Investment Management - A Leading UK University · Investment Management ... – Elton, E.J.,...

18

1 Investment Management Professor Giorgio Valente University of Leicester MSc Financial Economics http://www.le.ac.uk/users/gv20/teaching.htm http://www.le.ac.uk/ec/teach/ec7092/index.html Outline • Introduction • Market instruments, risk and return • Portfolio analysis and diversification • Implementation of Portfolio theory (CAPM, APT) • Equities • Performance measurement • Interest rate theory and pricing of bonds • Managing equities and bond portfolios • Derivatives • International portfolio management (FX) • Introduction to behavioural finance

Transcript of Investment Management - A Leading UK University · Investment Management ... – Elton, E.J.,...

1

Investment Management

Professor Giorgio ValenteUniversity of Leicester

MSc Financial Economics

http://www.le.ac.uk/users/gv20/teaching.htm

http://www.le.ac.uk/ec/teach/ec7092/index.html

Outline

• Introduction

• Market instruments, risk and return

• Portfolio analysis and diversification

• Implementation of Portfolio theory (CAPM, APT)

• Equities

• Performance measurement

• Interest rate theory and pricing of bonds

• Managing equities and bond portfolios

• Derivatives

• International portfolio management (FX)

• Introduction to behavioural finance

2

Preliminary information

• Prerequisites: basic mathematics, statistics and economics (i.e. means, variances and linear regression)

• Readings:– Bodie, Kane and Marcus (2008), Investments, 7th edition,

McGraw-Hill– Elton, E.J., Gruber, M.J., Brown, S.J. and Goetzmann,

W.N. (2003), Modern Portfolio Theory and Investment Analysis, 6th edition, Wiley

• Mondays: 3 hours (lectures + classes) • Evaluation:

Investment project : 30%Final Examination : 70%

Preliminary information

• Study groups: The investment project is the result of a collaborative effort done in study group. Groups of no more than 4 members must be formed. Send me by email the composition of each group. I will allocate the students who do not belong to any group.

• Feedbacks and office hours: Mondays 10:45am –12:45pm or by appointment. Make use of them. Ask questions and clarifications if what I said is not clear to you.

3

Road Map

• Investment Management

• Financial instruments

• Financial markets and financial agents

• Risk and return (historical perspective)

• Risk and expected returns

• Risk aversion and investors’ preferences

What is Investment Management?

• Investment Management (IM) involves:

– constructing a portfolio of assets which best matches the investor’s preferences and needs

– evaluating the performance of this portfolio

– adjusting the composition of the portfolio, as necessary

• Hence: IM is broader than Security Analysis, which only focuses on pricing of individual securities

4

The investment setting

• What is an investment?

• How do individuals invest?

• How do investors measure the rate of return on an investment?

• How do investors measure the risk related to alternative investments?

• How do expected rates of return and attitude toward risk affect investment choices?

Asset allocation

• Asset allocation is the key activity in IM, that is how much of an investor’s wealth should be invested in each of the following financial instruments:

– cash

– equities

– bonds

– properties

– derivative securities

5

Financial instruments

• Financial security

– legal contract

– confers the right to receive future benefits

– usually traded in organised markets

• Classification

– cash products versus derivative securities

– debt versus equities

• Sub-classification

– by issuer (e.g. public versus private)

– by maturity

Financial securities: classification

6

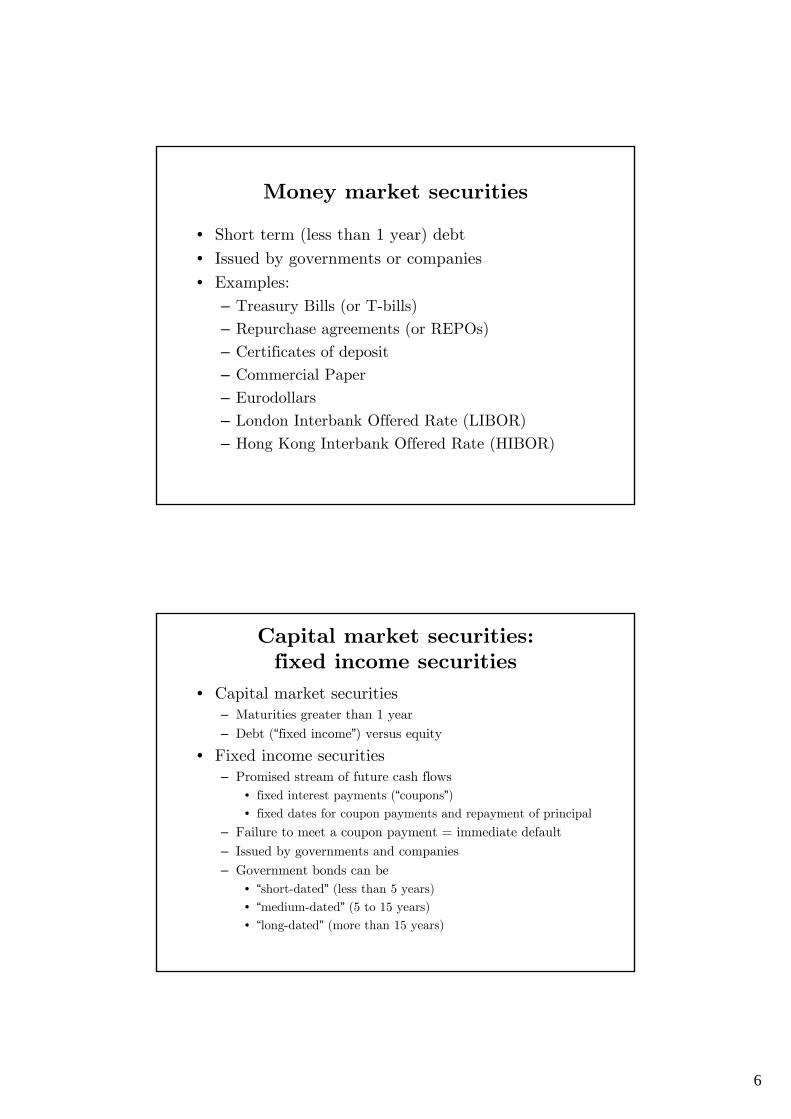

Money market securities

• Short term (less than 1 year) debt

• Issued by governments or companies

• Examples:

– Treasury Bills (or T-bills)

– Repurchase agreements (or REPOs)

– Certificates of deposit

– Commercial Paper

– Eurodollars

– London Interbank Offered Rate (LIBOR)

– Hong Kong Interbank Offered Rate (HIBOR)

Capital market securities: fixed income securities

• Capital market securities– Maturities greater than 1 year

– Debt (“fixed income”) versus equity

• Fixed income securities– Promised stream of future cash flows

• fixed interest payments (“coupons”)• fixed dates for coupon payments and repayment of principal

– Failure to meet a coupon payment = immediate default

– Issued by governments and companies

– Government bonds can be

• “short-dated” (less than 5 years)

• “medium-dated” (5 to 15 years)

• “long-dated” (more than 15 years)

7

Capital market securities: equities

• Ownership claim on the assets and earnings of a company

• Unique feature is limited liability

– if company goes bankrupt, investor’s loss is limited to his original stake in the company

Derivative securities

• Value derived from the value of some underlying asset

(i.e. equity, bonds, currencies)

– Futures, options

• Options are side-bets on the performance of individual securities

– buying/selling options on a particular stock does not affect that company’s cashflows

– no change in the number or type of outstanding securities

• Companies can issue their own contingent claims

– warrants (that allow the holder to purchase common stock from the corporation at a set price for a period of time) and convertibles (that allow the holder to convert an instrument into common stock under specified conditions)

– if these options are exercised, company attributes (such as the number of outstanding shares) do change

8

Indirect investment

• Mutual Funds

– “open-end” funds (Unit Trusts)

• “Units” are bought from (sold to) the Mutual Fund directly

• “Units” are bought (sold) at the net asset value of the Fund, which is determined daily

• Fund manager may charge a fee when the investor buys (“front-end load”) and sells (“back-end load”)

Indirect investment (cont’d)

– “closed-end” funds (Investment Trusts)

• Pre-determined number of shares in the Fund issued initially

• Net proceeds of sale of these shares is invested in equities and/or bonds

• Shares in the Fund are traded on an Exchange

• Owning shares in a “closed-end” fund is similar to owning shares in a company, except the assets of the “company” are the equities and bonds which the Fund owns

• Unlike “open-end” funds, shares in a “closed-end” fund can sell at a premium or discount to the net asset value

9

How do individuals invest?

• Passive management

– “buy and hold” a well-diversified portfolio of assets

• Active management

– security selection attempts to identify securities that have been mispriced - e.g. “buy low and sell high”

– market timing tilts the portfolio composition in favour of (away from) equities when the investor is bullish (bearish) about the stock market

• Portfolio insurance

– use derivative securities to “manage” risk

The major players

• In general, institutional investors:

– pension funds

– insurance companies

• and foreign investors

Source: own calculations, various

sources10.5%2.1%Other

0.1%1.5%Public sector

0.9%5.1%Industrial and comm.

32.1%7.0%Overseas

14.3%54.0%Individuals

2.1%1.3%Banks

1.8%11.3%Investment trusts

1.6%1.3%Unit trust

19.9%10.0%Insurance companies

15.6%6.4%Pension funds

20031963

10

The major players (cont’d)

• How do institutional investors allocate their assets?

Source: own calculations, various sources

Other assets

Overseas securities

Domestic companies securities

Domestic govt securities

Short-term asset

14.7%9.4%

19.8%14.6%

49.8%52.2%

11.7%13.6%

4.0%10.3%

Pension funds

Insurance companies

What about Asia? (the case of HK)

Source: Tsoi, E. (2004), HKEx

11

What about Asia? (HK cont’d)

Source: Tsoi, E. (2004), HKEx

Risk and return: an introduction

• Investments are evaluated on the basis of their return/risk profiles

• Historical versus expected measures of returns

• Historical measures of return and risk: – holding-period return (HPR), that is capital gain income (plus

dividend income) per dollar invested

– standard deviation (SD), variability of realized HPRs

+ ++

− += 1 1

, 1t t t

t t

t

P P DHPR

P+

=

= ∑ , 11

1 n

i ii

AHPR HPRn

( )+

=

−⎛ ⎞= ⎜ ⎟−⎝ ⎠∑

2

, 1

11

ni i

ni

HPR AHPRnSD

n n

12

What prices?

• Quoted prices for each asset at any point in time in the real world trading are not single numbers

• We can distinguish between:– ask prices, the price at which an agent (i.e. dealer) is willing

to sell a security

– bid prices, the price at which an agent (i.e. dealer) is willing to purchase a security

• Therefore ask price is always greater then bid price.

• The difference between ask and bid prices (= bid-ask spread) represents dealer’s profit

• During our course, for simplicity we assume a single price, i.e. mid-price (=[ask + bid]/2)

Returns: historical perspective

13

Risk: historical perspective

Returns in the US

14

Wealth in the US (B&H)

Expected returns and risk

• Historical returns are realized returns

• Investors decide on potential investment opportunities by looking at anticipated or expected rates of return

• Risk is therefore the uncertainty that an investment will earn its expected rate of return

15

Expected returns and risk (cont’d)

• Expected returns are weighted averages of rates of returns in each scenario:

in our example:

E(r) = (.25 x 44%) + (.5 x 14%) + (.25 x -16%) = 14%

• The uncertainty (or risk) surrounding E(r) can be measured by the standard deviation of returns

in our example σ = 21.21%

• How much would you invest in the stock market if the bill rate is equal to 5%?

• It depends on each investor’s risk aversion

( ) ( ) ( )s

E r p s r s=∑

( ) ( ) ( ) 2

s

p s r s E rσ = −⎡ ⎤⎣ ⎦∑

Risk and risk aversion

• Example: an investor owns an initial endowment of $100,000 and he/she has to decide to invest in one of the following alternative investments.

– Investment 1: Two possible outcomes are available: 1) with probability 0.6 the investor will receive $150,000, 2) with probability 0.4 the investor will receive $80,000.

– Investment 2: Invest safely his/her endowment in T-bills and earn 5% (or $5,000).

16

Risk and risk aversion (cont’d)

• the expected outcome (wealth) of the risky Investment 1 is:

E(W) = .6 x 150,000 + .4 x 80,000 = $122,000 or differently its expected profit is $22,000

• The incremental profit of the risky investment over the safe investment is $22,000 - $5,000 = $17,000

• $17,000 is defined as risk premium, that is the compensation for the risk of the investment 1.

• Investors can be classified according to their preferences with respect risk premia

Risk and preferences

• Investors can be:

– risk averse, those who reject gambles with zero risk premia (= fair games) or worse

– risk lover, those who will always engage in fair games

– risk neutral, those who are indifferent to the level of risk and will judge investments prospects on the basis on expected returns only

17

Risk aversion and utility scores

• Risk-averse investors penalize the expected return from a risky portfolio by a certain percentage to take into account the risk involved

• Scoring system, Mean-Variance utility (commonly used, Association of Investment Management and Research; AIMR)

that means that investors’ utility (U) is increased by high expected returns and reduced by high levels of risk.

A denotes the coefficient of risk aversion.

( )= − σ21 2U E r A

How risk averse you are

• There are stylized facts in the investment literature describing risk aversion among individuals

• Please fill in the questionnaire (no grades associated with it! Just for discussion) clearly indicating your gender and your background (i.e. Engineering, Finance, Humanities etc.)

• Next week I will present the results and discuss them in class

18

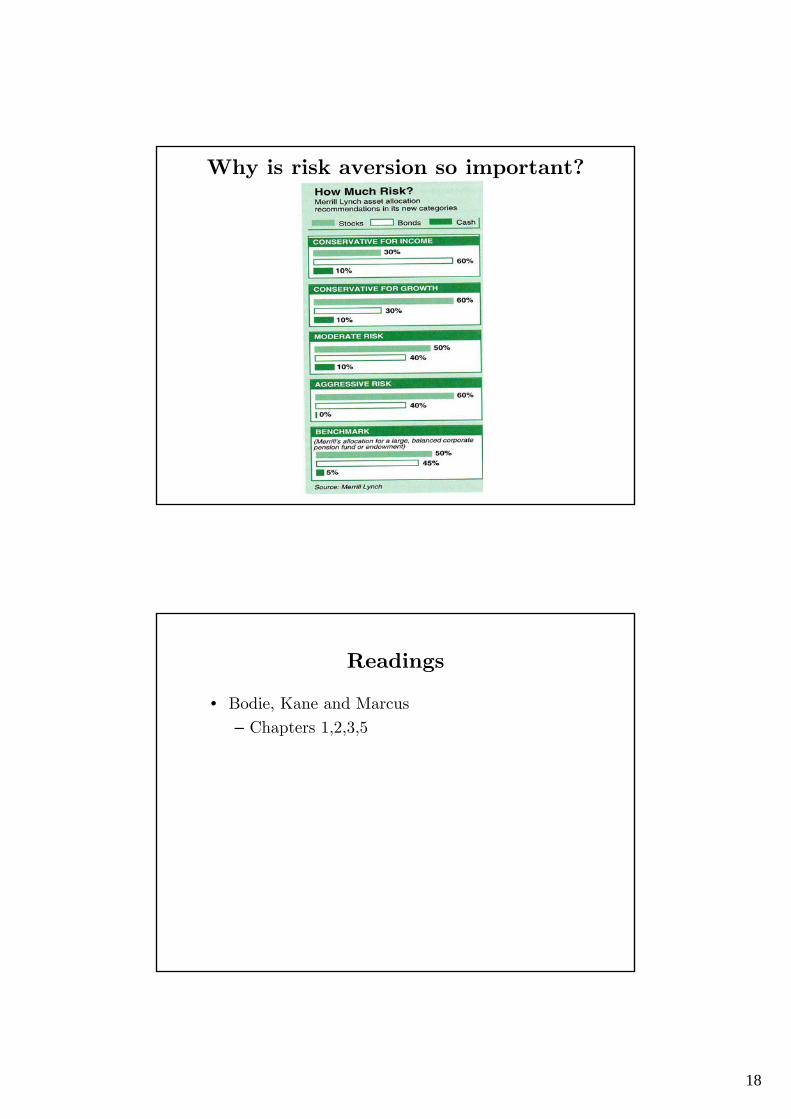

Why is risk aversion so important?

Readings

• Bodie, Kane and Marcus

– Chapters 1,2,3,5