INVESTOR PRESENTATION Q2-2015 RESULTS JULY 23, 2015 · PDF fileINVESTOR PRESENTATION Q2-2015...

21

July 23, 2015 Page 1 INVESTOR PRESENTATION Q2-2015 RESULTS JULY 23, 2015

Transcript of INVESTOR PRESENTATION Q2-2015 RESULTS JULY 23, 2015 · PDF fileINVESTOR PRESENTATION Q2-2015...

July 23, 2015 Page 1

INVESTOR PRESENTATION

Q2-2015 RESULTS

JULY 23, 2015

July 23, 2015 Page 2

Safe Harbor Statement

This presentation contains statements about management's future expectations, plans and prospects of our business that

constitute forward-looking statements, which are found in various places throughout the press release, including , but not

limited to, statements relating to expectations of orders, net sales, product shipments, backlog, expenses, timing of

purchases of assembly equipment by customers, gross margins, operating results and capital expenditures. The use of

words such as “anticipate”, “estimate”, “expect”, “can”, “intend”, “believes”, “may”, “plan”, “predict”, “project”, “forecast”,

“will”, “would”, and similar expressions are intended to identify forward looking statements, although not all forward looking

statements contain these identifying words. The financial guidance set forth under the heading “Outlook” constitutes forward

looking statements. While these forward looking statements represent our judgments and expectations concerning the

development of our business, a number of risks, uncertainties and other important factors could cause actual developments

and results to differ materially from those contained in forward looking statements, including the discovery of weaknesses in

our internal controls and procedures; our inability to maintain continued demand for our products; the impact on our

business of potential disruptions to European economies from euro zone sovereign credit issues; failure of anticipated

orders to materialize or postponement or cancellation of orders, generally without charges; the volatility in the demand for

semiconductors and our products and services; failure to adequately decrease costs and expenses as revenues decline,

loss of significant customers, lengthening of the sales cycle, incurring additional restructuring charges in the future, acts of

terrorism and violence; inability to forecast demand and inventory levels for our products, the integrity of product pricing and

protection of our intellectual property in foreign jurisdictions; risks, such as changes in trade regulations, currency

fluctuations, political instability and war, associated with substantial foreign customers, suppliers and foreign manufacturing

operations; potential instability in foreign capital markets; the risk of failure to successfully manage our diverse operations;

those additional risk factors set forth in Besi's annual report for the year ended December 31, 2014 and other key factors

that could adversely affect our businesses and financial performance contained in our filings and reports, including our

statutory consolidated statements. We are under no obligation to (and expressly disclaim any such obligation to) update or

alter our forward-looking statements whether as a result of new information, future events or otherwise.

July 23, 2015 Page 3

Table of Contents

I. Key Highlights

II. Financial Review

III. Strategic Highlights

IV. Outlook & Summary

July 23, 2015 Page 4

I. KEY HIGHLIGHTS

I. KEY HIGHLIGHTS

July 23, 2015 Page 5

Key Financial Highlights

• € 104.3 million:

• +9.9% vs. Q1-15

• -10.2% vs. Q2-14

Revenue

• € 91.9 million:

• -11.8% vs. Q1-15

• -26.0% vs. Q2-14

Orders

• € 15.5 million:

• +9.2% vs. Q1-15 (ex-restructuring benefit)

• -32.3% vs. Q2-14

Net Income

• Net cash of € 91.4 million

• -€ 41.7 million vs. Q1-15 (€ 56.9 million cash dividend payment)

Liquidity

Besi Posts Strong Q2 and H1-15 Results.

Significant Expansion of Net Cash Position vs. Q2-14

• € 199.2 million:

• +7.0% vs. 2014

Revenue

• € 196.1 million:

• -16.7% vs. 2014

Orders

• € 33.0 million, +10.4% vs. 2014

• € 29.8 million (ex-restructuring benefit) vs. € 29.9 million H1-14

Net Income

• Net cash +€ 28.9 million vs. Q2-14

Liquidity

Q2-15 H1-15

July 23, 2015 Page 6

€ 116.2

€ 104.3

19.7% 14.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

€ 0

€ 20

€ 40

€ 60

€ 80

€ 100

€ 120

€ 140

Q2 2014 Q2 2015

Net

marg

in %

€ m

illio

ns

Revenue Net Income

Gross Margin

OPEX

Headcount

Effective Tax Rate

9.4% 11.8%

1,672 1,684

€ 24.6

MM

€ 32.0

MM

+12

+2.4%

+30.1%

43.2% 47.9%

-10.2%

-4.9 points

Q2-14/Q2-15 H1-14/H1-15*

+4.7 points

€ 15.5

€ 186.2

€ 199.2

16.1% 15.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 €

50 €

100 €

150 €

200 €

250 €

2014 2015*

Net

marg

in %

€ m

illio

ns

Revenue Net Income

Gross Margin

OPEX

Headcount

Effective Tax Rate

9.9% 12.7%

1,672 1,684

€ 46.1

MM

€ 60.2

MM

42.9% 48.1%

+12

+2.8 points

+30.6%

+5.2 points

+7.0%

-1.1 points

€ 29.8 € 29.9

Solid Revenue and Profit Development In Less Favorable Industry Environment

€ 22.9

* Excluding net restructuring benefit

July 23, 2015 Page 7

II. FINANCIAL REVIEW

July 23, 2015 Page 8

Revenue/Order Trends

Quarterly Trends

YTD Trends

53.1

70.0

116.2

103.5 89.0 94.9

104.3

57.2

111.1

124.2

90.9 81.4

104.2

91.9

0

20

40

60

80

100

120

140

Q4-2013 Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015 Q2-2015

(eu

ro in

mill

ion

s)

Revenue Orders

186.2 199.2

235.3

196.1

0

50

100

150

200

250

2014 2015

(eu

ro in

mill

ion

s)

Revenue Orders

Q2-15 vs. Q1-15

• Revenue: € 104.3 million (+9.9%)

• Low end of guidance due to customer push outs

• Increased sales for auto, high end server, China

handset and plating applications

• Orders: € 91.9 million (-11.8%)

• Lower memory and smart phone applications

• Partial offset: higher auto, high end server and

solar plating applications

• -€ 8.8 million (15.1%) IDMs

• -€ 3.5 million (7.6%) subcontractors

Q2-15 vs. Q2-14

• Revenue: -€ 11.9 million (-10.2%)

• Lower die attach sales for high end smart phones

• Orders: -€ 32.3 million (-26.0%)

YTD 15 vs. YTD 14

• Revenue: +€ 13.0 million (+7.0%)

•Higher memory and high end server, auto and

plating/solar applications.

• Partial offset: lower flip chip and MMA die attach

+ ultra-thin molding for high end smart phones

• Orders: -€ 39.2 million (-16.7%)

July 23, 2015 Page 9

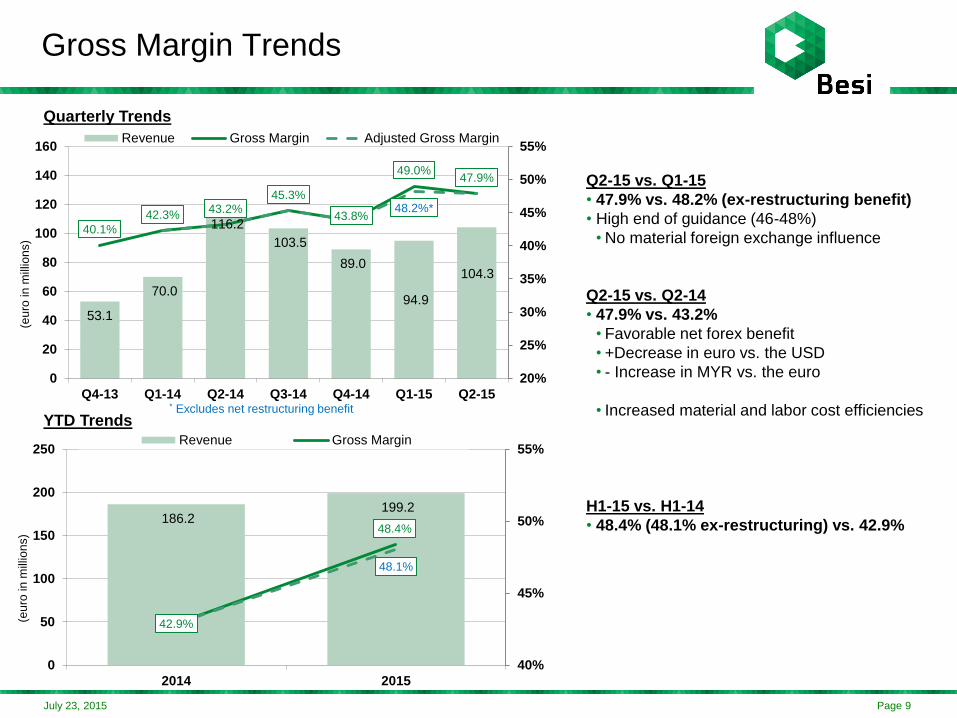

Gross Margin Trends

Quarterly Trends

186.2 199.2

42.9%

48.4%

48.1%

40%

45%

50%

55%

0

50

100

150

200

250

2014 2015

(eu

ro in

mill

ion

s)

Revenue Gross Margin

YTD Trends

53.1

70.0

116.2

103.5

89.0

94.9

104.3

40.1%

42.3% 43.2%

45.3%

43.8%

49.0% 47.9%

48.2%*

20%

25%

30%

35%

40%

45%

50%

55%

0

20

40

60

80

100

120

140

160

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15

(eu

ro in

mill

ion

s)

Revenue Gross Margin Adjusted Gross Margin

Q2-15 vs. Q1-15

• 47.9% vs. 48.2% (ex-restructuring benefit)

• High end of guidance (46-48%)

•No material foreign exchange influence

Q2-15 vs. Q2-14

• 47.9% vs. 43.2%

• Favorable net forex benefit

• +Decrease in euro vs. the USD

• - Increase in MYR vs. the euro

• Increased material and labor cost efficiencies

H1-15 vs. H1-14

• 48.4% (48.1% ex-restructuring) vs. 42.9%

* Excludes net restructuring benefit

July 23, 2015 Page 10

Operating Expense Trends

Quarterly Trends

32.4 38.8

12.7

21.4 1.0

2.9-

46.1

57.3

60.3*

-10

10

30

50

70

90

2014 2015

(eu

ro in

mill

ion

s)

Restructuring/Other R&D SG&A

YTD Trends

13.1 15.2 17.2 15.5 17.3 20.5 20.6

5.2 6.1

6.6 7.5

7.3 9.9

11.4

2.2 0.2

0.8 0.0

-3.0

-2.9

0.1

20.5 21.5 24.6

23.0 24.6 25.3

32.0 28.3*

-10

-5

0

5

10

15

20

25

30

35

40

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15

(eu

ro in

mill

ion

s)

Restructuring/Other R&D SG&A

Q2-15 vs. Q1-15

• +€ 3.7 million (+13.1%)

• Above guidance: (+5-7%)

• +€ 0.9 million TCB R&D related costs

• +€ 1.0 million warranty (forex + TCB)

• +€ 0.9 million personnel expenses

• +€ 0.5 million travel (restructuring Switzerland)

Q2-15 vs. Q2-14

• +€ 7.4 million (+30.1%)

• +€ 4.4 million R&D, principally TCB related

• +€ 1.5 million CHF increase vs. euro

• +€ 0.6 million incentive compensation

H1-15 vs. H1-14

• +€ 14.2 million (+30.8%)

• +€ 8.5 million R&D:

• € 3.9 million lower cap/higher amortization of

development costs

• +higher TCB personnel and materials

• +€ 3.4 million CHF increase vs. euro

• +€ 2.4 million incentive compensation

* Excludes net restructuring benefit

July 23, 2015 Page 11

Quarterly Base Line Operating Expense Trends

20.9 22.0 21.4 22.5 22.2 26.1

0.6 2.6

1.7 2.2 3.1

5.9

21.5

24.6 23.1

24.7 25.3

32.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15

Base Opex Other Operating Expenses

Baseline Opex 20.9 22.0 21.4 22.5 22.2 26.1

Other Operating Expenses

Capitalization of R&D (2.8) (2.4) (2.0) (2.1) (1.5) (1.4)

Amortization of R&D 1.1 1.2 1.3 1.2 1.7 2.2

Capitalization & Amortization , net (1.7) (1.2) (0.7) (0.9) 0.2 0.8

Forex CHF/EUR 0.0 0.0 0.0 0.0 1.9 1.5

Restructuring cost/(benefit) 0.2 0.8 (0.0) (0.0) (3.0) 0.1

Variable Pay 2.1 3.0 2.4 3.1 4.0 3.5

Subtotal 0.6 2.6 1.7 2.2 3.1 5.9

Total 21.5 24.6 23.0 24.6 25.3 32.0

July 23, 2015 Page 12

3.4

12.2 14.2

15.5

(2.0)

7.5 3.3

1.4

7.0

22.9 21.5

19.7

17.5 15.5

6.4%*

10.0%

19.7% 20.8%

13.7%* 15.0%* 14.8%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

(3)

0

3

6

9

12

15

18

21

24

Q4-13 (*) Q1-14 Q2-14 Q3-14 Q4-14 (*) Q1-15 (*) Q2-15

(euro

in m

illio

ns)

Net Income ex. NR Non Recurring Net Margin ex. NR

Net Income Trends

Quarterly Trends

YTD Trends

• € 15.5 million Q2-15 net income

• +€ 1.3 million vs. €14.2 million (ex-

restructuring) in Q1-15

• -€ 7.4 million vs. Q2-14

• Sequential quarterly profit growth since

Q4-14 ex non recurring items

• Less volatile trajectory than prior years

• Reflects absence of H1-14 smart phone

capacity spike

• Higher base line profits and margins than

prior years

• Tax rate up slightly in 2015 due to

absence of Q2-14 tax benefit ($700k)

• 9.9% in H1-14 (12.0% ex. deferred tax

benefit) vs. 12.4% in H1-15

(*) Excludes net restructuring (€ 3.3 million) and deferred tax benefits (€ 7.5 million) in Q1-15

and Q4-14, respectively, and € 2.0 million non recurring charge in Q4-13

29.7

3.3 29.9

33.0

16.1% 14.9%

-5%

5%

15%

25%

35%

0

5

10

15

20

25

30

35

2014 YTD 2015YTD

(euro

in m

illio

ns)

Net Income ex. NR Non Recurring Net Margin ex. NR

July 23, 2015 Page 13

Liquidity Trends

Q2-15 vs. Q1-15

• Net cash -€ 41.7 million to € 91.4 million

Q2-15 cash movements

Principal sources of cash

• € 18.4 million cash from operations

Principal uses of cash

• -€ 56.9 million dividend payments

• -€ 6.1 million debt payments

• -€ 1.3 million capex

• -€ 1.4 million capitalized R&D

Q2-15 vs. Q2-14

• Net cash +€ 28.9 million

• Increased profit and improved working capital

management

91.9

83.8

105.4

135.3

161.6

113.7

19.1 21.3 19.3 17.3

28.5 22.3

72.8

62.5

86.1

118.0

133.1

91.4

0

20

40

60

80

100

120

140

160

180

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15

(eu

ro in

mill

ion

s)

Cash Debt Net Cash

July 23, 2015 Page 14

III. STRATEGIC HIGHLIGHTS

July 23, 2015 Page 15

Assembly Equipment Market Trends

• VLSI forecasts flat growth in 2015 and 2016 after big 2014 increase as capacity digested

• Growth reaccelerates in 2017 and 2018

• Besi revenue growth exceeding assembly market in 5 of past 6 years

326.9

273.7 254.9

378.8

186.2 199.2

-16.3% -6.9%

48.6%

7.0%

-50%

0%

50%

100%

150%

-

100.0

200.0

300.0

400.0

2011 2012 2013 2014 YTD 2014 YTD 2015

(€ m

illi

on

s)

Besi Revenue Revenue YoY Growth Rate

4.4 4.0

3.1

4.0 4.0 3.9

4.6 4.9 4.8

-9.2%

-22.4%

29.1%

1.6% -2.5%

16.3%

7.7%

-2.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2011 2012 2013 2014 2015F 2016F 2017F 2018F 2019F

(US

$ b

illi

on

s)

Assembly Equipment Market Size YoY Growth Rate

Source: VLSI May 2015

July 23, 2015 Page 16

• Spending on <25 nano nodes has increased from ~15% in 2011 to an estimated 70% of

total spending in 2015

• Node shift below 25 nano = new assembly equipment capacity

New Technology Cycle Focused on < 25 Nano Nodes Drives Assembly Equipment Spending

July 23, 2015 Page 17

Besi Revenue Growth Drivers

Revenue Growth Drivers

World tooling up for new

tech cycle <20 nano

Increased smart phone functionality

New device introductions: IoT, wearables

Wire bond/flip chip

conversion

Solar cell plating

transition from copper to

silver

Increased share of

Japanese supply chain and China handsets

TCB expansion to memory and logic devices

July 23, 2015 Page 18

Key Development and Operational Objectives

Development Objectives

Advanced TCB die bonding development

Introduction of next generation packaging systems

Common parts/platform activities

Operational Objectives

Transfer of certain Swiss Die Attach software, logistics and administrative functions to Singapore

Transfer of certain die bonding production from Malaysia to China

Transfer of Plating Production from NL to Malaysia

Further reduction of European based costs

Expansion of Asian supply chain. System module outsourcing

2015 2016

July 23, 2015 Page 19

IV. OUTLOOK & SUMMARY

July 23, 2015 Page 20

Q3-15 Guidance

Revenue Gross Margin Operating Expenses

Q2 Q3 Q2 Q3 Q2 Q3

€ 104.3 47.9% € 32.0

Down

15-20%

• Revenue declines by 15-20% reflecting seasonal trends and less favorable

industry conditions

• Gross margins decline to 45-47% range

• Opex down approximately 10% vs. Q2-15

• Expect solid profit and cash flow generation in H2-15

Down ~10%

47%

-

45%

July 23, 2015 Page 21

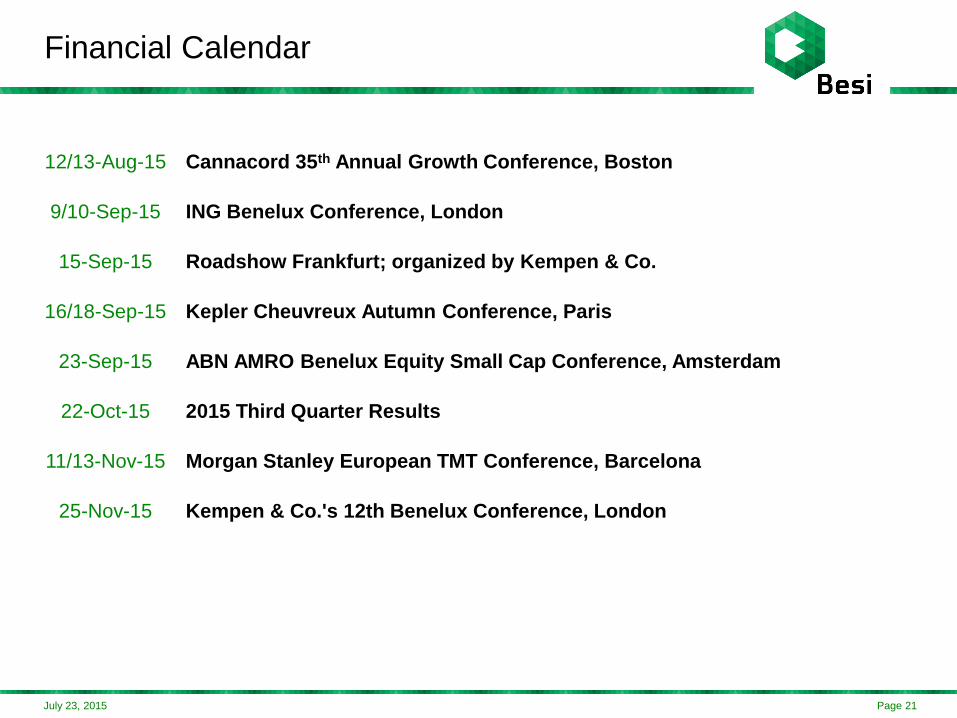

Financial Calendar

12/13-Aug-15 Cannacord 35th Annual Growth Conference, Boston

9/10-Sep-15 ING Benelux Conference, London

15-Sep-15 Roadshow Frankfurt; organized by Kempen & Co.

16/18-Sep-15 Kepler Cheuvreux Autumn Conference, Paris

23-Sep-15 ABN AMRO Benelux Equity Small Cap Conference, Amsterdam

22-Oct-15 2015 Third Quarter Results

11/13-Nov-15 Morgan Stanley European TMT Conference, Barcelona

25-Nov-15 Kempen & Co.'s 12th Benelux Conference, London