Introduction to RPC Group/media/Files/R/RPC-Group/documents... · Introduction to RPC Group ......

29

Introduction to RPC Group September 2017 101 THE ESSENTIAL INGREDIENT RPC Group Plc Introduction to RPC Group September 2017

Transcript of Introduction to RPC Group/media/Files/R/RPC-Group/documents... · Introduction to RPC Group ......

Introduction to RPC GroupSeptember 2017

101

THE ESSENTIAL INGREDIENT

RPC Group PlcIntroduction to RPC Group

September 2017

Introduction to RPC GroupSeptember 2017

102

The Group, markets and strategySetting the scene 3Brexit impact? 8RPC Group Strategy: Vision 2020 10Back up 23

Introduction to RPC GroupSeptember 2017

103Setting the scene

Introduction to RPC GroupSeptember 2017

104

A leading global plastic product design and engineering company for packaging and selected non-packaging markets

Europe 75%North America 17%Asia 4%Rest of World 4%

RPC Sales 2016/17 – by destination*

Food 29%Non-Food 26%Personal Care 12%Beverage 11%Healthcare 5%Technical Components 17%

RPC Sales 2016/17 – by end market*

£1.7bn*by end market by region

£1.7bn*

*Pro forma to include a full year of completed acquisitions

€4bn+sales

194+operations

34+countries

32+innovation

centres

24,900+employees

€4bn*By end market

€4bn*By region

Introduction to RPC GroupSeptember 2017

105

Global footprint

RPC Group is well placed to support its customers globallywith leading design and engineering capabilities

• Over 194 operations in 34 countries and 32 design & engineering centres

• Over 24,900 employees

• Major European plastic converter

• Industry leading innovator

• Listed on London StockExchange - 1993

• Member of the FTSE 250

Where we manufactureWhere we sell

Introduction to RPC GroupSeptember 2017

106

Corporate history

0

50

100

150

200

250

£0

£500

£1,000

£1,500

£2,000

£2,500

£3,000

£3,500

£4,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

UK growth phase Mainland European growth phase Consolidation Selective growth

Turnover (£m) Operating sites

Promens and Pet Power acquisitions

FlotationMBO

Acquisition of Wiko division

M&H acquisition

Superfos acquisitionAcquisition of 11 sites from Rexam / Nampak

Various smaller acquisitions

Ace acquisition

Turnover: ReportedTurnover: Analyst expectations*Number of operating sites

GCS and BPI acquisitionsAcquisition of Schmalbach-Lubeca’s plastics division

Impact of Letica

* Based on 9 analysts at 19 July 2017

Introduction to RPC GroupSeptember 2017

107

10.7%

20.6% 21.2% 21.9% 22.4%

26.0%

08/09 12/13 13/14 14/15 15/16 16/17

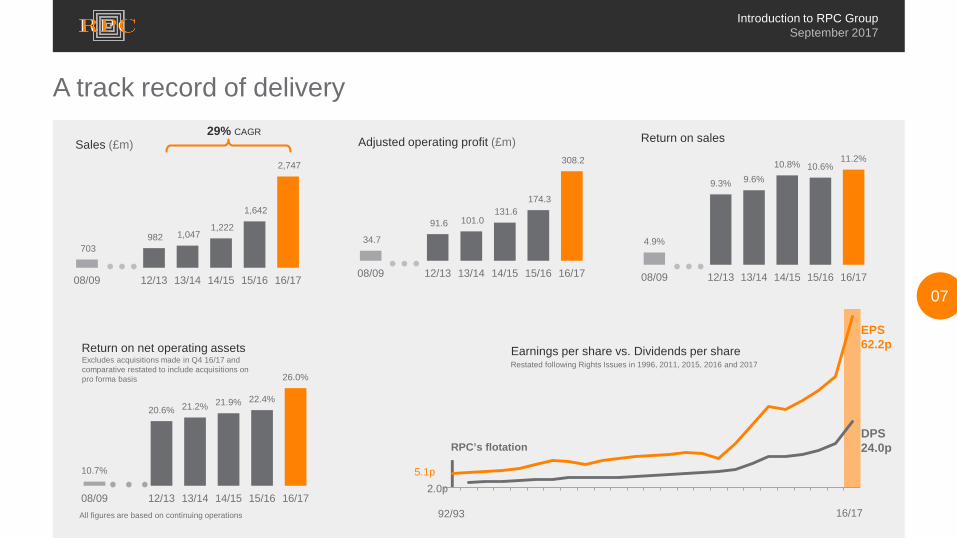

A track record of delivery

703 982 1,047

1,222

1,642

2,747

08/09 12/13 13/14 14/15 15/16 16/17

Sales (£m)

4.9%

9.3% 9.6%10.8% 10.6%

11.2%

08/09 12/13 13/14 14/15 15/16 16/17

34.7

91.6 101.0 131.6

174.3

308.2

08/09 12/13 13/14 14/15 15/16 16/17

Return on salesAdjusted operating profit (£m)29% CAGR

Earnings per share vs. Dividends per share

EPS62.2p

DPS24.0pRPC’s flotation

2.0p

16/17

Restated following Rights Issues in 1996, 2011, 2015, 2016 and 2017

5.1p

• • • • • • • • •

92/93

Return on net operating assets

All figures are based on continuing operations

Excludes acquisitions made in Q4 16/17 and comparative restated to include acquisitions on pro forma basis

Introduction to RPC GroupSeptember 2017

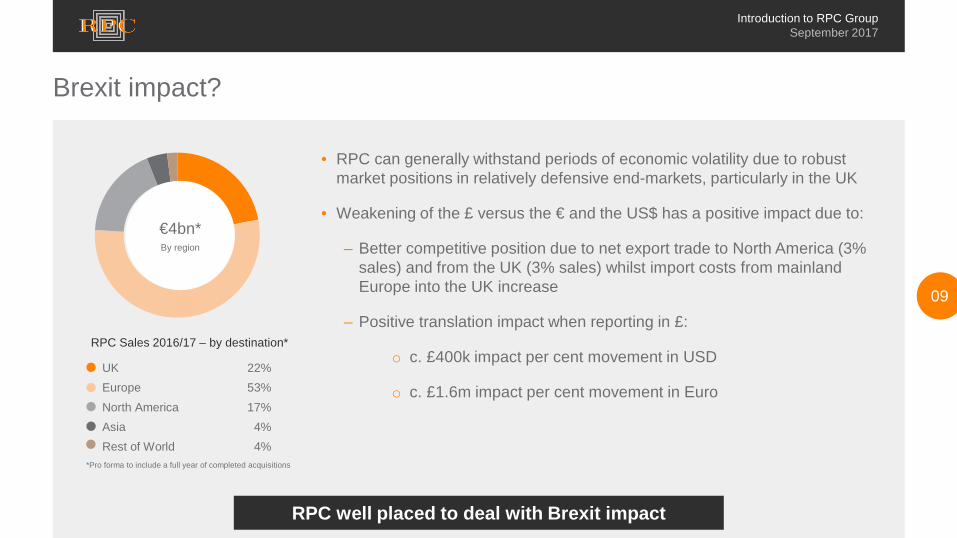

108Brexit impact?

Introduction to RPC GroupSeptember 2017

109

Brexit impact?

UK 22%Europe 53%North America 17%Asia 4%Rest of World 4%

RPC Sales 2016/17 – by destination*

€4bn*By region

• RPC can generally withstand periods of economic volatility due to robust market positions in relatively defensive end-markets, particularly in the UK

• Weakening of the £ versus the € and the US$ has a positive impact due to:

– Better competitive position due to net export trade to North America (3% sales) and from the UK (3% sales) whilst import costs from mainland Europe into the UK increase

– Positive translation impact when reporting in £:

o c. £400k impact per cent movement in USD

o c. £1.6m impact per cent movement in Euro

RPC well placed to deal with Brexit impact

*Pro forma to include a full year of completed acquisitions

Introduction to RPC GroupSeptember 2017

110RPC Group Strategy: Vision 2020

Introduction to RPC GroupSeptember 2017

111

High added value niche strategy outside Europe

Plastic packaging is forecast to grow by 5.1% outside Europe whilst 75% of RPC’s sales are currently in Europe

Plastic packaging - whilst concentrated in selective niches -remains a largely segmented market

Plastic packaging market forecast to grow by 4.4% globally in the next five years with 2.3% growth in Europe

Vision 2020: focused growth

Source: Smithers Pira, 2015

Innovative design and engineering company

Leading consolidatorin Europe

FOC

USE

D G

RO

WTH

Continuing focus on organic growth

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Pursuing added value opportunities in nonpackaging markets

Growing high value added products

A strategic extension of RPC’s core competencies – focus on selected niches where opportunities exist to add value

Introduction to RPC GroupSeptember 2017

112

Opportunities for organic growth

Paper Paper

Metal MetalGlass Glass

Rigid plastic

Rigid plastic

2015 2020

Rigid packaging market projections

Source: Smithers Pira, 2015

$ Billions, based on constant prices and exchange rates

Plastic continues to advance at the expense of competing materials

Europeby packaging type

Rest of

World

Rest of

World

2015 2020

EuropeEurope

CAGR

1.7%

4.4%

3.5%

Globalby region

CAGR

1.4%

2.3%

1.9%

(0.5)%

1.7%

$630

$755

$177$193

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

Introduction to RPC GroupSeptember 2017

113

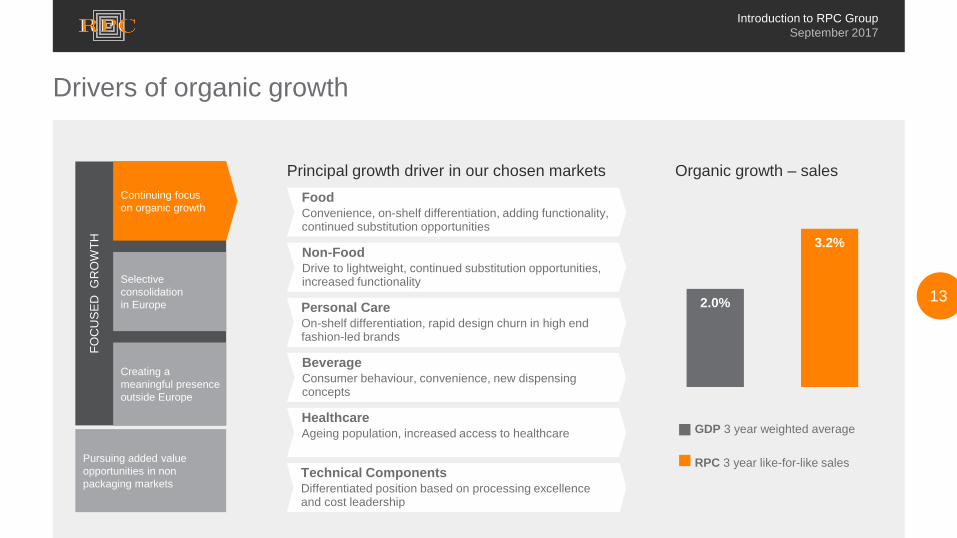

Drivers of organic growthFO

CU

SED

GR

OW

TH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

Organic growth – sales

GDP 3 year weighted average

RPC 3 year like-for-like sales

Non-FoodDrive to lightweight, continued substitution opportunities, increased functionality

Personal CareOn-shelf differentiation, rapid design churn in high end fashion-led brands

BeverageConsumer behaviour, convenience, new dispensing concepts

HealthcareAgeing population, increased access to healthcare

Technical ComponentsDifferentiated position based on processing excellence and cost leadership

FoodConvenience, on-shelf differentiation, adding functionality, continued substitution opportunities

Principal growth driver in our chosen markets

2.0%

3.2%

Introduction to RPC GroupSeptember 2017

114

Leveraging our key strengths

Strong market positionsin selected segments

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Driven byindustry leading

management teamsProcess and operational excellencein addition to cost leadership– conversion cost and polymer buying

Leading design and innovation capabilitiesacross all conversion technologies

Blue chip customer basePursuing added value opportunities in nonpackaging markets

Introduction to RPC GroupSeptember 2017

115

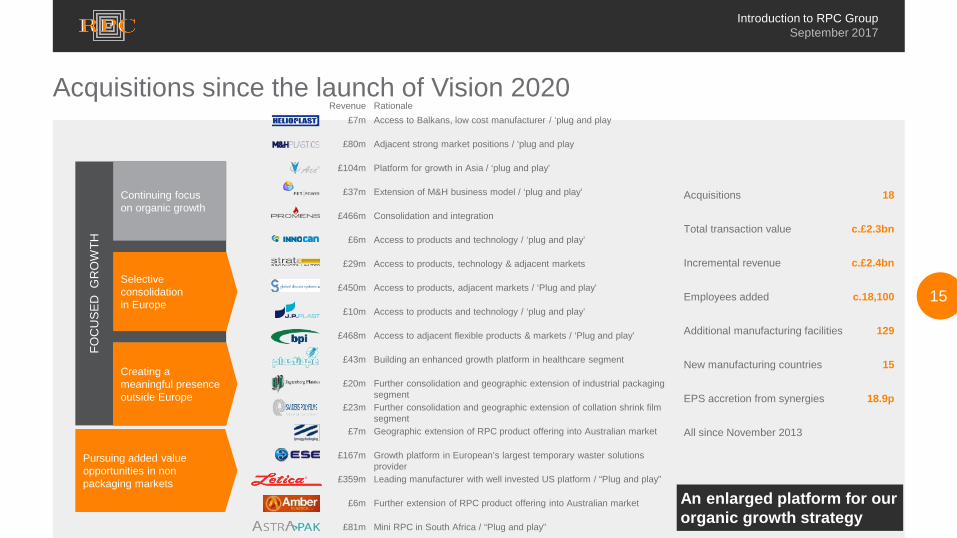

Revenue Rationale£7m Access to Balkans, low cost manufacturer / ‘plug and play

£80m Adjacent strong market positions / ‘plug and play

£104m Platform for growth in Asia / ‘plug and play’

£37m Extension of M&H business model / ‘plug and play’

£466m Consolidation and integration

£6m Access to products and technology / ‘plug and play’

£29m Access to products, technology & adjacent markets

£450m Access to products, adjacent markets / ‘Plug and play’

£10m Access to products and technology / ‘plug and play’

£468m Access to adjacent flexible products & markets / ‘Plug and play’

£43m Building an enhanced growth platform in healthcare segment

£20m Further consolidation and geographic extension of industrial packaging segment

£23m Further consolidation and geographic extension of collation shrink film segment

£7m Geographic extension of RPC product offering into Australian market

£167m Growth platform in European’s largest temporary waster solutions provider

£359m Leading manufacturer with well invested US platform / “Plug and play”

£6m Further extension of RPC product offering into Australian market

£81m Mini RPC in South Africa / “Plug and play”

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

An enlarged platform for ourorganic growth strategy

Acquisitions since the launch of Vision 2020

Creating a meaningful presence outside Europe

Pursuing added value opportunities in nonpackaging markets

Acquisitions 18

Total transaction value c.£2.3bn

Incremental revenue c.£2.4bn

Employees added c.18,100

Additional manufacturing facilities 129

New manufacturing countries 15

EPS accretion from synergies 18.9p

All since November 2013

Introduction to RPC GroupSeptember 2017

116

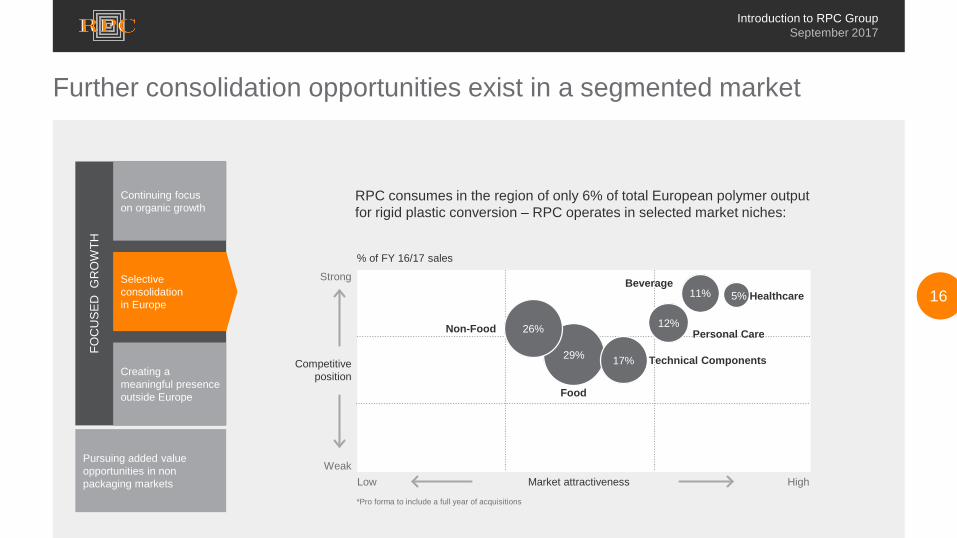

29%

26% 12%

11% 5%

17%

HighLow Market attractiveness

Competitiveposition

Weak

Strong

% of FY 16/17 sales

Further consolidation opportunities exist in a segmented market

RPC consumes in the region of only 6% of total European polymer output for rigid plastic conversion – RPC operates in selected market niches:

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

Food

Non-Food Personal Care

BeverageHealthcare

Technical Components

*Pro forma to include a full year of acquisitions

Introduction to RPC GroupSeptember 2017

117

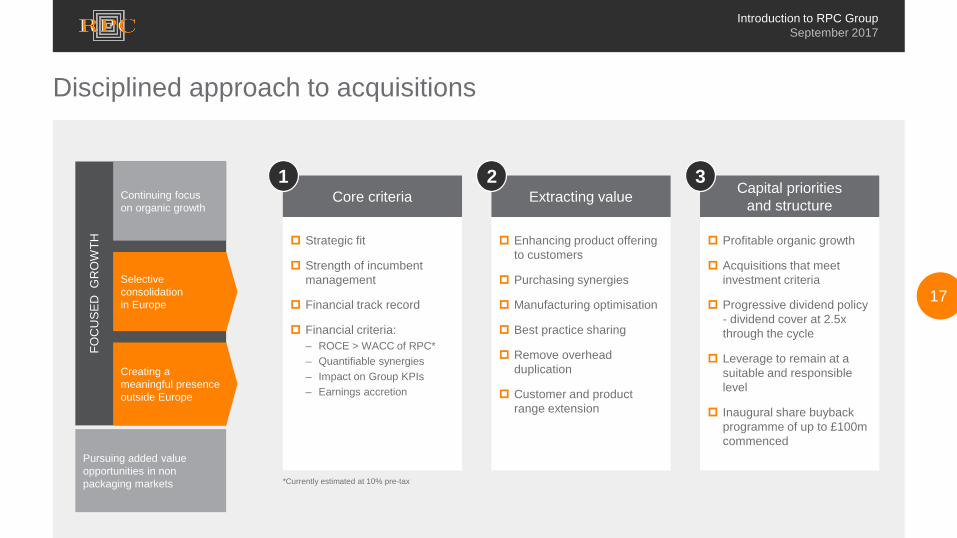

Disciplined approach to acquisitions

Enhancing product offering to customers

Purchasing synergies

Manufacturing optimisation

Best practice sharing

Remove overhead duplication

Customer and product range extension

Profitable organic growth

Acquisitions that meet investment criteria

Progressive dividend policy - dividend cover at 2.5x through the cycle

Leverage to remain at a suitable and responsible level

Inaugural share buyback programme of up to £100m commenced

*Currently estimated at 10% pre-tax

Strategic fit

Strength of incumbent management

Financial track record

Financial criteria:– ROCE > WACC of RPC*– Quantifiable synergies– Impact on Group KPIs– Earnings accretion

Capital prioritiesand structure

3Extracting valueCore criteria

21

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

Introduction to RPC GroupSeptember 2017

118

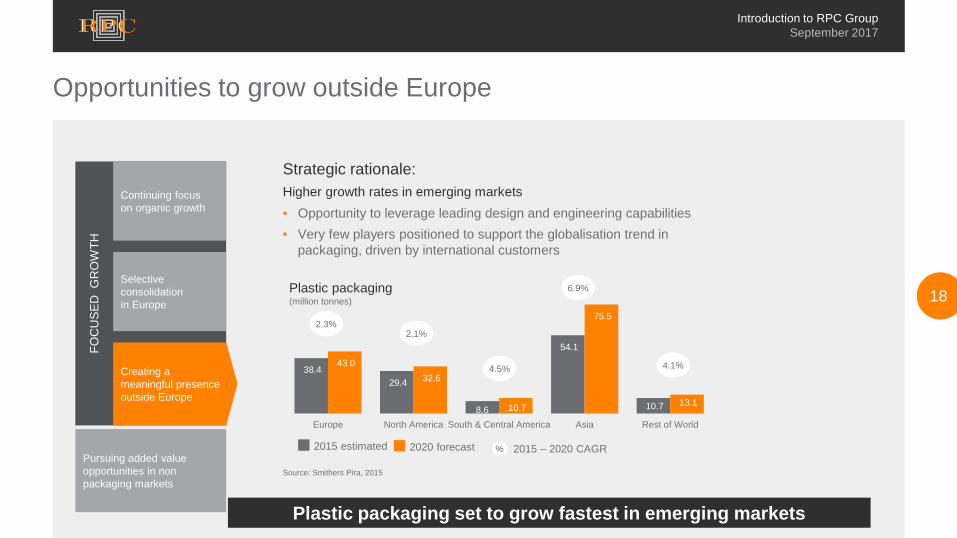

38.4 29.4

8.6

54.1

10.7

43.0 32.6

10.7

75.5

13.1

Europe North America South & Central America Asia Rest of World

Opportunities to grow outside Europe

Strategic rationale:Higher growth rates in emerging markets

Plastic packaging set to grow fastest in emerging markets

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

Source: Smithers Pira, 2015

• Opportunity to leverage leading design and engineering capabilities• Very few players positioned to support the globalisation trend in

packaging, driven by international customers

Plastic packaging(million tonnes)

2015 estimated 2020 forecast % 2015 – 2020 CAGR

2.3%2.1%

4.5%

6.9%

4.1%

Introduction to RPC GroupSeptember 2017

119

Approach to growth outside Europe

• Follow our customers globally utilising design and engineering capabilities

FOC

USE

D G

RO

WTH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Pursuing added value opportunities in nonpackaging markets

• Looking for solid platforms or greenfield where appropriate

• Continued investment in existing operations

• Export processing excellence across enlarged footprint

Introduction to RPC GroupSeptember 2017

120

Moulds£67m11 sites

Roto moulding£120m10 sites

Speciality vehicles£92m3 sites

Asian precision engineering platform£109m5 sites

Extracting value from core competences

Industry leading engineering capabilities

Strategy:

Continue to build world class mould making capacity for internal and external customers

Build on leading European position and leverage branded products worldwide

Continue to create value in selective niches

Focus on growing high added value co-engineered products, packaging and non-packaging

Industry leading technical capabilities

Leading position in Europe, scale in polymer purchasing

Design and engineering excellence, scale in polymer purchasingFO

CU

SED

GR

OW

TH

Selective consolidationin Europe

Creating a meaningful presence outside Europe

Continuing focuson organic growth

Key source ofcompetitive advantage:

Technical Components

RPC Sales*2016/1717%

*Pro forma to include a full year of acquisitions

Pursuing added value opportunities in nonpackaging markets

Temporary waste solutions£173m3 sites

Largest “pure play” temporary waste storage provider in Europe

Build on leading European position and brands

Flexible construction products£53m4 sites

Market leader in water proofing and other construction materials

Build on leading market position and brands

Introduction to RPC GroupSeptember 2017

121

Pursuing added value opportunities in non-packaging marketsRPC can leverage its core competences of design and engineering of plastic products together with a competitive buying position of the main raw materials used, in a number of selected non-packaging markets. World class in-house mould-making allows RPC to deliver technically challenging projects for its customers

Summary Vision 2020 strategy

Selective consolidation in EuropeWith a limited number of consolidators, further acquisition opportunities exist in a segmented market place. RPC continues to seek opportunities that either enhance and strengthen its presence in existing markets or represent attractive complementary markets

Creating a meaningful presence outside Europe Packaging markets outside Europe are forecast to grow faster with multi-national customers indicating an increasing demand for RPC’s leading design and engineering capabilities

Continuing focus on organic growthPlastic continues to advance at the expense of competing materials. Innovative solutions built on excellence in design and engineering, positions RPC for above GDP organic growth

3 year weighted average GDP 3 year RPC like-for-like sales

38.4 29.4

8.6

54.1

10.7

43.0 32.6

10.7

75.5

13.1

Europe North America South & Central America Asia Rest of World

Plastic packaging(million tonnes)

6%RPC’s consumption of total Western European polymer output for rigid plastic packaging

Moulds 11%Roto moulding 20%Speciality vehicles 15%Asian precision engineering platform 18%Temporary waste solutions 28%Flexible construction products 8%

2015 estimated 2020 forecast % 2015 – 2020 CAGR

2.3%2.1%

4.5%

6.9%

4.1%

£614m*Technical

Components

*Pro forma to include a full year of acquisitions

2.0%

3.2%

Introduction to RPC GroupSeptember 2017

122

Why RPC GroupLeading design and engineering business in a growing and globalising market

• Strong market shares in chosen product market segments

• Cost leadership in both conversion cost and raw material buying

Creating value through consolidating fragmented market in Europe

• Leading industry consolidator in a highly segmented market

• Strong track record of delivery

• Strict acquisition criteria in placeAcquisitions

Total transaction value

Incremental revenue

Employees added

18

c.£2.3n

c.£2.4bn

c. 18,100

129

15

18.9p

Additional manufacturing facilities

New manufacturing countries

EPS accretion from synergies

All since November 2013Where we manufactureWhere we sell

Organic growth opportunities• Innovation, design and engineering capabilities across all

plastic conversion technologies

• Increasing demand for higher added value products in fast growing emerging markets

Attractive dividend streams• Progressive dividend policy since flotation in 1993

• Dividend cover targeted at 2.5x earnings through the cycle

Introduction to RPC GroupSeptember 2017

123Back up

Introduction to RPC GroupSeptember 2017

124

The plastic packaging market

MetalRigid

Plastic

Flexible

Glass

Paper

EuropeValue: $839bnCAGR: 3.5%

2015-20

Global Packaging Market(1)

PlasticsPackaging Market(2)

Source: Smithers Pira(1) 2015 - Global packaging market, materials, by value(2) 2015 - Global packaging market, materials & regions, by value

Introduction to RPC GroupSeptember 2017

125

Conversion processes

Our competitors tend to specialise in only one technology. Thanks to our strategic acquisitions over the years we have expertise, R&D and production facilities, that allows RPC to offer the widest range of options to customers.

ThermoformingBlow mouldingInjection moulding

High volumeLow cost

Barrier applications

Re-closableNarrow neck

Pourable

Complex designsHigh level decoration

High added value

Rotational moulding Blown film extrusion

Multilayer co-extruded filmsFilm, tube & sheet productsPlain, printed or converted

Extremely versatileLow tooling costsSmaller volumes

Introduction to RPC GroupSeptember 2017

126

Award winning design and innovation

UK Packaging

Awards

ScanStarAwards

Winner2016

FPA Awards

WinnerProcessor of the Year 2014Training and Development

Programme of the Year 2014Apprentice of the Year 2015

Plastic Industry Awards

Continue to focus on organic growth built on innovationOver 50 award winners and finalists since 2012

Winner & Finalist2016

PLC Awards

Winner2015

World Food Innovation

Awards

Winner2015

WorldStarAwards

Winner2014, 2015 & 2016

Winner2013, 2014, 2015

& 2016

WinnerCompany of the Year

2014 & 2015 Product Categories: Winners & Finalists

2013, 2014, 2015 & 2016

WinnerCompany of the Year

2015

Hong Kong Innovative

Technologies & Manufacturing

UK Stock Market Awards

WinnerBest Industrial Goods, Services

& Automobiles PLC2016

Norwegian Award for

Design Excellence

Introduction to RPC GroupSeptember 2017

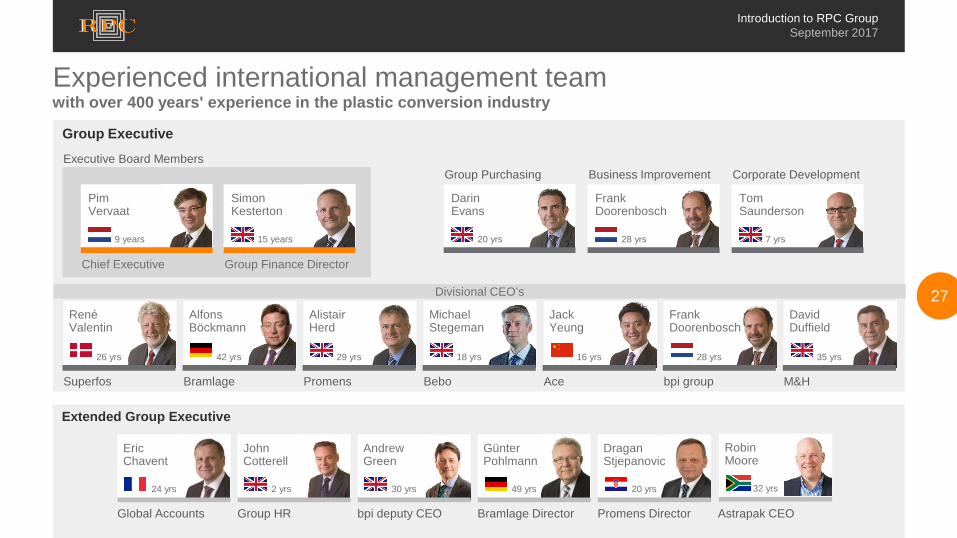

127Divisional CEO’s

Chief Executive

Executive Board Members

Group Finance Director

Group Purchasing Business Improvement Corporate Development

Superfos Bramlage Promens Bebo Ace

Pim Vervaat

Simon Kesterton

9 years 15 years

Darin Evans

Frank Doorenbosch

Tom Saunderson

7 yrs28 yrs20 yrs

Group Executive

Extended Group Executive

bpi group

Frank Doorenbosch

RenéValentin

Alfons Böckmann

Alistair Herd

Michael Stegeman

JackYeung

David Duffield

26 yrs 29 yrs 16 yrs42 yrs 18 yrs 28 yrs 35 yrs

M&H

Eric Chavent

John Cotterell

Andrew Green

Günter Pohlmann

Dragan Stjepanovic

24 yrs 2 yrs 30 yrs 49 yrs 20 yrs

Global Accounts Group HR bpi deputy CEO Bramlage Director Promens Director

Experienced international management teamwith over 400 years' experience in the plastic conversion industry

RobinMoore

32 yrs

Astrapak CEO

Introduction to RPC GroupSeptember 2017

128

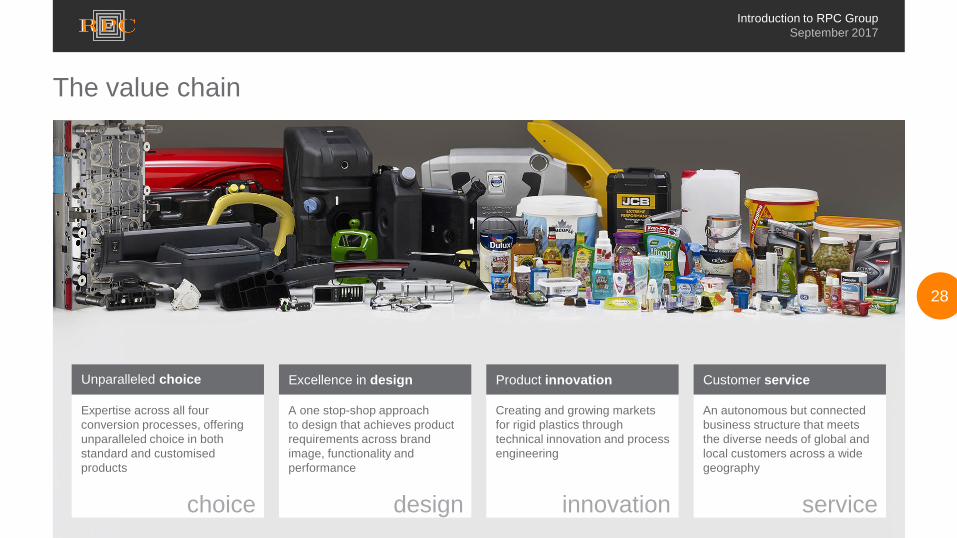

The value chain

Expertise across all four conversion processes, offering unparalleled choice in both standard and customised products

A one stop-shop approach to design that achieves product requirements across brand image, functionality and performance

Creating and growing markets for rigid plastics through technical innovation and process engineering

An autonomous but connected business structure that meets the diverse needs of global and local customers across a wide geography

Unparalleled choice Excellence in design Product innovation Customer service

choice design innovation service

Introduction to RPC GroupSeptember 2017

129Forward looking statements

This presentation contains forward-looking statements, which:have been made by the directors in good faith based on the information available to them up to the time of their approval of this presentation; and should be treated with caution due to the inherent uncertainties, including both economic and business risk factors, underlying such forward-looking information.The Group undertakes no obligation to update these forward-looking statements and nothing in this presentation should be construed as a profit forecast.