Introduction to Islamic Finance Finance Conference: Near ... Ross... · CIC PB SGP. Coutts PB SG....

28

HSBC Amanah Debt Capital Markets Introduction to Islamic Finance Finance Conference: Near & Middle East 28 April 2010 Best International Islamic Bank 2010 Best Sukuk House 2010 Best Global Bank “HSBC has adopted a clear policy of focusing expansion on emerging markets, and on the international connectivity of those markets with the developed world. It is a truly global bank.” 2009 Best Global Debt House “The crisis showed up which banks the markets thought were safest - and HSBC came out firmly on top.” 2009

Transcript of Introduction to Islamic Finance Finance Conference: Near ... Ross... · CIC PB SGP. Coutts PB SG....

HSBC Amanah Debt Capital Markets

Introduction to Islamic FinanceFinance Conference: Near & Middle East

28 April 2010

Best International Islamic Bank

2010

Best Sukuk House

2010

Best Global Bank

“HSBC has adopted a clear policy of focusing expansion on emerging markets, and on the international connectivity of those markets with the developed world. It is a truly global bank.”2009

Best Global Debt House

“The crisis showed up which banks the markets thought were safest - and HSBC came out firmly on top.”

2009

2

Contents

Why Sukuk?

Sukuk Overview

How to Structure a Sukuk – What to Consider?

HSBC Amanah Credentials

Section 1

Section 2

Section 3

Section 4

I

Why Sukuk?

4

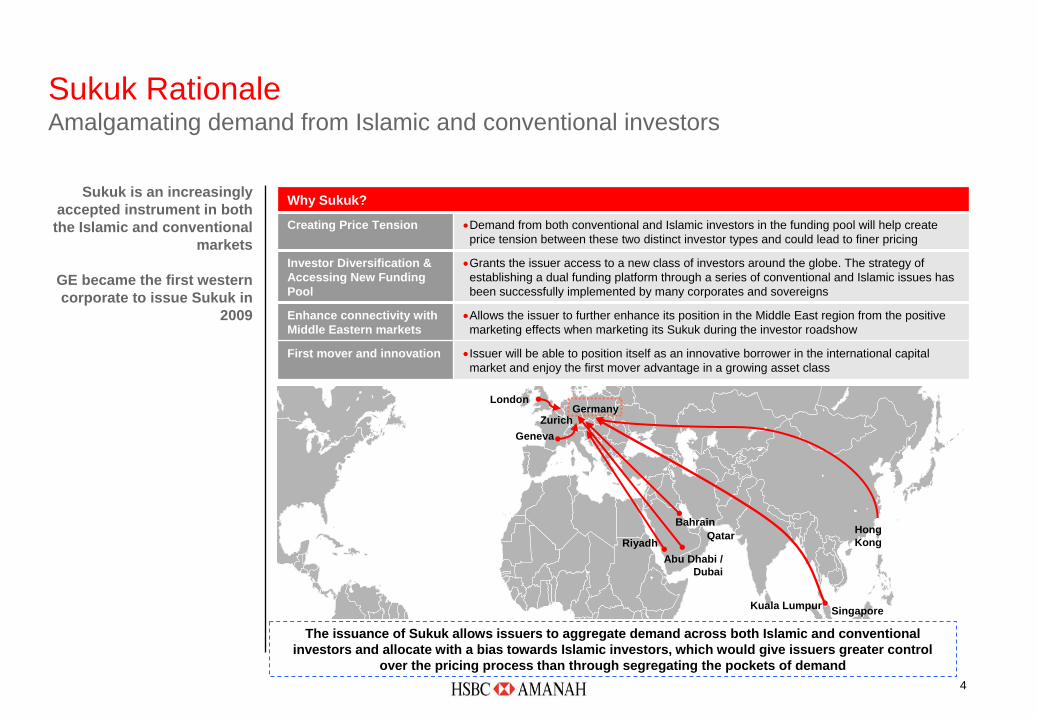

Sukuk Rationale Amalgamating demand from Islamic and conventional investors

Why Sukuk?

Creating Price Tension •Demand from both conventional and Islamic investors in the funding pool will help create price tension between these two distinct investor types and could lead to finer pricing

Investor Diversification & Accessing New Funding Pool

•Grants the issuer access to a new class of investors around the globe. The strategy of establishing a dual funding platform through a series of conventional and Islamic issues has been successfully implemented by many corporates and sovereigns

Enhance connectivity with Middle Eastern markets

•Allows the issuer to further enhance its position in the Middle East region from the positive marketing effects when marketing its Sukuk during the investor roadshow

First mover and innovation •Issuer will be able to position itself as an innovative borrower in the international capital market and enjoy the first mover advantage in a growing asset class

The issuance of Sukuk allows issuers to aggregate demand across both Islamic and conventional investors and allocate with a bias towards Islamic investors, which would give issuers greater control

over the pricing process than through segregating the pockets of demand

London

Geneva

RiyadhAbu Dhabi /

Dubai

Bahrain

Singapore

Hong Kong

GermanyZurich

Qatar

Kuala Lumpur

Sukuk is an increasingly accepted instrument in both

the Islamic and conventional markets

GE became the first western corporate to issue Sukuk in

2009

5

2010 TrendsInvestors

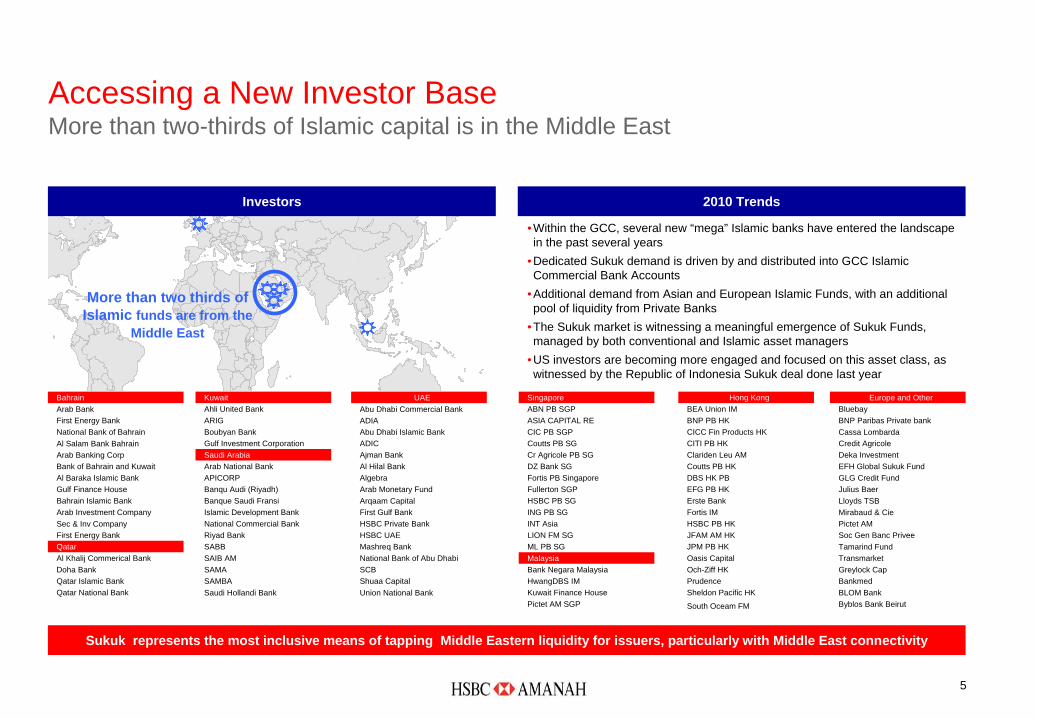

More than two thirds of Islamic funds are from the

Middle East

• Within the GCC, several new “mega” Islamic banks have entered the landscape in the past several years

• Dedicated Sukuk demand is driven by and distributed into GCC Islamic Commercial Bank Accounts

• Additional demand from Asian and European Islamic Funds, with an additional pool of liquidity from Private Banks

• The Sukuk market is witnessing a meaningful emergence of Sukuk Funds, managed by both conventional and Islamic asset managers

• US investors are becoming more engaged and focused on this asset class, as witnessed by the Republic of Indonesia Sukuk deal done last year

Sukuk represents the most inclusive means of tapping Middle Eastern liquidity for issuers, particularly with Middle East connectivity

BahrainArab BankFirst Energy BankNational Bank of BahrainAl Salam Bank BahrainArab Banking CorpBank of Bahrain and KuwaitAl Baraka Islamic BankGulf Finance HouseBahrain Islamic BankArab Investment CompanySec & Inv CompanyFirst Energy BankQatarAl Khalij Commerical BankDoha BankQatar Islamic BankQatar National Bank

KuwaitAhli United BankARIGBoubyan BankGulf Investment CorporationSaudi ArabiaArab National BankAPICORPBanqu Audi (Riyadh)Banque Saudi FransiIslamic Development BankNational Commercial BankRiyad BankSABBSAIB AMSAMASAMBASaudi Hollandi Bank

UAEAbu Dhabi Commercial BankADIAAbu Dhabi Islamic BankADICAjman BankAl Hilal BankAlgebraArab Monetary FundArqaam CapitalFirst Gulf BankHSBC Private BankHSBC UAEMashreq BankNational Bank of Abu DhabiSCBShuaa Capital Union National Bank

SingaporeABN PB SGPASIA CAPITAL RECIC PB SGPCoutts PB SGCr Agricole PB SGDZ Bank SGFortis PB SingaporeFullerton SGPHSBC PB SGING PB SGINT AsiaLION FM SGML PB SGMalaysiaBank Negara MalaysiaHwangDBS IMKuwait Finance HousePictet AM SGP

Hong KongBEA Union IMBNP PB HKCICC Fin Products HKCITI PB HKClariden Leu AMCoutts PB HKDBS HK PBEFG PB HKErste BankFortis IMHSBC PB HKJFAM AM HKJPM PB HKOasis CapitalOch-Ziff HKPrudenceSheldon Pacific HK

South Oceam FM

Europe and OtherBluebayBNP Paribas Private bankCassa LombardaCredit AgricoleDeka InvestmentEFH Global Sukuk FundGLG Credit FundJulius BaerLloyds TSBMirabaud & CiePictet AMSoc Gen Banc PriveeTamarind FundTransmarketGreylock CapBankmedBLOM Bank Byblos Bank Beirut

Accessing a New Investor Base More than two-thirds of Islamic capital is in the Middle East

6

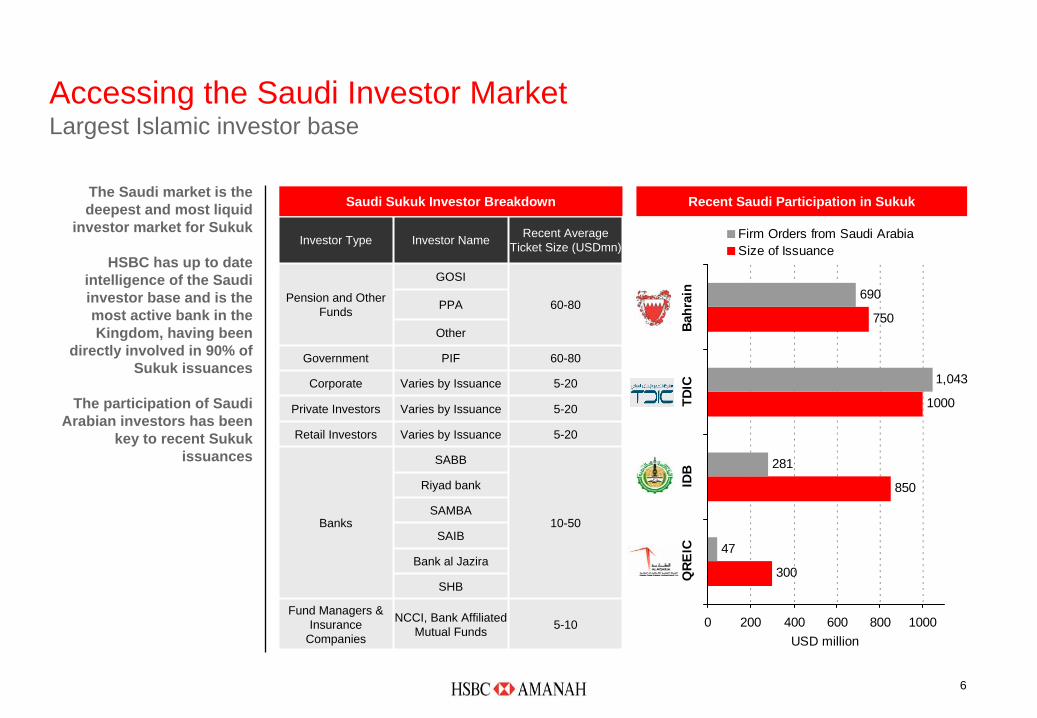

Investor Type Investor Name Recent Average Ticket Size (USDmn)

Pension and Other Funds

GOSI

60-80PPA

Other

Government PIF 60-80

Corporate Varies by Issuance 5-20

Private Investors Varies by Issuance 5-20

Retail Investors Varies by Issuance 5-20

Banks

SABB

10-50

Riyad bank

SAMBA

SAIB

Bank al Jazira

SHB

Fund Managers & Insurance

Companies

NCCI, Bank Affiliated Mutual Funds 5-10

Saudi Sukuk Investor Breakdown Recent Saudi Participation in Sukuk

300

850

1000

750

47

281

1,043

690

0 200 400 600 800 1000

QRE

ICID

BTD

ICBa

hrai

n

USD million

Firm Orders from Saudi ArabiaSize of Issuance

Accessing the Saudi Investor Market Largest Islamic investor base

The Saudi market is the deepest and most liquid

investor market for Sukuk

HSBC has up to date intelligence of the Saudi investor base and is the most active bank in the Kingdom, having been

directly involved in 90% of Sukuk issuances

The participation of Saudi Arabian investors has been

key to recent Sukuk issuances

7

Fund Name GeofocusEFH Global Sukuk Plus Fund (Qatar

Islamic)Global

Fund Name GeofocusSanad Investment Co. Ltd GCC

Fund Name GeofocusIIAB Sukuk & Murabaha MENA Fund GCC

Fund Name GeofocusFalcom Sukuk Fund GCC

Jadwa Global Sukuk Fund Global

Fund Name GeofocusNoor Financial GCC

Fund Name GeofocusAlgebra Sukuk Fund GCCAl Hilal Sukuk Fund GCC

Fund Name GeofocusADCB Sukuk Fund Global

Emirates Sukuk Fund No.1 Limited

MENA

Emirates International Discretionary Portfolios

MENA

EFG Sukuk Fund GlobalENBD Sukuk Fund Global

Mashreq Sukuk Fund GlobalNational Bonds Corp. UAE

Fund Name GeofocusAIMAN Cash Fund (formerly HWANGDBS

Islamic Cash Fund)Malaysia

AmAl-amin MalaysiaAMB Dana Arif MalaysiaAmBon Islam Malaysia

ARMB Syariah Trust MalaysiaCIMB Islamic Sukuk Fund (formerly SBB

Dana Al-Hafiz)Malaysia

HWANGDBS Investment Management Bhd

Malaysia

ING Bon Islam MalaysiaMAAKL As-Saad Malaysia

PB Islamic Bond Fund MalaysiaPRUdana al-islah Malaysia

PRUdana Wafi MalaysiaPublic Islamic Bond Fund Global

Public Islamic Enhanced Bond Fund Asia PacificPublic Islamic Select Bond Fund Global

TA Dana Fokus Malaysia

Fund Name GeofocusUnited Islamic Income Fund

(UIIF)Global

Fund Name GeofocusGlobal Sukuk Plus Fund Global

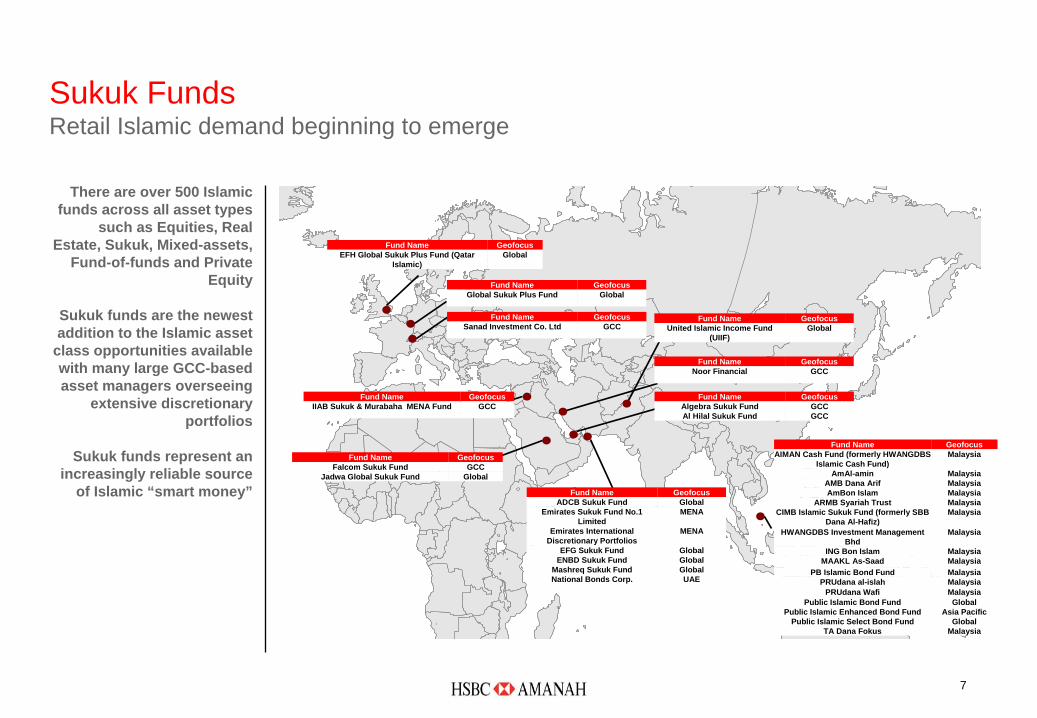

Sukuk Funds Retail Islamic demand beginning to emerge

There are over 500 Islamic funds across all asset types

such as Equities, Real Estate, Sukuk, Mixed-assets,

Fund-of-funds and Private Equity

Sukuk funds are the newest addition to the Islamic asset

class opportunities available with many large GCC-based asset managers overseeing

extensive discretionary portfolios

Sukuk funds represent an increasingly reliable source

of Islamic “smart money”

8

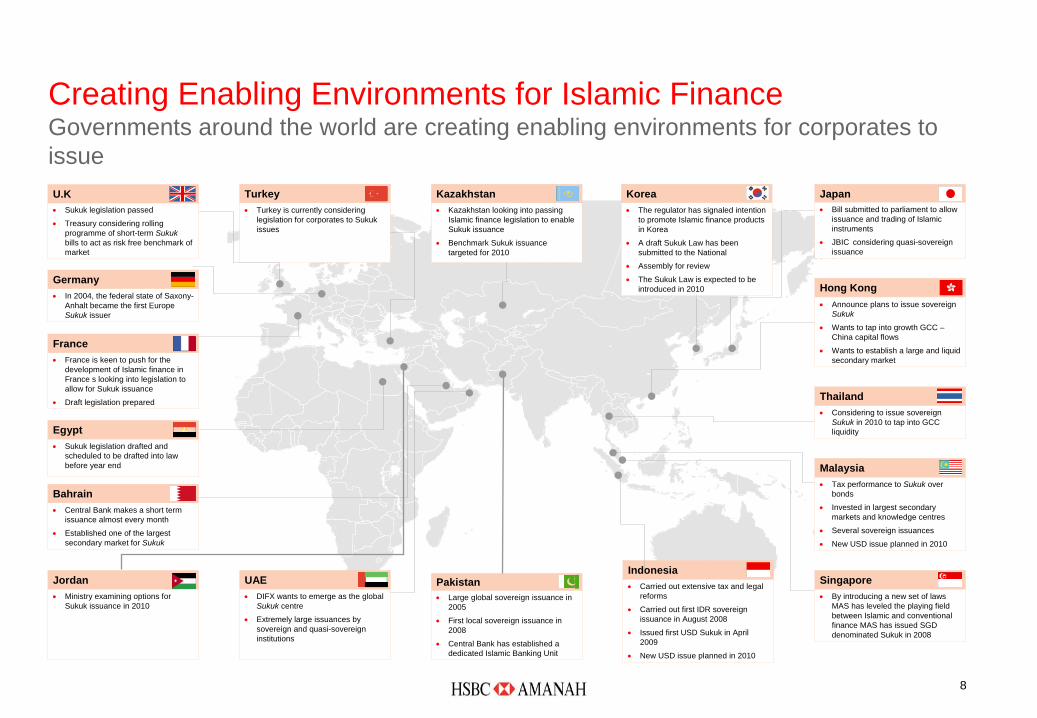

•

Large global sovereign issuance in 2005

•

First local sovereign issuance in 2008

•

Central Bank has established a dedicated Islamic Banking Unit

Pakistan

•

Considering to issue sovereign Sukuk in 2010 to tap into GCC liquidity

Thailand

•

Announce plans to issue sovereign Sukuk

•

Wants to tap into growth GCC – China capital flows

•

Wants to establish a large and liquid secondary market

Hong Kong

•

Carried out extensive tax and legal reforms

•

Carried out first IDR sovereign issuance in August 2008

•

Issued first USD Sukuk in April 2009

•

New USD issue planned in 2010

Indonesia

Japan•

Bill submitted to parliament to allow issuance and trading of Islamic instruments

•

JBIC considering quasi-sovereign issuance

Korea•

The regulator has signaled intention to promote Islamic finance products in Korea

•

A draft Sukuk Law has been submitted to the National

•

Assembly for review

•

The Sukuk Law is expected to be introduced in 2010

•

Turkey is currently considering legislation for corporates to Sukuk issues

Turkey•

Kazakhstan looking into passing Islamic finance legislation to enable Sukuk issuance

•

Benchmark Sukuk issuance targeted for 2010

Kazakhstan

•

By introducing a new set of laws MAS has leveled the playing field between Islamic and conventional finance MAS has issued SGD denominated Sukuk in 2008

Singapore

•

Tax performance to Sukuk over bonds

•

Invested in largest secondary markets and knowledge centres

•

Several sovereign issuances

•

New USD issue planned in 2010

Malaysia

•

DIFX wants to emerge as the global Sukuk centre

•

Extremely large issuances by sovereign and quasi-sovereign institutions

UAE

•

Central Bank makes a short term issuance almost every month

•

Established one of the largest secondary market for Sukuk

Bahrain

•

Sukuk legislation drafted and scheduled to be drafted into law before year end

Egypt

•

France is keen to push for the development of Islamic finance in France s looking into legislation to allow for Sukuk issuance

•

Draft legislation prepared

France

•

Sukuk legislation passed

•

Treasury considering rolling programme of short-term Sukuk bills to act as risk free benchmark of market

U.K

•

In 2004, the federal state of Saxony- Anhalt became the first Europe Sukuk issuer

Germany

Creating Enabling Environments for Islamic Finance Governments around the world are creating enabling environments for corporates to issue

•

Ministry examining options for Sukuk issuance in 2010

Jordan

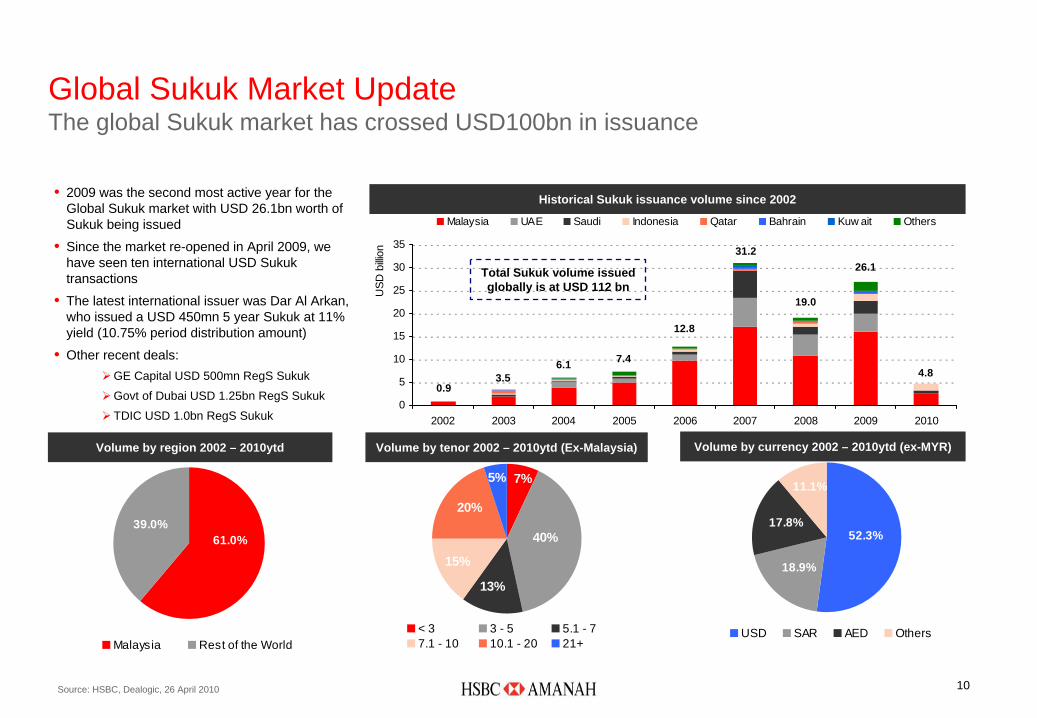

Sukuk Market Update

10

0

5

10

15

20

25

30

35

2002 2003 2004 2005 2006 2007 2008 2009 2010

USD

billi

on

Malaysia UAE Saudi Indonesia Qatar Bahrain Kuw ait Others

Historical Sukuk issuance volume since 2002

Volume by currency 2002 – 2010ytd (ex-MYR)

5% 7%

40%

13%

15%

20%

< 3 3 - 5 5.1 - 77.1 - 10 10.1 - 20 21+

61.0%39.0%

Malaysia Rest of the World

11.1%

18.9%

17.8%52.3%

USD SAR AED Others

Volume by tenor 2002 – 2010ytd (Ex-Malaysia)Volume by region 2002 – 2010ytd

0.93.5

6.1 7.4

12.8

31.2

19.0

26.1

Source: HSBC, Dealogic, 26 April 2010

Total Sukuk volume issuedglobally is at USD 112 bn

4.8

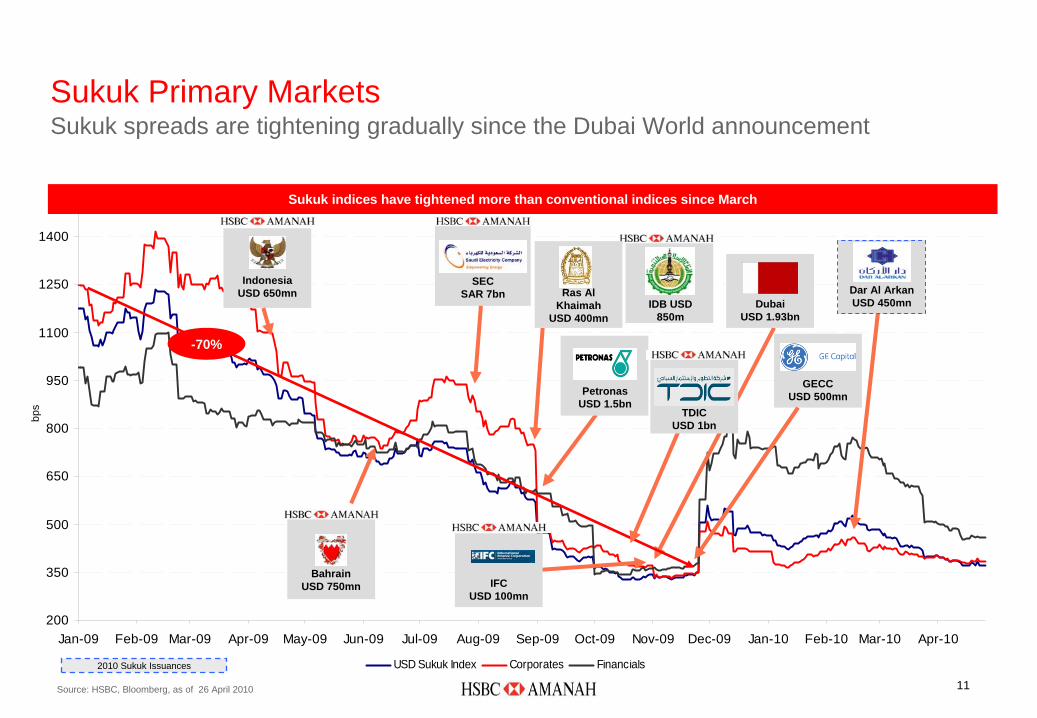

Global Sukuk Market Update The global Sukuk market has crossed USD100bn in issuance

• 2009 was the second most active year for the Global Sukuk market with USD 26.1bn worth of Sukuk being issued

• Since the market re-opened in April 2009, we have seen ten international USD Sukuk transactions

• The latest international issuer was Dar Al Arkan, who issued a USD 450mn 5 year Sukuk at 11% yield (10.75% period distribution amount)

• Other recent deals:GE Capital USD 500mn RegS Sukuk

Govt of Dubai USD 1.25bn RegS Sukuk

TDIC USD 1.0bn RegS Sukuk

11

200

350

500

650

800

950

1100

1250

1400

Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10

Source: HSBC, Bloomberg, as of 26 April 2010

Sukuk Primary Markets Sukuk spreads are tightening gradually since the Dubai World announcement

Sukuk indices have tightened more than conventional indices since March

-70%

Petronas USD 1.5bn

Indonesia USD 650mn

SEC SAR 7bn

IDB USD 850m

2010 Sukuk Issuances

bps

Ras Al Khaimah

USD 400mn

Bahrain USD 750mn

TDIC USD 1bn

DubaiUSD 1.93bn

GECCUSD 500mn

IFCUSD 100mn

USD Sukuk Index Corporates Financials

Dar Al ArkanUSD 450mn

12

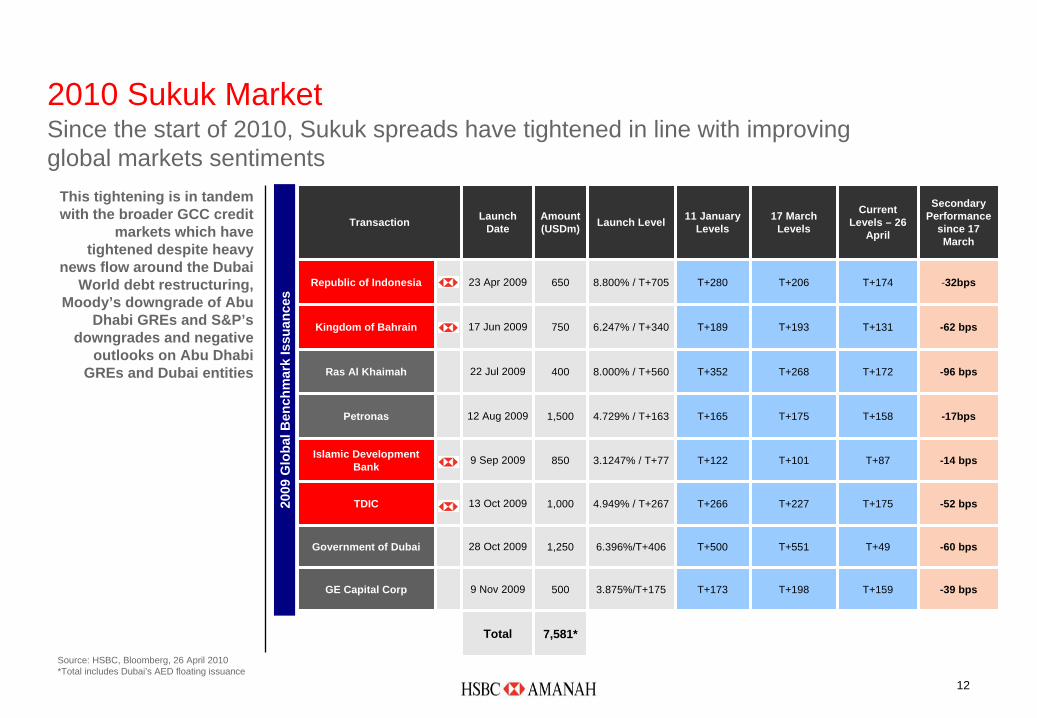

2010 Sukuk Market Since the start of 2010, Sukuk spreads have tightened in line with improving global markets sentiments

Source: HSBC, Bloomberg, 26 April 2010*Total includes Dubai’s AED floating issuance

2009

Glo

bal B

ench

mar

k Is

suan

ces

Transaction Launch Date

Amount (USDm) Launch Level 11 January

Levels17 March

Levels

Current Levels – 26

April

Secondary Performance

since 17 March

Republic of Indonesia 23 Apr 2009 650 8.800% / T+705 T+280 T+206 T+174 -32bps

Kingdom of Bahrain 17 Jun 2009 750 6.247% / T+340 T+189 T+193 T+131 -62 bps

Ras Al Khaimah 22 Jul 2009 400 8.000% / T+560 T+352 T+268 T+172 -96 bps

Petronas 12 Aug 2009 1,500 4.729% / T+163 T+165 T+175 T+158 -17bps

Islamic Development Bank 9 Sep 2009 850 3.1247% / T+77 T+122 T+101 T+87 -14 bps

TDIC 13 Oct 2009 1,000 4.949% / T+267 T+266 T+227 T+175 -52 bps

Government of Dubai 28 Oct 2009 1,250 6.396%/T+406 T+500 T+551 T+49 -60 bps

GE Capital Corp 9 Nov 2009 500 3.875%/T+175 T+173 T+198 T+159 -39 bps

Total 7,581*

This tightening is in tandem with the broader GCC credit

markets which have tightened despite heavy

news flow around the Dubai World debt restructuring,

Moody’s downgrade of Abu Dhabi GREs and S&P’s

downgrades and negative outlooks on Abu Dhabi

GREs and Dubai entities

13

20%

20%

60%

21%

17%

48%14%

Bre

akdo

wn

by in

vest

ors

Bre

akdo

wn

by g

eogr

aphy

15%

26%

55%

30%

26%34%

10%

40%

11%

30%19%

45%

14%

37%4%

30%

35% 35%

34%

21%

40%5%

TDIC (RegS) Bahrain (RegS) Indonesia (RegS/144a) IDB (RegS)

MENA Asia Europe OtherUSA

Banks Funds Insurance/Private Banks Others

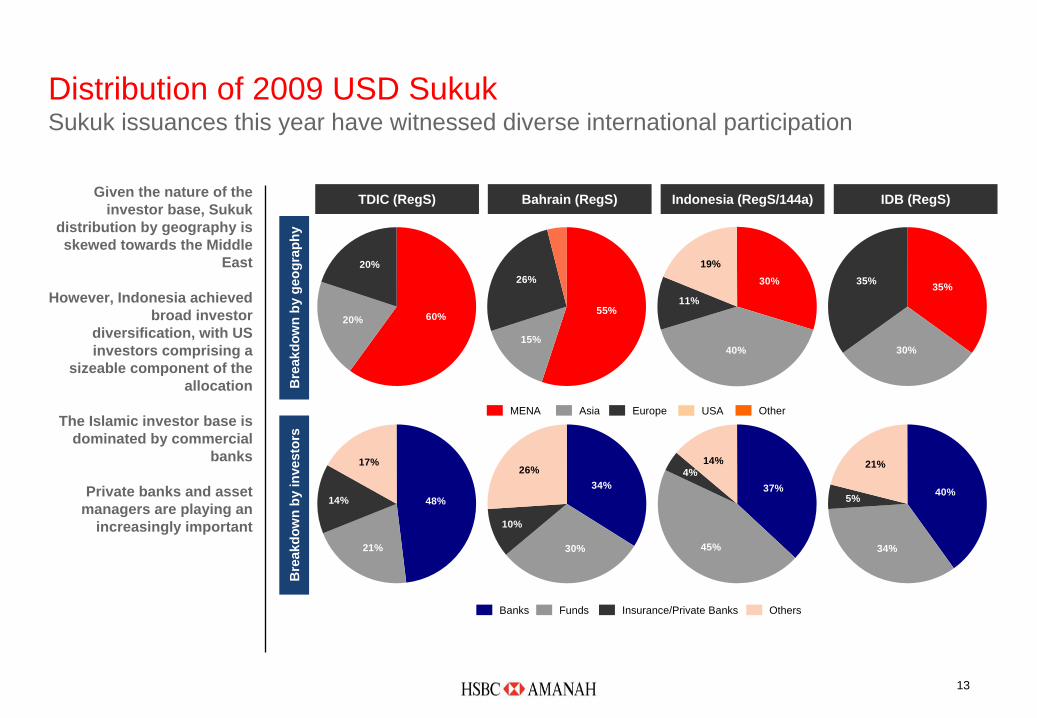

Distribution of 2009 USD Sukuk Sukuk issuances this year have witnessed diverse international participation

Given the nature of the investor base, Sukuk

distribution by geography is skewed towards the Middle

East

However, Indonesia achieved broad investor

diversification, with US investors comprising a

sizeable component of the allocation

The Islamic investor base is dominated by commercial

banks

Private banks and asset managers are playing an

increasingly important

How to Structure a Sukuk – What to Consider?

15

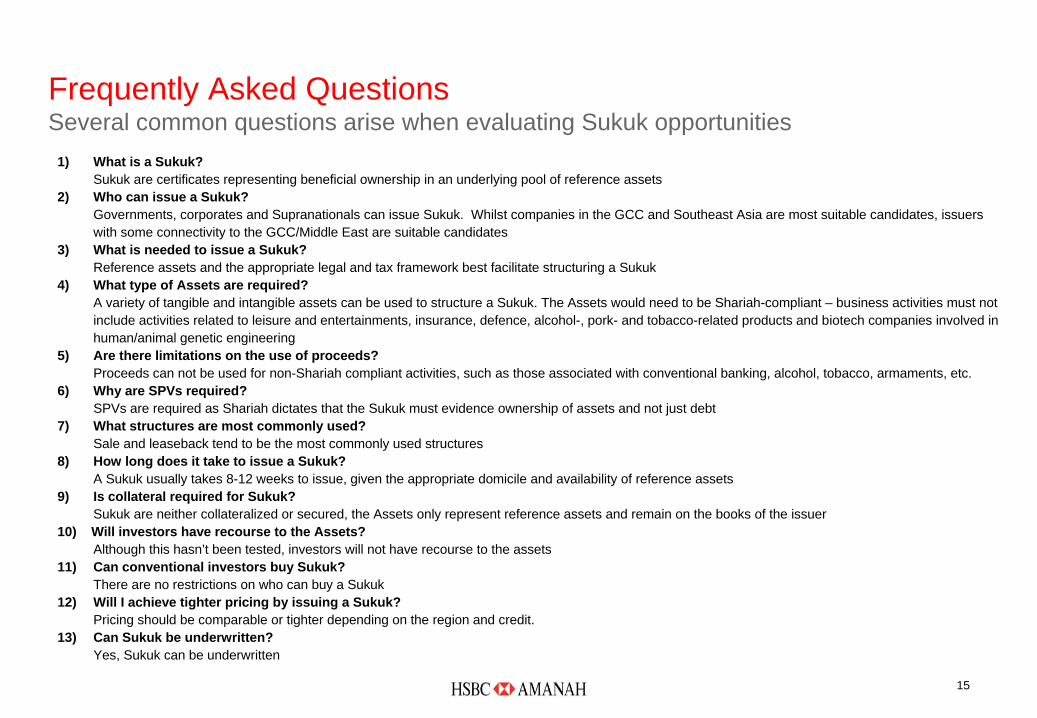

1) What is a Sukuk?Sukuk are certificates representing beneficial ownership in an underlying pool of reference assets

2) Who can issue a Sukuk?Governments, corporates and Supranationals can issue Sukuk. Whilst companies in the GCC and Southeast Asia are most suitable candidates, issuers with some connectivity to the GCC/Middle East are suitable candidates

3) What is needed to issue a Sukuk?Reference assets and the appropriate legal and tax framework best facilitate structuring a Sukuk

4) What type of Assets are required?A variety of tangible and intangible assets can be used to structure a Sukuk. The Assets would need to be Shariah-compliant – business activities must not include activities related to leisure and entertainments, insurance, defence, alcohol-, pork- and tobacco-related products and biotech companies involved in human/animal genetic engineering

5) Are there limitations on the use of proceeds?Proceeds can not be used for non-Shariah compliant activities, such as those associated with conventional banking, alcohol, tobacco, armaments, etc.

6) Why are SPVs required?SPVs are required as Shariah dictates that the Sukuk must evidence ownership of assets and not just debt

7) What structures are most commonly used?Sale and leaseback tend to be the most commonly used structures

8) How long does it take to issue a Sukuk?A Sukuk usually takes 8-12 weeks to issue, given the appropriate domicile and availability of reference assets

9) Is collateral required for Sukuk?Sukuk are neither collateralized or secured, the Assets only represent reference assets and remain on the books of the issuer

10) Will investors have recourse to the Assets?Although this hasn’t been tested, investors will not have recourse to the assets

11) Can conventional investors buy Sukuk?There are no restrictions on who can buy a Sukuk

12) Will I achieve tighter pricing by issuing a Sukuk?Pricing should be comparable or tighter depending on the region and credit.

13) Can Sukuk be underwritten?Yes, Sukuk can be underwritten

Frequently Asked Questions Several common questions arise when evaluating Sukuk opportunities

16

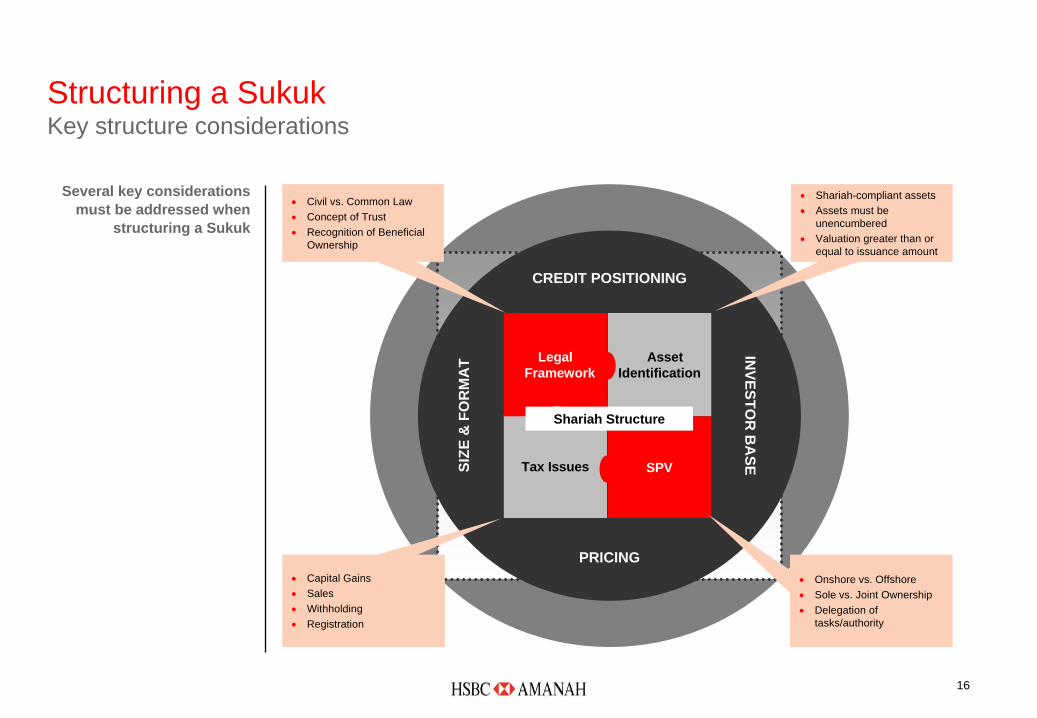

Structuring a Sukuk Key structure considerations

Tax Issues

Asset Identification

Legal Framework

SPV

Shariah Structure

CREDIT POSITIONING

PRICING

SIZE

& F

OR

MA

T

INVESTO

R B

ASE

•

Shariah-compliant assets•

Assets must be unencumbered

•

Valuation greater than or equal to issuance amount

•

Onshore vs. Offshore•

Sole vs. Joint Ownership•

Delegation of tasks/authority

•

Civil vs. Common Law•

Concept of Trust•

Recognition of Beneficial Ownership

•

Capital Gains•

Sales•

Withholding•

Registration

Several key considerations must be addressed when

structuring a Sukuk

17

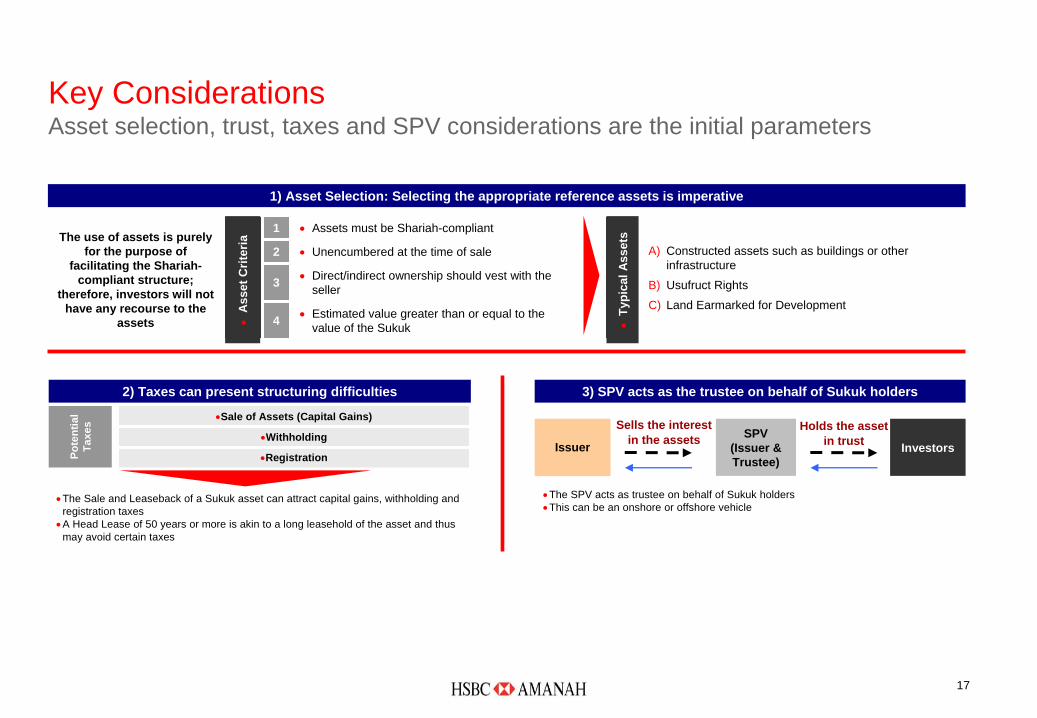

The use of assets is purely for the purpose of

facilitating the Shariah- compliant structure;

therefore, investors will not have any recourse to the

assets

Asset C

riteria

1 •

Assets must be Shariah-compliant Typical Assets

A) Constructed assets such as buildings or other infrastructure

B) Usufruct Rights

C) Land Earmarked for Development

2 •

Unencumbered at the time of sale

3 •

Direct/indirect ownership should vest with the seller

4 •

Estimated value greater than or equal to the value of the Sukuk

1) Asset Selection: Selecting the appropriate reference assets is imperative

•A

sset

Crit

eria

Pote

ntia

l Ta

xes

2) Taxes can present structuring difficulties

•Registration

•Withholding

•Sale of Assets (Capital Gains)

•The Sale and Leaseback of a Sukuk asset can attract capital gains, withholding and registration taxes

•A Head Lease of 50 years or more is akin to a long leasehold of the asset and thus may avoid certain taxes

3) SPV acts as the trustee on behalf of Sukuk holders

SPV(Issuer & Trustee)

Sells the interest in the assets InvestorsIssuer

Holds the asset in trust

•The SPV acts as trustee on behalf of Sukuk holders•This can be an onshore or offshore vehicle

•Ty

pica

l Ass

ets

Key Considerations Asset selection, trust, taxes and SPV considerations are the initial parameters

18

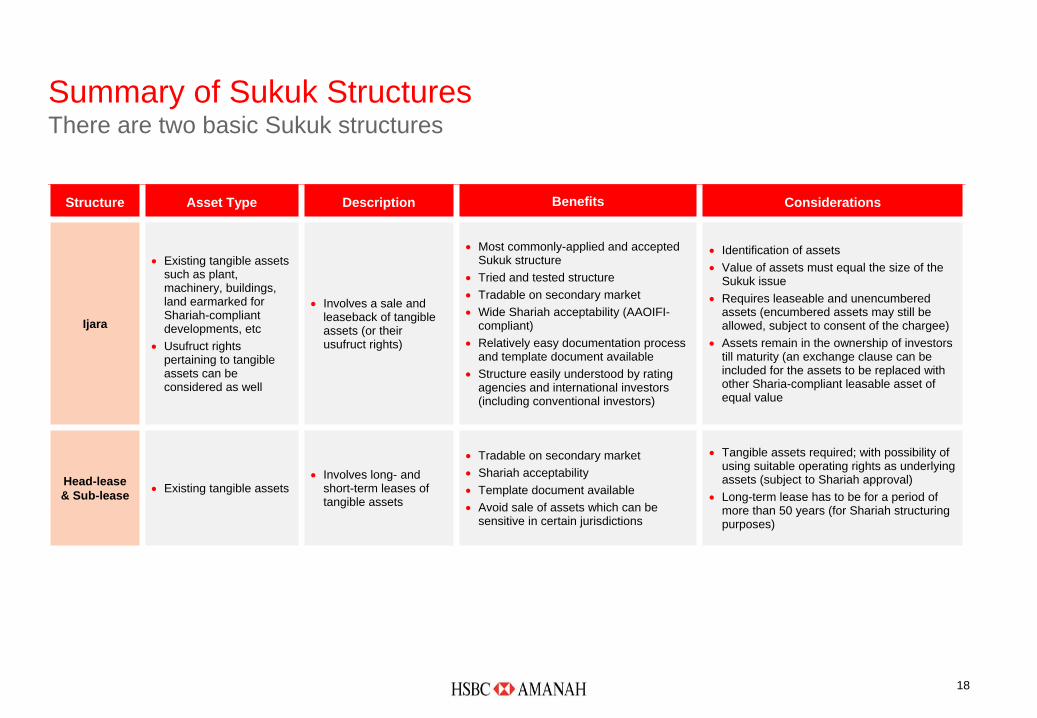

Structure Asset Type Description Benefits Considerations

Ijara

•

Existing tangible assets such as plant, machinery, buildings, land earmarked for Shariah-compliant developments, etc

•

Usufruct rights pertaining to tangible assets can be considered as well

•

Involves a sale and leaseback of tangible assets (or their usufruct rights)

•

Most commonly-applied and accepted Sukuk structure

•

Tried and tested structure•

Tradable on secondary market•

Wide Shariah acceptability (AAOIFI- compliant)

•

Relatively easy documentation process and template document available

•

Structure easily understood by rating agencies and international investors (including conventional investors)

•

Identification of assets•

Value of assets must equal the size of the Sukuk issue

•

Requires leaseable and unencumbered assets (encumbered assets may still be allowed, subject to consent of the chargee)

•

Assets remain in the ownership of investors till maturity (an exchange clause can be included for the assets to be replaced with other Sharia-compliant leasable asset of equal value

Head-lease & Sub-lease •

Existing tangible assets •

Involves long- and short-term leases of tangible assets

•

Tradable on secondary market•

Shariah acceptability•

Template document available•

Avoid sale of assets which can be sensitive in certain jurisdictions

•

Tangible assets required; with possibility of using suitable operating rights as underlying assets (subject to Shariah approval)

•

Long-term lease has to be for a period of more than 50 years (for Shariah structuring purposes)

Summary of Sukuk Structures There are two basic Sukuk structures

19

Funds Transaction

SPV(Issuer)

Transfer of Asset

Sukuk Proceeds

SPV leases asset to Obligor

SPV issues floating or fixed rate Sukuk

I. Initial Cashflow

Sukuk Proceeds

Investors

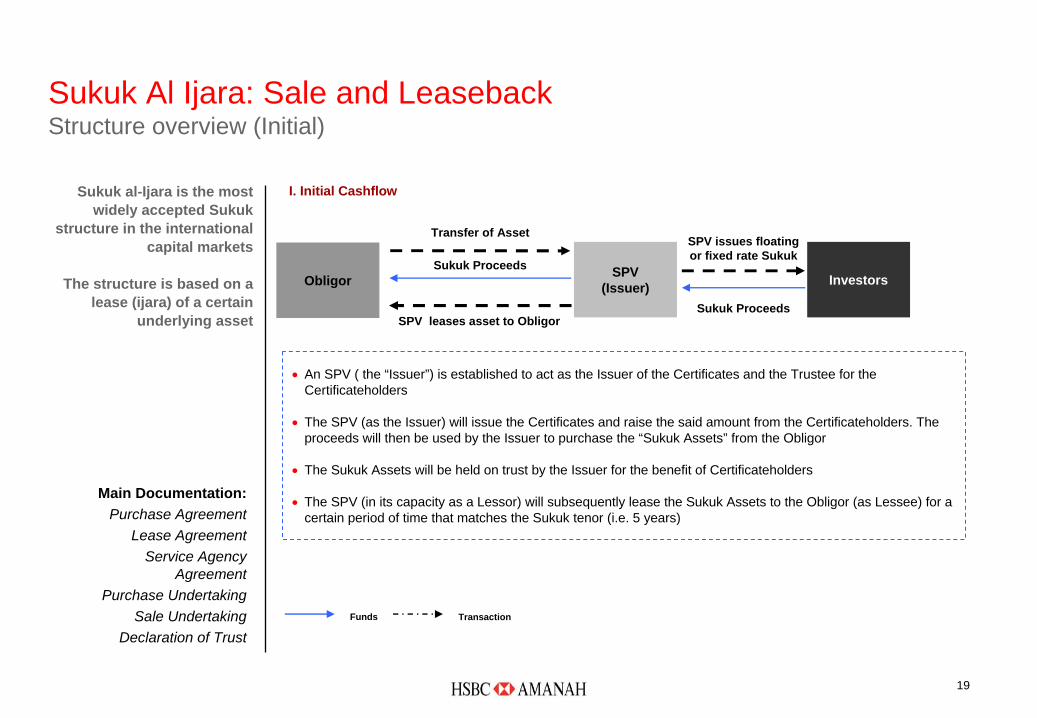

Main Documentation:Purchase Agreement

Lease AgreementService Agency

AgreementPurchase Undertaking

Sale UndertakingDeclaration of Trust

Sukuk Al Ijara: Sale and Leaseback Structure overview (Initial)

Sukuk al-Ijara is the most widely accepted Sukuk

structure in the international capital markets

The structure is based on a lease (ijara) of a certain

underlying asset

•

An SPV ( the “Issuer”) is established to act as the Issuer of the Certificates and the Trustee for the Certificateholders

•

The SPV (as the Issuer) will issue the Certificates and raise the said amount from the Certificateholders. The proceeds will then be used by the Issuer to purchase the “Sukuk Assets” from the Obligor

•

The Sukuk Assets will be held on trust by the Issuer for the benefit of Certificateholders

•

The SPV (in its capacity as a Lessor) will subsequently lease the Sukuk Assets to the Obligor (as Lessee) for a certain period of time that matches the Sukuk tenor (i.e. 5 years)

Obligor

20

Sukuk Al Ijara: Sale and Leaseback Structure overview (Ongoing)

SPV(Issuer)

May include repayments of principal

Periodic lease rental payments

Periodic lease rental payments

II. Payment of Periodic Rentals/Distribution Amounts (“Coupon”)

Investors

•

The Lessee shall pay lease rentals to the Issuer on certain periodic distribution dates, which the Issuer would then pay out to the Certificateholders as the periodic distribution amount (Profit Payment).

•

The lease rentals are predetermined and calculated based on a fixed percentage

Funds Transaction

The ongoing step during the life of the Sukuk is the

periodic distribution payment to the certificate

holders Obligor(as the Lessee)

21

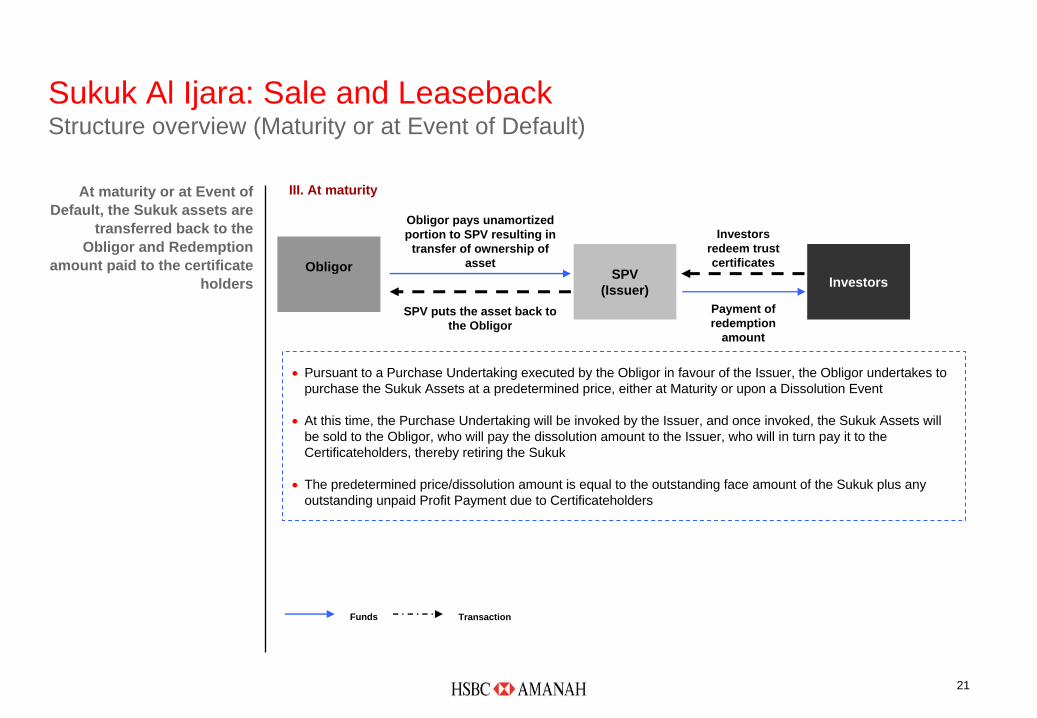

Sukuk Al Ijara: Sale and Leaseback Structure overview (Maturity or at Event of Default)

SPV(Issuer)

Obligor pays unamortized portion to SPV resulting in

transfer of ownership of asset

Payment of redemption

amount

SPV puts the asset back to the Obligor

Investors redeem trust certificates

III. At maturity

Investors

•

Pursuant to a Purchase Undertaking executed by the Obligor in favour of the Issuer, the Obligor undertakes to purchase the Sukuk Assets at a predetermined price, either at Maturity or upon a Dissolution Event

•

At this time, the Purchase Undertaking will be invoked by the Issuer, and once invoked, the Sukuk Assets will be sold to the Obligor, who will pay the dissolution amount to the Issuer, who will in turn pay it to the Certificateholders, thereby retiring the Sukuk

•

The predetermined price/dissolution amount is equal to the outstanding face amount of the Sukuk plus any outstanding unpaid Profit Payment due to Certificateholders

Funds Transaction

At maturity or at Event of Default, the Sukuk assets are

transferred back to the Obligor and Redemption

amount paid to the certificate holders

Obligor

22

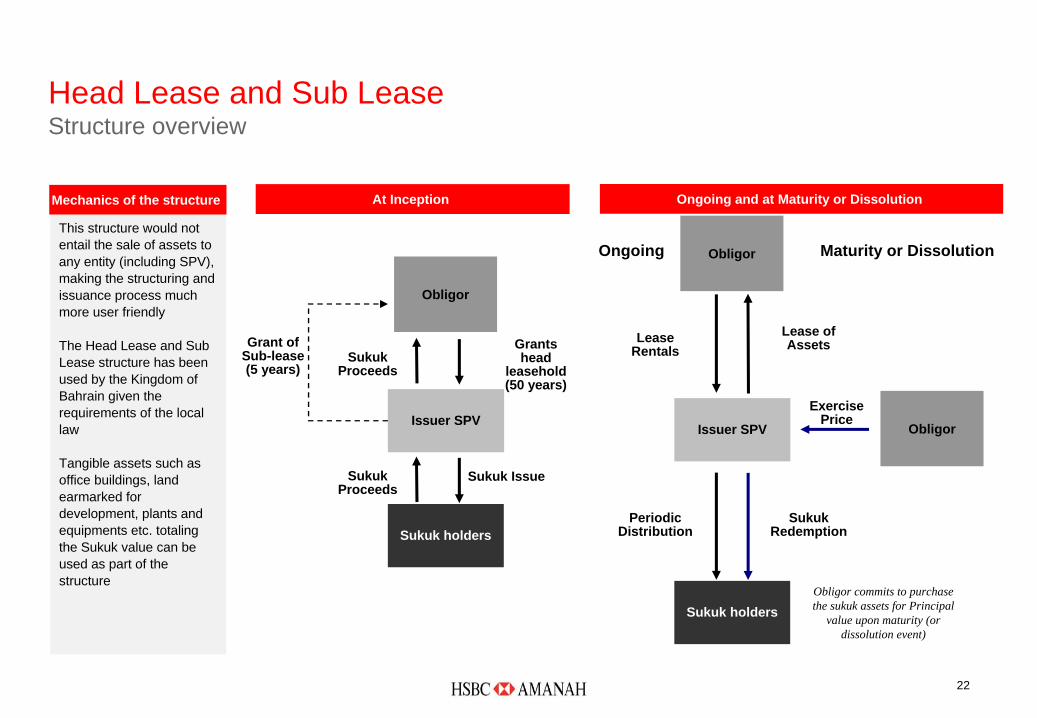

At Inception Ongoing and at Maturity or Dissolution

Exercise Price

Ongoing Maturity or Dissolution

Obligor commits to purchase the sukuk assets for Principal

value upon maturity (or dissolution event)

Sukuk holders

Sukuk Redemption

Lease Rentals

Periodic Distribution

Issuer SPV

Lease of Assets

Sukuk holders

Sukuk Proceeds

Issuer SPV

Grants head

leasehold (50 years)

Sukuk Issue

Sukuk Proceeds

Grant of Sub-lease (5 years)

Mechanics of the structure

This structure would not entail the sale of assets to any entity (including SPV), making the structuring and issuance process much more user friendly

The Head Lease and Sub Lease structure has been used by the Kingdom of Bahrain given the requirements of the local law

Tangible assets such as office buildings, land earmarked for development, plants and equipments etc. totaling the Sukuk value can be used as part of the structure

Head Lease and Sub Lease Structure overview

Obligor

Obligor

Obligor

HSBC Amanah Credentials

24

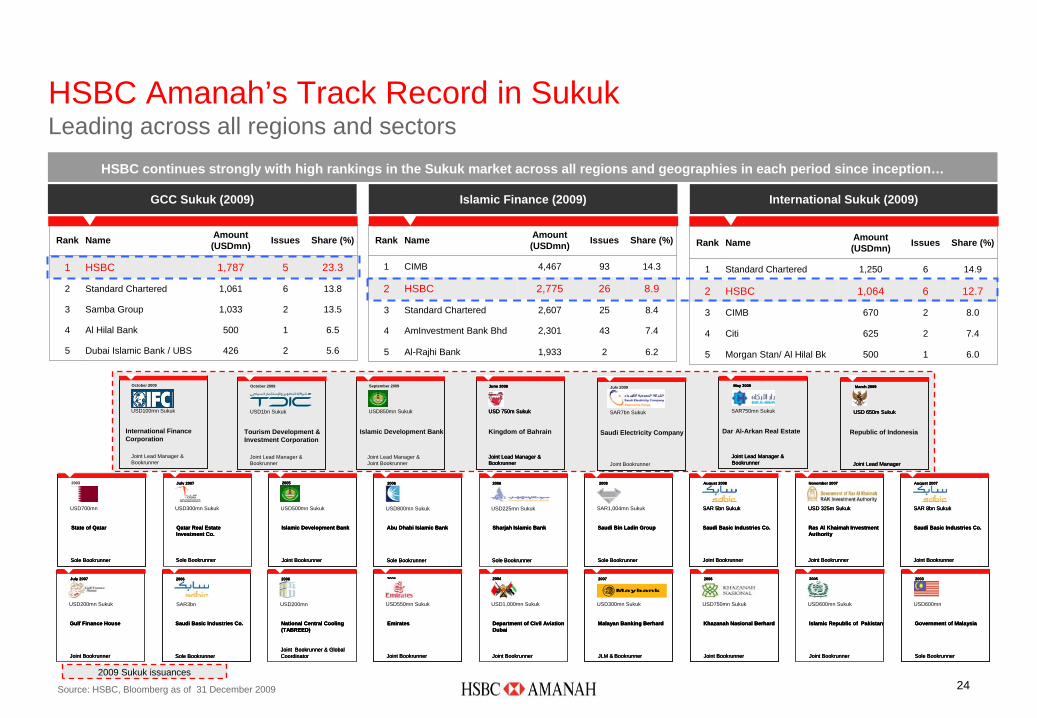

HSBC continues strongly with high rankings in the Sukuk market across all regions and geographies in each period since inception…

Source: HSBC, Bloomberg as of 31 December 2009

Rank Name Amount (USDmn) Issues Share (%)

1 Standard Chartered 1,250 6 14.9

2 HSBC 1,064 6 12.7

3 CIMB 670 2 8.0

4 Citi 625 2 7.4

5 Morgan Stan/ Al Hilal Bk 500 1 6.0

Rank Name Amount (USDmn) Issues Share (%)

1 HSBC 1,787 5 23.3

2 Standard Chartered 1,061 6 13.8

3 Samba Group 1,033 2 13.5

4 Al Hilal Bank 500 1 6.5

5 Dubai Islamic Bank / UBS 426 2 5.6

Rank Name Amount (USDmn) Issues Share (%)

1 CIMB 4,467 93 14.3

2 HSBC 2,775 26 8.9

3 Standard Chartered 2,607 25 8.4

4 AmInvestment Bank Bhd 2,301 43 7.4

5 Al-Rajhi Bank 1,933 2 6.2

HSBC Amanah’s Track Record in Sukuk Leading across all regions and sectors

International Sukuk (2009)GCC Sukuk (2009) Islamic Finance (2009)

2009 Sukuk issuances

USD 750m Sukuk

Kingdom of Bahrain

Joint Lead Manager & Bookrunner

June 2009

USD 750m Sukuk

Joint Lead Manager & Bookrunner

June 2009

USD 750m Sukuk

Joint Lead Manager & Bookrunner

June 2009

USD850mn Sukuk

Islamic Development Bank

September 2009

Joint Lead Manager & Joint Bookrunner

SAR7bn Sukuk

Saudi Electricity Company

Joint Bookrunner

July 2009

USD1bn Sukuk

Tourism Development & Investment Corporation

Joint Lead Manager &Bookrunner

October 2009

SAR750mn Sukuk

Dar Al-Arkan Real Estate

Joint Lead Manager & Bookrunner

May 2009

Joint Lead Manager & Bookrunner

May 2009

Joint Lead Manager & Bookrunner

May 2009

USD 650m Sukuk

Republic of Indonesia

Joint Lead Manager

March 2009

USD 650m Sukuk

Joint Lead Manager

March 2009

USD 650m Sukuk

Joint Lead Manager

March 2009

USD100mn Sukuk

International FinanceCorporation

Joint Lead Manager &Bookrunner

October 2009

USD700mn

State of Qatar

Sole Bookrunner

2003

State of Qatar

Sole Bookrunner

State of Qatar

Sole Bookrunner

USD300mn Sukuk

Qatar Real Estate Investment Co.

Sole Bookrunner

July 2007

Qatar Real Estate Investment Co.

Sole Bookrunner

July 2007

Qatar Real Estate Investment Co.

Sole Bookrunner

July 2007

USD500mn Sukuk

Islamic Development Bank

Joint Bookrunner

2005

Islamic Development Bank

Joint Bookrunner

2005

Islamic Development Bank

Joint Bookrunner

2005

USD800mn Sukuk

Abu Dhabi Islamic Bank

Sole Bookrunner

2006

Abu Dhabi Islamic Bank

Sole Bookrunner

2006

Abu Dhabi Islamic Bank

Sole Bookrunner

2006

USD225mn Sukuk

Sharjah Islamic Bank

Sole Bookrunner

2006

Sharjah Islamic Bank

Sole Bookrunner

2006

Sharjah Islamic Bank

Sole Bookrunner

2006

SAR1,004mn Sukuk

Saudi Bin Ladin Group

Sole Bookrunner

2008

Saudi Bin Ladin Group

Sole Bookrunner

2008

Saudi Bin Ladin Group

Sole Bookrunner

2008

SAR 5bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2008

SAR 5bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2008

SAR 5bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2008

USD 325m Sukuk

Ras Al Khaimah Investment Authority

Joint Bookrunner

November 2007

USD 325m Sukuk

Ras Al Khaimah Investment Authority

Joint Bookrunner

November 2007

USD 325m Sukuk

Ras Al Khaimah Investment Authority

Joint Bookrunner

November 2007

SAR 8bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2007

SAR 8bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2007

SAR 8bn Sukuk

Saudi Basic Industries Co.

Joint Bookrunner

August 2007

USD200mn Sukuk

Gulf Finance House

Joint Bookrunner

July 2007

Gulf Finance House

Joint Bookrunner

July 2007

Gulf Finance House

Joint Bookrunner

July 2007

SAR3bn

Saudi Basic Industries Co.

Sole Bookrunner

2006

Saudi Basic Industries Co.

Sole Bookrunner

2006

Saudi Basic Industries Co.

Sole Bookrunner

2006

USD200mn

National Central Cooling (TABREED)

Joint Bookrunner & Global Coordinator

2006

National Central Cooling (TABREED)

Joint Bookrunner & Global Coordinator

2006

National Central Cooling (TABREED)

Joint Bookrunner & Global Coordinator

2006

USD550mn Sukuk

Emirates

Joint Bookrunner

2005

Emirates

Joint Bookrunner

2005

Emirates

Joint Bookrunner

2005

USD1,000mn Sukuk

Department of Civil Aviation Dubai

Joint Bookrunner

2004

Department of Civil Aviation Dubai

Joint Bookrunner

2004

Department of Civil Aviation Dubai

Joint Bookrunner

2004

USD300mn Sukuk

Malayan Banking Berhard

JLM & Bookrunner

2007

Malayan Banking Berhard

JLM & Bookrunner

2007

Malayan Banking Berhard

JLM & Bookrunner

2007

USD750mn Sukuk

Khazanah Nasional Berhard

Joint Bookrunner

2006

Khazanah Nasional Berhard

Joint Bookrunner

2006

Khazanah Nasional Berhard

Joint Bookrunner

2006

USD600mn Sukuk

Islamic Republic of Pakistan

Joint Bookrunner

2005

Islamic Republic of Pakistan

Joint Bookrunner

2005

Islamic Republic of Pakistan

Joint Bookrunner

2005

USD600mn

Government of Malaysia

Sole Bookrunner

2003

Government of Malaysia

Sole Bookrunner

2003

Government of Malaysia

Sole Bookrunner

2003

25

Islamic Achievements of 2009 DCM achieved a record year across various jurisdictions

In 2009, HSBC marked itself out from its competitors as

it pushed forward with several new and innovative

deals despite difficult market conditions an

-Deal of the Year: Indonesia IDR5.56tn Retail Sukuk

-Sovereign Deal of the Year: Indonesia IDR5.56tn Retail and Indonesia USD650mn

Global Sukuk (joint winners)

-Wakalah Deal of the Year: IFC USD100mn

-Indonesia Deal of the Year: Indonesia IDR5.56tn Retail and Indonesia USD650mn

Global Sukuk (joint winners)

-Saudi Arabia Deal of the Year: SEC SAR7bn Sukuk

-UAE Deal of the Year: TDIC USD1bn Sukuk

-Yemen Deal of the Year: Sabafon USD5.7mn ECA-backed Murabaha

USD 750m Sukuk

Kingdom of Bahrain

Joint Lead Manager &Bookrunner

June 2009

SAR 750m Sukuk

Dar Al-Arkan Real Estate

Joint Lead Manager & Bookrunner

May 2009

US$ 650m Sukuk

Republic of Indonesia

Joint Lead Manager

March 2009

Joint Lead Manager

USD 850m Sukuk

Islamic Development Bank

September 2009

Joint Lead Manager & Bookrunner

SAR 7bn Sukuk

Saudi Electricity Company

Joint Bookrunner

July 2009

USD 1 bn Sukuk

Tourism Development & Investment Corporation

Joint Lead Manager &Bookrunner

October 2009

USD 100m Sukuk

International FinanceCorporation

Joint Lead Manager &Bookrunner

October 2009

Best Islamic Bond House 2009

Best Sukuk House 2010

Best International Islamic Bank

2010

FinanceAsiaBest Islamic Financing

IFRasiaIslamic Deal of the Year

The Asset Deal AwardsBest Deal Indonesia

ROI SukukMulti-Award Deal

Best Sukuk for 2009 Kingdom of

Bahrain

Islamic Awards Won

HSBC Led Islamic Transactions

26

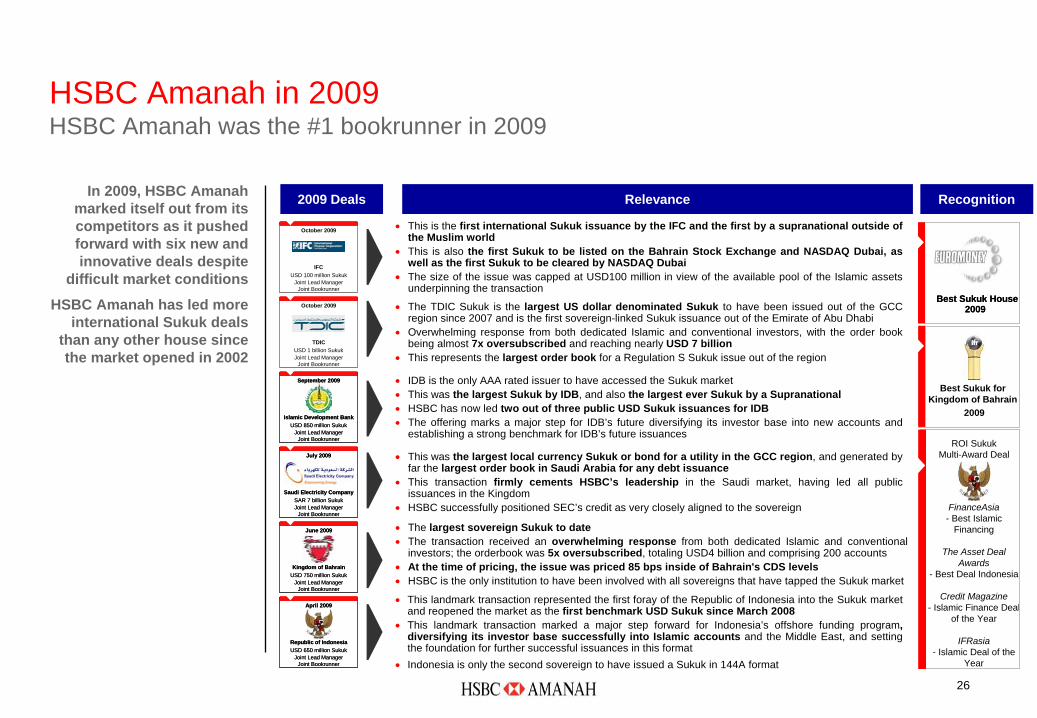

Relevance2009 Deals Recognition

•

The TDIC Sukuk is the largest US dollar denominated Sukuk to have been issued out of the GCC region since 2007 and is the first sovereign-linked Sukuk issuance out of the Emirate of Abu Dhabi

•

Overwhelming response from both dedicated Islamic and conventional investors, with the order book being almost 7x oversubscribed and reaching nearly USD 7 billion

•

This represents the largest order book for a Regulation S Sukuk issue out of the regionTDIC

USD 1 billion Sukuk

October 2009

Joint Lead Manager Joint Bookrunner

•

IDB is the only AAA rated issuer to have accessed the Sukuk market •

This was the largest Sukuk by IDB, and also the largest ever Sukuk by a Supranational•

HSBC has now led two out of three public USD Sukuk issuances for IDB•

The offering marks a major step for IDB’s future diversifying its investor base into new accounts and establishing a strong benchmark for IDB’s future issuances

Islamic Development BankUSD 850 million Sukuk

September 2009

Joint Lead Manager Joint Bookrunner

Islamic Development BankUSD 850 million Sukuk

September 2009

Joint Lead Manager Joint Bookrunner

•

This was the largest local currency Sukuk or bond for a utility in the GCC region, and generated by far the largest order book in Saudi Arabia for any debt issuance

•

This transaction firmly cements HSBC’s leadership in the Saudi market, having led all public issuances in the Kingdom

•

HSBC successfully positioned SEC’s credit as very closely aligned to the sovereignSaudi Electricity Company

SAR 7 billion Sukuk

July 2009

Joint Lead Manager Joint Bookrunner

Saudi Electricity CompanySAR 7 billion Sukuk

July 2009

Joint Lead Manager Joint Bookrunner

•

The largest sovereign Sukuk to date•

The transaction received an overwhelming response from both dedicated Islamic and conventional investors; the orderbook was 5x oversubscribed, totaling USD4 billion and comprising 200 accounts

•

At the time of pricing, the issue was priced 85 bps inside of Bahrain's CDS levels•

HSBC is the only institution to have been involved with all sovereigns that have tapped the Sukuk marketKingdom of Bahrain

USD 750 million Sukuk

June 2009

Joint Lead Manager Joint Bookrunner

Kingdom of BahrainUSD 750 million Sukuk

June 2009

Joint Lead Manager Joint Bookrunner

•

This landmark transaction represented the first foray of the Republic of Indonesia into the Sukuk market and reopened the market as the first benchmark USD Sukuk since March 2008

•

This landmark transaction marked a major step forward for Indonesia’s offshore funding program, diversifying its investor base successfully into Islamic accounts and the Middle East, and setting the foundation for further successful issuances in this format

•

Indonesia is only the second sovereign to have issued a Sukuk in 144A format

Republic of IndonesiaUSD 650 million Sukuk

April 2009

Joint Lead Manager Joint Bookrunner

Republic of IndonesiaUSD 650 million Sukuk

April 2009

Joint Lead Manager Joint Bookrunner

IFCUSD 100 million Sukuk

October 2009

Joint Lead Manager Joint Bookrunner

•

This is the first international Sukuk issuance by the IFC and the first by a supranational outside of the Muslim world

•

This is also the first Sukuk to be listed on the Bahrain Stock Exchange and NASDAQ Dubai, as well as the first Sukuk to be cleared by NASDAQ Dubai

•

The size of the issue was capped at USD100 million in view of the available pool of the Islamic assets underpinning the transaction

FinanceAsia- Best Islamic

Financing

The Asset Deal Awards

- Best Deal Indonesia

Credit Magazine- Islamic Finance Deal

of the Year

IFRasia- Islamic Deal of the

Year

ROI SukukMulti-Award Deal

2009

Best Sukuk for Kingdom of Bahrain

Best Sukuk House 2009

Best Sukuk House 2009

In 2009, HSBC Amanah marked itself out from its competitors as it pushed forward with six new and innovative deals despite

difficult market conditions

HSBC Amanah has led more international Sukuk deals

than any other house since the market opened in 2002

HSBC Amanah in 2009 HSBC Amanah was the #1 bookrunner in 2009

27

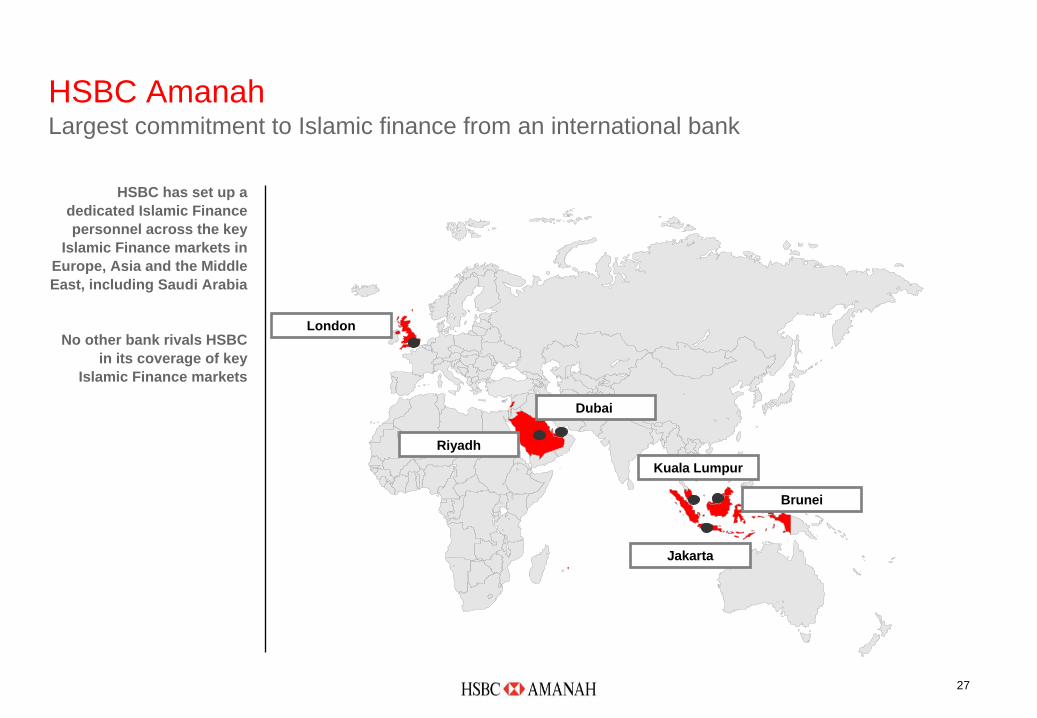

HSBC has set up a dedicated Islamic Finance personnel across the key

Islamic Finance markets in Europe, Asia and the Middle East, including Saudi Arabia

No other bank rivals HSBC in its coverage of key

Islamic Finance markets

London

Riyadh

Dubai

Kuala Lumpur

Brunei

Jakarta

HSBC Amanah Largest commitment to Islamic finance from an international bank

28

Issued by HSBC Bank Middle East Limited, PO Box 4604, Dubai, United Arab Emirates, which is incorporated in Jersey, Channel Islands and regulated by the Jersey Financial Services Commission to carry on investment business under the Financial Services (Jersey) Law 1998. Services are subject to HSBC Bank Middle East Limited’s terms and conditions.

HBME is a member of the HSBC Group of companies (the “HSBC Group”), any member of which may trade for its own account as Principal, may have underwritten an issue within the last 36 months or, together with its Directors, officers and employees, may have a long or short position in securities or instruments or in any related instrument mentioned in this document. Brokerage or fees may be earned by any member of the HSBC Group or persons associated with them in respect of any business transacted by them in all or any of the securities or instruments referred to in this document.

The information in this document is derived from sources believed to be reliable but which have not been independently verified. HSBC Bank makes no guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor is it liable for damages arising out of any person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary data. The opinions in this document constitute the present judgment of HSBC Bank, which is subject to change without notice.

This document is neither an offer to sell, purchase or subscribe for any investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for the use of private customers.

This document is not intended for distribution in the United States of America or to US persons. This document is intended to be distributed in its entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Any transaction will be subject to HSBC Bank’s Terms of Business.

HSBC Bank Middle East Limited

Incorporated in Jersey, Channel Islands

Registered Office: HSBC House, Esplanade

St. Helier, Jersey JE4 8UB

Channel Islands

Member of HSBC Group

Disclaimer

![CALIFORNIA [ADVANCE RELEASE] · Sh Sh MgCp SG SG SG SG SG SG SG SG SG Fe Fe Gr-s Gr-s Per CS Pum Pum Salt Salt Salt S-o S-o Zeo Dia Bent Bent Bent B B Clay Clay Dia DS DS DS DS DS](https://static.fdocuments.in/doc/165x107/5d435e0888c993ea558bc1de/california-advance-release-sh-sh-mgcp-sg-sg-sg-sg-sg-sg-sg-sg-sg-fe-fe-gr-s.jpg)