Introduction to the Accounting Environment and Accounting Equation Chapter 1 1.

36

Introduction to the Accounting Environment and Accounting Equation Chapte r 1

-

Upload

oswin-griffith -

Category

Documents

-

view

243 -

download

5

Transcript of Introduction to the Accounting Environment and Accounting Equation Chapter 1 1.

Introduction to the Accounting

Environment and Accounting

Equation

Chapter

11

Learning OutcomesLearning Outcomes

Understand the importance of financial information in business

Understand the basic concepts and purpose of financial accounting

Understand the objective and characteristics of financial statements

Identify the users of financial statements and their information needs

Identify the differences and changes between assets, liabilities and capital

ACCOUNTINGACCOUNTING

Definition: an information system that provides report to stakeholders about the economic activities and condition of a business.

So, accounting is the process of:

- Identifying

- Measuring

- Communicating economic information to

permit informed judgments and decisions by users of the information

IdentifiesIdentifies

RecordsRecords

CommunicatesCommunicatesRelevantRelevant

ReliableReliable

ComparableComparable

Importance of AccountingImportance of Accounting

AccountingAccountingis a

system that

information

that is

to help users make better decisions.

to help users make better decisions.

Identifying Business Activities

Recording Business Activities

Communicating

Business Activities

Accounting ActivitiesAccounting Activities

Users of Accounting InformationUsers of Accounting Information

External Users

•Lenders

•Shareholders

•Governments

•Consumer Groups

•External Auditors

•Customers

Internal Users

•Managers

•Officers

•Internal Auditors

•Sales Staff

•Budget Officers

•Controllers

Tutorial 1: Basic Accounting ConceptsTutorial 1: Basic Accounting Concepts

1) Business Entity

2) Going Concern

3) Historical Cost

4) Objectivity

5) Consistency

6) Conservatism

7) Accounting Period

8) Accrual Concept

9) Matching Principle

10) Types of Business Units

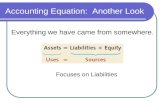

The accounting equation must remain in balance after each transaction.

LiabilitiesLiabilities EquityEquityAssetsAssets = +

Transaction Analysis EquationTransaction Analysis Equation

Let’s discuss the

components of the

equation

Categories of a Classified Balance SheetAssets Liabilities and Equity

Current Assets Current LiabilitiesNoncurrent Assets Noncurrent Liabilities

Long-Term Investments EquityPlant AssetsIntangible Assets

Current items are those expected to come due (both collected and owed) within the longer of one year or

the company’s normal operating cycle.

Balance SheetBalance Sheet

• Statement that lists all the assets, owner’s equity and liabilities at a particular date.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current assets Cash 6,500$ Short-term investments 2,100 Accounts receivable 4,400 Merchandise inventory 27,500 Prepaid expenses 2,400 Total current assets 42,900$ Long-term investments Notes receivable 1,500 Investments in stocks and bonds 18,000 Land held for future expansion 48,000 Total investments 67,500 Plant assets Store equipment 33,200$ Less accumulated depreciation 8,000 25,200 Buildings 170,000 Less accumulated depreciation 45,000 125,000 Land 73,200 Total plant assets 223,400 Intangible assets 10,000 Total assets 343,800$

ASSETS

Current assets are expected to be sold, collected, or used within one year or the company’s operating

cycle.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current assets Cash 6,500$ Short-term investments 2,100 Accounts receivable 4,400 Merchandise inventory 27,500 Prepaid expenses 2,400 Total current assets 42,900$ Long-term investments Notes receivable 1,500 Investments in stocks and bonds 18,000 Land held for future expansion 48,000 Total investments 67,500 Plant assets Store equipment 33,200$ Less accumulated depreciation 8,000 25,200 Buildings 170,000 Less accumulated depreciation 45,000 125,000 Land 73,200 Total plant assets 223,400 Intangible assets 10,000 Total assets 343,800$

ASSETS

Long-term investments are expected to be held for the longer of one year or the operating cycle.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current assets Cash 6,500$ Short-term investments 2,100 Accounts receivable 4,400 Merchandise inventory 27,500 Prepaid expenses 2,400 Total current assets 42,900$ Long-term investments Notes receivable 1,500 Investments in stocks and bonds 18,000 Land held for future expansion 48,000 Total investments 67,500 Plant assets Store equipment 33,200$ Less accumulated depreciation 8,000 25,200 Buildings 170,000 Less accumulated depreciation 45,000 125,000 Land 73,200 Total plant assets 223,400 Intangible assets 10,000 Total assets 343,800$

ASSETS

Plant assets are tangible long-lived assets used to produce or sell

products and services.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current assets Cash 6,500$ Short-term investments 2,100 Accounts receivable 4,400 Merchandise inventory 27,500 Prepaid expenses 2,400 Total current assets 42,900$ Long-term investments Notes receivable 1,500 Investments in stocks and bonds 18,000 Land held for future expansion 48,000 Total investments 67,500 Plant assets Store equipment 33,200$ Less accumulated depreciation 8,000 25,200 Buildings 170,000 Less accumulated depreciation 45,000 125,000 Land 73,200 Total plant assets 223,400 Intangible assets 10,000 Total assets 343,800$

ASSETS

Intangible assets are long-term resources used to produce or sell

products and services and that lack physical form.

Current liabilities are obligations due within the longer of one year or the

company’s operating cycle.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current liabilities Accounts payable 15,300$ Wages payable 3,200 Notes payable 3,000 Current portion of long-term liabilities 7,500 Total current liabilities 29,000$ Long-term liabilities: Notes payable (net of current portion) 150,000 Total liabilities 179,000$

T. Hawk, Capital 164,800 Total liabilities and equity 343,800$

LIABILITIES

EQUITY

Long-term liabilities are obligations not due within the longer of one year

or the company’s operating cycle.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current liabilities Accounts payable 15,300$ Wages payable 3,200 Notes payable 3,000 Current portion of long-term liabilities 7,500 Total current liabilities 29,000$ Long-term liabilities: Notes payable (net of current portion) 150,000 Total liabilities 179,000$

T. Hawk, Capital 164,800 Total liabilities and equity 343,800$

LIABILITIES

EQUITY

Equity is the owner’s claim on the assets.

Snowboarding ComponentsBalance Sheet

January 31, 2005

Current liabilities Accounts payable 15,300$ Wages payable 3,200 Notes payable 3,000 Current portion of long-term liabilities 7,500 Total current liabilities 29,000$ Long-term liabilities: Notes payable (net of current portion) 150,000 Total liabilities 179,000$

T. Hawk, Capital 164,800 Total liabilities and equity 343,800$

LIABILITIES

EQUITY

The accounts involved are:

(1) Cash (asset)

(2) J. Scott, Capital (equity)

1. J. Scott, the owner, contributed $20,000 cash to start the business.

Example of Transaction AnalysisExample of Transaction Analysis

Continue…Continue…

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

(1) 20,000$ 20,000$

20,000$ -$ -$ -$ -$ 20,000$

20,000$ = 20,000$

J. Scott, the owner, contributed $20,000 cash to start the business.

The accounts involved are:

(1) Cash (asset)

(2) Supplies-Ali (asset)

Continue…Continue…

2. Purchased supplies (Ali) paying $1,000 cash.

Continue…Continue…

Purchased supplies paying $1,000 cash.

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

(1) 20,000$ 20,000$ (2) (1,000) 1,000$

19,000$ 1,000$ -$ -$ -$ 20,000$

20,000$ = 20,000$

The accounts involved are:

(1) Cash (asset)

(2) Equipment (asset)

Continue…Continue…

3. Purchased equipment for $15,000 cash.

Continue…Continue…

Purchased equipment for $15,000 cash.

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

(1) 20,000$ 20,000$ (2) (1,000) 1,000$ (3) (15,000) 15,000$

4,000$ 1,000$ 15,000$ -$ -$ 20,000$

20,000$ = 20,000$

The accounts involved are:

(1) Supplies-Purchases (asset)

(2) Equipment (asset)

(3) Accounts Payable (liability)

Continue…Continue…

4. Purchased Supplies on credit of $200 and Equipment of $1,000 also in

credit.

Continue…Continue…

Purchased Supplies of $200 and Equipment of $1,000 on account.

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

(1) 20,000$ 20,000$ (2) (1,000) 1,000$ (3) (15,000) 15,000$ (4) 200 1,000 1,200$

4,000$ 1,200$ 16,000$ 1,200$ -$ 20,000$

21,200$ = 21,200$

The accounts involved are:

(1) Cash (asset)

(2) Notes payable-Loan (liability)

Continue…Continue…

5. Borrowed $4,000 from 1st American Bank.

Continue…Continue…

Borrowed $4,000 from 1st American Bank.

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

(1) 20,000$ 20,000$ (2) (1,000) 1,000$ (3) (15,000) 15,000$ (4) 200 1,000 1,200$ (5) 4,000 4,000$

8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$

25,200$ = 25,200$

Assets = Liabilities + Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

Bal. 8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$

8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$

25,200$ = 25,200$

Continue…Continue…

The balances so far appear below. Note that the Balance Sheet Equation is still in balance.

Now let’s look at transactions involving revenue, expenses and withdrawals.

The accounts involved are:

(1) Cash (asset)

(2) Revenues-I/S (equity)

Continue…Continue…

6. Rendered consulting services (buss. xtvt) receiving $3,000 cash.

Assets = Liabilities +

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital Revenue

Bal. 8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ (6) 3,000 3,000$

11,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ 3,000$

28,200$ = 28,200$

Equity

Continue…Continue…

Rendered consulting services receiving $3,000 cash.

The accounts involved are:

(1) Cash (asset)

(2) Salaries expense (equity)

Continue…Continue…

7. Paid salaries of $800 to employees.

Remember that the balance in the salaries expense account actually increases.

But, equity actually decreases because expenses reduce equity.

Continue…Continue…

Assets = Liabilities +

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital Revenue Expenses

Bal. 8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ (6) 3,000 3,000$ (7) (800) (800)$

10,200$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ 3,000$ (800)$

27,400$ = 27,400$

Equity

Remember that expenses decrease equity.

Paid salaries of $800 to employees.

The accounts involved are:

(1) Cash (asset)

(2) J. Scott, Withdrawals (equity)

Continue…Continue…

8. J. Scott withdrew $500 from the business for personal use.

Remember that the balance in the J. Scott, Withdrawals account actually increases.

But, equity actually decreases because withdrawals reduce equity.

Continue…Continue…

Assets = Liabilities +

Cash Supplies EquipmentAccounts Payable

Notes Payable

J. Scott, Capital

J. Scott, Withdrawal Revenue Expenses

Bal. 8,000$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ (6) 3,000 3,000$ (7) (800) (800)$ (8) (500) (500)$

9,700$ 1,200$ 16,000$ 1,200$ 4,000$ 20,000$ (500)$ 3,000$ (800)$

26,900$ = 26,900$

Equity

Remember that withdrawals decrease equity.

J. Scott withdrew $500 from the business for personal use.

Tutorial 2: Write the accounting equation and the balance sheet Tutorial 2: Write the accounting equation and the balance sheet

Apr. 1 Karen commenced business by depositing cash $25000 in the bank as capital

4 A motor vehicle was purchased and paid with company cheque, $20 000 10 Furniture $4 500 was purchased on credit from

Home Style Pte Ltd. 18 Karen withdrew cash $1000 from the business account to pay for his private expenditure 25 A cheque $2500 was paid to Home Style Pte Ltd., as

part of the payment for amount owing 30 Karen paid Home Style Pte Ltd. For the balance of

the amount owing with his personal cheque

End of Chapter 1End of Chapter 1