INVESTMENT ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT€¦ · · 2015-11-23This...

60

TWEEDY, BROWNE FUND INC. This booklet consists of two separate documents: INVESTMENT ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT Tweedy, Browne Global Value Fund (TBGVX) Tweedy, Browne Global Value Fund II – Currency Unhedged (TBCUX) Tweedy, Browne Value Fund (TWEBX) Tweedy, Browne Worldwide High Dividend Yield Value Fund (TBHDX) September 30, 2015

Transcript of INVESTMENT ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT€¦ · · 2015-11-23This...

TWEEDY, BROWNE FUND INC.

This booklet consists of two separate documents:

INVESTMENT ADVISER’S LETTERTO SHAREHOLDERS

SEMI-ANNUAL REPORT

Tweedy, Browne Global Value Fund (TBGVX)Tweedy, Browne Global Value Fund II – Currency Unhedged (TBCUX)

Tweedy, Browne Value Fund (TWEBX)Tweedy, Browne Worldwide High Dividend Yield Value Fund (TBHDX)

September 30, 2015

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter to Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1Different Perspectives on Investment Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix

Semi-Annual Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-1

Tweedy, Browne Fund Inc.Expense Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-2

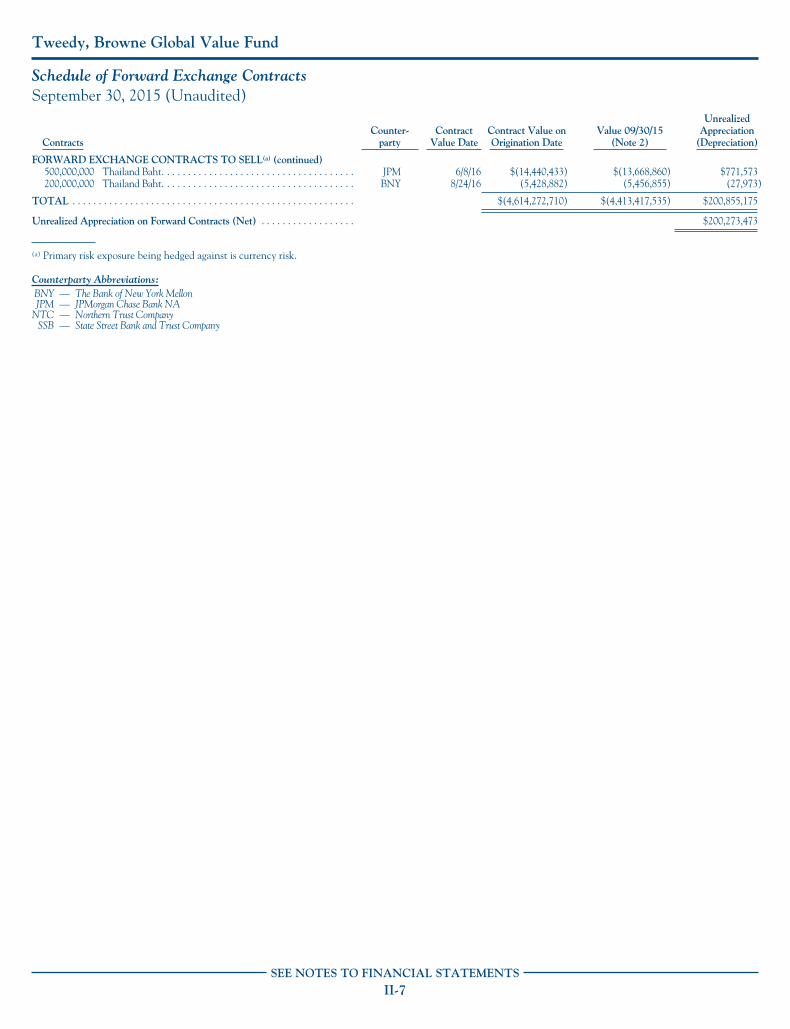

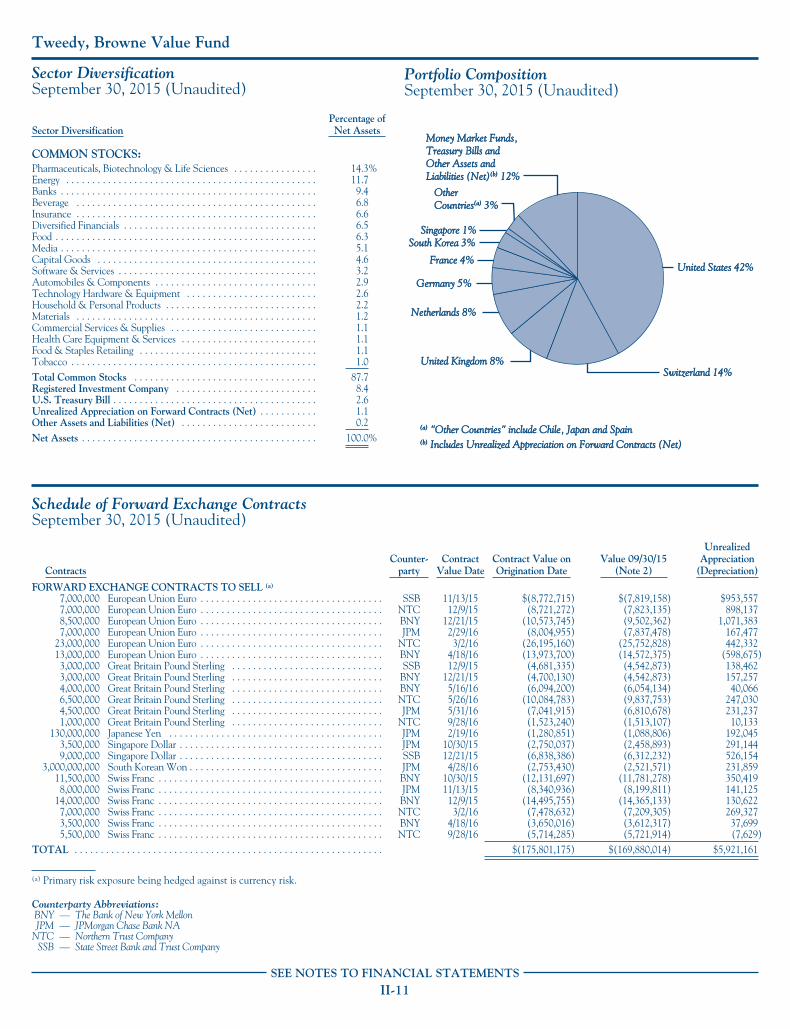

Tweedy, Browne Global Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-3Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5

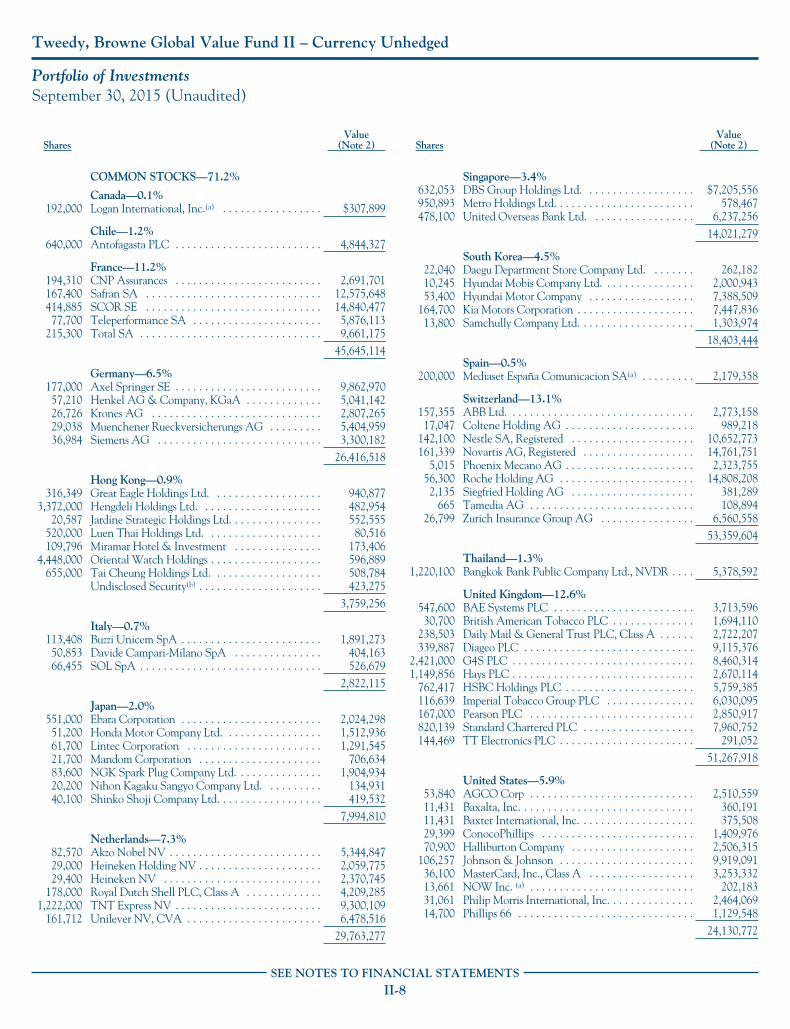

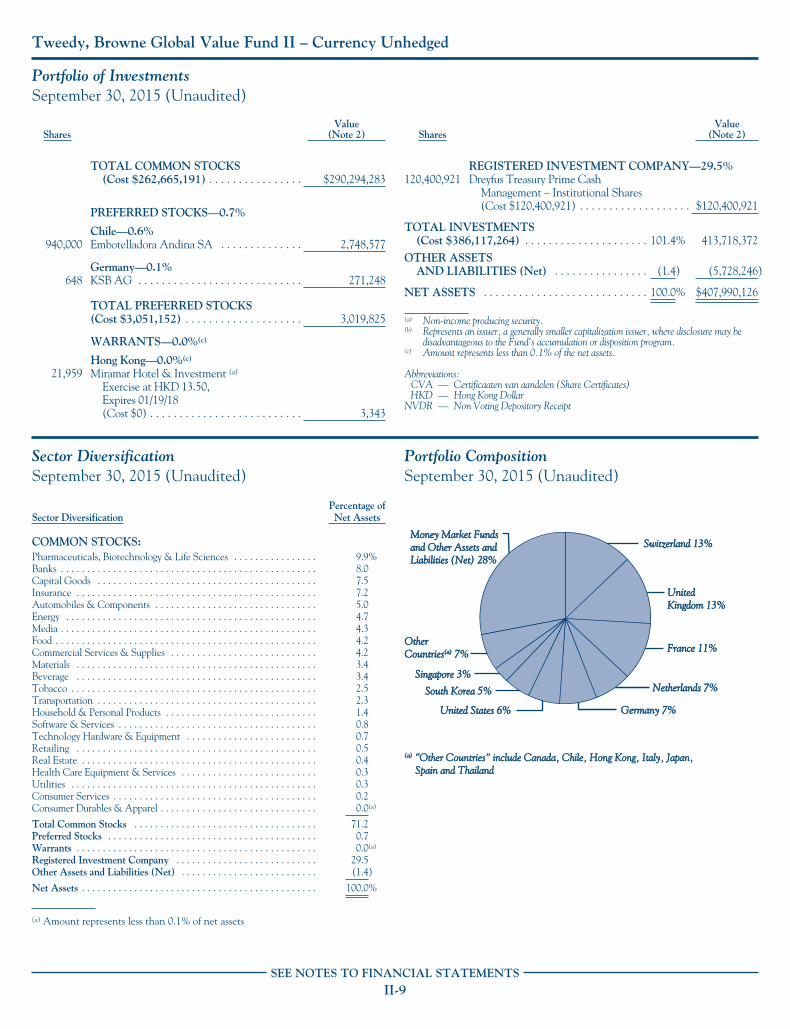

Tweedy, Browne Global Value Fund II – Currency UnhedgedPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-8Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-9Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-9

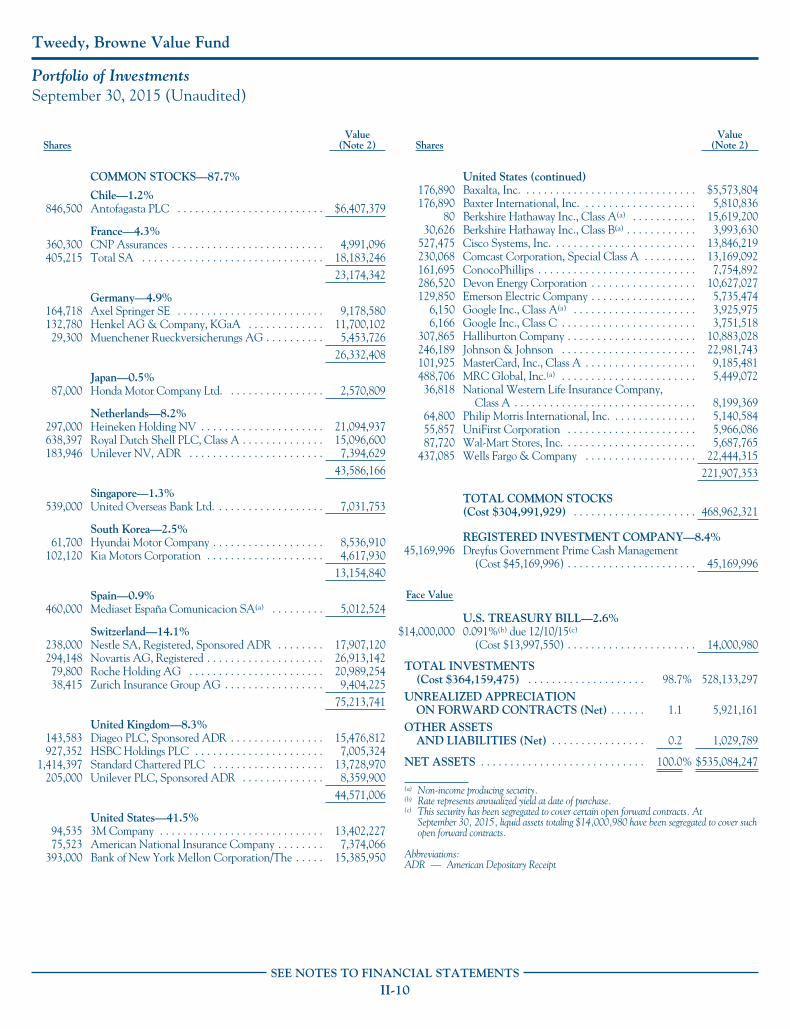

Tweedy, Browne Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-10Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11

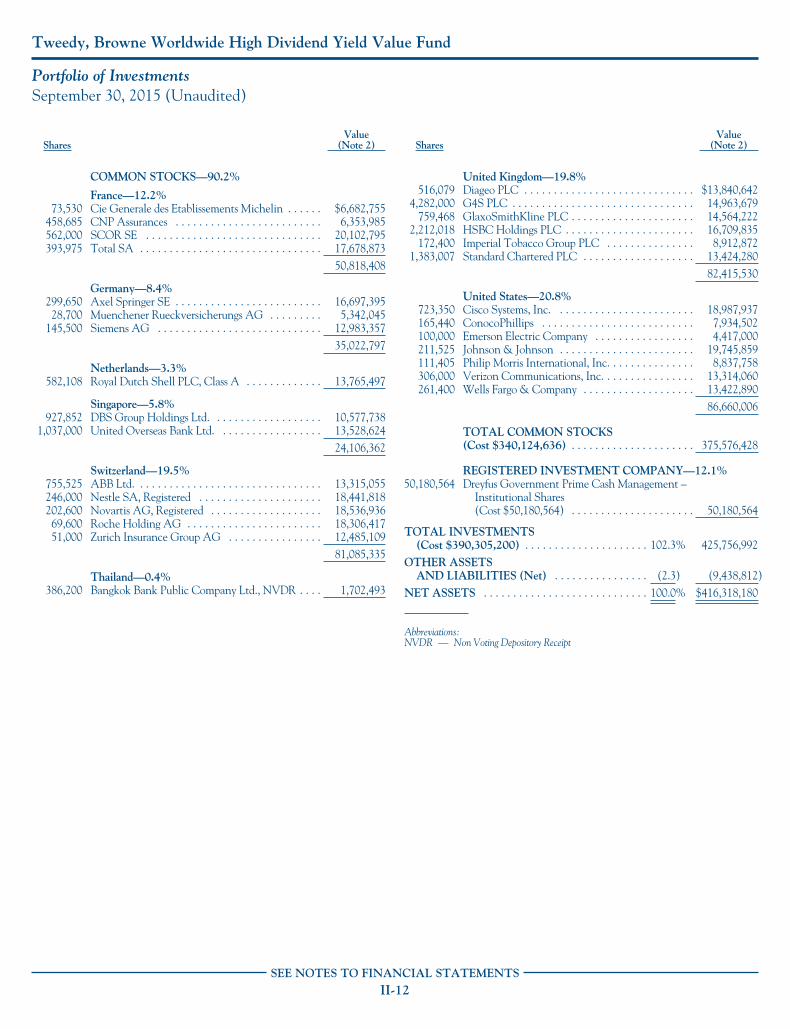

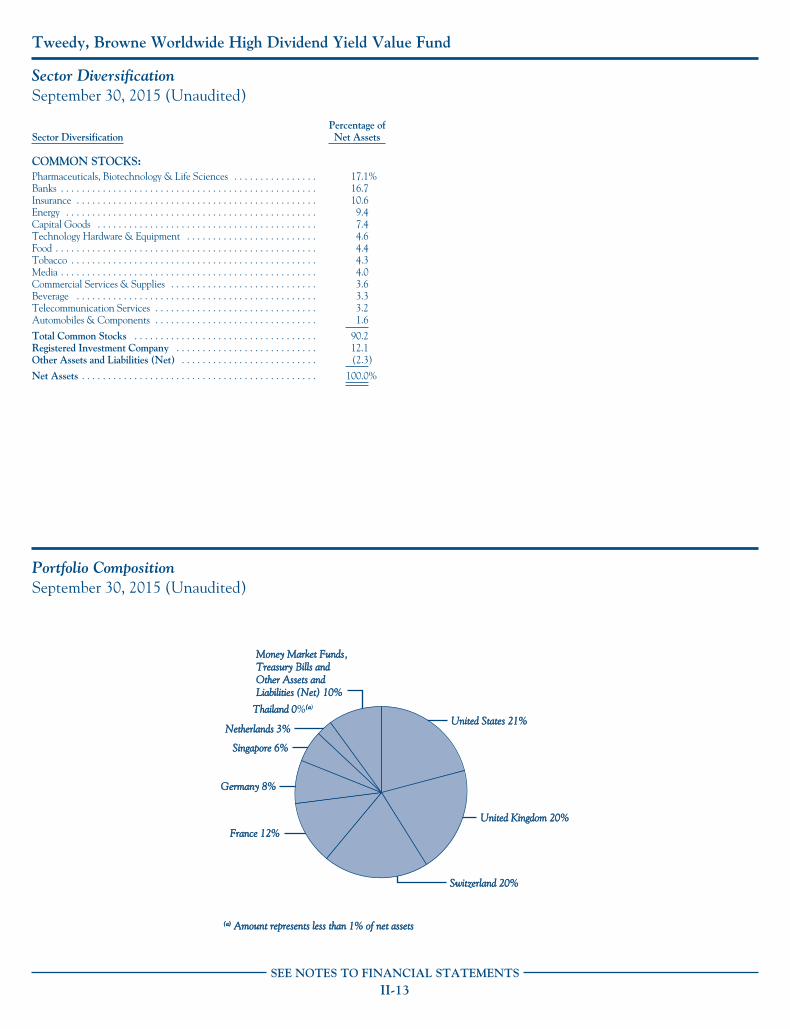

Tweedy, Browne Worldwide High Dividend Yield Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-12Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-13Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-13

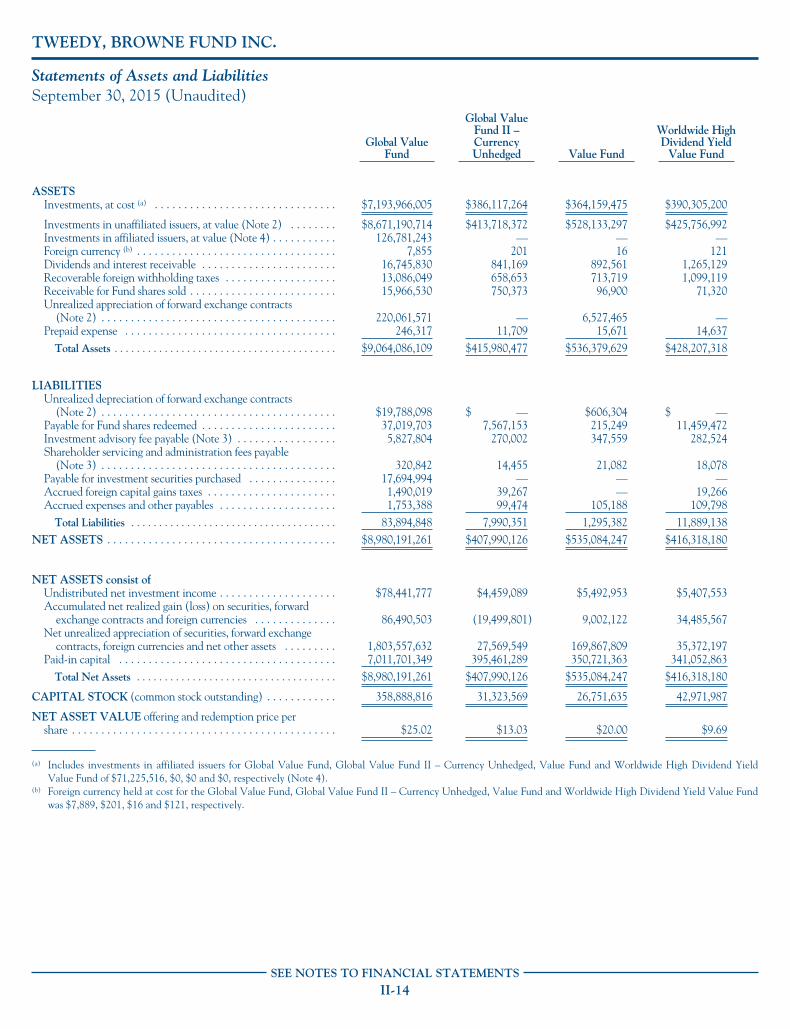

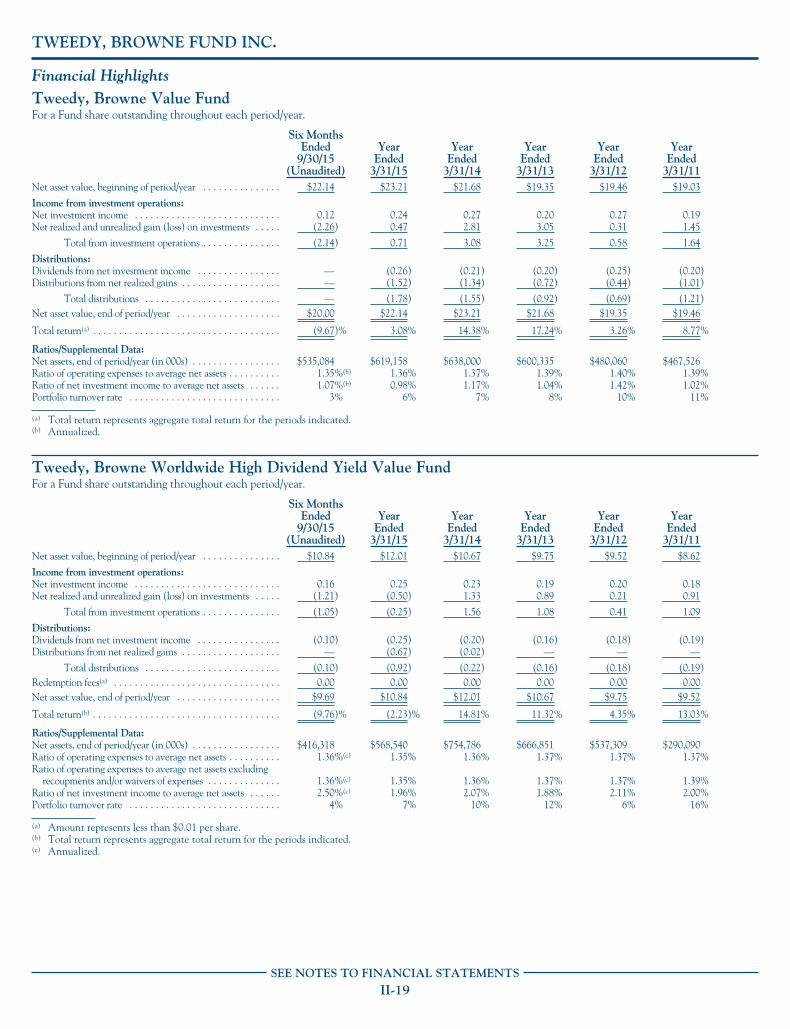

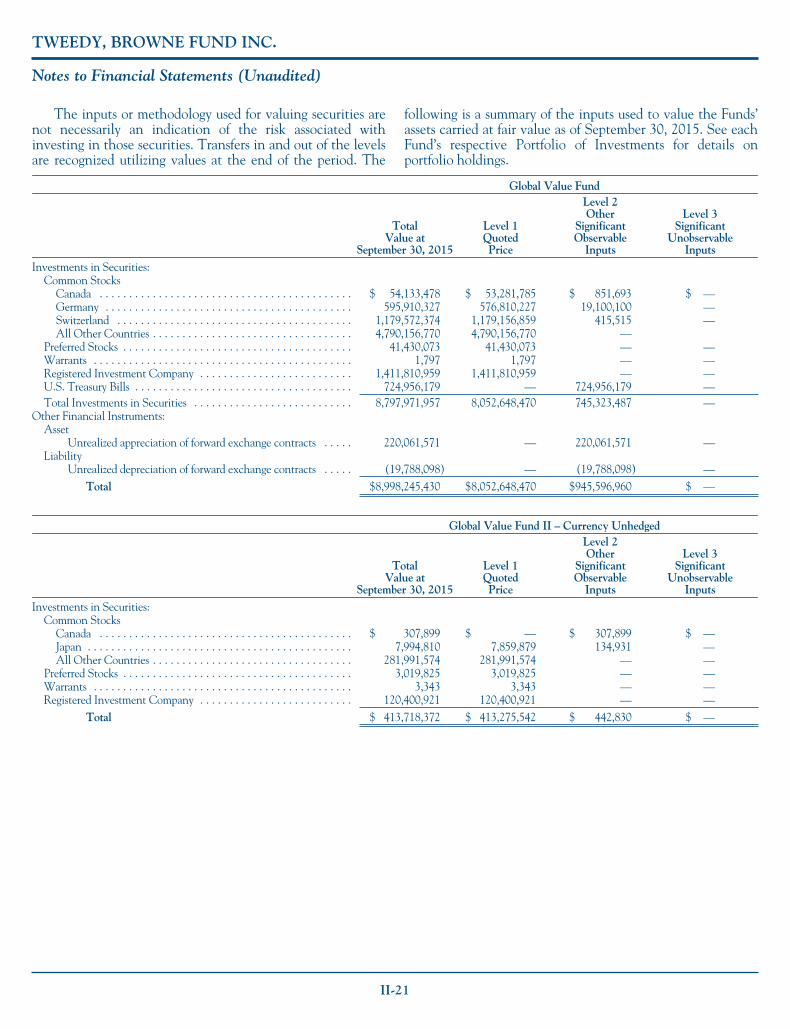

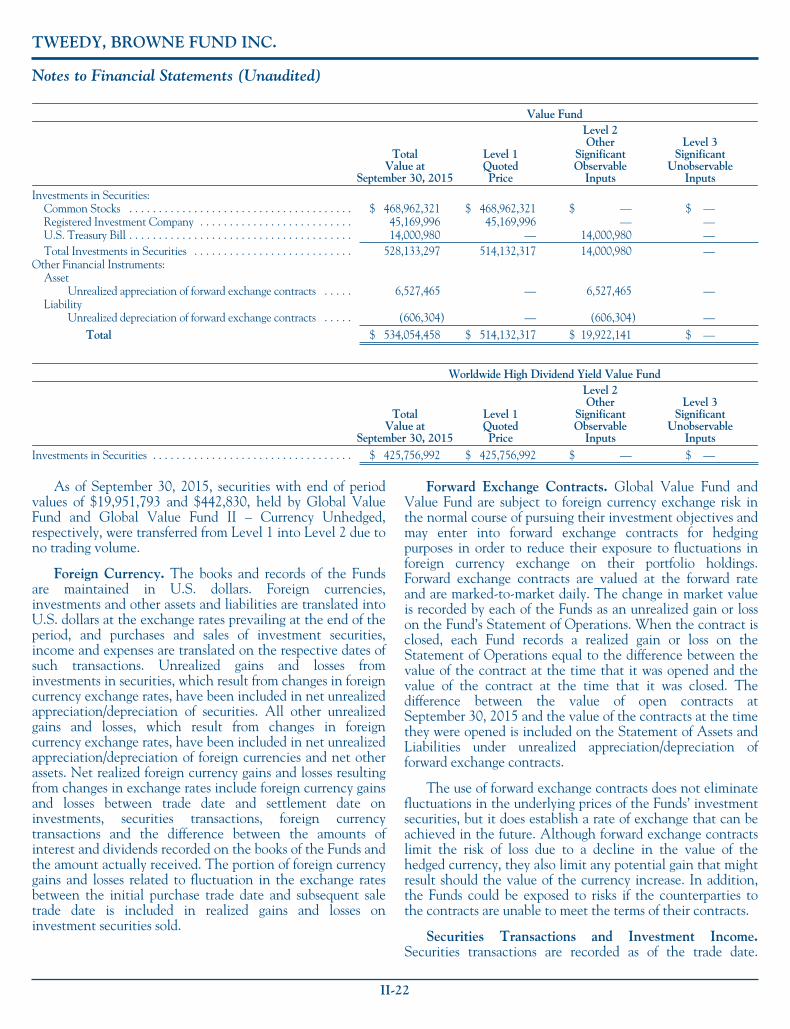

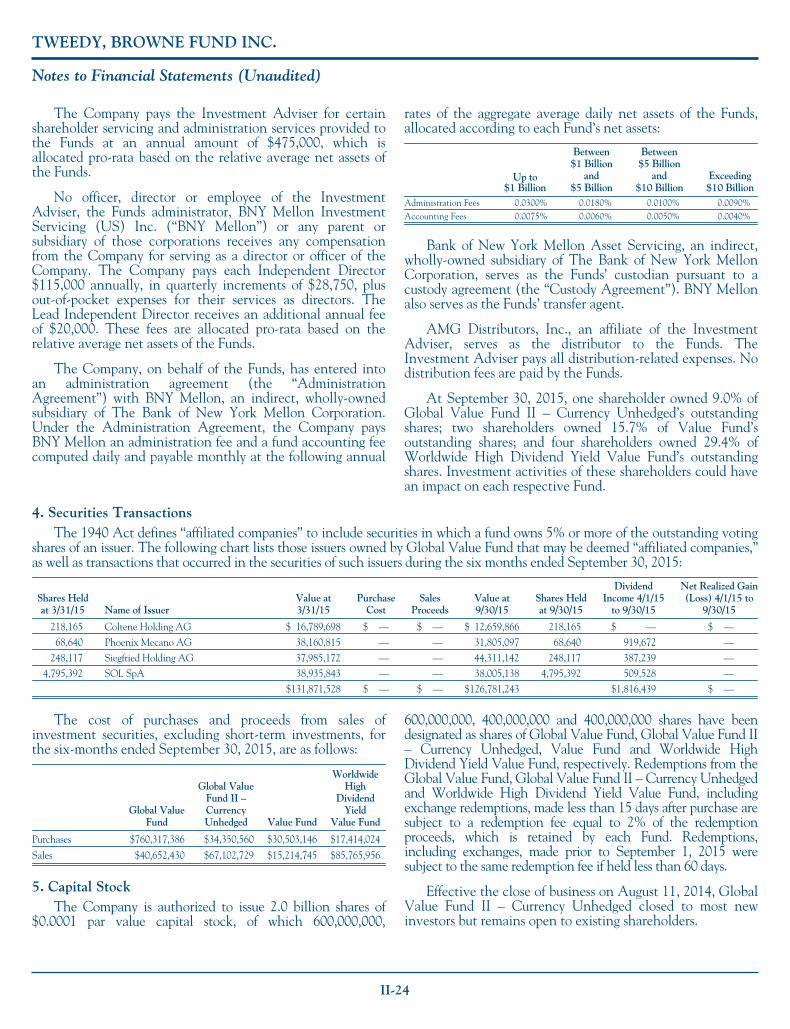

Tweedy, Browne Fund Inc.Statements of Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-14Statements of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-15Statements of Changes in Net Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-16Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-18Notes to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-20Investment in the Fund by Managing Directors and Employees of the

Investment Adviser . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-23Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-28

TWEEDY, BROWNE FUND INC.

Our Investment Team

Managing Directors

William H. Browne*†

John D. Spears*†

Thomas H. Shrager*†

Robert Q. Wyckoff, Jr.*†

Olivier Berlage Frank H. Hawrylak, CFA†

Dave Krasne, CFA Elliot H. Larner Sean McDonald, CFAJay Hill, CFA†

Roger R. de Bree†Will Browne, CFA

Security Analysts

* Management Committee member† Investment Committee member

This page left blank intentionally.

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter to Shareholders (Unaudited)

Slowing growth in China, the world’s second largesteconomy, coupled with uncertainty surrounding theprospective normalization of interest rates in theUnited States sent tremors through global equity markets overthe last several months. After a rather short lived and furiouscorrection in late August and early September, global equitymarkets regained their footing and, as we write, have takenback much of the ground they lost as summer came to an end.

For value investors such as ourselves, it remained businessas usual through this turbulence, although we would admit toa certain counterintuitive satisfaction as equity markets begantheir long overdue retreat. After six and a half years ofrelatively smooth sailing, setting aside a brief hiccup in 2011,it had become quite a challenging environment for valueinvestors. Bargains had become increasingly scarce and manyof our existing holdings were trading at or near our estimatesof their intrinsic value – consequently, we were selling andtrimming back a number of those positions. As a result, cashreserves had increased and our returns were somewhat dilutedwhile the bull markets and their associated benchmark indicesraged on. We were able to take some advantage of themarkets’ downside volatility in late summer. However, it didnot last long enough, nor was it steep enough, for us to makesignificant headway in putting our cash reserves to work.

As we have explained in previous letters, equity returnstreams are lumpy by their nature. We can identify companiesthat we believe are undervalued at purchase, but have nocontrol as to when (or if) that value gets recognized in public

markets. That recognition often occurs with a great deal ofrandomness. Therefore, in all investment records, there is anelement of both luck and skill. As we mentioned in last year’ssemi-annual report, since a multitude of variables move stockprices around, particularly in the short run, it is virtuallyimpossible to divine skill from luck without a large samplesize, i.e., a long record. One thing we have in abundance atTweedy, Browne, given our long history and pedigree, arelong, successful investment records. In the case of our mutualfunds, those records have bested benchmark indices sincetheir respective inceptions. However, those return streamshave been lumpy, with multiple interim periods ofunderperformance like the one we are going through now.And yet this periodic underperformance has been part andparcel, in our case, of long-term, successful performancerecords.

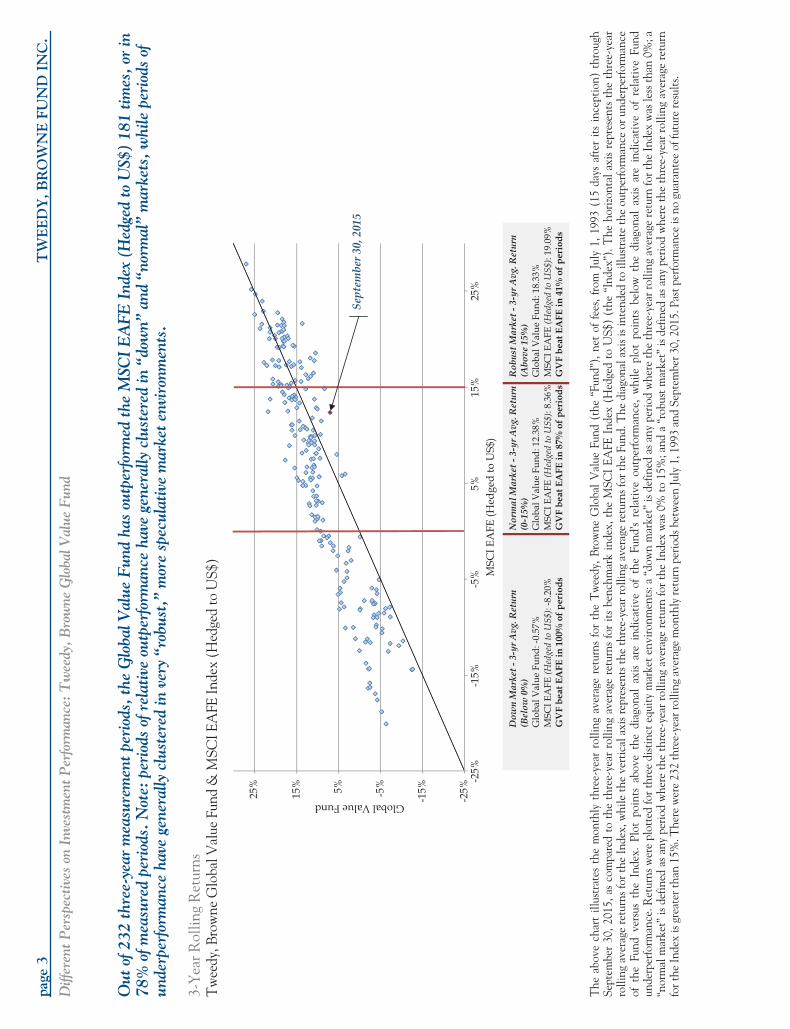

Included below is a chart that we believe providesadditional perspective on the Global Value Fund’s 22 plus-year investment record. It is in the form of a scatterplot, andexamines 3-year rolling returns since inception for the GlobalValue Fund as compared to the MSCI EAFE Index (Hedgedto US$) for different types of equity market environments.The chart illustrates that periods of relative outperformancefor the Fund have tended to occur in “down” and more“normal” market environments, while periods of relativeunderperformance have tended to cluster in very “robust,”more speculative market environments, like the one we havebeen in over the last three years.

I-1

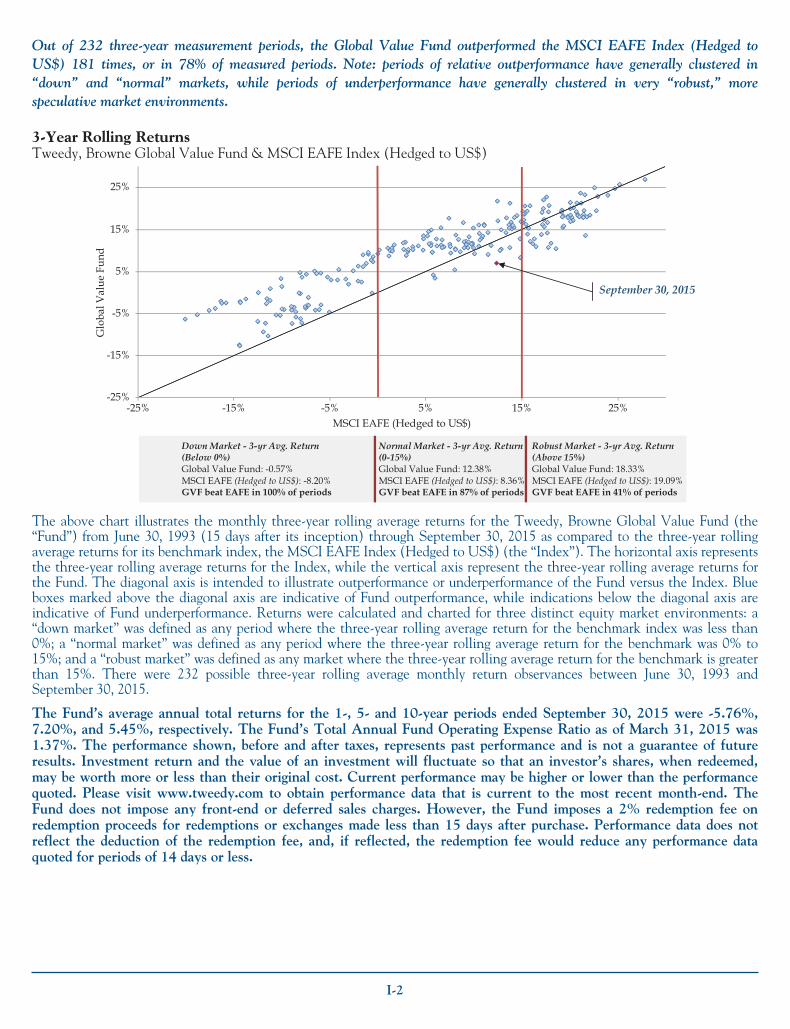

Out of 232 three-year measurement periods, the Global Value Fund outperformed the MSCI EAFE Index (Hedged toUS$) 181 times, or in 78% of measured periods. Note: periods of relative outperformance have generally clustered in“down” and “normal” markets, while periods of underperformance have generally clustered in very “robust,” morespeculative market environments.

3-Year Rolling ReturnsTweedy, Browne Global Value Fund & MSCI EAFE Index (Hedged to US$)

Down Market - 3-yr Avg. Return (Below 0%) Global Value Fund: -0.57% MSCI EAFE (Hedged to US$): -8.20%GVF beat EAFE in 100% of periods

Normal Market - 3-yr Avg. Return (0-15%) Global Value Fund: 12.38% MSCI EAFE (Hedged to US$): 8.36%GVF beat EAFE in 87% of periods

Robust Market - 3-yr Avg. Return (Above 15%) Global Value Fund: 18.33% MSCI EAFE (Hedged to US$): 19.09%GVF beat EAFE in 41% of periods

-25%

-15%

-5%

5%

15%

25%

25%15%5%-5%-15%-25%

Glo

bal V

alue

Fun

d

MSCI EAFE (Hedged to US$)

September 30, 2015

The above chart illustrates the monthly three-year rolling average returns for the Tweedy, Browne Global Value Fund (the“Fund”) from June 30, 1993 (15 days after its inception) through September 30, 2015 as compared to the three-year rollingaverage returns for its benchmark index, the MSCI EAFE Index (Hedged to US$) (the “Index”). The horizontal axis representsthe three-year rolling average returns for the Index, while the vertical axis represent the three-year rolling average returns forthe Fund. The diagonal axis is intended to illustrate outperformance or underperformance of the Fund versus the Index. Blueboxes marked above the diagonal axis are indicative of Fund outperformance, while indications below the diagonal axis areindicative of Fund underperformance. Returns were calculated and charted for three distinct equity market environments: a“down market” was defined as any period where the three-year rolling average return for the benchmark index was less than0%; a “normal market” was defined as any period where the three-year rolling average return for the benchmark was 0% to15%; and a “robust market” was defined as any market where the three-year rolling average return for the benchmark is greaterthan 15%. There were 232 possible three-year rolling average monthly return observances between June 30, 1993 andSeptember 30, 2015.

The Fund’s average annual total returns for the 1-, 5- and 10-year periods ended September 30, 2015 were -5.76%,7.20%, and 5.45%, respectively. The Fund’s Total Annual Fund Operating Expense Ratio as of March 31, 2015 was1.37%. The performance shown, before and after taxes, represents past performance and is not a guarantee of futureresults. Investment return and the value of an investment will fluctuate so that an investor’s shares, when redeemed,may be worth more or less than their original cost. Current performance may be higher or lower than the performancequoted. Please visit www.tweedy.com to obtain performance data that is current to the most recent month-end. TheFund does not impose any front-end or deferred sales charges. However, the Fund imposes a 2% redemption fee onredemption proceeds for redemptions or exchanges made less than 15 days after purchase. Performance data does notreflect the deduction of the redemption fee, and, if reflected, the redemption fee would reduce any performance dataquoted for periods of 14 days or less.

I-2

As the above chart demonstrates, the underperformanceof our value driven strategy in the Global Value Fund overthe last several years would appear to be quite normal and tobe expected in the later stages of a bull market, when equityvaluations become untethered from underlying estimatedintrinsic values. In fact, if we were “winning big” in thisenvironment, it would certainly seem out of step with thepattern of our historical returns, and would no doubt promptsome questions.

Following this letter is a study we’ve recently publishedentitled “Different Perspectives on Investment Performance –Tweedy, Browne Global Value Fund.” The study examines in-depth the long-term return history of our flagship Fund, theTweedy, Browne Global Value Fund, since its inception in thesummer of 1993. The study includes an analysis of rollingperiod results in different market environments, the variabilityof returns, down market performance, “peak-to-trough”declines and subsequent recovery, upside/downside captureratios, and after-tax returns.

We hope it provides some additional perspective on whathas been a long and successful, yet “lumpy” investmentexperience for Global Value Fund shareholders. Included inthe study are several rolling period return charts that illustratethat, the longer the measurement period, the greater theconsistency of outperformance of the Fund. We believe thesecharts provide interesting perspective about the returns of theGlobal Value Fund over long measurement periods. Since itsinception on June 15, 1993, an initial investment of $100,000in the Global Value Fund would be worth $739,293, as ofSeptember 30, 2015. By comparison, an investment onJune 15, 1993 in the MSCI EAFE Index (Hedged to US$)would be worth $339,350.

While there are no guarantees, the study also suggests thatthis difficult slice of time will eventually pass, and we willonce again have new opportunities. With the FederalReserve’s back against the wall and the Chinese economycontinuing to grind down, we suspect we have not seen theend of unsettled markets, and if the recent volatility persists,as we suspect it will, we feel we are well positioned to takemeaningful advantage. In times like these, we are once againreminded of Ben Graham’s cautionary parable of “Mr.Market,” the obliging, but moody fellow who turns up everyday at the shareholder’s door, offering to buy his shares at aprice. Depending on his mood, that price could be absurdlyhigh, perhaps about right, ridiculously low, or somewhere inbetween. As Warren Buffett has counseled:

Mr. Market is there to serve you, not to guide you. It ishis pocketbook, not his wisdom that you will finduseful. If he shows up someday in a particularly foolishmood, you are free to ignore him or to take advantageof him, but it will be disastrous if you fall under hisinfluence.

As your Fund manager, you can count on us to try to putMr. Market’s anxiety into perspective, and behave rationally,so that we can capture for you some of the rewards that webelieve will come in the future. We hope that, through ouractions and words, we are able to do just that.

Stability of People and Process

We thought it might make sense, in addition toruminating about our Funds and markets, to reflect upon theorganization to which you have entrusted a portion of yourhard-earned capital. We are rapidly approaching our 95th

birthday as an investment organization grounded in a deeplyrooted value oriented investment discipline that has provenits efficacy both empirically and in practice over the years. Aswe have said quite often, we remain deeply indebted toMessrs. Graham, Buffett, Munger and Schloss, our intellectualforebears, for having paved the way for multiple generationsof Tweedy, Browne employees. We are now fortunate to havea third generation of Brownes working at our firm.

While new investment products in the moneymanagement industry have multiplied and investor timehorizons have shortened, we have remained dedicated toGraham’s simple but elegant proposition that there are inessence two prices for every share of stock: the price listed onthe exchange on any given day, and the other price, the onethat would accrue to investors if the entire company werepurchased outright in an arms-length negotiated transactionbetween a knowledgeable buyer and seller. Graham referredto this price as the intrinsic value of the business, and to hisway of thinking, the essence of investment was to try toexploit discrepancies between these two prices – in otherwords, to try to take advantage of mis-pricings in public equitymarkets. To this day, judgments around these two prices formthe basis for everything that we do at Tweedy, Browne.Thank you, Ben.

Looking back, surviving intact for roughly 95 years is arather remarkable feat for an investment organization,particularly in this day and age. We believe the key to thissuccess has been our strict adherence to a highly efficaciousinvestment approach and process, stewardship by successivegenerations of partners who have been willing to subsumetheir individual egos for the sake of the firm as a whole, and ahealthy dollop of good luck. We have been incrediblyfortunate in running our business, relying on a collaborative,team-oriented approach that we feel provides a betterframework for investment decision-making than an approachbased on any one individual’s investment acumen. It hasbecome clear to us over time that the diversity of perspectivethat this structure provides often leads to unique insights,deeper understanding, and occasional breakthroughs inresearch, all necessary for high quality investment decisions. Ithas also become clear that maintaining a balance ofpersonalities and skill sets is essential in preserving theinterpersonal harmony necessary for long and successfulcareers at our firm. We feel we have been successful atcreating a culture that fosters cooperation for the good of thefirm with the result being that each individual is better for it.

Our Investment Committee today is comprised of our fourlong-serving Managing Directors, Will Browne, Tom Shrager,John Spears, and Bob Wyckoff, and three of our analysts,Roger de Bree, Frank Hawrylak, and Jay Hill, each of whomjoined our Investment Committee within the last two yearsafter many years of service to our firm. The four ManagingDirectors have worked together at Tweedy continuously for

I-3

between 24 and 41 years, while the analysts on theInvestment Committee have been on board for between 12and 29 years. No Managing Director or past partner ofTweedy, Browne has ever left the firm to take another job.All of the members of our Investment Committee haveownership stakes in the firm, and have a significant portion oftheir net worth invested alongside clients in the variousinvestment products that the firm offers. While none of us atthe Managing Director level have any immediate plans forretirement, our clients should be able to take comfort in thefact that, given the skill sets of our Investment Committeeanalysts, the transition to new leadership when the day comesshould once again be seamless.

The long tenure and dedication of personnel at Tweedy,Browne extends across virtually all departments. For example,the remaining five analysts who do not currently serve on ourInvestment Committee have been employed at Tweedy,Browne for between six and 28 years. The average time inservice at Tweedy of traders on our trading desk is 20 years,and the eight members of our Client Services team have beenat the firm for an average of 13 years. Jason Minard, whoheads our Client Services department, Glenn Finn, our ChiefOperations Officer, and Pat Rogers, our Chief Legal Counsel,are each in their 17th year at the firm; Jane Ciar, our MutualFund Coordinator, is in her 27th year; John Mullahey, thehead of our computer department, is in his 28th year; andMary Gaddist, our Librarian, is in her 36th year at Tweedy,Browne. We have also made it a practice that all departmentheads are responsible for grooming their potential successors,so that we have coverage in the event they get hit by theproverbial bus.

So while the near-term environment has beenchallenging for value investors such as ourselves, the longer-term results of the Funds continue to be strong. Themanagement team that produced these long-term records islargely the same management team that is in place today. Theinvestment approach and process have not changed, and wecontinue to hammer away at our business, day in and day out.

Performance Results

While the Tweedy, Browne Funds and their respectivebenchmark indices finished the six months endedSeptember 30 in the red, relative results for the Funds weremixed. Our two international Funds, the Tweedy, BrowneGlobal Value Fund and the Tweedy, Browne Global ValueFund II – Currency Unhedged, bested their respectivebenchmark indices by a considerable margin, while our twoglobal Funds, the Tweedy, Browne Value Fund and theTweedy, Browne Worldwide High Dividend Yield ValueFund, trailed their respective benchmarks for the period. Nearquarter-end, equity markets began to rebound, and as we writein October, they have regained much of the ground that waslost in August and early September, and the same holds truefor the Tweedy, Browne Funds. Longer-term comparisonsremain more favorable.

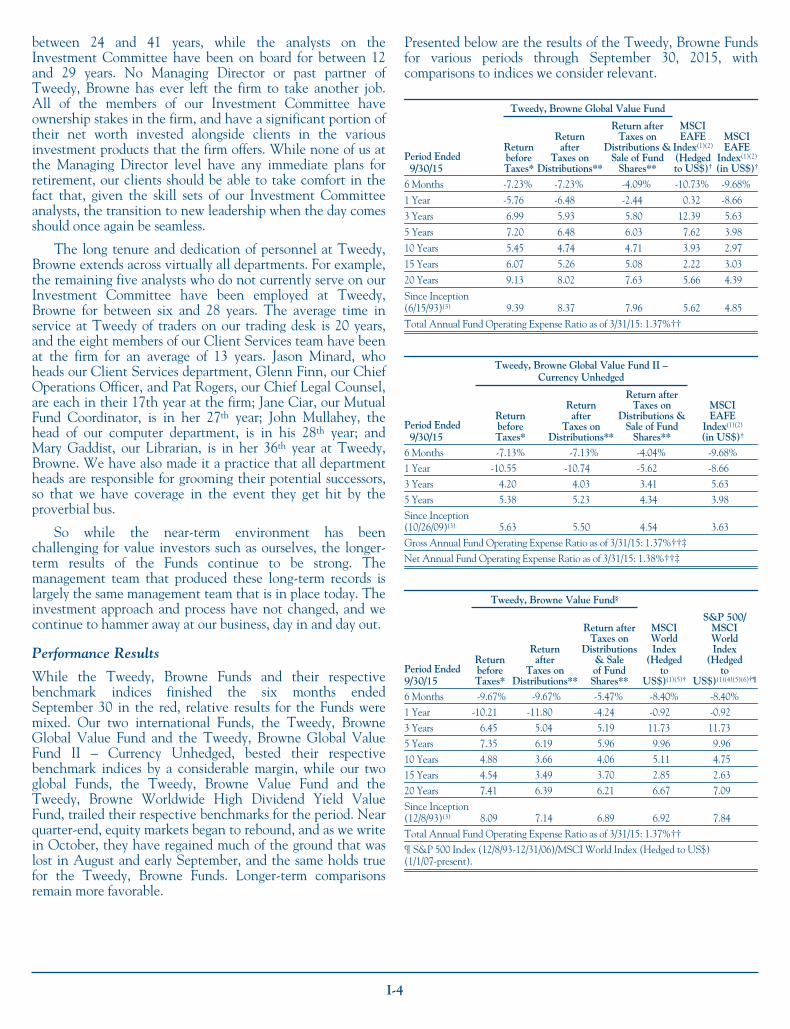

Presented below are the results of the Tweedy, Browne Fundsfor various periods through September 30, 2015, withcomparisons to indices we consider relevant.

Tweedy, Browne Global Value Fund

Period Ended9/30/15

ReturnbeforeTaxes*

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIEAFE

Index(1)(2)

(Hedgedto US$)†

MSCIEAFE

Index(1)(2)

(in US$)†

6 Months -7.23% -7.23% -4.09% -10.73% -9.68%

1 Year -5.76 -6.48 -2.44 0.32 -8.66

3 Years 6.99 5.93 5.80 12.39 5.63

5 Years 7.20 6.48 6.03 7.62 3.98

10 Years 5.45 4.74 4.71 3.93 2.97

15 Years 6.07 5.26 5.08 2.22 3.03

20 Years 9.13 8.02 7.63 5.66 4.39

Since Inception(6/15/93)(3) 9.39 8.37 7.96 5.62 4.85

Total Annual Fund Operating Expense Ratio as of 3/31/15: 1.37%††

Tweedy, Browne Global Value Fund II –Currency Unhedged

Period Ended9/30/15

ReturnbeforeTaxes*

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIEAFE

Index(1)(2)

(in US$)†

6 Months -7.13% -7.13% -4.04% -9.68%1 Year -10.55 -10.74 -5.62 -8.663 Years 4.20 4.03 3.41 5.635 Years 5.38 5.23 4.34 3.98Since Inception(10/26/09)(3) 5.63 5.50 4.54 3.63Gross Annual Fund Operating Expense Ratio as of 3/31/15: 1.37%††‡Net Annual Fund Operating Expense Ratio as of 3/31/15: 1.38%††‡

Tweedy, Browne Value Fund§

Period Ended9/30/15

ReturnbeforeTaxes*

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions& Saleof FundShares**

MSCIWorldIndex

(Hedgedto

US$)(1)(5)†

S&P 500/MSCIWorldIndex

(Hedgedto

US$)(1)(4)(5)(6)†¶

6 Months -9.67% -9.67% -5.47% -8.40% -8.40%1 Year -10.21 -11.80 -4.24 -0.92 -0.923 Years 6.45 5.04 5.19 11.73 11.735 Years 7.35 6.19 5.96 9.96 9.96

10 Years 4.88 3.66 4.06 5.11 4.7515 Years 4.54 3.49 3.70 2.85 2.6320 Years 7.41 6.39 6.21 6.67 7.09

Since Inception(12/8/93)(3) 8.09 7.14 6.89 6.92 7.84

Total Annual Fund Operating Expense Ratio as of 3/31/15: 1.37%††¶ S&P 500 Index (12/8/93-12/31/06)/MSCI World Index (Hedged to US$)(1/1/07-present).

I-4

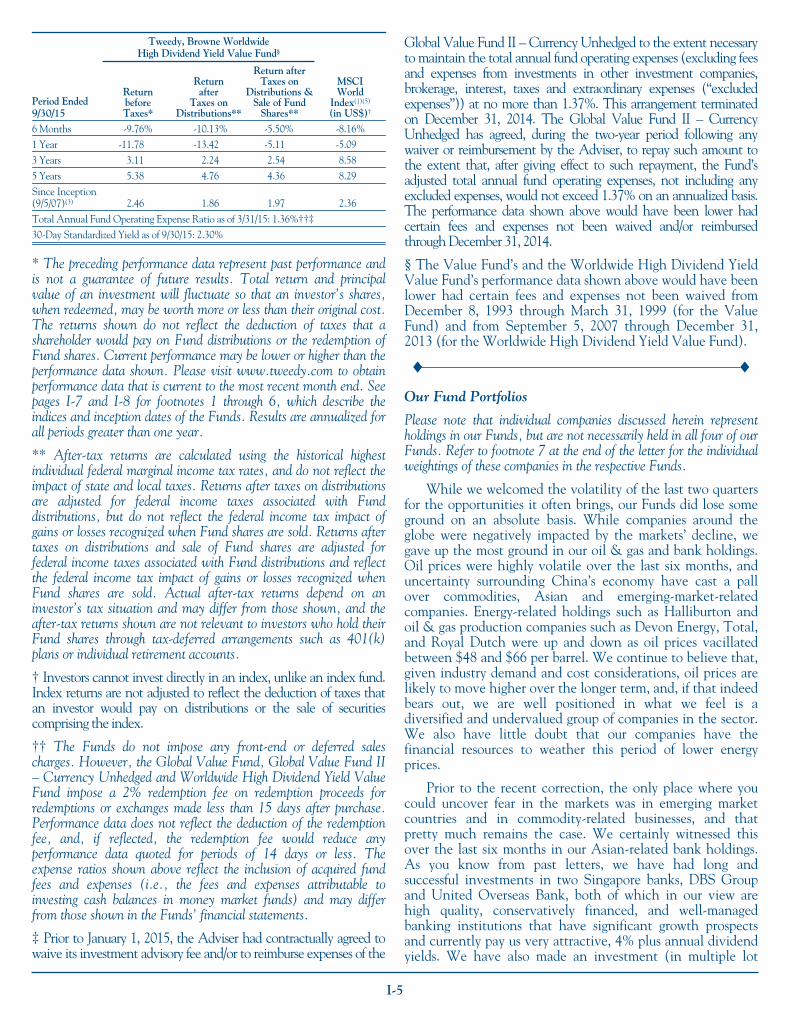

Tweedy, Browne WorldwideHigh Dividend Yield Value Fund§

Period Ended9/30/15

ReturnbeforeTaxes*

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIWorld

Index(1)(5)

(in US$)†

6 Months -9.76% -10.13% -5.50% -8.16%1 Year -11.78 -13.42 -5.11 -5.093 Years 3.11 2.24 2.54 8.585 Years 5.38 4.76 4.36 8.29Since Inception(9/5/07)(3) 2.46 1.86 1.97 2.36Total Annual Fund Operating Expense Ratio as of 3/31/15: 1.36%††‡30-Day Standardized Yield as of 9/30/15: 2.30%

* The preceding performance data represent past performance andis not a guarantee of future results. Total return and principalvalue of an investment will fluctuate so that an investor’s shares,when redeemed, may be worth more or less than their original cost.The returns shown do not reflect the deduction of taxes that ashareholder would pay on Fund distributions or the redemption ofFund shares. Current performance may be lower or higher than theperformance data shown. Please visit www.tweedy.com to obtainperformance data that is current to the most recent month end. Seepages I-7 and I-8 for footnotes 1 through 6, which describe theindices and inception dates of the Funds. Results are annualized forall periods greater than one year.

** After-tax returns are calculated using the historical highestindividual federal marginal income tax rates, and do not reflect theimpact of state and local taxes. Returns after taxes on distributionsare adjusted for federal income taxes associated with Funddistributions, but do not reflect the federal income tax impact ofgains or losses recognized when Fund shares are sold. Returns aftertaxes on distributions and sale of Fund shares are adjusted forfederal income taxes associated with Fund distributions and reflectthe federal income tax impact of gains or losses recognized whenFund shares are sold. Actual after-tax returns depend on aninvestor’s tax situation and may differ from those shown, and theafter-tax returns shown are not relevant to investors who hold theirFund shares through tax-deferred arrangements such as 401(k)plans or individual retirement accounts.

† Investors cannot invest directly in an index, unlike an index fund.Index returns are not adjusted to reflect the deduction of taxes thatan investor would pay on distributions or the sale of securitiescomprising the index.

†† The Funds do not impose any front-end or deferred salescharges. However, the Global Value Fund, Global Value Fund II– Currency Unhedged and Worldwide High Dividend Yield ValueFund impose a 2% redemption fee on redemption proceeds forredemptions or exchanges made less than 15 days after purchase.Performance data does not reflect the deduction of the redemptionfee, and, if reflected, the redemption fee would reduce anyperformance data quoted for periods of 14 days or less. Theexpense ratios shown above reflect the inclusion of acquired fundfees and expenses (i.e., the fees and expenses attributable toinvesting cash balances in money market funds) and may differfrom those shown in the Funds’ financial statements.

‡ Prior to January 1, 2015, the Adviser had contractually agreed towaive its investment advisory fee and/or to reimburse expenses of the

Global Value Fund II – Currency Unhedged to the extent necessaryto maintain the total annual fund operating expenses (excluding feesand expenses from investments in other investment companies,brokerage, interest, taxes and extraordinary expenses (“excludedexpenses”)) at no more than 1.37%. This arrangement terminatedon December 31, 2014. The Global Value Fund II – CurrencyUnhedged has agreed, during the two-year period following anywaiver or reimbursement by the Adviser, to repay such amount tothe extent that, after giving effect to such repayment, the Fund’sadjusted total annual fund operating expenses, not including anyexcluded expenses, would not exceed 1.37% on an annualized basis.The performance data shown above would have been lower hadcertain fees and expenses not been waived and/or reimbursedthrough December 31, 2014.

§ The Value Fund’s and the Worldwide High Dividend YieldValue Fund’s performance data shown above would have beenlower had certain fees and expenses not been waived fromDecember 8, 1993 through March 31, 1999 (for the ValueFund) and from September 5, 2007 through December 31,2013 (for the Worldwide High Dividend Yield Value Fund).

/ /

Our Fund Portfolios

Please note that individual companies discussed herein representholdings in our Funds, but are not necessarily held in all four of ourFunds. Refer to footnote 7 at the end of the letter for the individualweightings of these companies in the respective Funds.

While we welcomed the volatility of the last two quartersfor the opportunities it often brings, our Funds did lose someground on an absolute basis. While companies around theglobe were negatively impacted by the markets’ decline, wegave up the most ground in our oil & gas and bank holdings.Oil prices were highly volatile over the last six months, anduncertainty surrounding China’s economy have cast a pallover commodities, Asian and emerging-market-relatedcompanies. Energy-related holdings such as Halliburton andoil & gas production companies such as Devon Energy, Total,and Royal Dutch were up and down as oil prices vacillatedbetween $48 and $66 per barrel. We continue to believe that,given industry demand and cost considerations, oil prices arelikely to move higher over the longer term, and, if that indeedbears out, we are well positioned in what we feel is adiversified and undervalued group of companies in the sector.We also have little doubt that our companies have thefinancial resources to weather this period of lower energyprices.

Prior to the recent correction, the only place where youcould uncover fear in the markets was in emerging marketcountries and in commodity-related businesses, and thatpretty much remains the case. We certainly witnessed thisover the last six months in our Asian-related bank holdings.As you know from past letters, we have had long andsuccessful investments in two Singapore banks, DBS Groupand United Overseas Bank, both of which in our view arehigh quality, conservatively financed, and well-managedbanking institutions that have significant growth prospectsand currently pay us very attractive, 4% plus annual dividendyields. We have also made an investment (in multiple lot

I-5

purchases over the last two years) in Standard CharteredBank, a UK-headquartered but largely emerging-market-dependent bank that again in our view was conservativelyfinanced by deposits well in excess of loans, and has, in ouropinion, one of the best banking networks across Asia, theMiddle East, Africa and other emerging markets. Unlike ourother Asian bank holdings, Standard Chartered has incurredabove average loan losses and recently replaced seniormanagement and undertaken multiple steps to address whatwe consider to be “fixable” problems. While this process may,and usually does, take longer than expected, we are optimisticthat the bank will be able to get through this difficult period,and ultimately emerge stronger and more profitable. As youcan imagine, given the uncertainty around China’s futuregrowth (as evidenced by the recent devaluation of the yuan),these bank investments have not been getting the votes from“Mr. Market” over the near term; however, over the longerterm, China and other parts of Asia should, in our opinion,continue to grow at rates in excess of the growth rates foundin most of the Western world, and we believe these banksshould remain significant beneficiaries of that growth.

With markets in a state of flux, it was some of the moredefensive components of our Fund portfolios that held up thebest over the six months ended September 30, 2015. Thisincludes food companies such as Nestlé, beverage companiessuch as Heineken, and tobacco holdings such as ImperialTobacco, Philip Morris and British American Tobacco. Wealso had strong results in our more recent Korean autocompany investments, Hyundai Motor and Kia; Safran, theFrench civil jet engine manufacturer; and in Google andMasterCard.

With price volatility on the rise, portfolio activity acrossour Funds also perked up, allowing us to work down the cashreserve positions somewhat in our Fund portfolios. Weestablished new positions in the two Korean automobilecompanies mentioned above, Hyundai Motor and Kia, andadded to our position in the company that supplies them withparts and maintenance, Hyundai Mobis. At purchase,Hyundai Motor, Kia, and Hyundai Mobis were all trading atdiscounts to book value and mid-single digit price/earningsratios. The reputations of these companies in terms of productquality and customer satisfaction have risen dramatically overthe last decade, but a strong Korean won and concerns aboutChinese demand in the near term gave us a pricingopportunity during the summer.

We also established positions in MRC Global, a US-basedbut global producer of pipes, valves, and fittings largely for theoil and gas industry; Ebara, a medium-capitalization Japanesemanufacturer of pumps, compressors, and incinerators; andIBM. All three of these companies at purchase were trading atsignificant discounts from our conservative estimates of theirrespective intrinsic values. In addition, we believe they arefinancially strong and have attractive prospects for futuregrowth in intrinsic value. Moreover, in the case of IBM, itcurrently pays us an attractive dividend yield as we wait forvalue recognition in the market. On the sell side of our Fundportfolios, we did some modest tax loss selling in September,

and trimmed a number of positions across all four Funds thatwere trading at, or marginally above, our estimates of theirintrinsic value.

As we write, all four of our Fund portfolios remain highlydiversified by issue, industry, and country; are composed ofsecurities that, overall, trade at what we believe are reasonablevaluations and that currently pay attractive dividend yields onaverage; and carry meaningful, but declining levels of cashreserves. Should global equity markets continue their advance,our Funds should participate; however, should we revisit theinstability of August and early September, we believe we arewell positioned to take meaningful advantage.

Re-Opening the Tweedy, Browne Global Value Fund II –Currency Unhedged

In the summer of 2014, we closed our unhedged GlobalValue Fund II to new investors as the cash reserve position hadgrown to be greater than 25% of total portfolio assets, and flowsinto the Fund were growing at a rapid pace far in excess of ourability to put the new cash to work in undervalued securities.Today, cash reserves in the Fund represent approximately 15%of total assets, flows have subsided significantly, and theinvestment opportunity set, given the volatility of late, hasimproved somewhat, putting us in a position to re-open theFund for new investments. Barring a substantial change incurrent market conditions or a resumption of rapid inflows nearterm, our intention is to re-open Global Value Fund II to newinvestors in the near future.

Looking Forward

Just five years from now, we will celebrate our 100th yearof operation as an investment organization. This will be quitea landmark for our Firm, and as mentioned earlier, a rareoccurrence in our industry. We have worked hard over theyears to develop what is in essence a “recurring golf swing” inthe investment business – one that we hope will allow forsome consistency of results over the longer term. We believethe case study discussed above and appended heretodemonstrates some success in that regard for the Global ValueFund, but we remain humbled by the day-to-day vagaries ofour capital markets, and how little control we ultimately haveover our investment fortunes in the short run. The stocks weown don’t know that we own them, and therefore do notbehave in ways that are always consistent with our near terminterests. We can ferret out pockets of what we believe to beundervaluation in our markets and individual securities thatoffer clues to future investment opportunity, but we have noassurance as to when, or if, that value will be recognized byother market participants, or by an acquirer.

What we do know is that Graham’s “big idea” hasempirically and practically worked over the long term, and wehave done our best to hone an investment organization thatcan execute on Graham’s promise. One of our ManagingDirectors read a book this past summer called The Boys in theBoat, which is about the University of Washington crew teamand their epic quest for Olympic Gold in the 2,000 meter,eight-oared crew race at the 1936 Berlin Olympics. It is awonderful emotional and historic account of how eight young

I-6

men, mostly from extraordinary hardscrabble backgrounds,came together for a remarkable and unexpected achievement.We were particularly struck by the author’s description of thebenefits associated with a diverse crew, and what it took forthem to find their “swing” on the water. We couldn’t help butthink about our many years at Tweedy, Browne and the crewsthat have made Tweedy what it is today:

Crew races are not won by clones. They are won bycrews, and great crews are carefully balanced blends ofboth physical abilities and personality types. In physicalterms, for instance, one rower’s arms might be longerthan another’s, but the latter might have a stronger backthan the former. Neither is necessarily a better or morevaluable oarsman than the other; both the long arms andthe strong back are assets to the boat. But if they are torow well together, each of these oarsmen must adjust tothe needs and capabilities of the other. Each must beprepared to compromise something in the way ofoptimizing his stroke for the overall benefit of the boat –the shorter-armed man reaching a little farther, thelonger-armed man foreshortening his reach just a bit – sothat both men’s oars remain parallel and both blades enterand exit the water at precisely the same moment …

… Good crews are good blends of personalities: someoneto lead the charge; someone to hold something in reserve;someone to pick a fight; someone to make peace;someone to think things through; someone to chargeahead without thinking. Somehow all this must mesh.That’s the steepest challenge. Even after the right mixtureis found, each man or woman in the boat must recognizehis or her place in the fabric of the crew, accept it, andaccept the others as they are. It is an exquisite thing whenit all comes together in just the right way. The intensebonding and the sense of exhilaration that results from itare what many oarsmen row for, far more than fortrophies or accolades. But it takes young men or womenof extraordinary character as well as extraordinaryphysical ability to pull it off.

- The Boys in the Boat by Daniel James Brown

Thank you for investing with us, and for your continuedconfidence.

Sincerely,

TWEEDY, BROWNE COMPANY LLC

William H. BrowneThomas H. ShragerJohn D. SpearsRobert Q. Wyckoff, Jr.Managing Directors

October 2015

Footnotes:(1) Indexes are unmanaged, and the figures for the indexes

shown include reinvestment of dividends and capital gainsdistributions and do not reflect any fees or expenses.Investors cannot invest directly in an index. We stronglyrecommend that these factors be considered before aninvestment decision is made.

(2) MSCI EAFE Index is an unmanaged capitalization-weighted index of companies representing the stock marketsof Europe, Australasia and the Far East. The MSCIEAFE Index (in US$) reflects the return of the MSCIEAFE Index for a U.S. dollar investor. The MSCI EAFEIndex (Hedged to US$) consists of the results of the MSCIEAFE Index hedged 100% back into U.S. dollars andaccounts for interest rate differentials in forward currencyexchange rates. Results for both indexes are inclusive ofdividends and net of foreign withholding taxes.

(3) Inception dates for the Global Value Fund, Global ValueFund II – Currency Unhedged, Value Fund andWorldwide High Dividend Yield Value Fund are June 15,1993, October 26, 2009, December 8, 1993, andSeptember 5, 2007, respectively. Prior to 2004,information with respect to the MSCI EAFE and MSCIWorld Indexes used was available at month end only;therefore, the since-inception performance of the MSCIEAFE Indexes quoted for the Global Value Fund reflectsperformance from May 31, 1993, the closest month end tothe Global Value Fund’s inception date, and the sinceinception performance of the MSCI World Index quoted forthe Value Fund reflects performance from November 30,1993, the closest month end to the Value Fund’s inceptiondate.

(4) The S&P 500/MSCI World Index (Hedged to US$) is acombination of the S&P 500 Index and the MSCI WorldIndex (Hedged to US$), linked together by Tweedy,Browne Company, and represents the performance of theS&P 500 Index for the periods 12/8/93 – 12/31/06 and theperformance of the MSCI World Index (Hedged to US$),beginning 1/01/07 and thereafter. For the period from theFund’s inception through 2006, the Investment Adviserchose the S&P 500 as the relevant market benchmark.Starting in mid-December 2006, the Fund’s investmentmandate changed from investing at least 80% of its assets inU.S. securities to investing no less than approximately 50%in U.S securities, and the Investment Adviser chose theMSCI World Index (Hedged to US$) as the most relevantbenchmark for the Fund starting January 1, 2007. EffectiveJuly 29, 2013, the Value Fund removed the 50%requirement, and continues to use the MSCI World Index(Hedged to US$) as the most relevant index.

(5) The MSCI World Index is a free float-adjusted unmanagedmarket capitalization weighted index that is designed tomeasure the equity market performance of developedmarkets. The MSCI World Index (in US$) reflects thereturn of this index for a U.S. dollar investor. The MSCIWorld Index (Hedged to US$) consists of the results of the

I-7

MSCI World Index with its foreign currency exposurehedged 100% back into U.S. dollars. The index accountsfor interest rate differentials in forward currency exchangerates. Results for each index are inclusive of dividends andnet of foreign withholding taxes.

(6) The S&P 500 Index is an unmanaged capitalizationweighted index composed of 500 widely held common stocksthat assumes the reinvestment of dividends. The index isgenerally considered representative of U.S. largecapitalization stocks.

(7) As of September 30, 2015, Tweedy, Browne Global ValueFund, Tweedy, Browne Global Value Fund II- CurrencyUnhedged, Tweedy, Browne Value Fund and Tweedy,Browne Worldwide High Dividend Yield Value Fund hadeach invested the following percentages of its net assets,respectively, in the following portfolio holdings: Halliburton(0.7%, 0.6%, 2.0%, 0.0%); Devon Energy (0.5%,0.0%, 2.0%, 0.0%); Total (2.3%, 2.3%, 3.4%, 4.1%);Royal Dutch (1.9%, 1.0%, 2.8%, 3.2%); DBS Group(1.4%, 1.7%, 0.0%, 2.5%); United Overseas Bank(1.4%, 1.5%, 1.3%, 3.2%); Standard Chartered (2.8%,1.9%, 2.6%, 3.1%); Nestlé (2.3%, 2.6%, 3.3%,4.3%); Heineken (2.5%, 1.1%, 3.9%, 0.0%); ImperialTobacco (0.6%, 1.5%, 0.0%, 2.1%); Philip Morris(0.8%, 0.6%, 1.0%, 2.1%); British American Tobacco(0.8%, 0.4%, 0.0%, 0.0%); Hyundai Motor (1.7%,1.8%, 1.6%, 0.0%); Kia (1.3%, 1.8%, 0.9%, 0.0%);Safran (3.3%, 3.0%, 0.0%, 0.0%); Google (1.1%,0.0%, 1.4%, 0.0%); MasterCard (0.0%, 0.8%, 1.7%,0.0%); Hyundai Mobis (0.5%, 0.5%, 0.0%, 0.0%);MRC Global (0.0%, 0.0%, 1.0%, 0.0%); Ebara (0.2%,0.5%, 0.0%, 0.0%); and IBM (0.2%, 0.0%, 0.0%,0.0%).

Current and future portfolio holdings are subject to risk.Investing in foreign securities involves additional risks beyondthe risks of investing in U.S. securities markets. These risksinclude currency fluctuations; political uncertainty; different

accounting and financial standards; different regulatoryenvironments; and different market and economic factors invarious non-U.S. countries. In addition, the securities ofsmall, less well known companies may be more volatile thanthose of larger companies. Value investing involves the riskthat the market will not recognize a security’s intrinsic valuefor a long time, or that a security thought to be undervaluedmay actually be appropriately priced when purchased.Dividends are not guaranteed, and a company currentlypaying dividends may cease paying dividends at any time.Diversification does not guarantee a profit and does notprotect against a loss in declining markets. Please refer to theFunds’ prospectus for a description of risk factors associatedwith investments in securities which may be held by theFunds.

Although the practice of hedging against currency exchangerate changes utilized by the Tweedy, Browne Global ValueFund and Tweedy, Browne Value Fund reduces the risk of lossfrom exchange rate movements, it also reduces the ability ofthe Funds to gain from favorable exchange rate movementswhen the U.S. dollar declines against the currencies in whichthe Funds’ investments are denominated and in some interestrate environments may impose out-of-pocket costs on theFunds.

This letter contains opinions and statements on investmenttechniques, economics, market conditions and other matters.Of course there is no guarantee that these opinions andstatements will prove to be correct, and some of them areinherently speculative. None of them should be relied upon asstatements of fact.

Tweedy, Browne Global Value Fund, Tweedy, Browne GlobalValue Fund II – Currency Unhedged, Tweedy, Browne ValueFund, and Tweedy, Browne Worldwide High Dividend YieldValue Fund are distributed by AMG Distributors, Inc.,Member FINRA/SIPC.

This material must be preceded or accompanied by a prospectus forTweedy, Browne Fund Inc.

I-8

TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment PerformanceTweedy, Browne Global Value Fund

This booklet provides an historical perspective concerning the year-by-year variability of investment returnsfor the Tweedy, Browne Global Value Fund since its inception in 1993, as compared to benchmark indices.The Fund has had an excellent long-term record, which has bested its benchmark by a considerable margin,yet unquestionably the return stream has been lumpy, with numerous periods of underperformance followedby periods of outperformance. (Past performance is no guarantee of future results. See page 1 for the Fund’sperformance records.) We believe it is important for investors to be aware of the general pattern, sequence,and composition of investment returns for the many smaller periods of time that comprise a successful long-term investment track record. You can think of investing as a long-term journey, a veritable marathon, withmany starts, stops, changes of scenery and occasional bumps. Moreover, we believe you will be much morelikely to achieve your investment objectives if you know what to expect along the way. Your ownpsychology and ability to handle the emotional ups and downs of investing are likely to be importantdeterminants of your long-run investment success. If this booklet serves to keep you on your journey,especially when there are some bumps, then we at Tweedy, Browne will have served you well.

September 30, 2015

TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

Notes

Past performance is no guarantee of future results.A fund’s portfolio characteristics are subject to change at any time.

Current and future portfolio holdings are subject to risk. The securities of small, less well-known companies may be more volatilethan those of larger companies. In addition, investing in foreign securities involves additional risks beyond the risks of investing insecurities of U.S. markets. These risks include economic and political considerations not typically found in U.S. markets, includingcurrency fluctuation, political uncertainty and different financial standards, regulatory environments, and overall market andeconomic factors in the countries. These risks are magnified in emerging markets. Value investing involves the risk that the marketwill not recognize a security’s intrinsic value for a long time, or that a security thought to be undervalued may actually beappropriately priced when purchased. Investors should refer to the prospectus for a description of risk factors associated withinvestments in securities held by the Fund.

Although hedging against currency exchange rate changes reduces the risk of loss from exchange rate movements, it also reduces theability of a fund to gain from favorable exchange rate movements when the U.S. dollar declines against the currencies in which thefund’s investments are denominated and in some interest rate environments may impose out-of-pocket costs on the fund.

The MSCI EAFE Index (in US$) is an unmanaged capitalization-weighted index of companies representing the stock markets ofEurope, Australasia and the Far East. Index results are inclusive of dividends and net of foreign withholding taxes. The MSCIEAFE Index (Hedged to US$) consists of the results of the MSCI EAFE Index 100% hedged back into U.S. dollars and accountsfor interest differentials in forward currency exchange rates. Index results are inclusive of dividends and net of foreign withholdingtaxes. Index performance is not representative of Fund performance. Please call (800) 432-4789 or visit www.tweedy.com toobtain Fund performance information. An investor cannot invest directly in an index.

The Tweedy, Browne Global Value Fund, Tweedy, Browne Global Value Fund II – Currency Unhedged, Tweedy, BrowneValue Fund and Tweedy, Browne Worldwide High Dividend Yield Value Fund are distributed by AMG Distributors, Inc.,Member FINRA/SIPC.

This material must be preceded or accompanied by a current prospectus for Tweedy, Browne Fund Inc.

TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

Table of Contents

Page

Tweedy, Browne Global Value Fund Investment Results Since Inception . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

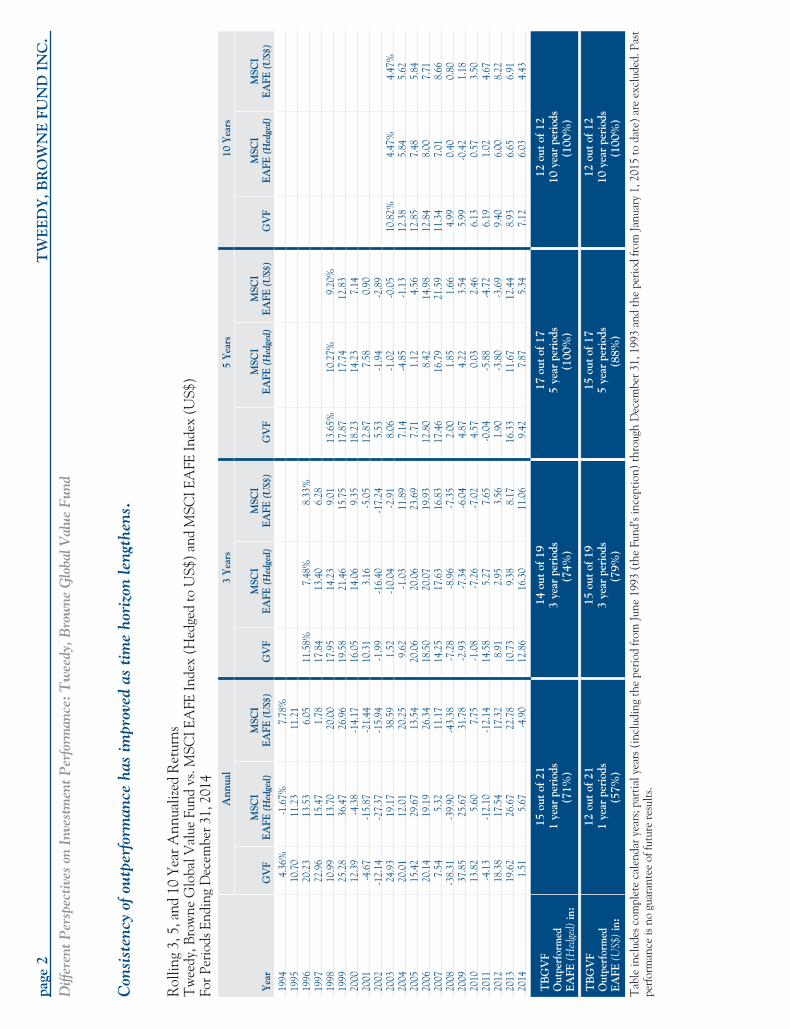

Consistency of outperformance: Rolling 3, 5, and 10 Year Annualized Returns . . . . . . . . . . . . . . . . . . . . . . . 2

Periods of underperformance have generally clustered in very “robust,” speculative market environments: 3-Yearand 5-Year Rolling Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-4

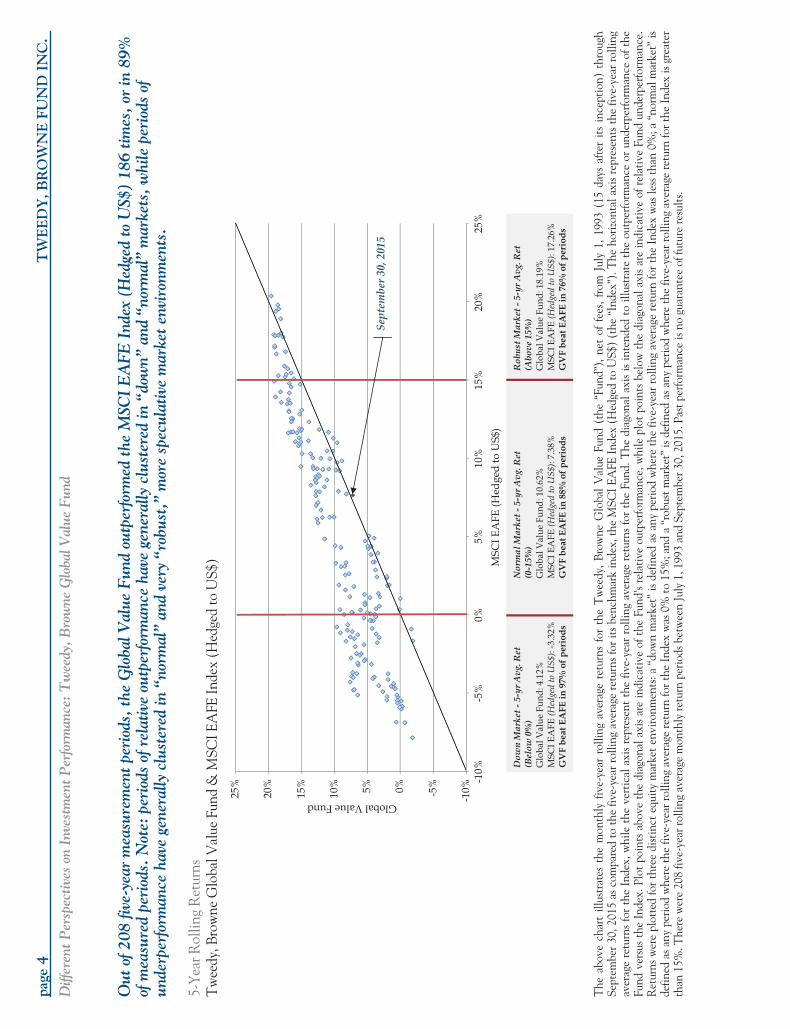

The Ups and Downs of the Tweedy, Browne Global Value Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Performance in Down Market Years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Drawdown: The peak-to-trough decline and subsequent recovery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Upside/Downside Capture Ratio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Tweedy, Browne Global Value Fund: After Tax Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

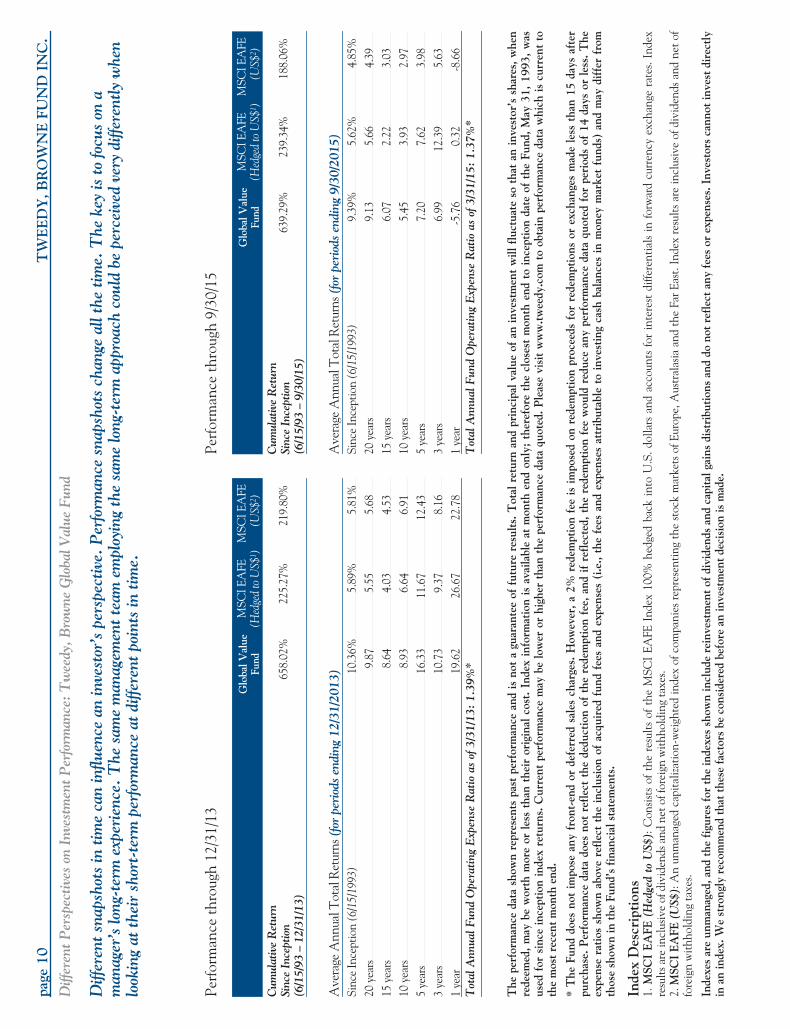

Different snapshots in time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Characteristics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

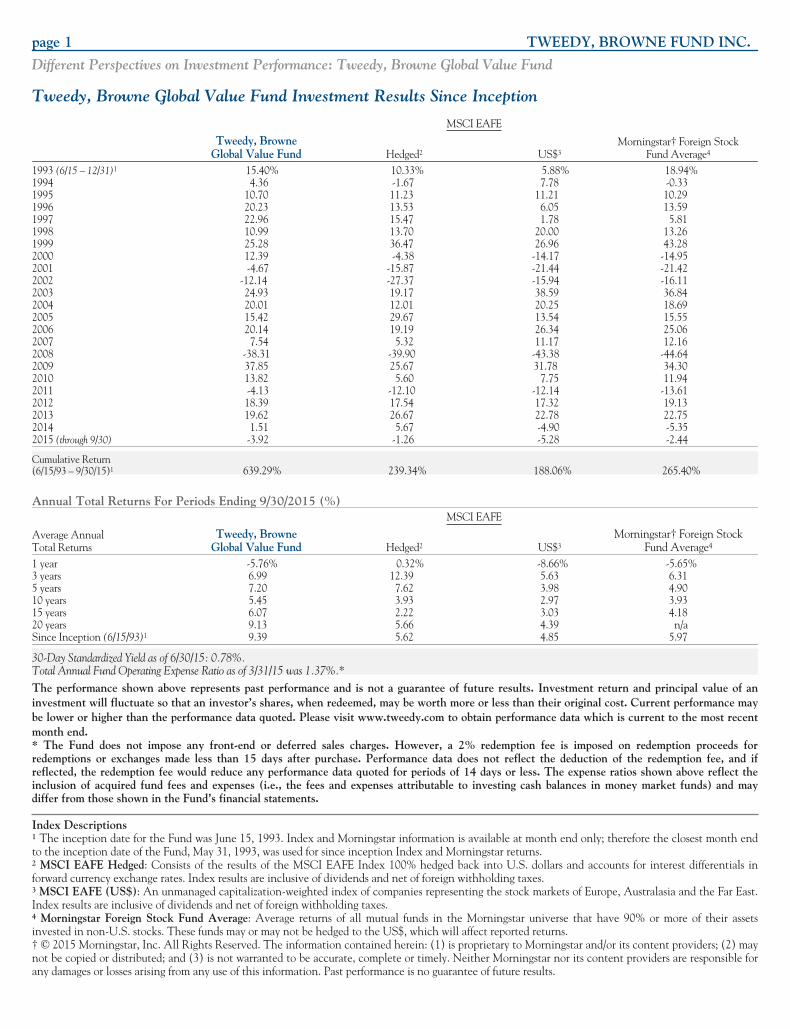

page 1 TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

Tweedy, Browne Global Value Fund Investment Results Since Inception

MSCI EAFE

Tweedy, BrowneGlobal Value Fund Hedged2 US$3

Morningstar† Foreign StockFund Average4

1993 (6/15 – 12/31)1 15.40% 10.33% 5.88% 18.94%1994 4.36 -1.67 7.78 -0.331995 10.70 11.23 11.21 10.291996 20.23 13.53 6.05 13.591997 22.96 15.47 1.78 5.811998 10.99 13.70 20.00 13.261999 25.28 36.47 26.96 43.282000 12.39 -4.38 -14.17 -14.952001 -4.67 -15.87 -21.44 -21.422002 -12.14 -27.37 -15.94 -16.112003 24.93 19.17 38.59 36.842004 20.01 12.01 20.25 18.692005 15.42 29.67 13.54 15.552006 20.14 19.19 26.34 25.062007 7.54 5.32 11.17 12.162008 -38.31 -39.90 -43.38 -44.642009 37.85 25.67 31.78 34.302010 13.82 5.60 7.75 11.942011 -4.13 -12.10 -12.14 -13.612012 18.39 17.54 17.32 19.132013 19.62 26.67 22.78 22.752014 1.51 5.67 -4.90 -5.352015 (through 9/30) -3.92 -1.26 -5.28 -2.44

Cumulative Return(6/15/93 – 9/30/15)1 639.29% 239.34% 188.06% 265.40%

Annual Total Returns For Periods Ending 9/30/2015 (%)MSCI EAFE

Average AnnualTotal Returns

Tweedy, BrowneGlobal Value Fund Hedged2 US$3

Morningstar† Foreign StockFund Average4

1 year -5.76% 0.32% -8.66% -5.65%3 years 6.99 12.39 5.63 6.315 years 7.20 7.62 3.98 4.9010 years 5.45 3.93 2.97 3.9315 years 6.07 2.22 3.03 4.1820 years 9.13 5.66 4.39 n/aSince Inception (6/15/93)1 9.39 5.62 4.85 5.97

30-Day Standardized Yield as of 6/30/15: 0.78%.Total Annual Fund Operating Expense Ratio as of 3/31/15 was 1.37%.*The performance shown above represents past performance and is not a guarantee of future results. Investment return and principal value of aninvestment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance maybe lower or higher than the performance data quoted. Please visit www.tweedy.com to obtain performance data which is current to the most recentmonth end.* The Fund does not impose any front-end or deferred sales charges. However, a 2% redemption fee is imposed on redemption proceeds forredemptions or exchanges made less than 15 days after purchase. Performance data does not reflect the deduction of the redemption fee, and ifreflected, the redemption fee would reduce any performance data quoted for periods of 14 days or less. The expense ratios shown above reflect theinclusion of acquired fund fees and expenses (i.e., the fees and expenses attributable to investing cash balances in money market funds) and maydiffer from those shown in the Fund’s financial statements.

Index Descriptions1 The inception date for the Fund was June 15, 1993. Index and Morningstar information is available at month end only; therefore the closest month endto the inception date of the Fund, May 31, 1993, was used for since inception Index and Morningstar returns.2 MSCI EAFE Hedged: Consists of the results of the MSCI EAFE Index 100% hedged back into U.S. dollars and accounts for interest differentials inforward currency exchange rates. Index results are inclusive of dividends and net of foreign withholding taxes.3 MSCI EAFE (US$): An unmanaged capitalization-weighted index of companies representing the stock markets of Europe, Australasia and the Far East.Index results are inclusive of dividends and net of foreign withholding taxes.4 Morningstar Foreign Stock Fund Average: Average returns of all mutual funds in the Morningstar universe that have 90% or more of their assetsinvested in non-U.S. stocks. These funds may or may not be hedged to the US$, which will affect reported returns.† © 2015 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) maynot be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible forany damages or losses arising from any use of this information. Past performance is no guarantee of future results.

page

2T

WE

ED

Y,B

RO

WN

EFU

ND

INC

.

Diff

eren

tPer

spec

tives

onIn

vest

men

tPer

form

ance

:Tw

eedy

,Bro

wne

Glo

balV

alue

Fund

Con

sist

ency

ofou

tper

form

ance

has

impr

oved

asti

me

hori

zon

leng

then

s.

Rol

ling

3,5,

and

10Ye

arA

nnua

lized

Ret

urns

Tw

eedy

,Bro

wne

Glo

balV

alue

Fund

vs.M

SCIE

AFE

Inde

x(H

edge

dto

US$

)an

dM

SCIE

AFE

Inde

x(U

S$)

ForP

erio

dsEn

ding

Dec

embe

r31,

2014

Ann

ual

3Y

ears

5Y

ears

10Y

ears

Yea

rG

VF

MSC

IEA

FE(H

edge

d)M

SCI

EAFE

(US$

)G

VF

MSC

IEA

FE(H

edge

d)M

SCI

EAFE

(US$

)G

VF

MSC

IEA

FE(H

edge

d)M

SCI

EAFE

(US$

)G

VF

MSC

IEA

FE(H

edge

d)M

SCI

EAFE

(US$

)

1994

4.36

%-1

.67%

7.78

%19

9510

.70

11.2

311

.21

1996

20.2

313

.53

6.05

11.5

8%7.

48%

8.33

%19

9722

.96

15.4

71.

7817

.84

13.4

06.

2819

9810

.99

13.7

020

.00

17.9

514

.23

9.01

13.6

5%10

.27%

9.20

%19

9925

.28

36.4

726

.96

19.5

821

.46

15.7

517

.87

17.7

412

.83

2000

12.3

9-4

.38

-14.

1716

.05

14.0

69.

3518

.23

14.2

37.

1420

01-4

.67

-15.

87-2

1.44

10.3

13.

16-5

.05

12.8

77.

580.

9020

02-1

2.14

-27.

37-1

5.94

-1.9

9-1

6.40

-17.

245.

53-1

.94

-2.8

920

0324

.93

19.1

738

.59

1.52

-10.

04-2

.91

8.06

-1.0

2-0

.05

10.8

2%4.

47%

4.47

%20

0420

.01

12.0

120

.25

9.62

-1.0

311

.89

7.14

-4.8

5-1

.13

12.3

85.

845.

6220

0515

.42

29.6

713

.54

20.0

620

.06

23.6

97.

711.

124.

5612

.85

7.48

5.84

2006

20.1

419

.19

26.3

418

.50

20.0

719

.93

12.8

08.

4214

.98

12.8

48.

007.

7120

077.

545.

3211

.17

14.2

517

.63

16.8

317

.46

16.7

921

.59

11.3

47.

018.

6620

08-3

8.31

-39.

90-4

3.38

-7.2

8-8

.96

-7.3

52.

001.

851.

664.

990.

400.

8020

0937

.85

25.6

731

.78

-2.9

3-7

.34

-6.0

44.

874.

223.

545.

99-0

.42

1.18

2010

13.8

25.

607.

75-1

.08

-7.2

6-7

.02

4.57

0.03

2.46

6.13

0.57

3.50

2011

-4.1

3-1

2.10

-12.

1414

.58

5.27

7.65

-0.0

4-5

.88

-4.7

26.

191.

024.

6720

1218

.38

17.5

417

.32

8.91

2.95

3.56

1.90

-3.8

0-3

.69

9.40

6.00

8.22

2013

19.6

226

.67

22.7

810

.73

9.38

8.17

16.3

311

.67

12.4

48.

936.

656.

9120

141.

515.

67-4

.90

12.8

616

.30

11.0

69.

427.

875.

347.

126.

034.

43

TB

GV

FO

utpe

rfor

med

EAFE

(Hed

ged)

in:

15ou

tof2

11

year

peri

ods

(71%

)

14ou

tof1

93

year

peri

ods

(74%

)

17ou

tof1

75

year

peri

ods

(100

%)

12ou

tof1

210

year

peri

ods

(100

%)

TB

GV

FO

utpe

rfor

med

EAFE

(US$

)in

:

12ou

tof2

11

year

peri

ods

(57%

)

15ou

tof1

93

year

peri

ods

(79%

)

15ou

tof1

75

year

peri

ods

(88%

)

12ou

tof1

210

year

peri

ods

(100

%)

Tab

lein

clud

esco

mpl

ete

cale

ndar

year

s;pa

rtia

lyea

rs(i

nclu

ding

the

perio

dfro

mJu

ne19

93(t

heFu

nd’s

ince

ptio

n)th

roug

hD

ecem

ber3

1,19

93an

dth

epe

riod

from

Janu

ary

1,20

15to

date

)ar

eex

clud

ed.P

ast

perfo

rman

ceis

nogu

aran

tee

offu

ture

resu

lts.

page

3T

WE

ED

Y,B

RO

WN

EFU

ND

INC

.

Diff

eren

tPer

spec

tives

onIn

vest

men

tPer

form

ance

:Tw

eedy

,Bro

wne

Glo

balV

alue

Fund

Out

of23

2th

ree-

year

mea

sure

men

tper

iods

,the

Glo

balV

alue

Fund

has

outp

erfo

rmed

the

MSC

IE

AFE

Inde

x(H

edge

dto

US$

)18

1tim

es,o

rin

78%

ofm

easu

red

peri

ods.

Not

e:pe

riod

sof

rela

tive

outp

erfo

rman

ceha

vege

nera

llycl

uste

red

in“d

own”

and

“nor

mal

”m

arke

ts,w

hile

peri

ods

ofun

derp

erfo

rman

ceha

vege

nera

llycl

uste

red

inve

ry“r

obus

t,”

mor

esp

ecul

ativ

em

arke

tenv

iron

men

ts.

3-Y

earR

ollin

gR

etur

nsT

wee

dy,B

row

neG

loba

lVal

ueFu

nd&

MSC

IEA

FEIn

dex

(Hed

ged

toU

S$)

Dow

n M

arke

t - 3

-yr A

vg. R

etur

n

(Bel

ow 0

%)

Glo

bal V

alue

Fun

d: -0

.57%

M

SCI E

AFE

(Hed

ged

to U

S$):

-8.2

0%G

VF

beat

EA

FE in

100

% o

f per

iods

Nor

mal

Mar

ket -

3-y

r Avg

. Ret

urn

(0-1

5%)

Glo

bal V

alue

Fun

d: 1

2.38

%

MSC

I EA

FE (H

edge

d to

US$

): 8.

36%

GV

F be

at E

AFE

in 8

7% o

f per

iods

Rob

ust M

arke

t - 3

-yr A

vg. R

etur

n (A

bove

15%

) G

loba

l Val

ue F

und:

18.

33%

M

SCI E

AFE

(Hed

ged

to U

S$):

19.0

9%G

VF

beat

EA

FE in

41%

of p

erio

ds

-25%

-15%-5%5%15%

25%

25%

15%

5%-5

%-1

5%-2

5%

Global Value Fund

MSC

I EA

FE (H

edge

d to

US$

)

Sept

embe

r 30,

201

5

The

abov

ech

art

illus

trat

esth

em

onth

lyth

ree-

year

rolli

ngav

erag

ere

turn

sfo

rth

eT

wee

dy,B

row

neG

loba

lV

alue

Fund

(the

“Fun

d”),

net

offe

es,f

rom

July

1,19

93(1

5da

ysaf

ter

itsin

cept

ion)

thro

ugh

Sept

embe

r30

,201

5,as

com

pare

dto

the

thre

e-ye

arro

lling

aver

age

retu

rns

for

itsbe

nchm

ark

inde

x,th

eM

SCI

EAFE

Inde

x(H

edge

dto

US$

)(t

he“I

ndex

”).T

heho

rizon

tala

xis

repr

esen

tsth

eth

ree-

year

rolli

ngav

erag

ere

turn

sfor

the

Inde

x,w

hile

the

vert

ical

axis

repr

esen

tsth

eth

ree-

year

rolli

ngav

erag

ere

turn

sfor

the

Fund

.The

diag

onal

axis

isin

tend

edto

illus

trat

eth

eou

tper

form

ance

orun

derp

erfo

rman

ceof

the

Fund

vers

usth

eIn

dex.

Plot

poin

tsab

ove

the

diag

onal

axis

are

indi

cativ

eof

the

Fund

’sre

lativ

eou

tper

form

ance

,w

hile

plot

poin

tsbe

low

the

diag

onal

axis

are

indi

cativ

eof

rela

tive

Fund

unde

rper

form

ance

.Ret

urns

wer

epl

otte

dfo

rthr

eedi

stin

cteq

uity

mar

kete

nviro

nmen

ts:a

“dow

nm

arke

t”is

defin

edas

any

perio

dw

here

the

thre

e-ye

arro

lling

aver

age

retu

rnfo

rthe

Inde

xw

asle

ssth

an0%

;a“n

orm

alm

arke

t”is

defin

edas

any

perio

dw

here

the

thre

e-ye

arro

lling

aver

age

retu

rnfo

rth

eIn

dex

was

0%to

15%

;and

a“r

obus

tmar

ket”

isde

fined

asan

ype

riod

whe

reth

eth

ree-

year

rolli

ngav

erag

ere

turn

fort

heIn

dex

isgr

eate

rtha

n15

%.T

here

wer

e23

2th

ree-

year

rolli

ngav

erag

em

onth

lyre

turn

perio

dsbe

twee

nJu

ly1,

1993

and

Sept

embe

r30,

2015

.Pas

tper

form

ance

isno

guar

ante

eof

futu

rere

sults

.

page

4T

WE

ED

Y,B

RO

WN

EFU

ND

INC

.

Diff

eren

tPer

spec

tives

onIn

vest

men

tPer

form

ance

:Tw

eedy

,Bro

wne

Glo

balV

alue

Fund

Out

of20

8fiv

e-ye

arm

easu

rem

entp

erio

ds,t

heG

loba

lVal

ueFu

ndou

tper

form

edth

eM

SCI

EA

FEIn

dex

(Hed

ged

toU

S$)

186

times

,or

in89

%of

mea

sure

dpe

riod

s.N

ote:

peri

ods

ofre

lativ

eou

tper

form

ance

have

gene

rally

clus

tere

din

“dow

n”an

d“n

orm

al”

mar

kets

,whi

lepe

riod

sof

unde

rper

form

ance

have

gene

rally

clus

tere

din

“nor

mal

”an

dve

ry“r

obus

t,”

mor

esp

ecul

ativ

em

arke

tenv

iron

men

ts.

5-Ye

arR

ollin

gR

etur

nsT

wee

dy,B

row

neG

loba

lVal

ueFu

nd&

MSC

IEA

FEIn

dex

(Hed

ged

toU

S$)

Dow

n M

arke

t - 5

-yr A

vg. R

et

(Bel

ow 0

%)

Glo

bal V

alue

Fun

d: 4

.12%

M

SCI E

AFE

(Hed

ged

to U

S$):

-3.3

2%

GV

F be

at E

AFE

in 9

7% o

f per

iods

Nor

mal

Mar

ket -

5-y

r Avg

. Ret

(0

-15%

) G

loba

l Val

ue F

und:

10.

62%

M

SCI E

AFE

(Hed

ged

to U

S$):

7.38

%

GV

F be

at E

AFE

in 8

8% o

f per

iods

Rob

ust M

arke

t - 5

-yr A

vg. R

et

(Abo

ve 1

5%)

Glo

bal V

alue

Fun

d: 1

8.19

%

MSC

I EA

FE (H

edge

d to

US$

): 17

.26%

G

VF

beat

EA

FE in

76%

of p

erio

ds

-10%-5%0%5%10%

15%

20%

25% -1

0%

Global Value Fund

MSC

I EA

FE (H

edge

d to

US$

)

Sept

embe

r 30,

201

5

25%

20%

15%

10%

5%0%

-5%

The

abov

ech

art

illus

trat

esth

em

onth

lyfiv

e-ye

arro

lling

aver

age

retu

rns

for

the

Tw

eedy

,B

row

neG

loba

lV

alue

Fund

(the

“Fun

d”),

net

offe

es,

from

July

1,19

93(1

5da

ysaf

ter

itsin

cept

ion)

thro

ugh

Sept

embe

r30

,201

5as

com

pare

dto

the

five-

year

rolli

ngav

erag

ere

turn

sfor

itsbe

nchm

ark

inde

x,th

eM

SCIE

AFE

Inde

x(H

edge

dto

US$

)(t

he“I

ndex

”).T

heho

rizon

tala

xisr

epre

sent

sthe

five-

year

rolli

ngav

erag

ere

turn

sfo

rth

eIn

dex,

whi

leth

eve

rtic

alax

isre

pres

ent

the

five-

year

rolli

ngav

erag

ere

turn

sfo

rth

eFu

nd.T

hedi

agon

alax

isis

inte

nded

toill

ustr

ate

the

outp

erfo

rman

ceor

unde

rper

form

ance

ofth

eFu

ndve

rsus

the

Inde

x.Pl

otpo

ints

abov

eth

edi

agon

alax

isar

ein

dica

tive

ofth

eFu

nd’s

rela

tive

outp

erfo

rman

ce,w

hile

plot

poin

tsbe

low

the

diag

onal

axis

are

indi

cativ

eof

rela

tive

Fund

unde

rper

form

ance

.R

etur

nsw

ere

plot

ted

for

thre

edi

stin

cteq

uity

mar

ket

envi

ronm

ents

:a“d

own

mar

ket”

isde

fined

asan

ype

riod

whe

reth

efiv

e-ye

arro

lling

aver

age

retu

rnfo

rth

eIn

dex

was

less

than

0%;a

“nor

mal

mar

ket”

isde

fined

asan

ype

riod

whe

reth

efiv

e-ye

arro

lling

aver

age

retu

rnfo

rthe

Inde

xw

as0%

to15

%;a

nda

“rob

ustm

arke

t”is

defin

edas

any

perio

dw

here

the

five-

year

rolli

ngav

erag

ere

turn

fort

heIn

dex

isgr

eate

rth

an15

%.T

here

wer

e20

8fiv

e-ye

arro

lling

aver

age

mon

thly

retu

rnpe

riods

betw

een

July

1,19

93an

dSe

ptem

ber3

0,20

15.P

astp

erfo

rman

ceis

nogu

aran

tee

offu

ture

resu

lts.

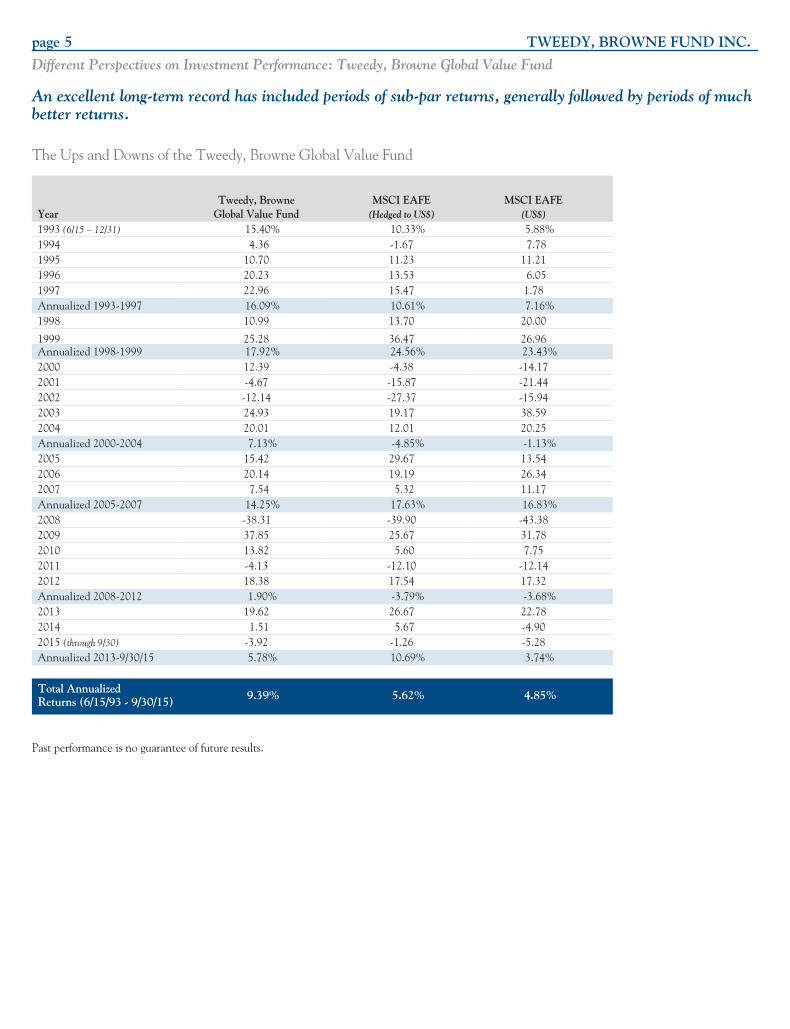

page 5 TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

An excellent long-term record has included periods of sub-par returns, generally followed by periods of muchbetter returns.

The Ups and Downs of the Tweedy, Browne Global Value Fund

YearTweedy, Browne

Global Value FundMSCI EAFE

(Hedged to US$)MSCI EAFE

(US$)

1993 (6/15 – 12/31) 15.40% 10.33% 5.88%1994 4.36 -1.67 7.781995 10.70 11.23 11.211996 20.23 13.53 6.051997 22.96 15.47 1.78Annualized 1993-1997 16.09% 10.61% 7.16%1998 10.99 13.70 20.00

1999 25.28 36.47 26.96Annualized 1998-1999 17.92% 24.56% 23.43%2000 12.39 -4.38 -14.172001 -4.67 -15.87 -21.442002 -12.14 -27.37 -15.942003 24.93 19.17 38.592004 20.01 12.01 20.25Annualized 2000-2004 7.13% -4.85% -1.13%2005 15.42 29.67 13.542006 20.14 19.19 26.342007 7.54 5.32 11.17Annualized 2005-2007 14.25% 17.63% 16.83%2008 -38.31 -39.90 -43.382009 37.85 25.67 31.782010 13.82 5.60 7.752011 -4.13 -12.10 -12.142012 18.38 17.54 17.32Annualized 2008-2012 1.90% -3.79% -3.68%2013 19.62 26.67 22.782014 1.51 5.67 -4.902015 (through 9/30) -3.92 -1.26 -5.28Annualized 2013-9/30/15 5.78% 10.69% 3.74%

Total AnnualizedReturns (6/15/93 - 9/30/15) 9.39% 5.62% 4.85%

Past performance is no guarantee of future results.

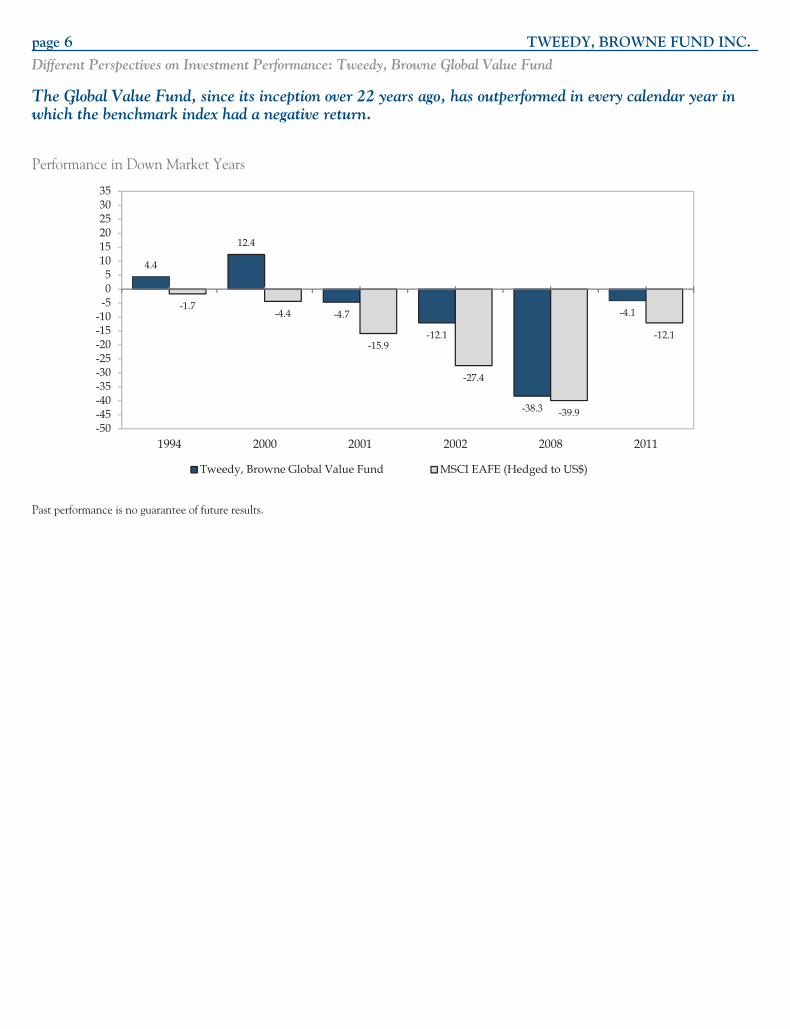

page 6 TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

The Global Value Fund, since its inception over 22 years ago, has outperformed in every calendar year inwhich the benchmark index had a negative return.

Performance in Down Market Years

4.4

12.4

-4.7

-12.1

-38.3

-4.1-1.7-4.4

-15.9

-27.4

-39.9

-12.1

-50-45-40-35-30-25-20-15-10

-505

101520253035

1994

Tweedy, Browne Global Value Fund MSCI EAFE (Hedged to US$)

20112008200220012000

Past performance is no guarantee of future results.

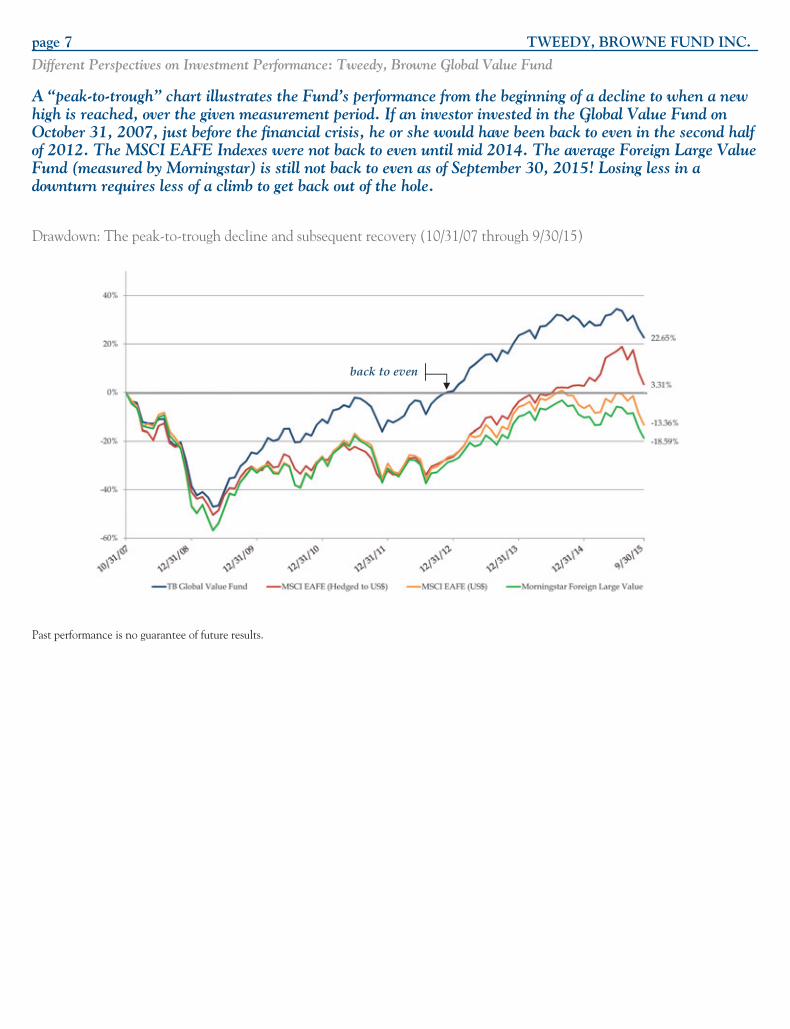

page 7 TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

A “peak-to-trough” chart illustrates the Fund’s performance from the beginning of a decline to when a newhigh is reached, over the given measurement period. If an investor invested in the Global Value Fund onOctober 31, 2007, just before the financial crisis, he or she would have been back to even in the second halfof 2012. The MSCI EAFE Indexes were not back to even until mid 2014. The average Foreign Large ValueFund (measured by Morningstar) is still not back to even as of September 30, 2015! Losing less in adownturn requires less of a climb to get back out of the hole.

Drawdown: The peak-to-trough decline and subsequent recovery (10/31/07 through 9/30/15)

back to even

Past performance is no guarantee of future results.

page 8 TWEEDY, BROWNE FUND INC.

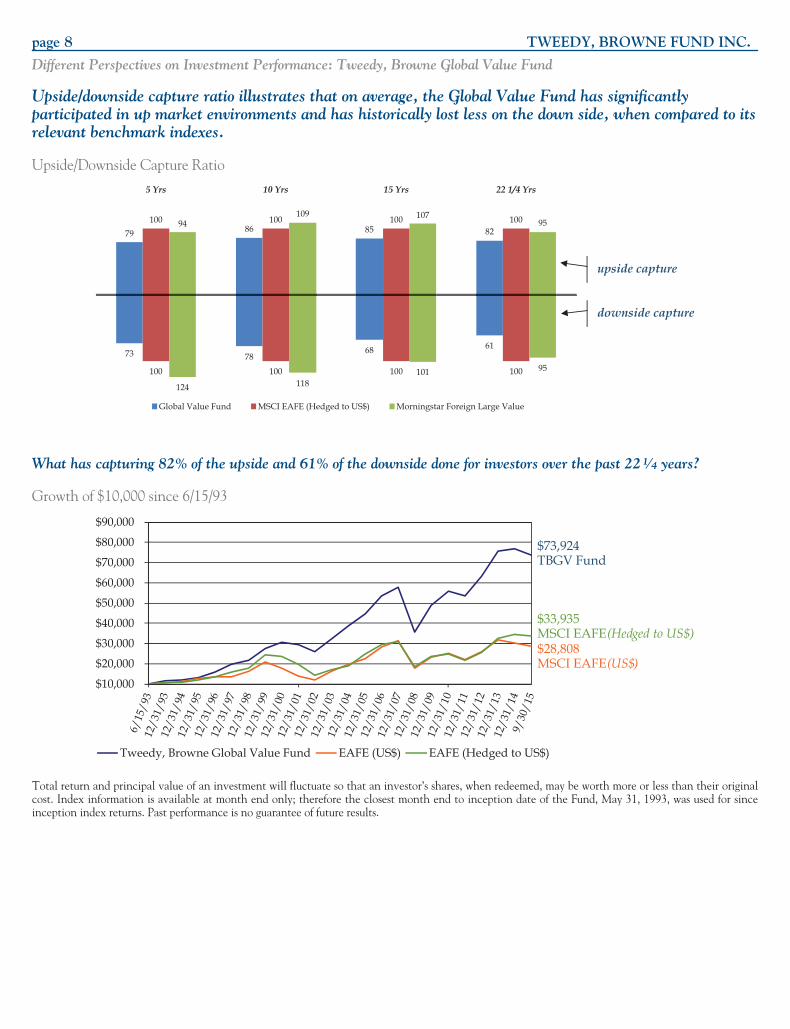

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

Upside/downside capture ratio illustrates that on average, the Global Value Fund has significantlyparticipated in up market environments and has historically lost less on the down side, when compared to itsrelevant benchmark indexes.

Upside/Downside Capture Ratio

79 86 85 82100100100100 94

109 10795

73 7868 61

100100100100

124 118101 95

22 1/4 Yrs15 Yrs10 Yrs5 Yrs

Global Value Fund MSCI EAFE (Hedged to US$) Morningstar Foreign Large Value

upside capture

downside capture

What has capturing 82% of the upside and 61% of the downside done for investors over the past 221⁄4 years?

Growth of $10,000 since 6/15/93

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

Tweedy, Browne Global Value Fund EAFE (US$) EAFE (Hedged to US$)

$73,924 TBGV Fund

$33,935 MSCI EAFE (Hedged to US$)$28,808 MSCI EAFE (US$)

Total return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their originalcost. Index information is available at month end only; therefore the closest month end to inception date of the Fund, May 31, 1993, was used for sinceinception index returns. Past performance is no guarantee of future results.

page 9 TWEEDY, BROWNE FUND INC.

Different Perspectives on Investment Performance: Tweedy, Browne Global Value Fund

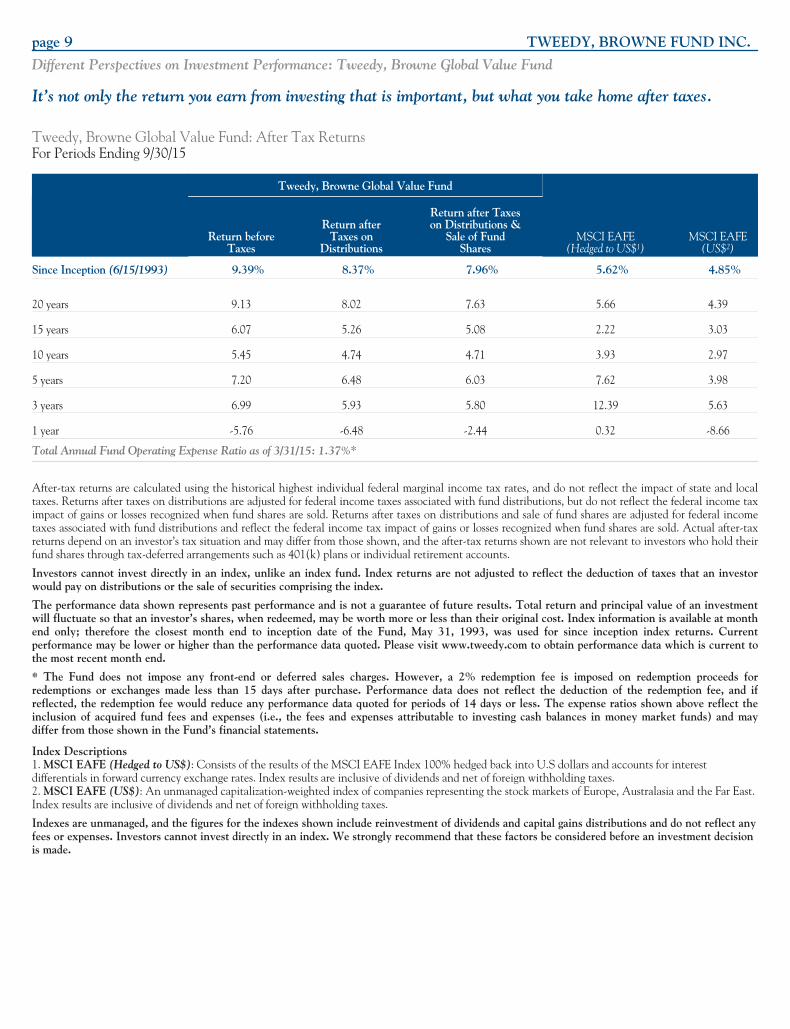

It’s not only the return you earn from investing that is important, but what you take home after taxes.

Tweedy, Browne Global Value Fund: After Tax ReturnsFor Periods Ending 9/30/15

Tweedy, Browne Global Value Fund

MSCI EAFE(Hedged to US$1)

MSCI EAFE(US$2)

Return beforeTaxes

Return afterTaxes on

Distributions

Return after Taxeson Distributions &

Sale of FundShares