,000

2012 2013 2014 2015

USD EUR

4.3%

10.3%

12.0%

2.8%

5.5%

11.2%

7.6%*

5.7% 6.1%

12.4%

14.5%

9.4%

Q1 Q2 Q3 Q4

2013 2014 2015

Sequential

improvement

18

Fluorspar

Sulphuric

Acid

HF

Aluminum

Fluoride

Refrigerant

Gases

2. Margin Growth vs Volume Growth

80%

12%

8% Gases –

134a

Gases –

Medical

Fluorspar,

HF & ALF3

0%

20%

40%

60%

80%

100%

2014 2015

Cement Steel & Others

15% 30%

Fluor EBITDA by Product (2015)

Metallurgic Fluorspar Sales Volume

($MM)

(% of total contribution)

• Fluor Business Group is focus to increase its presence on:

• Cement industry in upstream

• Medical applications in downstream

• Largest fluorspar mine in the world in one site

• Production of ~20% of global fluorspar needs and proven reserves for the next 40 years

• Mexichem has developed Fluorine-based solutions for the cement industry to optimize clinker production

• Only non-Chinese, fully vertical integrated producer of refrigerant gases

• The leading manufacturer and supplier of medical propellants:

• Around 100 million people uses propelled with Zephex®

• Propellant for 85% of the world’s metered dose inhalers

Highlights

19

1.

Vertical Integration:

Ensuring Supply +

Building Specialty

Product Portfolio

2.

Margin - Versus

Volume – Driven

3.

Mexichem’s

Growth Model:

Presence by

Industry and

Specific Markets

4.

Strong Financial

Position

5.

Focused

Leadership

Through

Collaboration &

Simplicity

20

South America

23%

Europe

35%

USA

16%

AMEA

3%

MEX & Cent.Am

23%

3. Mexichem’s Growth Model Total Sales Distribution by Region (all in USD terms)

• Our presence in >30 countries (mainly through our Fluent business) can be used as a growth platform for all our products

• Given our existing presence and potential future growth opportunities, Mexichem has identified 5 countries and 3 regions where our growth strategy will be uniquely focused:

Countries

– India

– United States

– Brazil

– Turkey

– Colombia

Regions

– Southeast Asia

– Africa

– ME

21

3. Mexichem’s Growth Model Mexichem has over 30 avenues for growth worldwide

Compounds

General Resins

Specialty Resins

Fluorspar (Met)

Chemicals

Refrigerants

Medical

H&C

Datacom

Geotextiles

Irrigation

(Mexico)

(México)

(UK)

(UK)

(Netherlands)

(USA)

(Colombia)

(Guatemala)

Category Global Expert

(Mexico)

(Colombia)

Fluent

Fluor

Vinyl 1

2

3

Business Group

Translate the strategy in Business

Case + Commercial Execution

Develop Business Case with Country

Head + Know How

Role Accountabilities P&L will be rolled up under both

parties to incentive businesses

and tracking

Results

3. Mexichem’s Growth Model Global Experts will foster and prioritize for growth in their categories, based on

the strategic plan

22

Highlights

23

1.

Vertical Integration:

Ensuring Supply +

Building Specialty

Product Portfolio

2.

Margin - Versus

Volume – Driven

3.

Mexichem’s Growth

Model:

Presence by

Industry and

Specific Markets

4.

Strong Financial

Position

5.

Focused

Leadership

Through

Collaboration &

Simplicity

• On a constant currency basis excluding restructuring charges:

Revenues and EBITDA would have increased 13% and 22%, respectively

24

4. Strong Financial Position Summary of 2015 Results

0 47 18

83

924

400

750

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2042 2044

Bank debt Debt Securities

4. Manageable Debt Profile and Long-Term Maturity Profile

25

Comfortable Debt Amortization Profile US$MM, as of December 31, 2015

More than 98% of

debt in long term

Conservative Leverage Ratios Most Debt at HoldCo Level

91%

4% 4% 1%

Holding Vinyl Fluor Fluent

Debt by Division (2015)

Alignment of Debt to Revenue Currency

Debt by Currency

(2015)

1.8x

2.4x 2.4x

2.7x 2.6x

1.1x

0.7x

1.0x

2.0x

1.9x

2011 2012 2013 2014 2015

Total Debt / EBITDA Net Debt / EBITDA

Self Imposed target of 2.0x over

medium term

58%

34%

8%

US$ Euro Others

• US$1.5B revolving credit facility (100% available)

Source: Company filings

Fitch Ratings BBB

S&P BBB-

Moody’s Baa3

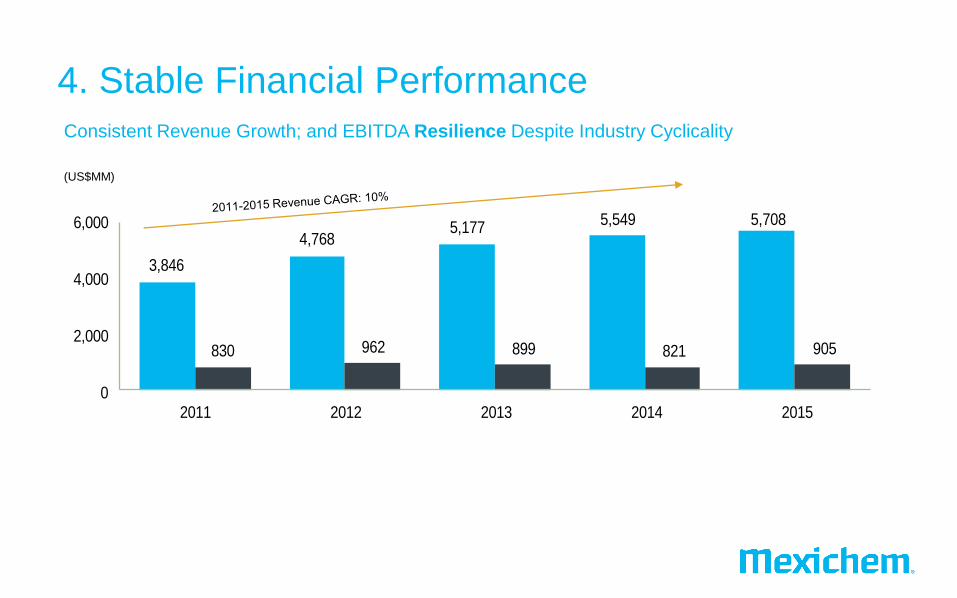

4. Stable Financial Performance

Consistent Revenue Growth; and EBITDA Resilience Despite Industry Cyclicality

(US$MM)

3,846

4,7685,177

5,549 5,708

830 962 899 821 905

0

2,000

4,000

6,000

2011 2012 2013 2014 2015

4. Consistent Investment in New Projects

27

Market

VCM

Ethane

Ethylene Salt

Chlorine

Caustic

PVC

~56% ~44%

+ = Ingleside

Cracker

OxyChem

Ingleside

VCM Facility

Mexichem

PVC Facilities

Ethylene VCM

JV with Oxychem to Build an Ethylene

Cracker

JV with PEMEX(1) to Produce Ethylene and VCM Capture the shale gas opportunity as a competitive advantage of NA

$173 $252 $276 $231 $276

$322

$725 $532

$1,061

$390

2011 2012 2013 2014 2015

Non M&A M&A CAPEX (incl. JV's)

$666

$1,292

$808 $977

$495

Capex (US$MM)

Note:

1. PEMEX’s contribution corresponds to part of Complejo Pajaritos

50%/50%

Operating Cash Flow before CAPEX/ EBITDA

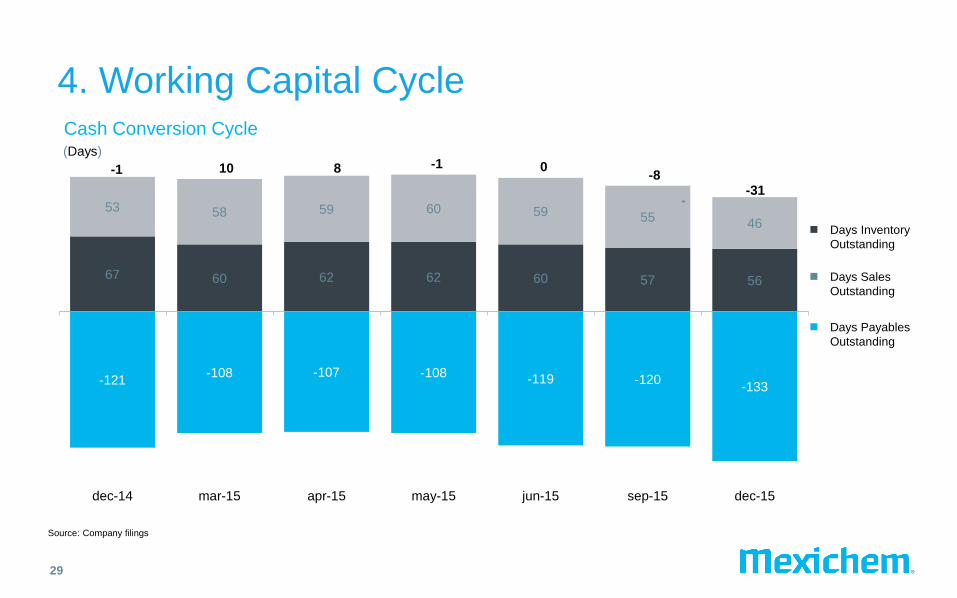

4. Strong Cash Flow Conversion

28

(US$MM)

Source: Company filings, * Including discontinued operations in UK and Rumania

65%

78%

86%

99%

2012 2013 2014* 2015*

-121 -108 -107 -108 -119 -120

-133

67 60 62 62 60 57 56

53 58 59 60 59 55 46

dec-14 mar-15 apr-15 may-15 jun-15 sep-15 dec-15

Cash Conversion Cycle

4. Working Capital Cycle

29

Days Payables

Outstanding

Days Inventory

Outstanding

Days Sales

Outstanding

Source: Company filings

(Days)

-1 10 8 -1 0 -8

-31 -

Highlights

30

1.

Vertical Integration:

Ensuring Supply +

Building Specialty

Product Portfolio

2.

Margin - Versus

Volume – Driven

3.

Mexichem’s Growth

Model:

Presence by

Industry and

Specific Markets

4.

Strong Financial

Position

5.

Focused

Leadership

Through

Collaboration &

Simplicity

31

South America

+7,000

USA

+2,000

AMEA

+30

MEX & Cent.Am

+3,000

Europe

+6,000

5. Focused Leadership Through Collaboration More than >18,000 employees

5. Focused leadership Through Collaboration

32

A. Carrillo CEO

P. Chari President, Fluent

Business Group

>30

>35

R.Guzmán CFO

M. Roef President, Fluent

Europe

>25

>25

A. Soto General Counsel

V. Aguilera President, Fluent

LatAm

>20

>35

A. Rodríguez Corporate VP, HR

G. Álvarez VP Energy

Business Group

>20

15

A. Mugica President, Fluor

Business Group

>25

>20

C. Manrique President, Vinyl

Business Group

JL. Guzmán VP Corporate

Internal Audit

>30

>20

~20 years of professional experience

Pedro Martínez VP IT

>18

Thank You

33

APPENDIX

34

Source: IHS (formerly CMAI)

0

20

40

60

80

100

120

0

500

1,000

1,500

2,000

Jan-2

01

0

Mar-

2010

May-2

010

Jul-201

0

Sep-2

01

0

Nov-2

010

Jan-2

01

1

Mar-

2011

May-2

011

Jul-201

1

Sep-2

01

1

Nov-2

011

Jan-2

01

2

Mar-

2012

May-2

012

Jul-201

2

Sep-2

01

2

Nov-2

012

Jan-2

01

3

Mar-

2013

May-2

013

Jul-201

3

Sep-2

01

3

Nov-2

013

Jan-2

01

4

Mar-

2014

May-2

014

Jul-201

4

Sep-2

01

4

Nov-2

014

Jan-2

01

5

Mar-

2015

May-2

015

Jul-201

5

Sep-2

01

5

Nov-2

015

Ethylene-Spot USA (Left) PVC Export USA (Left) Crude Oil WTI (Right)

1. Vertical Integration: Tested in 4Q14 Prices of oil and ethylene falling rapidly

35

EBITDA** without FX in 4Q14, and non recurrent effects of 4Q13

64

22

4Q13 4Q14

66

4Q13 4Q14

Vinyl Business Group

Resins, compounds & derivatives EBITDA USD$MM

~30M USD 66% 59%

Salt

Ethane

Chlorine &

Caustic

Ethylene

VCM PVC Resin

Compounds Fluent Specialty

1B – Margin/Value Added

1A – Cost and Supply

USD/ ton USD/ barrel

Fluent Business Group EBITDA* USD$MM

5%

8%

14% 10%

Source: IHS (formerly CMAI)

0

20

40

60

80

100

120

0

500

1,000

1,500

2,000

Jan-2

01

0

Mar-

2010

May-2

010

Jul-201

0

Sep-2

01

0

Nov-2

010

Jan-2

01

1

Mar-

2011

May-2

011

Jul-201

1

Sep-2

01

1

Nov-2

011

Jan-2

01

2

Mar-

2012

May-2

012

Jul-201

2

Sep-2

01

2

Nov-2

012

Jan-2

01

3

Mar-

2013

May-2

013

Jul-201

3

Sep-2

01

3

Nov-2

013

Jan-2

01

4

Mar-

2014

May-2

014

Jul-201

4

Sep-2

01

4

Nov-2

014

Jan-2

01

5

Mar-

2015

May-2

015

Jul-201

5

Sep-2

01

5

Nov-2

015

Ethylene-Spot USA (Left) PVC Export USA (Left) Crude Oil WTI (Right)

1. Vertical Integration: Margin Expansions in 4Q15 Prices of oil, ethylene and PVC resins

36

22

74

0

100

4Q14 4Q15

66

83

0

100

4Q14 4Q15

Vinyl Business Group

Positive performance on PMV + Resins, compounds & derivatives EBITDA* USD$MM

5% 26%

15% 244%

Fluent Business Group

Amid FX fluctuations, EBITDA margin expansions EBITDA* USD$MM 12%

8%

Salt

Ethane

Chlorine &

Caustic

Ethylene

VCM PVC Resin

Compounds Fluent Specialty

USD/ ton USD/ barrel

Ethylene Prices Worldwide

37

Source: IHS

Monthly World Ethylene Price – US$ per Metric Ton Last Update Date -14 /02 /2016

400

600

800

1,000

1,200

1,400

1,600

1,800

20

12

-11

20

12

-12

20

13

-01

20

13

-02

20

13

-03

20

13

-04

20

13

-05

20

13

-06

20

13

-07

20

13

-08

20

13

-09

20

13

-10

20

13

-11

20

13

-12

20

14

-01

20

14

-02

20

14

-03

20

14

-04

20

14

-05

20

14

-06

20

14

-07

20

14

-08

20

14

-09

20

14

-10

20

14

-11

20

14

-12

20

15

-01

20

15

-02

20

15

-03

20

15

-04

20

15

-05

20

15

-06

20

15

-07

20

15

-08

20

15

-09

20

15

-10

20

15

-11

20

15

-12

20

16

-01

20

16

-02

20

16

-03

20

16

-04

20

16

-05

20

16

-06

20

16

-07

20

16

-08

20

16

-09

20

16

-10

20

16

-11

20

16

-12

Pri

ce

Ethylene, Contract-Net Transaction Pipeline, Delivered US Gulf Coast Ethylene, Spot Pipeline, Average, Delivered US Gulf Coast

FORECAST

USD/ ton

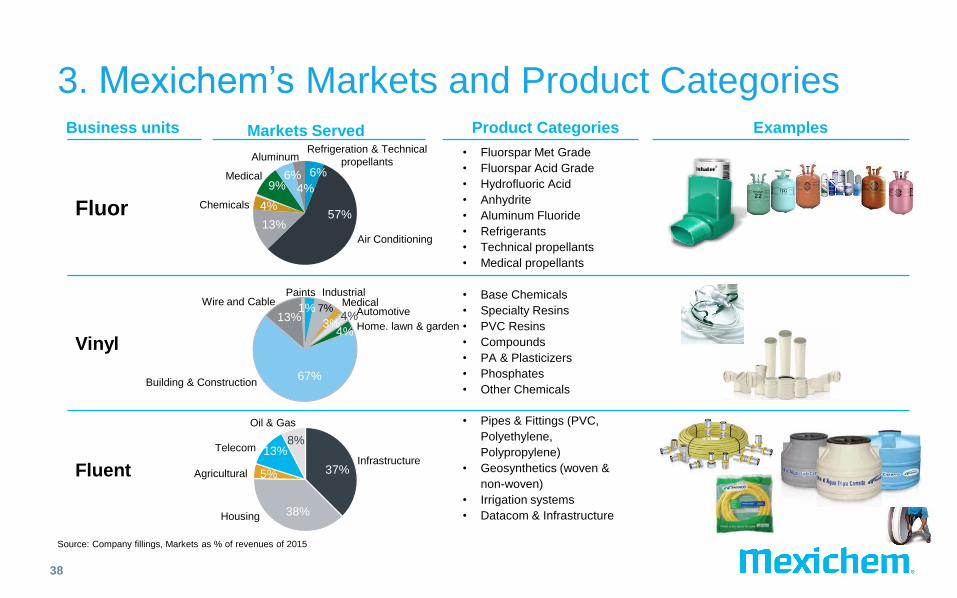

3. Mexichem’s Markets and Product Categories

38

Fluor

Product Categories Examples

Vinyl

Fluent

• Fluorspar Met Grade

• Fluorspar Acid Grade

• Hydrofluoric Acid

• Anhydrite

• Aluminum Fluoride

• Refrigerants

• Technical propellants

• Medical propellants

Business units

• Base Chemicals

• Specialty Resins

• PVC Resins

• Compounds

• PA & Plasticizers

• Phosphates

• Other Chemicals

• Pipes & Fittings (PVC,

Polyethylene,

Polypropylene)

• Geosynthetics (woven &

non-woven)

• Irrigation systems

• Datacom & Infrastructure

Source: Company fillings, Markets as % of revenues of 2015

Markets Served

6%

57% 13%

4%

9% 6%

4% Medical

Refrigeration & Technical

propellants

Air Conditioning

3% 4%

4%

67%

13% 1% Automotive

Industrial

37%

38%

5%

13% 8%

Telecom

Oil & Gas

Infrastructure

Housing

Chemicals

Building & Construction

Agricultural

7% Wire and Cable

Paints

Aluminum

Home. lawn & garden

Medical

Wholesalers 46%

Building Contractors

17%

Retail 27%

End Users 4%

Governmental Institutions

2% Other 4%

LatAm

Salt

Ethane

Chlorine &

Caustic

Ethylene

VCM PVC Resin

Compounds Specialty

Fluent

Specific Markets: Sales by Distribution Channel

39

Wholesalers 78%

Building Contractors

12%

Retail 4%

End Users 0%

Governmental Institutions

2% Other 4%

Europe

3. Mexichem’s Markets and Product Categories

39

Source: Company fillings, Information as of 2015

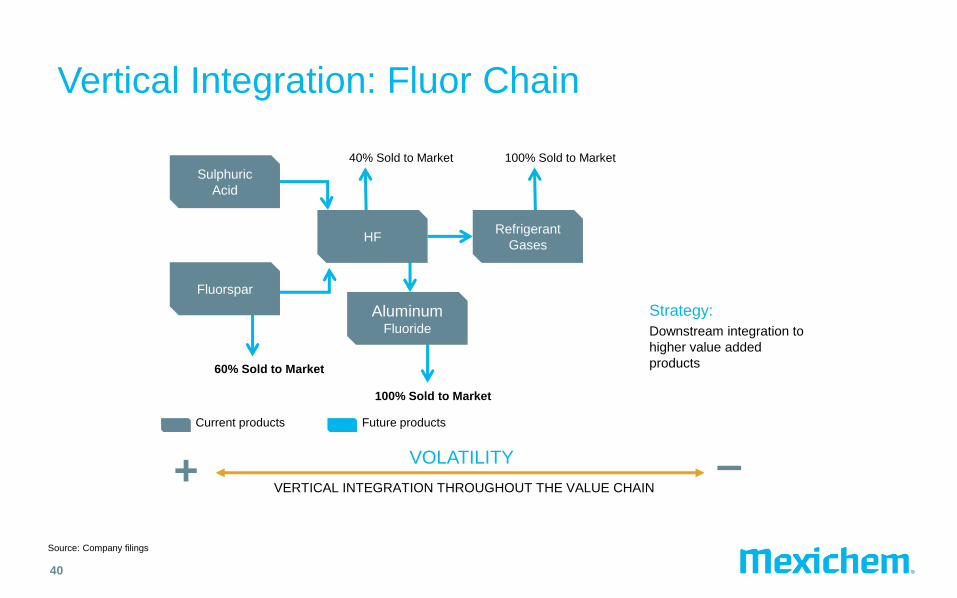

Vertical Integration: Fluor Chain

40

60% Sold to Market

40% Sold to Market 100% Sold to Market

100% Sold to Market

Fluorspar

Sulphuric

Acid

HF

Aluminum Fluoride

Refrigerant

Gases

Strategy:

Downstream integration to

higher value added

products

Current products Future products

+ – VERTICAL INTEGRATION THROUGHOUT THE VALUE CHAIN

VOLATILITY

Source: Company filings