An Economic Analysis of Bangladesh's Foreign Exchange Reserves

Bank of Israel

Market Operations Department

Investment of the

Foreign Exchange

Reserves

Annual Report 2014

1

Contents

Main developments………………………………………………………………………2

A. The foreign exchange reserves……………………………………………………….4

1. The framework for holding and managing the reserves……………………………4

2. The risk profile of the reserves and investment policy guidelines…………...…….5

3. The risk management framework and strategic allocation…………………..……. 6

4. Changes in the level of the reserves in 2014…………………………………..…...8

5. The level of Israel’s foreign exchange reserves…………………………………..10

B. The global economic and financial environment……………………………………12

C. The holding period rate of return on the reserves in 2014…………………………..17

1. The rate of return on the reserves portfolio………………………………….……17

2. The active management contribution………………………………………….….19

2.a Contribution of the investment in equities………………………………..…..20

2.b Contribution of active management in numeraire currencies portfolios……..23

2.c Contribution of strategic exposures……………………………….………… 24

3. CVaR and risk - return measurement…………………………………….………28

Appendix 1: Glossary…………………………………………………….…………….31

Appendix 2: Foreign exchange reserves: investment policy guidelines………..………34

Appendix 3: Principles for determining the desired level of the foreign exchange

Reserves……………………………………………………………………….………. 40

2

Main developments1

Israel's foreign exchange reserves increased by about $4 billion in 2014,

compared with an increase of about $6 billion in the previous year, and at the end of

2014 they totaled $86.1 billion.2

In 2014, the Bank of Israel purchased $7 billion. Half the sum was purchased

within the framework of the Bank of Israel’s intervention intended to moderate

exchange rate volatility which is not in line with fundamental economic conditions in

Israel, and the other half was purchased within the framework of implementing the plan

to moderate the effect of natural gas production on the exchange rate. The change in the

reserves that is attributed to interest income, capital gains, and exchange rate

differentials between the dollar and the currencies in which the reserves are invested,

reduced the reserves by around $3 billion. This was mainly the result of the

strengthening of the dollar vis-à-vis the other currencies in which the reserves portfolio

is held.

At the beginning of the year, the investment policy guidelines for the foreign

exchange reserves were revised—the maximum permitted allocation to equities was

increased to 12 percent, from 6 percent, and investments in corporate bonds were

approved, to a maximum of 6 percent of the reserves. The guidelines were updated

following the definition of the reserves’ risk profile that was determined toward the end

of 2013. The risk profile then was defined so that given the worst 5 percent of possible

outcomes the average loss would not exceed 400 basis points, in a one-year horizon

(CVaR5%). During the course of the year, the CVaR5% of the reserves portfolio ranged

around 300 basis points.

Within the framework of the process of the strategic allocation of the reserves

portfolio for 2014, it was decided to allocate 8 percent to equities and the remainder to

bonds; to increase the portfolio’s duration from 10 months to 12 months; and to include

a corporate bond component in the reserves. Accordingly, toward the end of the year,

one percent of the reserves were invested in US corporate bonds as a pilot investment.

This year, the holding period rate of return on the reserves, in terms of the

numeraire3, was 1.28 percent, of which 0.22 percent was the benchmark return and 1.06

percent was the active management contribution. The active management contribution,

which was double the previous decade’s average, is attributed primarily to investment in

equities, which contributed 67 basis points. Investing the reserves in longer maturities,

1 The report on the investment of Israel's foreign exchange reserves has been published each year since

2000. Previous years’ reports are published on the Bank of Israel website at:

http://www.boi.org.il/en/Markets/ForeignExchangeReservesReport/Pages/Default.aspx 2 The level of the reserves includes allocations of Special Drawing Rights by the International Monetary

Fund to member countries (SDR Allocation) and Israel's balance in the Reserve Tranche of the Fund. At

the end of 2014 these totaled $1.8 billion. For more on this issue, see the Bank of Israel's Financial

Statements for 2014. 3 The numeraire is a currency basket in which the foreign exchange reserves are measured. For more

information, see Chapter A, Section 3 of this report.

3

while diversifying assets across the curve differently than in the benchmark, contributed

about 35 basis points to the active management return. This was due to a decline in

yields in countries whose currencies are included in the numeraire, which generated

capital gains.

In continuation of the process, which began in 2013, of reducing the exposure of

the reserves to currencies and assets of commodity-oriented economies, the share of

strategic exposures in the reserves portfolio in 2014 remained low, similar to that at the

end of 2013.

4

A. The foreign exchange reserves

1. The framework for holding and managing the reserves

According to the Bank of Israel Law, 5770–2010, one of the Bank's functions is to

hold and manage the country's foreign exchange reserves.4

In accordance with this law, the Monetary Committee, headed by the Governor, was

granted the authority, among others, to manage the reserves. The Monetary

Committee’s role is to establish the guidelines for the investment of the reserves, in

consultation with the Minister of Finance, and to monitor the implementation of such

policy. The Committee approves and revises the allocation of responsibilities for the

investment of the reserves between it on the one hand and the Foreign Currency

Committee5 and the Market Operations Department on the other. In addition, the

Monetary Committee, with the approval of the Minister of Finance, has the power to

change the guidelines according to which the Governor decides on the appropriate long-

term level of foreign exchange reserves.

Countries hold foreign exchange reserves for three main purposes:

To provide the economy with sufficient foreign currency for an emergency situation

(such as war or natural disaster). In such instances, it may be necessary to maintain

imports or to rapidly increase them in order to deal with the emergency, while

exports are liable to be negatively impacted, thus reducing the inflow of foreign

currency. In these circumstances, the government and the private sector will find it

difficult to raise foreign currency abroad, and the foreign exchange reserves will

become the country’s main source for financing in foreign currency.

To enable the central bank to intervene in the foreign currency market in the

following circumstances: (1) the foreign exchange rate has deviated from the range

that is consistent with the economy’s fundamental equilibrium; or (2) the foreign

currency market is not functioning properly (market failure).

To allow the central bank to operate in the foreign currency market in order to

moderate the effect of significant capital flows of either foreign or local residents,

which are liable to undermine the stability of the financial markets, thereby

negatively impacting the stability of the economy as a whole (a specific case of the

previous function).

In order to achieve these goals, the investment of the reserves is carried out according to

the following three basic principles: Maintaining the purchasing power of the

reserves, managing the reserves at a high level of liquidity and achieving a

suitable holding-period rate of return on the reserves portfolio, as long as this

does not interfere with achieving the previous objectives (as discussed in Appendix

2—Foreign Exchange Reserves: Investment Policy Guidelines).

4 Until the Bank of Israel Law, 5770–2010 came into force, on June 1, 2010, the reserves were managed

in accordance with the Bank of Israel Law, 5714–1954 and its legal interpretations over the years, and in

accordance with the investment policy decided on by the Governor. 5 The Foreign Currency Committee is an internal committee of the Bank, headed by the Governor. Its

function is to translate the guidelines for investing the reserves into detailed instructions for their

management.

5

2. The risk profile of the reserves and investment policy guidelines

The reserves portfolio is managed within a framework of investment rules. These rules

were set in order to achieve the investment policy objectives, while controlling the

exposure of the reserves to various financial risks—currency risk, price risk,6 credit risk

and liquidity risk. In principle, the rules are conservative and express cautious

management of the reserves. The reserves’ investment policy makers are aware of

developments in the markets and changes in the level of the reserves, and make changes

and revisions in the rules and the characteristics of investment when necessary.

Toward the end of 2013, the Monetary Committee completed the process of adjusting

the risk profile of the reserves to their current level and the integration of the foreign

currency purchases in the framework of the natural gas program, whose investment

horizon is long-term. The risk profile was defined in terms of the maximum loss that the

Committee is willing to accept, without affecting the attainment of the objectives for

which the reserves are kept. Accordingly, the risk profile was determined so that given

the worst 5 percent of possible outcomes the average loss would not be greater than 400

basis points over a one-year horizon (CvaR5%).7 Nevertheless, the Committee

determined that the strategic allocation would be limited to a maximum CVaR of 300

basis points. This is consistent with the Committee’s risk appetite and the desire not to

utilize the entire risk budget so as to leave some risk margin for the active management

of the reserves portfolio and to make any possible necessary changes in the CVaR due

to volatility of the markets.

The guidelines for the investment policy were revised at the beginning of 2014

according to the risk profile defined.8 Two changes stand out in particular: the

maximum permitted allocation for investment in equities was increased from 6 percent

to 12 percent of the reserves, and for the first time investment in corporate bonds was

approved, up to a maximum of 6 percent of the reserves.9

6 The price risk for bonds is the interest rate risk measured in terms of modified duration.

7 CvaR5% is the average of the 5 percent percentile of the distribution of the expected returns of the

reserves portfolio. 8 See Appendix 2 for the revised guidelines.

9 The utilization rate for the permitted allocation in each type of assets for foreign exchange reserves

investment is subject to compliance with the defined risk profile.

6

3. The risk management framework and strategic allocation

Like other investors around the world, management of the various financial risks in the

Bank of Israel’s foreign exchange reserves portfolio is based on management of the

reserves portfolio vis-a-vis a benchmark. A benchmark is a hypothetical portfolio

composed of various investable assets and formulated according to known and fixed

rules. The benchmark represents the portfolio holder’s preferences and risk profile,

which are reflected in its composition and in its characteristics. The benchmark provides

a yardstick for measuring performance of the portfolio manager’s investment decisions.

The numeraire is a basket of currencies whose composition reflects the possible uses of

the reserves, when necessary, and the principles that reflect the goals of holding those

reserves. The holding period rate of return on foreign exchange reserves is measured in

terms of the numeraire, and from the point of view of the reserves portfolio manager, its

composition is considered to be a neutral composition. The composition of the

numeraire is reviewed at least once a year and revised when necessary with the approval

of the Monetary Committee. The numeraire is defined quantitatively (a quantity-based

currency basket) so that its composition varies daily in line with changes in the

exchange rates of its composite currencies. The numeraire consists of three currencies,

whose weights were distributed over the year, on average, as follows:10

dollar—63.8

percent, euro—33.2 percent, and pound sterling—3.0 percent.

The numeraire benchmark (“the benchmark”) represents a conservative composition

of investable assets, which meets the first two goals of the investment policy for the

reserves—maintaining their purchasing power and managing the reserves with a high

level of liquidity. The benchmark is therefore invested in highly rated, short-term

government bonds of selected countries whose currencies are included in the numeraire,

and they provide a high degree of security and liquidity. The currency composition of

the benchmark and the numeraire are identical, so that the benchmark has no currency

exposure.

In the past, prior to March 2014, the benchmark represented the risk profile consistent

with the portfolio holder’s risk appetite. In March 2014, it was decided that the

benchmark composition would represent an investable portfolio with minimum risk,

high levels of security and liquidity. The duration of the portfolio was therefore

reduced, 11

and set at six months, instead of the previous ten months.12

Notably, the change in the benchmark lowers its expected return due to its minimal risk

level, and reduces its volatility. Therefore, the result obtained by comparing the

portfolio performance to the benchmark performance may differ from the result of

comparing the portfolio performance to the performance of the benchmark which the

portfolio was measured against in the years preceding the change.

10

In November 2013, as part of a periodic assessment, the parameters that form the basis for

determining the numeraire’s distribution were reviewed. The Monetary Committee decided not to

change the numeraire’s currency composition, and to leave its distribution as it was previously: 63

percent—dollar, 34 percent—euro, and 3 percent— pound sterling. 11

Throughout this document, duration refers to duration of the portfolio excluding the equity

component. 12

Until March 2014, the duration of the portfolios that make up the benchmark was 9, 10, and 16

months for the dollar, euro and pound sterling portfolios, respectively. Since March 2014, each of

these portfolios has a duration of 6 months.

7

At the beginning of 2014, a process of strategic allocation of the reserves portfolio was

conducted. The various characteristics of this allocation were determined by the

Monetary Committee in an effort to attain a suitable return, subject to the risk profile

defined by the Committee, while meeting the first two goals of the reserves portfolio

holding policy. The allocation takes place as necessary, in line with market

developments and at least once a year.

As part of the strategic allocation, the strategic composition of the reserves portfolio

was determined so that the expected return on the portfolio is high within the

framework of the desired risk level and the guidelines’ limitations. This, given the

forecasts for the returns on the different assets included in the allocation.

The Monetary Committee approved the following strategic allocation for 2014:

8 percent will be invested in equities.

92 percent will be invested in fixed income.

The portfolio duration was increased so as to increase the expected return. In

2014 the duration of the reserves portfolio was 12 months13

compared to 10

months in 2013.

During the strategic allocation process, it was decided that corporate bonds would

comprise 2 to 6 percent of the portfolio, in accordance with market conditions and the

expected spread levels. Therefore, toward the end of 2014, the Bank of Israel began to

invest in US corporate bonds with a rating of BBB- and above, subject to the guidelines

according to which the maximum permitted investment in this type of bonds is up to 6

percent of the portfolio. As this is a new component in the reserves portfolio, an initial

pilot investment in corporate bonds of 1 percent of the reserves was made—half of

which is managed internally and half of which is managed through an external manager

specializing in the management of investments in this channel. Although corporate bond

spreads have declined in recent years, reducing the attractiveness of this investment

channel relative to the past, the expectation of an excess return compared with Treasury

notes supports the inclusion of corporate bonds in the portfolio.

13

Average duration over the course of the year.

8

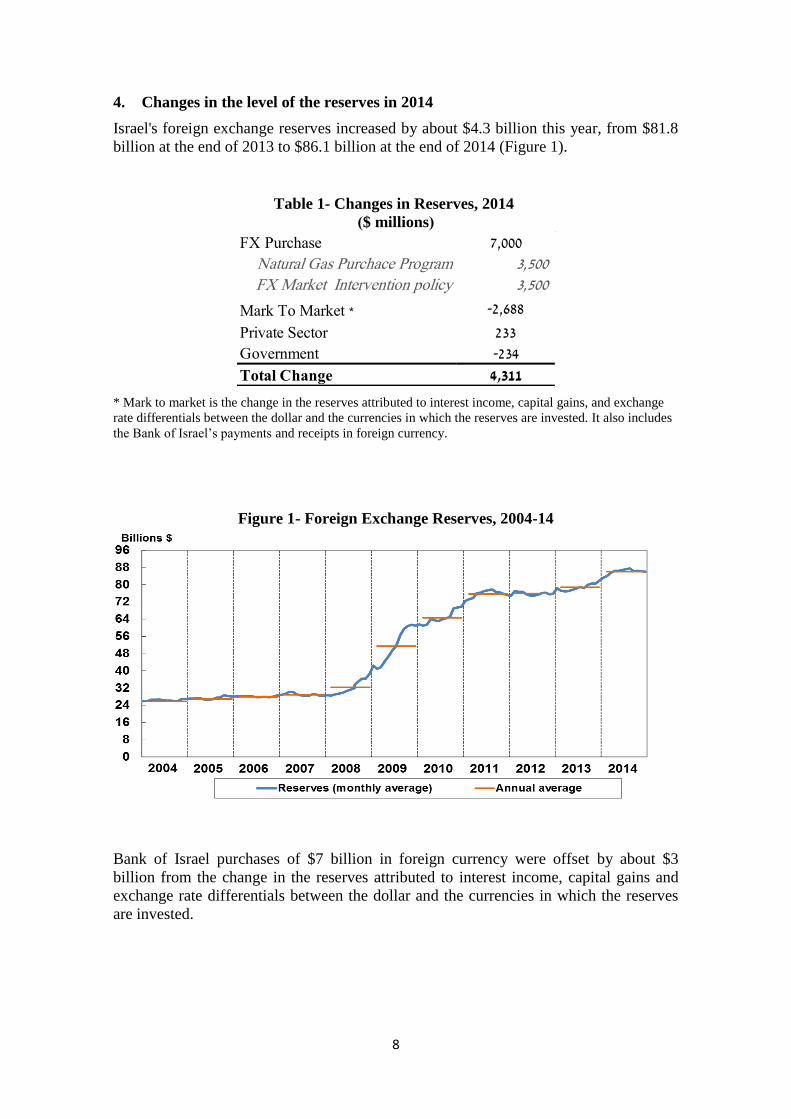

4. Changes in the level of the reserves in 2014

Israel's foreign exchange reserves increased by about $4.3 billion this year, from $81.8

billion at the end of 2013 to $86.1 billion at the end of 2014 (Figure 1).

Table 1- Changes in Reserves, 2014

)$ millions(

* Mark to market is the change in the reserves attributed to interest income, capital gains, and exchange

rate differentials between the dollar and the currencies in which the reserves are invested. It also includes

the Bank of Israel’s payments and receipts in foreign currency.

Figure 1- Foreign Exchange Reserves, 2004-14

Bank of Israel purchases of $7 billion in foreign currency were offset by about $3

billion from the change in the reserves attributed to interest income, capital gains and

exchange rate differentials between the dollar and the currencies in which the reserves

are invested.

FX Purchase 7,000

Natural Gas Purchace Program 3,500 FX Market Intervention policy 3,500

Mark To Market * -2,688

Private Sector 233

Government -234

Total Change 4,311

9

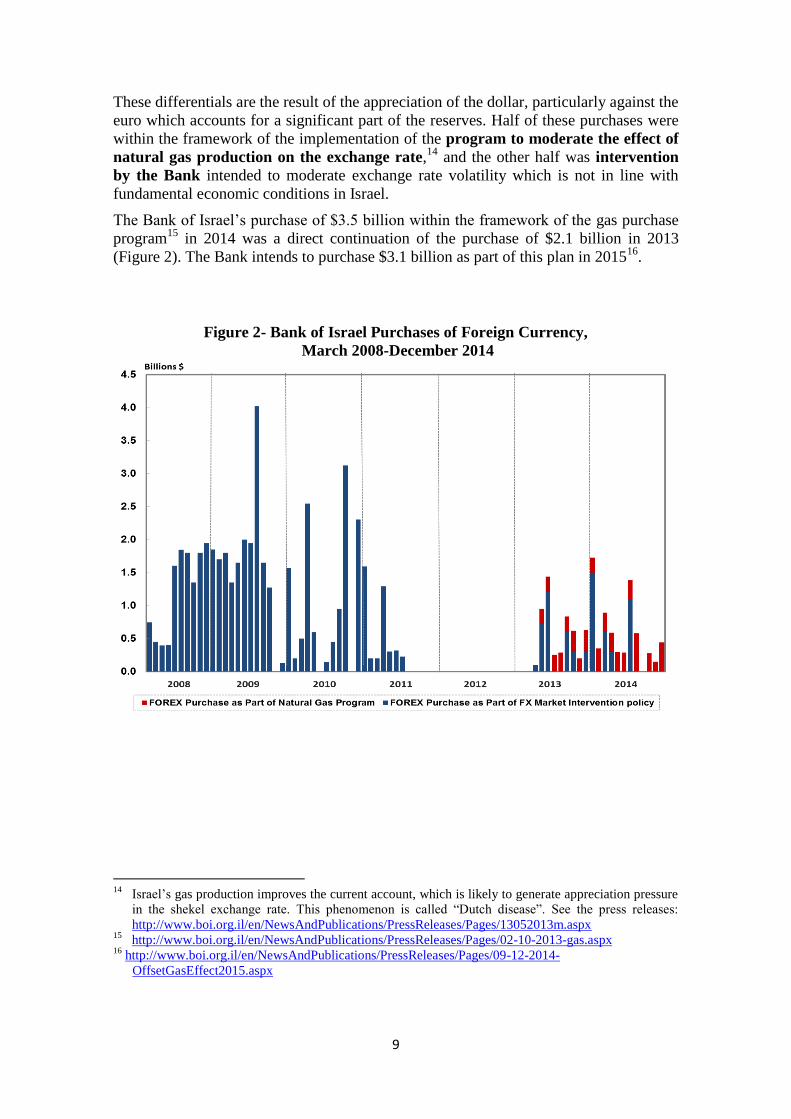

These differentials are the result of the appreciation of the dollar, particularly against the

euro which accounts for a significant part of the reserves. Half of these purchases were

within the framework of the implementation of the program to moderate the effect of

natural gas production on the exchange rate,14

and the other half was intervention

by the Bank intended to moderate exchange rate volatility which is not in line with

fundamental economic conditions in Israel.

The Bank of Israel’s purchase of $3.5 billion within the framework of the gas purchase

program15

in 2014 was a direct continuation of the purchase of $2.1 billion in 2013

(Figure 2). The Bank intends to purchase $3.1 billion as part of this plan in 201516

.

Figure 2- Bank of Israel Purchases of Foreign Currency,

March 2008-December 2014

14

Israel’s gas production improves the current account, which is likely to generate appreciation pressure

in the shekel exchange rate. This phenomenon is called “Dutch disease”. See the press releases:

http://www.boi.org.il/en/NewsAndPublications/PressReleases/Pages/13052013m.aspx 15

http://www.boi.org.il/en/NewsAndPublications/PressReleases/Pages/02-10-2013-gas.aspx 16 http://www.boi.org.il/en/NewsAndPublications/PressReleases/Pages/09-12-2014-

OffsetGasEffect2015.aspx

10

5. The level of Israel’s foreign exchange reserves

a. Adequacy of the level of the foreign exchange reserves

The adequacy of the level of foreign exchange reserves is an important indicator of

a country’s financial stability, and supports the central bank in carrying out its

functions. The reserves are a source of liquidity in foreign currency, which the bank

can use when needed. Furthermore, an adequate level of foreign exchange reserves

contributes to improving the country’s international financial standing by

increasing confidence in its ability to withstand shocks to the economy. This

advantage is manifested in the country’s credit rating, and in the evaluations

produced by rating agencies, allowing the economy to lower the costs of financing

debt raised abroad.

The principles for determining the appropriate level of reserves were defined

according to the goals for holding them.17

Based on these principles, at the

beginning of 2015, the Governor revised the appropriate range to between $70 and

$110 billion, replacing the previous range of $65-90 billion, defined by the

Governor in 2010. The appropriate range was revised on the basis of these

principles and in accordance with economic developments over the last five years.

In terms of GDP for 2014, the appropriate level is within the 23-36 percent range,

slightly lower than the previous range for GDP in 2010 of 28-39 percent. The

reserve level is currently close to the middle of the new range determined by the

Governor.

The Bank of Israel’s intervention in the foreign exchange market for the purpose of

carrying out its functions and attaining its objectives may lead to a deviation in the

actual level of reserves from the determined appropriate level. Such a deviation is

permitted under the Bank of Israel Law. Nevertheless, the Bank may take action to

alter the level of reserves only when the deviation is significant and sustained, and

only if such actions are consistent with attaining the Bank’s objectives as specified

in the Bank of Israel Law - including price stability, support for other objectives of

economic policy, and support for stability in the financial system. It is therefore

possible for the foreign exchange reserves to deviate from the desired level for

extended periods of time.

b. Israel’s actual levels of foreign exchange reserves

The adequacy of the level of reserves held by a country is generally evaluated in

terms of ratios of the reserves to various economic variables. In Israel, these ratios

have risen during the past decade as a result of the increase in the size of the

reserves since 2008 (Table 2).

17

See Appendix 3: Principles for determining the appropriate level.

11

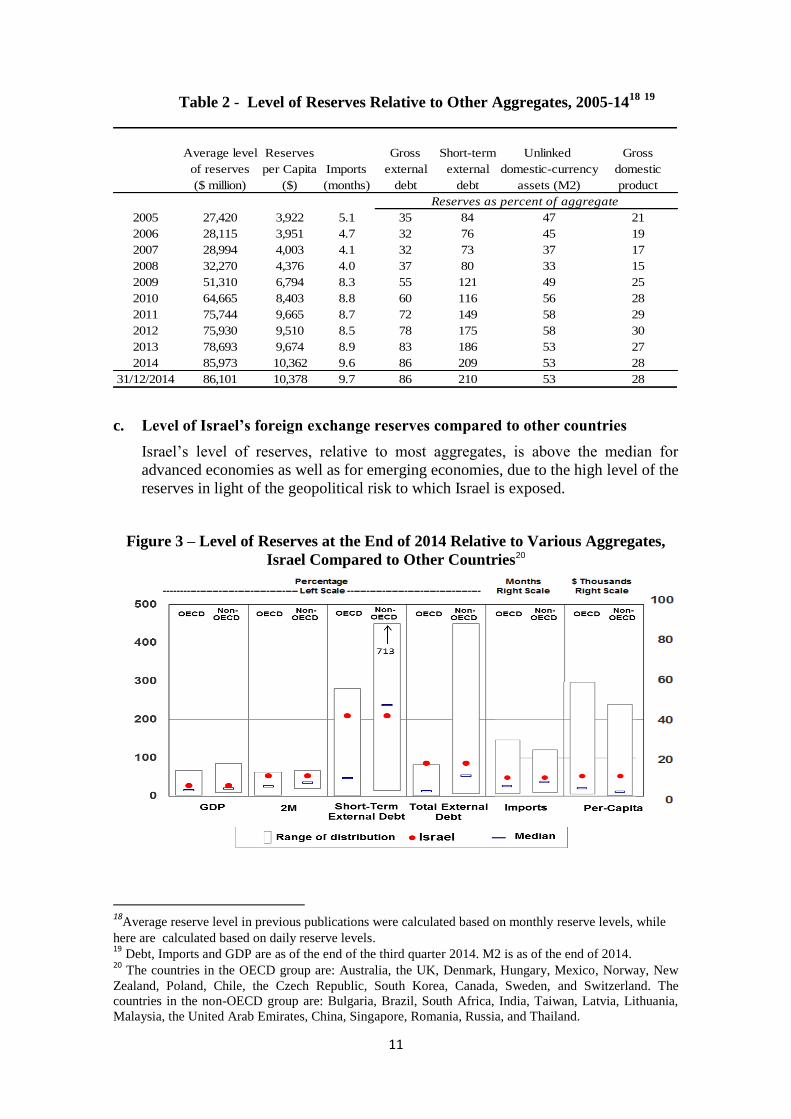

Table 2 - Level of Reserves Relative to Other Aggregates, 2005-1418

19

c. Level of Israel’s foreign exchange reserves compared to other countries

Israel’s level of reserves, relative to most aggregates, is above the median for

advanced economies as well as for emerging economies, due to the high level of the

reserves in light of the geopolitical risk to which Israel is exposed.

Figure 3 – Level of Reserves at the End of 2014 Relative to Various Aggregates,

Israel Compared to Other Countries20

18

Average reserve level in previous publications were calculated based on monthly reserve levels, while

here are calculated based on daily reserve levels. 19

Debt, Imports and GDP are as of the end of the third quarter 2014. M2 is as of the end of 2014. 20

The countries in the OECD group are: Australia, the UK, Denmark, Hungary, Mexico, Norway, New

Zealand, Poland, Chile, the Czech Republic, South Korea, Canada, Sweden, and Switzerland. The

countries in the non-OECD group are: Bulgaria, Brazil, South Africa, India, Taiwan, Latvia, Lithuania,

Malaysia, the United Arab Emirates, China, Singapore, Romania, Russia, and Thailand.

Average level Reserves Gross Short-term Unlinked Gross

of reserves per Capita Imports external external domestic-currency domestic

($ million) ($) (months) debt debt assets (M2) product

2005 27,420 3,922 5.1 35 84 47 21

2006 28,115 3,951 4.7 32 76 45 19

2007 28,994 4,003 4.1 32 73 37 17

2008 32,270 4,376 4.0 37 80 33 15

2009 51,310 6,794 8.3 55 121 49 25

2010 64,665 8,403 8.8 60 116 56 28

2011 75,744 9,665 8.7 72 149 58 29

2012 75,930 9,510 8.5 78 175 58 30

2013 78,693 9,674 8.9 83 186 53 27

2014 85,973 10,362 9.6 86 209 53 28

31/12/2014 86,101 10,378 9.7 86 210 53 28

Reserves as percent of aggregate

12

B. The global economic and financial environment

In the global financial environment, government bond yields declined sharply

in 2014 while prices in stock markets in advanced economies, particularly the

US, increased. In emerging economies, trends were mixed. Equity market

prices in advanced economies rose despite the tapering of the US quantitative

easing program, which reached an end in October, and against the

background of quantitative easing programs in the eurozone and Japan, and

the relative strength of the US economy. These factors also led to a sharp

appreciation of the dollar against most currencies, primarily in the second half

of the year. In parallel, the price of oil dropped markedly, as global demand

declined at the same time as the supply of oil increased. In the global economic

environment, inflation rates declined during the year to below the inflation

targets of many central banks—posing a critical risk in some of the economies.

In the first half of the year, stock market prices rose and government bond yields

declined, against the background of the accommodative monetary policy

worldwide, and despite the tapering of quantitative easing in the US. As Europe and

Japan showed further signs of weakness in the second half of the year, including

weak macroeconomic data and low inflation levels, the decoupling of Europe and

Japan from the resurgent US economy intensified. This was reflected in US

outperformance compared to volatile trading in Europe and Japan. In June, the

price of Brent crude oil began a steep decline from $105 to just $55 a barrel at the

end of the year, against the background of a slowdown in demand and an increase

supply. These trends derived from, among other things, further slowdown in China,

the energy revolution in the US and OPEC’s decision not to cut back the supply of

oil. The global economic and financial environment during the year was also

affected by the deteriorating geopolitical situation between Russia and Ukraine,

which led to increased risk aversion among investors.

In parallel with these financial developments, the real economy in most

countries—particularly in Europe, Japan and the emerging economies, continued to

slow. In October, the International Monetary Fund revised downward its global

growth forecast, according to which, in 2014 the global economy was expected to

grow by 3.3%, below the long-term trend. This was mainly due to continuing

weakness in emerging markets and the fact that various European economies as

well as Japan were once again in recession. The forecast for global growth in 2015

is 3.8%.

In October, the US Federal Reserve ended its quantitative easing program in light

of improved macro data, particularly in the employment market, where 215,000

jobs on average were added each month and the unemployment rate declined from

6.7 percent to just 5.8 percent.

Notwithstanding the tapering, yields on 10-year US government notes declined in

2014 from 3 percent to 2.2 percent. There are several reasons for this: excess

liquidity in the markets, accommodative monetary policy around the world, low

yields in Europe in general, and in its peripheral economies in particular, increased

demand for US Treasury notes by central banks worldwide (including China’s

central bank) and the strengthening of the dollar. In contrast, yields on two-year

notes increased from 38 to 66 basis points, against the background of market

assessments that the US would increase the interest rate in the near future.

13

Figure 4 – Ten-Year Yields to Maturity of US, Germany and UK

Government Bonds, 2014

Figure 5 – Two-Year Yields to Maturity of US, Germany and UK

Government Bonds, 2014

Severe weather in the US at the beginning of the year adversely affected economic

data (employment, real estate, manufacturing, and sales), resulting in negative

growth of 2.1 percent21

in the first quarter. Due to this weakness, investment houses

lowered US 2014 growth projections from 3 percent to just 1.7 percent. However,

with the economy’s recovery as the year progressed, growth rates rose significantly

in the following quarters, so that at the end of 2014 annual growth was 2.5 percent.

In the eurozone, against the background of economic weakness, reflected in weak

growth figures and low inflation, the ECB reduced the interest rate on bank deposits

to negative levels, beginning with a program to purchase asset-backed securities

21

The growth rates mentioned in this publication are quarter on quarter in annual terms, unless specified

otherwise.

14

and covered bonds, and it announced that it intended to increase its balance sheet

by a further trillion euros. As a result, yields in the eurozone declined markedly

during the year, and in Germany the 10-year yield fell from 1.9 percent to 0.6

percent (Figure 4). At the same time, spreads between the core and peripheral

countries continued to narrow, in part against the background of the ECB’s

announcement that it was committed to ensuring the eurozone’s stability.

Europe’s economy continued to weaken, with growth levels below 1 percent. This

year Germany, as well, lost strength: its growth rate in the third quarter was just 0.1

percent, following -0.1 percent in the second quarter. Over the last two years, the

2014 growth forecast for the eurozone was revised downward, and in October the

International Monetary Fund reduced its 2014 forecast from 1.4 percent to just 0.8

percent, with a slightly more optimistic forecast of 1.35 percent for 2015. Despite

the near-zero interest rate and quantitative easing programs, inflation remained low,

remaining a source of concern for European policy makers. The inflation rate

declined from 0.8 percent at the beginning of the year to -0.2 percent at year-end,

and although lower energy prices should support growth, they are also an obstacle

to higher inflation.

Against the background of the weak European economy and relatively strong US

economy, in 2014 the euro depreciated against major currencies by 14 percent22

,

reaching its lowest level since 2006 against the dollar. The only leading currencies

against which the euro strengthened in 2014 were the Norwegian Krone, which the

euro appreciated against by 7.7 percent, and the Swedish Krone, against which the

euro appreciated by 6.1 percent. This was largely due to the sharp decline in energy

prices that affected Norway’s economy, and the economic slowdown and negative

inflation in Sweden which motivated its central bank to lower the interest rate

during the year.23

In Japan, the Bank of Japan increased its bond purchases during the year from a

target of 60-70 trillion Yen per annum (announced in February) to a target 80

trillion Yen per annum (announced in October). The central bank purchases, of

which about two-thirds were government issues, were intended to inject liquidity

into the economy, depreciate the yen, encourage consumption and ensure that

yields on government bonds remained low. In fact, during the year, the 10-year

yield on government bonds declined from 0.7 percent to only 0.3 percent.

Nevertheless, despite a 12 percent devaluation and the sharp drop in oil prices,

exports failed to increase.

In the second quarter of 2014, Japan’s government increased the VAT rate from 5

percent to 8 percent as part of a government expansionary policy to improve the

country’s fiscal position. The VAT increase led growth to contract sharply by 6.7

percent in the second quarter, and -1.9 percent negative growth rate in the third

quarter put the Japanese economy back in recession. Against the background of the

VAT increase, the rate of inflation (excluding fresh food and energy) increased

from 0.3 percent to 1.8 percent, with a debt of 240% in GDP in the background and

structural changes and fiscal expansion that are still to be implemented.

In the UK, the economy grew rapidly compared with the rest of Europe, from 2.4

percent (year over year) in the first quarter, to 2.7 percent in the fourth quarter.

22

Against the dollar. 23

From 0.75 percent to 0 percent.

15

Financial markets were strongly impacted by comments made by the Governor of

the Bank of England, Mark Carney. In May, he raised the possibility of an interest

rate rise in 2014, although later in the year he commented that the economic

situation was less favorable than it appeared. The result was that the markets once

again postponed pricing in the first interest rate increase in the UK. The Bank of

England’s growth forecasts for 2015 and 2016 were lowered by 0.2 percent, to 2.8

percent and 2.6 percent respectively, and inflation is expected to be less than 1%,

after declining from 2 percent to just 0.5 percent in 2014. Over the year, 10-year

UK government bond yields declined from 3 percent to 1.8 percent.

In 2014, China continued to take the necessary steps for maintaining stable,

sustainable growth without exacerbating the slowdown arising from the

implementation of these changes.

The growth rate in the third quarter was 7.3% (in annual terms).24

Investment as a

component of GDP continued to moderate, mainly due to lower levels of

investment in real estate and infrastructure, whereas domestic consumption and net

exports grew. At the same time, inflation reached a six-year low, allowing

policymakers to introduce expansionary but focused monetary policy in an effort to

avoid increasing the high debt levels.

In emerging economies, growth in 2014 was relatively weak, with economic

activity in the central areas below the trend for the past three years. The year began

with a growing external deficit and high levels of inflation. The environment was

therefore sensitive to external shocks, seen as tapering began and was followed by

increased yields in the US. Due to the tightened financial conditions and liquidity in

these markets in the second half of 2013, which were accompanied by economic

slowdown in China and slowdown in world trade volume, the first half of 2014 was

the worst period for emerging economies since the financial crisis. The situation

improved somewhat as the year progressed due to a marked improvement in the

external balance, economic recovery in the US, the sharp decline in inflation and

accommodative policies introduced by the central banks in Europe and Japan. The

decline in inflation provided policymakers in the emerging markets with greater

freedom of action, and in some cases accommodative monetary policy and new

structural reforms were introduced.

Nevertheless, the economies in these markets are extremely diverse and global

developments affect them very differently. For example, the strengthening of the

dollar supports export-oriented countries, whereas lower energy prices support

import-oriented countries. The key to successfully coping with the changing

situation appears to be the ability of the different economies to implement

appropriate structural reforms.

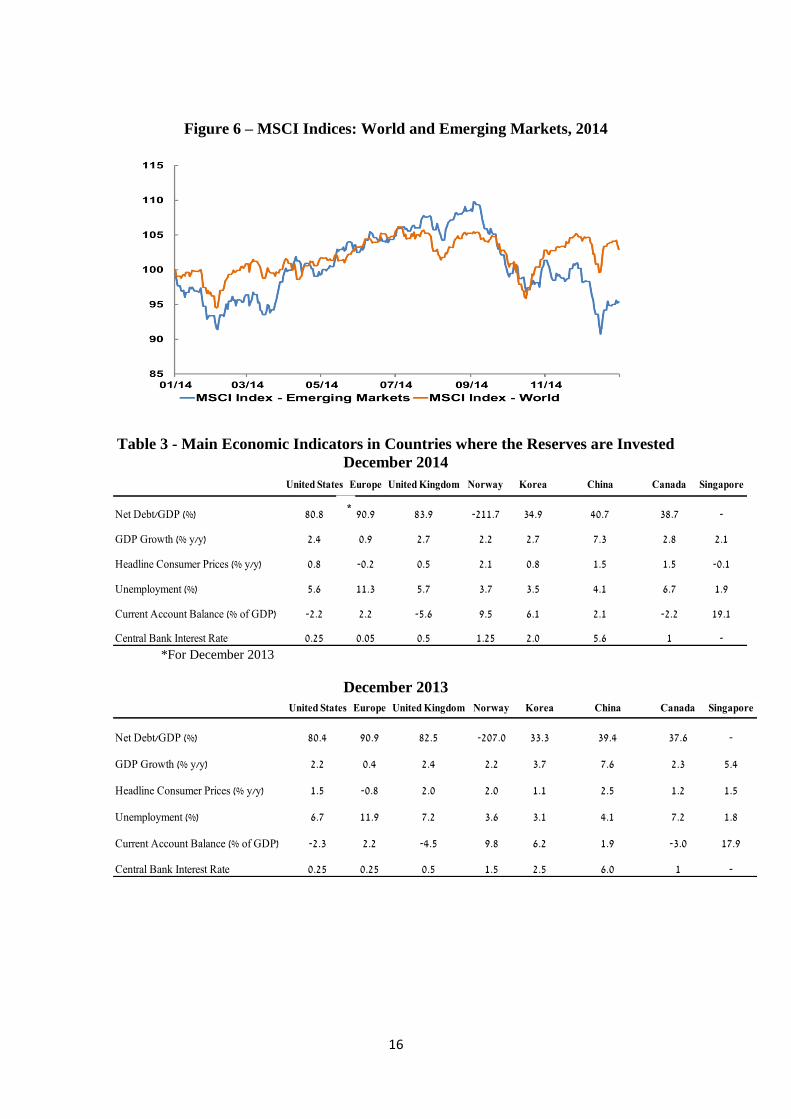

In the financial markets, the emerging economies did not benefit from the US

recovery. Their currencies weakened against the dollar and the MSCI Emerging

Markets Index declined by 4.6 percent, compared with a 3 percent increase in the

corresponding index for developed economies. In contrast, low commodities prices

and prolonged expansionary monetary policy provided a positive environment for

the government bonds of emerging markets. Since November, when risk aversion

increased due to tension with Russia, there has been an outflow of capital from the

emerging economies.

24

After 7.4% in the first quarter and 7.5% in the second quarter.

16

Figure 6 – MSCI Indices: World and Emerging Markets, 2014

Table 3 - Main Economic Indicators in Countries where the Reserves are Invested

December 2014

*For December 2013

December 2013

United States Europe United Kingdom Norway Korea China Canada Singapore

Net Debt/GDP (%) 80.8 90.9 83.9 -211.7 34.9 40.7 38.7 -

GDP Growth (% y/y) 2.4 0.9 2.7 2.2 2.7 7.3 2.8 2.1

Headline Consumer Prices (% y/y) 0.8 -0.2 0.5 2.1 0.8 1.5 1.5 -0.1

Unemployment (%) 5.6 11.3 5.7 3.7 3.5 4.1 6.7 1.9

Current Account Balance (% of GDP) -2.2 2.2 -5.6 9.5 6.1 2.1 -2.2 19.1

Central Bank Interest Rate 0.25 0.05 0.5 1.25 2.0 5.6 1 -

United States Europe United Kingdom Norway Korea China Canada Singapore

Net Debt/GDP (%) 80.4 90.9 82.5 -207.0 33.3 39.4 37.6 -

GDP Growth (% y/y) 2.2 0.4 2.4 2.2 3.7 7.6 2.3 5.4

Headline Consumer Prices (% y/y) 1.5 -0.8 2.0 2.0 1.1 2.5 1.2 1.5

Unemployment (%) 6.7 11.9 7.2 3.6 3.1 4.1 7.2 1.8

Current Account Balance (% of GDP) -2.3 2.2 -4.5 9.8 6.2 1.9 -3.0 17.9

Central Bank Interest Rate 0.25 0.25 0.5 1.5 2.5 6.0 1 -

*

17

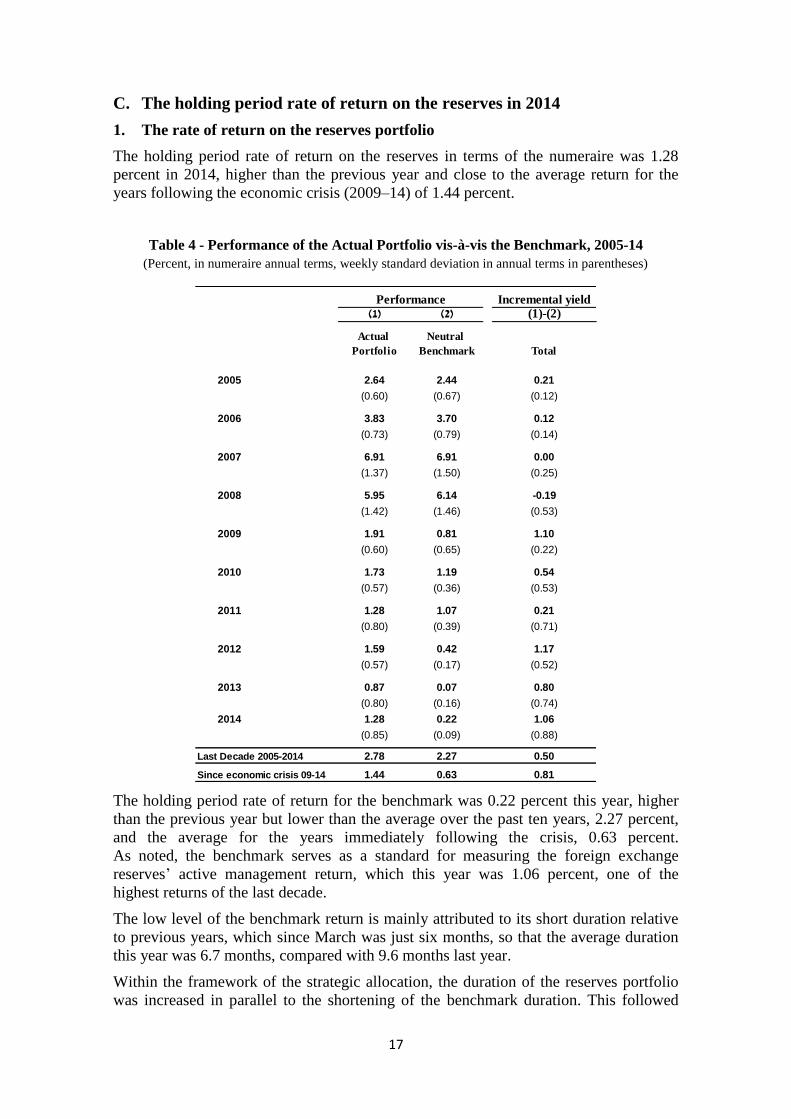

C. The holding period rate of return on the reserves in 2014

1. The rate of return on the reserves portfolio

The holding period rate of return on the reserves in terms of the numeraire was 1.28

percent in 2014, higher than the previous year and close to the average return for the

years following the economic crisis (2009–14) of 1.44 percent.

Table 4 - Performance of the Actual Portfolio vis-à-vis the Benchmark, 2005-14

(Percent, in numeraire annual terms, weekly standard deviation in annual terms in parentheses)

The holding period rate of return for the benchmark was 0.22 percent this year, higher

than the previous year but lower than the average over the past ten years, 2.27 percent,

and the average for the years immediately following the crisis, 0.63 percent.

As noted, the benchmark serves as a standard for measuring the foreign exchange

reserves’ active management return, which this year was 1.06 percent, one of the

highest returns of the last decade.

The low level of the benchmark return is mainly attributed to its short duration relative

to previous years, which since March was just six months, so that the average duration

this year was 6.7 months, compared with 9.6 months last year.

Within the framework of the strategic allocation, the duration of the reserves portfolio

was increased in parallel to the shortening of the benchmark duration. This followed

Incremental yield(1) (2) (1)-(2)

Actual

Portfolio

Neutral

Benchmark Total

2005 2.64 2.44 0.21

(0.60) (0.67) (0.12)

2006 3.83 3.70 0.12

(0.73) (0.79) (0.14)

2007 6.91 6.91 0.00

(1.37) (1.50) (0.25)

2008 5.95 6.14 -0.19

(1.42) (1.46) (0.53)

2009 1.91 0.81 1.10

(0.60) (0.65) (0.22)

2010 1.73 1.19 0.54

(0.57) (0.36) (0.53)

2011 1.28 1.07 0.21

(0.80) (0.39) (0.71)

2012 1.59 0.42 1.17

(0.57) (0.17) (0.52)

2013 0.87 0.07 0.80

(0.80) (0.16) (0.74)

2014 1.28 0.22 1.06

(0.85) (0.09) (0.88)

Last Decade 2005-2014 2.78 2.27 0.50

Since economic crisis 09-14 1.44 0.63 0.81

Performance

18

previous years in which the portfolio duration had been kept short—a response to the

significant decline of the yield curves in many markets around the world to their lowest

levels since 2008. Although maintaining short duration in the portfolio in recent years25

reduced the risk of a negative return in the event of a rise in yields to maturity, it also

led to lower interest income and limited capital gains from the declining yields.

Figure 7- Two-Year Yields to Maturity of US, Germany and UK

Government Bonds, 2008-14

25

From 2009 until the beginning of 2014.

19

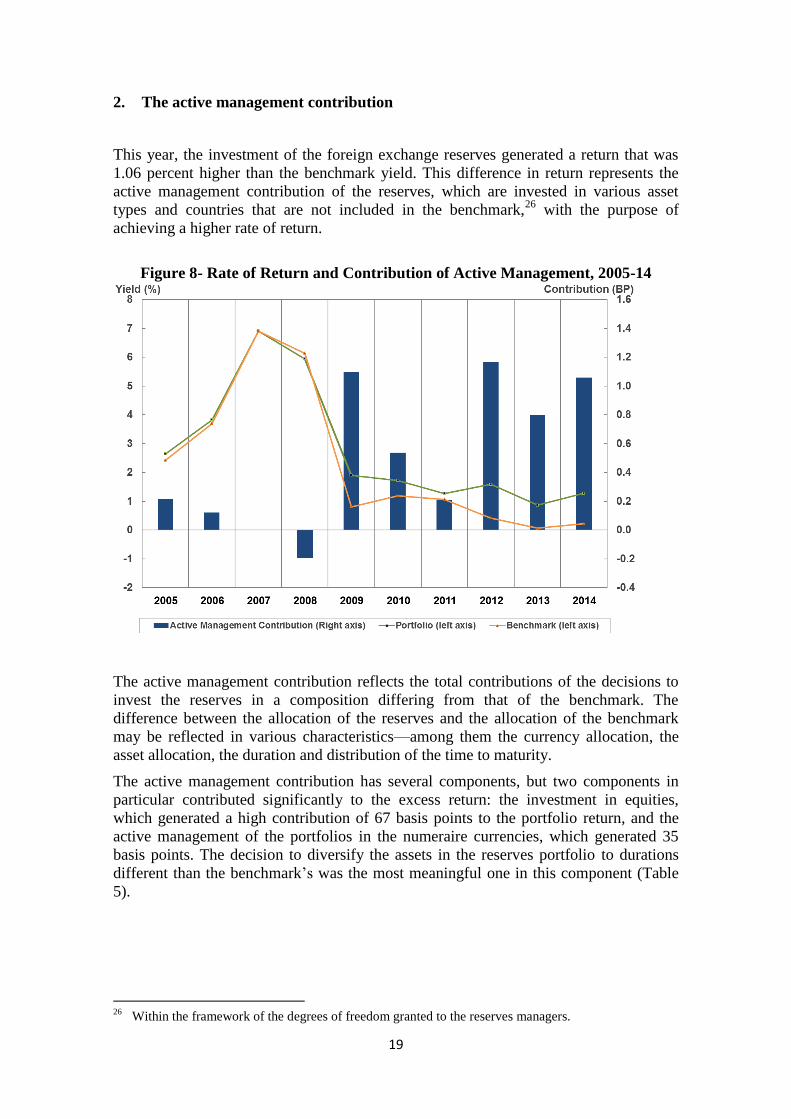

2. The active management contribution

This year, the investment of the foreign exchange reserves generated a return that was

1.06 percent higher than the benchmark yield. This difference in return represents the

active management contribution of the reserves, which are invested in various asset

types and countries that are not included in the benchmark,26

with the purpose of

achieving a higher rate of return.

Figure 8- Rate of Return and Contribution of Active Management, 2005-14

The active management contribution reflects the total contributions of the decisions to

invest the reserves in a composition differing from that of the benchmark. The

difference between the allocation of the reserves and the allocation of the benchmark

may be reflected in various characteristics—among them the currency allocation, the

asset allocation, the duration and distribution of the time to maturity.

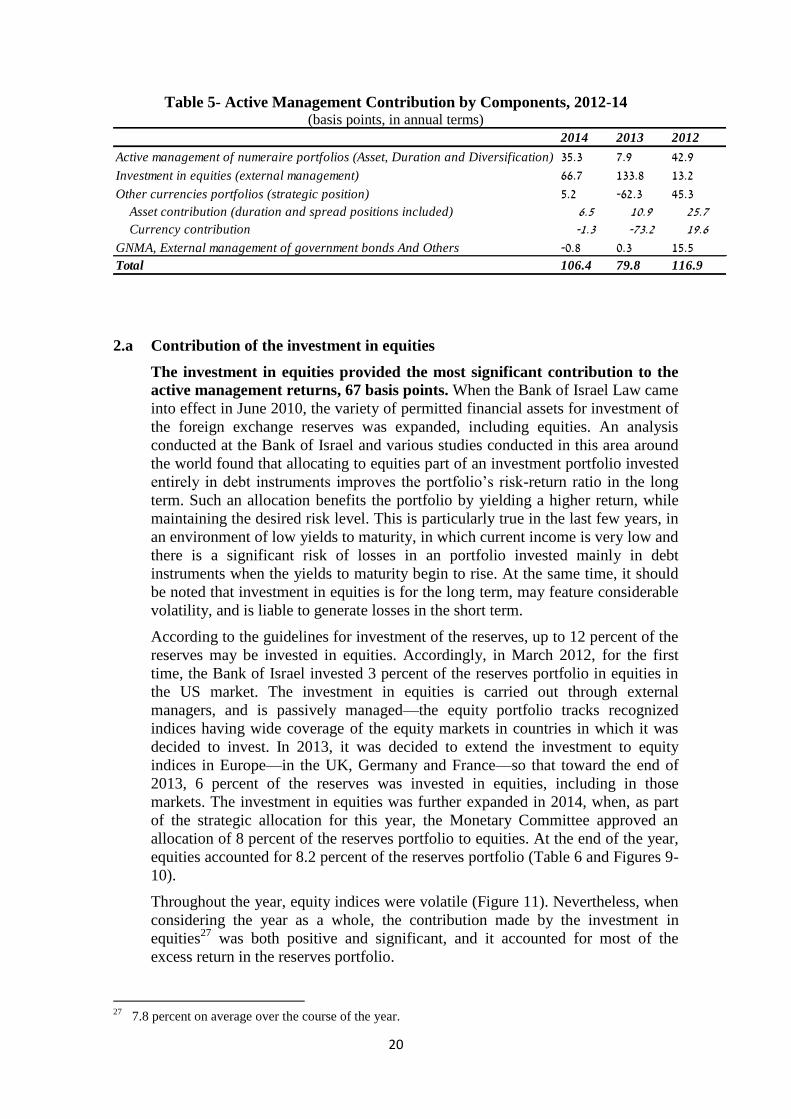

The active management contribution has several components, but two components in

particular contributed significantly to the excess return: the investment in equities,

which generated a high contribution of 67 basis points to the portfolio return, and the

active management of the portfolios in the numeraire currencies, which generated 35

basis points. The decision to diversify the assets in the reserves portfolio to durations

different than the benchmark’s was the most meaningful one in this component (Table

5).

26

Within the framework of the degrees of freedom granted to the reserves managers.

20

Table 5- Active Management Contribution by Components, 2012-14 (basis points, in annual terms)

2.a Contribution of the investment in equities

The investment in equities provided the most significant contribution to the

active management returns, 67 basis points. When the Bank of Israel Law came

into effect in June 2010, the variety of permitted financial assets for investment of

the foreign exchange reserves was expanded, including equities. An analysis

conducted at the Bank of Israel and various studies conducted in this area around

the world found that allocating to equities part of an investment portfolio invested

entirely in debt instruments improves the portfolio’s risk-return ratio in the long

term. Such an allocation benefits the portfolio by yielding a higher return, while

maintaining the desired risk level. This is particularly true in the last few years, in

an environment of low yields to maturity, in which current income is very low and

there is a significant risk of losses in an portfolio invested mainly in debt

instruments when the yields to maturity begin to rise. At the same time, it should

be noted that investment in equities is for the long term, may feature considerable

volatility, and is liable to generate losses in the short term.

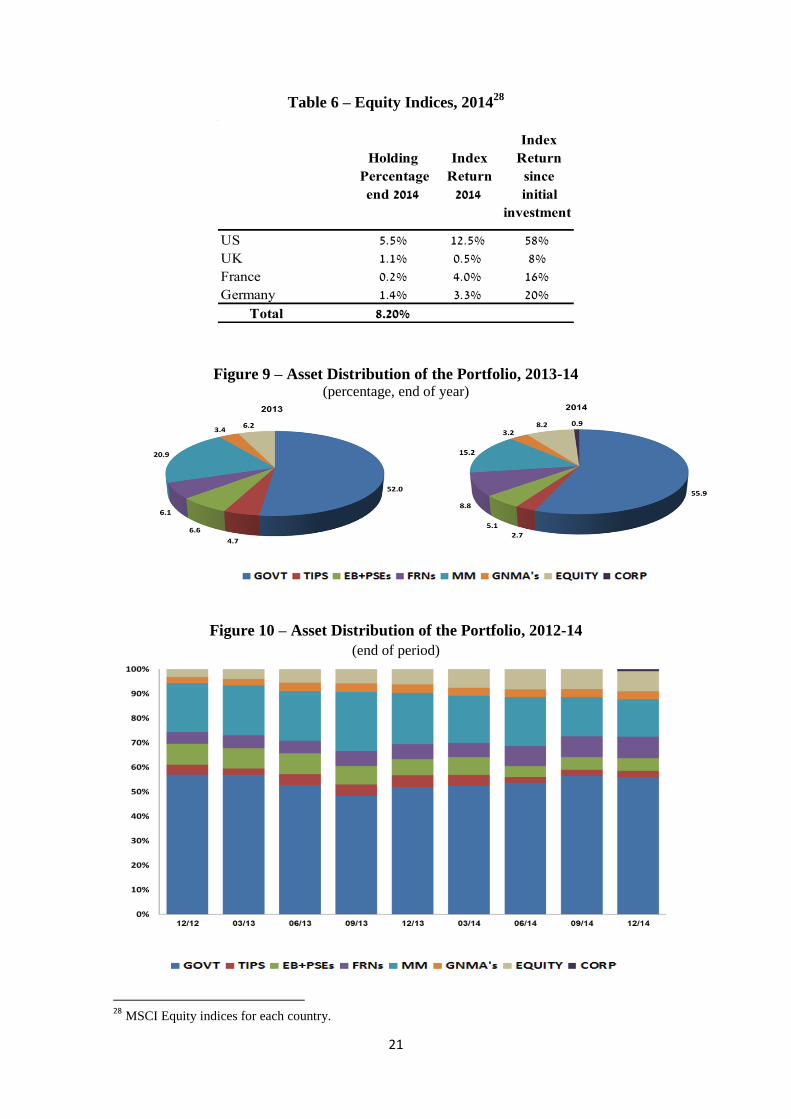

According to the guidelines for investment of the reserves, up to 12 percent of the

reserves may be invested in equities. Accordingly, in March 2012, for the first

time, the Bank of Israel invested 3 percent of the reserves portfolio in equities in

the US market. The investment in equities is carried out through external

managers, and is passively managed—the equity portfolio tracks recognized

indices having wide coverage of the equity markets in countries in which it was

decided to invest. In 2013, it was decided to extend the investment to equity

indices in Europe—in the UK, Germany and France—so that toward the end of

2013, 6 percent of the reserves was invested in equities, including in those

markets. The investment in equities was further expanded in 2014, when, as part

of the strategic allocation for this year, the Monetary Committee approved an

allocation of 8 percent of the reserves portfolio to equities. At the end of the year,

equities accounted for 8.2 percent of the reserves portfolio (Table 6 and Figures 9-

10).

Throughout the year, equity indices were volatile (Figure 11). Nevertheless, when

considering the year as a whole, the contribution made by the investment in

equities27

was both positive and significant, and it accounted for most of the

excess return in the reserves portfolio.

27

7.8 percent on average over the course of the year.

2014 2013 2012

Active management of numeraire portfolios (Asset, Duration and Diversification) 35.3 7.9 42.9

Investment in equities (external management) 66.7 133.8 13.2

Other currencies portfolios (strategic position) 5.2 -62.3 45.3 Asset contribution (duration and spread positions included) 6.5 10.9 25.7

Currency contribution -1.3 -73.2 19.6

GNMA, External management of government bonds And Others -0.8 0.3 15.5Total 106.4 79.8 116.9

21

Table 6 – Equity Indices, 201428

Figure 9 – Asset Distribution of the Portfolio, 2013-14 (percentage, end of year)

Figure 10 – Asset Distribution of the Portfolio, 2012-14

(end of period)

28

MSCI Equity indices for each country.

Index

Return

since

initial

investment

Index

Return

2014

Holding

Percentage

end 2014

58%12.5%5.5%US

8%0.5%1.1%UK

16%4.0%0.2%France

20%3.3%1.4%Germany

8.20%Total

22

Figure 11 – Equity Indices: US, UK, Germany and France, 2014

23

According to a large number of empirical findings that have been documented in

research, international diversification of investment in equities improves the risk-

return ratio. Although world markets have become more integrated in recent

years, international diversification of the investments is expected to improve the

portfolio’s risk-return ratio. This is confirmed by marked differences in the way

that the different markets reacted to the financial crisis and their behavior as they

emerged from the crisis.

Accordingly, as part of the strategic allocation for 2015, the Monetary Committee

decided to review the possible diversification of the investment in equities to other

markets—Japan, South Korea and Hong Kong—in addition to those of the

numeraire currencies.

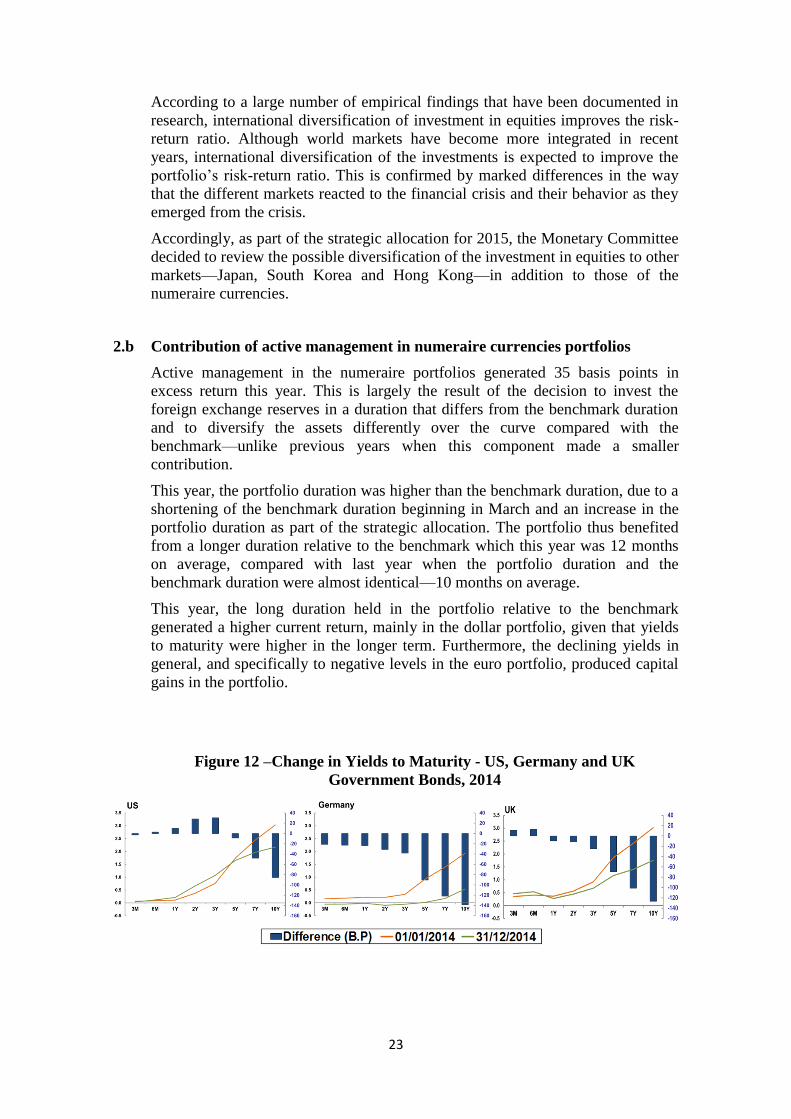

2.b Contribution of active management in numeraire currencies portfolios

Active management in the numeraire portfolios generated 35 basis points in

excess return this year. This is largely the result of the decision to invest the

foreign exchange reserves in a duration that differs from the benchmark duration

and to diversify the assets differently over the curve compared with the

benchmark—unlike previous years when this component made a smaller

contribution.

This year, the portfolio duration was higher than the benchmark duration, due to a

shortening of the benchmark duration beginning in March and an increase in the

portfolio duration as part of the strategic allocation. The portfolio thus benefited

from a longer duration relative to the benchmark which this year was 12 months

on average, compared with last year when the portfolio duration and the

benchmark duration were almost identical—10 months on average.

This year, the long duration held in the portfolio relative to the benchmark

generated a higher current return, mainly in the dollar portfolio, given that yields

to maturity were higher in the longer term. Furthermore, the declining yields in

general, and specifically to negative levels in the euro portfolio, produced capital

gains in the portfolio.

Figure 12 –Change in Yields to Maturity - US, Germany and UK

Government Bonds, 2014

24

Figure 13 – Yield Spreads, 2-5 years to maturity, 2014

(percent)

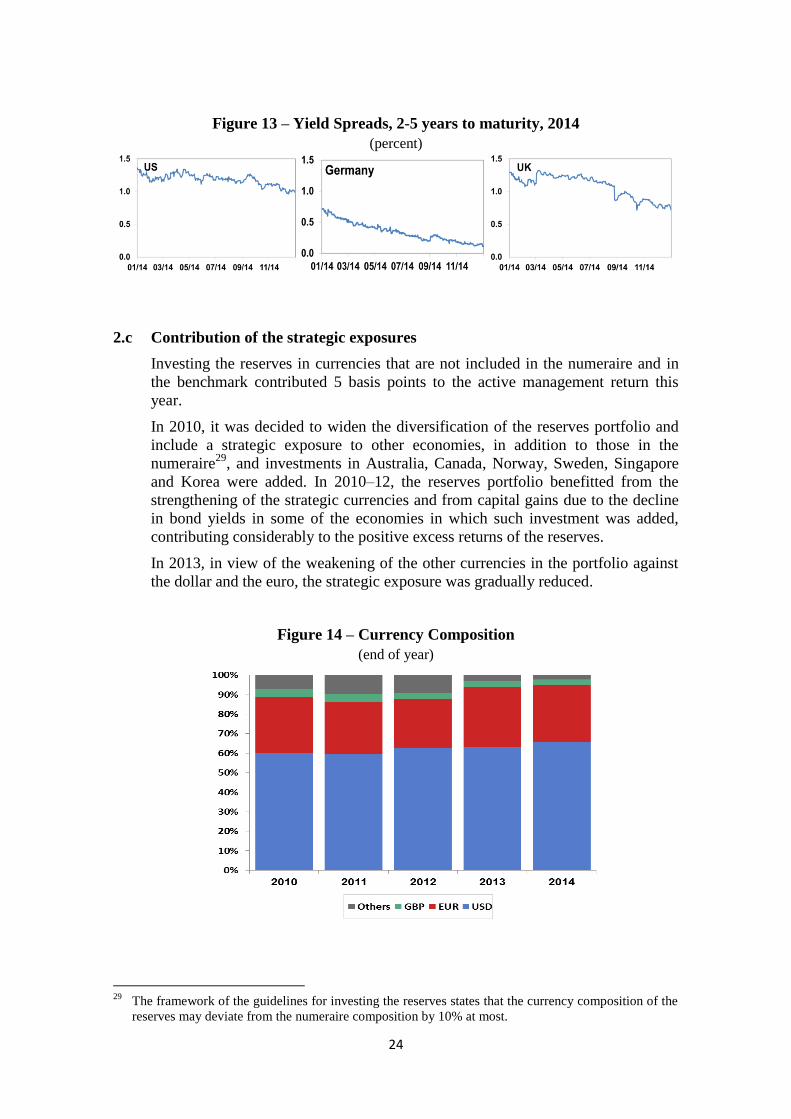

2.c Contribution of the strategic exposures

Investing the reserves in currencies that are not included in the numeraire and in

the benchmark contributed 5 basis points to the active management return this

year.

In 2010, it was decided to widen the diversification of the reserves portfolio and

include a strategic exposure to other economies, in addition to those in the

numeraire29

, and investments in Australia, Canada, Norway, Sweden, Singapore

and Korea were added. In 2010–12, the reserves portfolio benefitted from the

strengthening of the strategic currencies and from capital gains due to the decline

in bond yields in some of the economies in which such investment was added,

contributing considerably to the positive excess returns of the reserves.

In 2013, in view of the weakening of the other currencies in the portfolio against

the dollar and the euro, the strategic exposure was gradually reduced.

Figure 14 – Currency Composition

(end of year)

29

The framework of the guidelines for investing the reserves states that the currency composition of the

reserves may deviate from the numeraire composition by 10% at most.

25

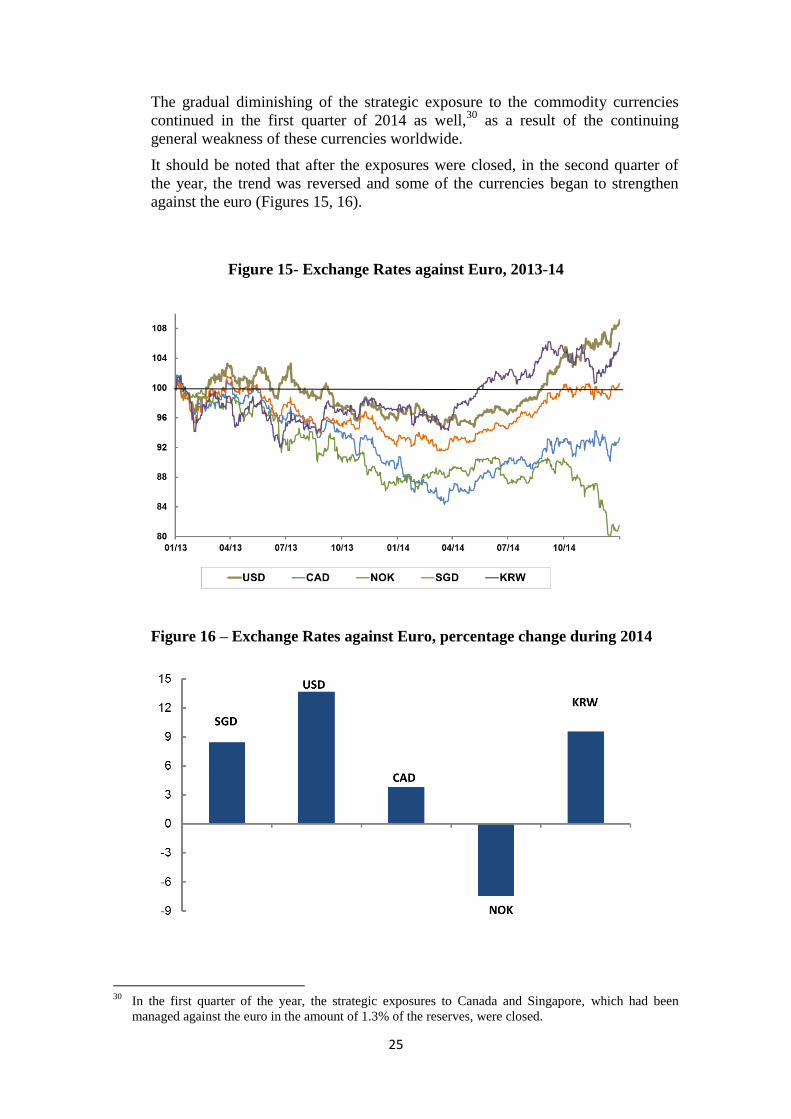

The gradual diminishing of the strategic exposure to the commodity currencies

continued in the first quarter of 2014 as well,30

as a result of the continuing

general weakness of these currencies worldwide.

It should be noted that after the exposures were closed, in the second quarter of

the year, the trend was reversed and some of the currencies began to strengthen

against the euro (Figures 15, 16).

Figure 15- Exchange Rates against Euro, 2013-14

Figure 16 – Exchange Rates against Euro, percentage change during 2014

30

In the first quarter of the year, the strategic exposures to Canada and Singapore, which had been

managed against the euro in the amount of 1.3% of the reserves, were closed.

26

In recent years, Asian markets have gained strength, and they seem to be playing a

more significant role in the global economy. In light of this, in 2014 it was

decided to increase the strategic exposure to these markets.

Table 7 – Average Currency Distribution of the Numeraire and the Portfolio

(2014, percentage)

Overall, during the year, the average share of the strategic exposures in the

portfolio remained low, at 2.2 percent of the reserves, similar to their share at the

end of the previous year31

(2.8 percent).

Figure 17 – Currency Composition, 2013-14

(end of year)

The active management of the strategic exposures added 5 basis points to the

excess return, in contrast to an addition of 57 basis points generated by the

cumulative investment in these positions from 2010 to 2013.

31

Following the process of reducing the strategic exposures, the average weight of the strategic

exposures in 2013 was 6.2% of the reserves, compared with 9.7% at the beginning of the year.

Portfolio Numeraire Deviation

USD 65.7 65.7 0.0

EUR 29.0 31.3 -2.3

GBP 3.0 3.0 0.0

NOK 1.2 1.2 2.5

KRW 0.7 0.7

CNH 0.5 0.5

CNY 0.1 0.1

OTHERS -0.2 -0.2

Total 100 100

Strategic

exposures

27

Table 8 – Strategic Exposures Summary, 2010-14

(percentage)

The positive contribution generated by the strategic exposures this year can be

attributed entirely to the asset management, which was slightly offset by a

currency loss. Yield curves in bond markets of the additional countries in which

the reserves were invested were higher than those in the benchmark bond markets,

and they were invested with a higher duration than that of the portfolios in the

numeraire currencies. The assets in these countries therefore yielded a higher

current return in the reserves portfolio, in addition to the capital gains generated

by the declining yields in these markets (Figure 18).

Figure 18 – Two-Year Yields to Maturity of Government Bonds of Various

Countries, 2014 (percentage)

Total Asset

Contribution

Currency

Contribution

0.470.030.442010

0.260.210.052011

0.460.260.22012

-0.620.11-0.732013

0.050.07-0.012014

0.620.68-0.05Total

28

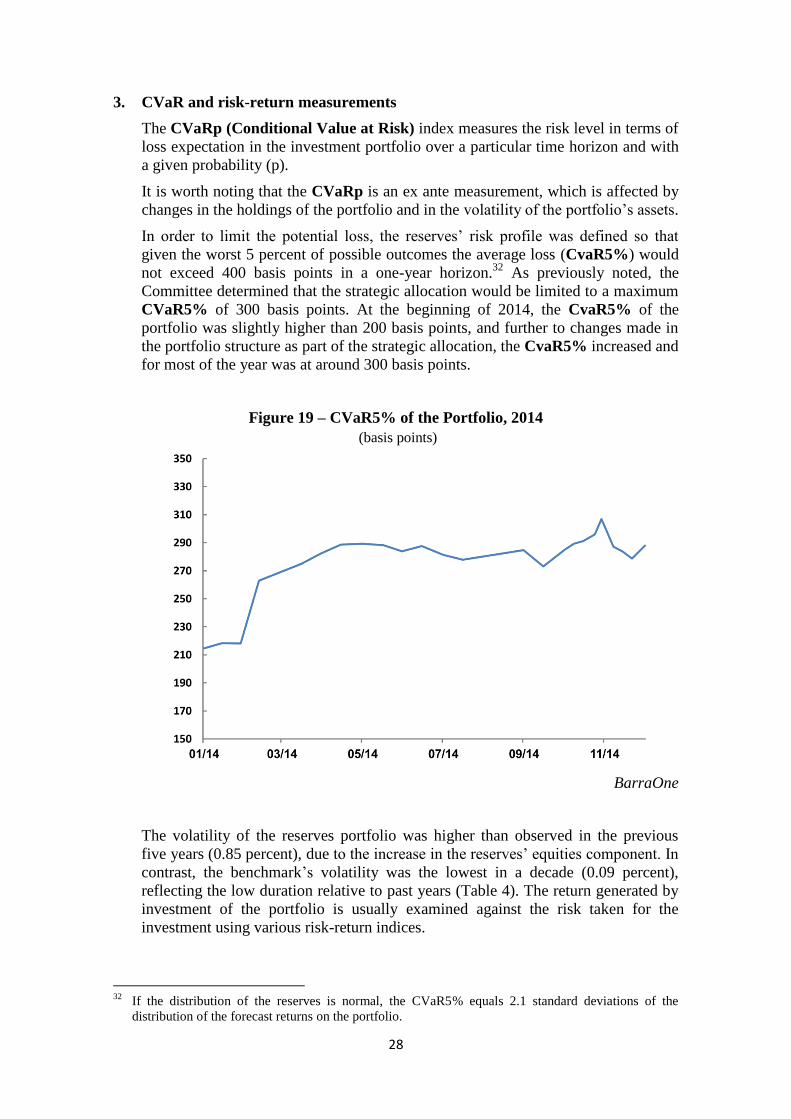

3. CVaR and risk-return measurements

The CVaRp (Conditional Value at Risk) index measures the risk level in terms of

loss expectation in the investment portfolio over a particular time horizon and with

a given probability (p).

It is worth noting that the CVaRp is an ex ante measurement, which is affected by

changes in the holdings of the portfolio and in the volatility of the portfolio’s assets.

In order to limit the potential loss, the reserves’ risk profile was defined so that

given the worst 5 percent of possible outcomes the average loss (CvaR5%) would

not exceed 400 basis points in a one-year horizon.32

As previously noted, the

Committee determined that the strategic allocation would be limited to a maximum

CVaR5% of 300 basis points. At the beginning of 2014, the CvaR5% of the

portfolio was slightly higher than 200 basis points, and further to changes made in

the portfolio structure as part of the strategic allocation, the CvaR5% increased and

for most of the year was at around 300 basis points.

Figure 19 – CVaR5% of the Portfolio, 2014

(basis points)

BarraOne

The volatility of the reserves portfolio was higher than observed in the previous

five years (0.85 percent), due to the increase in the reserves’ equities component. In

contrast, the benchmark’s volatility was the lowest in a decade (0.09 percent),

reflecting the low duration relative to past years (Table 4). The return generated by

investment of the portfolio is usually examined against the risk taken for the

investment using various risk-return indices.

32

If the distribution of the reserves is normal, the CVaR5% equals 2.1 standard deviations of the

distribution of the forecast returns on the portfolio.

29

The information ratio (IR) is generally used to examine the active management

contribution relative to the risk incurred to achieve it, and is equal to the ratio of the

excess return to its standard deviation. This year, the return on the portfolio was

higher than that of the previous year, and the risk level rose slightly—so that the IR

was slightly higher than the previous year and similar to the average for the past

decade (1.31).

Figure 20 –Ratio of the Active-Management Contribution to its Standard

Deviation (Information Ratio), 2005–14

Risk adjusted return calculated using the Modigliani & Modigliani measure

This measure is used to examine the portfolio’s return, adjusted for the risk of the

portfolio relative to the benchmark against which it is measured. The measure is

obtained by multiplying the portfolio’s Sharpe index by the standard deviation of

the benchmark return plus a risk-free rate.33

A comparison of the risk-adjusted return of the reserves portfolio with the return of

the benchmark against which the portfolio is measured shows that for most of the

last decade, active management of the reserves has been preferable: the portfolio’s

risk-adjusted return was higher than the benchmark return. This means that in most

of the last ten years, the ratio of return to the risk taken in active management was

preferable to the return obtained in passive management.

33 M2 =Rp−Rf

σp∗ σb + Rf

𝑹𝒑 Return of the portfolio; 𝝈𝒑 The standard deviation of the return of the portfolio; 𝝈𝒃 Standard

deviation of the benchmark return; 𝑹𝒇 The risk-free interest rate, calculated by weighting the risk-

free rate on the three numeraire currencies: dollar, euro and pound sterling. Based on the interest rate

on short-term deposits minus the TED spread.

30

Although the risk entailed in management of the portfolio was greater than in the

benchmark (as seen in the high standard deviation of the portfolio compared to the

benchmark), the excess return was greater than the additional risk taken, and

preferable to the return that would have been obtained by passive management

(remaining with the benchmark).

In contrast, this year, as in 2008 and 2011, the ratio shows that the benchmark

achieved a higher return relative to risk than this ratio in the portfolio. Although the

portfolio return was higher than the benchmark return in these years, the portfolio’s

risk-adjusted return was lower than the benchmark return. This finding confirms

that the increased return involved greater risk per unit of return—particularly this

year when the return produced by the benchmark was solid compared with the

minimal amount of risk taken to achieve it.

Figure 21 – Portfolio’s Risk Adjusted Return (Modigliani & Modigliani measure)

against the Benchmark’s Return, 2005-14

31

Appendix 1

Glossary

0.01 percent; one ten-thousandth. Basis point

A hypothetical portfolio constructed according to agreed-upon rules, which

is used as a yardstick for evaluating the performance of an investment

portfolio manager and as an anchor for the portfolio risk management.

Benchmark

portfolio

Zero-coupon securities that are sold at a discount, with an original term to

maturity of less than one year.

Commercial

paper (CP)

The exposure to the possibility of loss due to default on debt, whether of an

issuer, a financial institution or a country, or as a result of changes in the

market’s evaluation of the probability of such an event.

Credit risk

The exposure to the possibility of a loss as a result of a change in exchange

rates.

Currency risk

The rate of return obtained from multiplying the current values of all the

assets by the corresponding current rates of exchange of the currency or

basket of currencies.

Currency terms

(e.g., US dollar

terms)

Financial assets that are issued by foreign entities and which are

denominated in a foreign currency (including gold). They are owned

exclusively and managed by a central bank and are not pledged in any way.

Foreign

exchange

reserves

An agreement to buy or sell a particular type of asset, such as foreign

currency, at a predetermined price and on a predetermined future date.

Forward

Mortgage-backed securities that are issued by the Government National

Mortgage Association, which are fully guaranteed by the US government.

GNMA

Rate of change in the value of an asset or portfolio over a defined period. Holding-period

rate of return

The exposure to the possibility of a loss as a result of changes in the yield to

maturity.

Interest rate risk

The ability to realize assets immediately without a loss in value. Liquidity

An approximation of the sensitivity of a small change in the value of a debt

instrument, expressed as a percentage of its original value, to the change in

the yield to maturity (with the opposite sign) of the instrument. Measured in

units of time.

Modified

duration

A portfolio whose composition is identical to those of the benchmark. Neutral portfolio

32

A currency basket used for measuring the returns on the foreign exchange

reserves. See Section A.3 above.

Numeraire

The exposure to the possibility of a loss due to a system failure, human

error and the like.

Operational risk

The average duration of a portfolio of fixed income instruments (where the

duration of each asset is weighted according to its proportion of the

portfolio); a widely accepted measure used to estimate the portfolio’s

interest rate risk.

Portfolio

duration

The portfolio return adjusted to its risk relative to that of the benchmark

against which it is measured. Risk adjusted return is calculated by the

Modigliani and Modigliani measure, which is equal to the product of the

portfolio’s Sharpe Index and the standard deviation of the benchmark

return, plus a risk-free rate.

M2 =Rp−Rf

σp∗ σb + Rf

𝑹𝒑 − 𝒓eturn of the portfolio; 𝝈𝒑 − the standard deviation of the return of the

portfolio; 𝝈𝒃 −standard deviation of the benchmark return; 𝑹𝒇 − the risk-free

interest rate.

Risk adjusted

return

A portfolio in which the investor is not subject to gains or losses. Risk-free

portfolio

An asset which is not included in the benchmark. The yield spread of this

asset is measured as the difference between its yield to maturity and that of

an asset or benchmark with similar characteristics.

Spread asset

A statistical measure used to quantify the dispersion of a distribution

around its expected value. Often used as a measure to quantify the exposure

to uncertainty. See also volatility.

Standard

deviation

An intended deviation from investment characteristics of a portfolio vis-à-

vis the benchmark, managed as a long term exposure.

Strategic

exposure

The difference between the yield to maturity of a government bond and the

fixed interest rate that is paid from one party to the other in an interest rate

swap for a similar period.

Swap spread

Treasury Inflation-Protected Security; a bond issued by the US government

that is indexed to the CPI in the US.

TIPS

Debt instruments issued by the government. Treasury bill,

note or bond

The standard deviation (see definition in this glossary) of the distribution of

holding-period rates of return of a financial asset, such as a security or

Volatility

33

portfolio, over a defined time period (a day, a week, etc.).

A curve representing the yields to maturity of bonds with similar

characteristics (such as the bonds of a particular country in local currency)

and different maturities.

Yield curve

The difference between yields to maturity of two debt instruments. Yield spread

The holding-period rate of return, in annual terms, which would be obtained

from holding a debt instrument until its final redemption, if it was possible

to invest all of its cash flow at the same rate of return until that date.

Synonymous term: internal rate of return.

Yield to maturity

34

Appendix 2

Foreign Exchange Reserves: Investment Policy Guidelines

Foreign Exchange Reserves: Investment Policy Guidelines34

In effect from January 7, 2014

In accordance with Section 40(b) of the Bank of Israel Law, 5770-2010, the Monetary

Committee is to establish the guidelines for the investment policy of the foreign exchange

reserves.

1. Basic guidelines derived from the goals of holding the reserves

The investment policy of the reserves portfolio is based on the main goal of achieving the

Bank of Israel's objectives and proper fulfillment of its functions as they are detailed in the

Bank of Israel Law. Subject to that, the investment policy is also based on the following

goals:

a) Maintaining the purchasing power of the reserves: This principle is interpreted as

preserving the value of the reserves in terms of measurement currency chosen by the

Bank—the numeraire (see 3 below).

b) Managing the reserves with a high level of liquidity: A large part of the reserves are

to be invested in assets that can be liquidated rapidly at short notice and without

negatively impacting their value. The precise level of liquidity is to be increased to the

extent that the actual level of reserves relative to the desired level is low (5(e) below).

c) Achieving an appropriate return on the reserves portfolio, at an acceptable level of

risk, to the extent that it does not negatively impact the achievement of the previous

goals (see 4 below).

2. The division of work between the Monetary Committee, the Foreign Currency

Committee, and the Markets Operations Department

In implementing Section 40(b) of the Bank of Israel Law, the Committee made a distinction

between establishing the guidelines and periodic monitoring, and setting the detailed

instructions for the day to day management of the portfolio.

The Monetary Committee will set the guidelines, in consultation with the Minister of Finance as

established by law, will update the guidelines to the extent necessary, and will monitor the

implementation of the investment policy by the Markets Operations Department.

The Foreign Currency Committee Committee—an internal Bank of Israel committee headed by

the Governor—will translate the guidelines into the detailed foreign exchange reserves

investment policy.

34

The characteristics of the reserves portfolio are reported to the public in an annual report published on

the Bank of Israel website.

35

The Market Operations Department will implement the investment policy, within the

framework of degrees of freedom which will be set periodically by the Monetary Committee

and the Foreign Currency Committee, and will report to the Monetary Committee and the

Foreign Currency Committee on a quarterly basis on the implementation of the policy:

developments in international markets and their impact on the management of the reserves, the

investment decisions reached by the Department, the portfolio's rate of return, and the financial

and other risks to which the portfolio is exposed.

The Market Operations Department will advise the Monetary Committee and the Foreign

Currency Committee on fulfilling their functions, through position papers and suggestions for

discussion in the Committees.

The Monetary Committee will approve and update periodically the division of authorities

regarding the investment policy of the foreign exchange reserves.

3. The measurement currency for the holding rate of return on the foreign exchange

reserves and the principles for its determination

The measurement currency for the holding rate of return on the reserves—hereinafter, the

numeraire—is a basket of currencies and its composition allocation35

is decided by the

Monetary Committee. The allocation of the numeraire is set according to principles which

reflect the goals of holding the reserves.

The principles according to which the composition of the numeraire is set are:

a) The currency composition of actual imports, and of imports expected in an emergency

situation

b) The composition of the short and medium term external debt

c) Assessments regarding the liquidity of the various currencies in which investment is

possible.

The composition of the numeraire is also examined from the perspective of the currency

composition of foreign exchange reserves portfolios of all central banks of countries that are

IMF members, as reported by the IMF.

35

The numeraire is defined in terms of units of currency (i.e., X dollars, Y euro, and Z pound sterling).

The ratio between the currency units (in the above example, X:Y:Z) is determined by the currency

composition of the portfolio (in the above example, % of dollars in the portfolio, % euro, and % pound

sterling), which is set by the Committee and the exchange rates of the numeraire currencies at the time of

the decision.

36

The composition of the numeraire will be set at the end of each year by the Monetary

Committee, on the basis of the Market Operations Department’s recommendation, in

accordance with changes in domestic and global market conditions. If there are significant

changes in one or more of principles (a)–(c), the composition of the numeraire will be brought

to discussion by the Monetary Committee.

The reserves portfolio holding rate of return is measured in terms of the numeraire, so that the

currency basket which makes up the numeraire is seen by the reserves portfolio managers as a

risk-free currency composition.

4. The risk profile

The risk profile determines the maximum level of risk that the Monetary Committee is willing

to accept in order to achieve the goals of holding the reserves. In establishing the risk profile,

scenario analysis and a range of analytical tools to measure risk, such as VaR, CVaR, and others

should be used. The risk profile is to be set by the Committee on a periodic basis in accordance

with the changing conditions in the global capital markets.

The risk profile will be set so that given the worst 5 percent of outcomes, the average loss will

not be greater than 400 basis points over a 1-year horizon.

5. The rules for managing the financial risks of the reserves

The rules for managing the financial risks to which the reserves are exposed, and their asset

allocation, are to be set in accordance with the goals of the investment policy of the reserves

(Section 1 above) and subject to the risk profile set by the Monetary Committee (Section 4). The

asset allocation of the foreign exchange reserves will be approved at least once a year by the

Monetary Committee.

a) The types of assets approved for use in managing the reserves are:

1. Bonds (including bonds with fixed interest, with variable interest, and CPI-indexed

bonds)

2. Mortgage-backed securities (MBS) and asset-backed securities (ABS), a maximum of

6% of total reserves

3. Tradable Certificates of Deposit (CDs)

4. Fixed term deposits

5. Commercial Paper (CP)

6. Equities, a maximum of 12% of total reserves

7. Derivatives whose underlying asset is permitted for investment.

37

b) Management against a benchmark

Control over most features of the financial risk of the reserves is anchored in their

management against a system of benchmarks. The rules for managing the financial risks of

the reserves generate the currency allocation of the benchmarks, the features of their price

risk (such as duration) in each currency, and the asset types included in it. The investment

returns of the portfolio managers are measured against these benchmarks.

c) Currency risk:

The currency exposure of the reserves is set by:

1) The composition of the numeraire.

2) Strategic currency positions relative to the composition of the numeraire: The extent of the

strategic currency positions is limited to 10 percent of total reserves. The composition and

amounts of the positions will be set by the Monetary Committee.

3) Short and medium term currency positions relative to the composition of the numeraire:

Their amount is limited to 2 percent of the total reserves. The composition and amounts of

the positions will be set by the Market Operations Department.

d) Credit risk:

In order to limit the credit risk inherent in day-to-day management of the reserves portfolio,

the Monetary Committee set the following rules:

1. Investment is permitted in the currency of countries for which their major credit rating

category is at least A. Investment in countries for which their credit rating group is BBB

requires the specific authorization of the Monetary Committee.

2. Investment in bonds and commercial paper issued by governments, or with government

guarantees, is permitted if their major rating category is at least BBB. Investment in the

BBB major rating category is limited to 1 percent of total reserves. Investment in such

assets, if their major credit rating category is BBB, requires the specific authorization of the

Monetary Committee.

3. Investment in bonds of public sector entities (PSE) is limited to a maximum of 15 percent of

total reserves, and only in bonds those whose major credit rating category is at least A.

Investment in such assets, if their major credit rating category group is below AA, is limited

to 1 percent of total reserves.

4. Investment in corporate bonds is limited to 6 percent of total reserves, and only in bonds

whose major credit rating category is at least BBB.

38

5. Investment in bonds and deposits of international financial institutions is limited to 15

percent of the reserves.

6. The exposure of the reserves to the international banking system should not be greater than

10 percent of total reserves, and that is only to banks whose major credit rating category is

at least A. Activity with banks and brokers whose major credit rating category is BBB is

limited to DVP36

(delivery versus payment) alone.

e) Liquidity risk:

In order to provide an immediate response to the financial problems which arise during

emergencies, a large portion of the reserves should be invested in assets that can be

liquidated in large amounts at short notice and without negatively impacting their

realization value.

The assets in which the reserves are invested are classified into 3 levels of liquidity:

1. Assets that can be realized within a week without negatively impacting their realization

value.

2. Assets that can be realized within a month without negatively impacting their

realization value.

3. Assets that can be realized within six months without negatively impacting their

realization value.

There is a minimum level of investment in the two highest liquidity levels, and there is a

maximum threshold for the third level. Classification into the various liquidity levels can

change due to changes in market conditions. In order to meet the liquidity demands, the

Committee established that at least 45 percent of the total reserves are to be invested in

government bonds.

f) Active management and compliance rules:

The reserves portfolio is actively managed within the framework of limited and well defined

degrees of freedom, as long as the investment policy adheres to the guidelines.

6. The nonfinancial risks inherent in managing the reserves

In determining the investment policy for the reserves, there must be taken into account the

exposure of the Bank and of the portfolio to the various nonfinancial risks inherent in investing

the reserves—reputation risk, legal risk, political risk, operational risk, and so forth.

7. Measuring returns and reporting them

The reserves are managed with transparency. The Market Operations Department shall report

periodically to the Monetary Committee (see 2 above) on the amount of the reserves and

36

DVP activity is when the payment and the asset are transferred between the sides at the same time and

thus the credit risk in such activity is essentially zero.

39

changes in them, the currency composition, changes in currency positions, the asset allocation,

portfolio duration, country exposure, credit risk, liquidity risk, and the return on the portfolio

and its various components. The report should include an analysis of the current developments

in the financial markets and their effect on the management of the reserves.

40

Appendix 3

Principles for Determining the Desired Level of Foreign Exchange

Reserves

1. The appropriate level of foreign exchange reserves as an indicator of the economic

strength of the country

Countries hold foreign exchange reserves for three main purposes:

A. To enable the central bank to intervene in the foreign exchange market in circumstances

in which (1) the exchange rate deviates from the range that is consistent with the economy’s

fundamental equilibrium; or (2) the foreign exchange market is not functioning adequately

(market failure);

B. To enable the central bank to operate in the foreign exchange market in order to

moderate the effect of large capital flows from either foreign or local residents, which are liable

to undermine the stability of the financial markets, and thus negatively impact the stability of

the economy as a whole (a specific case of A);

C. To allow for the provision of sufficient foreign currency to the economy in an

emergency situation (such as a war or a strong earthquake). In such circumstances, there will be

a need to increase imports rapidly and by a significant amount in order to deal with the