Inventory Management. Overview To hold or not to hold To hold or not to hold Types of inventory...

25

Inventory Inventory Management Management

-

date post

20-Dec-2015 -

Category

Documents

-

view

233 -

download

1

Transcript of Inventory Management. Overview To hold or not to hold To hold or not to hold Types of inventory...

Inventory Inventory ManagementManagement

OverviewOverview

To hold or not to holdTo hold or not to hold

Types of inventoryTypes of inventory

Pareto principalPareto principal

ABC analysisABC analysis

Cycle countingCycle counting

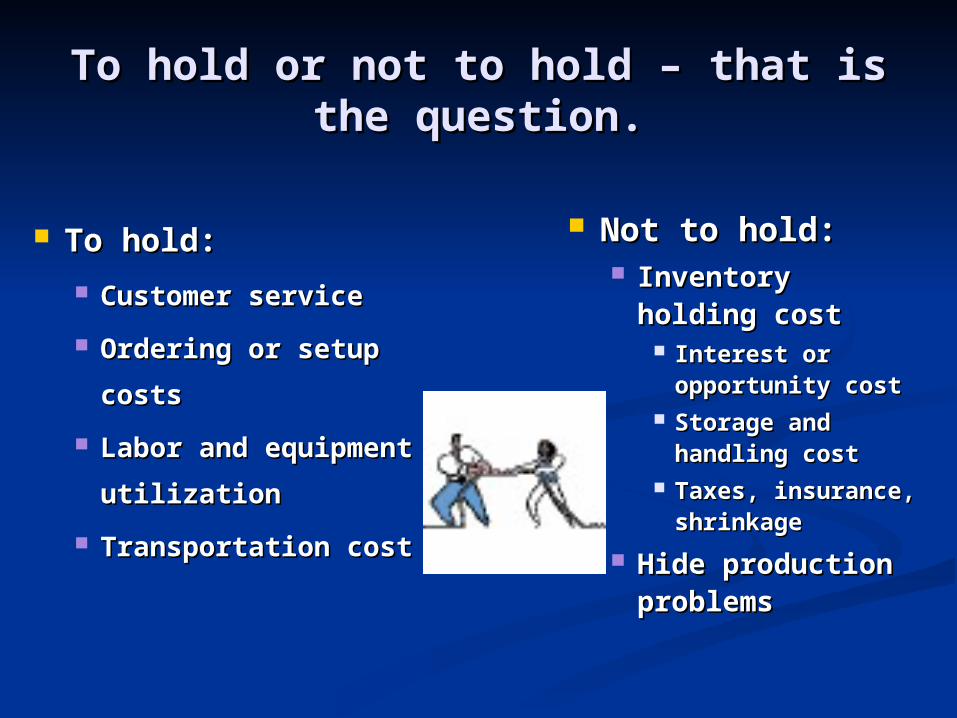

To hold or not to hold – that is the To hold or not to hold – that is the question.question.

To hold:To hold:

Customer serviceCustomer service

Ordering or setup Ordering or setup

costscosts

Labor and Labor and

equipment equipment

utilizationutilization

Transportation costTransportation cost

Not to hold:Not to hold: Inventory Inventory

holding costholding cost Interest or Interest or

opportunity costopportunity cost Storage and Storage and

handling costhandling cost Taxes, insurance, Taxes, insurance,

shrinkageshrinkage

Hide production Hide production problemsproblems

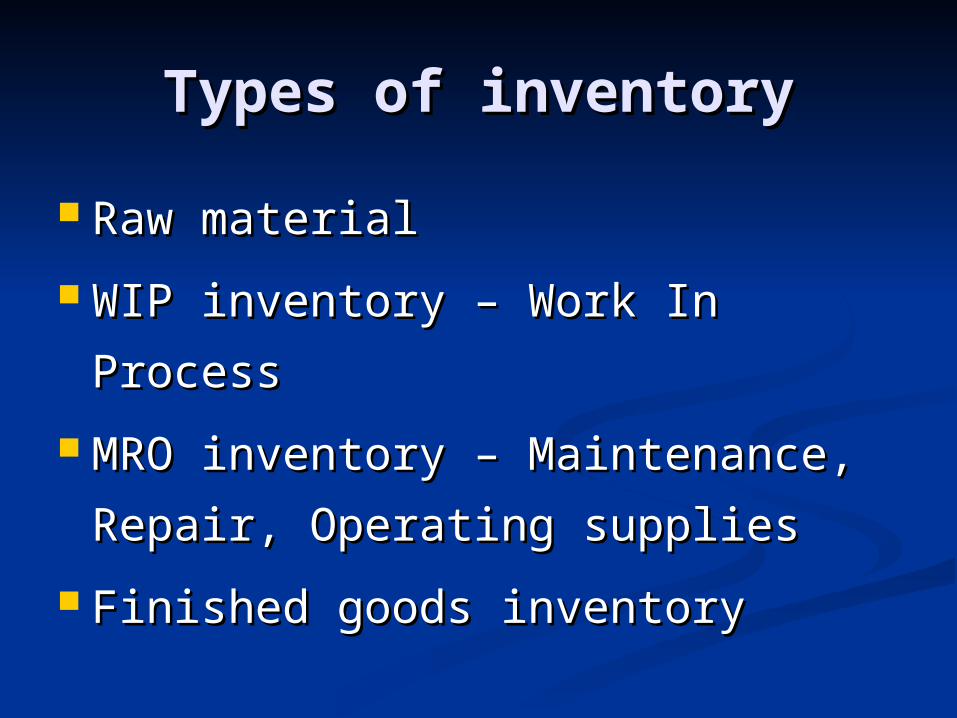

Types of inventoryTypes of inventory

Raw materialRaw material

WIP inventory – Work In ProcessWIP inventory – Work In Process

MRO inventory – Maintenance, MRO inventory – Maintenance,

Repair, Operating suppliesRepair, Operating supplies

Finished goods inventoryFinished goods inventory

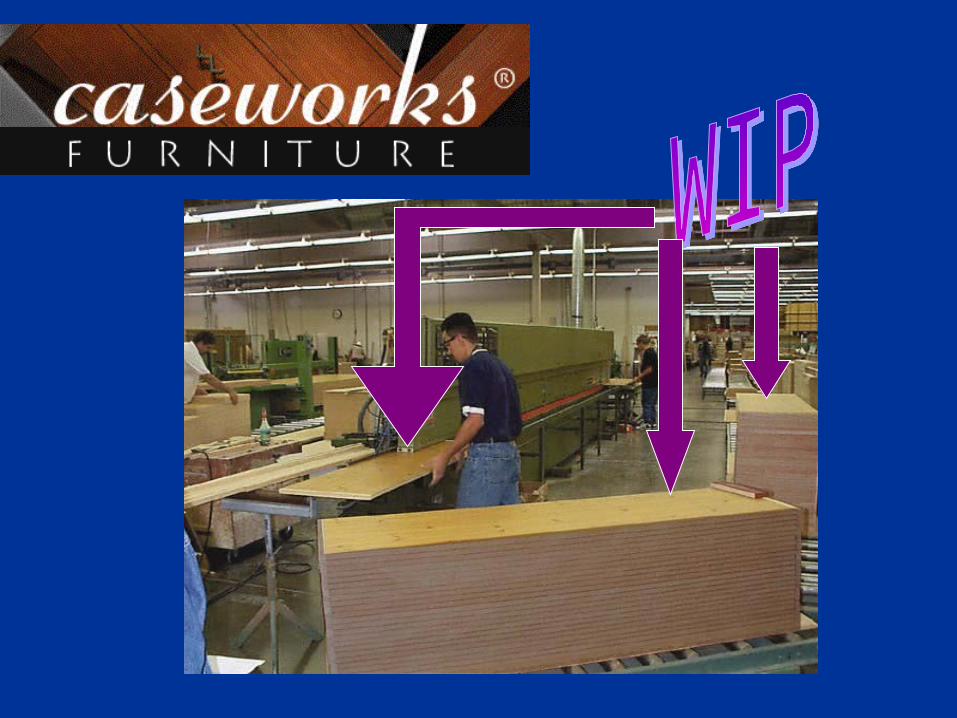

http://www.caseworksfurniture.com/healthcare/hcfactory.htm

•Located in Tucson, Arizona

•Produce furniture for: •Healthcare industry•Hospitals•Government

Pareto PrinciplePareto Principle

80/20 rule80/20 rule

Based on the work of an economist & avid Based on the work of an economist & avid

horticulturalist, V. Pareto in late 19horticulturalist, V. Pareto in late 19thth century century

Italy.Italy. 80% of the land was owned by 20% of the people.80% of the land was owned by 20% of the people.

80% of the peas were produced by 20% of the pods80% of the peas were produced by 20% of the pods

Applied to business by quality guru Dr. JuranApplied to business by quality guru Dr. Juran

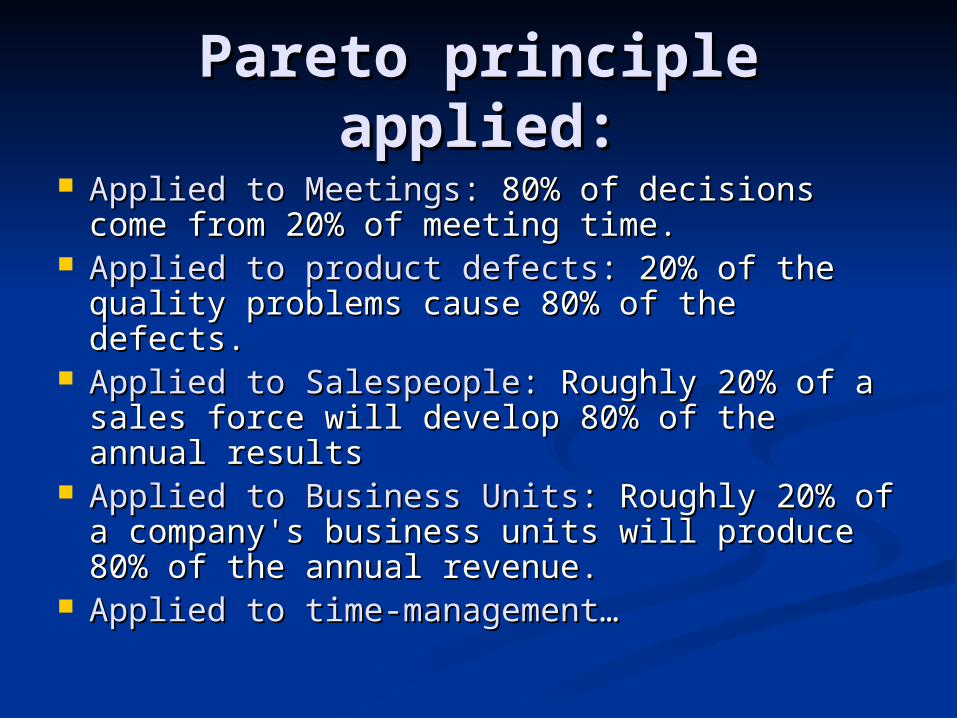

Pareto principle applied:Pareto principle applied: Applied to MeetingsApplied to Meetings: 80% of decisions : 80% of decisions

come from 20% of meeting time.come from 20% of meeting time. Applied to product defectsApplied to product defects: 20% of the : 20% of the

quality problems cause 80% of the defects. quality problems cause 80% of the defects. Applied to SalespeopleApplied to Salespeople: Roughly 20% of a : Roughly 20% of a

sales force will develop 80% of the annual sales force will develop 80% of the annual resultsresults

Applied to Business UnitsApplied to Business Units: Roughly 20% of : Roughly 20% of a company's business units will produce a company's business units will produce 80% of the annual revenue. 80% of the annual revenue.

Applied to time-managementApplied to time-management……

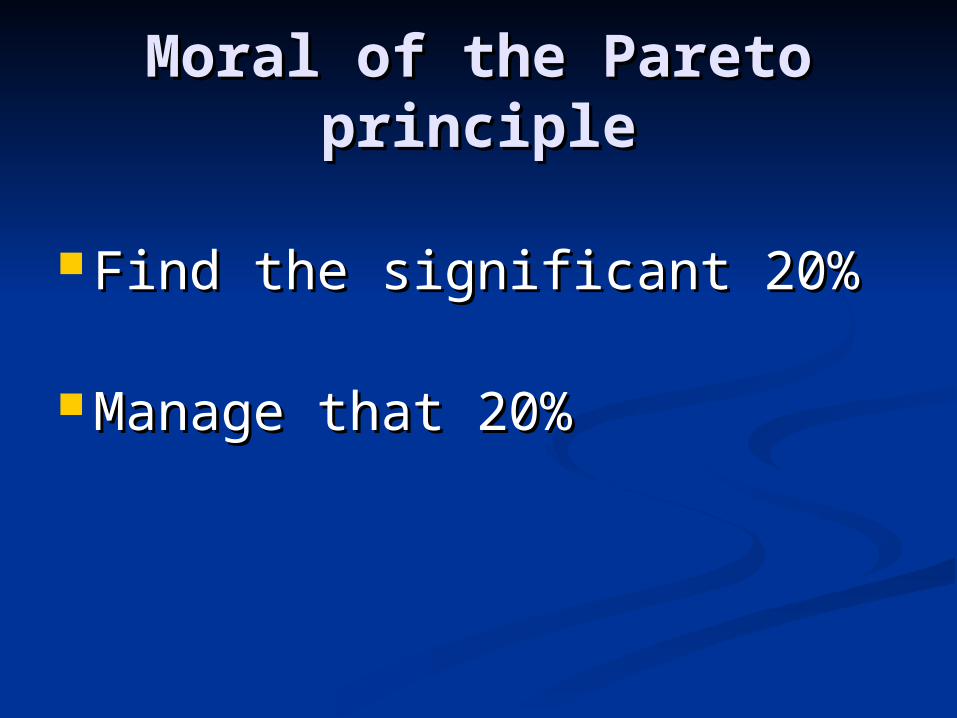

Moral of the Pareto Moral of the Pareto principleprinciple

Find the significant 20% Find the significant 20%

Manage that 20%Manage that 20%

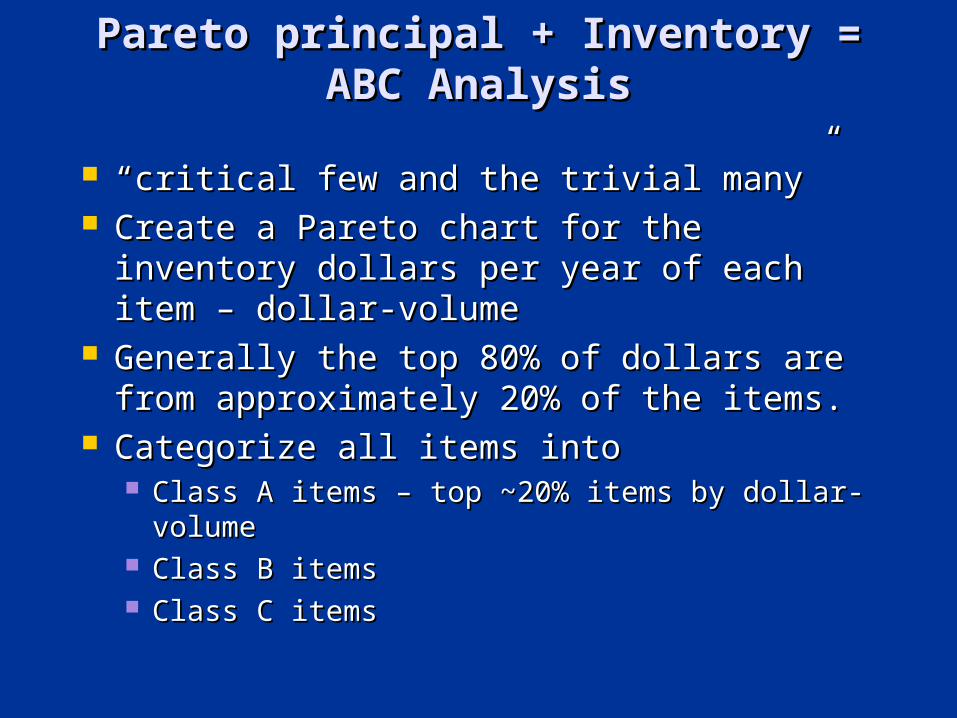

Pareto principal + Inventory = Pareto principal + Inventory = ABC AnalysisABC Analysis

““critical few and the trivial many”critical few and the trivial many” Create a Pareto chart for the inventory Create a Pareto chart for the inventory

dollars per year of each item – dollar-dollars per year of each item – dollar-volumevolume

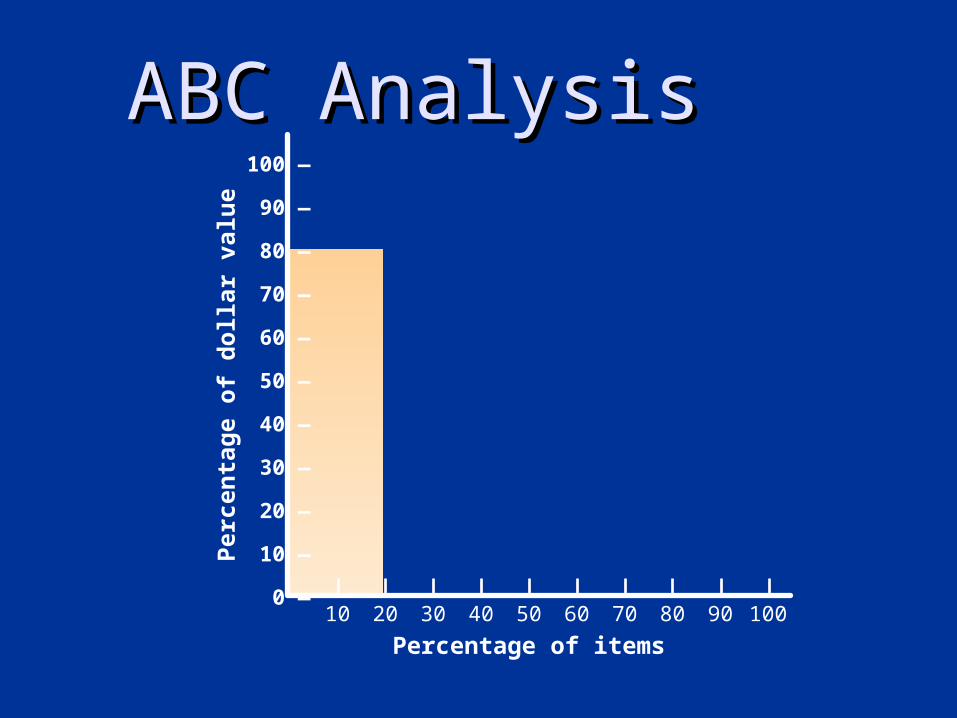

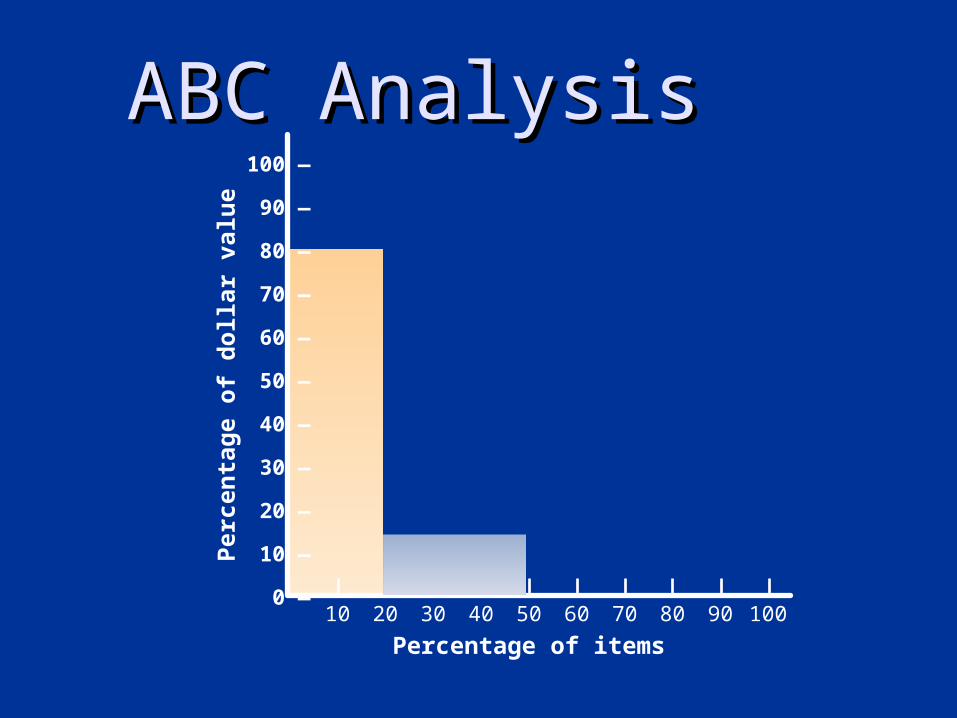

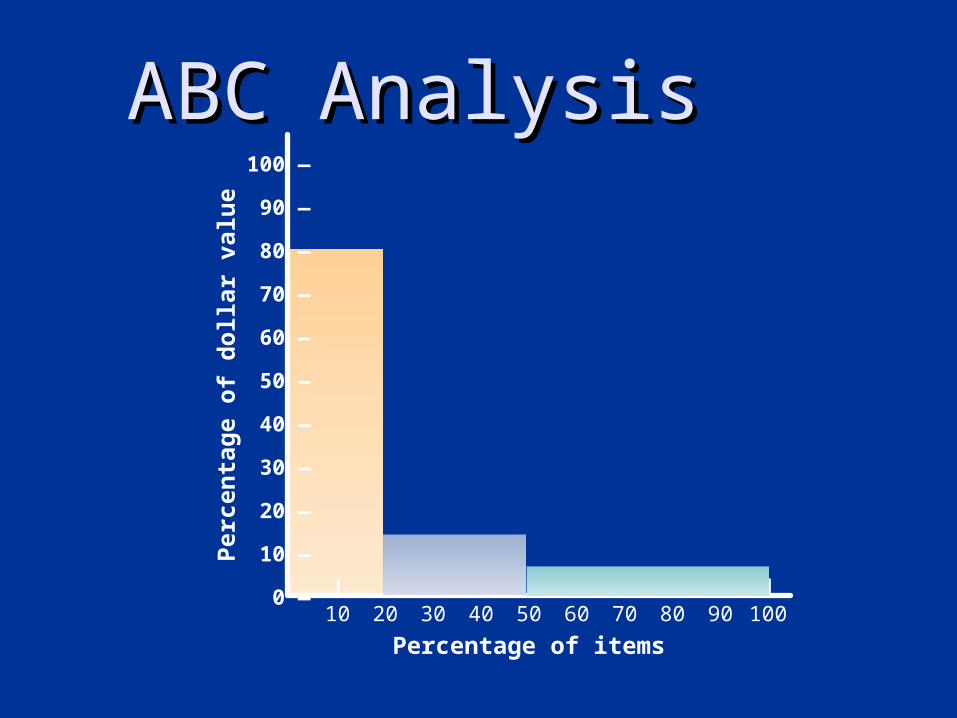

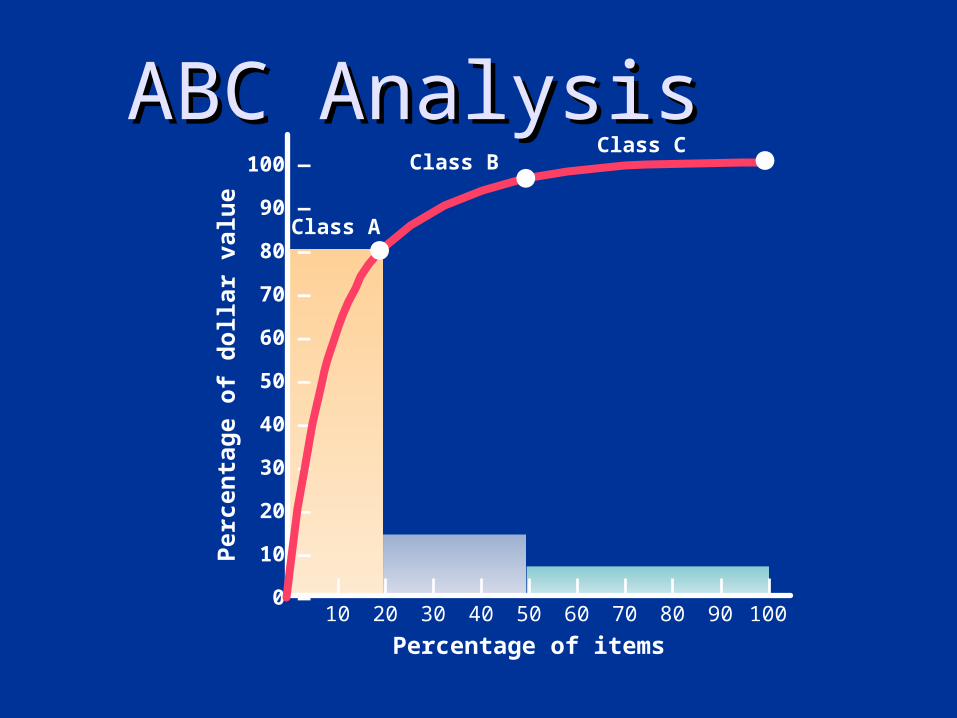

Generally the top 80% of dollars are from Generally the top 80% of dollars are from approximately 20% of the items.approximately 20% of the items.

Categorize all items into Categorize all items into Class A items – top ~20% items by dollar-Class A items – top ~20% items by dollar-

volumevolume Class B itemsClass B items Class C itemsClass C items

ABC AnalysisABC Analysis

10 20 30 40 50 60 70 80 90 100

Percentage of items

Per

cen

tag

e o

f d

oll

ar v

alu

e

100 —

90 —

80 —

70 —

60 —

50 —

40 —

30 —

20 —

10 —

0 —

ABC AnalysisABC Analysis

10 20 30 40 50 60 70 80 90 100

Percentage of items

Per

cen

tag

e o

f d

oll

ar v

alu

e

100 —

90 —

80 —

70 —

60 —

50 —

40 —

30 —

20 —

10 —

0 —

ABC AnalysisABC Analysis

10 20 30 40 50 60 70 80 90 100

Percentage of items

Per

cen

tag

e o

f d

oll

ar v

alu

e

100 —

90 —

80 —

70 —

60 —

50 —

40 —

30 —

20 —

10 —

0 —

ABC AnalysisABC Analysis

10 20 30 40 50 60 70 80 90 100

Percentage of items

Per

cen

tag

e o

f d

oll

ar v

alu

e

100 —

90 —

80 —

70 —

60 —

50 —

40 —

30 —

20 —

10 —

0 —

ABC AnalysisABC Analysis

10 20 30 40 50 60 70 80 90 100

Percentage of items

Per

cen

tag

e o

f d

oll

ar v

alu

e

100 —

90 —

80 —

70 —

60 —

50 —

40 —

30 —

20 —

10 —

0 —

Class C

Class A

Class B

ABC AnalysisABC Analysis

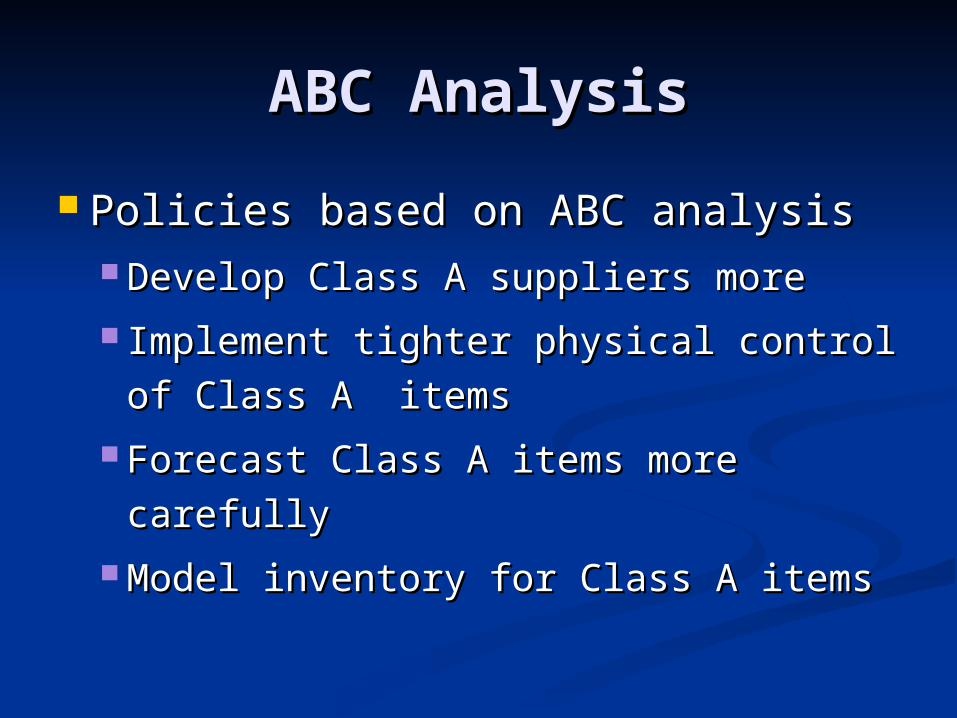

Policies based on ABC analysisPolicies based on ABC analysis Develop Class A suppliers moreDevelop Class A suppliers more

Implement tighter physical control Implement tighter physical control

of Class A itemsof Class A items

Forecast Class A items more Forecast Class A items more

carefullycarefully

Model inventory for Class A itemsModel inventory for Class A items

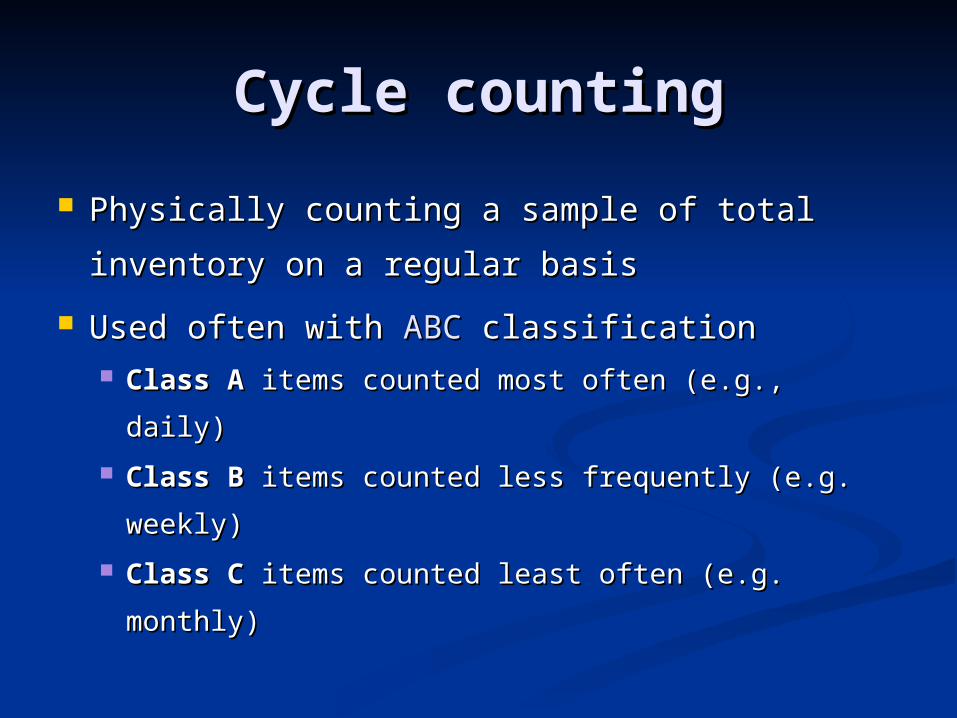

Cycle countingCycle counting

Physically counting a sample of total Physically counting a sample of total

inventory on a regular basisinventory on a regular basis

Used often with Used often with ABCABC classification classification Class AClass A items counted most often (e.g., daily) items counted most often (e.g., daily)

Class BClass B items counted less frequently (e.g. items counted less frequently (e.g.

weekly)weekly)

Class CClass C items counted least often (e.g. items counted least often (e.g.

monthly)monthly)

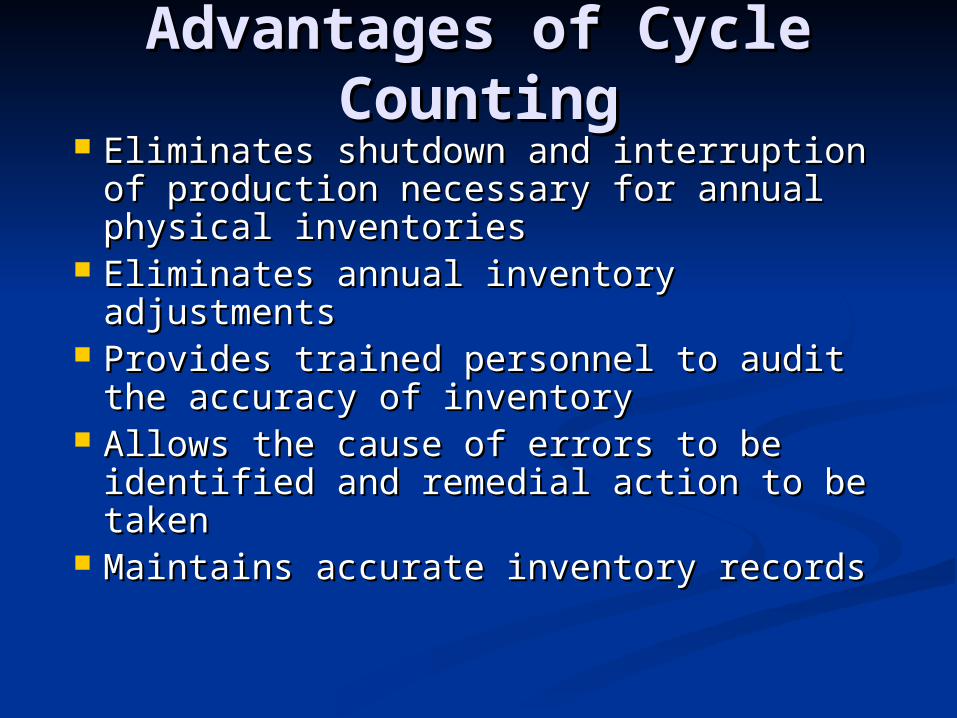

Advantages of Cycle Advantages of Cycle CountingCounting

Eliminates shutdown and interruption Eliminates shutdown and interruption of production necessary for annual of production necessary for annual physical inventoriesphysical inventories

Eliminates annual inventory Eliminates annual inventory adjustmentsadjustments

Provides trained personnel to audit Provides trained personnel to audit the accuracy of inventorythe accuracy of inventory

Allows the cause of errors to be Allows the cause of errors to be identified and remedial action to be identified and remedial action to be takentaken

Maintains accurate inventory recordsMaintains accurate inventory records

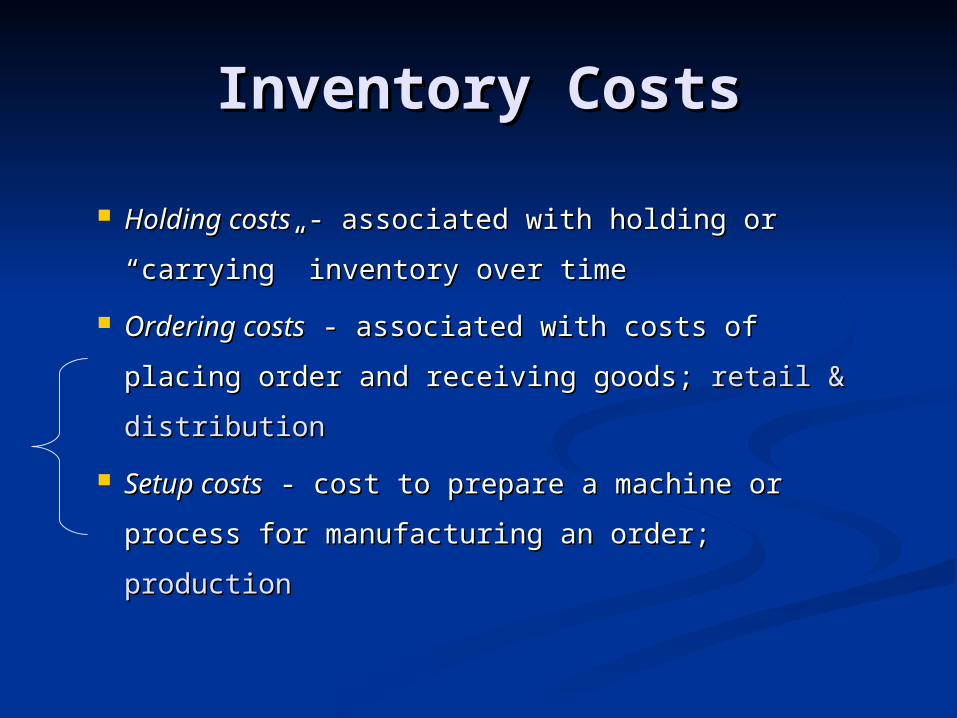

Inventory CostsInventory Costs

Holding costsHolding costs - associated with holding or - associated with holding or

“carrying” inventory over time“carrying” inventory over time

Ordering costsOrdering costs - associated with costs of - associated with costs of

placing order and receiving goods; placing order and receiving goods; retail & retail &

distributiondistribution

Setup costsSetup costs - cost to prepare a machine or - cost to prepare a machine or

process for manufacturing an order; process for manufacturing an order; productionproduction

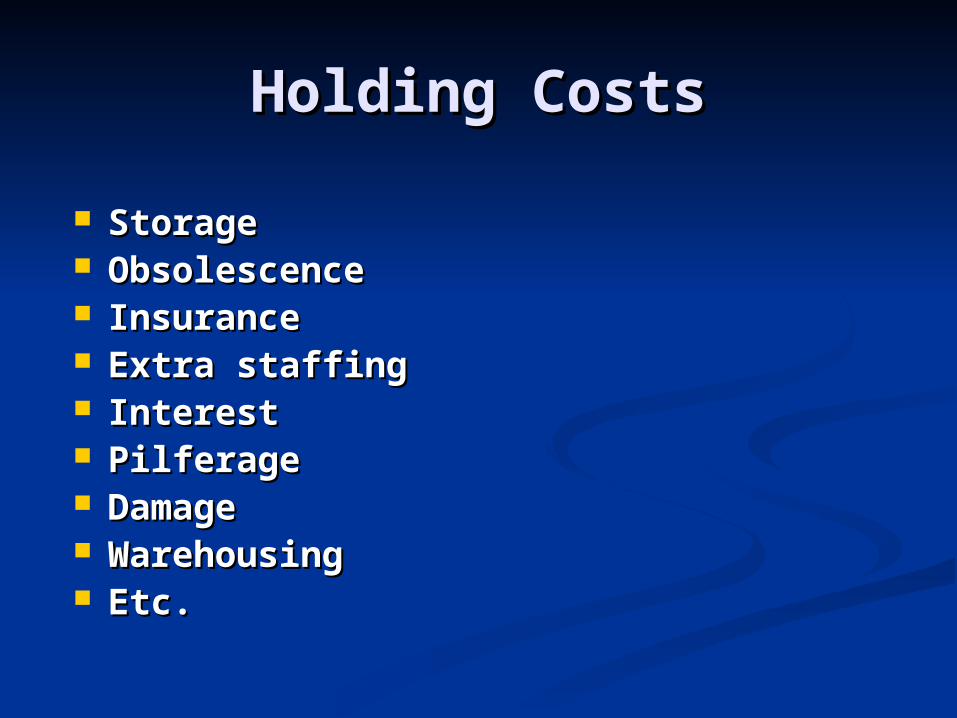

Holding CostsHolding Costs

StorageStorage ObsolescenceObsolescence InsuranceInsurance Extra staffingExtra staffing InterestInterest PilferagePilferage DamageDamage WarehousingWarehousing Etc.Etc.

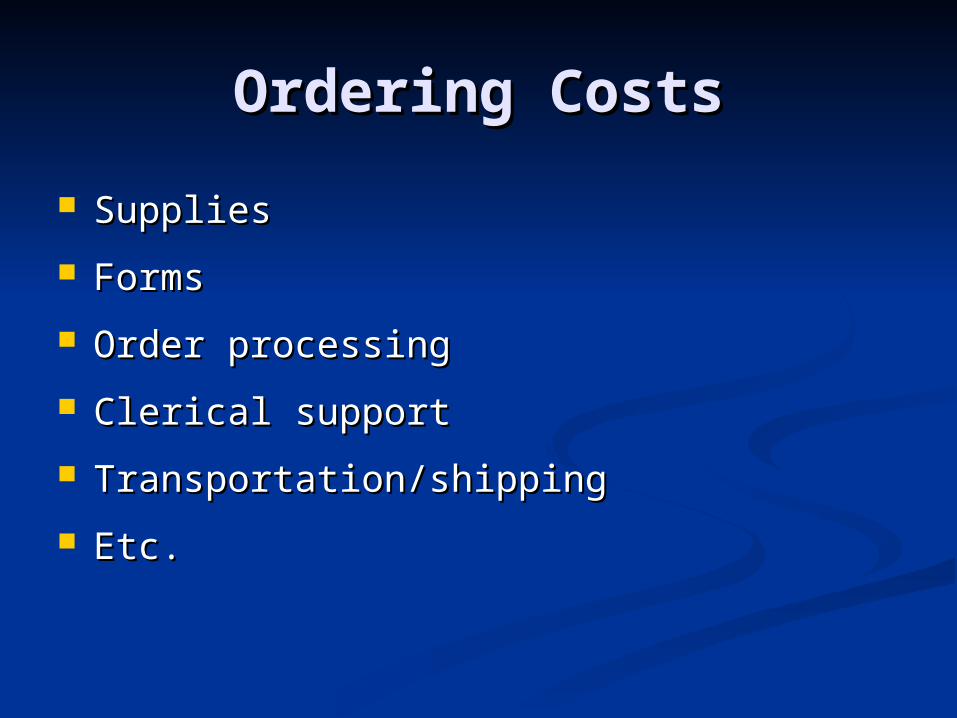

Ordering CostsOrdering Costs

SuppliesSupplies

FormsForms

Order processingOrder processing

Clerical supportClerical support

Transportation/shippingTransportation/shipping

Etc.Etc.

Setup CostsSetup Costs

Machine setup costsMachine setup costs

Clean-up costsClean-up costs

Re-tooling costsRe-tooling costs

Adjustment costsAdjustment costs

Etc.Etc.