Investor Presentation - Sound Energy Plc · Investor Presentation – Q2 2015 SLIDE 10 For more...

12

Investor Presentation – Q2 2015 SLIDE 1 Investor Presentation Q2 2015

Transcript of Investor Presentation - Sound Energy Plc · Investor Presentation – Q2 2015 SLIDE 10 For more...

Investor Presentation – Q2 2015SLIDE 1

Investor Presentation Q2 2015

Investor Presentation – Q2 2015SLIDE 2

• Active drill programme:• Second appraisal well on

Nervesa discovery underway• Badile exploration well end 2015• Wells addressing Laura and

SMG discoveries

• Strong funding position; First gas at Nervesa (2015) secures significant annual free cash flows

• Gas portfolio largely sheltered from recent oil price decline

• US$18.6M deferred and contingent consideration remaining from Indonesia

• Strong liquidity with blended institutional/retail register:• Chairman has £2.5M personally invested

Balanced Portfolio – key assets

A mid cap European oil & gas exploration/development company in the making

Reward

Dora/DallaNervesa I

Nervesa IISMG

Zibido Badile

Laura

Rapagnano

highupside

exploration

low riskexsisting

discoveries

costcovering

production

Ris

k

Investor Presentation – Q2 2015SLIDE 3

The team

London: Growth, funding, investor relations and compliance 5 people: 1 exec / 4 staff

James Parsons, Chief Executive Officer

• 23 years in Oil/Gas across Europe, South America and Central America• 12 years with Royal Dutch Shell• Specialising in restructuring, funding and growing small listed upstream companies• Strong background in upstream strategy, M&A and finance; Qualified accountant

Milan: Subsurface, operations and permitting 17 people: 2 exec / 9 staff / 6 contractors

Luca Madeddu, Italy Managing Director

• 25 years upstream experience across Europe, Asia and South America• Reservoir geologist with extensive experience in production operations,

field development, petroleum/reservoir engineering and supply chain management• Able to navigate Italian approval processes

Leonardo Spicci, Italy Technical Manager & Badile Director

• 25 years upstream experience in Europe, Kazakhstan and North Africa• Reservoir geologist with extensive experience in production operations

and petroleum/reservoir engineering• Former ENI Managing Director for Northern Italy portfolio

Investor Presentation – Q2 2015SLIDE

Investor Presentation – Q2 2015SLIDE 4

Dora/Dalla

Laura

Rapagnano

Nervesa

Badile/Zibido

Attractive Italian fundamentals

• Good scale: 3rd/5th largest producer of oil /gas in Western Europe

• Attractive gas market: High (US$9/Mscf+) prices

• Extensive gas pipeline network

• Competitive fiscal terms

• Multiple hydrocarbon plays: Deep Mesozoic oil and gas – condensate

to shallow Tertiary oil and biogenic gas

• Flexible licenses: Low initial outlay and exit costs

SMG

Investor Presentation – Q2 2015SLIDE 5

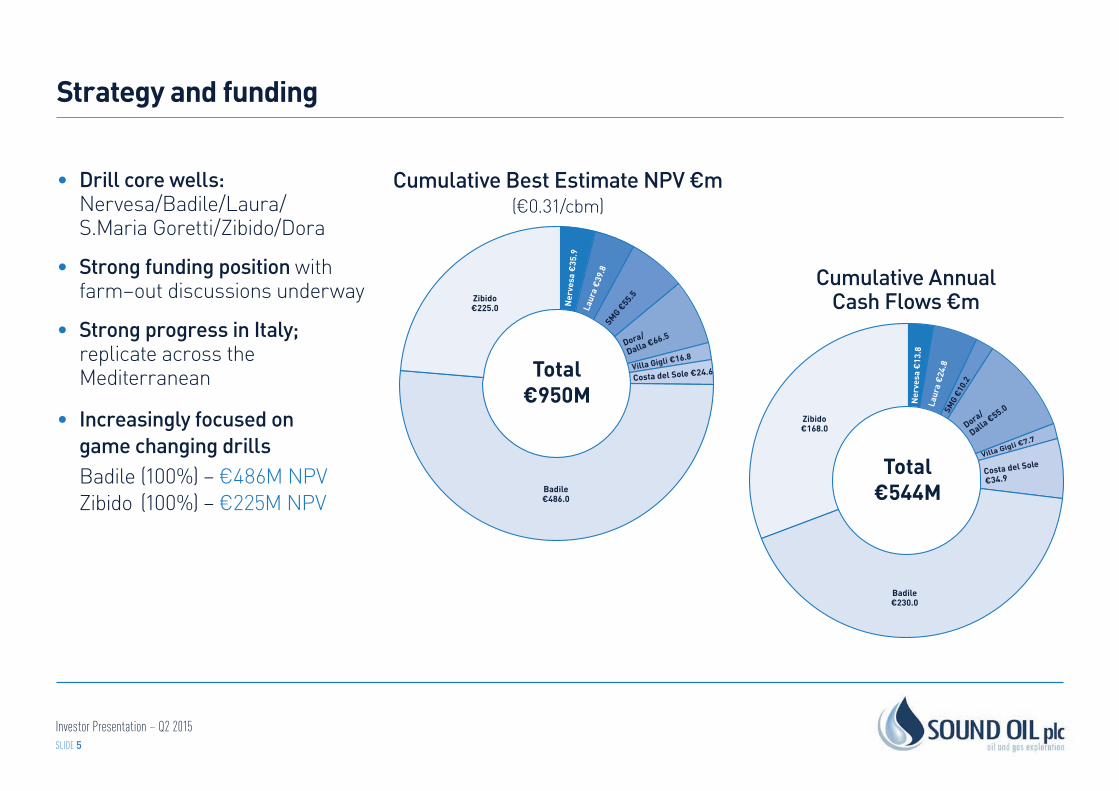

Strategy and funding

• Drill core wells: Nervesa/Badile/Laura/ S.Maria Goretti/Zibido/Dora

• Strong funding position with farm–out discussions underway

• Strong progress in Italy; replicate across the Mediterranean

• Increasingly focused on game changing drills

Badile (100%) – €486M NPV Zibido (100%) – €225M NPV

Total€950M

Zibido€225.0

Badile€486.0

Costa del Sole €24.6Villa Gigli €16.8

Ner

vesa

€35

.9La

ura

€39.

8SMG €

55.5

Dora/

Dalla €66.5

Total€544M

Zibido€168.0

Badile€230.0

Villa Gigli €7.7

SMG

€10.2

Ner

vesa

€13

.8La

ura

€24

.8

Dora/

Dalla €55.0

Costa del Sole

€34.9

Cumulative Best Estimate NPV €m(€0.31/cbm)

Cumulative AnnualCash Flows €m

Investor Presentation – Q2 2015SLIDE 6

Key development assets: “building material cash flows”

NErVESA GAS DISCoVEry, owNED 100%

rAPAGNANo GAS DISCoVEry, owNED 100%

• Veneto region• Play type: anticline structure, multiple gas

bearing Miocene sand intervals (TD 1,500-1,800m)

• 1st well drilled July 2013; flowed 2.7 million scf/day on test; first gas 2015

• 3 well development plan addressing the two fields; 2nd well currently drilling

• Potential exploration prospect• Daily webcam available for live operations

• Marche Region

• First gas achieved 15 May 2013 from the Sabbie reservoir

• 12 years production remaining

Up to €70M NPV 10(Best Estimate €36M)

Recoverableresource26.5 Bscf

3C+€18M

3C+7.7

2P3.0

3P+5.5

1C5.9

2C+4.4

2P€8M

3P+€16M

1C€13M

2C+€15M

Recoverableresource1.3 Bscf

1P€2.9M

2P+€0.5M

3P+€0.4M

2P+0.3

3P+0.2

1P0.8

Up to €4M NPV 10(Best Estimate €3M)

NPV10 (Eurocent 31/cbm) Recoverable resource (bscf)

Investor Presentation – Q2 2015SLIDE 7

Drilling existing discoveriesLAUrA• Gulf of Taranto (4km offshore, 200m water depth)• Play type: inverted fault block, gas in Pleistocene

(TD 1,300m)• Long reach deviated well from onshore• €16.2M well cost

Recoverableresource25.6 Bscf

1C12.3

1C€27M

3C+€24M

Prospective €6M

2C+€7M

Prospective 4.2

3C+7.2

2C+1.9

Up to €65M NPV 10(Best Estimate €40M)

DorA/DALLA• Adriatic Sea (21km offshore)• Play type: faulted anticline, Gas-condensate in Scaglia

Formation (TD 1,400m)• Dora gas discovery previously drilled 1972, tested 20MMScf/d• €13M well cost• Exploration potential from Dalla prospect

Potential >€81M NPV 10(Best Estimate €66M)

Recoverableresource74.5 Bscf

2C17.6

2C€19M

3C+6.4

3C+€15M

Low8.9Best

+15.7

High+25.9

Best€47M

Hightbc

Lowtbc

NPV10 (Eurocent 28/cbm)

Recoverable resource (bscf)

NPV10 (Eurocent 31/cbm)

Recoverable resource (bscf)

NPV10 (Eurocent 31/cbm)

Recoverable resource (bscf)

Up to €105M NPV 10(Best Estimate €56M,

at Eurocent 31/cbm)

Recoverableresource67.7 Bscf

Best+€36M

Low€8M

High+€61M

High+34.4

Best+23.7

Low9.7

SANtA MArIA GorEttI• Marche Region (Central Italy)• Play type: inverted fault block, gas in Pleistocene (TD 3,800m)• Southern extension of two producing gas fields• €8.5M well cost (dry hole)

Investor Presentation – Q2 2015SLIDE 8

Significant exploration potential

• Po Valley (Northern Italy) • Play type: Inverted fault block;

Gas-condensate in Mesozoic (TD 4,200m)• 45km South West of analogous

“Malossa” gas field• EIA recently approved• €22.6M (dry hole case)

ZIBIDo, owNED 100%• Po Valley; Zibido is adjacent to Badile prospect• Play type: Downthrown fault terrace

Gas/oil in Mesozoic (TD 5,600m)• Zibido P50 NPV10 €225M (Eurocent 31/cbm)

Up to €1,745M NPV 10(Best Estimate €486M)

Recoverableresource673 Bscf

Low46

High+€1,259M

Best+€385M

Best+132

High+495

Low€101M

NPV10 (Eurocent 31/cbm) Recoverable resource (bscf)

BADILE, owNED 100%

Lacchiarella 2 previously drilled

Badile drill target

Investor Presentation – Q2 2015SLIDE 9

Summary and outlook

END GAME

• European /Mediterranean focused oil and gas company of some scale

TEAM

• Balance of technical, operational financial /M&A

• High energy; Action orientated

• Cornerstone investor secured with strong relationships across Mediterranean

SHORT TERM NEWS FLOW

• Second Nervesa well

• Laura financing or farm in

• Badile permitting and farm in

• First gas Nervesa

• Badile exploration well (NPV €486M)

• Producing the Laura field (NPV €40M)

MEDIUM TERM

• SMG appraisal well (NPV €56M)

• Zibido (Badile License) exploration well (NPV €225M)

• Dora appraisal well (NPV €66M)

ASSETS

• Producing portfolio covering Italian cost base

• Low risk existing discoveries with a P50 NPV of €197M (34 pence per share)

• High upside prospects with a mid case NPV of a further €711M (48 pence per share post farm out)

Investor Presentation – Q2 2015SLIDE 10

For more information please contact:

JAMES PArSoNSChief Executive [email protected]

DETAILED INFORMATION ON OUR INVESTOR WEBSITE www.soundoil.co.uk

Disclaimer: The investment mentioned in this document may not be suitable for all recipients or be appropriate for their personal circumstances. The information in this document is believed to be correct but cannot be guaranteed. Opinions constitute our judgment as of this date and are subject to change without warning. This document is not intended as an offer or solicitation to buy or sell securities. Past performance is not necessarily indicative of future performance and the value of investments may fall as well as rise and the income from them may fluctuate and is not guaranteed. Investors may not recover the amount invested. Some securities carry a higher degree of risk than others. The levels and basis of taxation can change. The contents of this document have been prepared by, are the sole responsibility of, and have been issued by the Company.

Investor Presentation – Q2 2015SLIDE 11

12 month share price

Price analysis

• Gas focus has insulated the Company from the fall in the oil price

• Demonstrated ability to progress developments and navigate Italian permitting process

0

2

4

6

8

10

12

14

16

18

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

240.0

Mar 15

Feb 15

Jan 15

Dec 14

Nov 14

Oct 14

Sep 14

Aug 14

Jul 14

Jun 14

May 14

Sound OilBrent Crude ($)

Apr14

Mar14

Shar

e pr

ice

(p)

Brent Crude ($/barrel)

14 Apr ‘14Casa Tiberi operations commence

25 Apr ‘14Continental investment announced

09 Jun ‘14Rapagnano

Reserve Upgrade

12 Jun ‘14Laura gas discovery

permit award

15 Jul ‘14SMG CPR

29 Jul ‘14Casa Tiberi

first gas

13 oct ‘14Badile land purchase

13 Nov ‘14Nervesa RBL

signature

12 Dec ‘14Nervesa

EIA Approval

12 Jan ‘152014

Production Update

17 Feb ‘15Nervesa Drilling

Authorisation

17 Mar ‘15Badile

EIA Approval

Investor Presentation – Q2 2015SLIDE 12

Italy: infrastructure and production

High pressure gas pipeline network Oil production (million tons) – time series years 1993-2013

Production of gas (billion cubic meters) – series years 1993-2013