Investor Presentation - CLP Group | Energy for Brighter ... · 4 Strong industry fundamentals One...

33

April 2012 Investor Presentation

Transcript of Investor Presentation - CLP Group | Energy for Brighter ... · 4 Strong industry fundamentals One...

April 2012

Investor

Presentation

2

Agenda

1. TRUenergy overview

2. Retail scale and quality

3. Diverse generation portfolio supported by

strong fuel position

4. Strong financial position

5. Recent corporate activity

TRUenergy Overview

4

Strong industry fundamentals

One of Australia’s largest gas and electricity utilities

Vertically integrated, diversified portfolio provides earnings stability

Outstanding track record of earnings growth through disciplined acquisition and

organic growth

Low cost generation portfolio is well positioned for upside through rising

wholesale prices

Extensive pipeline of development opportunities in retail and generation

Financial strength and flexibility

Well positioned for a low carbon economy driving efficient energy use

Highly experienced management team and Board

TRUenergy Overview

5

Ownership Hong Kong listed CLP Holdings Limited

Total Assets A$9.3b

Gross Debt A$2.4b

Revenue* A$6.9b (12 months to 31 Dec 2011)

EBITDAF* A$1,047m (normalised) (12 months to 31 Dec 2011)

NPAT* A$355m (normalised) (12 months to 31 Dec 2011)

Employees 1,285 FTE

Capacity Total installed capacity under management of 5,613 MW

Customers 2.8m accounts

TRUenergy has evolved to be one of Australia’s leading vertically integrated and diversified energy companies

Tallawarra Power

Station

(MW)

Tallawarra Power

Station

(420MW)

Hallett Power

Station

(203MW)

Cathedral Rocks

(66/33MW)

QLD Retail

63,000 accounts

Yallourn Power

Station and Coal Mine

(1,480MW)

Ecogen Hedge

(up to 966MW)

Gas Storage Facility

(22PJ Storage;

500TJ/d Processing)

Brisbane

Melbourne

Sydney Adelaide

SA Retail

0.2 million accounts

QLD Retail

0.1 million accounts

VIC Retail

1.2 million accounts

NSW/ACT Retail

1.4 million accounts

Waterloo

(111MW)

20% interest in Narrabri

(500PJ) Delta West

GenTrader

(2,400MW))

As at 31 December 2011

Power generation

The largest privately held supplier of generation output to the National

Electricity Market (“NEM”)

Diversified and reliable owned and contracted fuel supplies

Retail electricity and gas

Australia’s third largest energy retailer

Market share of 22% across Eastern Australia

Gas processing and storage

Owns the largest underground gas storage facility in Australia

Long-term gas storage contracts

Company Overview

Financial and Operational Overview (as at 31 Dec 2011)

* Includes only 10 months contribution from EnergyAustralia and Delta West Gentrader

A strong portfolio of diversified assets

6

Notes 1. As at 31 December 2011 2. TRUenergy analysis; Company presentations; Electricity Statement of Opportunities for the National Electricity Market 2011, Australian Energy Market Operator 3. Based on control and ownership of output; ORG includes Mortlake; AGL includes 32.5% of Loy Yang A (“LYA”); On 24 February 2012, AGL announced its intention to acquire the

remaining interest in LYA, should this transaction be successful, AGL’s generation capacity and output would increase to 5,377MW and 19,519GWh, respectively 4. 12 months to 30 June 2011; Inclusive of full year generation for Eraring, Shoalhaven, Mount Piper and Wallerawang 5. Total Registered Capacity with Australian Energy Market Operator

AGL Origin TRUenergy

# Mass Market Customers (‘000’s)(1)

Electricity 2,013 3,075 1,967

Gas 1,382 950 840

Generation Capacity (MW)(1,2,3,5) 3,906 5,784 5,613

Generation Output (GWh)(2,3,4) 9,148 17,596 29,603

Total capitalisation at 31 December 2011

(A$m book net debt + equity) 7,335 17,269 6,763

S&P / Moody’s Credit Ratings BBB (Negative) / – BBB+ (Stable) / Baa1 (Neg) BBB (Stable) / –

A scale player in the industry following acquisitions in NSW

NEM-wide Generation Capacity (MW)(1,2,3,5) NEM-wide Energy output (GWh) (2,3,4)

National Market Share % / Million Customers

Electricity & Gas Retail Customers(1,2)

TRUenergy is the national No. 1 generator by output and No. 3 energy retailer

4.0

3.4

2.82.3

-

1

2

3

4

5

Origin AGL TRU Other

32%

27% 22%

18%

15.7%

11.3% 11.1% 10.0% 9.7% 9.3%

4.9%

-

4.0%

8.0%

12.0%

16.0%

20.0%

TRU MacGen Stanwell CS Energy

Int. Power

Origin AGL

Private sector Government owned

5,784 5,6134,690 4,358 4,251 3,906

3,033

-

2,000

4,000

6,000

8,000

Origin TRU MacGen Snowy Hydro

Stanwell AGL Int. Power

Private sector Government owned

7

Managing Director

Richard McIndoe

Chief Financial Officer

James Spence

General Counsel & Company Secretary

David Lambert

Group Executive Manager Operations

& Construction

Michael Hutchinson

Group Executive Manager Energy

Markets

Mark Collette

Executive Manager Information

Services Gary Martin

Group Executive Manager Retail

Adrian Merrick

Executive Manager Human Resources

Adrian Merrick (Acting)

Experienced management team

Significant business and industry experience, track record of delivery

8

TRUenergy has evolved from a base load generator to a fully

integrated energy company

A clear strategy has resulted in a unique group of assets which fit the long term vision

Standalone Generator

Fully Integrated

Vertical Integration

Horizontal Integration

Base load brown coal

generator

Some vertical integration

through AusPower and

retailer contracts

Risks associated with single

generator in a single

market, long generation

position

Generation expansion

through acquisition, merger

and Greenfield development

Portfolio of generating

capacity in different states,

different fuel types, across

the merit order

Expansion of the I&C

business through AusPower

to track generation growth

Acquired direct interest in

mass market retailer

Creation of a horizontally

and vertically integrated

company

Generation and retail across

states

Australia’s third largest

energy retailer

Inv

estm

en

t

Time

Acquisition of NSW

assets 2011

Tallawarra site

commissioned 2009 Acquisition of Merchant

Energy Business 2005

Acquisition of Yallourn 2001

Iona expansion 2009

Acquisition of Narrabri

(20%)

Acquisition of Roaring

40s Wind Assets

9

Vertical integration is the key strategic driver

Mass Market

Retail Load

Sold

Contracts

Load

Swing

National Electricity

Market

Generation

Energy

Bought

Contracts

Electricity

Operations &

Construction Energy Markets

Hallett

Tallawarra

Ecogen

Yallourn

Electricity

Channels to Market

Mass Market Retail

Business Retail

Generation

Capacity

Reta

il

Energ

y M

ark

ets

I&C/Business Load

Balanced Capacity

Balanced Energy

Available for Sale Sales

Mt Piper & Wallerawang Pricing, forecasting & green certificates

Outage planning, bidding & dispatch

The TRUenergy portfolio is well balanced with significant scale and diversity

10

TRUenergy value chain

Fuel Wholesale MarketsRetail

Markets

Gas Market

Electricity Market

TRUenergy Business Units

Operations and ConstructionEnergy Markets

Retail

Yallourn Coal Mine

Coal Contracts

Iona Gas Processing and

Storage

Tallawarra

Hallett

Ecogen

Yallourn

Delta West

Mass Market and Business

customer segments

Mass Market and Business

customer segments

Hedging

Wholesale (pool)

Contracts

Wholesale Market

Industrial Contracts

Industrial Contracts

Hedging

Gas Supply / Transportation

Contracts

Waterloo

Cathedral Rocks

Wind

Narrabri CSM

Gas Supply / Transportation

Contracts

Narrabri CSM

11

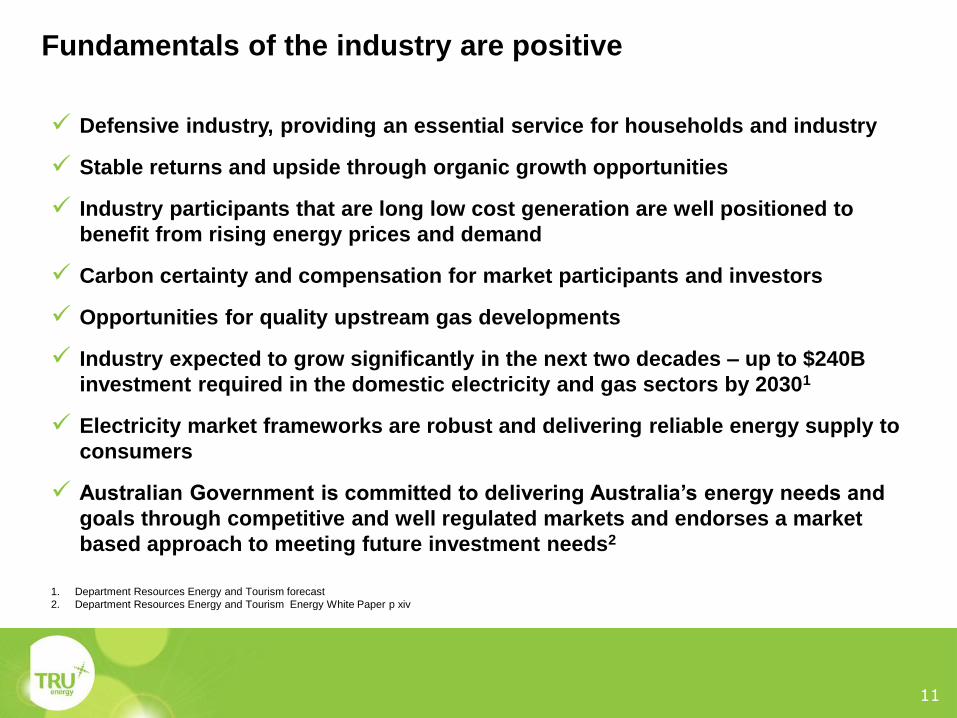

Defensive industry, providing an essential service for households and industry

Stable returns and upside through organic growth opportunities

Industry participants that are long low cost generation are well positioned to

benefit from rising energy prices and demand

Carbon certainty and compensation for market participants and investors

Opportunities for quality upstream gas developments

Industry expected to grow significantly in the next two decades – up to $240B

investment required in the domestic electricity and gas sectors by 20301

Electricity market frameworks are robust and delivering reliable energy supply to

consumers

Australian Government is committed to delivering Australia’s energy needs and

goals through competitive and well regulated markets and endorses a market

based approach to meeting future investment needs2

Fundamentals of the industry are positive

1. Department Resources Energy and Tourism forecast

2. Department Resources Energy and Tourism Energy White Paper p xiv

12

Key business strengths

Robust financial position and strong

credit metrics supporting

investment grade rating

Proven strong debt market and

shareholder support

Clear carbon strategy and

actively managed environmental

issues

Sound operating performance

Experienced management team

Horizontally diversified retail and generation portfolio

and fuel base

Vertically integrated business model

provides a natural hedge

Strong market position

TRUenergy

Retail Scale and Quality

14

NSW

~32% of market

Victoria

~25% of market

South Australia

~12% of market

Queensland

~5% of market

TRU

948

EA

200

TRU

97

EA

1,307

TRU

65

EA

31

TRU

157

One of Australia’s largest gas and electricity utilities

22% share of the NEM, #3 provider

Over 2.8m customer accounts, comprising 2.0m electricity and

0.8m gas accounts

Geographically diversified customer base across the NEM

High quality, recognised retail brands

EnergyAustralia and TRUenergy are trusted brands with a

reputation for efficiency and service

Significant organic growth opportunities in

Queensland and South Australia

Ability to flex sales effort in these states according to value

opportunities

Positioned to leverage growth in retail gas

Able to leverage existing NSW electricity customers into new

retail gas accounts

The combined business of EnergyAustralia and TRUenergy creates a truly national leader with ~22% share of the NEM

TRUenergy has a market leading position in the NEM

As at 31 December 2011

15

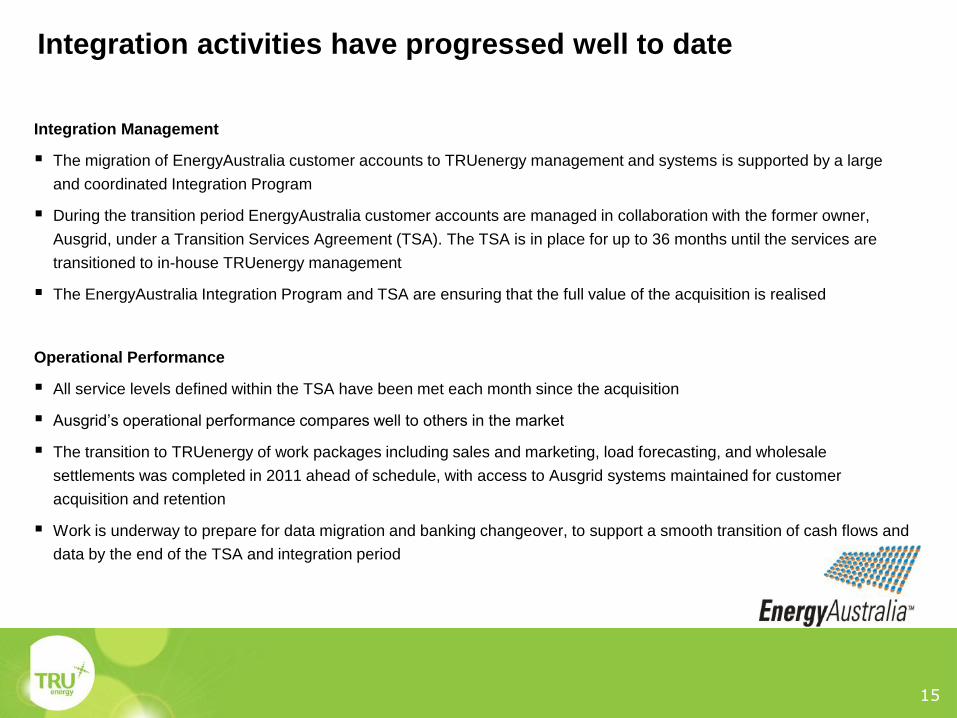

Integration activities have progressed well to date

Integration Management

The migration of EnergyAustralia customer accounts to TRUenergy management and systems is supported by a large

and coordinated Integration Program

During the transition period EnergyAustralia customer accounts are managed in collaboration with the former owner,

Ausgrid, under a Transition Services Agreement (TSA). The TSA is in place for up to 36 months until the services are

transitioned to in-house TRUenergy management

The EnergyAustralia Integration Program and TSA are ensuring that the full value of the acquisition is realised

Operational Performance

All service levels defined within the TSA have been met each month since the acquisition

Ausgrid’s operational performance compares well to others in the market

The transition to TRUenergy of work packages including sales and marketing, load forecasting, and wholesale

settlements was completed in 2011 ahead of schedule, with access to Ausgrid systems maintained for customer

acquisition and retention

Work is underway to prepare for data migration and banking changeover, to support a smooth transition of cash flows and

data by the end of the TSA and integration period

Diverse generation portfolio supported by strong fuel position

17

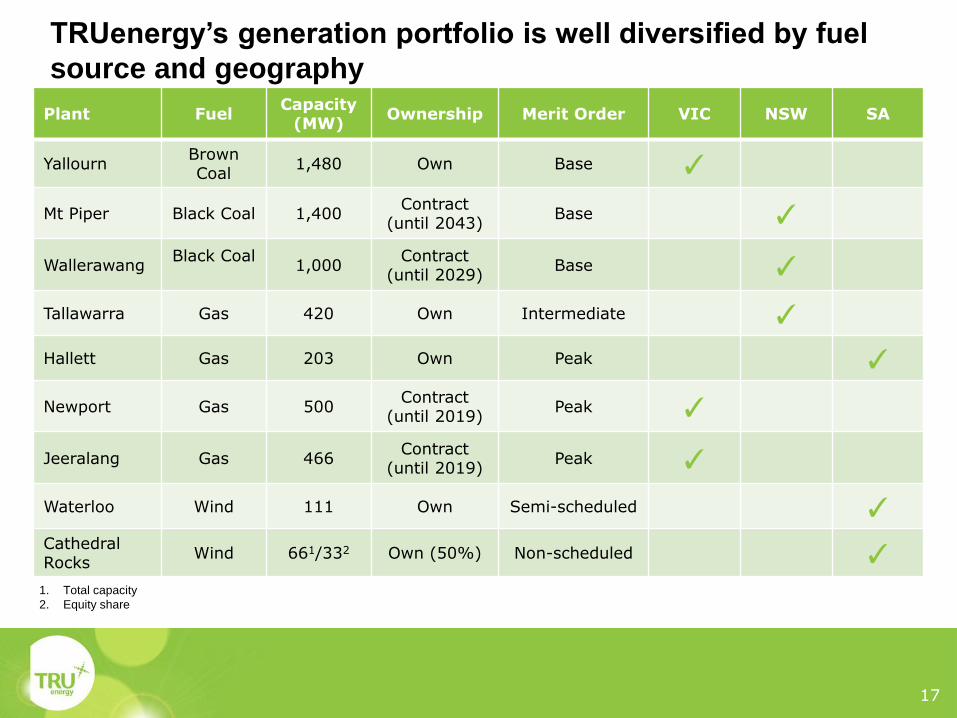

TRUenergy’s generation portfolio is well diversified by fuel

source and geography

Plant Fuel Capacity

(MW) Ownership Merit Order VIC NSW SA

Yallourn Brown Coal

1,480 Own Base ✓

Mt Piper Black Coal 1,400 Contract

(until 2043) Base ✓

Wallerawang Black Coal

1,000

Contract (until 2029)

Base ✓

Tallawarra Gas 420 Own Intermediate ✓

Hallett Gas 203 Own Peak ✓

Newport Gas 500 Contract

(until 2019) Peak ✓

Jeeralang Gas 466 Contract

(until 2019) Peak ✓

Waterloo Wind 111 Own Semi-scheduled ✓ Cathedral Rocks

Wind 661/332 Own (50%) Non-scheduled ✓ 1. Total capacity

2. Equity share

18

Fuel Plant Fuel Arrangement

Brown Coal Yallourn TRUenergy owns the brown coal mine adjacent to power

station Operating licence to 2026 and reserves beyond 2032

Black Coal

Mt Piper Portfolio of long term coal supply contracts through to 2029 Diversity of coal supply from different mines Volume flexibility in existing supply contracts and ability to

defer to take advantage of uplift in pool prices Continue to negotiate longer term coal supply contract on

competitive prices Wallerawang

Gas

Tallawarra

Portfolio of long term gas contracts through to 2021 (plus equity gas from Narrabri) Subject to Take-or-Pay arrangements, but with rights to bank

gas for use at later times Gas storage provides considerable flexibility in managing gas

requirements

Hallett

Newport

Jeeralang

Generation assets are supported by long term fuel supply

contracts

19

Other TRUenergy assets further reinforces it as an integrated

energy business

Upstream Gas Gas Supply Contracts

Gas Storage

Acquired 20% interest in Narrabri Project in Gunnedah

Basin (NSW)

Effective interest of over 500PJ of coal seam gas

reserves

Hedges rising gas price risk with potential development

upside

Experienced partner in Santos

Portfolio of gas supply contracts from multiple suppliers

Total volumes of 1,100PJ over the next seven years

(sufficient to cover internal requirements over this

period)

Gas storage facility at Iona (Victoria)

22PJ of underground gas storage

Capacity of 500TJ/day

Supplies gas to Victoria and South Australia

Provides TRUenergy with the option to store surplus gas

during off peak periods and withdraw during peak periods to

manage seasonality in demand and hedge against price

spikes

20

TRUenergy’s generation portfolio broadly reflects NEM

intensity

Largest privately-owned energy portfolio in the NEM

TRUenergy’s portfolio carbon intensity of 0.95 compared with NEM of ~0.89

Yallourn’s captive coal mine provides a fixed low cost fuel source, contributing to a low cost generation

portfolio

Yallourn is very well positioned to benefit from a rising wholesale gas price market, despite the

introduction of the carbon tax from 1 July 2012

20%

27%

53%

Source: TRUenergy estimates and ACIL Tasman market model data

TRUenergy Fuel Mix1 NEM Fuel Mix2

Yallourn 27%

Tallawarra 8%

Hallett 4%

Ecogen 18%

Mt Piper 25%

Wallerawang 18%

Brown Coal Gas Black Coal

2. Excludes hydro, wind and others

Source: TRUenergy estimates and ACIL Tasman market model data

1. Excludes wind

21

Thermal Status

Marulan 700MW Investment decision to be made first half 2012 Fully Permitted

Ipswich Up to

1,500MW

Development underway; targeting 2013 investment decision for

500MW Early Stage

Gladstone Up to

1,500MW Development process progressing for 500MW Early Stage

Tallawarra B 420MW Permitted for CCGT; awaiting market signals Fully Permitted

Yallourn CCGT 1,000MW Near finalisation of permits; awaiting contract for closure outcomes Late Stage

Strzelecki Up to 800MW Land option secured; permitting to commence in 2012 Early Stage

Wind Status

Stony Gap 123 MW Development application lodged Late Stage

Robertstown 75MW Meetings conducted with landowners Late Stage

Waterloo II 18MW Aim to lodge development application May 2012 Late Stage

White Rock 150MW+ Site secured with milestone based option agreement Early Stage

Pipeline of generation projects at different stages of permitting

Final investment decision will be contingent on strategic fit within portfolio, market signals and

maintaining current credit rating

Strong pipeline of new generation projects to support

retail load

22

Asset CO2 Int.*

(kg/kWh) Increase in carbon price

Increase in gas price

Comment

Yallourn 1.39 ✓ A$350m impairment (pre-tax) Transitional Assistance (cash and free

carbon permits)

Delta Western (Mt Piper/Wallerawang)

0.90 / 0.92 ✓ Lower gross margins following introduction

of carbon pricing but offset by increasing gas prices

Ecogen (Newport / Jeeralang)

0.56 / 0.94 ✓ Improved position in merit order following

introduction of carbon

Tallawarra 0.37 ✓ Higher efficiency reduces its exposure to

increases in gas prices relative to other gas power plants

Hallett 1.05 ✓ - Increase market price volatility results in

higher usage and profitability

Wind n/a ✓ ✓ Higher pool prices with no change to cost

base

Iona Gas Storage n/a ✓ ✓ Value of inventory and gross margins

increases with increases in carbon and gas prices

Narrabri CSM n/a ✓ ✓ Increase in underlying asset value

Impact of carbon and gas price on TRUenergy’s asset portfolio

* Calculated on a “sent out” basis

Strong financial position

24

170

180

190

200

210

220

2008 2009 2010 2011*

A$

m

CAPEX^

0

2,000

4,000

6,000

8,000

2008 2009 2010 2011*

A$

m

Revenue

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011*

A$

m

EBITDAF

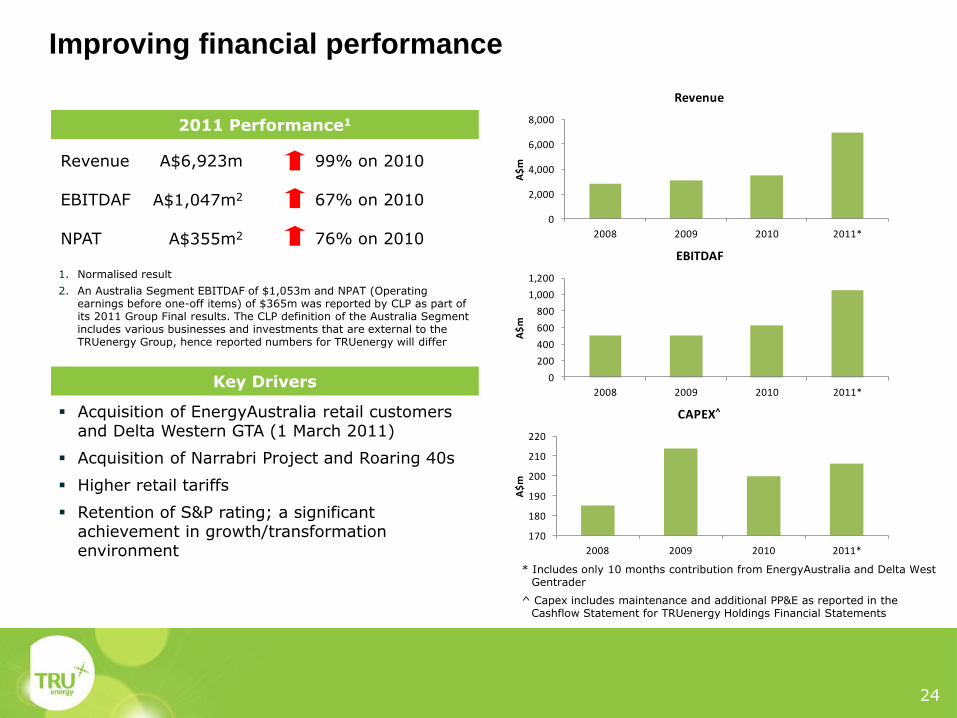

Revenue A$6,923m 99% on 2010

EBITDAF A$1,047m2 67% on 2010

NPAT A$355m2 76% on 2010

*

Improving financial performance

Acquisition of EnergyAustralia retail customers and Delta Western GTA (1 March 2011)

Acquisition of Narrabri Project and Roaring 40s

Higher retail tariffs

Retention of S&P rating; a significant achievement in growth/transformation environment

1. Normalised result

2. An Australia Segment EBITDAF of $1,053m and NPAT (Operating earnings before one-off items) of $365m was reported by CLP as part of its 2011 Group Final results. The CLP definition of the Australia Segment includes various businesses and investments that are external to the TRUenergy Group, hence reported numbers for TRUenergy will differ

2011 Performance1

Key Drivers

* Includes only 10 months contribution from EnergyAustralia and Delta West Gentrader

^ Capex includes maintenance and additional PP&E as reported in the Cashflow Statement for TRUenergy Holdings Financial Statements

25

Revolving

47%

MTN

19%

USPP14%

WCF20%

0

200

400

600

800

1,000

1,200

2012 2013 2014 2015 2016 2017 2018+

Revolving MTN USPP WCF

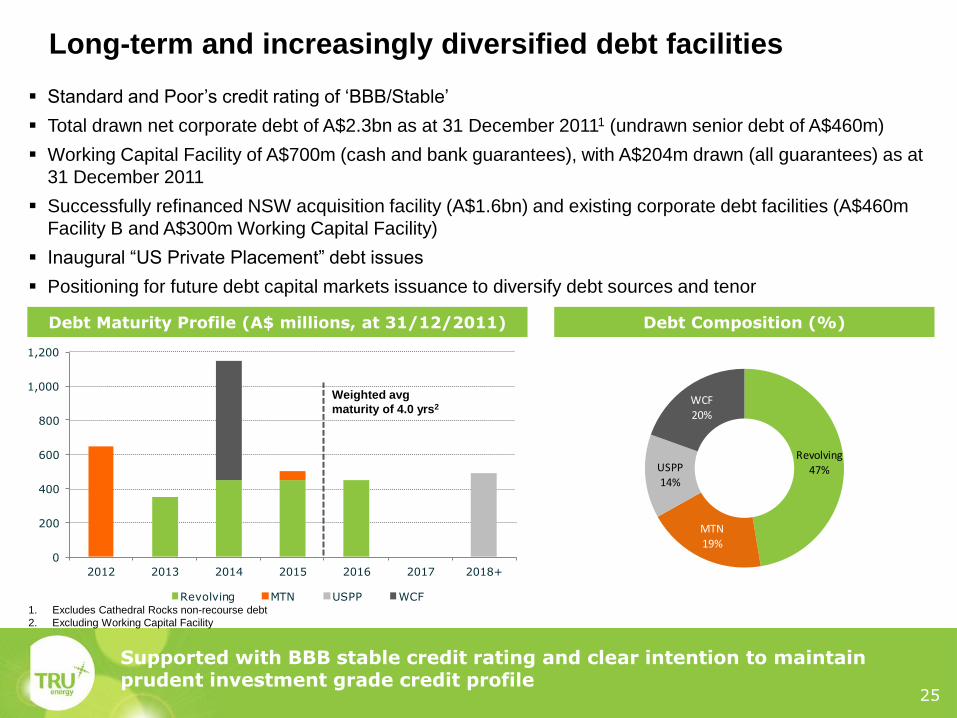

Supported with BBB stable credit rating and clear intention to maintain prudent investment grade credit profile

Standard and Poor’s credit rating of ‘BBB/Stable’

Total drawn net corporate debt of A$2.3bn as at 31 December 20111 (undrawn senior debt of A$460m)

Working Capital Facility of A$700m (cash and bank guarantees), with A$204m drawn (all guarantees) as at

31 December 2011

Successfully refinanced NSW acquisition facility (A$1.6bn) and existing corporate debt facilities (A$460m

Facility B and A$300m Working Capital Facility)

Inaugural “US Private Placement” debt issues

Positioning for future debt capital markets issuance to diversify debt sources and tenor

1. Excludes Cathedral Rocks non-recourse debt

2. Excluding Working Capital Facility

Debt Maturity Profile (A$ millions, at 31/12/2011) Debt Composition (%)

Weighted avg

maturity of 4.0 yrs2

Long-term and increasingly diversified debt facilities

Recent Corporate

Activity

27

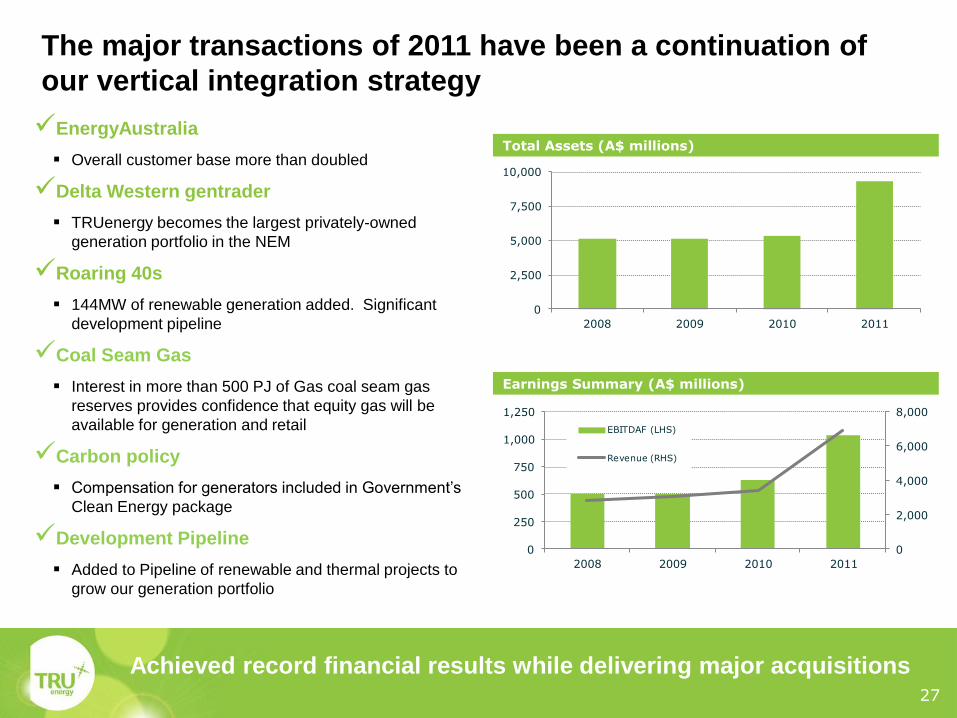

The major transactions of 2011 have been a continuation of

our vertical integration strategy

EnergyAustralia

Overall customer base more than doubled

Delta Western gentrader

TRUenergy becomes the largest privately-owned

generation portfolio in the NEM

Roaring 40s

144MW of renewable generation added. Significant

development pipeline

Coal Seam Gas

Interest in more than 500 PJ of Gas coal seam gas

reserves provides confidence that equity gas will be

available for generation and retail

Carbon policy

Compensation for generators included in Government’s

Clean Energy package

Development Pipeline

Added to Pipeline of renewable and thermal projects to

grow our generation portfolio

Total Assets (A$ millions)

Earnings Summary (A$ millions)

Achieved record financial results while delivering major acquisitions

0

2,500

5,000

7,500

10,000

2008 2009 2010 2011

0

2,000

4,000

6,000

8,000

0

250

500

750

1,000

1,250

2008 2009 2010 2011

EBITDAF (LHS)

Revenue (RHS)

Appendix

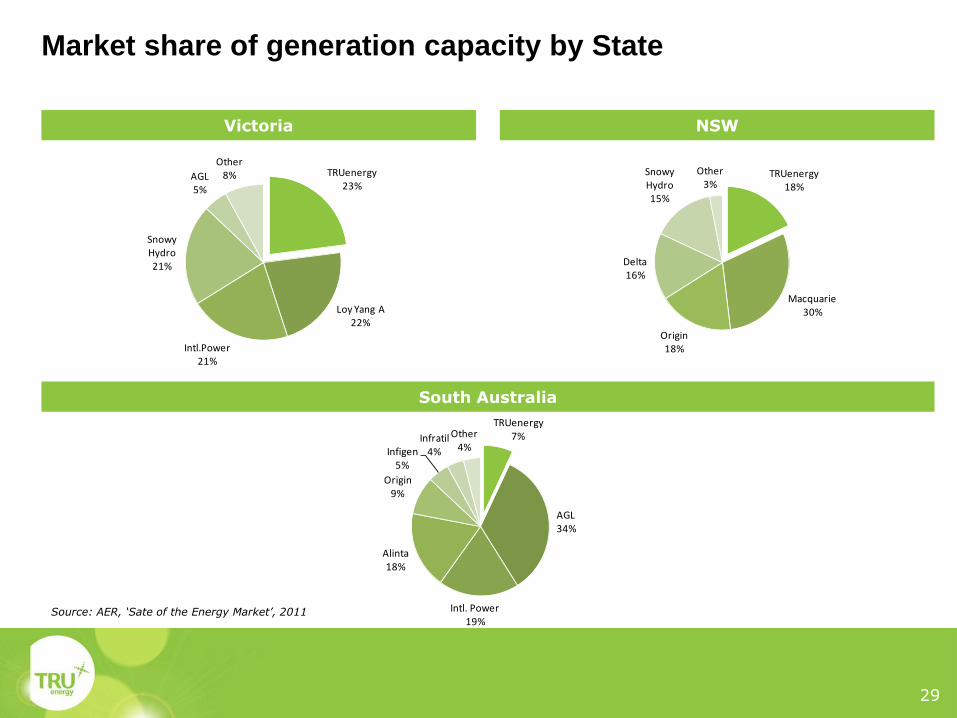

29

TRUenergy18%

Macquarie30%

Origin18%

Delta16%

Snowy Hydro15%

Other3%

TRUenergy23%

Loy Yang A22%

Intl.Power21%

Snowy Hydro21%

AGL5%

Other8%

Market share of generation capacity by State

Victoria NSW

South Australia

Source: AER, ‘Sate of the Energy Market’, 2011

TRUenergy7%

AGL34%

Intl. Power19%

Alinta18%

Origin9%

Infigen5%

Infratil4%

Other4%

30

Retail customer market share by fuel type

Source: AER, ‘State of the Energy Market’, 2011, p.103. Source: UBS

Electricity Gas

0%

25%

50%

75%

100%

VIC NSW SA QLD ACT

TRUenergy AGL Origin

ActewAGL Other - Private Other - Govt

0%

25%

50%

75%

100%

VIC NSW SA QLD ACT

TRUenergy AGL Origin

ActewAGL Other - Private Other - Govt

31

Portfolio helps to maximise returns in a volatile market

Source: TRUenergy Source: TRUenergy

Actual 2011 Volume (TWh) Actual 2011 Generation Capacity and

Retail Load (MW)

0

5

10

15

20

25

30

35

40

Long Short

Yallourn Delta West Other Contracts VIC NSW SA/QLD

0

2,000

4,000

6,000

8,000

Long ShortYallourn Delta Tallawarra Ecogen Hallett Swaps

Caps Vic NSW Qld SA

TRUenergy is effectively internally hedged

32

Merit order adjusted for carbon price

Portfolio of generation assets with strength in both geographic and fuel diversity

TRUenergy’s average weighted short run marginal cost to generate is slightly below the NEM weighted average

TRUenergy’s portfolio is lower than market average merit order with or without carbon

Excludes semi scheduled capacity (such as wind power) and hydro, which effectively has zero SRMC, and assumes fuel cost is held constant Brown coal (excl. Yallourn) generators highlighted in brown Source: TRUenergy modelling.

Halle

tt:

203M

W G

as

Jeera

lang

: 466M

W G

as

Talla

warr

a:

420M

W G

as

Mt

Pip

er:

1,4

00M

W B

lack C

oal

Walle

raw

ang: 1,0

00M

W B

lack C

oal

Yallo

urn

: 1,4

80M

W B

row

n C

oal

0 10,000 15,000 20,000

460

25,000 30,000 35,000

0

20

40

5,000

80

100

120

400

420

140

New

port

: 500M

W G

as

60

2010 Indicative Merit Order ($23/t Carbon)

SRM

C (

$/M

Wh)

Indicative capacity (MW)

33

Disclaimer

This presentation may contain forward looking statements and comments about future events, including our expectations about the performance of TRUenergy Group's business. Such comments are not audited and are based on a number of factors that we cannot control and so no representation or warranty is provided by or on behalf of TRUenergy or CLP that they should or will be achieved. We cannot be certain that the comments will be accurate or complete and so they should not be relied on.

Please note that, in providing this presentation, TRUenergy has not considered the objectives, financial position or needs of any particular recipient.