INVESTED - overend.co.za · Ditabe Chocho CA(SA) ... The Venture invested in energy efficient...

28

`+ INVESTED IN LONG-TERM SUSTAINABLE PARTNERSHIPS MERAFE RESOURCES LIMITED Merrill Lynch 14 th Annual Sun City Conference March 2013 Presented by Zanele Matlala (CEO)

Transcript of INVESTED - overend.co.za · Ditabe Chocho CA(SA) ... The Venture invested in energy efficient...

`+

INVESTED IN LONG-TERM SUSTAINABLE

PARTNERSHIPS

MERAFE RESOURCES LIMITED

Merrill Lynch 14th Annual Sun City Conference

March 2013

Presented by Zanele Matlala (CEO)

Legal notice/disclaimer

This presentation is published solely for informational purposes and does not constitute investment,

legal, tax or other advice nor is it to be relied upon in making an investment decision. Information

contained herein has been taken from sources considered by Merafe Resources to be reliable but no

warranty is given that such information is accurate or complete and it should not be relied upon as

such. Views and opinions expressed in this presentation reflect the judgment of Merafe Resources as

of the date of this presentation and are subject to change. Merafe Resources will not be responsible

for any liability for loss or damage of any kind which arises, directly or indirectly, and is caused by the

use of any of the information provided. The entire presentation is subject to copyright with all rights

reserved. The information contained herein shall not be published, rewritten for broadcast or

publication or redistributed in any medium without prior written consent from Merafe Resources.

Prospective investors should take appropriate investment advice and inform themselves as to

applicable legal requirements, exchange control regulations and tax considerations in the countries of

their citizenship, residence or domicile. The distribution of the information contained in this

presentation in certain countries may be restricted by law and persons who access it are required to

inform themselves and to comply with any such restrictions. This information does not constitute an

offer or solicitation in any jurisdiction in which such an offer or solicitation is not authorised or to any

person to whom it is unlawful to make such an offer or solicitation. Past performance is not a

guarantee of future performance. The price of shares can go down as well as up and may be affected

by change in exchange rates, market conditions and risks associated with a mining venture.

2

3

Agenda

1. Corporate and Operational Overview

2. Key Drivers

3. Challenges

4. Outlook

Annexures

3

Corporate and

Operational

Overview

The Tswelopele pelletising and

sintering plant

North West province

5

Experienced Management Team focused on delivering returns

Bruce McBride – Commercial Director

• Joined Merafe in 2001 as Commercial Director

• Formerly a Senior Partner at law firm Bell, Dewar and Hall where he specialised in commercial

litigation, banking and mining law

Zanele Matlala CA(SA) – Chief Executive Officer

• Appointed CFO in October 2010 having been on the Merafe Board as a non-executive director since 2005. Appointed CEO in June 2012

• Extensive financial experience at Industrial Development Corporation and formerly CFO of Kagiso Investments and Development Bank of Southern Africa

Ditabe Chocho CA(SA) – Chief Financial Officer

• Appointed CFO on 2 January 2013

• Extensive experience in financial and investment management gained during his tenure at various companies including ZICO Capital, Aflease Gold and Uranium Limited and Transnet

Kajal Bisessor CA(SA) – Finance and IR Manager

• Joined Merafe as Financial Controller in March 2009 and was appointed to current position in June 2010

• Formerly worked at KPMG as Audit Manager

Dr Jurg Zaayman – General Manager, Merafe Chrome

• Joined Merafe in 2001 as Operations Manager and became General Manager of the Boshoek plant

• In 2004 seconded to the Xstrata-Merafe Chrome Venture and was the project leader for the Bokamoso pelletising plant before being appointed to his current position in 2007

6

Largest Ferrochrome Producer in the World

Xstrata-Merafe Venture

Formed 1 July 2004

20.5% of EBITDA 79.5% of EBITDA

Investor Profile

Ticker: MRF

Market Cap* : R2bn

Share price* : 78 cents

52 week high : 95 cents

52 week low : 64 cents

* As at 11 March 2013

6

7

On 1 July 2004 Merafe pooled assets with Xstrata to form the

Xstrata-Merafe Chrome Venture

7 Merafe is represented at all levels of the Xstrata Merafe Chrome Venture

Xstrata-Merafe Chrome Venture

EXCO

20.5% of EBITDA 79.5% of EBITDA

Joint Board

Treasury Audit SHEQ Trans-

formation Operations Marketing

8

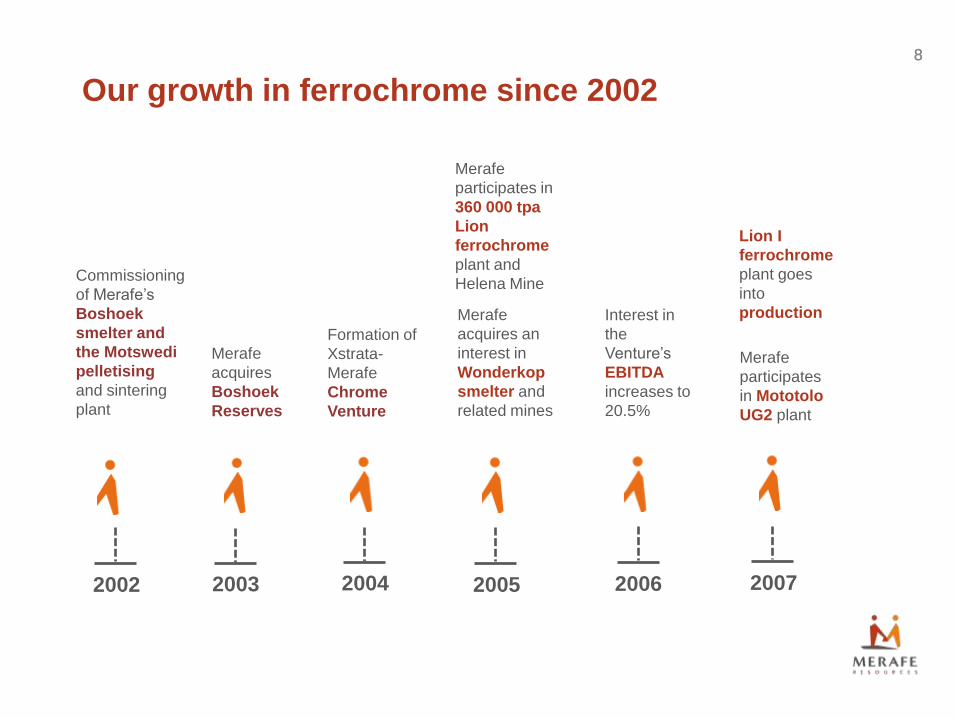

Our growth in ferrochrome since 2002

8

Commissioning

of Merafe’s

Boshoek

smelter and

the Motswedi

pelletising

and sintering

plant

Merafe

acquires

Boshoek

Reserves

Formation of

Xstrata-

Merafe

Chrome

Venture

Merafe

participates in

360 000 tpa

Lion

ferrochrome

plant and

Helena Mine

Merafe

acquires an

interest in

Wonderkop

smelter and

related mines

Interest in

the

Venture’s

EBITDA

increases to

20.5%

Lion I

ferrochrome

plant goes

into

production

Merafe

participates

in Mototolo

UG2 plant

2002 2004 2003 2005 2006 2007

9

Our growth in ferrochrome since 2002

9

Merafe

participates in

Bokamoso

pelletising

and sintering

plant

Merafe

participates in

expansionary

projects

including

Horizon and

Waterval

mines

Merafe

participates in

Lion II and

the

development

of Magareng

Mine

Project

Tswelopele

in

production

Lion II

ferrochrome

plant

scheduled for

commissioning

Merafe

participates in

Tswelopele

pelletising

and sintering

plant and K1

and K2 UG2

plants

2008 2009 2010 2011 2013 2012

10 Project Lion Phase II - 360,000 tonnes of ferrochrome

capacity

Project Rationale:

− Positioning the Venture to be one of the first movers in the ferrochrome industry, underpinned

by favourable supply-demand fundamentals

− Expected to reduce the total costs of the Venture’s ferrochrome production by 6%

Cost

− Total cost of R4,9bn (R4,2bn smelter & R700m mine) of which 50% was spent up until 31

Dec 2012

− Merafe’s 20.5% portion at cost is R1bn

Valuation

− IRR in excess of 20%

Commissioning

− Expected to be commissioned in the second half of 2013

Financing

− Combination of existing / future cash flows and debt

Sustainability

− Investment in community upliftment, job creation - is expected to result in 1 000 permanent

jobs and 1 800 jobs in the construction phase

− Investment in housing development in one of the poorest regions in SA

− Environmental - 30% less solid waste (slag and slimes)

10

11 What sets us apart from the competition

11

Lower quartile of the ferrochrome

cost curve with the gap widening

Energy efficient technology

reducing impact of high

electricity costs in SA

Secure long-term supply of ore

reserves

Strong Balance Sheet and proven

track record

Organic growth in ferrochrome –

Lion II

12

Shareholder Base

12

29%

22%

40%

9%

Royal Bafokeng

IDC

SA Free Float

Offshore Free Float

13

Global Chrome Reserves favour South Africa

13

4%

12%

11%

73%

Kazakhstan

Zimbabwe

Others

South Africa

14 Geographical Distribution Provides Competitive

Advantage

14

Lion I

Lydenburg

Helena & Magareng

Thorncliffe

Horizon

Boshoek

Rustenburg

Kroondal

Waterval East & West

Wonderkop Johannesburg

Wonderkop

Boshoek

New Project- Lion II

Mototolo UG2

Impala UG2

K1 & K2 UG2 Eland UG2

EPL UG2

Chrome ore

- 9 mines, chrome mineral resources in

excess of 450 Megatonnes, 6 UG2

plants and long-term supply

agreements with major

SA platinum producers

Ferrochrome

- 20 furnaces - 1.979 million tonnes

installed ferrochrome capacity per

annum

Key Drivers

Production Engineer,

Charlotte Ntsole, at work

on the new Tswelopele

pelletising and sintering plant

North West province

16

Key Drivers

Market

− Stainless steel production

− Ferrochrome demand

− Ferrochrome supply

Costs

− Labour

− Electricity

Pricing and foreign exchange

16

17

Global stainless steel production

3% increase in

stainless steel production

Heinz H. Pariser /Feb 2013

17

1% 4% 9%

3% 3%

1%

9%

3%

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

Others NAFTA India Japan S Korea / Taiwan

EU China Total

2011 ACTUAL TONNES in '000

2012 ESTIMATED TONNES in '000

1 1

07

1 1

14

2 0

74

1 9

85

2 2

65

2 4

69

3 2

56

3 1

73

3 3

60

3 2

43

7 5

59

7 4

47

14 4

60

15 7

30

34 0

81

35 1

61

18

Global ferrochrome demand

2% increase in

Ferrochrome demand

Heinz H. Pariser /Feb 2013

18

-

2 000

4 000

6 000

8 000

10 000

12 000

NAFTA India Japan Others S Korea / Taiwan

EU China Total

2011 ACTUAL TONNES in '000

2012 ESTIMATED TONNES in '000

4 5

96

4 8

42

9 5

54

9 7

34

4% 4% 0.1%

0.1%

5%

2%

469

462

553

495

695

664

752

781

767

766

1 7

22

1 7

24

1% 10%

19

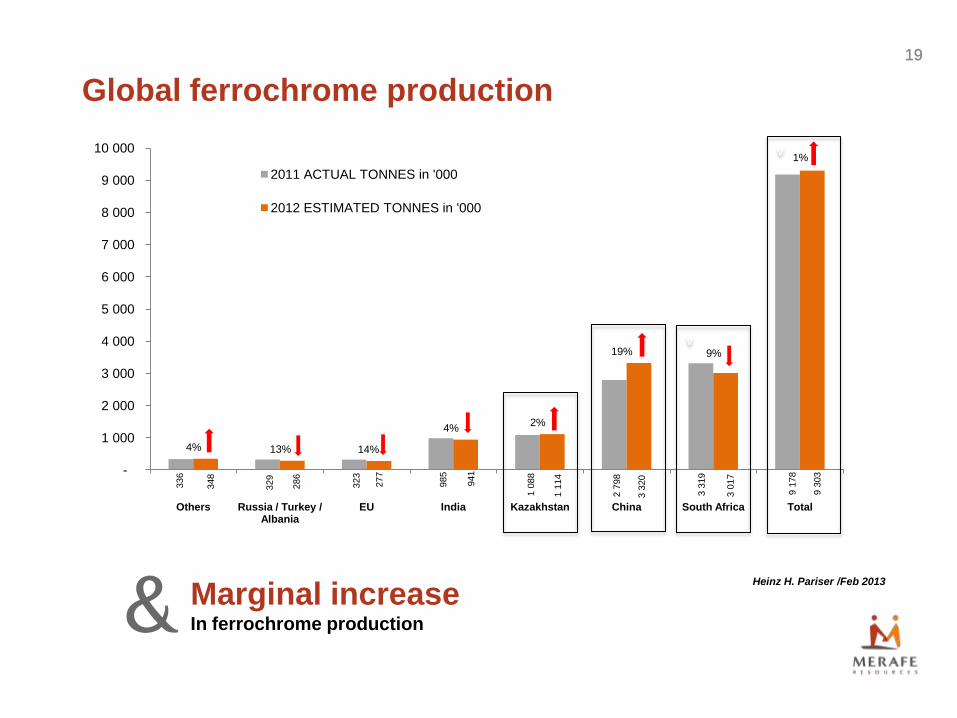

Global ferrochrome production

Marginal increase In ferrochrome production

Heinz H. Pariser /Feb 2013

19

4% 13% 14%

4% 2%

19% 9%

1%

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

Others Russia / Turkey / Albania

EU India Kazakhstan China South Africa Total

2011 ACTUAL TONNES in '000

2012 ESTIMATED TONNES in '000

v

v

336

348

329

286

323

277

985

941

1 0

88

1 1

14

2 7

98

3 3

20

3 3

19

3 0

17

9 1

78

9 3

03

The Lion ferrochrome plant at Steelpoort

Limpopo province

Challenges

21

Challenges

Chrome ore exports

Rising costs

− Electricity

− Labour

21

22

Chrome ore imports into China remain significant

2012

‘000

2011

‘000

2010

‘000

% change

2012/2011

South Africa 4 490 4 675 3 100 (4.0)

Turkey 1 840 1 612 1 933 14.1

Oman 426 645 902 (34.0)

India 310 439 389 (29.4)

Pakistan 472 440 512 7.3

Albania 305 357 363 (14.6)

Iran 448 330 350 35.8

Zimbabwe 1 212 160 (99.5)

Madagascar 118 86 115 37.2

Australia 501 208 201 140.9

Phillipines 180 137 150 31.4

Brazil 29 60 77 (51.7)

Kazakhstan 89 94 243 (5.3)

Others 91 149 172 (38.9)

Total 9 300 9 444 8 667 (1.5)

Heinz H. Pariser, Alloy Metals and Steel Market Research

What are we doing about this? – discussions with DMR are continuing

22

23

The Venture invested in energy efficient technologies

to counter the rising costs of electricity

Average energy efficiency improvements the Venture has achieved and expects to

achieve

This improvement

represents more than

25% in energy

efficiency over the past

decade.

MW

h/t

Ventu

re t

echnolo

gy

23

Outlook

The Lion ferrochrome plant at Steelpoort

Limpopo province

25 Positive long-term outlook

– Projected 5% CAGR in stainless global steel industry fuels ongoing demand for

ferrochrome

– Long-term demand fundamentals remain strong as China continues to expand

– The Xstrata-Merafe Venture will retain advantage as lowest cost SA producer

― outstanding historical cost performances of furnaces

― continuous electrical energy improvements that clearly set us apart from the rest

– Strong Balance Sheet enables the Company to take advantage of global economic

recovery

– Diversification opportunities will be explored post Lion II commissioning

25

Questions

26

Annexures

Lion II ferrochrome plant under construction

Limpopo province

Abridged Audited Group Annual Financial

Statements for 2012

28