Introduction to web.pdfstrategic decision making of its ... – Key actor in the €40bn merger of...

42

Introduction to March 2017

-

Upload

phunghuong -

Category

Documents

-

view

220 -

download

0

Transcript of Introduction to web.pdfstrategic decision making of its ... – Key actor in the €40bn merger of...

Introduction to

March 2017

GBL March 2017

1. GBL’s Strategy – 2016 and forward 2

2. 2016 Financial performance 22

3. Outlook 27

4. Appendix 30

2

GBL | March 2017

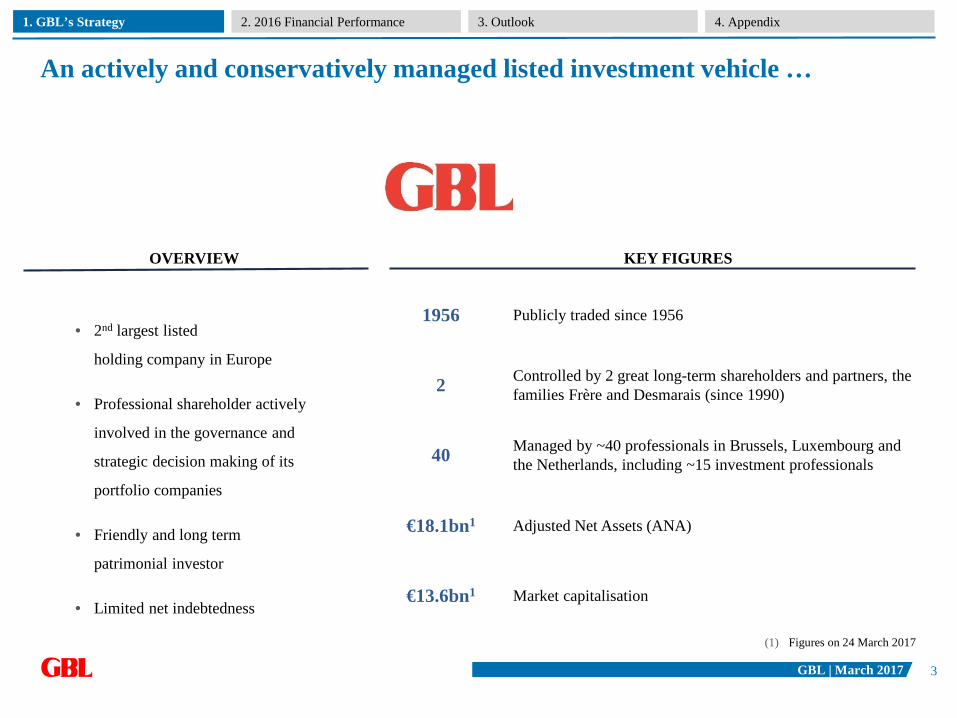

An actively and conservatively managed listed investment vehicle …

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

1956 Publicly traded since 1956

2 Controlled by 2 great long-term shareholders and partners, the families Frère and Desmarais (since 1990)

€13.6bn1 Market capitalisation

40 Managed by ~40 professionals in Brussels, Luxembourg and the Netherlands, including ~15 investment professionals

€18.1bn1 Adjusted Net Assets (ANA)

• 2nd largest listed

holding company in Europe

• Professional shareholder actively

involved in the governance and

strategic decision making of its

portfolio companies

• Friendly and long term

patrimonial investor

• Limited net indebtedness

KEY FIGURES

(1) Figures on 24 March 2017

OVERVIEW

3

GBL | March 2017

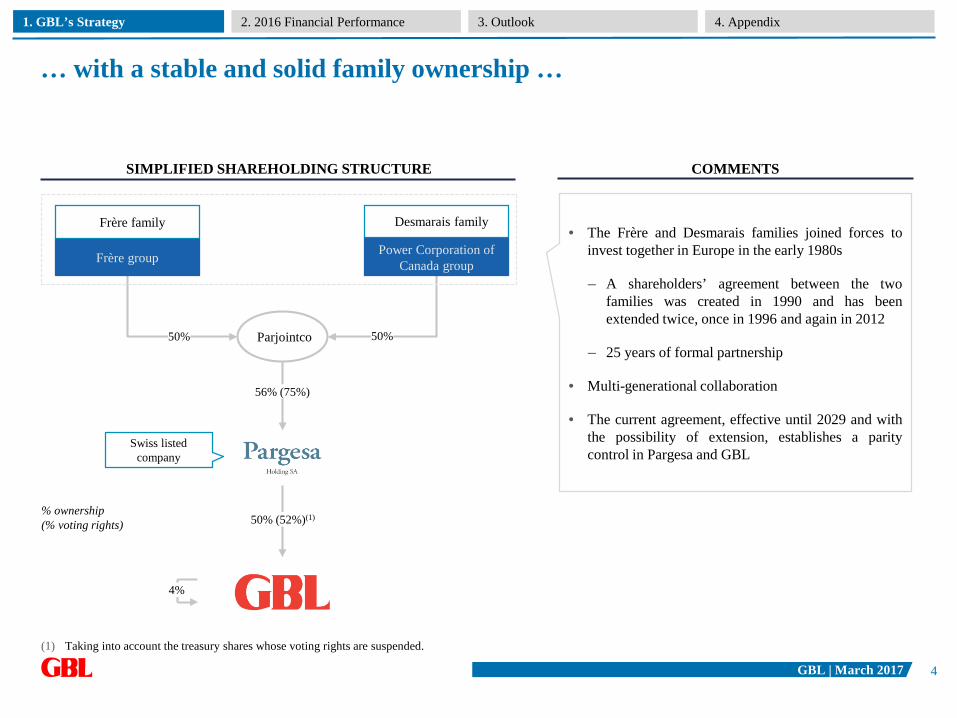

… with a stable and solid family ownership …

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

SIMPLIFIED SHAREHOLDING STRUCTURE

Desmarais familyFrère family

Frère group

Parjointco50% 50%

56% (75%)

Power Corporation of Canada group

% ownership(% voting rights)

• The Frère and Desmarais families joined forces toinvest together in Europe in the early 1980s

– A shareholders’ agreement between the twofamilies was created in 1990 and has beenextended twice, once in 1996 and again in 2012

– 25 years of formal partnership

• Multi-generational collaboration

• The current agreement, effective until 2029 and withthe possibility of extension, establishes a paritycontrol in Pargesa and GBL

Swiss listed company

4%

50% (52%)(1)

COMMENTS

(1) Taking into account the treasury shares whose voting rights are suspended.

4

GBL | March 2017

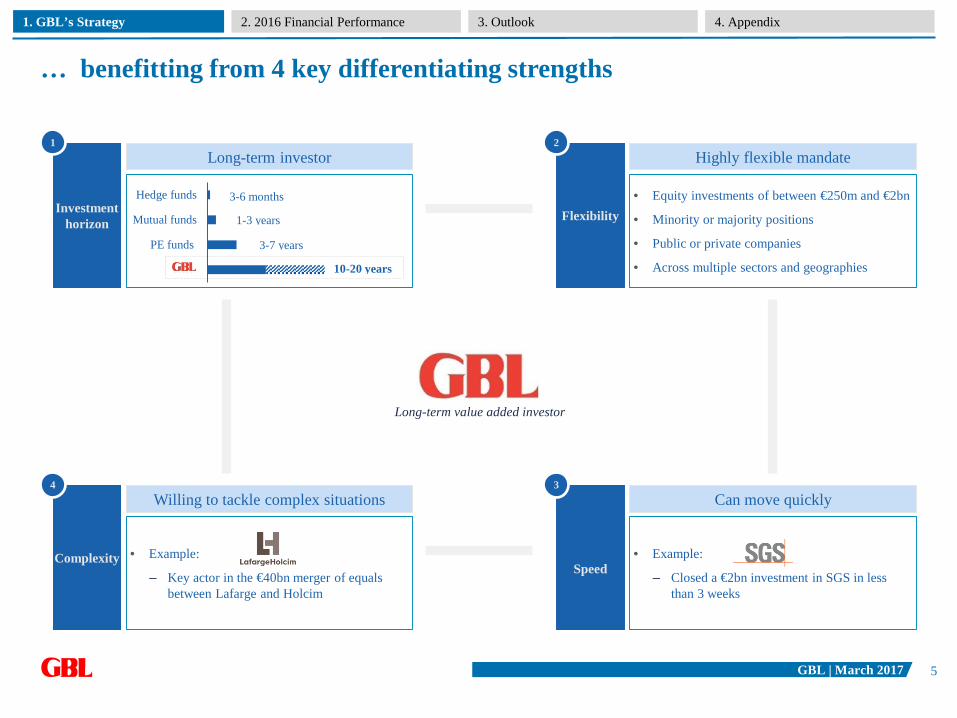

… benefitting from 4 key differentiating strengths

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Long-term value added investor

Investment horizon

Long-term investor1

• Equity investments of between €250m and €2bn

• Minority or majority positions

• Public or private companies

• Across multiple sectors and geographies

Flexibility

Highly flexible mandate 2

• Example:

– Key actor in the €40bn merger of equals between Lafarge and Holcim

Complexity

Willing to tackle complex situations 4

• Example:

– Closed a €2bn investment in SGS in less than 3 weeks

Speed

Can move quickly3

10-20 years

3-7 years

1-3 years

3-6 months

GBL

PE funds

Mutual funds

Hedge funds

5

GBL | March 2017

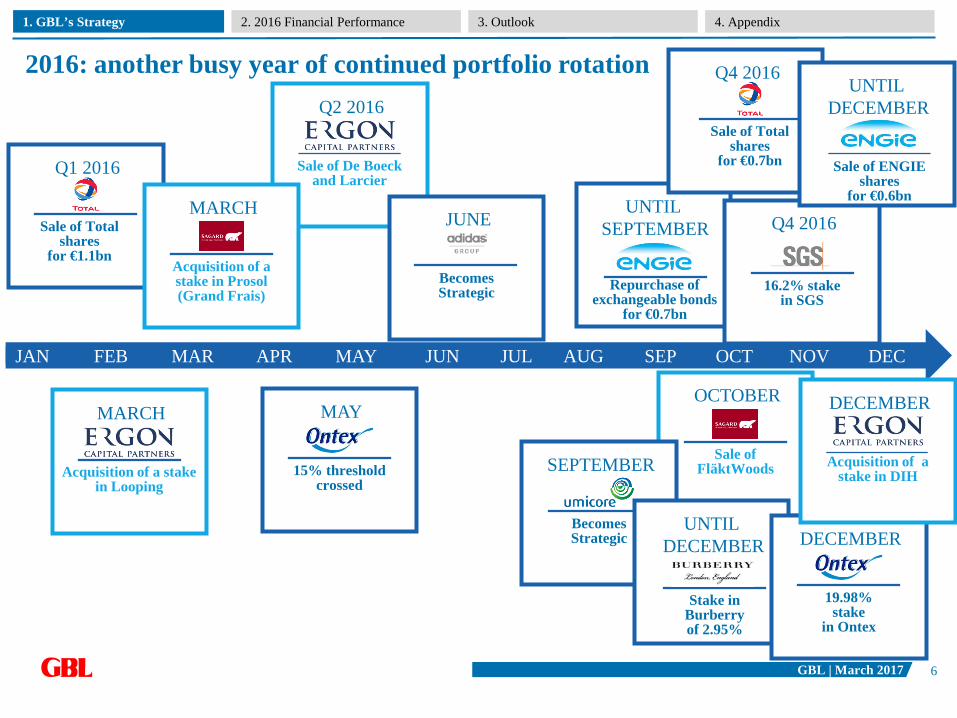

Q1 2016

MARCH

Q2 2016

MAY

2016: another busy year of continued portfolio rotation

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT DECNOV

OCTOBER

Sale of FläktWoodsSEPTEMBER

MARCH

Acquisition of a stake in Prosol(Grand Frais)

Acquisition of a stake in Looping

Becomes Strategic

15% threshold crossed

Sale of De Boeckand Larcier

Sale of Total shares

for €1.1bn

UNTIL DECEMBER

Stake in Burberry of 2.95%

UNTIL SEPTEMBER

Repurchase of exchangeable bonds

for €0.7bn

Q4 2016

Sale of Total shares

for €0.7bn

DECEMBER

19.98%stake

in Ontex

JUNE

Becomes Strategic

Q4 2016

16.2% stake in SGS

UNTIL DECEMBER

Sale of ENGIE shares

for €0.6bn

DECEMBER

Acquisition of a stake in DIH

6

GBL | March 2017

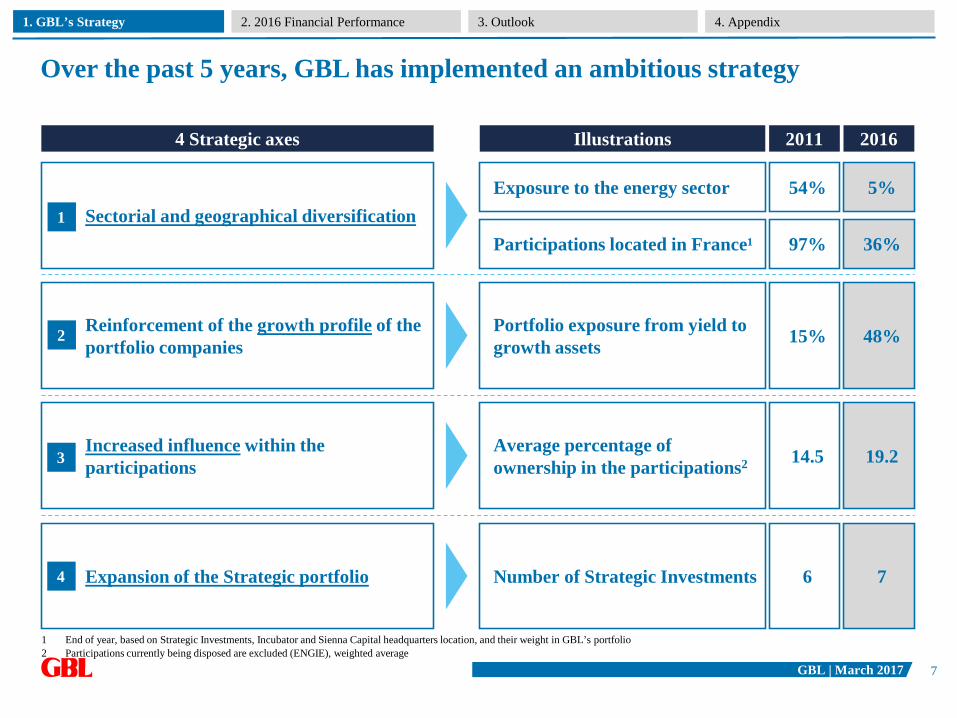

Over the past 5 years, GBL has implemented an ambitious strategy

1 End of year, based on Strategic Investments, Incubator and Sienna Capital headquarters location, and their weight in GBL’s portfolio2 Participations currently being disposed are excluded (ENGIE), weighted average

Sectorial and geographical diversification

4 Strategic axes Illustrations

Reinforcement of the growth profile of the portfolio companies

Increased influence within the participations

Expansion of the Strategic portfolio

Participations located in France¹

Exposure to the energy sector

Portfolio exposure from yield to growth assets

5%54%

20162011

36%97%

48%15%

Number of Strategic Investments 76

Average percentage of ownership in the participations2 19.214.5

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

1

4

3

2

7

GBL | March 2017

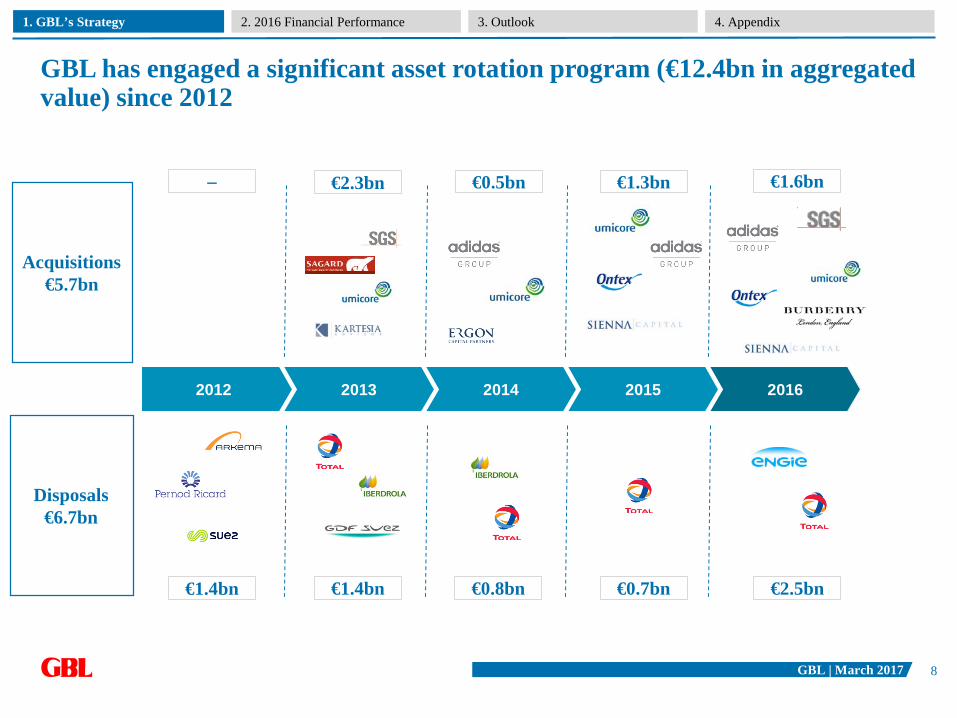

GBL has engaged a significant asset rotation program (€12.4bn in aggregatedvalue) since 2012

– €2.3bn €0.5bn €1.3bn

€1.4bn €1.4bn €0.8bn €0.7bn

€1.6bn

€2.5bn

2012 2013 2014 2015 2016

Acquisitions€5.7bn

Disposals€6.7bn

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

8

GBL | March 2017

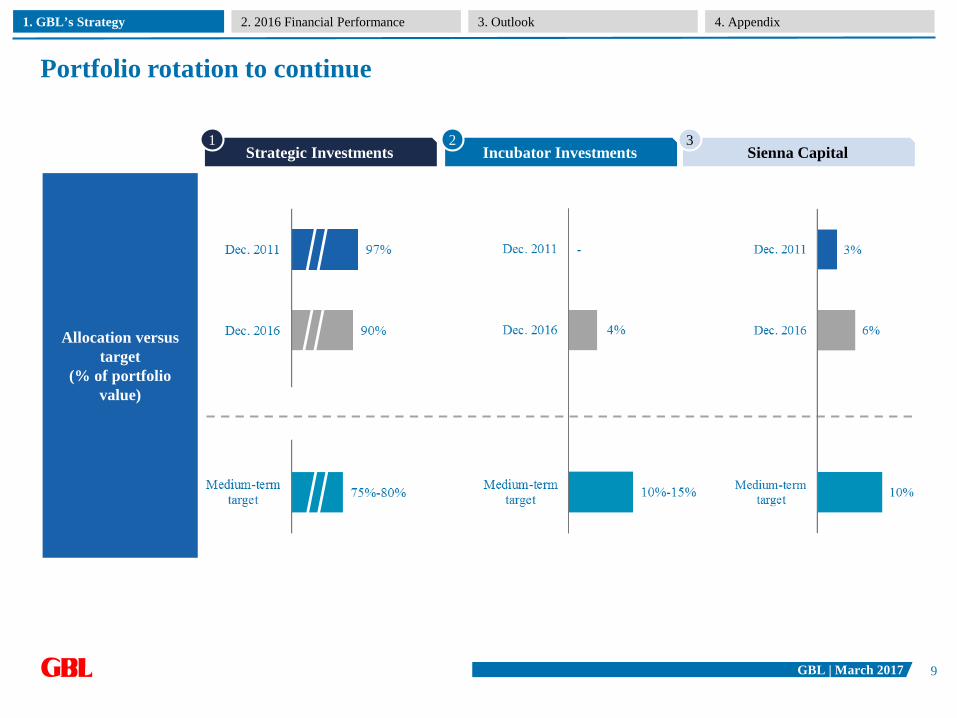

Portfolio rotation to continue

Strategic Investments1

Incubator Investments Sienna Capital

Allocation versus target

(% of portfolio value)

2 3

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

9

GBL | March 2017

Increase in adjusted net assets and anticipated decline in cash earnings

ADJUSTED NET ASSETS CASH EARNINGS

In €bn In €m

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

+56%

10

GBL | March 2017

A more balanced portfolio in terms of exposure between growth and yield

WEIGHT IN GBL PORTFOLIO PER ASSET TYPE AS AT END OF 2011

WEIGHT IN GBL PORTFOLIO PER ASSET TYPE AS AT END OF 2016

Value/CyclicalValue/Yield Growth Incubator Sienna Capital

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

11

GBL | March 2017

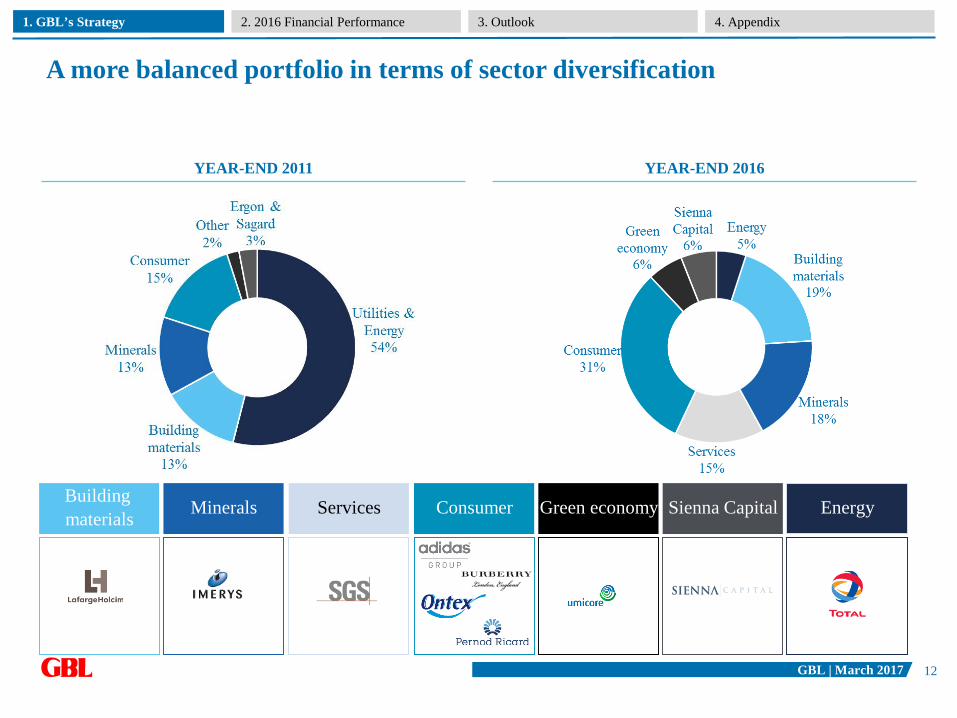

A more balanced portfolio in terms of sector diversification

YEAR-END 2011 YEAR-END 2016

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

MineralsBuilding materials Services Consumer Green economy Sienna Capital Energy

12

GBL | March 2017

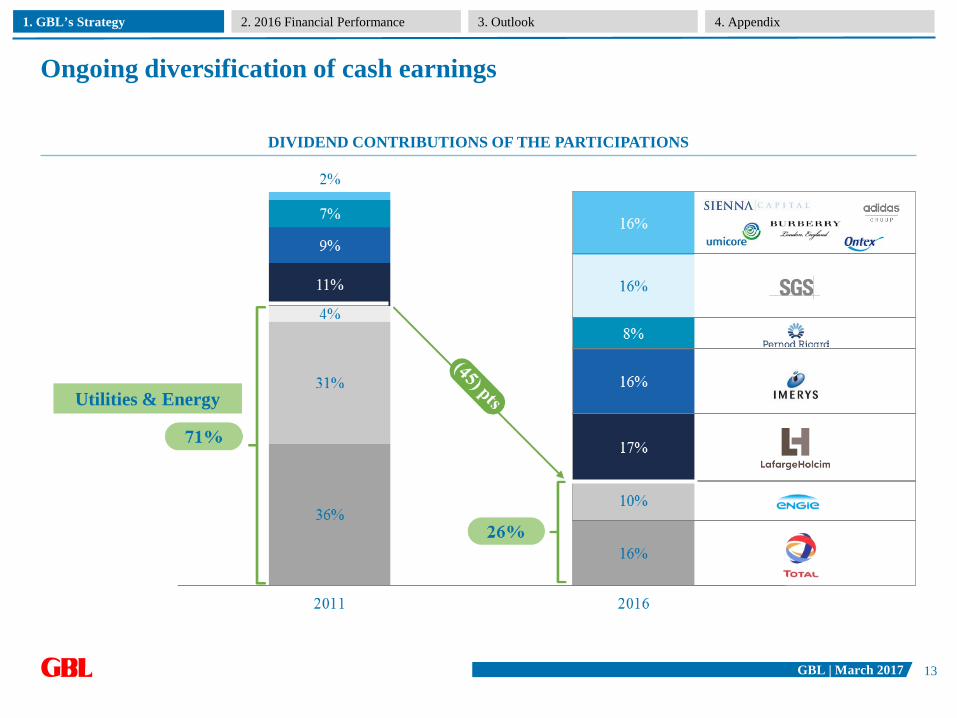

Ongoing diversification of cash earnings

DIVIDEND CONTRIBUTIONS OF THE PARTICIPATIONS

Utilities & Energy

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

13

GBL | March 2017

High return from the new participations

New participationsANA

contribution 31/12/2016

1

€2.4bn

€2.4bn

€1.0bn

€0.4bn

Stock price31/12/2016

CHF2,072

€150.15

€54.15

€28.25

Investedcapital

€2.2bn

€1.3bn

€0.7bn

€0.5bn

ANA contribution 31/12/2015

€2.1bn

€0.9bn

€0.7bn

€0.2bn

€0.2bnGBP14.97 €0.2bn -

Total €6.5bn€3.9bn

2

3

4

5

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

7%

78%

18%

11%

34%

TSR sinceinception

19%

ANA contribution 24/03/2017

€2.5bn

€2.8bn

€1.0bn

€0.5bn

€0.3bn

€7.0bn

14

GBL | March 2017

94,13

105,31

112,04

2,031,13 0,27

5,34

1,841,29 0,15 0,91

(1,09)

(0,15)(0,28)

2,94

(2,86) (0,34)

AN

A31

/12/

15

Imer

ys

Lafa

rge

Hol

cim

Tota

l

ENG

IE

adid

as

Um

icor

e

SGS

Bur

berr

y

Ont

ex

Pern

odR

icar

d

Sien

naC

apita

l

Div

.R

ecei

ved

Div

. Pai

d

Oth

ers

AN

A31

/12/

16

AN

A24

/03/

17

12% y/y increase of ANA ensuing new investments and the rise in stock price

Commodities Consumer and servicesSiennaCapital

Dividends, and others

In € per share

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

15

GBL | March 2017

A diversified portfolio composed of leaders in their sector

Strategic Investments Incubator Investments Sienna Capital

Sector Mining Buildingmaterials TIC Sports

equipmentFood &

Beverage Multiple Oil & Gas Consumer goods

Consumer goods

Alternative assets

Ranking in their sector #1 #1 #1 #2 #2 Top 3 Top 5 Top 3 Top 10 n.a.

GBL’s ranking in the shareholding

#1 #2 #1 #1 #3 #1 #4 #1 #10 n.a.

Date of first investment 1987 2005 2013 2015 2006 2013 1998 2015 2015 n.a.

GBL% ownership 53.9% 9.4% 16.2% 7.5% 7.5% 17.0% 0.7% 19.98% 2.95% 100%1

Market capitalisation

(€bn)5.7 30.3 15.1 31.4 27.3 6.1 118.4 2.1 7.8 n.a.

Value of GBL’s stake

(€bn)3.1 2.9 2.4 2.4 2.0 1.0 0.8 0.4 0.2 1.0

Note: figures for GBL financial performance and market capitalisation as of 31/12/2016

1 The 100% ownership percentage shown for Sienna Capital reflects GBL’s 100% ownership of this activity (i.e. does not reflect GBL’s ownership of the underlying assets)

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

16

GBL | March 2017

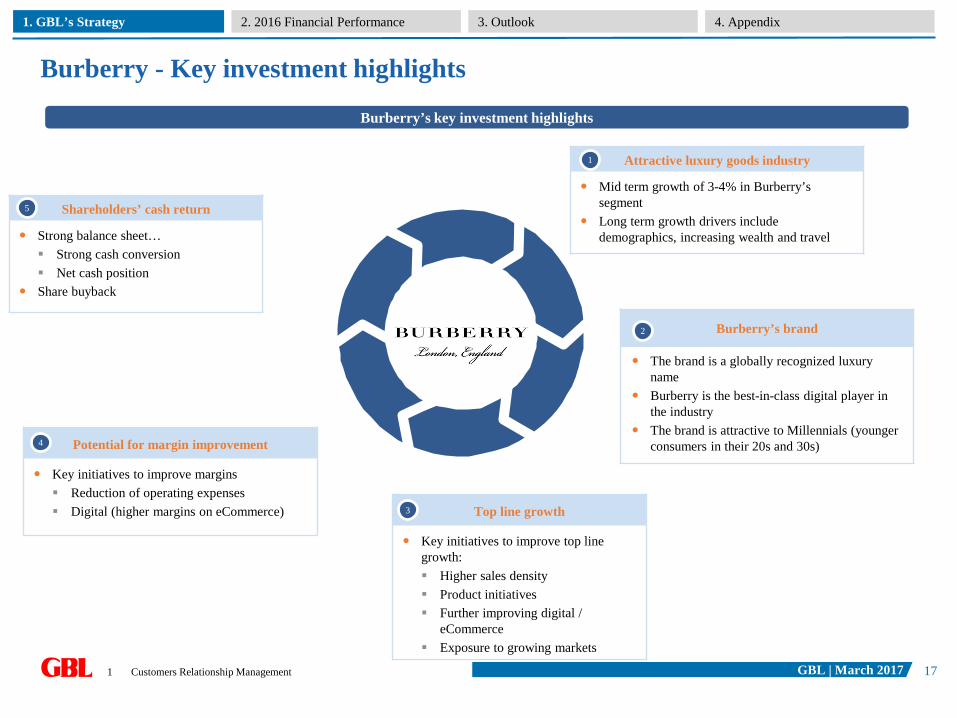

Burberry - Key investment highlights

Burberry’s key investment highlights

Attractive luxury goods industry

Mid term growth of 3-4% in Burberry’s segment

Long term growth drivers include demographics, increasing wealth and travel

1

Burberry’s brand

The brand is a globally recognized luxury name

Burberry is the best-in-class digital player in the industry

The brand is attractive to Millennials (younger consumers in their 20s and 30s)Potential for margin improvement

Key initiatives to improve margins Reduction of operating expenses Digital (higher margins on eCommerce) Top line growth

Key initiatives to improve top line growth: Higher sales density Product initiatives Further improving digital /

eCommerce Exposure to growing markets

Shareholders’ cash return

Strong balance sheet… Strong cash conversion Net cash position

Share buyback

5

4

3

2

1 Customers Relationship Management

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

17

GBL | March 2017

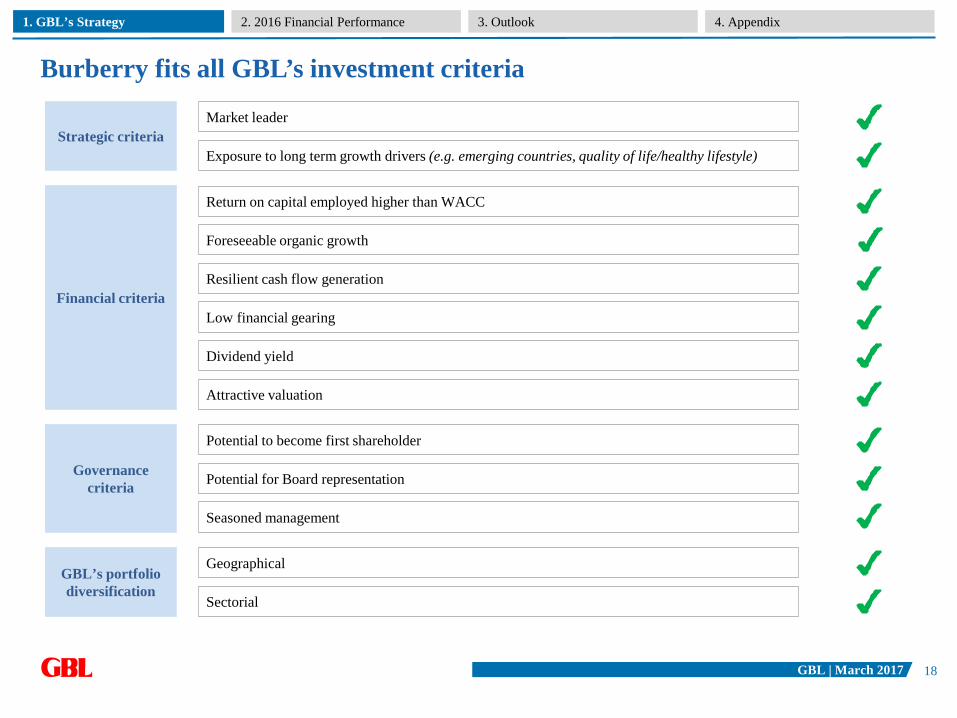

Burberry fits all GBL’s investment criteria

Strategic criteriaMarket leader

Exposure to long term growth drivers (e.g. emerging countries, quality of life/healthy lifestyle)

Governance criteria Potential for Board representation

Seasoned management

Potential to become first shareholder

GBL’s portfolio diversification

Sectorial

Geographical

Financial criteria

Return on capital employed higher than WACC

Foreseeable organic growth

Resilient cash flow generation

Low financial gearing

Dividend yield

Attractive valuation

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

18

GBL | March 2017

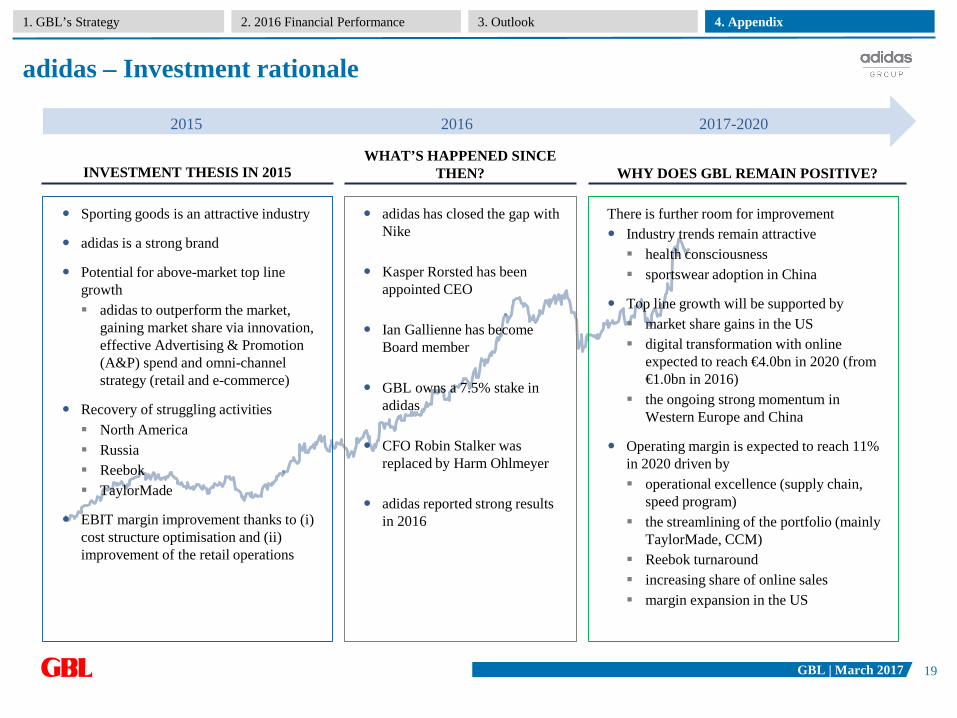

adidas – Investment rationale

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

2015 2016 2017-2020

INVESTMENT THESIS IN 2015WHAT’S HAPPENED SINCE

THEN? WHY DOES GBL REMAIN POSITIVE?

Sporting goods is an attractive industry

adidas is a strong brand

Potential for above-market top line growth adidas to outperform the market,

gaining market share via innovation, effective Advertising & Promotion (A&P) spend and omni-channel strategy (retail and e-commerce)

Recovery of struggling activities North America Russia Reebok TaylorMade

EBIT margin improvement thanks to (i) cost structure optimisation and (ii) improvement of the retail operations

adidas has closed the gap with Nike

Kasper Rorsted has been appointed CEO

Ian Gallienne has become Board member

GBL owns a 7.5% stake in adidas

CFO Robin Stalker was replaced by Harm Ohlmeyer

adidas reported strong results in 2016

There is further room for improvement Industry trends remain attractive health consciousness sportswear adoption in China

Top line growth will be supported by market share gains in the US digital transformation with online

expected to reach €4.0bn in 2020 (from €1.0bn in 2016)

the ongoing strong momentum in Western Europe and China

Operating margin is expected to reach 11%in 2020 driven by operational excellence (supply chain,

speed program) the streamlining of the portfolio (mainly

TaylorMade, CCM) Reebok turnaround increasing share of online sales margin expansion in the US

19

GBL | March 2017

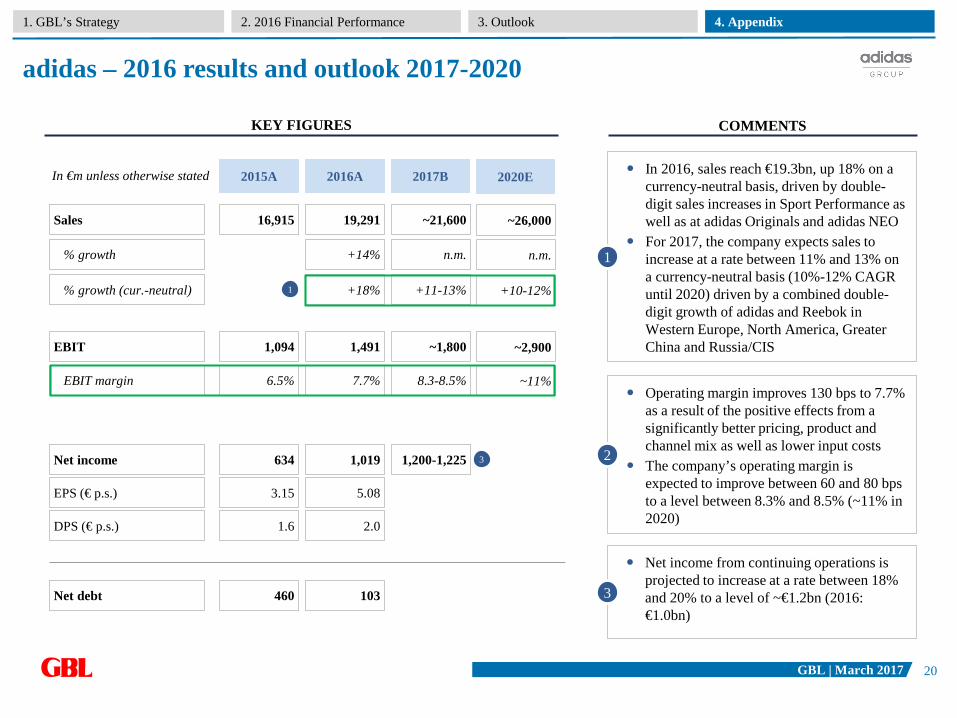

adidas – 2016 results and outlook 2017-2020

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

In 2016, sales reach €19.3bn, up 18% on a currency-neutral basis, driven by double-digit sales increases in Sport Performance as well as at adidas Originals and adidas NEO

For 2017, the company expects sales to increase at a rate between 11% and 13% on a currency-neutral basis (10%-12% CAGR until 2020) driven by a combined double-digit growth of adidas and Reebok in Western Europe, North America, Greater China and Russia/CIS

1

Operating margin improves 130 bps to 7.7% as a result of the positive effects from a significantly better pricing, product and channel mix as well as lower input costs

The company’s operating margin is expected to improve between 60 and 80 bps to a level between 8.3% and 8.5% (~11% in 2020)

2

Net income from continuing operations is projected to increase at a rate between 18% and 20% to a level of ~€1.2bn (2016: €1.0bn)

3

KEY FIGURES COMMENTS

EPS (€ p.s.)

DPS (€ p.s.)

Sales

EBIT

EBIT margin

Net income

3.15

1.6

16,915

1,094

6.5%

634

2015A

5.08

2.0

19,291

1,491

7.7%

1,019

2016A

1

3

% growth

% growth (cur.-neutral)

+14%

Net debt 460 103

In €m unless otherwise stated 2017B

~21,600

~1,800

8.3-8.5%

1,200-1,225

+11-13%

n.m.

+18%

2020E

~26,000

~2,900

~11%

+10-12%

n.m.

20

GBL | March 2017

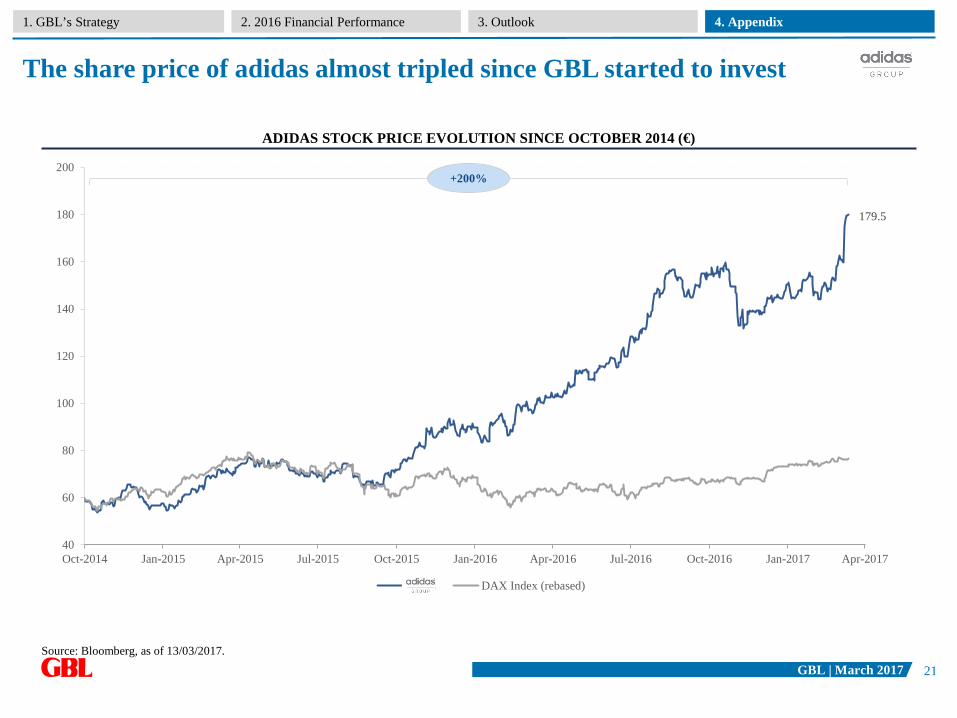

The share price of adidas almost tripled since GBL started to invest

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

179.5

40

60

80

100

120

140

160

180

200

Oct-2014 Jan-2015 Apr-2015 Jul-2015 Oct-2015 Jan-2016 Apr-2016 Jul-2016 Oct-2016 Jan-2017 Apr-2017

adidas DAX Index (rebased)

Source: Bloomberg, as of 13/03/2017.

ADIDAS STOCK PRICE EVOLUTION SINCE OCTOBER 2014 (€)

+200%

21

GBL March 2017

1. GBL’s strategy – 2016 and forward 2

2. 2016 Financial performance 22

3. Outlook 27

4. Appendix 30

22

GBL | March 2017

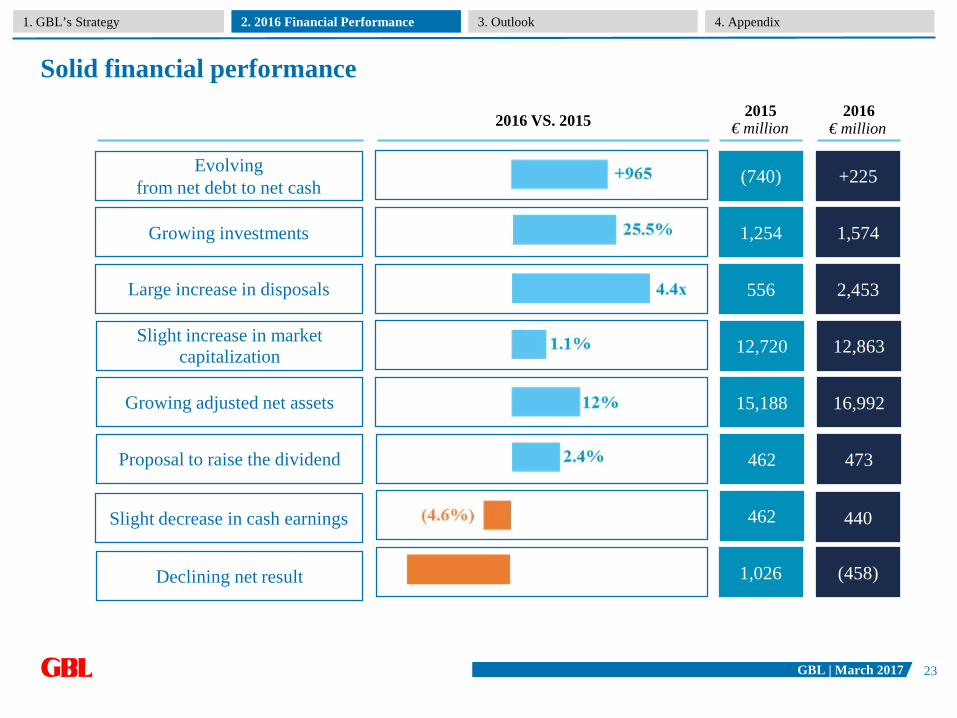

Solid financial performance

Declining net result

Slight decrease in cash earnings

Proposal to raise the dividend

(458)

440

473

Evolvingfrom net debt to net cash +225

Slight increase in marketcapitalization 12,863

Growing adjusted net assets 16,992

Growing investments 1,574

1,026

462

462

(740)

12,720

15,188

1,254

Large increase in disposals 2,453556

2016 VS. 2015 2015 2016€ million € million

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

23

GBL | March 2017

2015 2016 DifferenceWeight in portfolio

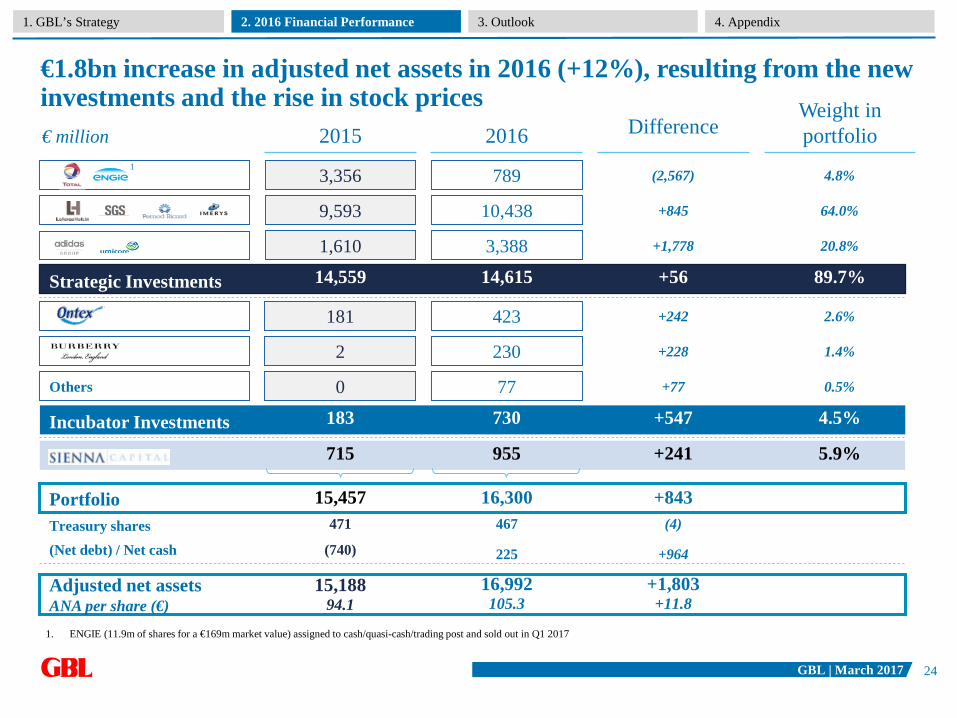

€1.8bn increase in adjusted net assets in 2016 (+12%), resulting from the new investments and the rise in stock prices

Portfolio

14,559 14,615

181 423

715 955

15,457 16,300

€ million

+56

+242

+241

89.7%

2.6%

5.9%

Treasury shares 471 467 (4)

(Net debt) / Net cash (740) 225 +964

Adjusted net assetsANA per share (€)

15,18894.1

16,992105.3

+1,803+11.8

+843

1. ENGIE (11.9m of shares for a €169m market value) assigned to cash/quasi-cash/trading post and sold out in Q1 2017

183 730 +547 4.5%

2 230 +228 1.4%

1,610 3,388 +1,778 20.8%

9,593 10,438 +845 64.0%

3,356 789 (2,567) 4.8%

0 77 +77 0.5%

Strategic Investments

Incubator Investments

Others

1

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

24

GBL | March 2017

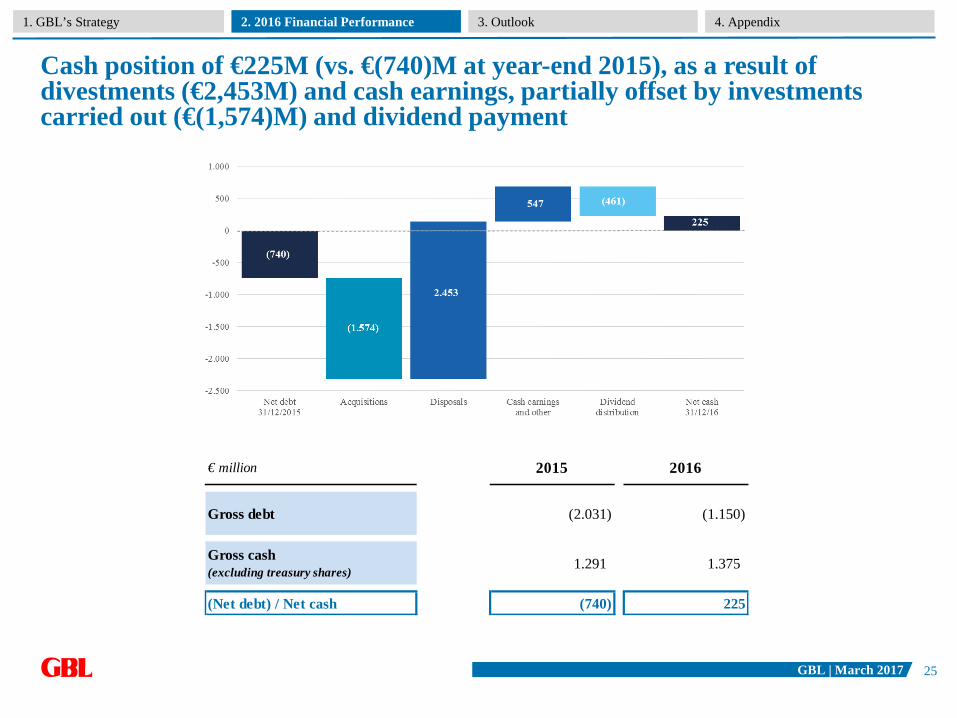

Cash position of €225M (vs. €(740)M at year-end 2015), as a result of divestments (€2,453M) and cash earnings, partially offset by investmentscarried out (€(1,574)M) and dividend payment

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Gross debt (2.031) (1.150)

Gross cash (excluding treasury shares) 1.291 1.375

(Net debt) / Net cash (740) 225

2016€ million 2015

25

GBL | March 2017

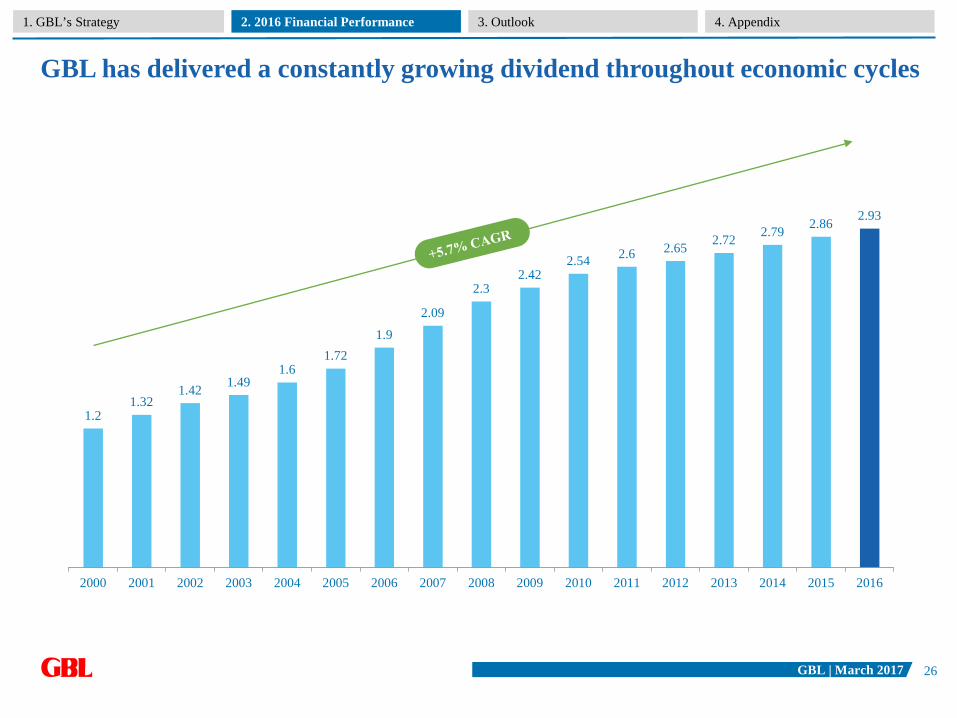

1.21.32

1.42 1.491.6

1.721.9

2.09

2.32.42

2.54 2.6 2.65 2.72 2.79 2.86 2.93

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GBL has delivered a constantly growing dividend throughout economic cycles

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

26

GBL March 2017

1. GBL’s strategy – 2016 and forward 2

2. 2016 Financial performance 22

3. Outlook 27

4. Appendix 30

27

GBL | March 2017

Total1

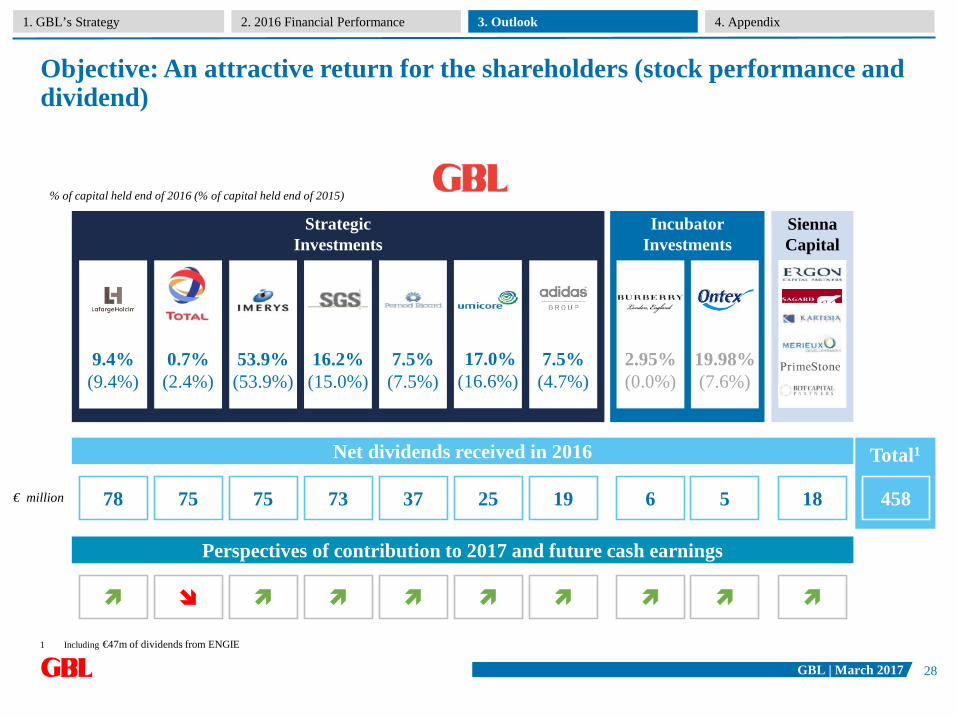

Objective: An attractive return for the shareholders (stock performance and dividend)

IncubatorInvestments

% of capital held end of 2016 (% of capital held end of 2015)

Strategic Investments

9.4%(9.4%)

16.2%(15.0%)

53.9%(53.9%)

7.5%(7.5%)

19.98%(7.6%)

17.0%(16.6%)

Sienna Capital

4581878 75 75 73 37 19 525

Net dividends received in 2016

€ million

7.5%(4.7%)

Perspectives of contribution to 2017 and future cash earnings

0.7%(2.4%)

6

2.95%(0.0%)

1 Including €47m of dividends from ENGIE

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

28

GBL | March 2017

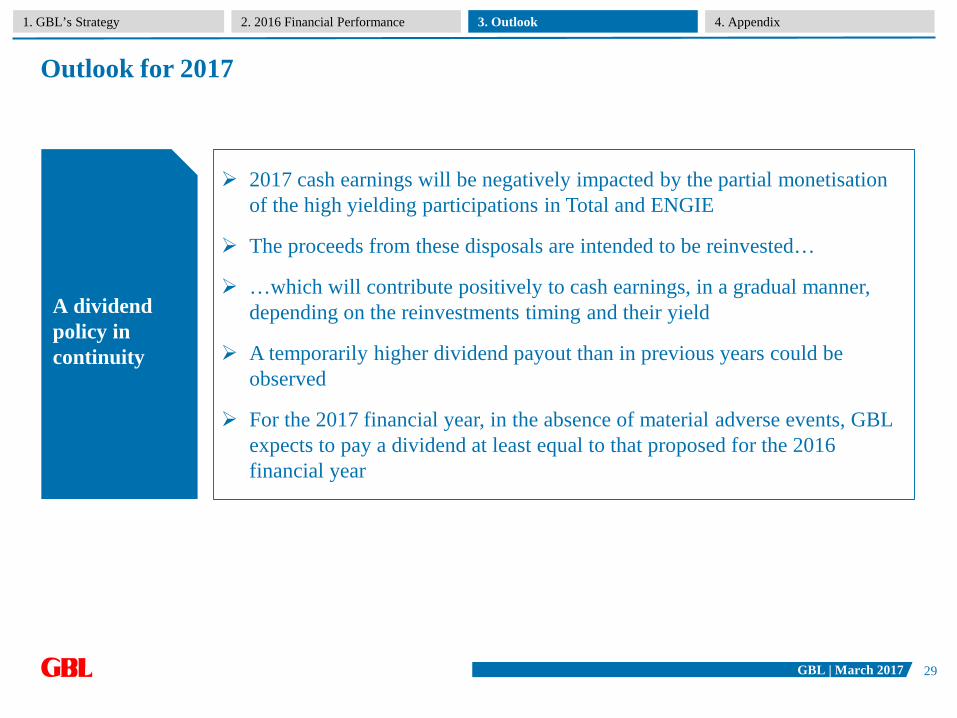

Outlook for 2017

A dividendpolicy in continuity

2017 cash earnings will be negatively impacted by the partial monetisationof the high yielding participations in Total and ENGIE

The proceeds from these disposals are intended to be reinvested…

…which will contribute positively to cash earnings, in a gradual manner, depending on the reinvestments timing and their yield

A temporarily higher dividend payout than in previous years could be observed

For the 2017 financial year, in the absence of material adverse events, GBL expects to pay a dividend at least equal to that proposed for the 2016 financial year

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

29

GBL March 2017

1. GBL’s strategy – 2016 and forward 2

2. 2016 Financial performance 22

3. Outlook 27

4. Appendix 30

30

GBL | March 2017

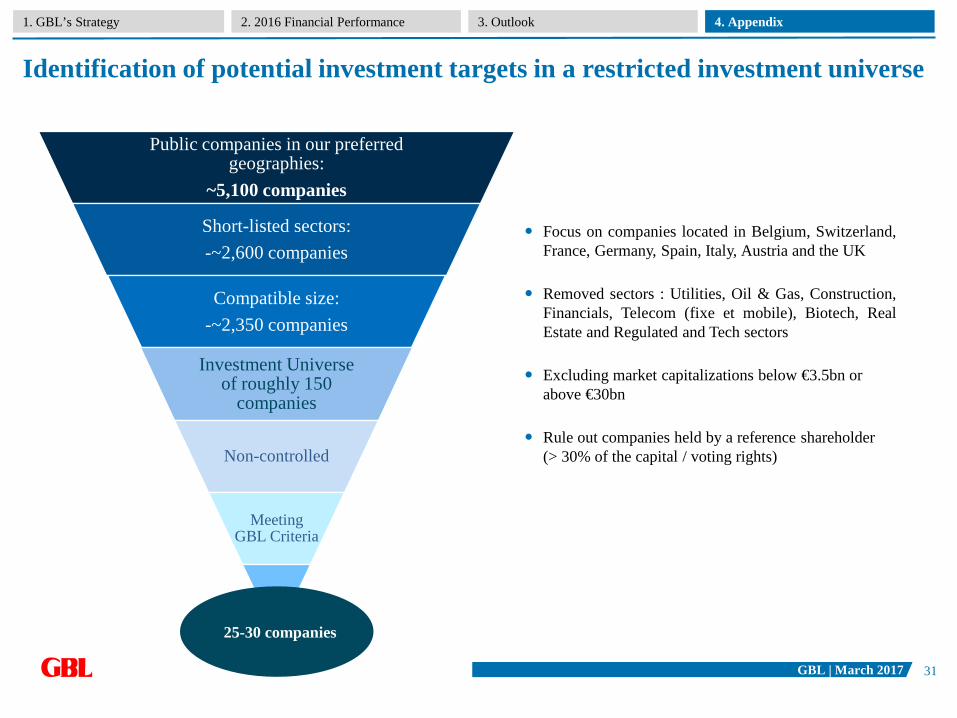

Identification of potential investment targets in a restricted investment universe

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Public companies in our preferred geographies:

~5,100 companies

Short-listed sectors: -~2,600 companies

Compatible size: -~2,350 companies

Investment Universe of roughly 150

companies

Non-controlled

Meeting GBL Criteria

25-30 companies

Focus on companies located in Belgium, Switzerland,France, Germany, Spain, Italy, Austria and the UK

Removed sectors : Utilities, Oil & Gas, Construction,Financials, Telecom (fixe et mobile), Biotech, RealEstate and Regulated and Tech sectors

Excluding market capitalizations below €3.5bn or above €30bn

Rule out companies held by a reference shareholder (> 30% of the capital / voting rights)

31

GBL | March 2017

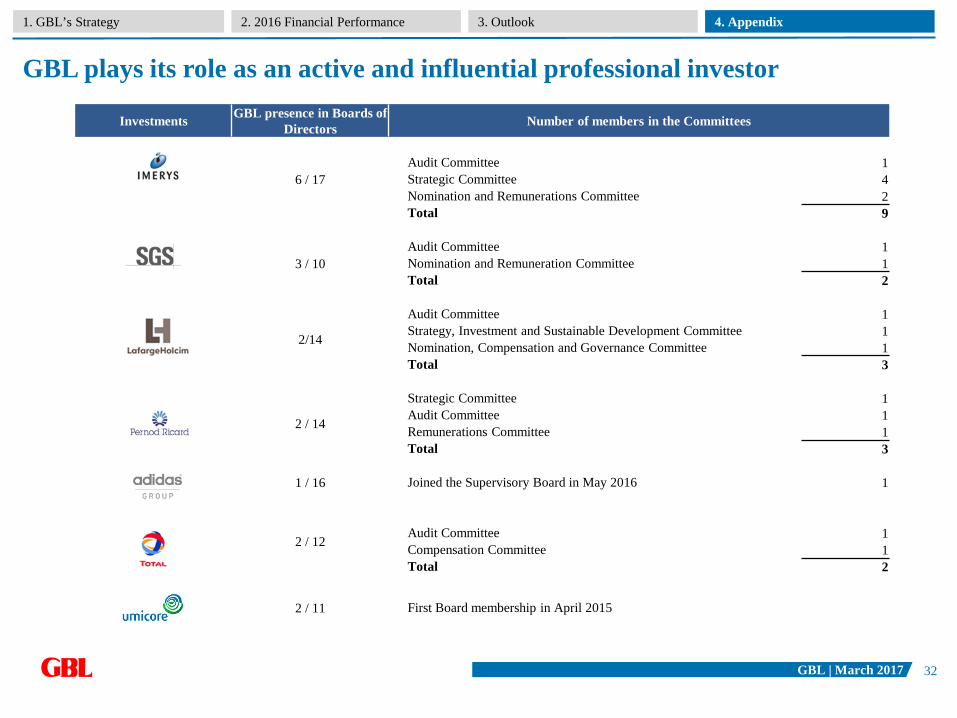

GBL plays its role as an active and influential professional investor

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Investments GBL presence in Boards of Directors Number of members in the Committees

6 / 17Audit Committee 1Strategic Committee 4Nomination and Remunerations Committee 2Total 9

3 / 10Audit Committee 1Nomination and Remuneration Committee 1Total 2

2/14

Audit Committee 1Strategy, Investment and Sustainable Development Committee 1Nomination, Compensation and Governance Committee 1Total 3

2 / 14

Strategic Committee 1Audit Committee 1Remunerations Committee 1Total 3

1 / 16 Joined the Supervisory Board in May 2016 1

2 / 12Audit Committee 1Compensation Committee 1Total 2

2 / 11 First Board membership in April 2015

32

GBL | March 2017

Sienna Capital provides several benefits to GBL

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Earn attractive risk-adjusted returns and contribute to growing GBL’s NAV and dividend+

Part of an ongoing diversification of GBL’s portfolio and revenue stream+

Attract talent around the activities of GBL and serve as a best ideas factory+

Provide co-investment opportunities +

100%

33

GBL | March 2017

Sienna Capital currently invested in six investment managers

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

34

GBL | March 2017

Sienna Capital – Description of the investments

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

Ergon Capital Partners (ECP) was created in 2005 as a private equity fund operating in the mid-market segment. It invests between €20m and €70m in companies operating in niche markets in the Benelux, Italy, Spain, France, Germany and Switzerland, with positions that are dominant and sustainable over the long term and in industries with prospects for consolidation.

Kartesia offers liquidity and credit solutions to mid-sized European companies, while providing a higher stable return to its investors. In general, Kartesia wishes to facilitate the participation of institutional investors and major individual investors in the European LBO debt market, by offering them exposure to highly rated, resilient and diversified credit through primary, secondary or rescue financing operations carried out with duly selected mid-sized companies.

Created in 2002 on the initiative of Power Corporation of Canada, Sagard invests in companies valued at more than €100m that are leaders in their markets, primarily in French-speaking European countries. Working with company management, it supports them in their growth.

Established in 2009, Mérieux Développement is an investment manager specialised in growth and venture capital investments in the healthcare sector. Mérieux Développement works alongside entrepreneurs and companies whose products and services can bring genuine advances to the health of patients and consumers worldwide, offering them access to its industry expertise and global network. Mérieux Développement is an affiliate of Institut Mérieux.

BDT Capital Partners was created in 2009 by Byron Trott, a longstanding partner of Goldman Sachs, with the aim of meeting the strategic and financial needs of families and/or company founders around the globe.

PrimeStone was established in 2014 by three former partners from the Carlyle Group, specialised in buyouts, having worked and invested together across Europe for more than 15 years. PrimeStone has a strategy of construc-tive and active management in mid-sized listed European companies that have significant value creation potential through strategic, operational or fin. improvement. PrimeStone creates value by taking a long-term perspective, adopting an active approach and having a significant influence over its under-lying investments through a dialogue with boards and management teams.

35

GBL | March 2017

A negative net result (€(458)m), mainly explained by LafargeHolcimimpairment

€ million 2015 2016 DIFFERENCE

Cash earnings 462 440 (21)

Mark to market and other non cash items 91 14 (76)

Operating companies and Sienna Capital (45) 223 +268

Eliminations, capital gains, depreciations and reversals 519 (1.136) (1.655)

Consolidated net result 1.026 (458) (1.484)

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

36

GBL | March 2017

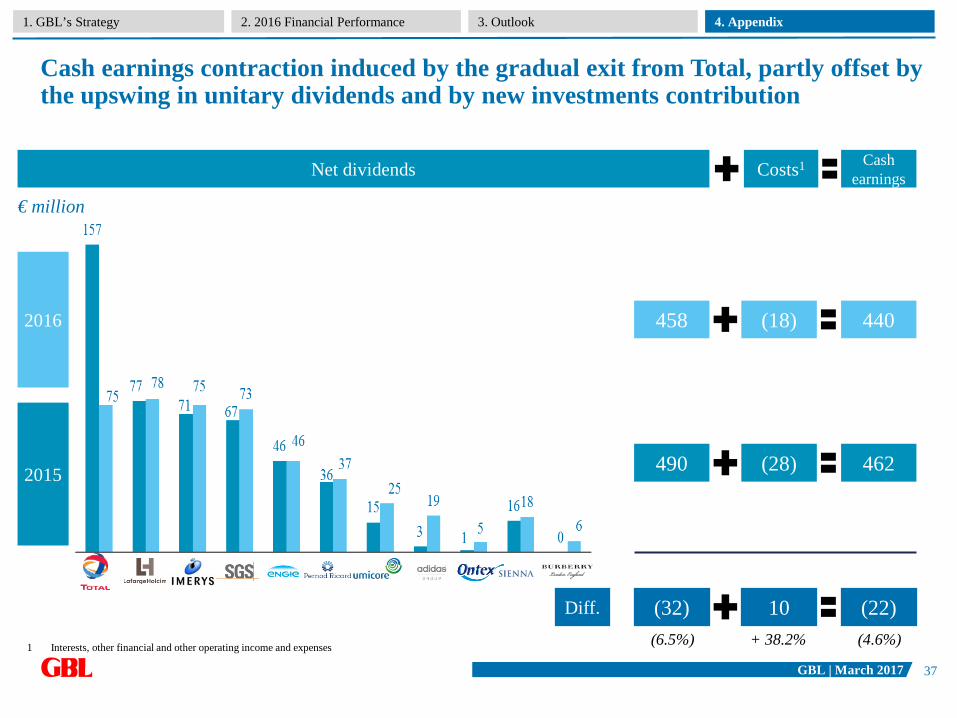

Cash earnings contraction induced by the gradual exit from Total, partly offset by the upswing in unitary dividends and by new investments contribution

2015

2016

Costs1Net dividends Cashearnings

10 (22)Diff. (32)

(28) 462490

(18) 440458

(4.6%)(6.5%) + 38.2%

€ million

1 Interests, other financial and other operating income and expenses

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

37

GBL | March 2017

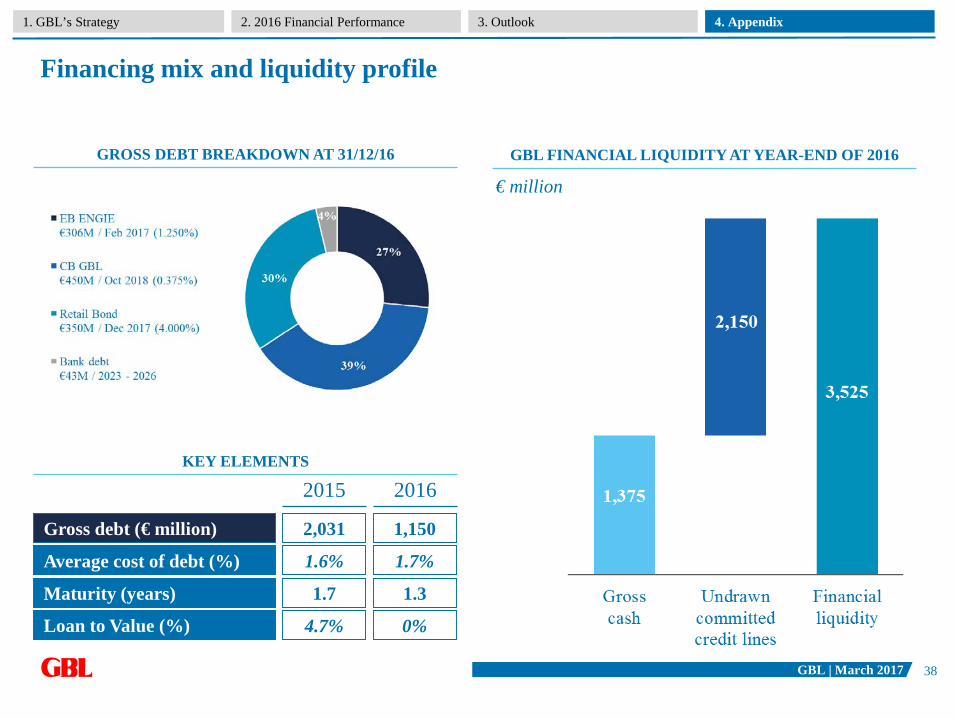

Financing mix and liquidity profile

GBL FINANCIAL LIQUIDITY AT YEAR-END OF 2016GROSS DEBT BREAKDOWN AT 31/12/16

2015 2016

Gross debt (€ million) 2,031 1,150

Average cost of debt (%) 1.6% 1.7%

Maturity (years) 1.7 1.3

Loan to Value (%) 4.7% 0%

KEY ELEMENTS

€ million

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

38

GBL | March 2017

Profiles

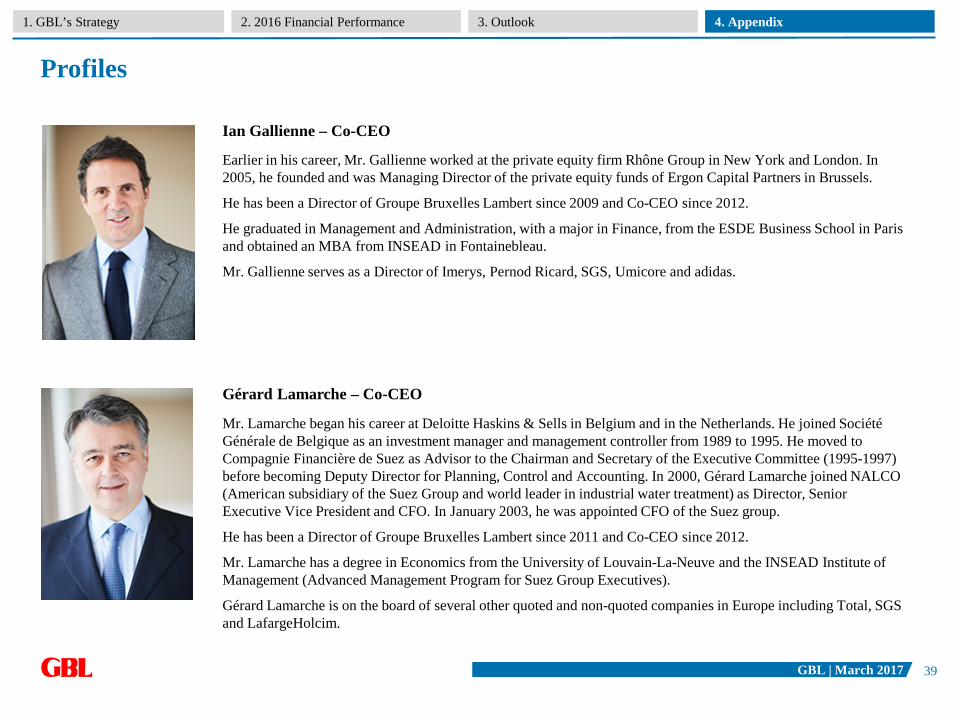

Earlier in his career, Mr. Gallienne worked at the private equity firm Rhône Group in New York and London. In 2005, he founded and was Managing Director of the private equity funds of Ergon Capital Partners in Brussels.

He has been a Director of Groupe Bruxelles Lambert since 2009 and Co-CEO since 2012.

He graduated in Management and Administration, with a major in Finance, from the ESDE Business School in Paris and obtained an MBA from INSEAD in Fontainebleau.

Mr. Gallienne serves as a Director of Imerys, Pernod Ricard, SGS, Umicore and adidas.

Ian Gallienne – Co-CEO

Mr. Lamarche began his career at Deloitte Haskins & Sells in Belgium and in the Netherlands. He joined SociétéGénérale de Belgique as an investment manager and management controller from 1989 to 1995. He moved to Compagnie Financière de Suez as Advisor to the Chairman and Secretary of the Executive Committee (1995-1997) before becoming Deputy Director for Planning, Control and Accounting. In 2000, Gérard Lamarche joined NALCO (American subsidiary of the Suez Group and world leader in industrial water treatment) as Director, Senior Executive Vice President and CFO. In January 2003, he was appointed CFO of the Suez group.

He has been a Director of Groupe Bruxelles Lambert since 2011 and Co-CEO since 2012.

Mr. Lamarche has a degree in Economics from the University of Louvain-La-Neuve and the INSEAD Institute of Management (Advanced Management Program for Suez Group Executives).

Gérard Lamarche is on the board of several other quoted and non-quoted companies in Europe including Total, SGS and LafargeHolcim.

Gérard Lamarche – Co-CEO

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

39

GBL | March 2017

Profiles

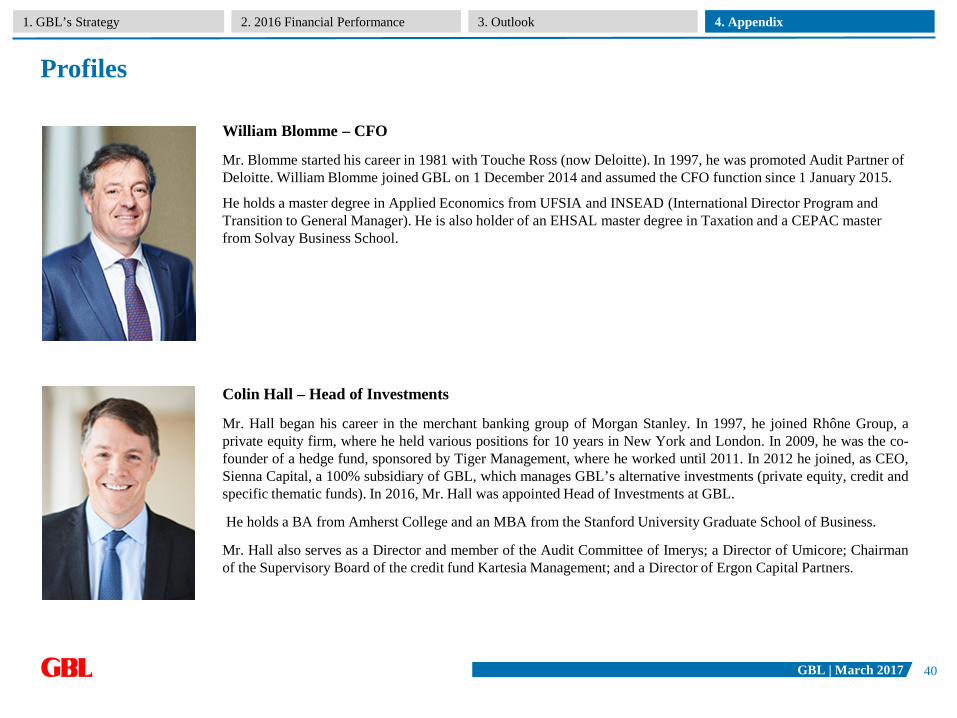

Mr. Blomme started his career in 1981 with Touche Ross (now Deloitte). In 1997, he was promoted Audit Partner of Deloitte. William Blomme joined GBL on 1 December 2014 and assumed the CFO function since 1 January 2015.

He holds a master degree in Applied Economics from UFSIA and INSEAD (International Director Program and Transition to General Manager). He is also holder of an EHSAL master degree in Taxation and a CEPAC master from Solvay Business School.

William Blomme – CFO

Mr. Hall began his career in the merchant banking group of Morgan Stanley. In 1997, he joined Rhône Group, aprivate equity firm, where he held various positions for 10 years in New York and London. In 2009, he was the co-founder of a hedge fund, sponsored by Tiger Management, where he worked until 2011. In 2012 he joined, as CEO,Sienna Capital, a 100% subsidiary of GBL, which manages GBL’s alternative investments (private equity, credit andspecific thematic funds). In 2016, Mr. Hall was appointed Head of Investments at GBL.

He holds a BA from Amherst College and an MBA from the Stanford University Graduate School of Business.

Mr. Hall also serves as a Director and member of the Audit Committee of Imerys; a Director of Umicore; Chairmanof the Supervisory Board of the credit fund Kartesia Management; and a Director of Ergon Capital Partners.

Colin Hall – Head of Investments

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

40

GBL | March 2017

Profiles

He started his career in the banking sector at Générale de Banque (now BNP Paribas Fortis), where he held various commercial positions. He moved on to Crédit Lyonnais Belgium (now Deutsche Bank) working mainly in fixed income and after a couple of years he joined de Buck Vermogensbankiers in Ghent where he managed for eight years the buy-side research department. After 12 years of experience as a sell-side equity analyst for Benelux holding and portfolio companies at Bank Degroof Petercam, Hans D’Haese joined GBL in December 2016, where he is in charge of investor relations.

Hans D’Haese graduated in Business Management from the Ghent Odysee University-College.

Hans D’Haese – IR

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

41

GBL | March 2017

Disclaimer

This presentation has been prepared by Groupe Bruxelles Lambert (“GBL”) exclusively for information purposes. This presentation isincomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by GBL.

This document should not be construed as an offer, invitation to offer, or solicitation, or any advice or recommendation to buy, subscribe for, issue or sell any financial instrument, investment or derivative thereof referred to in this document or as any form of commitment to enter into any transaction in relation to the subject matter of this document.

This presentation has not been reviewed or registered with any public authority or stock exchange. Persons into whose possession this presentation come are required to inform themselves about and to comply with all applicable laws and regulations in force in anyjurisdiction in or from which it invests or receives or possesses this presentation.

Prospective investors are required to make their own independent investigations and appraisals of GBL before taking any investment decision with respect to securities of GBL.

GBL does not make any representation or warranty (expressed or implied) as to the accuracy or completeness of the informationcontained in this document and as to the accuracy of the projections, estimates, assumptions and figures contained in this document. By receipt of this document, the recipient agrees that GBL (or either of its shareholders, directors or employees) shall have no liability for any misstatement or omission or fact or any opinion expressed herein, nor for the consequences of any reliance upon any statement, conclusion or opinion contained herein. All value indications included in this document are derived from the financial markets as of the date of this report. It is therefore obvious that a modification of the conditions prevailing in the financial markets will have an effect on the figures present hereafter.

This document is the exclusive property of GBL. Recipient of this presentation may not reproduce, redistribute or pass on, in whole or in part, this presentation to any person.

By using or retaining a copy hereof, user and/or retainer hereby acknowledge, agree and accept that they have read this disclaimer and agreed to be bound by it.

1. GBL’s Strategy 4. Appendix3. Outlook2. 2016 Financial Performance

42