INVESTOR PRESENTATION - Groupe Casino FR · INVESTOR PRESENTATION APRIL 2015 . CONTENTS Casino’s...

35

INVESTOR PRESENTATION APRIL 2015

Transcript of INVESTOR PRESENTATION - Groupe Casino FR · INVESTOR PRESENTATION APRIL 2015 . CONTENTS Casino’s...

INVESTOR

PRESENTATION

APRIL 2015

CONTENTS

Casino’s business profile

2014 highlights

Strategic priorities

Update on recent trading: Q1 2015

2

1

2

3

1

2

4

CASINO’S BUSINESS PROFILE

1

CASINO HAS A UNIQUE BUSINESS PROFILE

2014 Group sales

4

Strong mix of formats in France

Leadership positions in a limited number of attractive countries

Fast-growing non-food E-commerce platform

France Retail 39%

International Retail 54%

E-commerce 7%

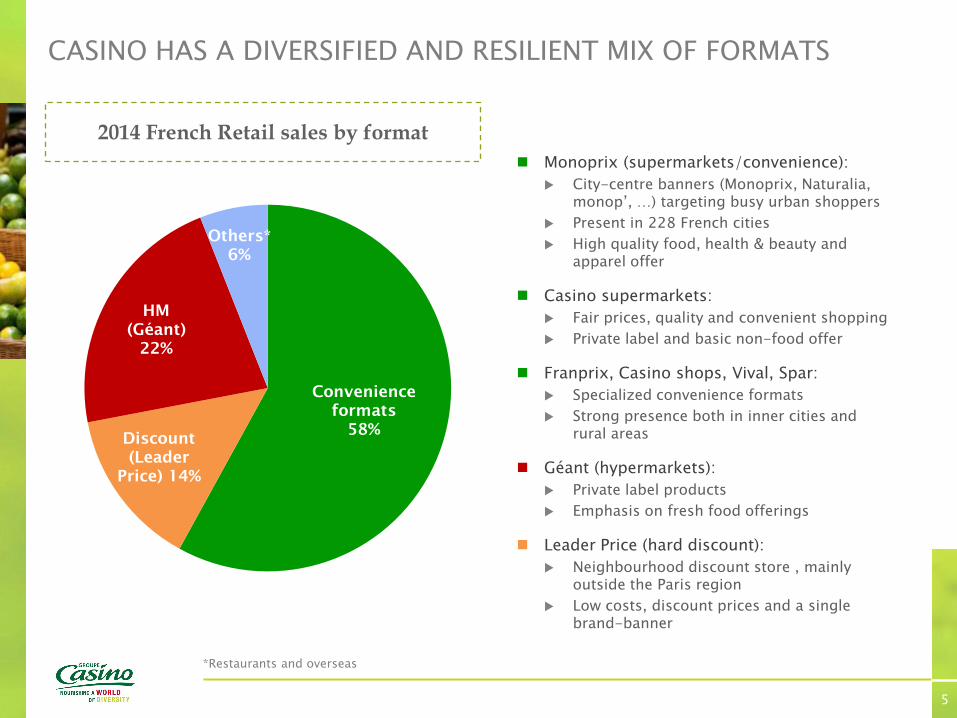

CASINO HAS A DIVERSIFIED AND RESILIENT MIX OF FORMATS

2014 French Retail sales by format

*Restaurants and overseas

5

Monoprix (supermarkets/convenience):

City-centre banners (Monoprix, Naturalia, monop’, …) targeting busy urban shoppers

Present in 228 French cities

High quality food, health & beauty and apparel offer

Casino supermarkets:

Fair prices, quality and convenient shopping

Private label and basic non-food offer

Franprix, Casino shops, Vival, Spar:

Specialized convenience formats

Strong presence both in inner cities and rural areas

Géant (hypermarkets):

Private label products

Emphasis on fresh food offerings

Leader Price (hard discount):

Neighbourhood discount store , mainly outside the Paris region

Low costs, discount prices and a single brand-banner

Convenience

formats

58% Discount

(Leader

Price) 14%

HM

(Géant)

22%

Others*

6%

CASINO HAS BUILT ITS INTERNATIONAL EXPOSURE WITH A CLEAR FOCUS ON ATTRACTIVE COUNTRIES

Casino has favored countries with the following characteristics:

Fast-growing markets

Large and young population

Business friendly environment

Casino has leading positions in 4 such countries representing c.400 million inhabitants : Brazil: GPA; Colombia: Exito; Thailand and Vietnam: Big C

Large and young populations

Thailand Vietnam Colombia Brazil

Modern trade* Traditional trade

Still low formal distribution Fast-growing markets

France

197

87 70

47

Millions of inhabitants

Thailand Vietnam Colombia Brazil

% of population below 15 years old

20% 25% 27% 26%

Sources: CIA World Factbook (May 2012), IMF World Economic Outlook Database (April 2012), AC Nielsen , World Bank, Economists Consensus

*as opposed to traditional retail shops, modern trade refers to a full range of sale methods based on marketing techniques

-0,7

3,6 3,8

6,0

1,3

3,7 3,9

6,1 2015

2016

Expected GDP growth

58%

86%

53% 52%

42%

14%

47% 48%

6

1

11

21

31

41

51

61

10

110

210

310

410

510

610

710

2010 2011 2012 2013 2014

Sales

EBITDA

200

300

400

500

600

700

800

900

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

2010 2011 2012 2013 2014

Sales

EBITDA

2

4

6

8

10

12

14

16

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014

Sales

EBITDA

BIG C, EXITO AND GPA HAVE POSTED STEADY AND REGULAR GROWTH IN SALES AND EARNINGS SINCE THEIR ACQUISITION BY CASINO

SALES (in BRL billions)

EBITDA (in BRL billions)

SALES (in THB billions)

EBITDA (in THB billions)

SALES (in COP billions)

EBITDA (in COP billions)

7

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014 2015

Exito

IGBC

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014 2015

GPA

IBOV

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013 2014 2015

Big C

SET

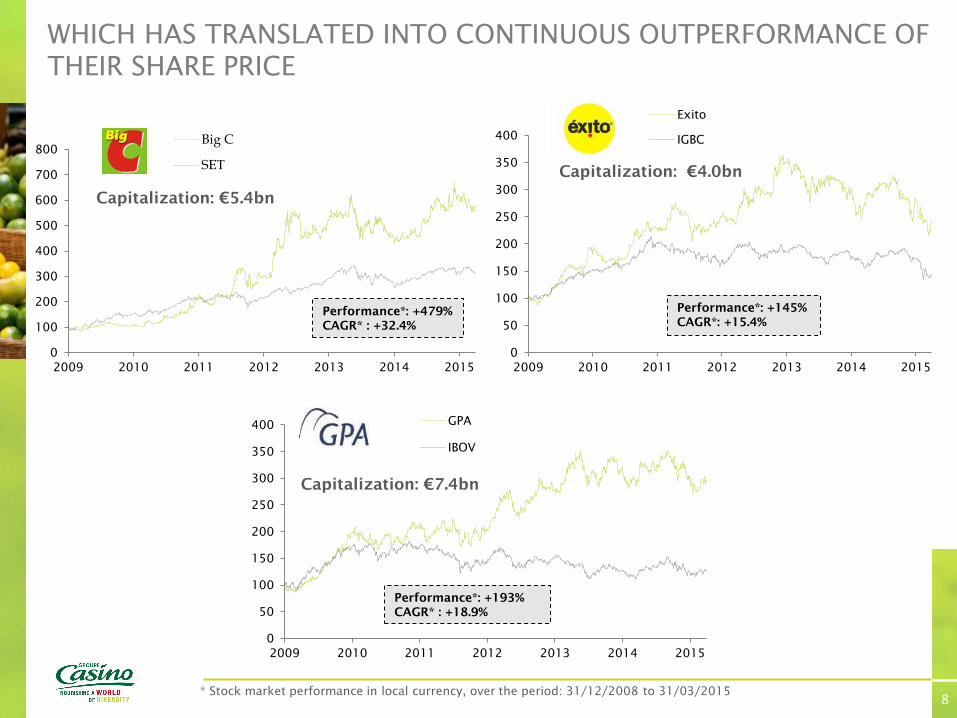

WHICH HAS TRANSLATED INTO CONTINUOUS OUTPERFORMANCE OF THEIR SHARE PRICE

* Stock market performance in local currency, over the period: 31/12/2008 to 31/03/2015

Performance*: +479%

CAGR* : +32.4%

Performance*: +193%

CAGR* : +18.9%

8

Capitalization: €5.4bn

Capitalization: €4.0bn

Capitalization: €7.4bn

Performance*: +145%

CAGR*: +15.4%

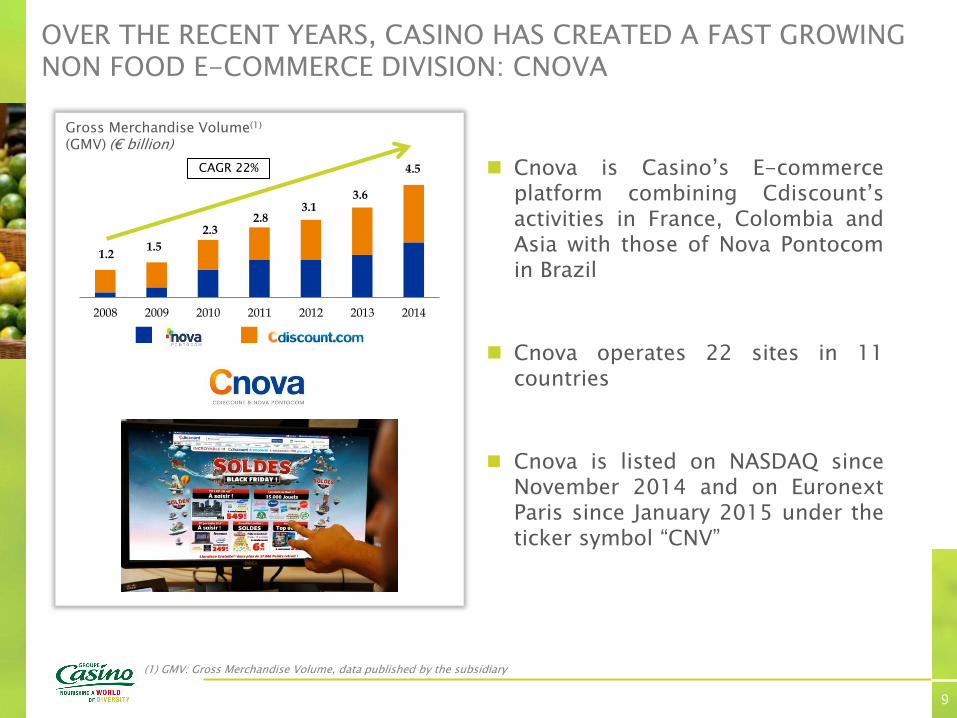

OVER THE RECENT YEARS, CASINO HAS CREATED A FAST GROWING NON FOOD E-COMMERCE DIVISION: CNOVA

Cnova is Casino’s E-commerce platform combining Cdiscount’s activities in France, Colombia and Asia with those of Nova Pontocom in Brazil

Cnova operates 22 sites in 11 countries

Cnova is listed on NASDAQ since November 2014 and on Euronext Paris since January 2015 under the ticker symbol “CNV”

(1) GMV: Gross Merchandise Volume, data published by the subsidiary

2008 2009 2010 2011 2012 2013 2014

3.6 3.1

2.8 2.3

1.5 1.2

CAGR 22%

Gross Merchandise Volume(1) (GMV) (€ billion)

4.5

9

2

2014 HIGHLIGHTS

Continuing the strategy centred on the 4 priorities of the Group: discount banners (hypermarkets and Leader Price), premium banners, convenience and E-commerce

End of the price repositioning cycle of discount banners : Géant and Leader Price

Géant: now co-leader in terms of price for the hypermarket segment* in France with food sales growing since Q4

Leader Price: Leader Price is now positioned as the least expensive banner on the market*

* Independent panels

FRANCE (1/2)

11

Satisfactory development of premium and convenience banners

Monoprix: continued expansion in different formats (Monoprix, Monop’, Naturalia, etc.) and high margin maintained

Convenience banners: substantial increase in sales, success of renovations and resumption of expansion (Leader Price Express)

Partnership agreement in the area of purchasing signed with Intermarché

* Independent panels

FRANCE (2/2)

12

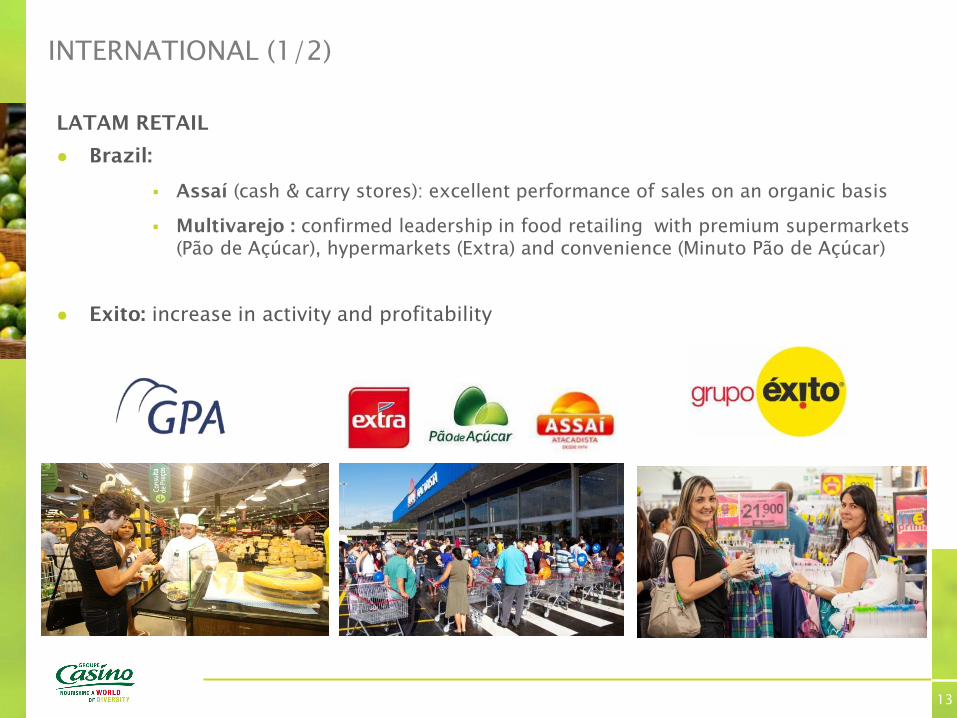

LATAM RETAIL

● Brazil:

Assaí (cash & carry stores): excellent performance of sales on an organic basis

Multivarejo : confirmed leadership in food retailing with premium supermarkets

(Pão de Açúcar), hypermarkets (Extra) and convenience (Minuto Pão de Açúcar)

● Exito: increase in activity and profitability

INTERNATIONAL (1/2)

13

LATAM ELECTRONICS

Viavarejo: leader in South America in the distribution of electronic products and furniture,

gaining market share

ASIE

● Very satisfactory operating and financial performances

● Big C Thailand : Improvement in profitability in an unfavorable local context

● Big C Vietnam : Organic growth of sales in a context of macroeconomic slowdown

INTERNATIONAL (2/2)

THAILAND VIETNAM

14

CNOVA: ANOTHER QUARTER OF STRONG GROWTH OF GMV AND NET SALES IN 2015

GMV(1) of €4.5bn (+28.2%)

Net sales of €906mn (+17,7%)

14.8m active customers(2) in the world (+27.6%)

9.3m orders(3) (+38.2%)

16.0m units sold (+38.9%)

(1) GMV: Gross Merchandise Volume, data published by the subsidiary (2) Active customers at the end of March having purchased at least once through our sites over the last 12 months (3) Total placed orders before cancellation due to fraud or customers not paying for their order

15

CASINO CONTINUOUSLY MAINTAINS A STRONG FINANCIAL DISCIPLINE

16

All international subsidiaries are FCF positive:

Strong cash-flow

Rigorous monitoring of capex and positive working capital generation

Casino operates in countries where dividends are fully convertible and can be repatriated without significant tax leakage

Our balance sheet no longer carries significant put options

Casino has a proven track record of optimizing its capital allocation through:

Disposals

Asset rotation

Partial recap

STRATEGIC PRIORITIES

3

● Casino’s revenue rose by +67% over the past 5 years, exceeding €48bn in 2014 to rank 11th among worldwide food distributors

● This strong growth, topping the largest distribution companies according to the most recent Deloitte study*, was built by prioritizing development in the most buoyant countries and formats

2010

2014

2010

2014

2010

2014

2010

2014

2010

2014

Casino Group

GPA

€48.5bn

€29.1bn

R$65.5bn

R$32.1bn

Cnova Exito Big C Thailand

€4.5bn

€2.3bn

COP11.420bn

COP7.325bn

THB121.8bn

THB83.9bn

CAGR: +19.5% CAGR: +18.3% CAGR: +11.7% CAGR: +9.8%

* Global Powers of Retailing 2015, published January 2015 – Growth rate of +11.1% for Casino between 2008 and 2013

CAGR: Compound Annual growth Rate of sales (except for Cnova – data in GMV)

CAGR +13.6%

THE GROUP IN 2015

18

● After their pricing repositioning, develop discount banners in France and accelerate international roll-out

● Strengthen leadership position in premium formats

● Boost expansion in convenience formats

● Cnova: maintain strong growth and Cash Flow generation

● Continue to improve operational efficiency: optimize costs and purchasing

CONTINUED ROLLOUT OF THE GROUP’S 5 STRATEGIC PRIORITIES

19

● Success of the overhaul of Géant and Leader Price’s business model

• Géant currently co-leader in terms of prices for hypermarkets*

• Leader Price now the lowest priced banner in the market* and in recovery since Q4 2014

● Roll-out of new concepts such as Leader Price Express,

a discount convenience format

● Internationally, continued and sustained Cash & Carry expansion

• Ongoing improvement in Assaí market share,

currently No. 2 in the segment in Brazil

• In Columbia, rapid roll-out of Surtimax using a single

membership model in addition to expansion

• Adaptation of Cash & Carry model in Asia: Big C compact

AFTER THEIR PRICING REPOSITIONING, DEVELOP DISCOUNT BANNERS IN FRANCE AND ACCELERATE INTERNATIONAL ROLL-OUT

* Independent panels

20

STRENGTHEN LEADERSHIP POSITION IN PREMIUM FORMATS

● Leading position in three of the Group’s key countries with 900 stores at the end of 2014:

• 540 Monoprix stores / 92 Naturalia in France

• 181 Pão de Açúcar in Brazil

• 71 Carulla in Colombia

● Accelerate expansion to strengthen this unique position

• In France, expansion into the profitable Monoprix formats: City Marché, Monop’, Naturalia, ...

• In Colombia and Brazil, an ambitious plan to open some 40 stores a year under existing banners

21

BOOST EXPANSION IN CONVENIENCE FORMATS

● In France, overhaul concepts and re-launch franchise: Franprix, Vival, Spar, ...

• A unique network owing to its density of over 6,000 stores

• Positive results from business re-launch plans and store renovations

• Launching of new formats in 2015

● Internationally, a new priority: convenience stores development

• A network of 704 stores at the end of 2014, 324 of which are in Thailand, 256 in Brazil and 102 in Colombia

• A strong ambition in international development (approximately 100 stores a year) with store models suited to the local market

22

● Continue solid sales growth and GMV

● Maintain price positioning for sites and broaden their assortment

● Sharply accelerate development of marketplaces and mobile sales

● Continue to launch new international and specialized sites

● Continue to improve synergies with the Group: procurement, logistics and pickup points

CNOVA: MAINTAIN STRONG GROWTH AND CASH FLOW GENERATION

23

● In France, agreement signed with Intermarché to create a shared buying group

● Internationally, the Group’s size is a major asset in business negotiations with international suppliers

● In non-food, improved purchasing synergies between Cnova, Viavarejo and Casino

OPERATIONAL EFFICIENCY: IMPROVING PURCHASING TERMS

24

● Proactive and highly disciplined approach to controlling costs at all banners in all of the Group’s geographic regions

● Lowering operational and structural costs: a systematic approach based on productivity benchmarks and shared processes

● Investment optimization: reducing per square meter building costs and expansion using models that require less capital

● Gradual implementation of synergies between banners

• Budget for IT and advertising agencies

• Sourcing and own brands (Casino, Finlandek, etc.)

• Multichannel: Click & Collect (France, Brazil, etc.)

• Etc.

OPERATIONAL EFFICIENCY: COST CONTROL AND SYNERGIES

25

UPDATE ON RECENT TRADING : Q1 2015

4

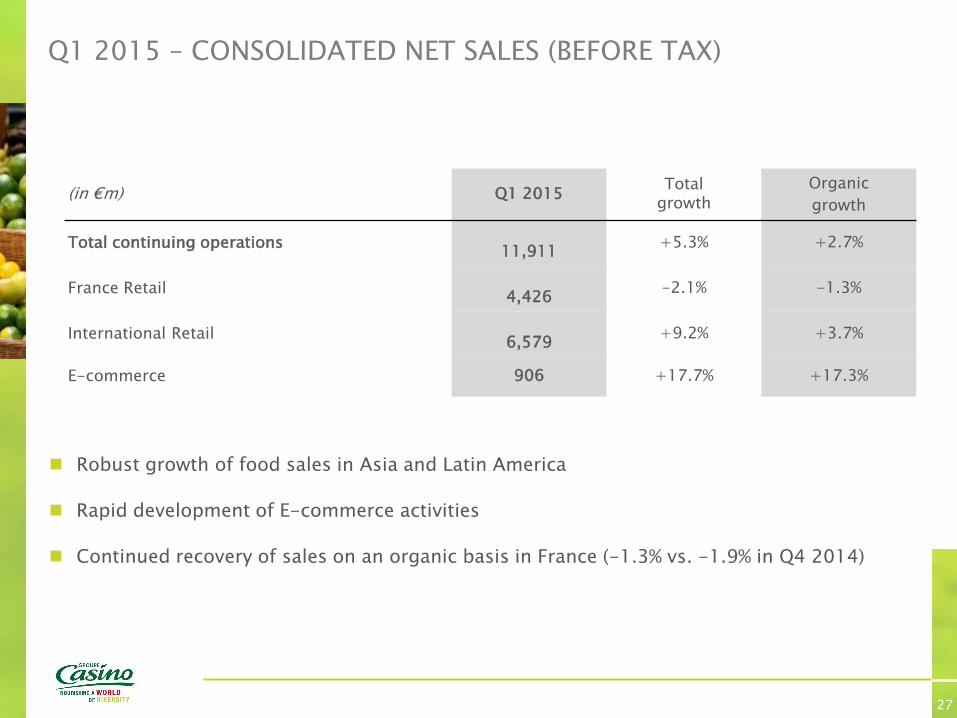

Q1 2015 – CONSOLIDATED NET SALES (BEFORE TAX)

27

(in €m) Q1 2015 Total

growth

Organic

growth

Total continuing operations

11,911 +5.3% +2.7%

France Retail

4,426 -2.1% -1.3%

International Retail

6,579 +9.2% +3.7%

E-commerce 906 +17.7% +17.3%

Robust growth of food sales in Asia and Latin America

Rapid development of E-commerce activities

Continued recovery of sales on an organic basis in France (-1.3% vs. -1.9% in Q4 2014)

Q1 2015 – PERFORMANCE BY SEGMENT

28

France Retail: price cuts in 2014 continue to impact sales in France of -1.9%. Same-store sales for all banners improved sequentially compared to the previous quarter. Volumes are up both in same-store sales (+0.3%) and organic (+0.6%)

Food sales in Latin America: strong growth due to an acceleration in organic growth and the integration of Super Inter in Colombia

Viavarejo: broadly stable excluding the impact of the store closings

Food retailing business in Asia: organic growth improved compared to the previous quarter and same-store growth is now positive

Cnova: strong growth in net sales with an increase in customer loyalty; very high rate of marketplace growth in both regions

(in €m) Q1 2015 Total growth Organic growth Same-store growth

France Retail 4,426 -2.1% -1.3% -1.6%

Latam Retail 3,870 +10.2% +6.1% +2.6%

Latam Electronics 1,666 -0.8% -1.3% -2.7%

Asia 1,043 +25.4% +3.7% +0.3%

E-commerce 906 +17.7% +17.3% +17.0%

APPENDICES

Q1 2015 FRANCE RETAIL – PERFORMANCE BY BANNERS

30

(in €m) Q1 2015 Total growth Organic growth Same-store growth

Géant Casino 1,053 -3.8% -1.5% -1.5%

Casino Supermarkets 741 -5.7% -3.7% -1.4%

Monoprix 1,016 +0.6% +0.9% +0.3%

Franprix – Leader Price 1,013 -1.8% -2.4% -5.6%

Convenience & Other* 602 +0.8% -0.3% +1.3%

* Includes the cafeterias, real estate, other and Indian Ocean activities

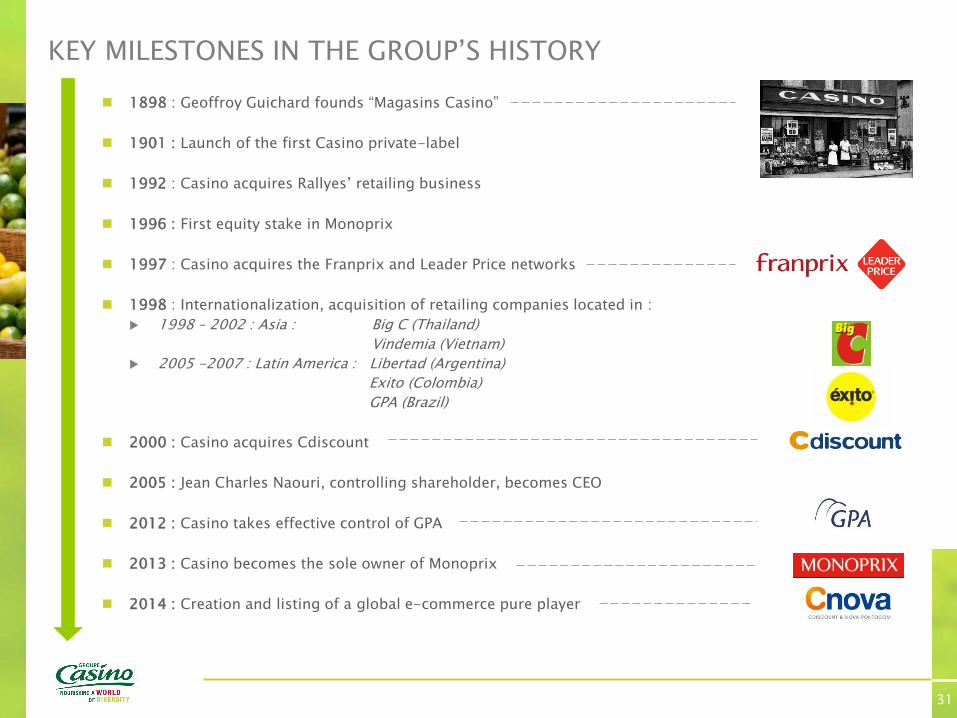

KEY MILESTONES IN THE GROUP’S HISTORY

1898 : Geoffroy Guichard founds “Magasins Casino”

1901 : Launch of the first Casino private-label

1992 : Casino acquires Rallyes’ retailing business

1996 : First equity stake in Monoprix

1997 : Casino acquires the Franprix and Leader Price networks

1998 : Internationalization, acquisition of retailing companies located in :

1998 – 2002 : Asia : Big C (Thailand)

Vindemia (Vietnam)

2005 -2007 : Latin America : Libertad (Argentina)

Exito (Colombia)

GPA (Brazil)

2000 : Casino acquires Cdiscount

2005 : Jean Charles Naouri, controlling shareholder, becomes CEO

2012 : Casino takes effective control of GPA

2013 : Casino becomes the sole owner of Monoprix

2014 : Creation and listing of a global e-commerce pure player

31

IN FRANCE, CASINO HAS UNDISPUTED LEADERSHIP IN CONVENIENCE FORMATS

Q1 2015 figures

32

Number

of stores

Average retail

space in sqm

444 c.1,600

632 c.1,200

860 c.430

1,267 c.160

200 c.180

889 c.270

1,726 c.100

Others (corners,…) 2,717 ns

Casino believes in smaller formats:

Various, segmented and flexible, they perfectly fit

the customers’ needs and behaviors for a more

diversified and easy-to-reach choice

Casino’s proximity stores in France

North-West

North-East

South-West

South-East

6%

39%

14%

41%

CASINO OPERATES IN A UNIQUE MIX OF COUNTRIES THROUGH LEADING RETAILERS

33

Q1 2015 Market capitalization (as of 31 March 2015): Bloomberg

#1 retailer

#2 e-tailer

2,159 stores

1.3m m²

#1 retailer

#1 e-tailer

1,397 stores

0.6m m² Co-leader

in HM

643 stores

1.7m m²

#1 in HM 40 stores 0.1m m²

#4 food retailer

#1 e-tailer

10,515 stores

4.1m m²

France

Vietnam

Thailand Brazil

Colombia Uruguay

€4.0bn market cap.

#1 retailer

54 stores

0.1m m²

€9.3bn market cap.

€7.4bn market cap.

€5.4bn market cap.

CNOVA SHAREHOLDER STRUCTURE

Economic interest

In % Cnova

Casino Group 58.1%

Minority 41.9%

Minority interests

43.3% 41.3%

52.3% 43.9% 43.3% 0.1%

54.8%

Management

50.0% 3.7%

6.6%

% of capital

Nova HoldCo

34

DISCLAIMER

This presentation contains forward-looking information and statements about Casino. Forward-looking statements are statements that are not historical facts. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, products and services, and statements regarding future performance. Forward-looking statements are generally identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates” and similar expressions. Although the management of Casino believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of Casino securities are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and generally beyond the control of Casino, that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in Casino’s public filings with the Autorité des marchés financiers (“AMF”), including those listed under “Risk Factors and Insurance” in the Registration Document filed by Casino on 28 March 2013. Except as required by applicable law, Casino undertakes no obligation to update any forward-looking information or statements.

This material was prepared solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Likewise it does not give and should not be treated as giving investment advice. It has no regard to the specific investment objectives, financial situation or particular needs of any recipient. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein. It should not be regarded by recipients as a substitute for the exercise of their own judgement. All opinions expressed in this material are subject to change without notice.

This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated in whole or in part without the prior written consent of Casino Group.