Inveatment analysis and portfolio management

25

-

Upload

works-in-gcuf -

Category

Business

-

view

163 -

download

1

Transcript of Inveatment analysis and portfolio management

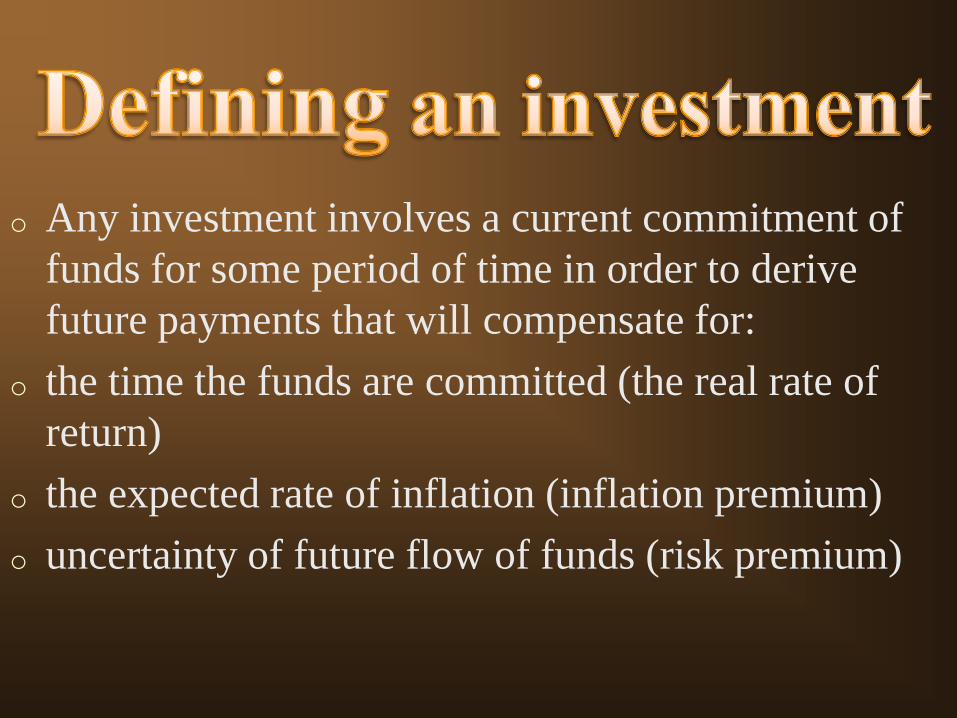

o Any investment involves a current commitment of

funds for some period of time in order to derive

future payments that will compensate for:

o the time the funds are committed (the real rate of

return)

o the expected rate of inflation (inflation premium)

o uncertainty of future flow of funds (risk premium)

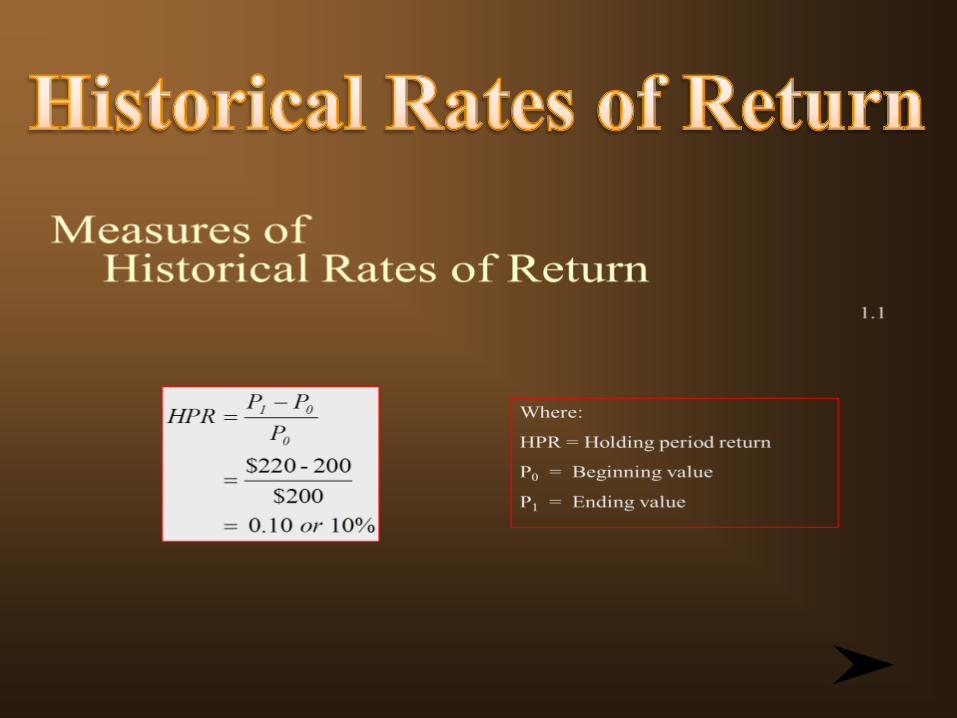

o EAR = Equivalent

Annual Return

o HPR = Holding Period

Return

o N = Number of years 111

NHPREAR

1 2 ... NR R RAM

N

1

1 21 1 ... 1 1NNGM R R R

AM = Arithmetic Mean

GM = Geometric Mean

Ri = Annual HPRs

N = Number of years

o The mean historical rate of return for a

portfolio of investments is measured as

the weighted average of the HPRs for

the individual investments in the

portfolio, or the overall change in the

value of the original portfolio

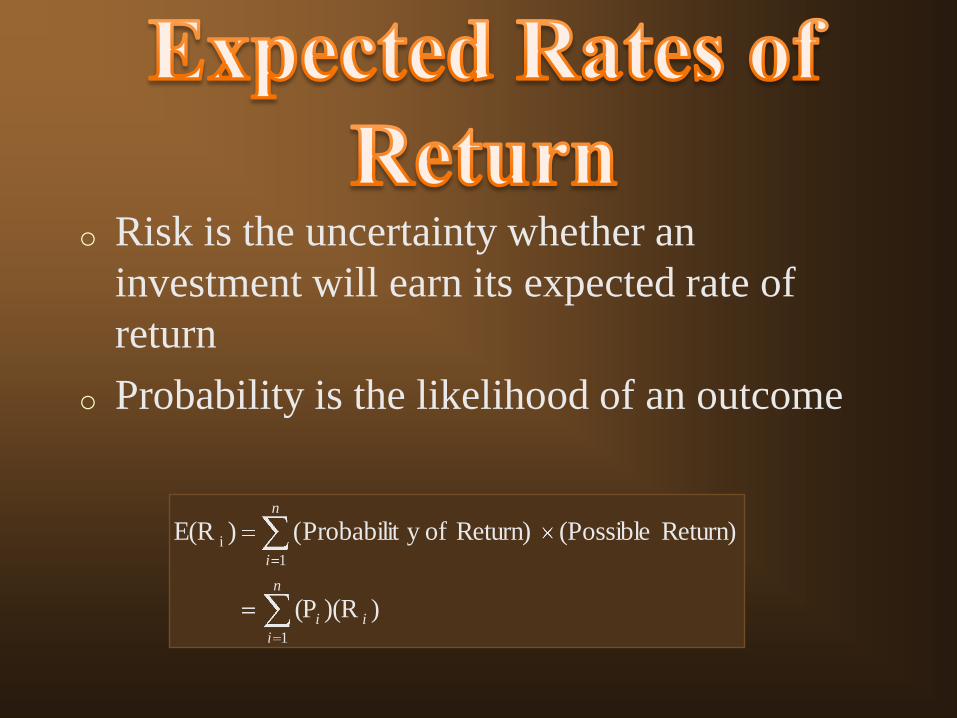

o Risk is the uncertainty whether an

investment will earn its expected rate of

return

o Probability is the likelihood of an outcome

))(RP(

Return) (Possible Return) ofy Probabilit( )E(R

1

1

i

ii

n

i

n

i

o Much of modern finance is based on the

principle that investors are risk averse

o Risk aversion refers to the assumption that,

all else being equal, most investors will

choose the least risky alternative and that

they will not accept additional risk unless

they are compensated in the form of higher

return

N

HPRE i

n

1i

2

i

2

HPRWhere:

= Variance (of the pop)

HPR = Holding Period Return i

E(HPR)i = Expected HPR*

N = Number of years

22

i i

1

(P ) R E(R)n

i

Note: Because we multiply by the

probability of each return occurring,

we do NOT divide by N. If each

probability is the same for all returns,

then the variance can be calculated by

either multiplying by the probability or

dividing by N.

= Variance

Ri = Return in period i

E(R) = Expected Return

Pi = Probability of Ri occurring

2

i i i

1

1

22

i i i

1

P[R -E(R )]

P [R -E(R )]

n

i

n

i

Standard Deviation is a measure of

dispersion around the mean. The higher

the standard deviation, the greater the

dispersion of returns around the mean and

the greater the risk.

o Coefficient of variation (CV) is a measure

of relative variability

o CV indicates risk per unit of return, thus

making comparisons easier among

investments with large differences in mean

returns

o Three factors influence an

investor’s required rate of return

oReal rate of return

oExpected rate of inflation during the

period

oRisk

oAssumes no inflation.

oAssumes no uncertainty about future cash flows.

oInfluenced by the time preference for consumption of income and investment opportunities in the economy

1 1 1Nominal Real Expected Inflation

The nominal risk free rate of return is

dependent upon:

Conditions in the Capital Markets

Expected Rate of Inflation

o Five factors affect the standard

deviation of returns over time.

oBusiness risk:

oFinancial risk

oLiquidity risk

oExchange rate risk

oCountry risk

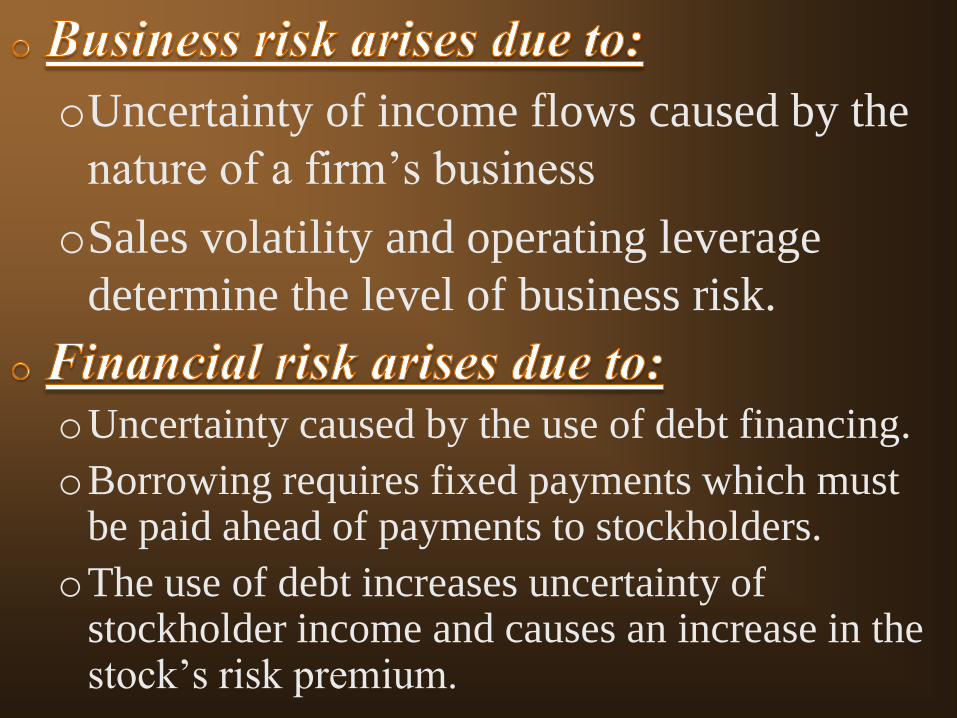

oUncertainty of income flows caused by the

nature of a firm’s business

oSales volatility and operating leverage

determine the level of business risk.

oUncertainty caused by the use of debt financing.

oBorrowing requires fixed payments which must be paid ahead of payments to stockholders.

oThe use of debt increases uncertainty of stockholder income and causes an increase in the stock’s risk premium.

o the uncertainty introduced by the secondary market

for an investment.

oHow long will it take to convert an investment into cash?

oHow certain is the price that will be received?

o the uncertainty introduced by acquiring securities

denominated in a currency different from that of the

investor.

o Changes in exchange rates affect the investors return

when converting an investment back into the

“home” currency.

o Country risk (also called political risk) refers to the

uncertainty of returns caused by the possibility of a

major change in the political or economic

environment in a country.

o Individuals who invest in countries that have

unstable political-economic systems must include a

country risk-premium when determining their

required rate of return

REFERENCE

Frank K. Reilly & Keith C. Brown