Investor Day 2015 -

59

Aspen Technology, Inc. Investor Day Antonio Pietri – President and Chief Executive Officer May 4 th , 2015

-

Upload

jason-want -

Category

Documents

-

view

102 -

download

1

Transcript of Investor Day 2015 -

Aspen Technology, Inc. Investor Day Antonio Pietri – President and Chief Executive Officer

May 4th, 2015

© 2015 Aspen Technology, Inc. All rights reserved 2

Safe Harbor Statement

These slides may contain forward-looking statements for purposes of the safe harbor

provisions of the Private Securities Litigation Reform Act of 1995. Actual results may vary

significantly from AspenTech’s expectations based on a number of risks and uncertainties,

including, without limitation, the risk factors described in AspenTech’s most recent Annual

Report on Form 10-K and any subsequent quarterly reports on Form 10Q, each as filed with

the U.S. Securities and Exchange Commission. AspenTech cannot guarantee any future

results, levels of activity, performance, or achievements. Further, AspenTech expressly

disclaims any current intention to update any forward-looking statements after the date hereof.

© 2015 Aspen Technology, Inc. All rights reserved 3

Key Highlights

Multi-Billion Dollar TLCV Opportunity

Market Leadership Position

World-Class Customer Base with Significant Upsell Opportunities

Subscription Model with Long-Term Contracts

Best-in-Class Profitability and

Cash Flow Generation

Focus on Driving Shareholder Value

© 2015 Aspen Technology, Inc. All rights reserved 4

Global Market

Industry characteristics

• $10 trillion global industries

• Complex manufacturing processes

• High capital costs

• High volume production

• Engineering and technology

Energy Chemicals Engineering & Construction

© 2015 Aspen Technology, Inc. All rights reserved 5

• Globalization

• Volatility

• Changing demographics

Energy Chemicals Engineering & Construction

• Environmental regulations

• Safety regulations

• Focus on operational excellence

Industry Dynamics

© 2015 Aspen Technology, Inc. All rights reserved 6

Industry Competitive Dynamics

Energy

• Upstream CAPEX: utilizing capital efficiently

• Refining capacity: supply chain challenges

• North American tight oil production

• Alternative fuels

• Disruptive dynamics: shale gas

• New capacity plans in North America

• Integrated refinery-chemical complexes

• Specialty chemicals

Chemicals

• Refinery and Chemical plant expansion/retooling

• Growth in LNG to support global carbon emission reductions

• Need to manage projects globally

• Productivity drivers

Engineering & Construction

© 2015 Aspen Technology, Inc. All rights reserved 7

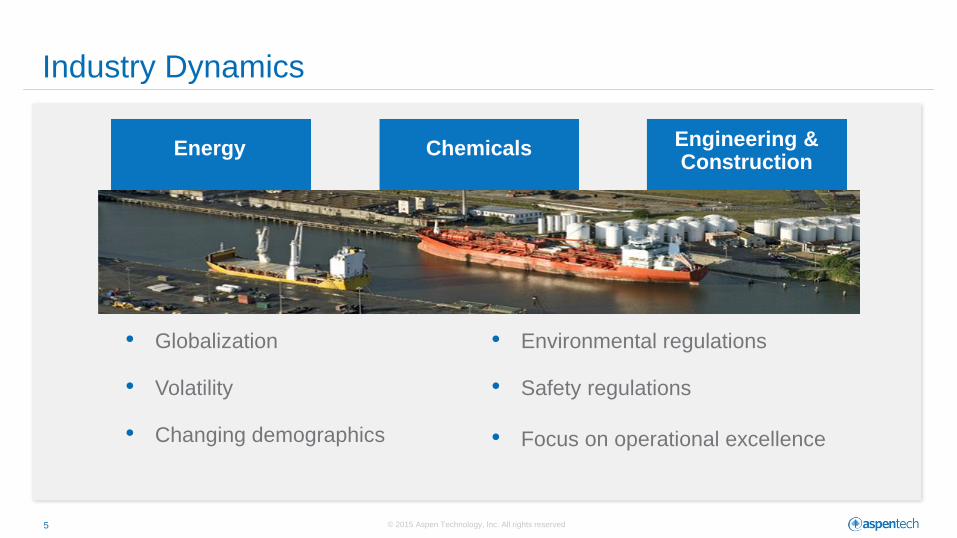

Oil Price Volatility

11.7%

14.5%

13.0% 12.2%

11.3%

12.8% 13.2%

12.7%

11.1% 12.3%

11.2%

12.3% 11.9%

112.48

$97.80 $102.16

$112.36

$94.67

$57.33 $56.21

FY '11 FY '12 FY '13 FY14 Q1 FY15 Q2 FY15 Q3 FY15

GTLCV YoY % AS YoY Growth % Brent Crude Oil $(1)

(1) Not available in FY’11

© 2015 Aspen Technology, Inc. All rights reserved 8

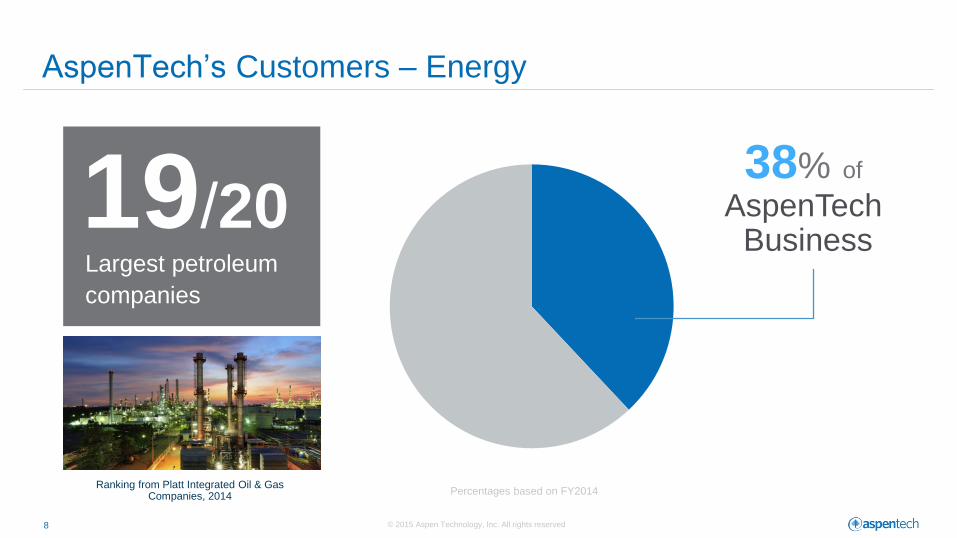

AspenTech’s Customers – Energy

38% of

AspenTech Business

Ranking from Platt Integrated Oil & Gas

Companies, 2014

Largest petroleum

companies

19/20

Percentages based on FY2014

© 2015 Aspen Technology, Inc. All rights reserved 9

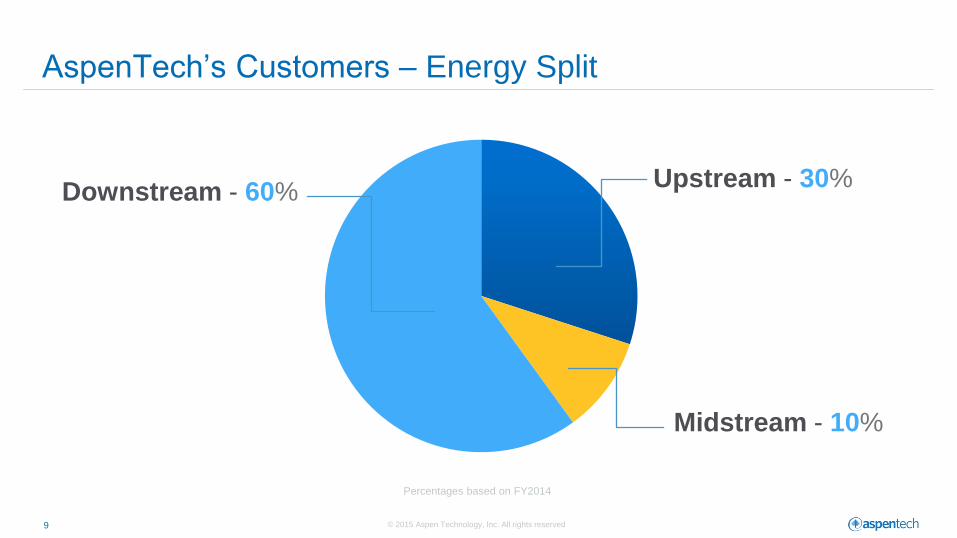

AspenTech’s Customers – Energy Split

Percentages based on FY2014

Downstream - 60%

Midstream - 10%

Upstream - 30%

© 2015 Aspen Technology, Inc. All rights reserved 10

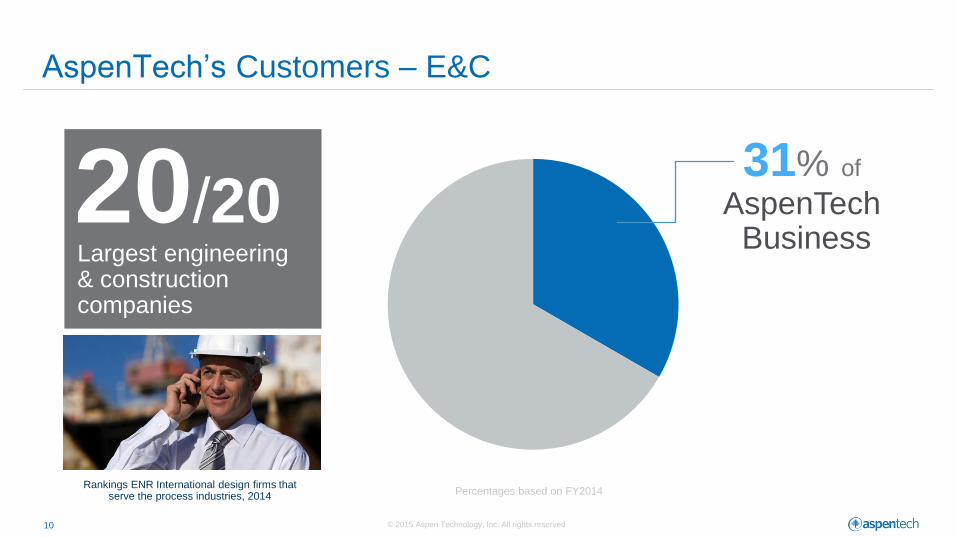

AspenTech’s Customers – E&C

31% of

AspenTech Business

20/20 Largest engineering & construction companies

Rankings ENR International design firms that

serve the process industries, 2014

Percentages based on FY2014

© 2015 Aspen Technology, Inc. All rights reserved 11

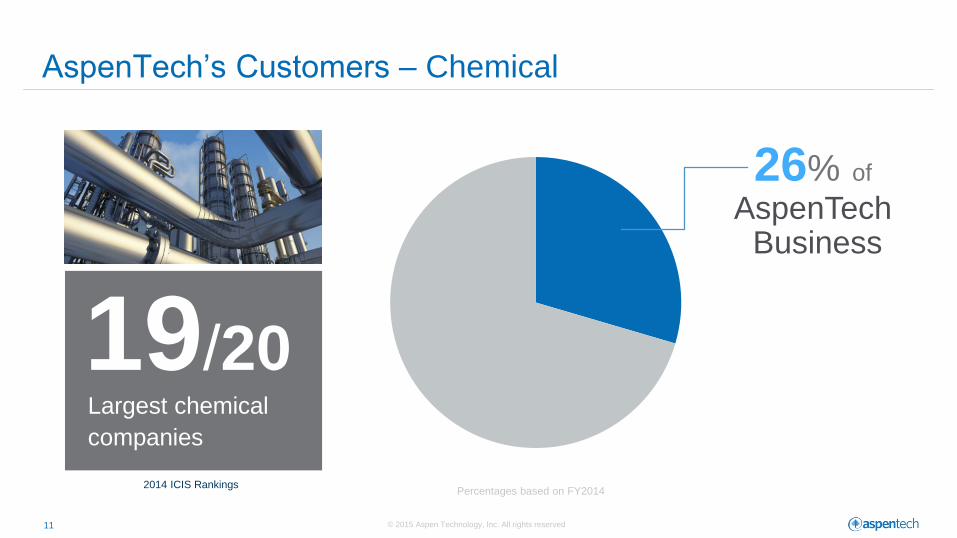

AspenTech’s Customers – Chemical

26% of

AspenTech Business

Largest chemical

companies

19/20

2014 ICIS Rankings

Percentages based on FY2014

© 2015 Aspen Technology, Inc. All rights reserved 12

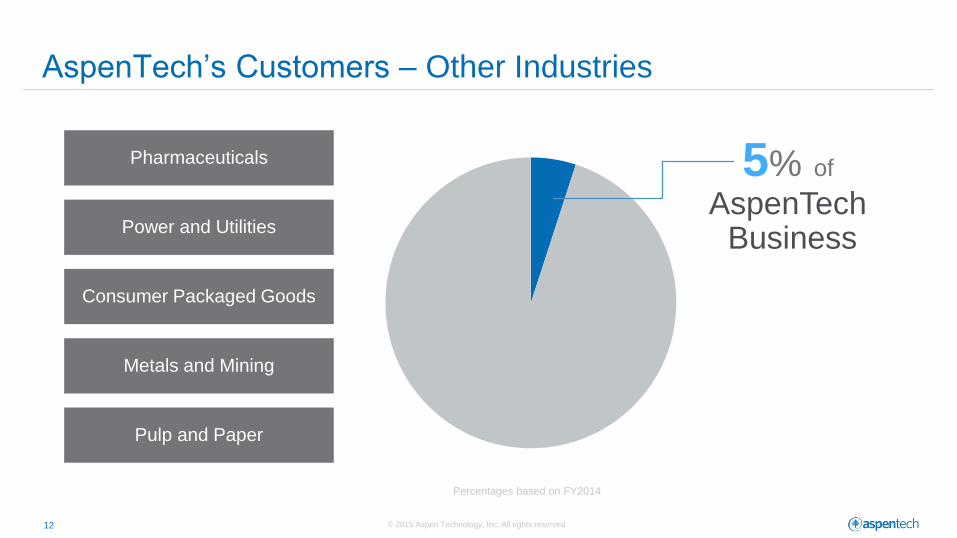

Pharmaceuticals

AspenTech’s Customers – Other Industries

5% of

AspenTech Business

Percentages based on FY2014

Power and Utilities

Consumer Packaged Goods

Metals and Mining

Pulp and Paper

© 2015 Aspen Technology, Inc. All rights reserved 13

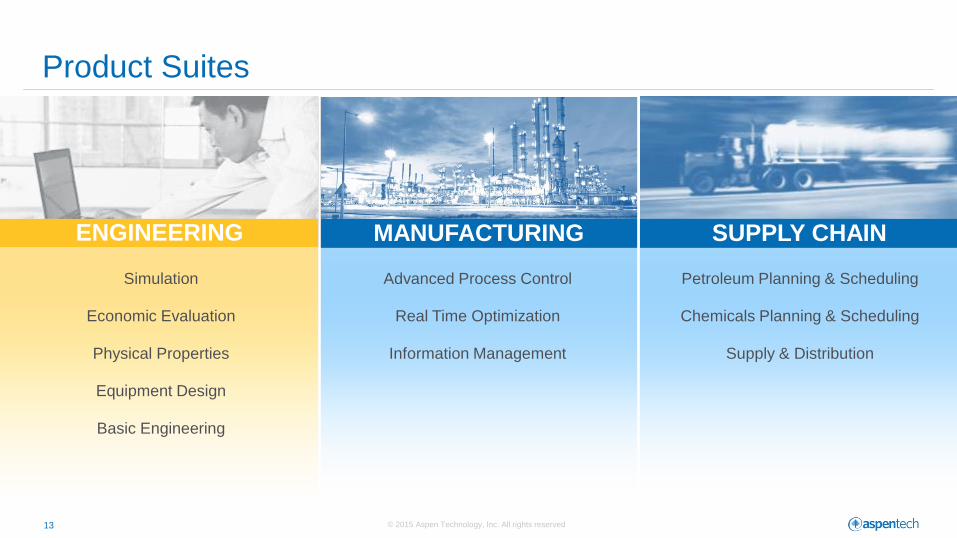

Product Suites

ENGINEERING MANUFACTURING SUPPLY CHAIN

Simulation

Economic Evaluation

Physical Properties

Equipment Design

Basic Engineering

Advanced Process Control

Real Time Optimization

Information Management

Petroleum Planning & Scheduling

Chemicals Planning & Scheduling

Supply & Distribution

© 2015 Aspen Technology, Inc. All rights reserved 14

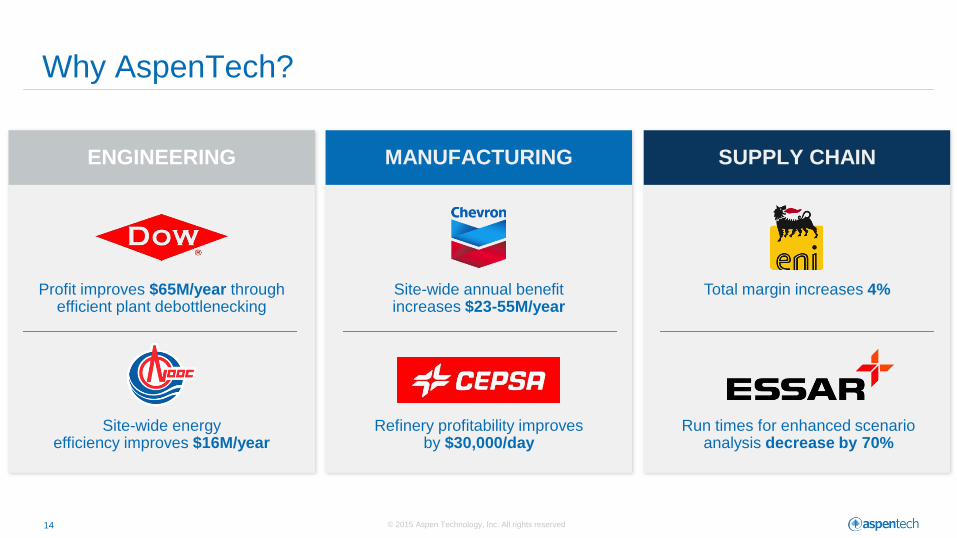

Why AspenTech?

ENGINEERING

Profit improves $65M/year through efficient plant debottlenecking

Site-wide energy efficiency improves $16M/year

MANUFACTURING

Refinery profitability improves by $30,000/day

Site-wide annual benefit increases $23-55M/year

SUPPLY CHAIN

Total margin increases 4%

Run times for enhanced scenario analysis decrease by 70%

© 2015 Aspen Technology, Inc. All rights reserved 15

Why is AspenTech Unique?

• #1 global provider of optimization software

solutions for the process industries

– Vertical focus

– Deep domain knowledge and expertise on

hydrocarbon processes

– Large return on investment

– Mission critical solutions

• Solve complex optimization problems

• Breadth of solutions

• Track record of innovation

• Singular focus on software

© 2015 Aspen Technology, Inc. All rights reserved 16

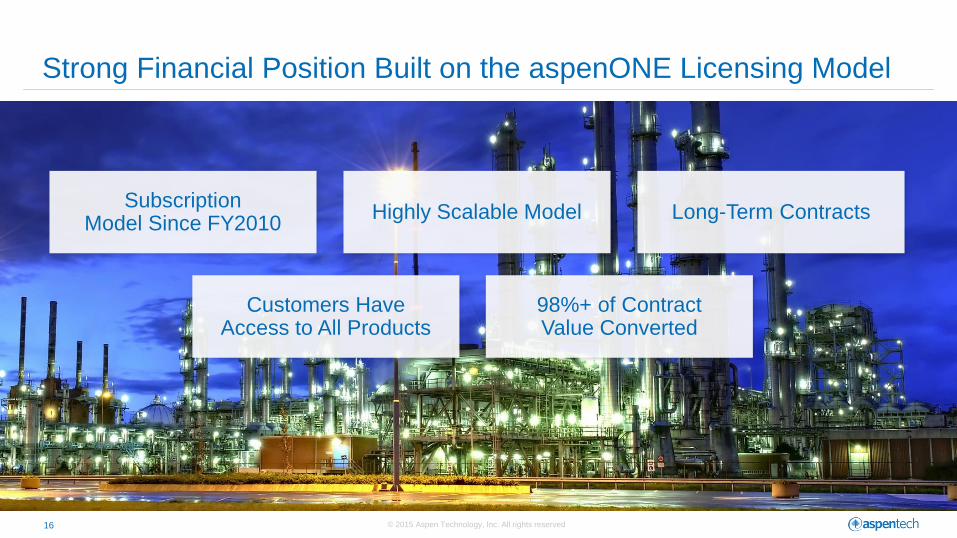

Strong Financial Position Built on the aspenONE Licensing Model

Subscription Model Since FY2010

Highly Scalable Model Long-Term Contracts

Customers Have Access to All Products

98%+ of Contract Value Converted

© 2015 Aspen Technology, Inc. All rights reserved 17

Growth Strategy

Usage and Product Adoption

© 2015 Aspen Technology, Inc. All rights reserved 18

Usage and Product Adoption Strategy

Invest in High Growth Markets

Pursue Acquisitions

Product Innovation

Scale through Digital

Channels

Expand Total Addressable Market

Penetrate Customer

Base

© 2015 Aspen Technology, Inc. All rights reserved 19

Product Innovation

Access Anywhere/ Anytime

Faster and Easier Implementation

Automation of Knowledge Work

Breakthrough Innovation

Intuitive User Experience

© 2015 Aspen Technology, Inc. All rights reserved 20

Penetrate Customer Base

© 2015 Aspen Technology, Inc. All rights reserved 21

• China

• Latin America

• Middle East

• Russia

• Inside Sales (SMB)

– High productivity

– New customers

Invest in High Growth Markets

© 2015 Aspen Technology, Inc. All rights reserved 22

Webinars

Community

Blog Article Content

Discussion Forum Content

Resource Library Content

• Hundreds of Thousands of Users

– Variety of skills, experience and business needs

• Need to Distribute Education and Support

Content to Key Segments and Users

– Map and deliver targeted messages to each

segment and users

• Digital Channel Solutions are Scalable and

Cost Effective

– Especially among global base of customers

• Technology Trends Require Multi-Channel

Access

– Mobility and Collaboration

Deploying a Comprehensive Digital Strategy

Social Media

Website

© 2015 Aspen Technology, Inc. All rights reserved. 23

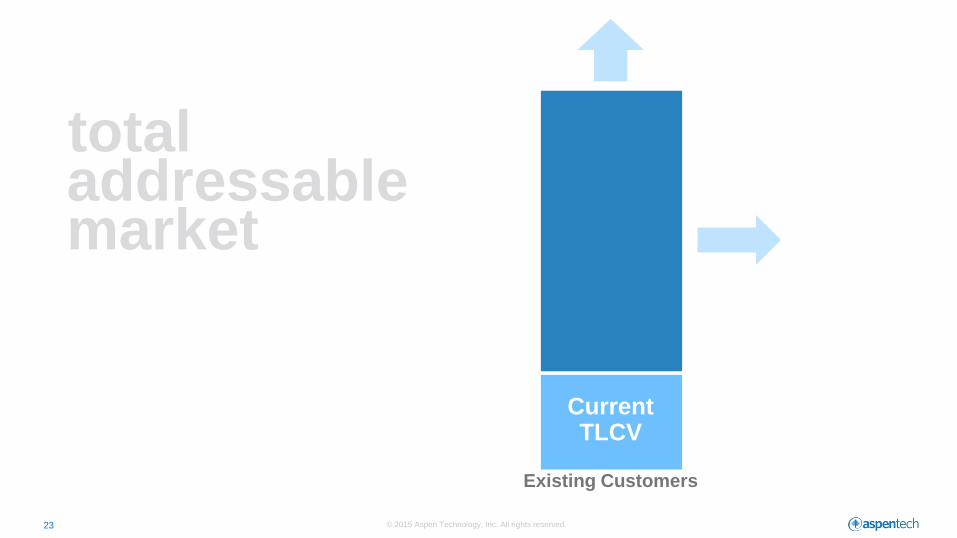

market addressable total

Existing Customers

Current TLCV

© 2015 Aspen Technology, Inc. All rights reserved 24

Acquisitions

• An effective way to drive shareholder

value

– Five small tuck-in acquisitions since

February 2012

• Buy versus make decision

• Growth and profitability a

key consideration

• Continuously evaluating

opportunities

© 2015 Aspen Technology, Inc. All rights reserved. 25

Total Addressable Market

© 2015 Aspen Technology, Inc. All rights reserved 26

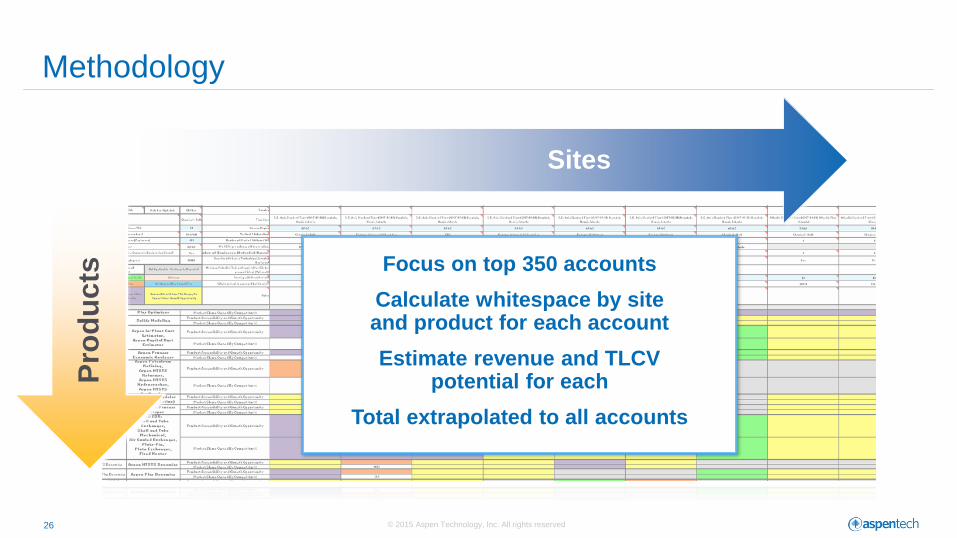

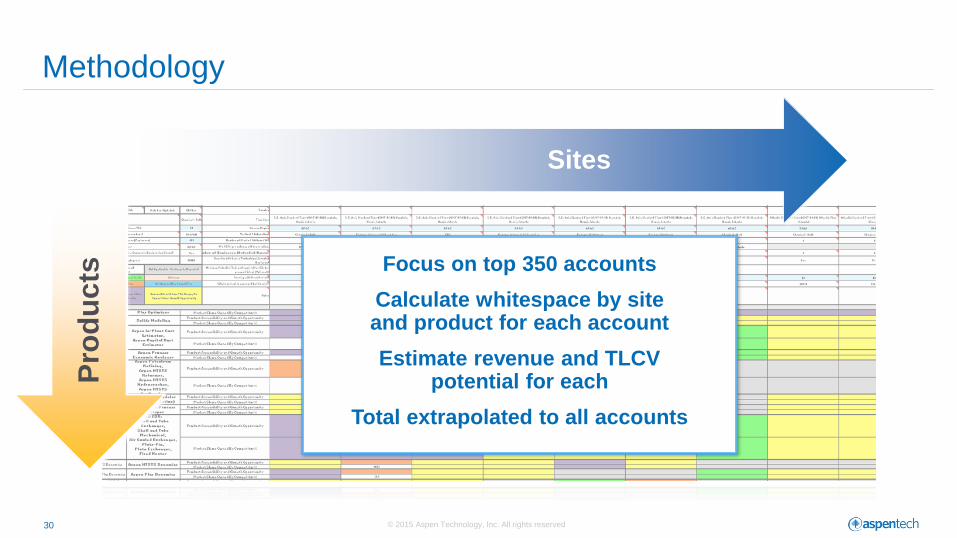

Methodology P

rod

uc

ts

Sites

Focus on top 350 accounts

Calculate whitespace by site and product for each account

Estimate revenue and TLCV potential for each

Total extrapolated to all accounts

© 2015 Aspen Technology, Inc. All rights reserved 27

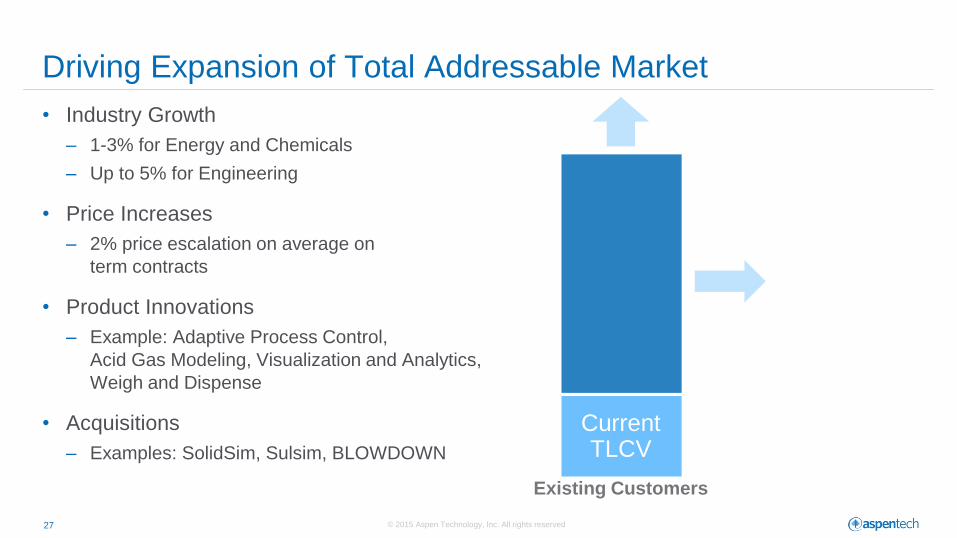

• Industry Growth

– 1-3% for Energy and Chemicals

– Up to 5% for Engineering

• Price Increases

– 2% price escalation on average on

term contracts

• Product Innovations

– Example: Adaptive Process Control,

Acid Gas Modeling, Visualization and Analytics,

Weigh and Dispense

• Acquisitions

– Examples: SolidSim, Sulsim, BLOWDOWN

Driving Expansion of Total Addressable Market

Existing Customers

Current TLCV

© 2015 Aspen Technology, Inc. All rights reserved 28

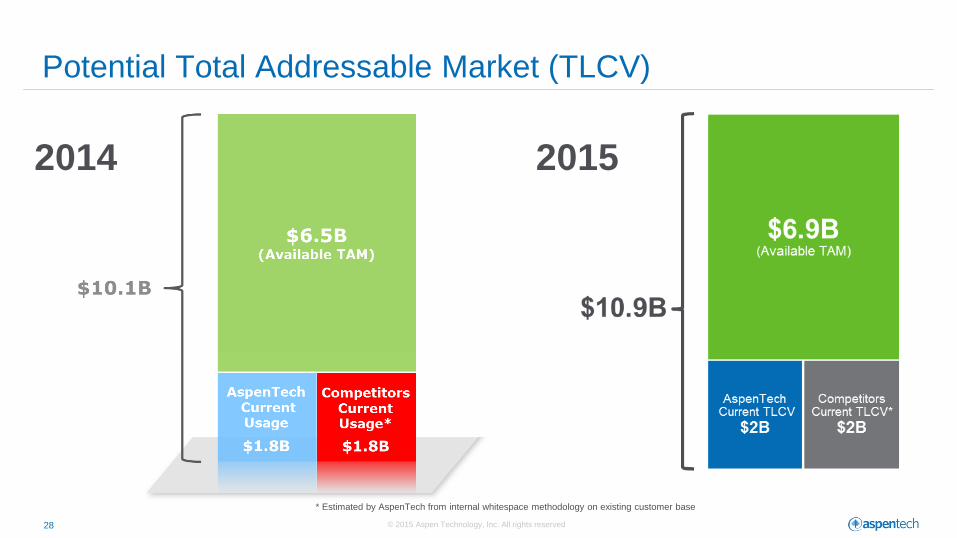

* Estimated by AspenTech from internal whitespace methodology on existing customer base

Potential Total Addressable Market (TLCV)

2014 2015

© 2015 Aspen Technology, Inc. All rights reserved 29

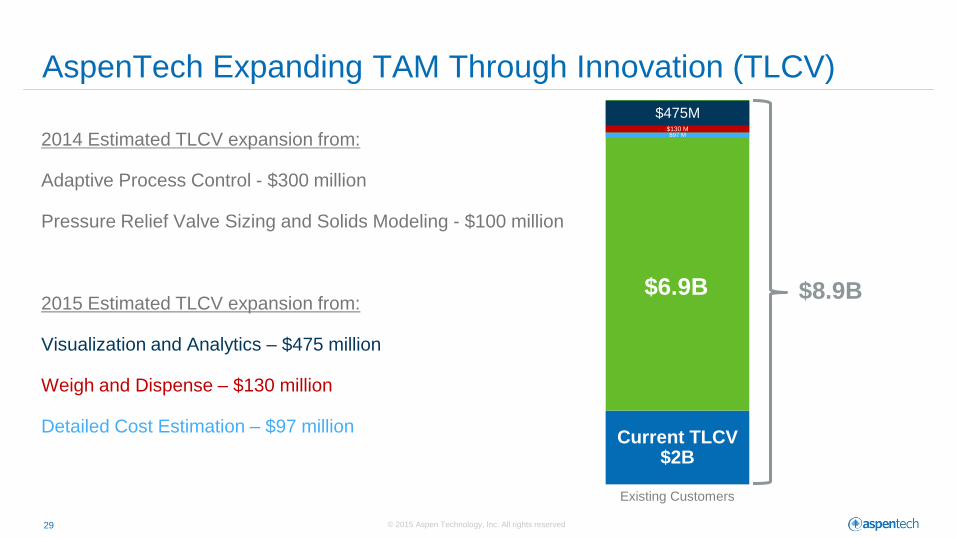

Existing Customers

Current TLCV $2B

$97 M $130 M

$6.9B $8.9B

AspenTech Expanding TAM Through Innovation (TLCV)

2014 Estimated TLCV expansion from:

Adaptive Process Control - $300 million

Pressure Relief Valve Sizing and Solids Modeling - $100 million

2015 Estimated TLCV expansion from:

Visualization and Analytics – $475 million

Weigh and Dispense – $130 million

Detailed Cost Estimation – $97 million

$475M

© 2015 Aspen Technology, Inc. All rights reserved 30

Methodology P

rod

uc

ts

Sites

Focus on top 350 accounts

Calculate whitespace by site and product for each account

Estimate revenue and TLCV potential for each

Total extrapolated to all accounts

© 2015 Aspen Technology, Inc. All rights reserved 31

Investment Allocation that Supports Growth

• Sales organization

– SMB organization

– Russia

– MENA

– China

• Marketing

– Digital channel

– User segmentation

– Market research

• Research and Development

• Acquisitions

© 2015 Aspen Technology, Inc. All rights reserved 32

Focus on Execution

Multi-Billion Dollar TLCV Opportunity

Market Leadership Position

World-Class Customer Base with Significant Upsell Opportunities

Subscription Model with Long-Term Contracts

Best-in-Class Profitability and

Cash Flow Generation

Focus on Driving Shareholder Value

Thank you

Aspen Technology, Inc. Investor Day Mark Sullivan – Chief Financial Officer

May 4th, 2015

© 2015 Aspen Technology, Inc. All rights reserved 35

Financial Highlights

• Multi-year history of delivering solid growth in license subscription contracts

• Substantial market white space opportunity

• Best in class profitability and cash flow profile

• Consistently returning capital to shareholders via share repurchases

• In final year of transition to subscription revenue model

• Strong YTD FY 2015 performance and solid outlook for FY 2015 and FY 2016

© 2015 Aspen Technology, Inc. All rights reserved 36

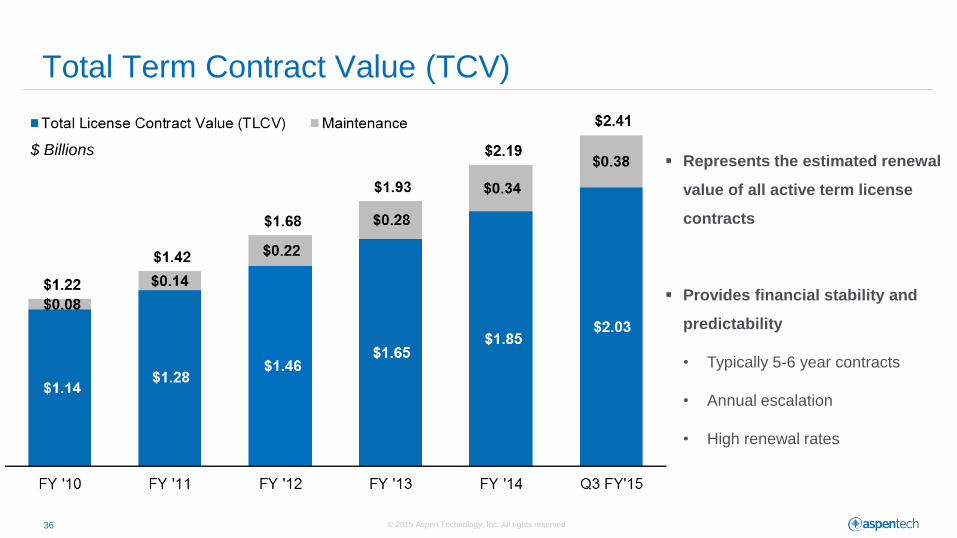

Total Term Contract Value (TCV)

$ Billions Represents the estimated renewal

value of all active term license

contracts

Provides financial stability and

predictability

• Typically 5-6 year contracts

• Annual escalation

• High renewal rates

© 2015 Aspen Technology, Inc. All rights reserved 37

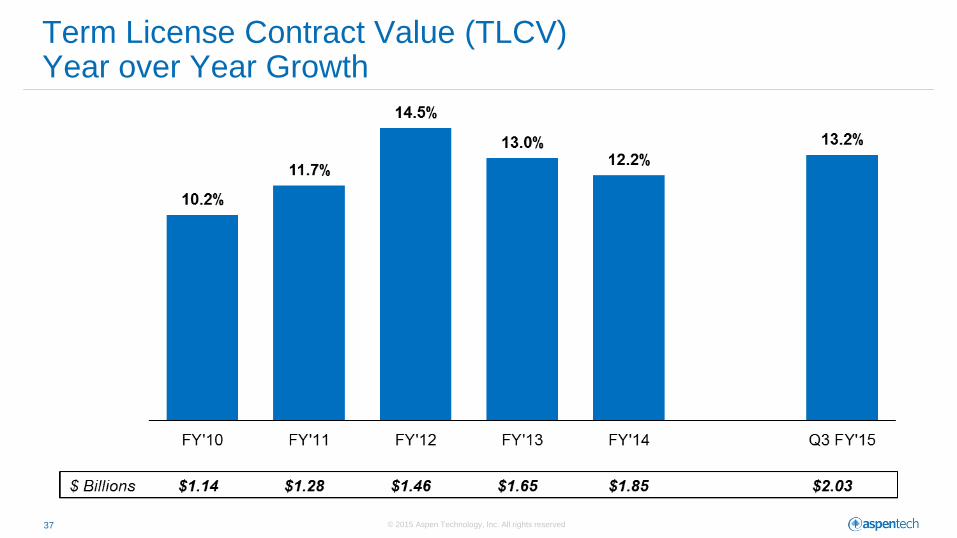

Term License Contract Value (TLCV) Year over Year Growth

© 2015 Aspen Technology, Inc. All rights reserved 38

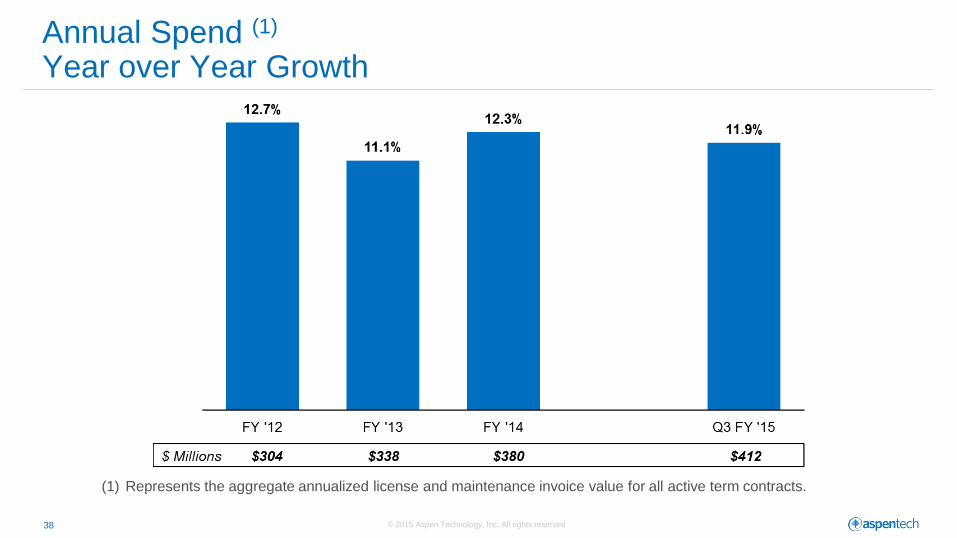

Annual Spend (1) Year over Year Growth

(1) Represents the aggregate annualized license and maintenance invoice value for all active term contracts.

© 2015 Aspen Technology, Inc. All rights reserved 39

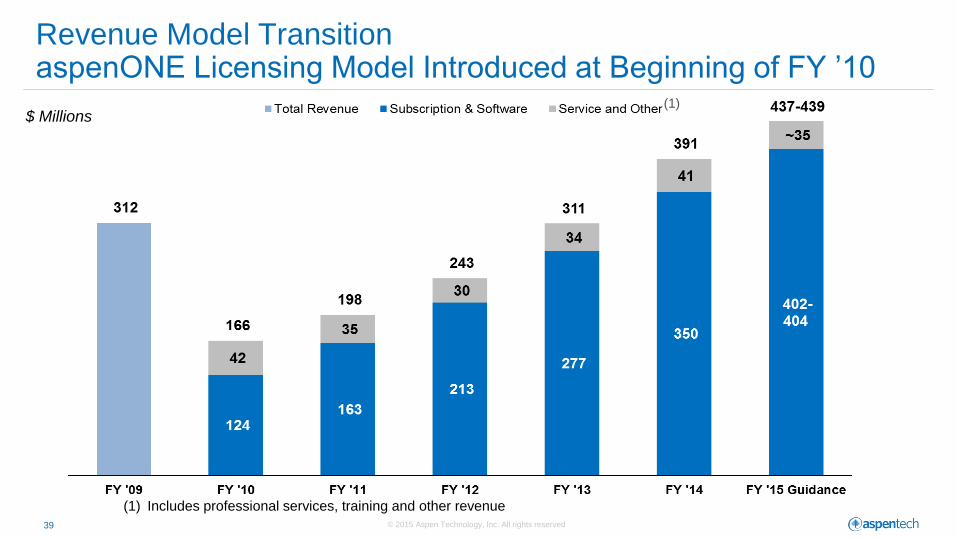

Revenue Model Transition aspenONE Licensing Model Introduced at Beginning of FY ’10

(1) Includes professional services, training and other revenue

$ Millions (1)

© 2015 Aspen Technology, Inc. All rights reserved 40

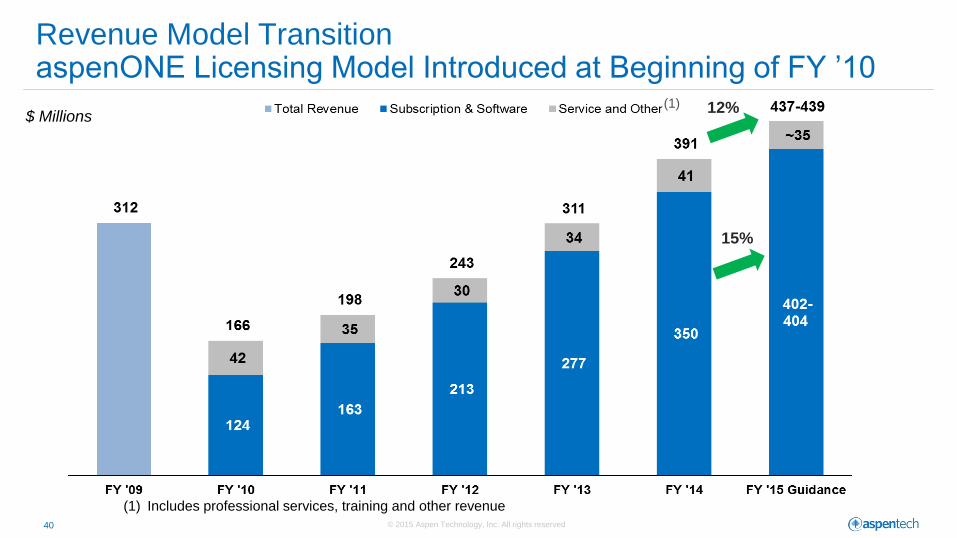

Revenue Model Transition aspenONE Licensing Model Introduced at Beginning of FY ’10

(1) Includes professional services, training and other revenue

$ Millions (1) 12%

15%

© 2015 Aspen Technology, Inc. All rights reserved 41

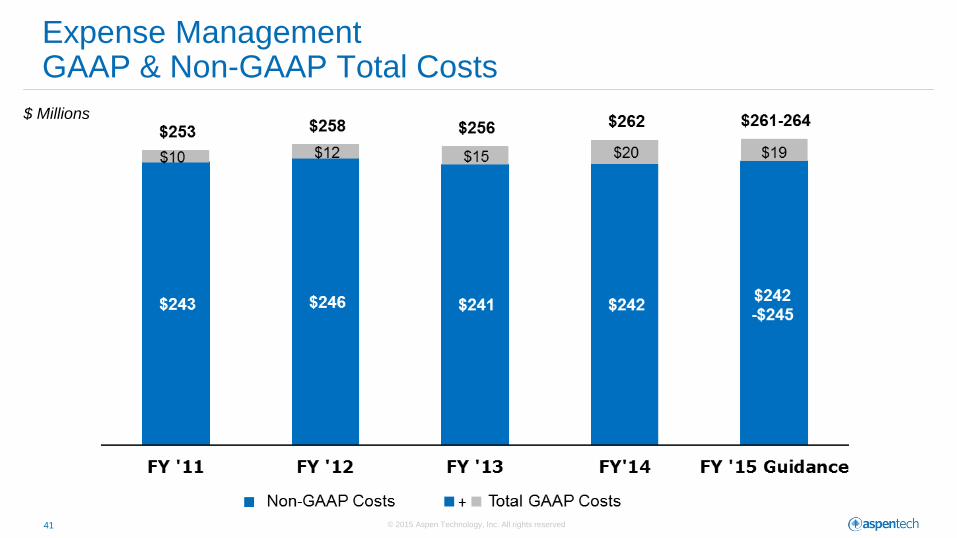

Expense Management GAAP & Non-GAAP Total Costs

$ Millions

© 2015 Aspen Technology, Inc. All rights reserved 42

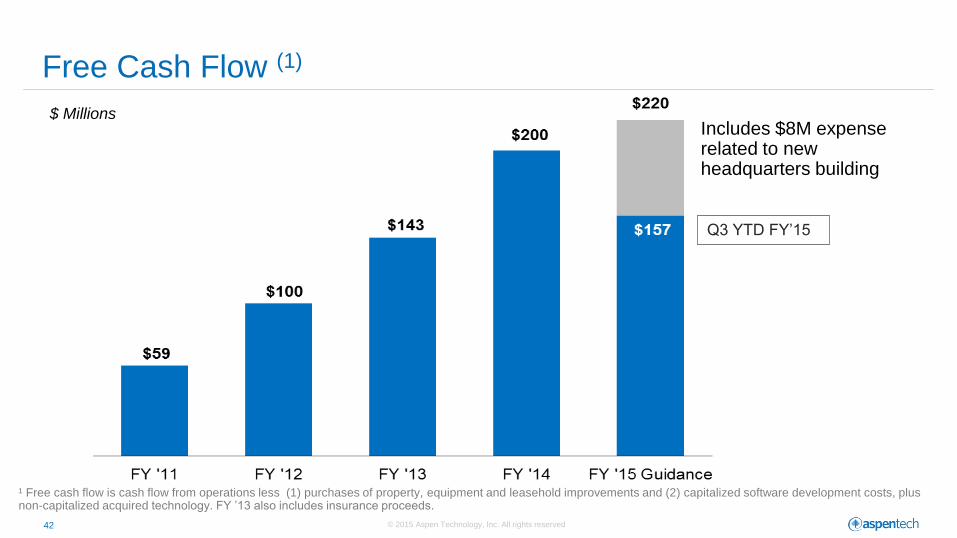

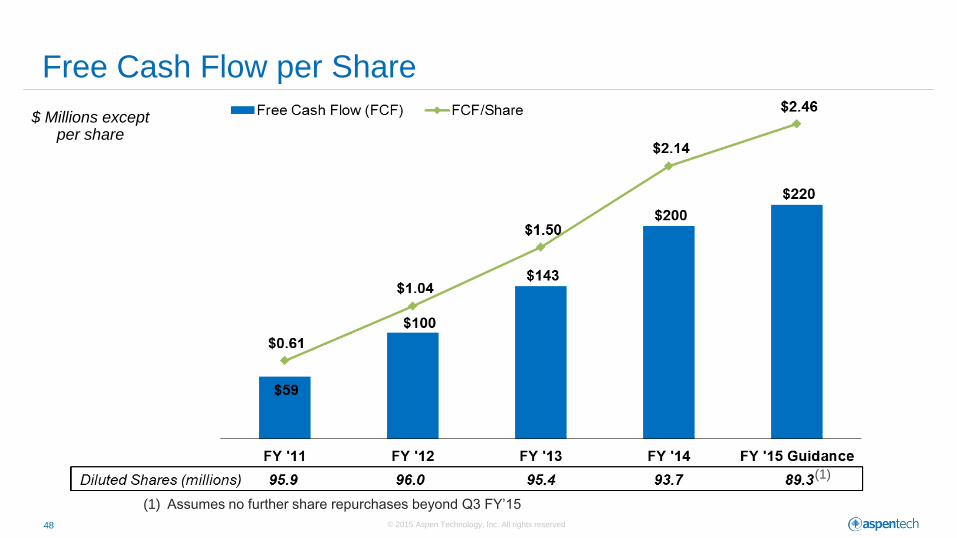

Free Cash Flow (1)

Q3 YTD FY’15

$ Millions Includes $8M expense related to new headquarters building

¹ Free cash flow is cash flow from operations less (1) purchases of property, equipment and leasehold improvements and (2) capitalized software development costs, plus non-capitalized acquired technology. FY ’13 also includes insurance proceeds.

© 2015 Aspen Technology, Inc. All rights reserved 43

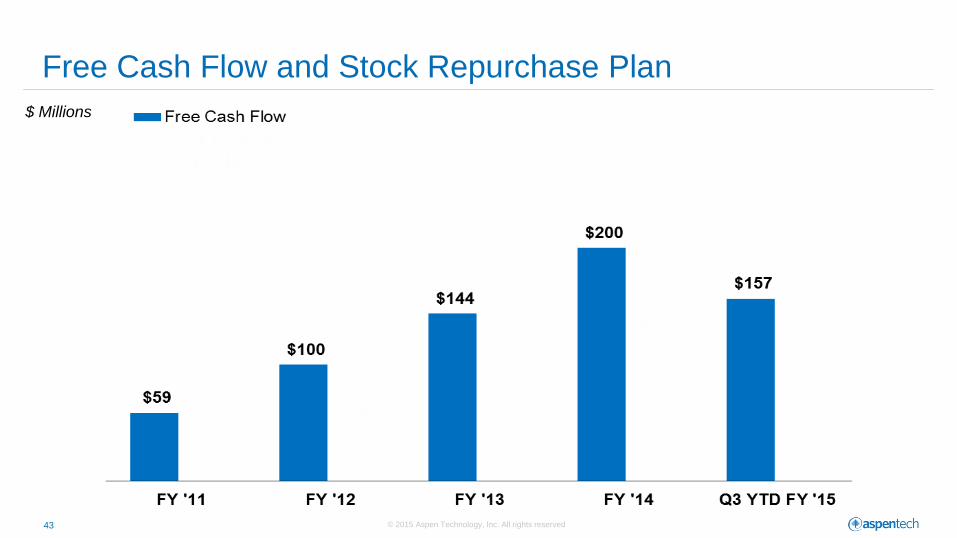

Free Cash Flow and Stock Repurchase Plan

$ Millions

© 2015 Aspen Technology, Inc. All rights reserved 44

$ Millions

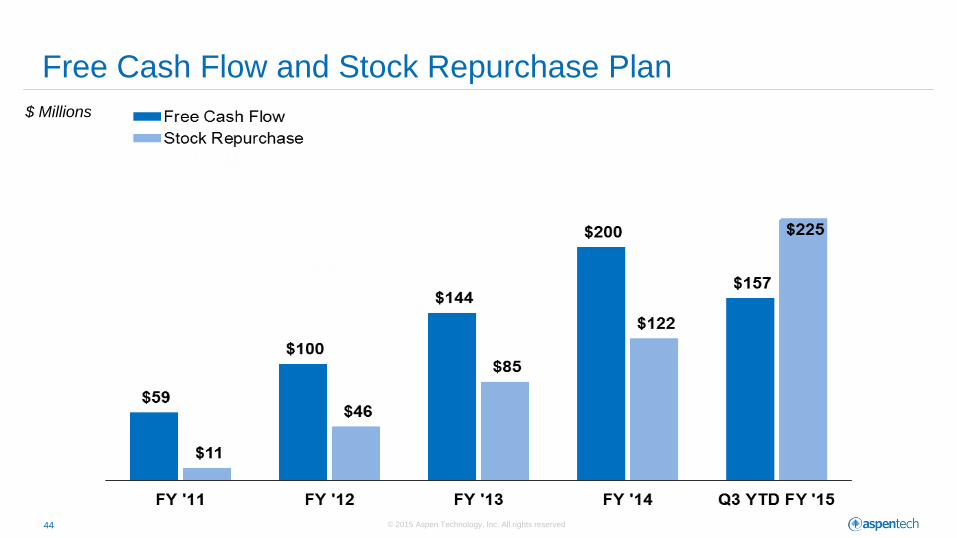

Free Cash Flow and Stock Repurchase Plan

© 2015 Aspen Technology, Inc. All rights reserved 45

$ Millions

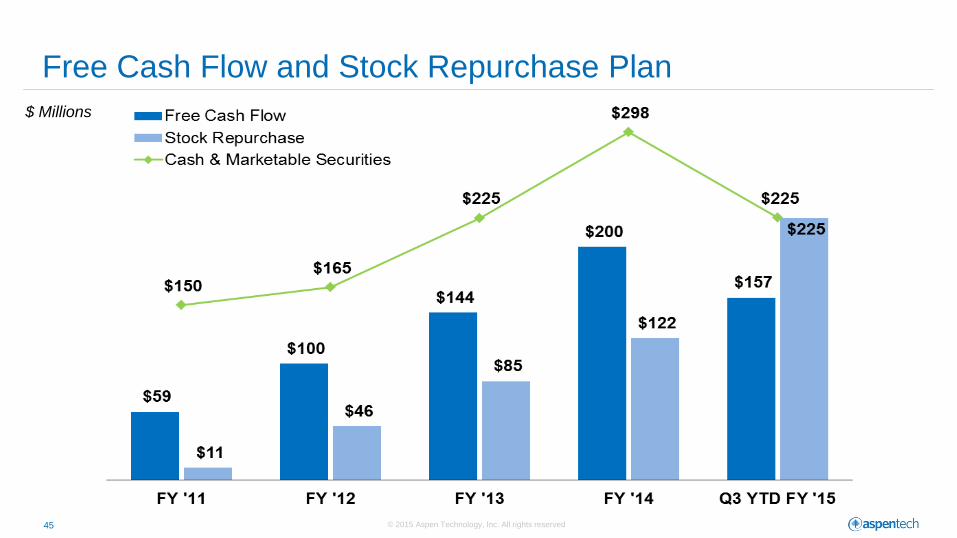

Free Cash Flow and Stock Repurchase Plan

© 2015 Aspen Technology, Inc. All rights reserved 46

Cumulative Amount Purchased: $488M

Cumulative Shares Purchased: 15.4M

Average cost: $31.77/share

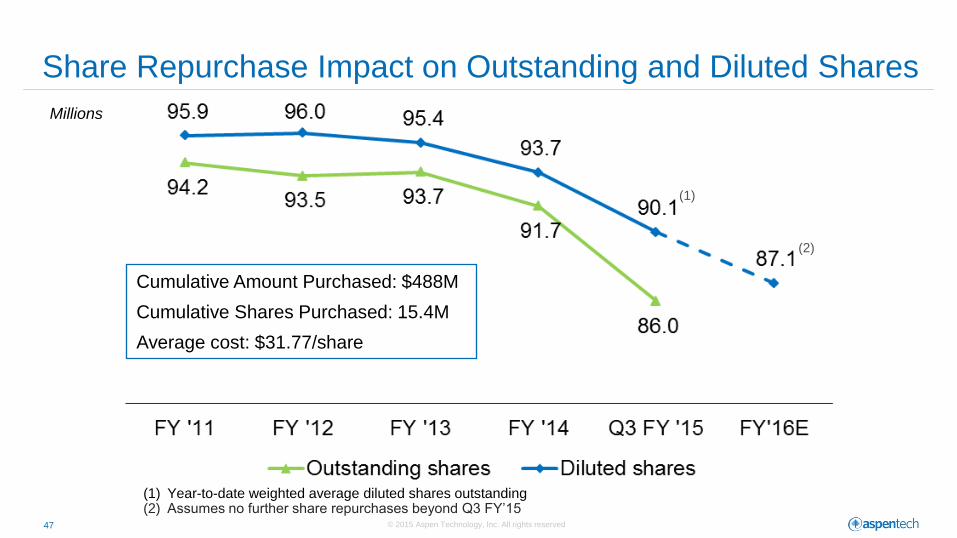

Share Repurchase Impact on Outstanding and Diluted Shares

© 2015 Aspen Technology, Inc. All rights reserved 47

Share Repurchase Impact on Outstanding and Diluted Shares

Millions

Cumulative Amount Purchased: $488M

Cumulative Shares Purchased: 15.4M

Average cost: $31.77/share

(1) Year-to-date weighted average diluted shares outstanding (2) Assumes no further share repurchases beyond Q3 FY’15

(2)

(1)

© 2015 Aspen Technology, Inc. All rights reserved 48

Free Cash Flow per Share

$ Millions except per share

(1) Assumes no further share repurchases beyond Q3 FY’15

(1)

© 2015 Aspen Technology, Inc. All rights reserved 49

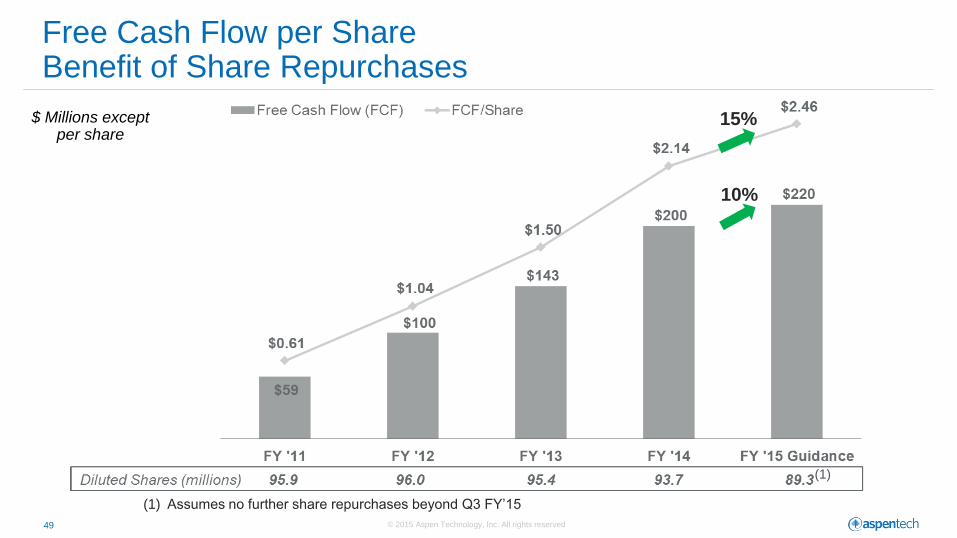

Free Cash Flow per Share Benefit of Share Repurchases

$ Millions except per share

10%

15%

(1) Assumes no further share repurchases beyond Q3 FY’15

(1)

© 2015 Aspen Technology, Inc. All rights reserved 50

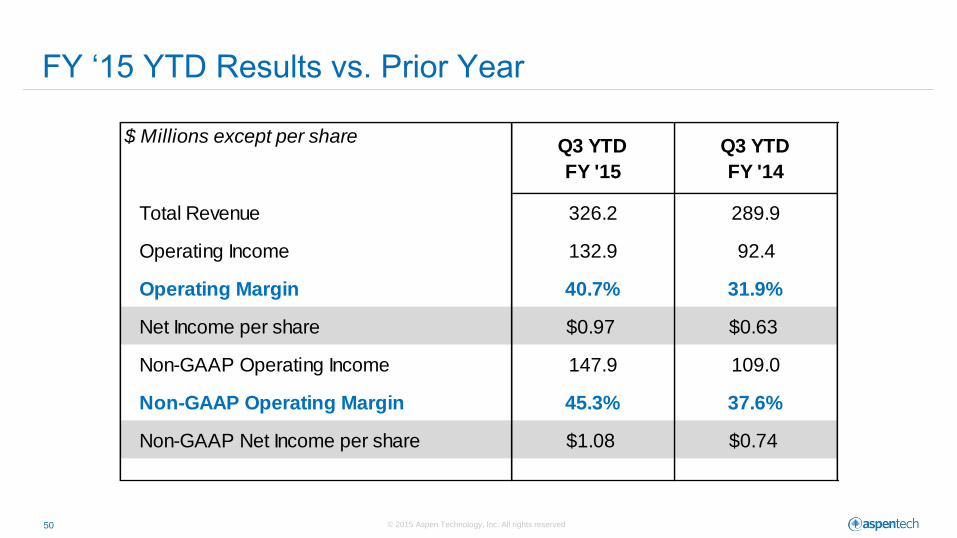

FY ‘15 YTD Results vs. Prior Year

$ Millions except per shareQ3 YTD

FY '15

Q3 YTD

FY '14

Total Revenue 326.2 289.9

Operating Income 132.9 92.4

Operating Margin 40.7% 31.9%

Net Income per share $0.97 $0.63

Non-GAAP Operating Income 147.9 109.0

Non-GAAP Operating Margin 45.3% 37.6%

Non-GAAP Net Income per share $1.08 $0.74

© 2015 Aspen Technology, Inc. All rights reserved. 51

FY 2016 Guidance

© 2015 Aspen Technology, Inc. All rights reserved 52

Non-GAAP Metrics We Will Provide in FY ’16

• Annual Spend: growth guidance and quarterly results

• TLCV/TCV on milestone basis or at year-end

• Non-GAAP P&L metrics

• Free Cash Flow guidance

© 2015 Aspen Technology, Inc. All rights reserved 53

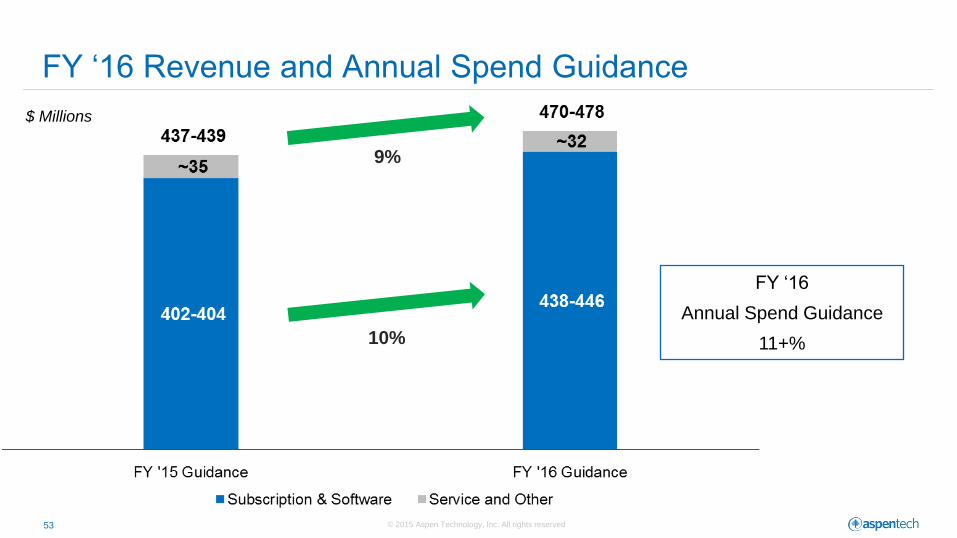

FY ‘16 Revenue and Annual Spend Guidance

$ Millions

10%

9%

FY ‘16

Annual Spend Guidance

11+%

© 2015 Aspen Technology, Inc. All rights reserved 54

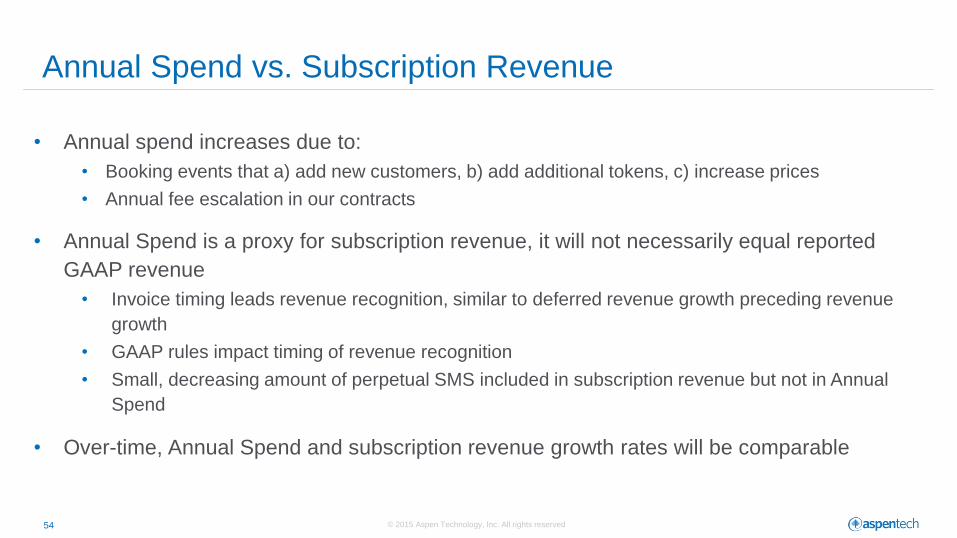

Annual Spend vs. Subscription Revenue

• Annual spend increases due to:

• Booking events that a) add new customers, b) add additional tokens, c) increase prices

• Annual fee escalation in our contracts

• Annual Spend is a proxy for subscription revenue, it will not necessarily equal reported

GAAP revenue

• Invoice timing leads revenue recognition, similar to deferred revenue growth preceding revenue

growth

• GAAP rules impact timing of revenue recognition

• Small, decreasing amount of perpetual SMS included in subscription revenue but not in Annual

Spend

• Over-time, Annual Spend and subscription revenue growth rates will be comparable

© 2015 Aspen Technology, Inc. All rights reserved 55

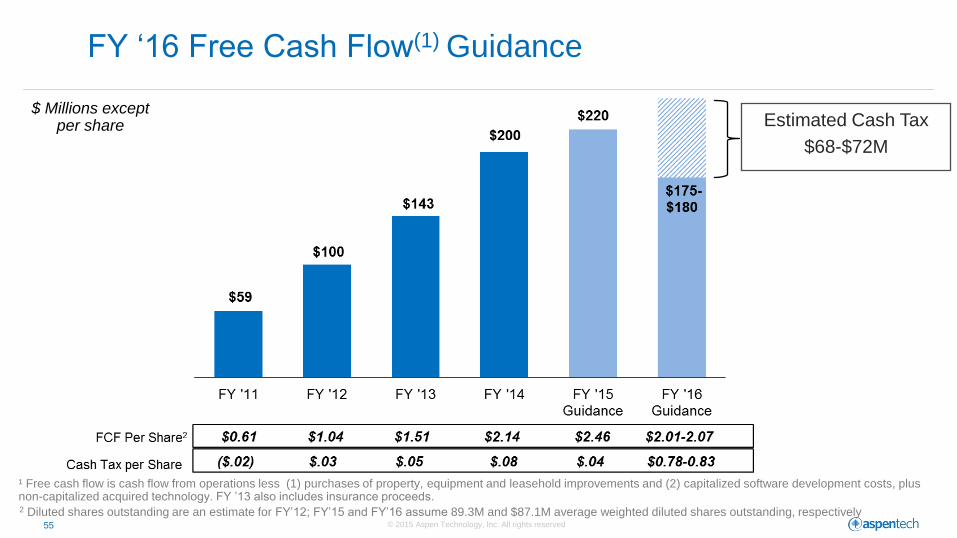

Estimated Cash Tax

$68-$72M

FY ‘16 Free Cash Flow(1) Guidance

¹ Free cash flow is cash flow from operations less (1) purchases of property, equipment and leasehold improvements and (2) capitalized software development costs, plus non-capitalized acquired technology. FY ’13 also includes insurance proceeds. 2 Diluted shares outstanding are an estimate for FY’12; FY’15 and FY’16 assume 89.3M and $87.1M average weighted diluted shares outstanding, respectively

$ Millions except per share

© 2015 Aspen Technology, Inc. All rights reserved 56

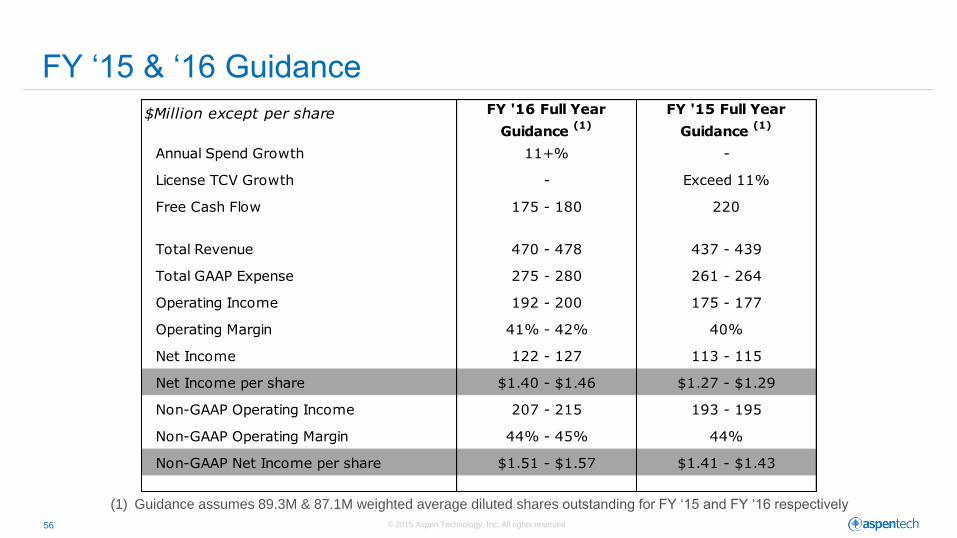

FY ‘15 & ‘16 Guidance

(1) Guidance assumes 89.3M & 87.1M weighted average diluted shares outstanding for FY ‘15 and FY ‘16 respectively

$Million except per share

Annual Spend Growth 11+% -

License TCV Growth - Exceed 11%

Free Cash Flow 175 - 180 220

Total Revenue 470 - 478 437 - 439

Total GAAP Expense 275 - 280 261 - 264

Operating Income 192 - 200 175 - 177

Operating Margin 41% - 42% 40%

Net Income 122 - 127 113 - 115

Net Income per share $1.40 - $1.46 $1.27 - $1.29

Non-GAAP Operating Income 207 - 215 193 - 195

Non-GAAP Operating Margin 44% - 45% 44%

Non-GAAP Net Income per share $1.51 - $1.57 $1.41 - $1.43

FY '15 Full Year

Guidance (1)

FY '16 Full Year

Guidance (1)

© 2015 Aspen Technology, Inc. All rights reserved 57

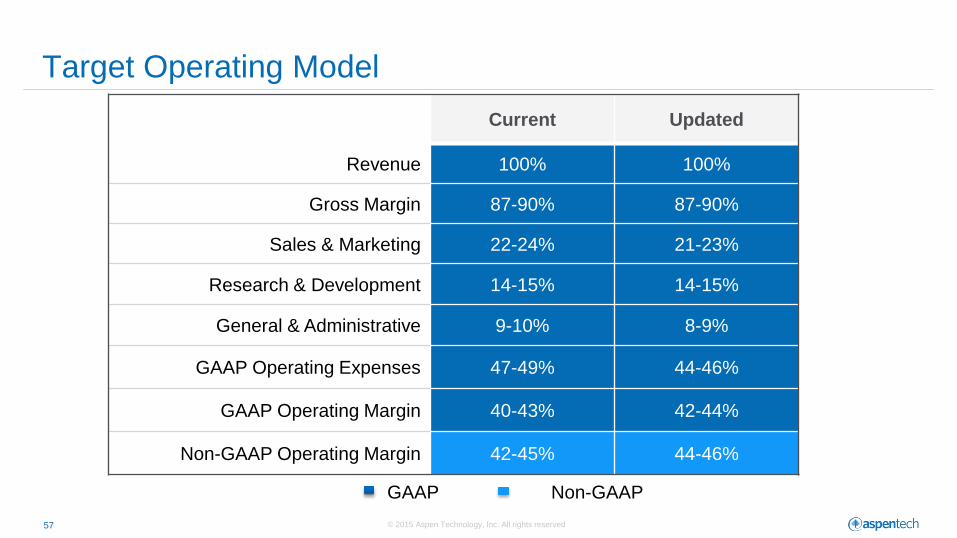

Target Operating Model

Current Updated

Revenue 100% 100%

Gross Margin 87-90% 87-90%

Sales & Marketing 22-24% 21-23%

Research & Development 14-15% 14-15%

General & Administrative 9-10% 8-9%

GAAP Operating Expenses 47-49% 44-46%

GAAP Operating Margin 40-43% 42-44%

Non-GAAP Operating Margin 42-45% 44-46%

GAAP Non-GAAP

© 2015 Aspen Technology, Inc. All rights reserved 58

• Multi-Billion Dollar Market Opportunity

• Market Leadership Position

• World-Class Customer Base with Significant Upsell Opportunities

• Subscription Model with Long-Term Contracts

• Shareholder Value Driven Focus

• Best In Class Profitability and Cash Flow Profile

Conclusion and Q&A

Q&A