Investment idea SKS Microfinance

47

SKS MICROFINANCE BUY CMP Rs. 475 - Holding Period 2 – 3 Years STOCK INVESTMENT IDEA APRIL 2015

-

Upload

chintan-chheda -

Category

Business

-

view

69 -

download

2

Transcript of Investment idea SKS Microfinance

SKS MICROFINANCE

BUY CMP Rs. 475 - Holding Period 2 – 3 Years

STOCK INVESTMENT IDEA

APRIL 2015

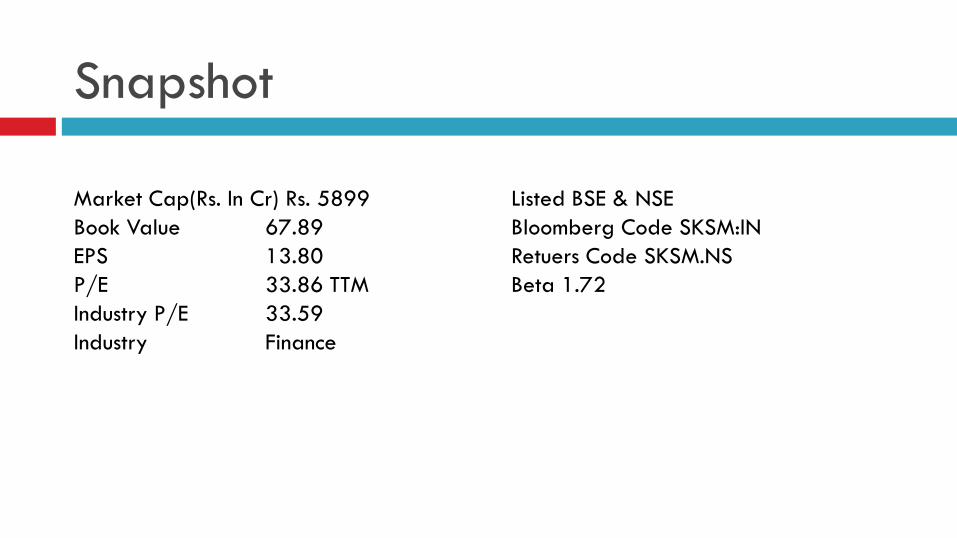

Snapshot

Market Cap(Rs. In Cr) Rs. 5899

Book Value 67.89

EPS 13.80

P/E 33.86 TTM

Industry P/E 33.59

Industry Finance

Listed BSE & NSE

Bloomberg Code SKSM:IN

Retuers Code SKSM.NS

Beta 1.72

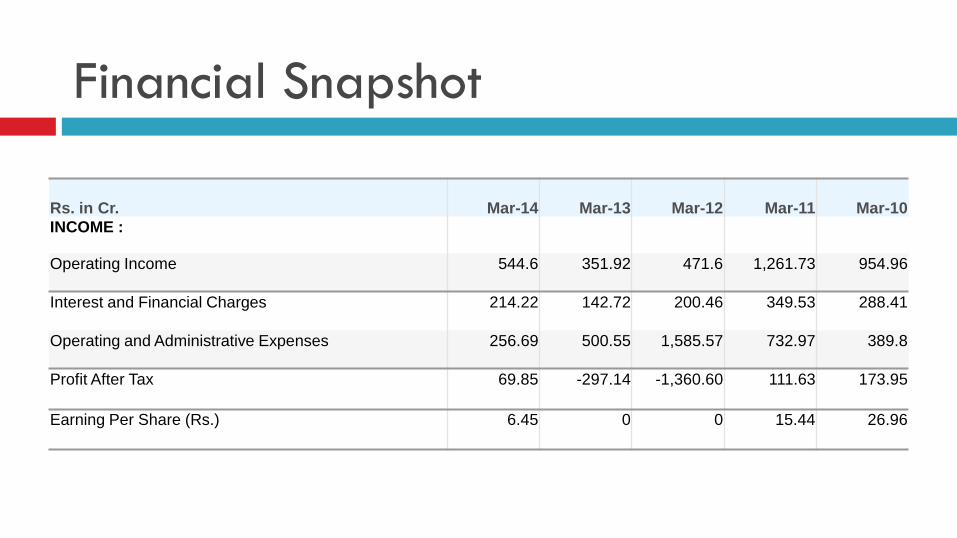

Financial Snapshot

Rs. in Cr. Mar-14 Mar-13 Mar-12 Mar-11 Mar-10

INCOME :

Operating Income 544.6 351.92 471.6 1,261.73 954.96

Interest and Financial Charges 214.22 142.72 200.46 349.53 288.41

Operating and Administrative Expenses 256.69 500.55 1,585.57 732.97 389.8

Profit After Tax 69.85 -297.14 -1,360.60 111.63 173.95

Earning Per Share (Rs.) 6.45 0 0 15.44 26.96

Management Structure

Name Designation

P H Ravi Kumar Chairman (Non-Executive)

Tarun Khanna Director

Geoffrey Tanner Woolley Director

Sumir Chadha Director

Punita Kumar Sinha Additional Director

M R Rao Managing Director & CEO

P Krishnamurthy Nominee (SIDBI)

Rajendra Patil Company Secretary

S Balachandran Additional Director

Paresh D Patel Director

MANAGEMENT

M R Rao, Managing Director & CEO

Dilli Raj, President

BOARD

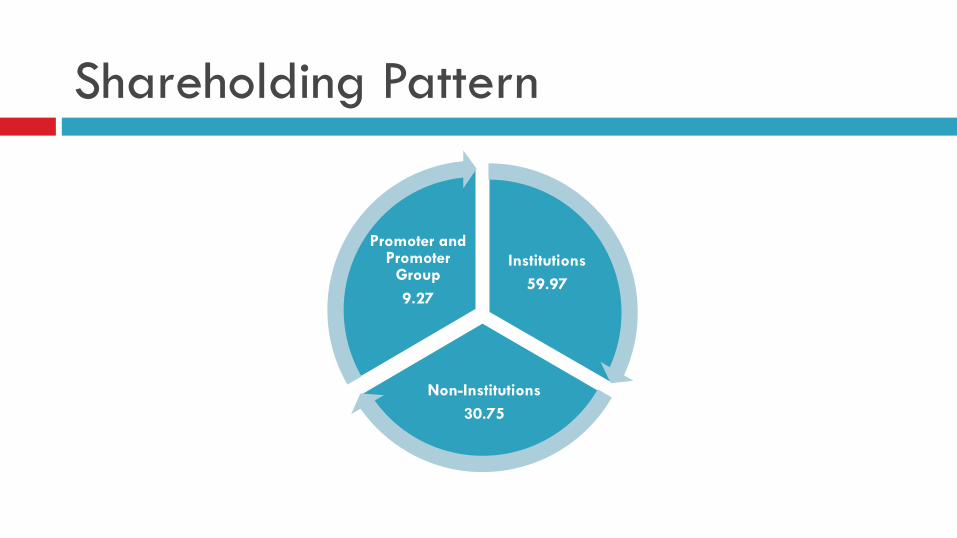

Shareholding Pattern

Institutions

59.97

Non-Institutions

30.75

Promoter and Promoter

Group

9.27

Share Holder with Significant Holding

No. Name of the Shareholder

Number Percentage

1 Kismet Microfinance 56,34,809 4.47

2 Westbridge Ventures II LLC (formerly Sequoia Capital India II , LLC) 34,90,422 2.77

3 Kumaon Investment Holdings (FII sub Account with HSBC Bank (Maurities) Ltd) 25,60,292 2.03

Total 1,16,85,523 9.27

Journey Started in 1997

SKS was formed as an NGO in December 1997

and started Operation in 1998

In 1998 Operation Began in Tumnoor Village in

Medak District of Andhra Pradesh

In 2000 Pioneers SmartCard Pliot Project level. It

wins the CGPA Pro-Poor Innovation award as well

as a $50,000 prize.

Journey

• In 2001 SKS bags the Digital Partners SEL Award

and a soft Loan of $52,000. The Grameen Foundation

matched the Award. Money is used in Technology

Development.

• 2002 it receives First ever loan of Rs. 5 Lakhs from

Friends of Women's World Banking, India

Towards IPO

2005 SKS incorporated as NBFC. SKS moves

from being Non for Profit Organisation to

becoming a for profit Organization.

2007 Was awarded the Excellence in

Information Integrity.

IPO

In 2008 SKS is listed as the Worlds most Influential

Emerging Company.

In 2009 ranked as number one MFI in the country.

In 2010 SKS becomes the first MFI in South Asia to

launch an IPO

Microfinance Then and Now

THEN

To most, microfinance means providing poor families with very small loans (microcredit) to help them engage in productive activities to grow their tiny businesses.

NOW

Microfinance has come to include a broader range of services (credit, savings, insurance and others) as it has been realised that the poor

AFFORDABLE LOANS

Microfinance started with the recognition that poor people had the capability to lift themselves out of poverty if they had access to affordable loans.

High repayment rates

in the industry have

changed the

perception that the

poor are not credit

worthy.

Growth at the Beginning 2005 to 2008

SKS witnessed a robust compounded growth rate

of (CAGR) 205% in its member base.

CAGR of 217% in its Disbursements.

CAGR 237% of Loan Outstanding.

PRODUCTS

Proprietary

Income Generation Loans (IGL) – Aarambh

Mid-Term Loan (MTL) – Vriddhi

Long Term Loan (LTL)

Housing Loans

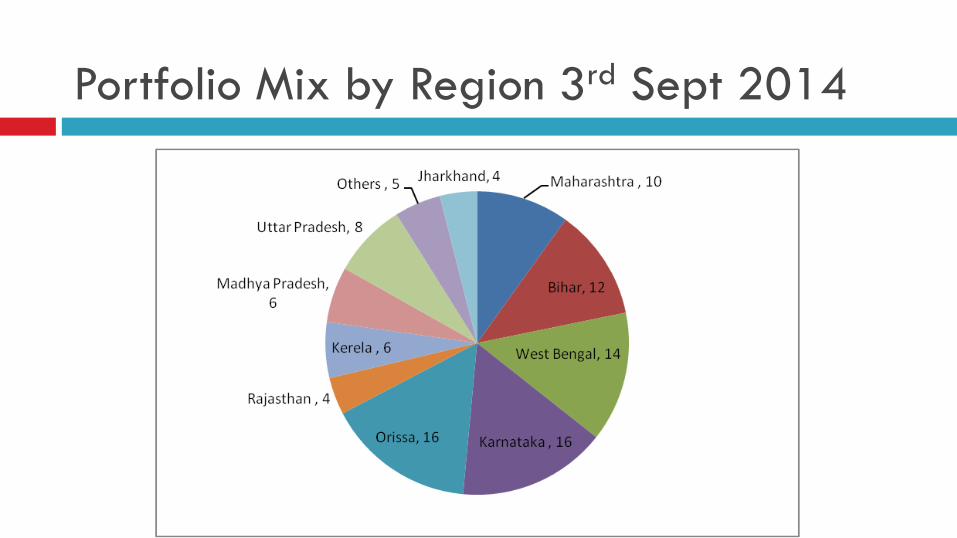

Portfolio Mix by Region 3rd Sept 2014

Market Share - Based on Disbursement

PHASE II

Enters into Allied Products

Insurance, Gold Loan & Mobile Loan.

Long Term Loan

New Products

Solar Loan

Mobile Loans

Swarna - pushpam Gold Loan

PRODUCTS

Distribution Products

Life Insurance

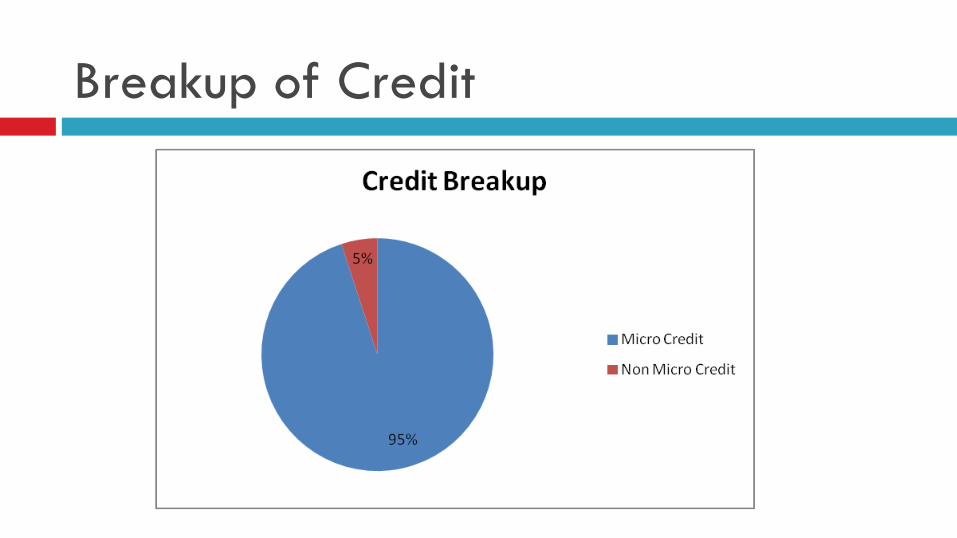

Breakup of Credit

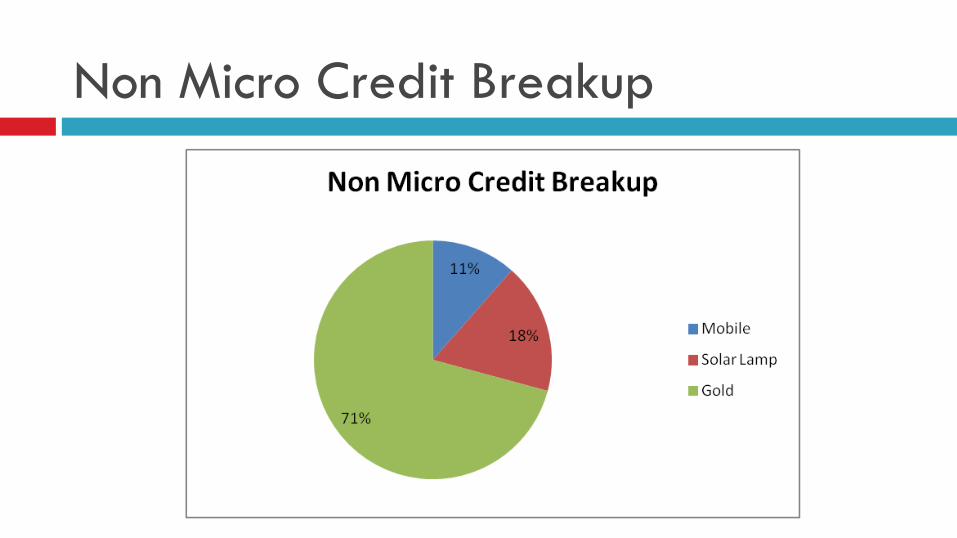

Non Micro Credit Breakup

Scalable Model

SKS tends to implement its growth model without

adding significant number of new branches.

Fresh addition of Head count will be in Sangam

Managers (Loan Officers)

Annual Rate rate of 1500 loan officers.

Cross Selling of Various Products

SKS Leverages its Network to Distribute financial

and Non Financial products of other institutions to its

members at lower cost.

While the focus remain on the core business of

providing micro credit, it continues to diversify into

other business involving fees based services.

Exploring Multiple Funding Avenues

After the crisis, scheduled commercial banks limited their funding to the MFI sector.

Gradually, the market stabilised, there was clarity on the regulatory front, fair‐pricing practices were adopted, and credit bureaus were established.

Securitisation regained its ground with improved business fundamentals

By this year end dependence on Securitization Funding to be remain High upto 45%.

Technology to Provide Operating

Leverage

SKS has completed all branch connectivity with

daily MIS flow to Head Office.

SKS other technology initiatives are refactoring of

its in‐house lending system for effective monitoring

and control, enabling loan officers with hand‐held

devices to improve productivity.

Risk Management Tools

The establishment of credit bureaus enables the

lender to check the credit history.

Wider geographical spread of portfolio another

effective way to manage political risk.

Credit Monitoring

SKS has advantage over other banks because of its

strong Joint Liability Group.

Under the Joint Liability Group its lends only to

woman borrowers.

Learning from Crisis

Post Andhra Pradesh crisis it does not have more

than 15% exposure in any state.

Diversified Portfolio in 15 States.

It has also put a disbursement cap on basis of per

district per branch.

INDUSTRY ATTRACTIVNESS

Microfinance could be $50bn financing

Opportunity

Microfinance highly under penerated

Penetration Limited in other regions

MFI grew faster over FY08-11

Assessesment

Risks

Political intervention could significantly impact

growth and asset quality.

Reliance on bank borrowing.

Market share taken by SHG

Microfinance Act regulations

Competitive Strenghts

High Entry Barrier

A strong brand, client base and pan-India

distribution network

Experienced management team

Better access to Capital Markets

CAGR

Expect FY16-18 AUM CAGR of 32%, supported by

growth in client base and higher ticket size

Scope

There are approx 175 Banks in India with over

76000 Branches and over 12000 NBFC’s.

Out of all the Small Enterprises in India only 5%

have access to the capital they require.

Opportunity

In fact a report released by Intellecap for the

International Finance Corporation (IFC), part of the

World Bank Group, estimates that the debt gap for

micro & small enterprises in India is about $198

billion, growing at 11% per year

M-Banking and Microfinance

With the advent of M-banking within the

Microfinance we can expect the entire change in the

landscape.

All the leading banks have tied up with leading tele

communications company for mbanking.

Sector Growth at 50% and above

The sector is growing at the pace of 50% and

above higher than mobile phone industry.

SKS Microfinance been ahead in the technology

would have an added advantage.

Loan Size

Global average Loan size is $522 were as in India

it is $144.

Huge opportunities with Untapped Market and

Untapped Customer.

Loan Portfolio

The gross loan portfolio of India's microfinance

sector accounts for more than 7 percent of the

sector's worldwide loan portfolio size.

As much as 30 percent of the world's microfinance

borrowers are in India.

Sustainability of Microfinance

The demand for microfinance services – savings, credit

and insurance – is apparently insatiable in India.

The total outreach of the existing specialized

microfinance service providers is quite limited.

MFIs are usually established to fulfil a mission – of

reaching credit and financial services to the poor who

are otherwise unreached by mainstream FIs.

Key Ratio Improvement

Key Ratios Mar-14 Mar-13 Mar-12 Mar-11 Mar-10

PBIDTM (%) 52.89 -41.97 -235.71 42.26 59.33

PBITM (%) 52.14 -43.8 -237.83 40.99 58.02

PBDTM (%) 13.57 -82.45 -278.16 14.73 29.24

CPM (%) 13.57 -82.45 -285.96 10.07 19.46

APATM (%) 12.82 -84.28 -288.08 8.79 18.15

ROCE (%) 9.9 0 0 13.51 17.25

RONW (%) 6.52 0 0 8.15 21.56

Technical Observation

The stocks have been doing Higher Tops and Higher

Bottoms and the same Trend is expected in continue.

It is touching its 52 week high with a price of Rs.575

Conclusion

Andhra Pradesh Crisis has brought the management

to a more cautious and diversified position.

Opportunity to recreate the Initial Growth

Huge Untapped Market and Highly Under

Penetrated.

Disclosure & Disclaimer

This document has been prepared by Advisors and is meant for sole use by the recipient and not for circulation.

. It should not be considered to be taken as an offer to sell or a solicitation to buy any security.

The information contained herein is from sources believed reliable.

We do not represent that it is accurate or complete and it should not be relied upon as such.

We may have from time to time positions or options on, and buy and sell securities referred to herein.

We may from time to time solicit from, or perform investment banking, or other services for, any company mentioned in this document.

The subject company may have been our client during twelve months preceding the date of distribution of the Research report.

Research analyst has not served as an officer, director or employee of the subject company.

Disclosure & Disclaimer

Research entity has not been engaged in market making activity for the subject company.

We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

Investors may note that markets are volatile in the short-term and their investments might experience high volatility including possibility of going negative.

The risks generally come from having an unsuitable asset allocation which would ideally vary from client to client. Having more exposure to equity than the risk appetite warrants, would expose to more volatility/risks. We only suggest clients on their equity portfolio.

Investing in small and mid caps stocks have high impact costs due to low liquidity. This might affect the ability to quickly take action on our recommendation at stated price

Disclosure & Disclaimer

Responsibility of taking investment decisions,

buy/sell transactions is solely at the discretion of

clients, and company does not bear any

responsibility of the consequences.