INVESTOR PRESENTATION Q3 2013 - PKC Group Investor Presentation Q3 2013 Maximizing current PKC...

23

INVESTOR PRESENTATION Q3 2013 October 31, 2013 Matti Hyytiäinen, President & CEO

-

Upload

vuongthien -

Category

Documents

-

view

215 -

download

0

Transcript of INVESTOR PRESENTATION Q3 2013 - PKC Group Investor Presentation Q3 2013 Maximizing current PKC...

INVESTOR PRESENTATION Q3 2013October 31, 2013

Matti Hyytiäinen, President & CEO

PKC’s Operations• Several production transfers and ramp-ups of

current and new customers’ programs on-going in Europe

• Received major recognitions and awards on quality and delivery performance from two main accounts in North America

2

Business Environment

Q3/2013 Highlights

• Truck production volumes improved from second quarter in Brazil and remained unchanged in Europe

• North American truck demand was softer than earlier forecasted

PKC’s Financial Performance

• EBITDA% was burdened by product transfers and ramp ups in Europe, and higher labour and material costs in Brazil

• Cash flow improved from the first half of the year

PKC Investor Presentation Q3 2013

Maximizing current PKC set-up

3

Strategy 2018 Update

• East/Midwest region office established in USA to focus on growth opportunities with existing and new accounts

• Decision to establish wiring systems factory in Serbia to serve existing and potential new customers in Europe

PKC Investor Presentation Q3 2013

Penetrating into APAC• Framework Agreement for Strategic

Cooperation signed with SINOTRUK on the opportunity to establish a joint venture to manufacture wiring systems for SINOTRUK and possibly also for other customers in China and abroad

Funding• The issue of 2.14 million new shares (proceeds

EUR 44.9 million) and EUR 100 million fixed rate unsecured bond maturing in 2018

• The proceeds are intended for refinancing, general corporate purposes and to enable strategy execution incl. potential acquisitions

4

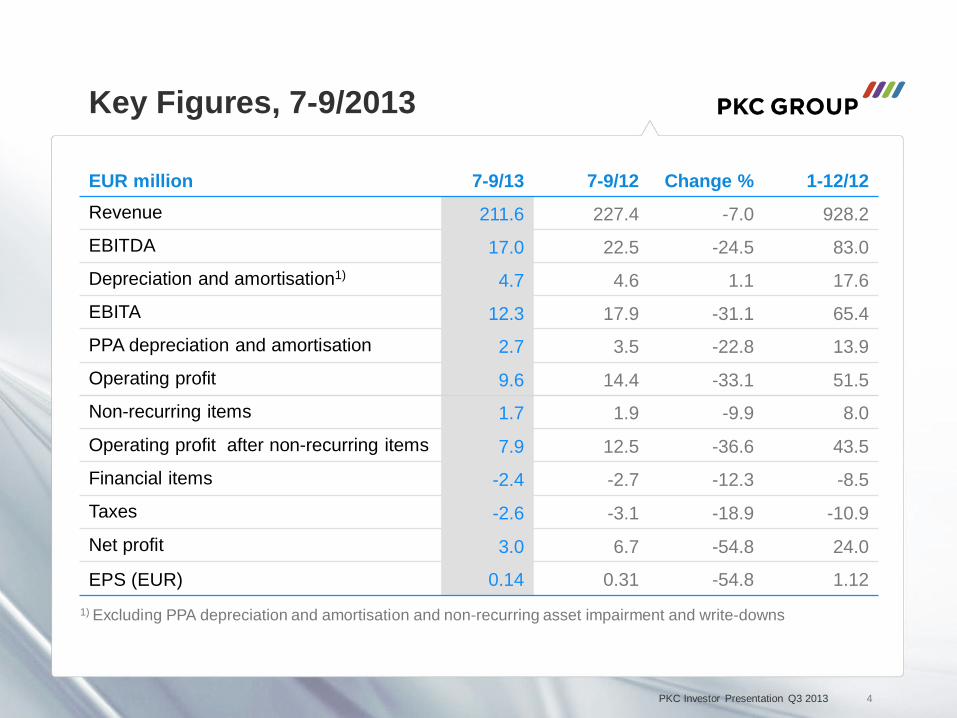

Key Figures, 7-9/2013

EUR million 7-9/13 7-9/12 Change % 1-12/12Revenue 211.6 227.4 -7.0 928.2

EBITDA 17.0 22.5 -24.5 83.0

Depreciation and amortisation1) 4.7 4.6 1.1 17.6

EBITA 12.3 17.9 -31.1 65.4

PPA depreciation and amortisation 2.7 3.5 -22.8 13.9

Operating profit 9.6 14.4 -33.1 51.5

Non-recurring items 1.7 1.9 -9.9 8.0

Operating profit after non-recurring items 7.9 12.5 -36.6 43.5

Financial items -2.4 -2.7 -12.3 -8.5

Taxes -2.6 -3.1 -18.9 -10.9

Net profit 3.0 6.7 -54.8 24.0

EPS (EUR) 0.14 0.31 -54.8 1.121) Excluding PPA depreciation and amortisation and non-recurring asset impairment and write-downs

PKC Investor Presentation Q3 2013

5

Key Figures, 1-9/2013

EUR million 1-9/13 1-9/12 Change % 1-12/12Revenue 671.9 714.2 -5.9 928.2

EBITDA 56.4 65.8 -14.3 83.0

Depreciation and amortisation1) 13.8 12.6 9.5 17.6

EBITA 42.6 53.2 -19.9 65.4

PPA depreciation and amortisation 8.4 10.6 -20.7 13.9

Operating profit 34.2 42.6 -19.7 51.5

Non-recurring items 8.3 3.2 164.3 8.0

Operating profit after non-recurring items 25.9 39.4 -34.4 43.5

Financial items -6.2 -5.2 20.5 -8.5

Taxes -7.5 -11.0 -32.0 -10.9

Net profit 12.1 23.3 -47.8 24.0

EPS (EUR) 0.55 1.09 -49.5 1.121) Excluding PPA depreciation and amortisation and non-recurring asset impairment and write-downs

PKC Investor Presentation Q3 2013

Revenue

6

242.0

225.2

244.8

235.1

227.4

211.6214.0

180

200

220

240

260

2012 2013

Q1 Q2 Q3 Q4

EUR million

PKC Investor Presentation Q3 2013

Geographical Split

56.8 %

25.7 %

9.5 %0.7 %

5.1 %

0.2 %1.9 %

0%

10%

20%

30%

40%

50%

60%

NorthAmerica

Europe SouthAmerica

APAC

Revenue 7-9/2013

Wiring Systems Electronics

120.3

65.3

20.5

5.5

EUR million

7

57.4 %

22.9 %16.0 %

0.3 %

1.4 %

2.0 %0%

10%

20%

30%

40%

50%

60%

70%

NorthAmerica

Europe SouthAmerica

APAC

Average Number of Personnel 7-9/2013

Wiring Systems Electronics

11,051

4,670

3,076

439

Temporary employees included

PKC Investor Presentation Q3 2013

Profitability

20.422.9 22.5

17.218.8

20.617.016.2

19.2 17.9

12.214.2

16.112.3

8.49.4

9.9

8.0 8.38.8

8.0

6.7

7.8 7.9

5.76.3

6.8

5.8

0

2

4

6

8

10

12

0

2

4

6

8

10

12

14

16

18

20

22

24

Q1/12 Q2/12 Q3/12 Q4/12 Q1/13 Q2/13 Q3/13

EBITDA (adjusted*) EBITA (adjusted**) EBITDA* % EBITA** %

8

EUR million %

* excluding non-recurring items in EBITDA ** excluding non-recurring items and PPA depreciation and amortisation in operating profit

PKC Investor Presentation Q3 2013

Earnings, Cash Flow and Dividend per Share

9

1.16 1.12 1.09

0.55

1.46

2.97

2.43

0.290.60 0.70

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2011 2012 1-9/12 1-9/13

Earnings per shareFree cash flow (excl. acquisitions) per shareDividend per share

EUR

PKC Investor Presentation Q3 2013

Net Working Capital

10

104.0 104.1 112.7 104.5 84.6 109.0 112.9 106.1

110.5 108.4 97.6 92.187.5

92.1 87.8 87.7

-90.8 -101.6 -91.3 -90.6 -75.5 -94.8 -90.8 -88.4

-23.0 -20.3 -22.1 -23.2-23.8

-25.3 -26.6 -23.4

-15

-10

-5

0

5

10

15

20

25

-150

-100

-50

0

50

100

150

200

250

Q4/11 Q1/12 Q2/12 Q3/12 Q4/12 Q1/13 Q2/13 Q3/13

Trade receivables InventoriesTrade payables Other liabilities and receivables***NWC* % of Revenue**

100.7 96.990.7 82.772.7

83.281.0 82.0

EUR million %

* Average of previous four quarters ** Revenue of previous 12 months

PKC Investor Presentation Q3 2013

*** related to employee benefits, taxes and financial items

Inventories Trade receivables

Cash Flow

40.0

76.060.8

16.8

-90.2

-12.3 -8.7 -10.3

-50.2

63.752.1

6.4

-100

-80

-60

-40

-20

0

20

40

60

80

100

2011 2012 1-9/12 1-9/13

Cash from operations Capital expenditure Free cash flow

11

EUR million

PKC Investor Presentation Q3 2013

110.7

56.669.4

17.8

2.1

0.70.9

0.3 0.0

0.4

0.8

1.2

1.6

2.0

2.4

0

20

40

60

80

100

120

2011 2012 Q3/12 Q3/13

Net debt Net debt to EBITDA*

Balance Sheet and Returns

12

30.033.9 32.5

39.1

05

1015202530354045

2011 2012 Q3/12 Q3/13

Equity ratio, %

72.6

34.442.0

9.0

01020304050607080

2011 2012 Q3/12 Q3/13

Gearing, %

17.015.1

19.5

9.0

18.916.7

20.1

15.2

0

5

10

15

20

25

30

2011 2012 1-9/12 1-9/13

ROE, % ROI, %

% %

EUR million %

PKC Investor Presentation Q3 2013*EBITDA of previous 12 months

13

Wiring Systems Segment, Q3/2013

• Revenue decreased 10% from previous quarter and 6% from previous year

• Headcount was reduced in Brazil despite growing volumes. Weaker real and continuing labour cost inflation had a negative impact on profitability– target is to return to profitability in 2014– actions to reduce headcount and fixed cost

are continuing– in addition, supply chain is being

streamlined

226.6

208.4

226.8

217.2

209.2

196.4196.1

180

190

200

210

220

230

2012 2013Q1 Q2 Q3 Q4

15.2

11.7

15.413.314.2

9.68.7

0

5

10

15

20

2012 2013Q1 Q2 Q3 Q4

RevenueEUR million

Adjusted Operating ProfitEUR million Illustrated net of non-recurring items

PKC Investor Presentation Q3 2013

PKC Market Share 1-9/2013

• Current business relationship with all key western OEMs in commercial vehicle industry enable future growth

• Global leader position as a target

59%41%

34%

66%

33%

67%

2%

98%

37%63%

17%

83%

North America BrazilEurope

Medium Commercial

Vehicle

HeavyCommercial

Vehicle

PKCOther

Source: PKC Group, ACT Build History October 2013, LMC Automotive forecasting Q3/2013. Note: Europe comprised of EU27 + Efta

1%

99%

APAC

0%

100%

PKC Investor Presentation Q3 2013 14

EU27+ EFTA Truck Production

050,000

100,000150,000200,000250,000300,000350,000400,000450,000500,000

Q1-Q32012

Q1-Q32013

2012 2013 2014 2015 2016 2017 2018

Heavy Trucks Medium Trucks

• Q3/13 heavy duty production volumes were flat compared to Q2/13 and up by 1% from Q3/12. Medium duty volumes decreased -4% from Q2/13

• Full year 2013 heavy duty forecast has been increased, but is still down slightly by about -1% from 2012 (previous forecast -6%) and medium truck production to remain unchanged compared to 2012 level

• Due to upcoming Euro 6 standard volumes are expected to increase in Q4/13

units

Source: LMC Automotive forecasting Q3/2013

EURO 6

-6%

-8%

-1%

0%

PKC Investor Presentation Q3 2013 15

North America Truck & LCV Production

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1-Q32012

Q1-Q32013

2012 2013 2014 2015 2016 2017 2018Heavy Trucks Medium Trucks

-15%

-10%

+7%

+7%

• Heavy duty truck production volume was down -4% from previous quarter, but unchanged year-on-year

• Full year heavy duty production estimate is down by -10%, medium duty up by +7%(earlier -6% and +7% respectively)

• LCV production volume estimate is unchanged at +5%

units

Source: LMC Automotive forecasting Q3/2013

EPA 2014

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

10,000,000

Q1-Q3

2012

Q1-Q3

2013

2012 2013 2014 2015 2016 2017 2018

+6%

+5%

Light Commercial Vehicle (Pick-up and SUV)PKC Investor Presentation Q3 2013 16

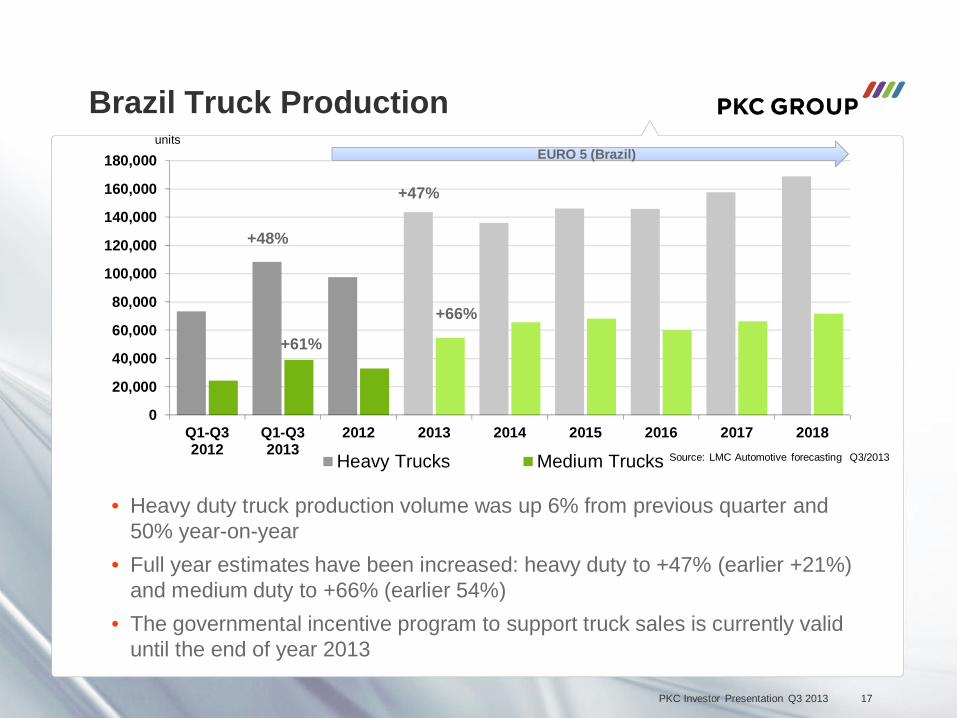

Brazil Truck Production

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Q1-Q32012

Q1-Q32013

2012 2013 2014 2015 2016 2017 2018

Heavy Trucks Medium Trucks

+47%

+66%

+61%

+48%

• Heavy duty truck production volume was up 6% from previous quarter and 50% year-on-year

• Full year estimates have been increased: heavy duty to +47% (earlier +21%) and medium duty to +66% (earlier 54%)

• The governmental incentive program to support truck sales is currently valid until the end of year 2013

units

Source: LMC Automotive forecasting Q3/2013

EURO 5 (Brazil)

PKC Investor Presentation Q3 2013 17

Market Outlook – Full Year 2013

• European truck production is estimated to remain roughly unchanged compared to 2012.

• North American heavy duty truck production is estimated to decrease by 10% and medium duty truck production to increase 7% from 2012 level.

• Brazilian heavy duty truck production is estimated to increase by 47% and medium duty truck production by 66% compared to 2012.

• PKC’s market outlook is further impacted by some light vehicle and component programs that are near end-of-life-cycle and will be ramped-down in 2013.

18PKC Investor Presentation Q3 2013

19

Electronics Segment, Q3/2013

• Revenue decreased 20% year-on-year• Profitability improvement continued

due to on-going measures to improve cost competitiveness

• Favourable product mix with stronger ODM sales

15.3

16.7

18.0 17.918.3

15.3

17.8

13

14

15

16

17

18

19

2012 2013Q1 Q2 Q3 Q4

-0.9

1.00.7

1.71.4 1.3

1.0

-1.5

-1

-0.5

0

0.5

1

1.5

2

2012 2013

Q1 Q2 Q3 Q4

EUR million

EUR million

Illustrated net of non-recurring items

Adjusted EBIT

Revenue

Market Outlook – Full Year 2013

• The demand of industrial electronic and telecommunications sector appliances is estimated to remain at the previous level

• Volumes of renewable-energy and energy saving products including smart grid solutions are expected to increase slightly

PKC Investor Presentation Q3 2013

PKC Group’s Outlook

• PKC Group estimates its full year 2013 revenue to be lower than in 2012 and estimates its comparable operating profit excluding non-recurring items not to reach 2012 level.

• In 2012 PKC’s revenue was EUR 928.2 million and comparable operating profit excluding non-recurring items was EUR 51.5 million.

20PKC Investor Presentation Q3 2013

STRATEGIC INITIATIVES

PKC’s Strategy Captures Growth Opportunities

VISION 2020

PKC is the Preferred Supplier in Electrical Distribution Systems for Transportation Industry globally.

21

Managing the Complexity

Developing PKC Uniqueness further

Maximizing currentPKC set-up

Penetrating into APAC

Exploring opportunities

to expand within Transportation

Industry

Developing Electronics business as a stand alone within PKC Group

PKC Investor Presentation Q3 2013

Long-Term Financial Targets

Annual Revenue EUR 1.4 Billion by 2018EBITDA > 10%Gearing < 75%

Dividends 30 – 60% of Free Cash Flow

Annual Revenue EUR 1.4 Billion by 2018EBITDA > 10%Gearing < 75%

Dividends 30 – 60% of Free Cash Flow

Developing PKC Uniqueness

further

Developing PKC Uniqueness

furtherMaximizing current

PKC set-upMaximizing current

PKC set-upPenetrating into

APACPenetrating into

APAC

Exploring opportunities

to expand within Transportation

Industry

Exploring opportunities

to expand within Transportation

Industry

22PKC Investor Presentation Q3 2013

PKC Group PlcUnioninkatu 20-22

FI-00130 Helsinki, Finland

www.pkcgroup.com