Investor Presentation - NBAD UAE · PDF fileInvestor Presentation ... 1 IMF World Economic...

44

1 March 2015 Investor Presentation Abu Dhabi at the Heart of the West-East Corridor

Transcript of Investor Presentation - NBAD UAE · PDF fileInvestor Presentation ... 1 IMF World Economic...

1

March 2015

Investor Presentation Abu Dhabi at the Heart of the West-East Corridor

2 2

Disclaimer

The information contained herein has been prepared by National Bank of Abu Dhabi P.J.S.C (“NBAD”). NBAD relies on information obtained

from sources believed to be reliable but does not guarantee its accuracy or completeness.

This presentation has been prepared for information purposes only and is not and does not form part of any offer for sale or solicitation of any

offer to subscribe for or purchase or sell any securities nor shall it or any part of it form the basis of or be relied on in connection with any

contract or commitment whatsoever.

Some of the information in this presentation may contain projections or other forward-looking statements regarding future events or the

future financial performance of NBAD. These forward-looking statements include all matters that are not historical facts. The inclusion of such

forward-looking information shall not be regarded as a representation by NBAD or any other person that the objectives or plans of NBAD will

be achieved. NBAD undertakes no obligation to publicly update or publicly revise any forward-looking statement, whether as a result of new

information, future events or otherwise.

3 3

UAE, Abu Dhabi & Banking Sector

NBAD Overview

Strategy & Updates

Financial Review 4Q / FY 2014

Appendix

Contents

4 4

UAE Economic Overview

Composition of UAE Real GDP by Sector (2013)3

1 IMF World Economic Outlook, 2013 2 Moody’s 3 National Bureau of Statistics, UAE

Public Debt in MENA Region (2013)²

UAE Public Debt vs GDP² • The United Arab Emirates comprises seven Emirates with Abu Dhabi being the largest contributor to its GDP

• Rating: Aa2 stable by Moody’s (unsolicited)

• Nominal GDP for 2013 estimated at USD 402.3bn, making it the 2nd largest economy in the GCC (after Saudi Arabia)1

• 6.06% of proven global oil reserves as of 20122

• UAE Banking sector offers the largest asset base within the GCC (NBAD is 4th largest bank by assets in the MENA region)

• UAE banking sector is dominated by domestic players domiciled within the market

Per cent (%)

24.5% 22.5% 23.6%

26.2% 26.2% 26.8%

2010 2011 2012 2013 2014F 2015F

Per cent (%)

131%

86%

44% 35%

26%

7% 6% 3%

Lebanon Jordan Bahrain Qatar UAE Oman Kuwait SaudiArabia

Per cent (%)

Oil & Gas 33%

Manufacturing 9%

Construction 9%

Real Estate 12%

Transport, storage and

communication 10%

Trade 12%

Financial Institutions

7%

Government Services

6%

Other 2%

5 5

Abu Dhabi – The Capital

Abu Dhabi Key Economic Indicators

Credit Rating Aa2 (Moody’s) / AA (S&P) / AA (Fitch)

Size Abu Dhabi accounts for 87% of UAE’s land area

Population (2012) 2.3mn1

Nominal GDP (2013) USD 259.7bn1

GDP Per Capita (2013) USD 106,0001

Oil & Gas as a % of GDP

54.9% (nominal GDP, 2013)1

Crude Oil -- Production -- Reserves

Approx 2.6mn bpd (2012)1 95 bn barrels1; Global ranking – 72

Other Principal Contributors to Nominal GDP (2013)1

Construction (9.0%), Real Estate (4.8%), FIs & Insurance (4.8%), Manufacturing (5.7%), Govt Services (4.6%), Transportation and storage (3.7%), Wholesale and retail trade (3.6%), Professional, scientific and technical (2.2%), Information and communication (2.3%), Public utilities (2.5%)

Abu Dhabi “2030 Economic Vision”

Initiative by the Government of Abu Dhabi to develop and diversify the economy beyond oil revenues

1 Statistics Centre of Abu Dhabi 2 IMF

Abu Dhabi’s Aa2 government rating reflects our expectation that resources accumulated during the recent period of high oil prices and a prudent budgeting of oil proceeds will mitigate the negative consequences of oil price volatility on the country’s fiscal and external accounts.

Abu Dhabi benefits from: (1) ample reserves derived from several consecutive years of fiscal surpluses; (2) a sound policy framework; (3) political stability and (4)a very high per capita income. After consolidated spending stabilized in 2014, the UAE’s fiscal breakeven oil price is just below $80 per barrel while its external breakeven oil price is around $64. At the same time, the government’s large net asset position provides a transition period of several years to adjust to oil price cycles.

Moody’s, January 26, 2015

Sovereign net foreign assets are the second-highest of all Fitch-rated sovereigns and rose by an estimated 27% of GDP during 2013 to 178.4% of GDP….These assets are equivalent to around five years of government spending and provide a substantial cushion….

Fitch Ratings, August 15, 2014

The exceptional strength of Abu Dhabi’s net asset positions also provides a buffer to counter the negative impact of oil price volatility on economic growth and government revenues, as well as on the external account.

Standard & Poor’s, October 3, 2014

6 6

472 511

572 632

291 318 348

387 311 323

347 380

2011 2012 2013 2014

Total Assets Deposits Loans & Advances

The UAE Banking Sector

UAE non-performing loans2 GCC banking sector assets3

UAE Banking System Key Indicators1

• As at 30 November 2014 there were a total of 49 banks (23 locally incorporated banks and 26 foreign banks)1

• 8 Islamic banks

• Strong capitalisation driven by cautious lending and healthy internal capital growth

• Most domestic banks focus on the UAE and GCC region, while the largest banks have international presence

• Regulated by the Central Bank of the UAE

USD Bn

632 568

269

189 189

64

UAE Saudi Arabia Qatar Bahrain Kuwait Oman

1.8% 4.8%

6.8% 7.2% 7.2% 6.2% 5.8% 5.0%

2.8% 0.9% 0.8% 0.3% 0.4% 0.8%

2.4% 2.2% 2.3% 2.0% 1.7%

2008 2009 2010 2011 2012 2013 2014F 2015F

Base Problem Loans Dubai World Problem LoanDubai Holding Problem Loan Dubai Holding RestructuredDubai World Restructured

1 UAE Central Bank 2 Moody’s UAE Banking System Outlook 3 Individual Central Banks

USD Bn

Kuwait, Qatar, Oman as of November 30th 2014 Saudi Arabia & UAE as of December 31st 2014

7 7

UAE, Abu Dhabi & Banking Sector

NBAD Overview

Strategy & Updates

Financial Review 4Q / FY 2014

Appendix

Contents

8 8

NBAD at a Glance (1/2)

Banker to the Abu Dhabi Government

70% owned by the Government of Abu Dhabi through ADIC (Abu Dhabi Investment Council)

Strongest ratings of any bank in the Middle East & Emerging Markets at Aa3/AA-/AA- - ‘Safest Bank in the Middle East & Emerging Markets’*

Largest bank by assets in the UAE (AED 376 billion as of 31st December 2014)

Well diversified Financial Group – across businesses and geography - Largest international presence among the UAE banks

Consistent profitability and value creation to shareholders

Well positioned for growth from global economic recovery

Clear and focused strategy for growth

* By Global Finance – Safest Bank in Middle East & Emerging Markets; Among the World’s 50 Safest Banks since 2009

9 9

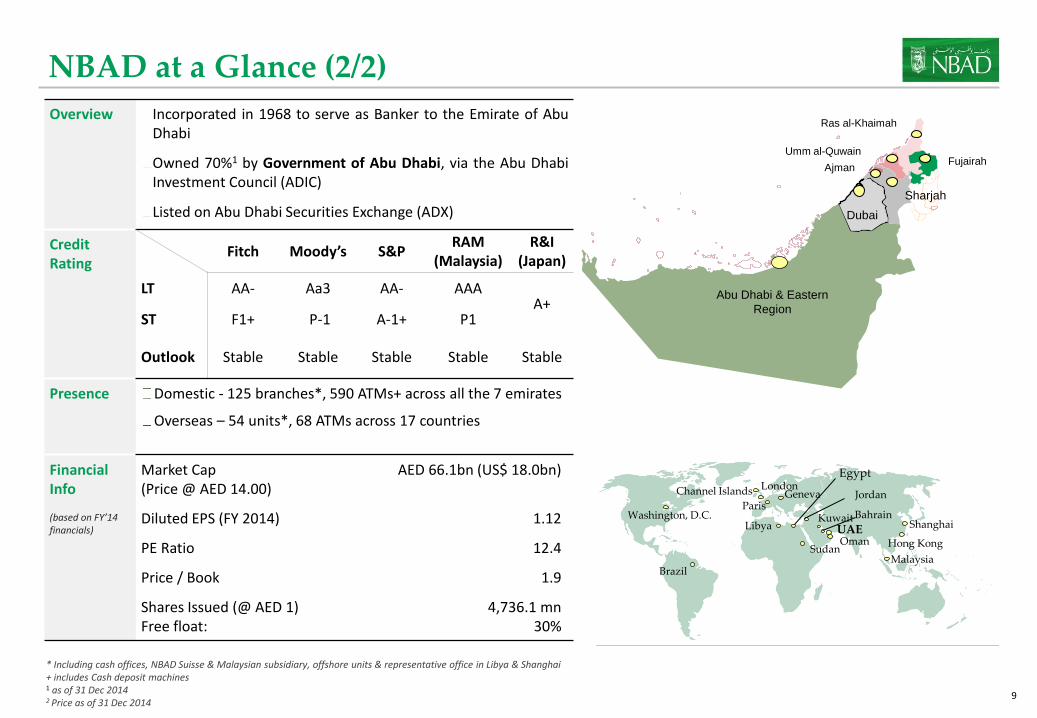

NBAD at a Glance (2/2)

Overview Incorporated in 1968 to serve as Banker to the Emirate of Abu Dhabi

Owned 70%1 by Government of Abu Dhabi, via the Abu Dhabi Investment Council (ADIC)

Listed on Abu Dhabi Securities Exchange (ADX)

Credit Rating

Fitch Moody’s S&P RAM

(Malaysia) R&I

(Japan)

LT AA- Aa3 AA- AAA A+

ST F1+ P-1 A-1+ P1

Outlook Stable Stable Stable Stable Stable

Presence Domestic - 125 branches*, 590 ATMs+ across all the 7 emirates

Overseas – 54 units*, 68 ATMs across 17 countries

Financial Info

(based on FY’14 financials)

Market Cap (Price @ AED 14.00)

AED 66.1bn (US$ 18.0bn)

Diluted EPS (FY 2014) 1.12

PE Ratio 12.4

Price / Book 1.9

Shares Issued (@ AED 1) Free float:

4,736.1 mn 30%

Dubai

Abu Dhabi & Eastern

Region

Ras al-Khaimah

Fujairah Umm al-Quwain

Ajman

Sharjah

* Including cash offices, NBAD Suisse & Malaysian subsidiary, offshore units & representative office in Libya & Shanghai + includes Cash deposit machines 1 as of 31 Dec 2014 2 Price as of 31 Dec 2014

Washington, D.C.

London

Paris Geneva

Egypt

Sudan

Kuwait Bahrain

Oman

Libya

Hong Kong

Jordan

UAE

Channel Islands

Malaysia Brazil

Shanghai

10 10

NBAD vs Global banks

NBAD

HSBC

StanChart

Barclays RBS

Lloyds

BNP Paribas Deutsche Bank

SocGen

Credit Suisse

UBS

Credit Agricole

ING Groep

Commerzbank

UniCredit

JP Morgan Chase

Goldman Sachs

Morgan Stanley Citigroup

BofA

30

40

50

60

70

80

90

100

110

120

CD

S (

bp

s)

Aa3S Aa3- A1+ A1S A1- A2+ A2S A2- A3+ A3S A3- Baa1+ Baa1S Baa1- Baa2+ Baa2S Baa2- Aa3+

Notes: X-axis represents the rating assigned by Moody’s. The ratings have been arranged from higher to lower based on the outlook assigned by Moody’s at each rating level. For example ‘Aa3+’ is the highest rating level for ‘Aa3’ rating category, where (+) refers to positive outlook. ‘Aa3+’ is followed by ‘Aa3S ‘ and ‘Aa3-’, where (S) refers to ‘stable outlook ‘ and (-) refers to ‘negative outlook’; CDS levels are for 26th January 2015; Source: Bloomberg

NBAD has the strongest rating from Moody’s (Aa3 with a Stable outlook), within the selected peer group below; Indeed NBAD is the only bank within the selected peer group here, to be rated in the double-A category by all three major agencies with Stable outlook

11 11

UAE, Abu Dhabi & Banking Sector

NBAD Overview

Strategy & Updates

Financial Review 4Q / FY 2014

Appendix

Contents

12 12

Our mission to be core to our chosen customers

Vision To be recognised as the World’s Best Arab Bank

Mission Be core to our chosen customers, helping them grow by providing exceptional

products and services across our West-East Corridor and provide an environment to attract and develop exceptional and diverse talent

Our Values Value our

people and foster great team work

Put our customers at the forefront and “do the

right things the right way”

Empower our people and

hold each other accountable for

performance and behaviour

Customer Value Proposition

Safety Relationship Connected Service Insight

Respect our heritage and be

loyal to our stakeholders

13 13

4 Geographical Pillars of our Strategy

Vision: To be recognised as the World’s Best Arab Bank to be achieved around four pillars…

Home Market

Build the largest, safest and best performing bank first in UAE, and over time

in the GCC

1

Wholesale / Wealth Network Markets

Deepen our network across the West-East

corridor & integrate our existing European & North American platforms into

this network

2

New Franchise Markets

Build 5 international bank franchises in the largest

and fastest growing economies in the West-

East corridor

3

Building the Spine

Supported by a world class spine (Operations & Technology, Risk, Finance, Legal, Compliance) combining best-in-class customer service with leading cost efficiency

4

14 14 SOURCE: United Nations, World Urbanization Prospects 2007; McKinsey Global Institute China All City Model; McKinsey Global Institute analysis

1 Cities with 10 million or more inhabitants

Megacities1 2007

Additional megacities by 2025

West-East corridor

Los Angeles

Mexico city

Bogotá

Lima Rio de Janeiro

Sao Paulo

Buenos Aires

London

Paris

Moscow

Cairo

Lagos

Kinshasa

Istanbul

Tehran Lahore

Karachi Ahmedabad

Mumbai

Bangalore Chennai

Hyderabad

Chengdu

Dhaka

Chongqing

Xi’an Beijing Seoul

Tianjin

Shanghai Hangzhou

Guangzhou Shenzhen/Hong Kong

Manila

Jakarta

Osaka-kobe New York

Wukan

Our primary drivers are trade and investment flows across the West/East corridor: We want to bank the customers from within the corridor We want to bank customers located outside of the corridor who trade and invest inside the corridor We want to support our chosen UAE customers in London, Paris, Switzerland and Washington

Banking the West-East corridor

Kolkata

Delhi

Tokyo

15 15

Trade and FDI flow across the West-East corridor

SOURCE: EIU estimates

Figures in USD Billion Trade = Sum of imports and exports FDI = Sum of M&A and Greenfield investments

Trade flows

1.1 Intra Middle East

Trade

2011

112

1.2 Middle East and Asia

2011

1.3 Middle East and Africa

2011

2.1 Asia and Africa 3.1 Intra Asia

Trade 3302 6607 8%

3.2 Intra Africa

50 Trade 103 8%

FDI flow 17

2020

270

2020

2020

38

CAGR 11-20

10%

CAGR 11-20

CAGR 11-20

9% FDI flow 213 614 12%

FDI flow 2 15 25%

2011 2020 CAGR 11-20 2011 2020

CAGR 11-20

2011 2020 CAGR 11-20

Trade

FDI flow

334

35

888

69

11%

8%

Trade

FDI flow

Trade

FDI flow

1008

26

2743

82

12%

14%

10%

19%

163

29

67

6

16 16

Key sectors

Financial Institutions

Aviation, rail and transport services

Real Estate and family conglomerates

Traders and retailers

Energy and Resources

Why is it an opportunity? Illustrations

Significant and fastest growing segment globally

40% contributor to the global Wholesale bank and the biggest volume segment in flow products

Controls 70% of the volumes in certain products

Strategic sector in the UAE & aligned with Abu Dhabi 2030

Attractive sector for corporate credit with low counterparty risk

Substantial growth & potential of supply chain business

Strategic sector the UAE & aligned with Abu Dhabi vision 2030

National champions with significant growth aspirations

Big 6 airlines within the new West-East corridor

Strategic sector the UAE (20% of UAE GDP) & aligned with Abu Dhabi vision 2030

Highly attractive sector for Arab investors

Attractive for GCC/Asian and other investors

Strategic and high growth sectors in the region

UAE is the 18th biggest trading country in world ahead of countries like India, Brazil and Australia

Retailing is USD ~$48Bn market in GCC expected to grow at ~8% annually from 2013/17

Key industry sectors aligned to our network markets strategy

17 17

We will increasingly utilise an ‘originate to distribute’ model

Originate from Customers Distribute to Customers

Government of Abu Dhabi

Financial institutions

Energy and resources

Aviation, rail and transport services

Real estate and family conglomerates

Traders and retailers

Financial institutions

Hedge funds

Pension funds and Insurance

Sovereigns

Private banks

HNW and affluent

On and off balance sheet

Primary distribution

Secondary distribution

Reverse inquiries

Cross-sell Cross-sell

Cash and Trade

FX and derivatives

Bonds syndications

Commodities

Specialised lending

Corporate finance

Flo

w

pro

du

cts

Clearing/settlements

Cash and trade

FX and derivatives

Bonds

Loans

Flow

p

rod

ucts

Single distribution hub

18 18

Wholesale banking model aligning to West-East corridor

1 Relationship, sales and product service

Abu Dhabi The Gulf/Middle East

Mumbai Indian sub-continent

Lagos South and West Africa

Singapore South-East Asia, Australia, Papua New Guinea

Hong Kong Greater China, Korea and Japan

London Scandinavia, Switzerland, and European Union

Washington North and South America

Global financial markets and booking centers Abu Dhabi Singapore or Hong Kong London

Key industry sectors

Financial institutions (Singapore)

Energy and resources (Abu Dhabi)

Aviation, rail and transport (Abu Dhabi)

Real estate and family conglomerates (Abu Dhabi)

Traders and retailers (Abu Dhabi)

Cash and trade Abu Dhabi

DCM Abu Dhabi Hong Kong

Advisory and specialized lending Abu Dhabi

Banking hubs1 Customer geographies Centers of excellence Operating centers

Abu Dhabi

(BCM in Al Ain)

One more location at a future point (e.g., India or Philippines)

Paris France and North Africa

19 19

NBAD Becoming the World’s Best Arab Bank

Improving Our Reputation for Safety Among World’s 50 Safest Banks

Enhancing our Retail Customer Experience Introduced New Branch Design

Expanding Global Brand & Reputation Exclusive banking partner of Real

Madrid in UAE

Intensive customer service initiatives underway “Bring Your Heart to Work” Day

Enhancing Brand/Investing in Abu Dhabi Renewed Sponsorship as “Official Bank of

FORMULA 1 ABU DHABI GRAND PRIX”

Building a Talented Bench of Professional Bankers Launch of Professional Bankers Programme

Real Madrid Partnership Enhanced Branch Design World’s 50 Safest Banks

FORMULA 1 Sponsor Bring Your Heart to Work Professional Bankers Programme

20 20

Geographical Pillars – Strategy Delivered in 2015

Geographical Pillars

Pillar 1 – Home Market

Retail

Branch Refurbishment (ongoing)

eChannels/Online/ Mobile Banking (ongoing)

Penetrate existing client base (refer cross sell target)

Major scaling up of direct sales leading to substantial volume increases

Enhance the customer experience

Commercial

Major customer acquisition/ Formation of 3 customer segments

Penetrate existing base

Launched proposition for: • Short-term working capital

related facilities

• Program lending

• Trade & FX

Major rebuild of team/ significant hiring

Focus on improving limits utilisation and cross sell

Pillar 2: Network

Wholesale

Key Hires complete: • All 5 Industry Group Heads

hired

• New Relationship Bankers’ teams

• Major upgrading of Product Team Heads

London – Canary Wharf established

Mumbai – License successful; planned mid-2015

Hong Kong – expanding the dealing room

Deepen relationship with the core 600+ clients

Build-out product capabilities (structured, corp finance)

Wealth

Customer acquisition

Regional expansion • Egypt build out

• Regional (MENA) & Asian distribution of AMG funds

• Establish regional network of sub-brokers & custodians

Define a strategy to become the leading asset manager in the Islamic world

Substantially grow our Swiss Private Banking business

21 21

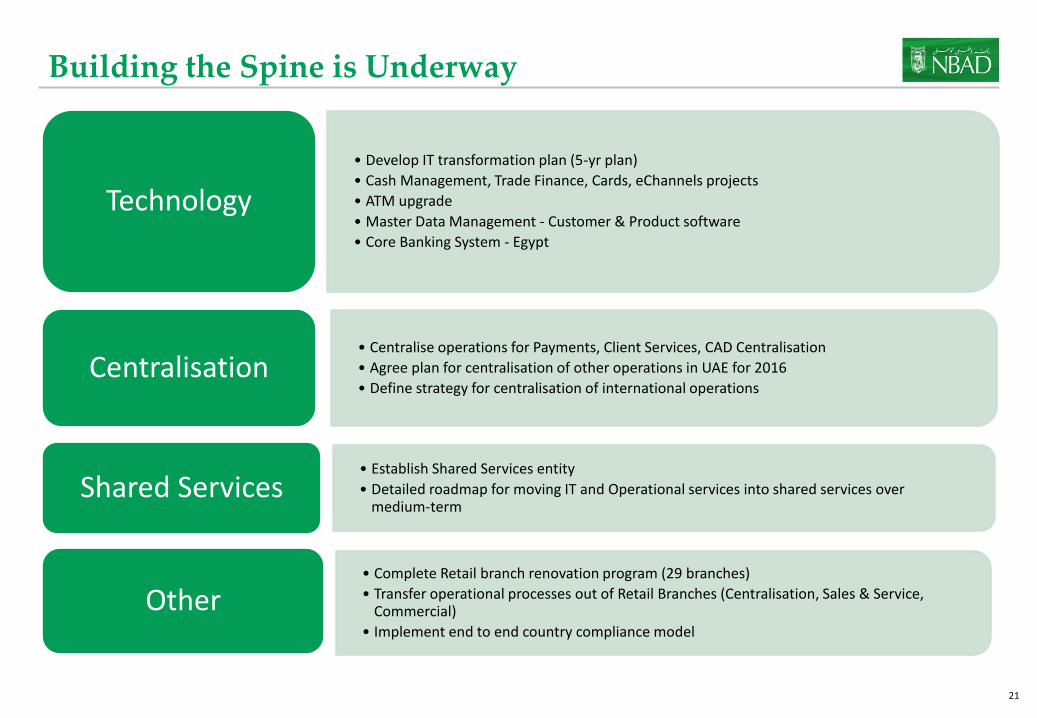

Building the Spine is Underway

• Develop IT transformation plan (5-yr plan)

• Cash Management, Trade Finance, Cards, eChannels projects

• ATM upgrade

• Master Data Management - Customer & Product software

• Core Banking System - Egypt

Technology

• Centralise operations for Payments, Client Services, CAD Centralisation

• Agree plan for centralisation of other operations in UAE for 2016

• Define strategy for centralisation of international operations Centralisation

• Establish Shared Services entity

• Detailed roadmap for moving IT and Operational services into shared services over medium-term

Shared Services

• Complete Retail branch renovation program (29 branches)

• Transfer operational processes out of Retail Branches (Centralisation, Sales & Service, Commercial)

• Implement end to end country compliance model

Other

22 22

Connecting Global Issuers to The Middle East Facilitating Landmark Transactions in 2014

2

Overall Emerging Market Deal of the Year

Emerging Asia Deal of the Year

Islamic Deal of the Year 2014

Emerging Market Financial Institution Deal of the Year

Deal of the Year Sovereign Deal of the Year

Sukuk Deal of the Year UK Deal of the Year

Middle East & Turkey Deal of the Year

Best Islamic Financing 2014

Perpetual Deal of the Year Regulatory Capital Deal of the Year

UAE Deal of the Year

Syndicated Deal of the Year

Sovereign/Supranational/Agency Sterling Deal of the Year

Social Impact Deal of the Year

Best Sovereign Bond 2014

Joint Bookrunner

Joint Bookrunner Joint Bookrunner Joint Bookrunner

Joint Bookrunner Joint Bookrunner Joint Bookrunner

Joint Bookrunner

Joint Bookrunner

Joint Bookrunner

Joint Bookrunner

Joint Bookrunner

23 23

Our Proposition to Clients is Improving

2

Category Current

Rank Prior Rank

GCC Bonds #3 #8

MENA Syndicated Loans

#3 #11

International Sukuk #3 #6

Bloomberg Rankings

*Rankings based on survey for corporates and financial institutions in the GCC

Client Metric NBAD’s

Rank

Client Coverage/Penetration #1

Greenwich Quality Index (S/T & R) #1

GQI Sales & RM #1

Sales Rep Ranking & Activity #1 / #2

Greenwich Survey

“Best Islamic Fund” – Global Islamic Finance Awards

“UAE Best Fund Manager” – Wealth Briefing GCC Region Awards

“Best GCC Equity Fund” – Banker Middle East “Best Brokerage House in UAE, 2014” –

International Finance Magazine

“Private Bank of the Year UAE” – The Banker & Professional WM Magazine

Global Wealth Awards

24 24

UAE, Abu Dhabi & Banking Sector

NBAD Overview

Strategy & Updates

Financial Review 4Q / FY 2014

Appendix

Contents

25 25

2014 – Key Highlights

+11%

REVENUES

9,398 10,415

FY'13 FY'14

+18% Up 835

AED mn

NET PROFITS

4,744

5,579

FY'13 FY'14

Up 1,016 AED mn

Among the Safest Banks in the World* Within the Top #50 since 2009

* Global Finance 2014

#25 RoE 15.4%

RoSF 16.8%

Tier-I 15.0%

CAR 16.4%

26 26

Business Drivers Grow in Line with Strategy

Assets were up year-over-year, driven by increases in Loans and Deposits; Trade & Market Contingencies grew significantly year-over-year as we continued to execute against our strategy.

Balance sheet indicators FY 2013 FY 2014 Variance

AED Bn AED Bn %

Assets 325 376

Equity 35 38

Customer Loans 184 194

Customer Deposits 211 243

CASA 58 68

Trade Contingencies 82 121

Market Contingencies 931 1,102

15.7%

9.5%

5.7%

15.2%

17.6%

46.9%

18.4%

27 27

Ratio FY 2014 FY 2013

Efficiency Diluted Earnings per Share (EPS in AED; restated for prior period) 1.12 0.95

Return on average Equity (annualised) 15.4% 14.4%

Return on average Sharehodlers' Funds (annualised; net of Tier-I capital notes & its interest thereof) 16.8% 15.6%

Return on average RWAs (annualised) 2.45% 2.48%

Net Interest Margin (based on NII & income from Islamic financing and total average assets for the period) 2.00% 2.08%

Cost-Income ratio 35.5% 34.4%

JAWS (revenue growth less expense growth) -3.6% -4.5%

Liquidity Percentage lent (Loans / Assets) 52% 57%

Loans to Customer Deposits ratio 80% 87%

Solvency* Capital adequacy 16.4% 18.2%

Tier-I ratio 15.0% 16.5%

Leverage ratio (Assets/ Equity) 9.9x 9.4x

Asset Quality Non-performing loans ratio [NPLs / Gross Loans (net of Interest in suspense)] 3.07% 3.16%

Total Provisions / NPLs 108% 105%

Specific Provisions coverage (Specific provisions / NPLs) 50.7% 55.7%

Collective Provisions coverage (Collective provisions / Performing Credit RWAs) 1.72% 1.66%

Key Ratios

* Basel-II framework as adopted by the UAE Central Bank

28 28

1,852 2,311

701

960 335

126 2,888 3,397

FY'13 FY'14

Fees & comissions FX & Investment income Other income

Revenues

2,331 2,570

2,757

4Q'13 3Q'14 4Q'14

AED Mn

9,398

10,415

FY'13 FY'14

QoQ +7%; YoY +18% YoY +11%

2.08%

1.84%

1.98%

1.89%

2.00%

4Q'13 1Q'14 2Q'14 3Q'14 4Q'14

Net Interest Margin*

* NIM% (Ytd) – annualised; based on total average assets for the period

512 563 619

135 196

231 22 14

12 669 774

862

4Q'13 3Q'14 4Q'14

Non-Interest Income

Revenues trend

AED Mn

• 4Q momentum driven by growth in non-interest income and NII: +7% q-o-q , +18% y-o-y; FY’14 up 11%

• NII up 6% sequentially as reflected in improved NIMs; expect continued pressure on NIMs going forward

• Continuing focus on non-interest income; growth of 29% y-o-y in 4Q’14 and 18% in FY’14

• Trade finance and corporate & retail lending were the main drivers of growth in fees, supported by strong growth in brokerage, asset management and IPO related fees on favourable market activity in 2014

Per cent (%)

29 29

Revenues by Business Segment

• Global Wholesale continued momentum with 6% sequential growth and 18% y-o-y growth in 4Q; Full-year growth was 9%

• Global Retail & Commercial grew 10% sequentially and 11% year-over-year for 4Q; Growth was 8% for FY2014

• In Global Wealth, 4Q growth was up 3% sequentially (impacted by market volatility and hiring talent) and up 37% y-o-y; FY’14 growth was 61%

Global Wholesale

AED Bn

Global Wealth

Per cent (%)

Global Retail & Commercial

Per cent (%)

4,959

4,546

YoY +9%QoQ +6%; YoY +18%

FY'13 FY'14

1,086 1,209

1,281

4Q'13 3Q'14 4Q'14

3,344

3,095

QoQ +10%; YoY +11% YoY +8%

FY'13 FY'14

810 813 898

4Q'13 3Q'14 4Q'14

1,063

659

QoQ +3%; YoY +37% YoY +61%

FY'13 FY'14

204

272 280

4Q'13 3Q'14 4Q'14

30 30

2,188 2,533

836 940 206 223 3,230

3,696

FY'13 FY'14

Staff costs Gen & Admin expenses Depreciation

Expenses

919 930 1,110

4Q'13 3Q'14 4Q'14

AED Mn

3,230 3,696

FY'13 FY'14

QoQ +19%; YoY +21% YoY +14%

595 643 721

271 231 331 54 56

58 919 930

1,110

4Q'13 3Q'14 4Q'14

Expenses breakdown

Expenses trend

AED Mn • Planned investments led to 4Q expenses up 19% sequentially

and up 21% year-over-year; for FY 2014, expenses were up 14%

• Cost to income ratio up slightly to 35.5% as we continue to invest in the business

• Staff costs increased as we hired key roles across the board, more than doubled direct sales force in Retail & Commercial, hired experienced bankers in Global Wholesale and Global Wealth

Cost-Income ratio

34.5%

31.6%

32.7%

33.9%

35.5%

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

Per cent (%)

31 31

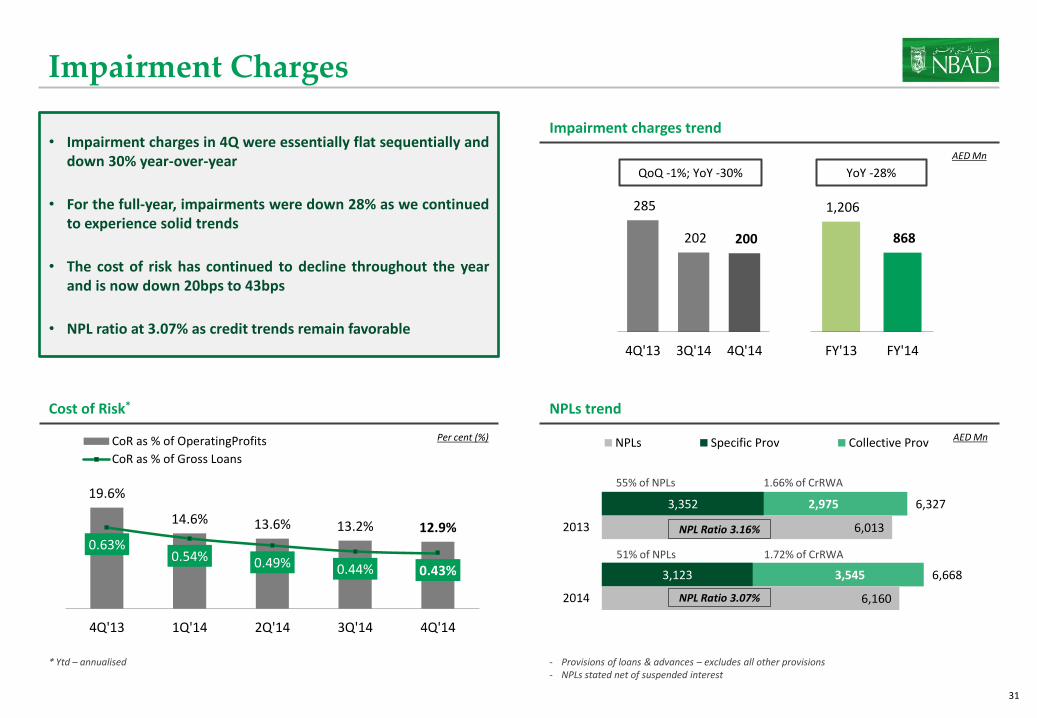

Impairment Charges

285

202 200

4Q'13 3Q'14 4Q'14

AED Mn

1,206

868

FY'13 FY'14

QoQ -1%; YoY -30% YoY -28%

NPLs trend

Impairment charges trend

AED Mn • Impairment charges in 4Q were essentially flat sequentially and

down 30% year-over-year

• For the full-year, impairments were down 28% as we continued to experience solid trends

• The cost of risk has continued to decline throughout the year and is now down 20bps to 43bps

• NPL ratio at 3.07% as credit trends remain favorable

Cost of Risk*

* Ytd – annualised

19.6%

14.6% 13.6% 13.2% 12.9% 0.63%

0.54% 0.49% 0.44% 0.43%

4Q'13 1Q'14 2Q'14 3Q'14 4Q'14

CoR as % of OperatingProfits

CoR as % of Gross Loans

Per cent (%)

3,545

2,975

3,123

3,352

6,160

6,013

6,668

6,327

2014

2013

NPLs Specific Prov Collective Prov

NPL Ratio 3.07%

NPL Ratio 3.16%

55% of NPLs

51% of NPLs

1.66% of CrRWA

1.72% of CrRWA

- Provisions of loans & advances – excludes all other provisions - NPLs stated net of suspended interest

32 32

Net Profits

1,075

1,370 1,372

4Q'13 3Q'14 4Q'14

4,744 5,579

FY'13 FY'14

QoQ flat; YoY +28% YoY +18%

Return on Equity & Return on Shareholders’ Funds

Net profits trend

AED Mn • Net profits in 4Q were flat sequentially and up 28% year-over-

year; for the full-year, profits were up 18%

• Profit growth was driven by increases in non-interest income, particularly fee income, as well as NII

• RoE remains above 15% and Return on Shareholders’ Funds was 16.8%

15.6%

17.7% 17.5% 17.0% 16.8%

14.4%

16.2% 16.0% 15.6% 15.4%

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

RoSF RoE

* Ytd and Annualised; RoSF excludes AED 4bn Tier-I capital and its annual coupon thereof

Per cent (%)

Diluted Earnings per Share (EPS)

1.12

AED

2013 2014

0.95

33 33

Net Profits by Business Segment

• Global Wholesale grew net profits up 10% sequentially and 39% year-over-year; FY 2014 growth was 18%

• Global Retail & Commercial grew 14% sequentially, but was down 15% year-over-year for 4Q; Growth was 11% for FY2014

• In Global Wealth, 4Q growth was down 7% sequentially (impacted by market volatility and hiring talent) and up 34% year-over-year; For FY 2014, profits were up 89%

Global Wholesale

AED Bn

Global Wealth

Per cent (%)

Global Retail & Commercial

Per cent (%)

3,325

2,828

QoQ +10%; YoY +39% YoY +18%

FY'13 FY'14

630

795 878

4Q'13 3Q'14 4Q'14

1,220

1,096

QoQ +14%; YoY -15% YoY +11%

FY'13 FY'14

314

234 267

4Q'13 3Q'14 4Q'14

626

332

QoQ -7%; YoY +34% YoY +89%

FY'13 FY'14

114

164 152

4Q'13 3Q'14 4Q'14

34 34

Assets & Liquidity

Loans 52%

Investments 22%

Due from Banks & Reverse

repos 7%

Cash & balances with CentralBanks

15%

Fixed assets & Other assets

4%

87%

76% 77% 75%

80%

4Q'13 1Q'14 2Q'14 3Q'14 4Q'14

• Assets ended the year at AED 376bn, declining 5% from peak 3rd quarter levels and up 16% year-over-year

• Growth came from Loans (and Deposits) for the full-year while the sequential decline was due mainly to less government related deposits

• Loans to deposits were 80%, up sequentially and down year-over-year, driven by loan growth overall and swings in deposits

Assets trend

Loans to Deposits ratio Asset mix

FY’14 AED 376bn

325 361 348 398 376

Dec'13 Mar'14 Jun'14 Sep'14 Dec'14

QoQ -5%; YoY +16% AED Bn

Per cent (%)

35 35

184 178 182 198 194

4Q'13 1Q'14 2Q'14 3Q'14 4Q'14

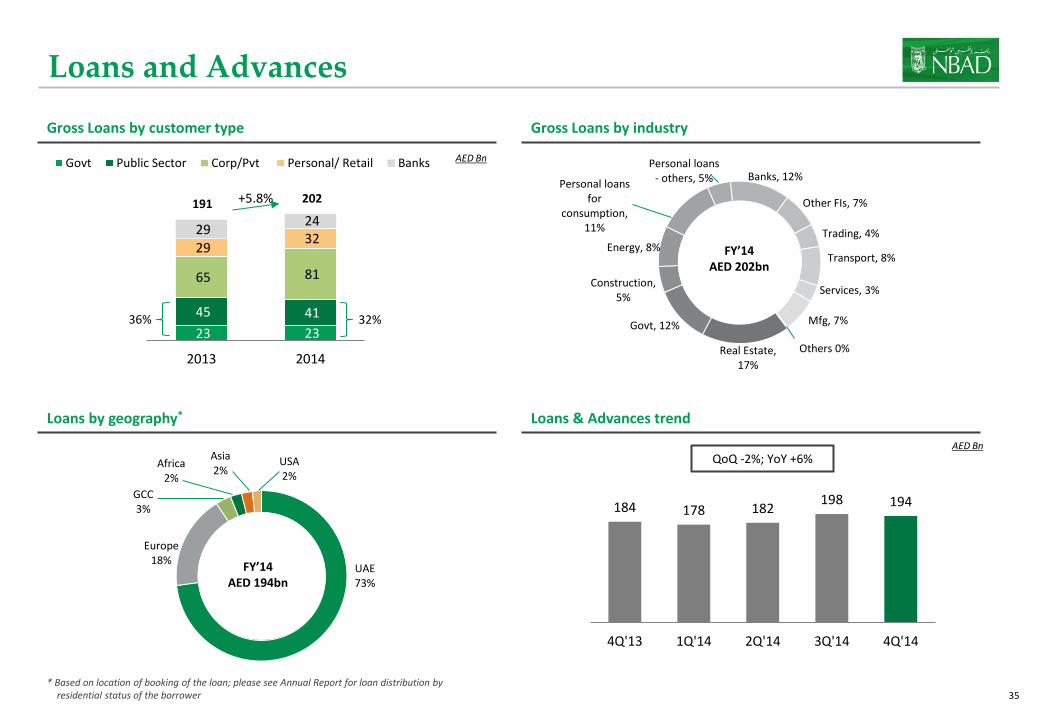

Loans and Advances

23 23

41 45

81 65

32 29

24 29

20142013

Govt Public Sector Corp/Pvt Personal/ Retail Banks

+5.8%

36% 32%

Loans & Advances trend

QoQ -2%; YoY +6% AED Bn

Gross Loans by customer type

AED Bn

191 202

Gross Loans by industry

Real Estate, 17%

Govt, 12%

Construction, 5%

Energy, 8%

Personal loans for

consumption, 11%

Personal loans - others, 5% Banks, 12%

Other FIs, 7%

Trading, 4%

Transport, 8%

Services, 3%

Mfg, 7%

Others 0%

FY’14 AED 202bn

Loans by geography*

UAE 73%

Europe 18%

GCC 3%

Africa 2%

Asia 2%

USA 2%

FY’14 AED 194bn

* Based on location of booking of the loan; please see Annual Report for loan distribution by residential status of the borrower

36 36

Investments

Investments by ratings

Investments Investments by issuer

Investments by region

HFT - Debt 16.7% HFT - Equity &

Funds 1.9%

Held to Maturity (Debt) 6.7%

AFS - Equity & Funds 0.7%

AFS - Debt 74.0%

FY’14 AED 83bn Sovereign

33.3%

GREs 22.3%

Sovereign Guaranteed

2.9%

Covered Bonds 6.7%

Banks 25.2%

Corporate/ Pvt Sector 7.0%

Supranational 2.5%

FY’14 AED 83bn

Europe 22.2%

GCC 12.6%

MENA (ex-GCC&UAE)

5.6% USA

18.7%

Australia & Others 14.7%

UAE 26.1%

AAA 20.4%

AA 34.7%

A 28.3%

BBB 4.9%

BB & below 5.8%

Unrated - Debt 3.2%

Equity & Funds 2.6%

FY’14 AED 83bn FY’14

AED 83bn

* Based on location of the issuer of the security or parent in case of SPVs

37 37

Funding Profile

* represents the nominal AED equivalent amount outstanding

Medium-term notes maturity profile* Subordinated debt maturity profile*

Due to banks 10.8% Repurchase

Agreements 4.1%

Euro Commercial Paper 1.6%

Customers' deposits

71.9%

Medium-term borrowings

4.4%

Subordinated convertible

notes 0.4%

Other liabilities 6.6%

3.3 3.2 2.7

4.1

0.5

1.3

2015 2016 2017 2018 2019 2020 >2020

AED Bn

1.0

0.5

2016 2027

AED Bn

• Stable funding mix over the years; emphasis on increasing contribution of medium-term funding

• Opportunistic in tapping the capital markets when pricing and terms favourable

• Benchmark trade issued in February 2015, USD 750mn @2.25% for 5 years under the existing EMTN programme

Funding mix

FY’14 AED 338bn

FY’14 - AED 15.2bn FY’14 - AED 1.5bn

38 38

Customer Deposits

211 235 237

265 243

63% 67% 66% 69% 66%

28% 27% 27% 26%

28%

9% 6% 6% 5% 6%

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

CDs & Margin A/c's CASA Notice & Time

211 235 237

265 243

4Q'13 1Q'14 2Q'14 3Q'14 4Q'14

• Customer deposits were down sequentially as some government related balances declined; FY growth was robust at 15%

• CASA* represented 28% of customer deposits at year-end and continues to be an area of focus at NBAD

• The percentage of deposits which were government related increased to 44% at YE 2014 from 40% at YE 2013

Customer Deposits trend

QoQ -8%; YoY +15% AED Bn

Customer Deposits trend Customer Deposits by Account

70 46

39 40

72 66

63 60

20142013

Govt Public Sector Corp/Pvt Retail

40% 44%

AED Bn

211 243

AED Bn

* Current accounts savings accounts

39 39

33.8 33.4 35.0

36.3 37.6

37.3 37.1 38.6

40.0 41.0

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

Tier-I Capital Resources

18.2% 16.1% 16.2% 16.3% 16.4%

16.5% 14.5% 14.7%

14.8% 15.0%

8%

12%

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

Total CAR Tier I%

Capital Resources (Basel-II*)

UAE CB CAR requirement

Minimum Tier-I requirement

• Capital Resources (Basel-II) of AED 41.0bn up 3.7% q-o-q and 11.2% y-o-y on higher earnings

• Tier-I capital of AED 37.6bn, up 2.6% q-o-q and 9.9% y-o-y on higher earnings as well

• Capital Adequacy ratio (Basel-II) at 31 Dec 2014 at 16.4% and 15.0% on Tier-I well above the UAE Central Bank’s minimum requirements of 12% and 8%, respectively and in line with our stated medium-term targets

Capital resources

AED Bn

* Basel-II framework as adopted by UAE Central Bank

Capital adequacy ratio

Per cent (%)

Risk Weighted Assets

AED Bn

182 210

13

24 11

17 205

250

2013 2014

Operational Market Credit

40 40

UAE, Abu Dhabi & Banking Sector

NBAD Overview

Strategy & Updates

Financial Review 4Q / FY 2014

Appendix

Contents

41 41

Results at a Glance

4Q'14 3Q'14 QoQ

% growth4Q'13

YoY %

growthFY'14

YoY %

growth

Income statement (AED mn)

Net Interest Income (incl income from Islamic financing)

1,895 1,796 5.5% 1,662 14.0% 7,018 7.8%

Non Interest Income 862 774 11.4% 669 28.8% 3,397 17.6%

Revenue 2,757 2,570 7.3% 2,331 18.3% 10,415 10.8%

Expenses (1,110) (930) 19.4% (919) 20.8% (3,696) 14.4%

Operating Profits 1,646 1,640 0.4% 1,412 16.6% 6,719 8.9%

Impairment Charges, net (200) (202) -1.0% (285) -29.6% (868) -28.0%

Prov for Taxes (74) (68) 9.3% (52) 43.0% (272) 24.5%

NET PROFIT 1,372 1,370 0.2% 1,075 27.6% 5,579 17.6%

Balance Sheet (AED bn)

Assets 376 398 -5.5% 325 15.7% 376 15.7%

Loans & Advances 194 198 -1.9% 184 5.7% 194 5.7%

Deposits & Others 243 265 -8.1% 211 15.2% 243 15.2%

Ratios %

RoE % 14.6% 15.0% -0.4% 12.7% 1.9% 15.4% -0.2%

RoSF % 15.9% 16.4% -0.4% 14.1% 1.8% 16.8% 14.7%

NIM % 1.96% 1.92% 3bps 1.98% -3bps 2.00% -8bps

Cost / Income % 40.3% 36.2% 4.1% 39.4% 0.9% 35.5% 1.1%

JAWS % -12.1% -2.5% -3.6%

42 42

Balance Sheet

Balance Sheet (AED Bn) Dec'14 Sep'14 qoq %

growthDec'13

yoy %

growth

Assets

Cash & Balances with Central Banks 55.5 64.8 -14.5% 35.1 58.2%

DFB & Reverse Repos 27.0 46.1 -41.5% 39.0 -30.9%

Investments 82.9 73.8 12.3% 53.5 55.0%

Loans & Advances 194.3 198.0 -1.9% 183.8 5.7%

Other Assets 16.5 15.3 7.7% 13.7 20.5%

Total Assets 376.1 398.1 -5.5% 325.1 15.7%

Liabilities & Equity

DTB/Repos/ECPs 56.0 47.8 17.1% 43.9 27.8%

Deposits & Others 243.2 264.7 -8.1% 211.1 15.2%

CASA 68.3 68.8 -0.7% 58.1 17.6%

Others 174.9 195.9 -10.7% 153.0 14.3%

Term Borrowings/Subdebt 16.5 16.7 -1.4% 20.2 -18.2%

Short term (<1 yr) 3.3 3.4 -4.9% 3.5 -6.5%

Long term 13.2 13.3 -0.5% 16.7 -20.7%

Other Liabilities 22.4 31.5 -29.0% 15.2 47.1%

Capital & Reserves 38.0 37.3 1.9% 34.7 9.5%

Total Liabilities & Equity 376.1 398.1 -5.5% 325.1 15.7%

43 43

Corporate Access Links

Corporate Headquarters:

One NBAD Tower, Sheikh Khalifa St PO Box 4, Abu Dhabi, UAE Tel : +971-2-6111111 Fax : +971-2-6273170 Website : http://www.nbad.com

Michael Miller Head – Investor Relations, Media & PR

Abhishek Kumat Investor Relations

Fadeela Khamis Media & PR

44