Investment Newsletter - July 2014

3

Investment Newsletter July 2014 By Mike Deverell Investment Manager Equilibrium Asset Management LLP (a limited liability partnership) is authorised and regulated by the Financial Conduct Authority. Equilibrium Asset Management is entered on the Financial Services Register under reference 452261. The FCA regulates advice which we provide on investment and insurance business; however it does not regulate advice which we provide purely in respect of taxation matters. Copyright Equilibrium Asset Management LLP. Not to be reproduced without permission. Markets Banking on the Fed We have noted several times before that markets are being increasingly driven by central banks. Monetary policy is one of the biggest risks to both economic growth and to investment portfolios. If they get things only slightly wrong, it could have a big effect. In the UK, we expect interest rates to increase in the relatively near future, late this year or more likely early next year. However, in our view, more important than the timing of the increase is the pace at which they rise. When rates do increase they will probably do so incredibly slowly. Base rate is currently at 0.5% pa and we expect that when it starts to go up it will probably increase in steps of 0.25%, perhaps leaving a six month gap after the first increase and maybe slightly shorter gaps after that. If rates were to increase on 1 January 2015, we therefore think that by January 2016 they may be at 1% or 1.25%, still very low by historical standard. There are many dangers to increasing rates too quickly. An obvious one is the number of people on variable rate mortgages who have grown used to ultra-low repayments. It might not take huge rate hikes for some people to struggle with repayments. Central bankers are trying to give as much guidance as possible so as not to shock the markets. In the US, the Federal Reserve has now said that quantitative easing will most likely end in October. It is likely that rates would not be increased for perhaps 6 months after QE ends. Whilst forward guidance is helpful in a number of ways, there is a danger that markets may have become too

-

Upload

equilibrium-asset-management-llp -

Category

Documents

-

view

212 -

download

0

description

Equilibrium's monthly investment newsletter, written by the investment team

Transcript of Investment Newsletter - July 2014

Investment Newsletter July 2014

By Mike DeverellInvestment Manager

Equilibrium Asset Management LLP (a limited liability partnership) is authorised and regulated by the Financial Conduct Authority. Equilibrium Asset Management is entered on the Financial Services Register under reference 452261. The FCA regulates advice which we provide on investment and insurance business; however it does not regulate advice which we provide purely in respect of taxation matters. Copyright Equilibrium Asset Management LLP. Not to be reproduced without permission.

Markets Banking on the FedWe have noted several times before that markets are being increasingly driven by central banks.

Monetary policy is one of the biggest risks to both economic growth and to investment portfolios. If they get things only slightly wrong, it could have a big effect.

In the UK, we expect interest rates to increase in the relatively near future, late this year or more likely early next year. However, in our view, more important than the timing of the increase is the pace at which they rise.

When rates do increase they will probably do so incredibly slowly. Base rate is currently at 0.5% pa and we expect that when it starts to go up it will probably increase in steps of 0.25%, perhaps leaving a six month gap after the first increase and maybe slightly shorter gaps after that.

If rates were to increase on 1 January 2015, we therefore think that by January 2016 they may be at 1% or 1.25%, still very low by historical standard.

There are many dangers to increasing rates too quickly. An obvious one is the number of people on variable rate mortgages who have grown used to ultra-low repayments. It might not take huge rate hikes for some people to struggle with repayments.

Central bankers are trying to give as much guidance as possible so as not to shock the markets. In the US, the Federal Reserve has now said that quantitative easing will most likely end in October. It is likely that rates would not be increased for perhaps 6 months after QE ends.

Whilst forward guidance is helpful in a number of ways, there is a danger that markets may have become too

Long term clients know that we are careful about the way we describe different portfolios or parts of portfolios in terms of risk.

For example, we break down equities into several different risk “buckets”. For overseas equity we break the world down into two main categories. Global Established invests in developed markets like Europe, North America and Japan, and Global Speculative invests in emerging economies.

Both of these portfolios have currency risk as they invest outside of the UK. Global Established should in theory have low political risk whereas Global Speculative funds might be affected by less stable governments as well as having less developed economies. We use the term “speculative” to demonstrate the amount of risk in these types of investment.

Within the UK we use two further risk buckets. UK Dynamic is our more aggressive UK portfolio which we’d expect to outperform generally in a rising market. However, if equities fall it quite possibly could fall more than the market.

By contrast, what we call UK Large Companies is our more conservative UK equity portfolio. This can underperform in a strongly rising market but will tend to do better in flatter markets and fall less than the market when it is going down.

complacent. Volatility in both equity and bond markets has been incredibly low of late, at least until the past few days. This in itself is a concern, because only a relatively small surprise such as a sooner than expected rate hike, could have a significant impact on markets.

It should also be noted that central banks might be forced to increase rates sooner or more steeply than they are indicating. For example, if they become worried about an over-exuberant economy, bubbles in the housing market, or a return of inflation. This isn’t something we think is especially likely, but we must always be mindful of what’s possible as well as what’s likely!

We continue to be underweight fixed interest and the funds we do hold in portfolios tend to have low sensitivity to interest rate increases. We believe this is important in an asset class where rate movements can have a big effect.

Whilst we still think there is value in equity markets, we do expect the recent increase in volatility could continue. As always, we hope to use this to our advantage and we may look to buy on any significant market dips.

The funds we hold tend to aim for a higher level of income than the market since this is one way of achieving stability. With these funds, even if markets go down we should still receive a reasonable dividend. They tend to invest in profitable and stable companies and there is usually a bias towards large companies.

However, to achieve the behaviour that we want it doesn’t actually matter whether we hold a large company or a small one. If the stocks have low volatility and preferably pay a decent dividend yield, then the size of the company is of low importance.

As a result, we have decided to use a new term to describe this part of portfolio, UK Conservative Equity. This doesn’t mean we invest in companies that support the Tory Party! It also doesn’t mean the portfolio can’t fall in value but we would normally expect it to be less volatile than the FTSE.

At present around 50% of this part of portfolios is in the FTSE 100 and 75% of it is in the top 350 stocks listed on the London Stock Exchange. It therefore is still largely invested in big companies.

We also have a third category of UK funds called UK All Companies. This is designed to reflect the market return which we do by investing in a low cost FTSE Allshare tracker.

Our UK Conservative Equity portfolio we would expect to provide returns similar to the Allshare in the long run but with lower volatility. UK Dynamic we hope should outperform over the long term although the ride could be bumpier.

By allocating between the three areas as appropriate we believe we can enhance returns whilst keeping risk in check.

Investment Newsletter July 2014

Markets Banking on the Fed cont’d

UK Conservative Equity

Equilibrium Asset Management LLP (a limited liability partnership) is authorised and regulated by the Financial Conduct Authority. Equilibrium Asset Management is entered on the Financial Services Register under reference 452261. The FCA regulates advice which we provide on investment and insurance business; however it does not regulate advice which we provide purely in respect of taxation matters. Copyright Equilibrium Asset Management LLP. Not to be reproduced without permission.

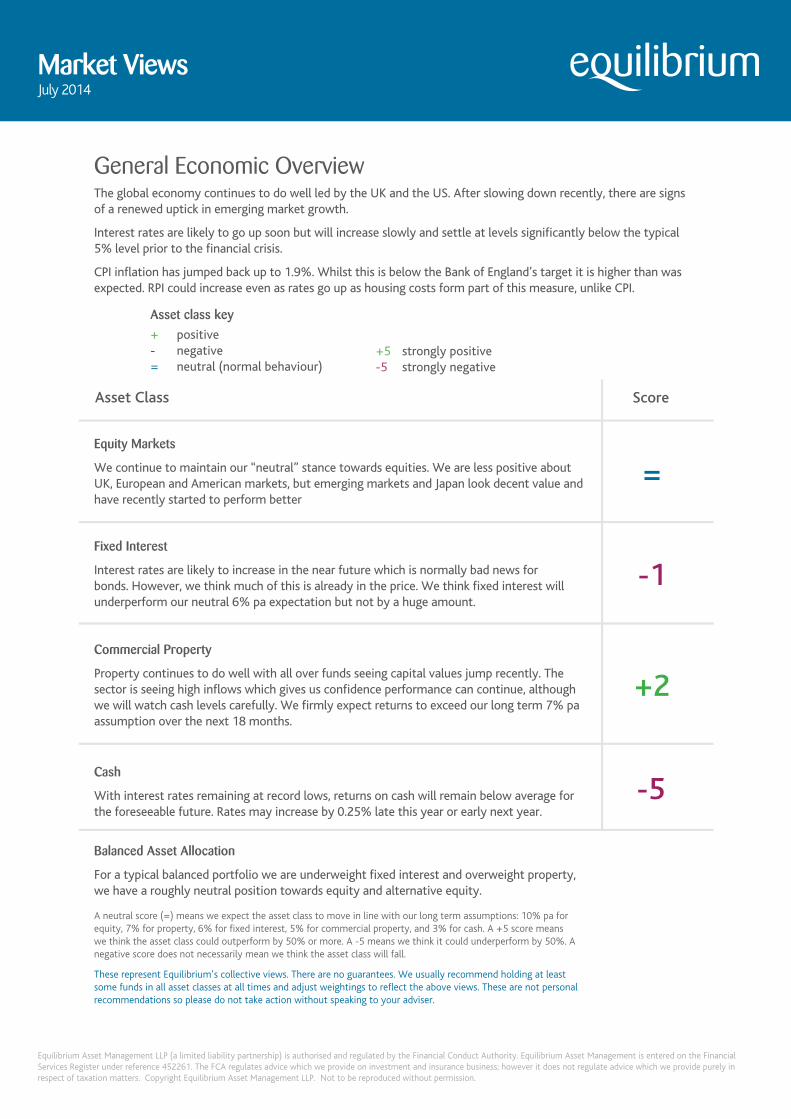

General Economic OverviewThe global economy continues to do well led by the UK and the US. After slowing down recently, there are signs of a renewed uptick in emerging market growth.

Interest rates are likely to go up soon but will increase slowly and settle at levels significantly below the typical 5% level prior to the financial crisis.

CPI inflation has jumped back up to 1.9%. Whilst this is below the Bank of England’s target it is higher than was expected. RPI could increase even as rates go up as housing costs form part of this measure, unlike CPI.

Equity Markets

We continue to maintain our “neutral” stance towards equities. We are less positive about UK, European and American markets, but emerging markets and Japan look decent value and have recently started to perform better

Fixed Interest

Interest rates are likely to increase in the near future which is normally bad news for bonds. However, we think much of this is already in the price. We think fixed interest will underperform our neutral 6% pa expectation but not by a huge amount.

Commercial Property

Property continues to do well with all over funds seeing capital values jump recently. The sector is seeing high inflows which gives us confidence performance can continue, although we will watch cash levels carefully. We firmly expect returns to exceed our long term 7% pa assumption over the next 18 months.

Cash

With interest rates remaining at record lows, returns on cash will remain below average for the foreseeable future. Rates may increase by 0.25% late this year or early next year.

Balanced Asset Allocation

For a typical balanced portfolio we are underweight fixed interest and overweight property, we have a roughly neutral position towards equity and alternative equity. A neutral score (=) means we expect the asset class to move in line with our long term assumptions: 10% pa for equity, 7% for property, 6% for fixed interest, 5% for commercial property, and 3% for cash. A +5 score means we think the asset class could outperform by 50% or more. A -5 means we think it could underperform by 50%. A negative score does not necessarily mean we think the asset class will fall.

These represent Equilibrium’s collective views. There are no guarantees. We usually recommend holding at least some funds in all asset classes at all times and adjust weightings to reflect the above views. These are not personal recommendations so please do not take action without speaking to your adviser.

=

-1

+2

-5

Asset class key+ positive - negative = neutral (normal behaviour)

+5 strongly positive-5 strongly negative

Score

Equilibrium Asset Management LLP (a limited liability partnership) is authorised and regulated by the Financial Conduct Authority. Equilibrium Asset Management is entered on the Financial Services Register under reference 452261. The FCA regulates advice which we provide on investment and insurance business; however it does not regulate advice which we provide purely in respect of taxation matters. Copyright Equilibrium Asset Management LLP. Not to be reproduced without permission.

Asset Class

Market Views July 2014