IDCEE 2013: Investing in tech startups - Igor Taber (Director for Russia/CIS @ Intel Capital)

Aster Capital – Confidential

Investing in startups in energy, resources and connectivity

A finance guys’ perspective

London, Oct 8th 2014 – Alexander Schlaepfer

Aster Capital – Confidential 2

A unique model to bring value to your business

New Energy Mix

Sustainable Cities

Energy Efficiency

ResourcesManagement

venture Funds ($ 200m)

years of experience(created in 2000)

UNIQUE SPONSORSHIPGLOBAL COVERAGE

offices locations

international team members

Unique access to sponsors' markets and technology experts

Aster Capital – Confidential 3

Cleantech asset class performance

• Listed equities all crashed in 2008

• Cleantech initially did relatively wellbut has been lagging since 2011

• Solar stock recovery from the brinkof bankrupcy drove goodperformance in 2013/2014

• While overall VC portfolios showed10% return p.a. between 2010-2012, Cleantech flatlined

• No exits, no stars (Tesla was 2013)

• Cleantech VC is not a popular assetclass for institutional investorstoday

Underperforming in both – listed and private – equity classes

Aster Capital – Confidential 4

How to make money in a difficult asset class ?

• Steady valuation progression to Exit

• Targeted VC multiples/returns -> entry valuation

• Exit valuations

• Dilution

• Capital Efficiency

• Conclusion

The ingredients of investment performance

Aster Capital – Confidential

Example: Fundraising History

• Production of oils and biofuels by fermentation of microalgae

• Created 2003

• IPO on 02.06.2011

• 2010 KPI

• Revenues: $38m

• EBITDA: ($13.7m)

• Net Income: ($16.3m)

• Shareholders:

• Harris & Harris Group

• Roda Group

• Braemar Energy Ventures

• Lightspeed Venture Partners

• VantagePoint Capital Partners

• Chevron Technology ventures

Solazyme - Valuation History

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1Q2005 2Q2007 3Q2009 3Q2010 2Q2011

A B C D IPO

$ m

illio

n

raised

pre-money

Round A B C D IPO

Year 1Q2005 2Q2007 3Q2009 3Q2010 2Q2011

pre-money 12.8 11.7 144.8 355.8 845.1

raised 8.0 5.0 57.6 60.0 227.2

Market Cap SZYM Oct 2014: $615m

Aster Capital – Confidential

Valuation Progression Analysis

• Fast increase in valuationbefore commercial PoC(volume customers) leads toset-backs

• Amyris

• Valuation trend is exponentialrather than linear

• Reflects time component and gradually declining investment risk

• Higher value of customers (commercial traction) vs. technology

• Keeping it attractive for new investors to join

0%

20%

40%

60%

80%

100%

120%

A B C D E IPO

% o

f final I

PO

valu

e

Valuation Progression US Biofuel IPOspre-money valuation

Amyris KiOR Codexis

Solazyme GEVO Average

Round A B C D E IPO

Amyris 4.2% 74.6% 82.8% 46.3% 85.1% 100%

KiOR 0.3% 1.2% 20.9% 29.0% 100%

Codexis 4.6% 14.3% 47.1% 100%

Solazyme 1.5% 1.4% 17.1% 42.1% 100%

GEVO 5.1% 12.8% 26.2% 29.6% 101.8% 100%

Average 2.8% 22.5% 30.3% 32.3% 78.0% 100.0%

Aster Capital – Confidential

Value of customers (‘proof of value’) vs. technology (‘proof of concept’)

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

A B C D E IPO

% o

f fi

na

l IP

O v

alu

e

Financing Rounds

Valuation Progression US Biofuel IPOs

pre-money valuation

Average valuation

CODEXIS

Signed collaboration with industry leaders (Teva, Pfizer, Shell)

Product revenues: $11M

R&D revenues: $8M

GEVO

Won TOTAL as a strategic investor

Signed Licensing agreement with Cargill

SOLAZYME

Proprietary diesel passed D-975 specification the year before

Various awards

$9M revenues

Proof of concept

‘it works’

Proof of Value‘’customers buy it

– a lot…’

*average valuation excludes Amyris

Aster Capital – Confidential 8

Valuation – VC Target IRR of ~30%

Valuation is primarily driven by expected exit valuationand dilution through future capital raises

Seed Round Series A Series B Seriec C … Exit

Valuation $

10x in 8 years

= 33% IRR

6x in 6 years

= 35%IRR

4x in 4 y

= 32% IRR

2x in 3 y

= 25% (undil.)

Aster Capital – Confidential 9

Growth is the key valuation driver in M&A and IPO’s

Valuation drivers – MIT study on 786 MedTech transactions, 1996 - 2008

Aster Capital – Confidential 10

Cleantech: all segments

Revenue Multiple vs. Sales Growth

• Recurring revenues and their visibility are theprimary value driver

• Second is scalability -> the cost/CAPEX foradding another user (or $ of revenue)

• At >20% growth, valuation of 4x revenues isalmost guaranteed

Software: SaaS business models

Source: Sand Hill Source: Aster, with data from Baird Energy Technology Monthly, June 2014

• Few ‘subscriber’ business models

• Capital intensive business models

• Average sector growth is lower (19% vs. 26%)

• With >20% growth, valuation can still be <1x revenues. Hardly any multiples >4x

Aster Capital – Confidential 11

Revenue Multiples vs. Sales GrowthCapital intensive Cleantech segments show poor correlation

Solar PV manufacturing

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 0.5 1 1.5 2 2.5 3

Revenue to Marketcap Multiple H1/2014

An

nu

al R

even

ue G

row

th

(fw

d)

PV Project Developers & EPC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 2 4 6 8 10 12 14

Revenue to Marketcap Multiple H1/2014

An

nu

al R

even

ue G

row

th

(fw

d)

Energy Storage

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 1 2 3 4 5 6

Revenue to Market Cap Multiple H1/2014

An

nu

al R

even

ue G

row

th

(fw

d)

Turbine Equipment (Wind, Heat, Gas)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 0.5 1 1.5 2 2.5

Revenue to Marketcap Multiple H1/2014

An

nu

al R

even

ue G

row

th

(fw

d)

Source: Aster, with data from Baird Energy Technology Monthly, June 2014

Aster Capital – Confidential 12

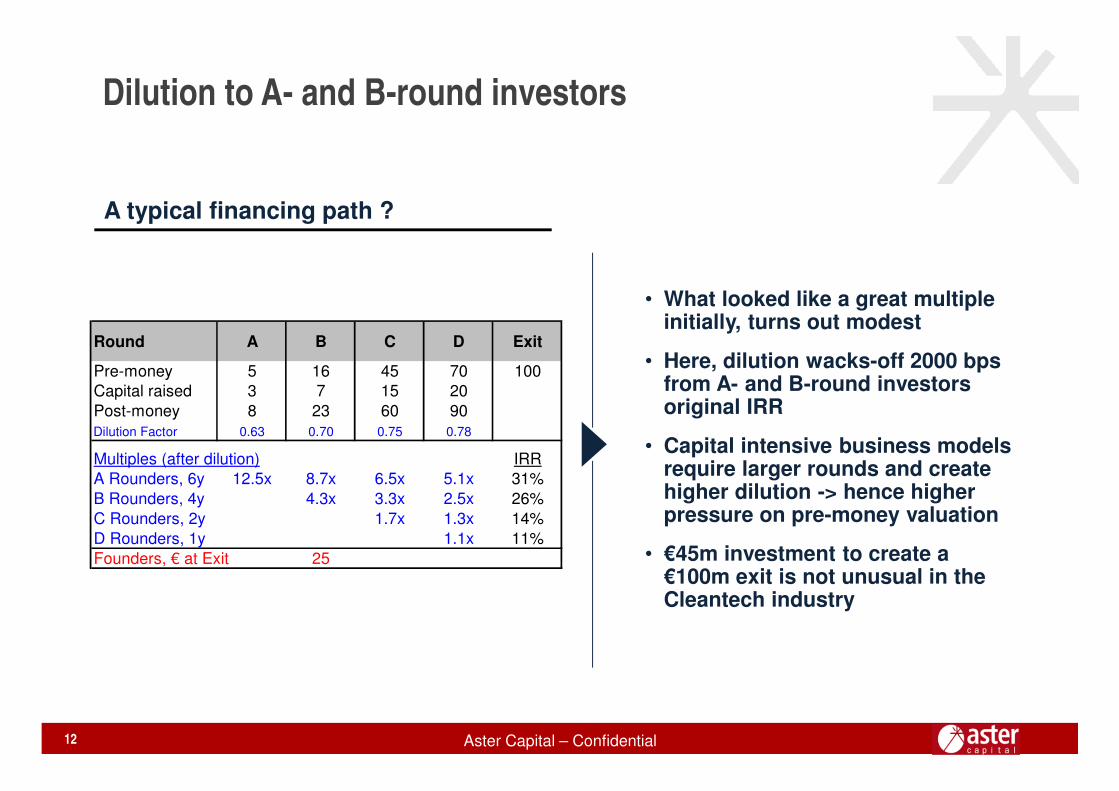

Dilution to A- and B-round investors

• What looked like a great multiple initially, turns out modest

• Here, dilution wacks-off 2000 bps from A- and B-round investorsoriginal IRR

• Capital intensive business modelsrequire larger rounds and createhigher dilution -> hence higherpressure on pre-money valuation

• €45m investment to create a €100m exit is not unusual in theCleantech industry

A typical financing path ?

Round A B C D Exit

Pre-money 5 16 45 70 100Capital raised 3 7 15 20

Post-money 8 23 60 90Dilution Factor 0.63 0.70 0.75 0.78

Multiples (after dilution) IRRA Rounders, 6y 12.5x 8.7x 6.5x 5.1x 31%

B Rounders, 4y 4.3x 3.3x 2.5x 26%

C Rounders, 2y 1.7x 1.3x 14%

D Rounders, 1y 1.1x 11%

Founders, € at Exit 25

Aster Capital – Confidential 13

Capital Efficiency

vs. the Cleantech world:

• €10m CAPEX for non-commercial pilotplant (technical PoC) ?

• €10m CAPEX in a commercialproduction plant that could produce for€10m p.a. in revenues ?

• Finding other people to make thatinvestment

• Grants, suppliers, customers

Turning one VC-€ into €10 (or €200)

or

Aster Capital – Confidential 14

Conclusions

• New Solar PV installations are at 52GW this year – even IEA now acknowledgesthat renewables are the future

• Utility business model is being re-invented -> distributed energy resoures

• Manufacturing industry is now seriouslydriving energy efficiency projects

• The ‘sharing economy’ is transformingthe transportation industry

But we need to be more intelligent

• Innovate where there is a real customer demand

• Watch valuation: customers andsales are the main value driver

• Watch capital efficiency -> is themoney we raise really creatingvalue ?

Cleantech is not ‘over’

Aster Capital – Confidential

Breakthrough liquid cooling technology for data centers.

Aster’s last investments

Leading modeling platform for complex systems.

15

Thank you!Aster Capital 7, bd Malesherbes 75008 Paris +33 1 45 61 30 95 www.aster.com

Aster Capital – Confidential 16

Energyconversion

Sustainableresources

Smart buildings

Industrialefficiency

Reliable energysupply

Intelligent Infrastructure

Advanced materials

Mobility

Aster focuses on Energy and Resources Innovation