Introduction to Interest Rate Trading - Interactive Brokers · Introduction to Interest Rate...

44

Introduction to Interest Rate Trading Andrew Wilkinson Andrew Wilkinson

Transcript of Introduction to Interest Rate Trading - Interactive Brokers · Introduction to Interest Rate...

Introduction to Interest Rate Trading

Andrew WilkinsonAndrew Wilkinson

Risk Disclosure

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. For a copy, call (203) 618-5800.

Any strategies discussed, including examples using actual securities and price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement, recommendation or solicitation to buy or sell securities. Past performance is not a guarantee of future results.

Interactive Brokers LLC is a member of NYSE, FINRA, SIPC

Monetary Policy

Central banks set monetary policyCentral banks set monetary policyIncludes level of interest ratesIncludes level of interest ratesProvision of liquidity Provision of liquidity Money supplyMoney supply

The outright benchmark or key rate is importantThe outright benchmark or key rate is importantSo to is the yield curveSo to is the yield curve

Factors Influencing Monetary Policy

GrowthGrowthInflationInflationEmploymentEmploymentRetail SalesRetail SalesHousing marketHousing marketBusiness and consumer confidenceBusiness and consumer confidenceExchange rateExchange rateFor a full discussion see For a full discussion see ““Introduction to FXIntroduction to FX””

The Yield Curve

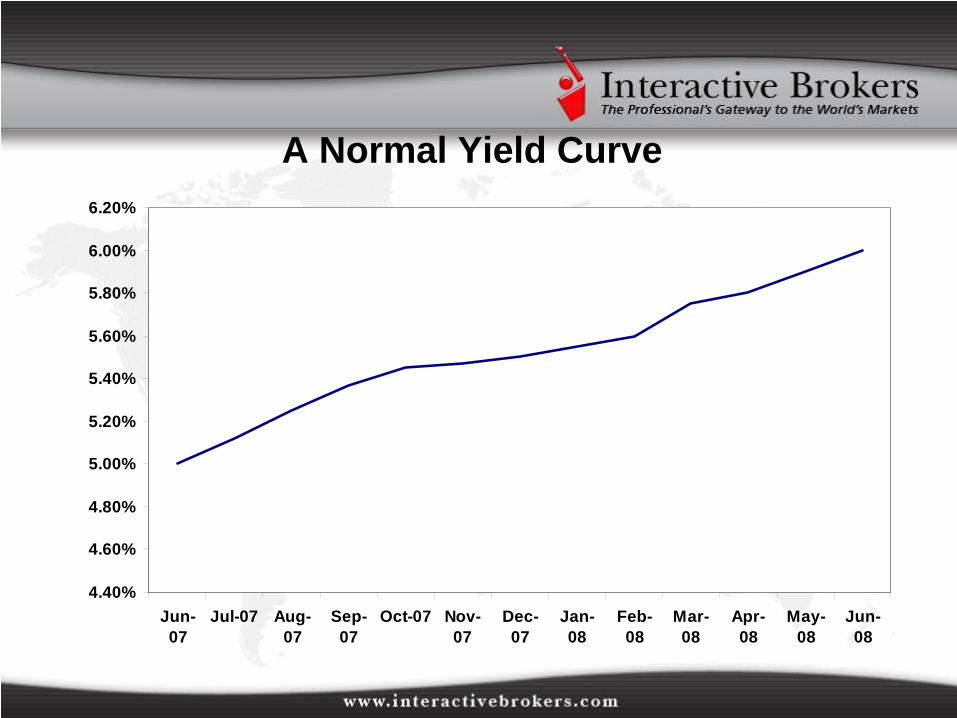

The shape depicting the time horizon of moneyThe shape depicting the time horizon of moneyKey to understanding this is that interest rates are Key to understanding this is that interest rates are market determined market determined –– outside of central bankoutside of central bankLook at the price of money from oneLook at the price of money from one--toto--12 months12 monthsYield curve can be positive or negativeYield curve can be positive or negative

A Normal Yield Curve

4.40%

4.60%

4.80%

5.00%

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

Jun-07

Jul-07 Aug-07

Sep-07

Oct-07 Nov-07

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

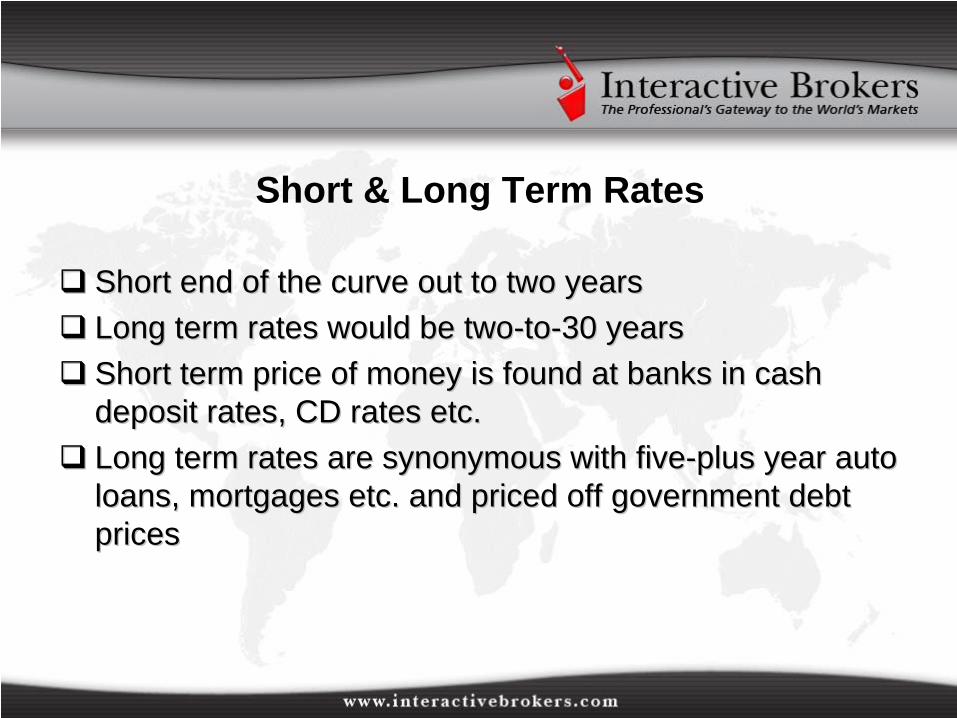

Short & Long Term Rates

Short end of the curve out to two yearsShort end of the curve out to two yearsLong term rates would be twoLong term rates would be two--toto--30 years30 yearsShort term price of money is found at banks in cash Short term price of money is found at banks in cash deposit rates, CD rates etc.deposit rates, CD rates etc.Long term rates are synonymous with fiveLong term rates are synonymous with five--plus year auto plus year auto loans, mortgages etc. and priced off government debt loans, mortgages etc. and priced off government debt pricesprices

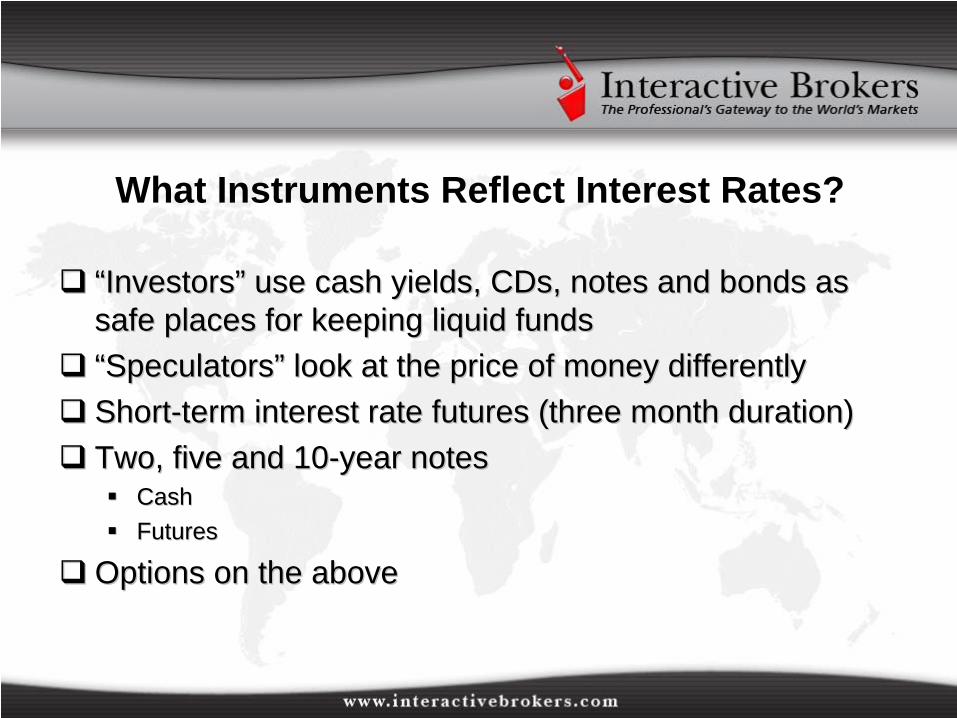

What Instruments Reflect Interest Rates?

““InvestorsInvestors”” use cash yields, CDs, notes and bonds as use cash yields, CDs, notes and bonds as safe places for keeping liquid fundssafe places for keeping liquid funds““SpeculatorsSpeculators”” look at the price of money differentlylook at the price of money differentlyShortShort--term interest rate futures (three month duration)term interest rate futures (three month duration)Two, five and 10Two, five and 10--year notesyear notes

CashCashFuturesFutures

Options on the aboveOptions on the above

Products and Trading

Each country (economic area) has its own short term Each country (economic area) has its own short term rate of interestrate of interestOf interest to us is the price of money and its relationship Of interest to us is the price of money and its relationship with current futures pricingwith current futures pricingWe are also interested in the relationship between one We are also interested in the relationship between one priceprice--point on the chart and other price points on the point on the chart and other price points on the chartchartWe are interested in the relationship over time between We are interested in the relationship over time between one market and anotherone market and another

Summary

Money market rates versus central bank policyMoney market rates versus central bank policyIntraIntra--market spreadsmarket spreadsInterInter--market spreadsmarket spreadsAT ALL TIMES: Shape of the curveAT ALL TIMES: Shape of the curve

United States

SymbolSymbol3 month eurodollar 3 month eurodollar GEGE2 year note2 year note ZTZT5 year note5 year note ZFZF10 year note10 year note ZNZN

CMECMECBOT CBOT CBOTCBOTCBOTCBOT

United Kingdom

SymbolSymbol3 3 mthmth short sterlingshort sterling LLLong giltLong gilt RR

London International Financial London International Financial Futures & Options ExchangeFutures & Options ExchangeLIFFELIFFE

European Currency

SymbolSymbol3 3 mthmth EuriborEuribor EU3EU3Euro Schatz Euro Schatz (2yr) (2yr) GBSGBSEuro BOBLEuro BOBL (5yr)(5yr) GBMGBMEuro Bund Euro Bund (10yr)(10yr) GBLGBL

LIFFELIFFEEUREXEUREXEUREXEUREXEUREXEUREX

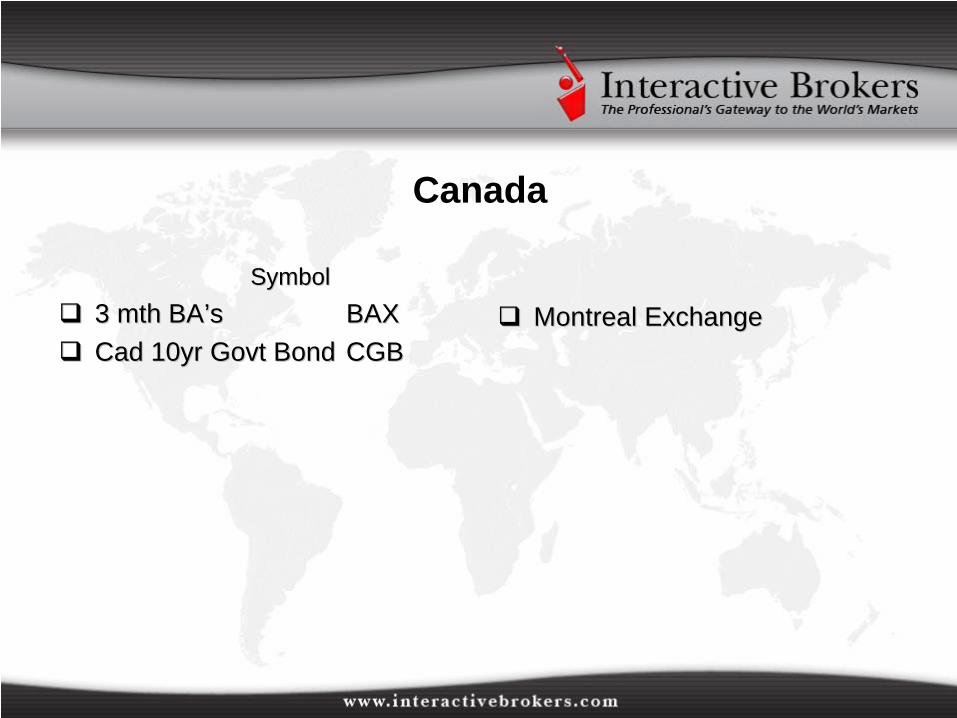

Canada

SymbolSymbol3 3 mthmth BABA’’ss BAXBAXCad 10yr Cad 10yr GovtGovt BondBond CGBCGB

Montreal ExchangeMontreal Exchange

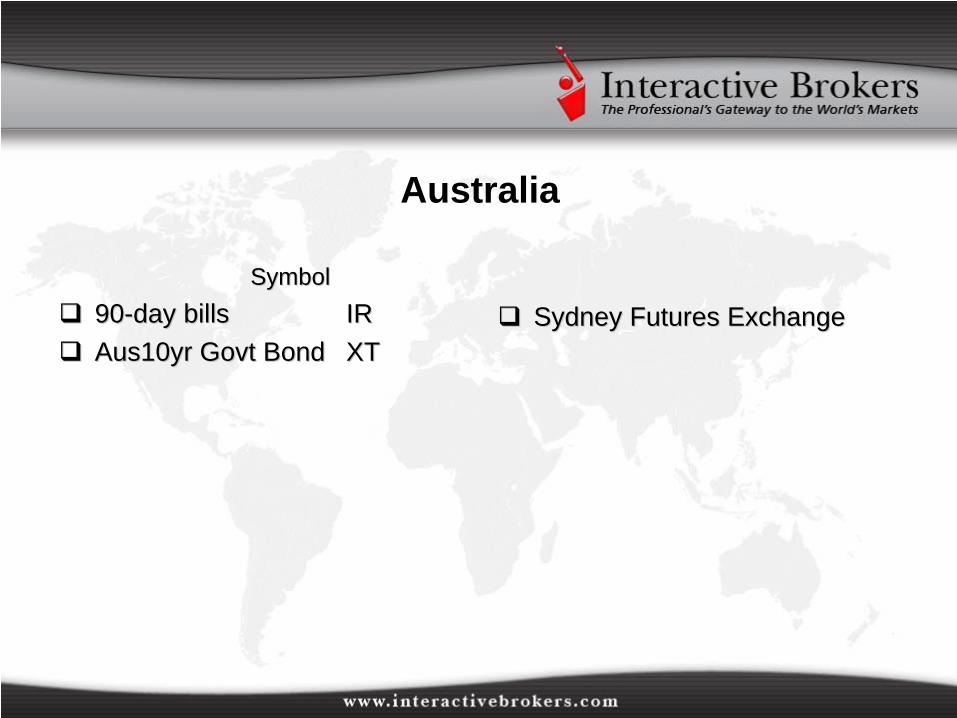

Australia

SymbolSymbol9090--day billsday bills IRIRAus10yr Aus10yr GovtGovt BondBond XTXT

Sydney Futures ExchangeSydney Futures Exchange

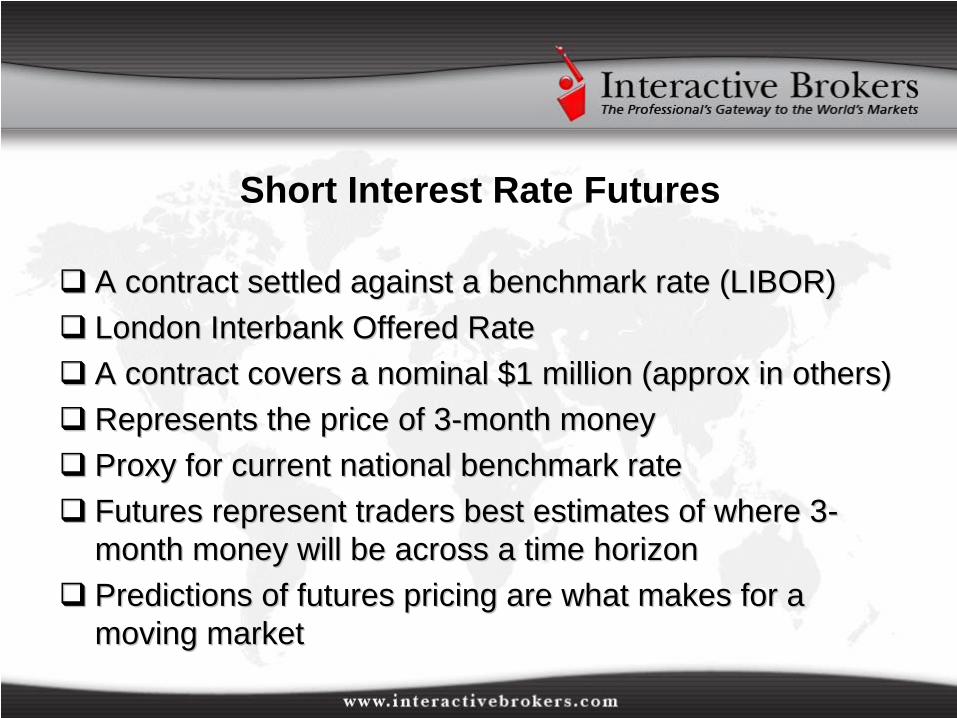

Short Interest Rate Futures

A contract settled against a benchmark rate (LIBOR)A contract settled against a benchmark rate (LIBOR)London London InterbankInterbank Offered Rate Offered Rate A contract covers a nominal $1 million (approx in others)A contract covers a nominal $1 million (approx in others)Represents the price of 3Represents the price of 3--month moneymonth moneyProxy for current national benchmark rateProxy for current national benchmark rateFutures represent traders best estimates of where 3Futures represent traders best estimates of where 3--month money will be across a time horizonmonth money will be across a time horizonPredictions of futures pricing are what makes for a Predictions of futures pricing are what makes for a moving marketmoving market

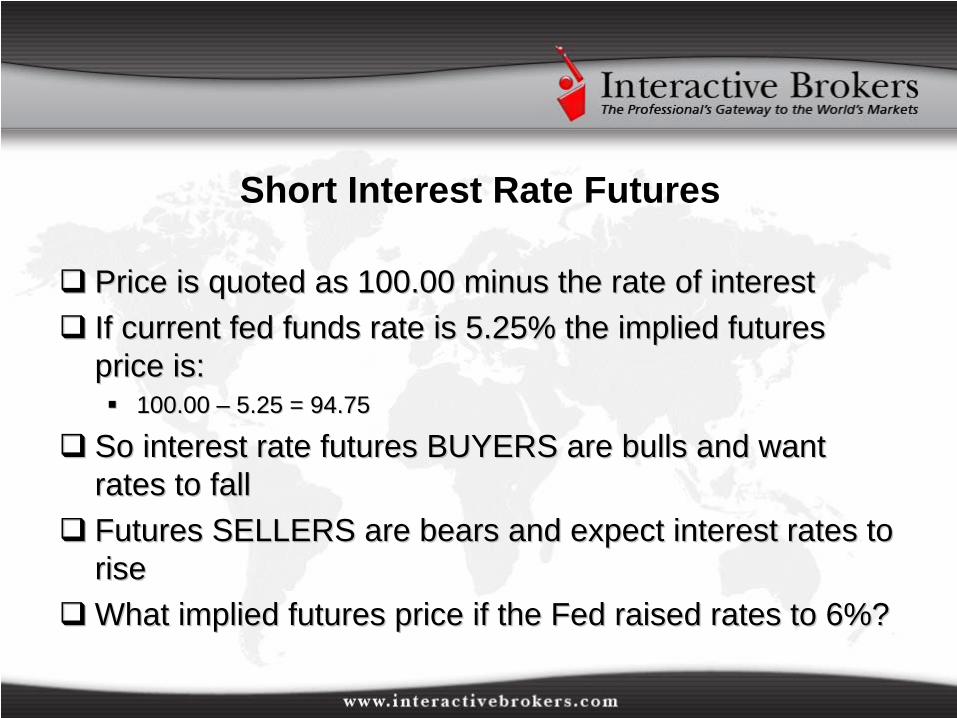

Short Interest Rate Futures

Price is quoted as 100.00 minus the rate of interestPrice is quoted as 100.00 minus the rate of interestIf current fed funds rate is 5.25% the implied futures If current fed funds rate is 5.25% the implied futures price is:price is:

100.00 100.00 –– 5.25 = 94.755.25 = 94.75

So interest rate futures BUYERS are bulls and want So interest rate futures BUYERS are bulls and want rates to fallrates to fallFutures SELLERS are bears and expect interest rates to Futures SELLERS are bears and expect interest rates to riseriseWhat implied futures price if the Fed raised rates to 6%?What implied futures price if the Fed raised rates to 6%?

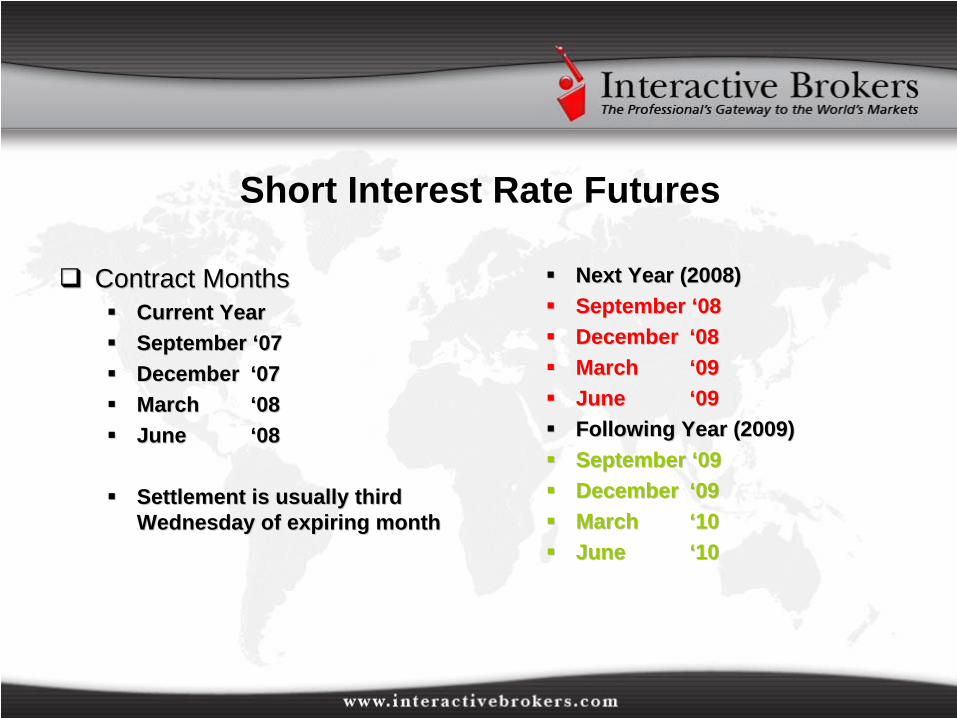

Short Interest Rate Futures

Contract MonthsContract MonthsCurrent YearCurrent YearSeptember September ‘‘0707DecemberDecember ‘‘0707MarchMarch ‘‘0808JuneJune ‘‘0808

Settlement is usually third Settlement is usually third Wednesday of expiring monthWednesday of expiring month

Next Year (2008)Next Year (2008)September September ‘‘0808DecemberDecember ‘‘0808MarchMarch ‘‘0909JuneJune ‘‘0909Following Year (2009)Following Year (2009)September September ‘‘0909DecemberDecember ‘‘0909MarchMarch ‘‘1010JuneJune ‘‘1010

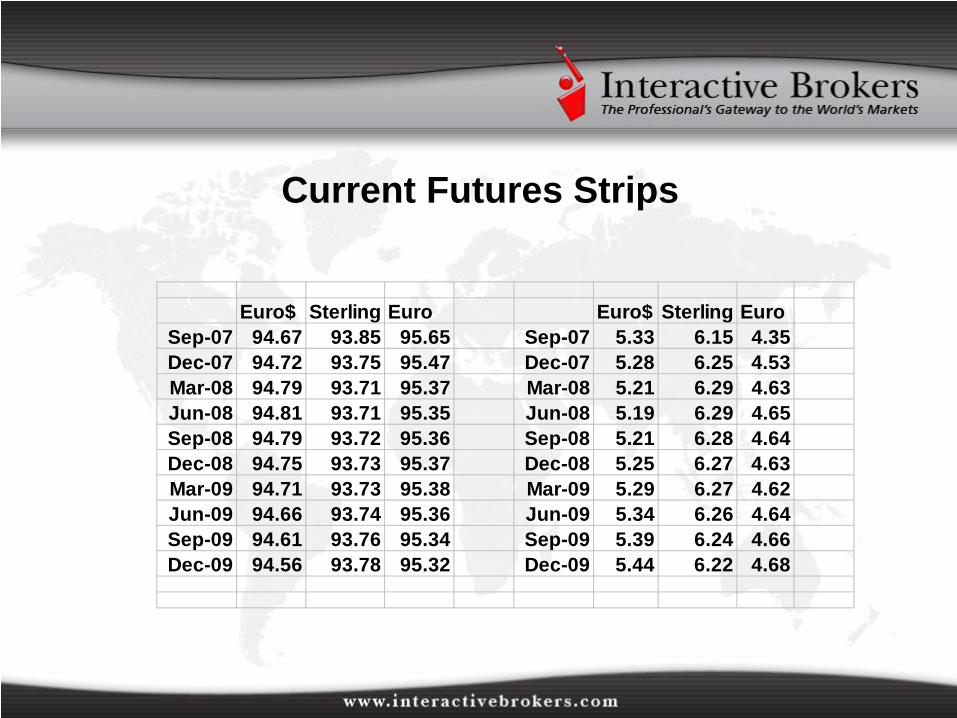

Current Futures Strips

Euro$ Sterling Euro Euro$ Sterling EuroSep-07 94.67 93.85 95.65 Sep-07 5.33 6.15 4.35Dec-07 94.72 93.75 95.47 Dec-07 5.28 6.25 4.53Mar-08 94.79 93.71 95.37 Mar-08 5.21 6.29 4.63Jun-08 94.81 93.71 95.35 Jun-08 5.19 6.29 4.65Sep-08 94.79 93.72 95.36 Sep-08 5.21 6.28 4.64Dec-08 94.75 93.73 95.37 Dec-08 5.25 6.27 4.63Mar-09 94.71 93.73 95.38 Mar-09 5.29 6.27 4.62Jun-09 94.66 93.74 95.36 Jun-09 5.34 6.26 4.64Sep-09 94.61 93.76 95.34 Sep-09 5.39 6.24 4.66Dec-09 94.56 93.78 95.32 Dec-09 5.44 6.22 4.68

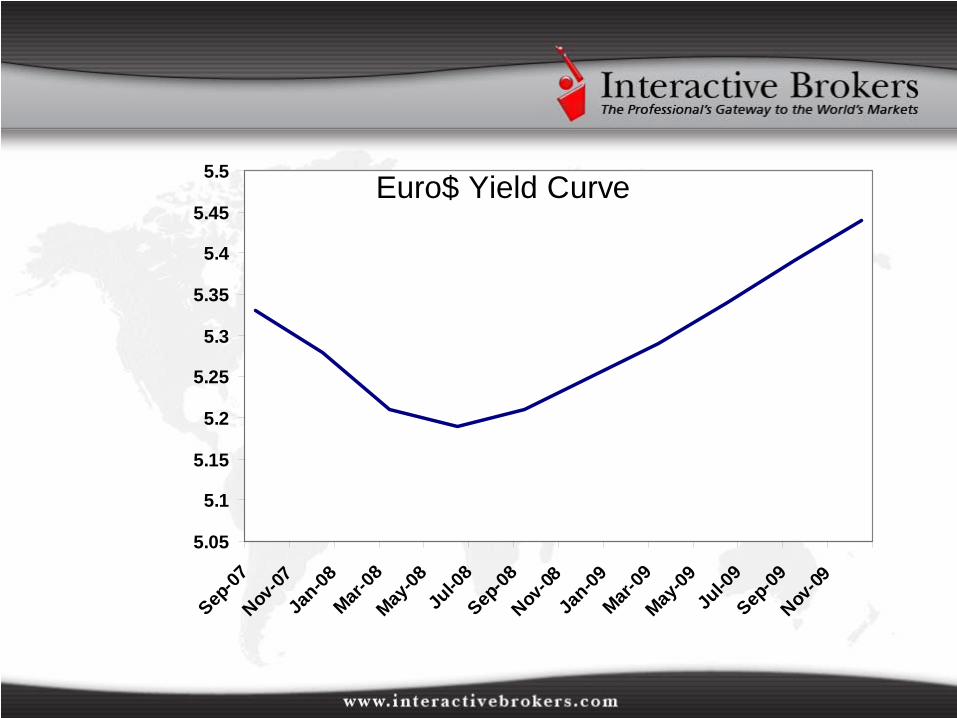

Euro$ Yield Curve

5.05

5.1

5.15

5.2

5.25

5.3

5.35

5.4

5.45

5.5

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-0

8Sep

-08Nov

-08Ja

n-09Mar-

09May

-09Ju

l-09

Sep-09

Nov-09

Eurodollars

December 2007 eurodollar future = 94.72December 2007 eurodollar future = 94.72Implies 3Implies 3--month LIBOR will be 5.28% in Decembermonth LIBOR will be 5.28% in DecemberQ> What would one do if you believed the Fed would Q> What would one do if you believed the Fed would RAISE interest rates by a half percent before then? RAISE interest rates by a half percent before then?

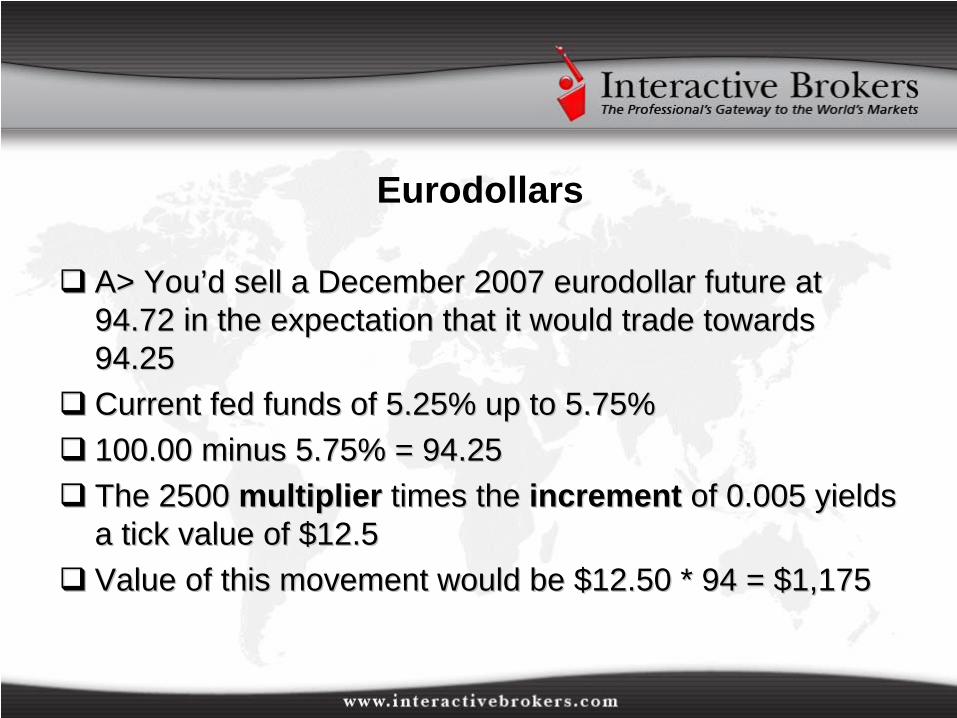

Eurodollars

A> YouA> You’’d sell a December 2007 eurodollar future at d sell a December 2007 eurodollar future at 94.72 in the expectation that it would trade towards 94.72 in the expectation that it would trade towards 94.2594.25Current fed funds of 5.25% up to 5.75%Current fed funds of 5.25% up to 5.75%100.00 minus 5.75% = 94.25100.00 minus 5.75% = 94.25The 2500 The 2500 multiplier multiplier times the times the increment increment of 0.005 yields of 0.005 yields a tick value of $12.5a tick value of $12.5Value of this movement would be $12.50 * 94 = $1,175Value of this movement would be $12.50 * 94 = $1,175

Eurodollars

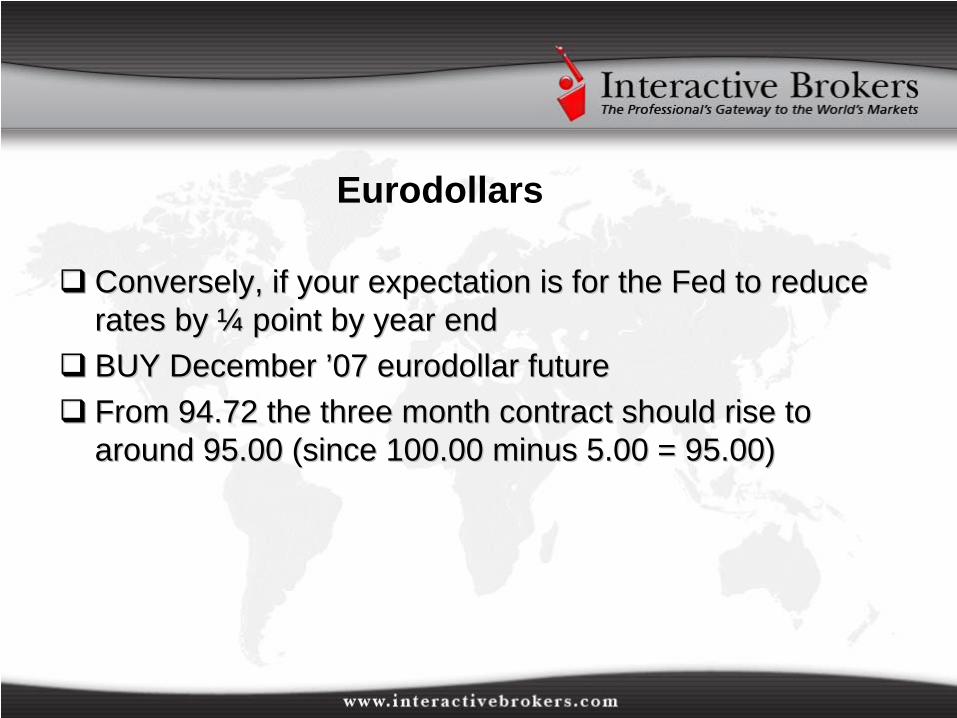

Conversely, if your expectation is for the Fed to reduce Conversely, if your expectation is for the Fed to reduce rates by rates by ¼¼ point by year endpoint by year endBUY December BUY December ’’07 eurodollar future07 eurodollar futureFrom 94.72 the three month contract should rise to From 94.72 the three month contract should rise to around 95.00 (since 100.00 minus 5.00 = 95.00)around 95.00 (since 100.00 minus 5.00 = 95.00)

Trade Size Warning!

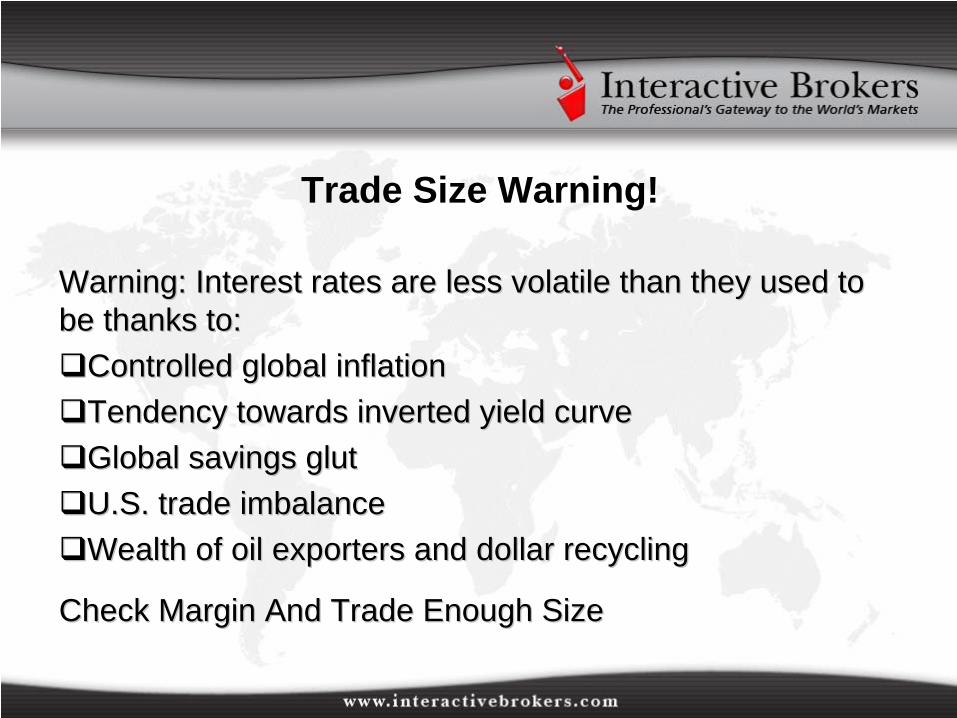

Warning: Interest rates are less volatile than they used to Warning: Interest rates are less volatile than they used to be thanks to:be thanks to:

Controlled global inflationControlled global inflationTendency towards inverted yield curveTendency towards inverted yield curveGlobal savings glutGlobal savings glutU.S. trade imbalanceU.S. trade imbalanceWealth of oil exporters and dollar recyclingWealth of oil exporters and dollar recycling

Check Margin And Trade Enough SizeCheck Margin And Trade Enough Size

Eurodollar Summary

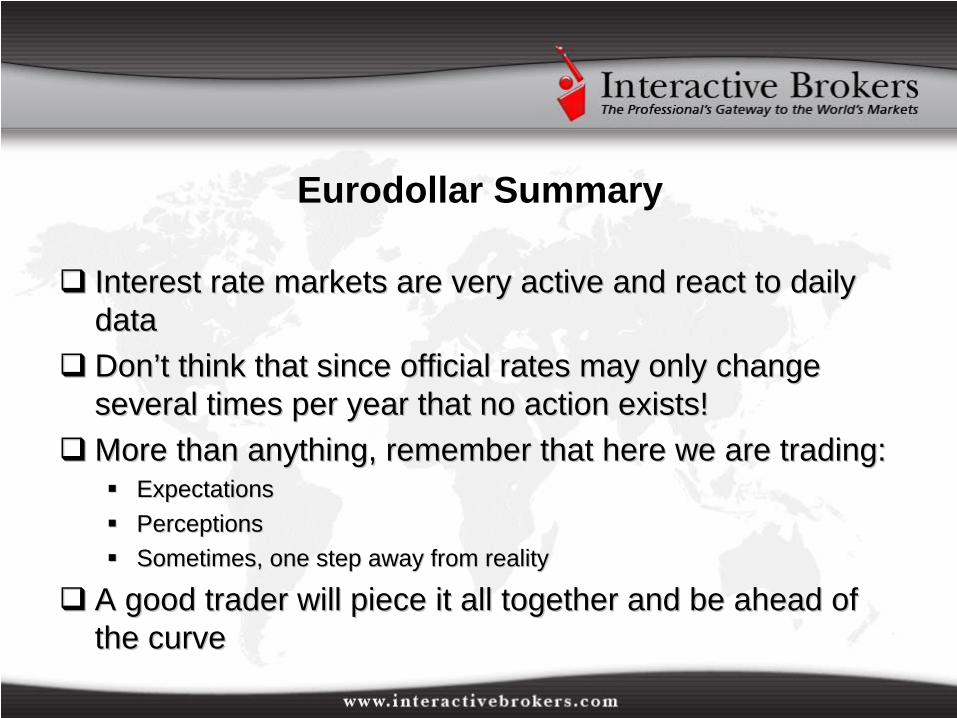

Interest rate markets are very active and react to daily Interest rate markets are very active and react to daily datadataDonDon’’t think that since official rates may only change t think that since official rates may only change several times per year that no action exists!several times per year that no action exists!More than anything, remember that here we are trading:More than anything, remember that here we are trading:

ExpectationsExpectationsPerceptionsPerceptionsSometimes, one step away from realitySometimes, one step away from reality

A good trader will piece it all together and be ahead of A good trader will piece it all together and be ahead of the curvethe curve

Eurodollar Spread Trading

A single eurodollar contract is one piece of the jigsawA single eurodollar contract is one piece of the jigsawRepresents just one point in timeRepresents just one point in timeYield curves shift up or downYield curves shift up or down

Outright directional movementOutright directional movement

They also behave like a piece of elastic They also behave like a piece of elastic Relative movementRelative movement

LetLet’’s consider the relationship between two points in s consider the relationship between two points in timetime

December 2007 futureDecember 2007 futureDecember 2008 futureDecember 2008 future

Eurodollar Spreads

December 2007 future = 94.72 (5.28%)December 2007 future = 94.72 (5.28%)December 2008 future = 94.75 (5.25%)December 2008 future = 94.75 (5.25%)At present, very little between them (curve is flat)At present, very little between them (curve is flat)But the history reveals vastly different pictureBut the history reveals vastly different pictureTwo aspects to this type of trade:Two aspects to this type of trade:

Forces the trader to watch the yield curveForces the trader to watch the yield curveRequires some relative out performance and therefore precisionRequires some relative out performance and therefore precision

Long versus short combination also requires less marginLong versus short combination also requires less margin

Eurodollar Spreads

Spread loosely defined is the current best guess of what shape tSpread loosely defined is the current best guess of what shape the he yield curve will have between two future timeframes (future versyield curve will have between two future timeframes (future versus us future)future)Concept: Use Concept: Use ““buybuy”” and and ““sellsell”” to refer to the furthest contractto refer to the furthest contractOrder: Order:

Sell spread (buy near contract) and (sell far contract ) Sell spread (buy near contract) and (sell far contract ) Buy spread (sell near contract) and (buy far contract ) Buy spread (sell near contract) and (buy far contract )

Spread Spread sellerseller looks for out performance of front month relative to looks for out performance of front month relative to far month far month –– curve steepening tradecurve steepening tradeSpread Spread buyerbuyer looks for out performance of far month relative to front looks for out performance of far month relative to front month month -- curve flattening tradecurve flattening trade

Eurodollar Spreads

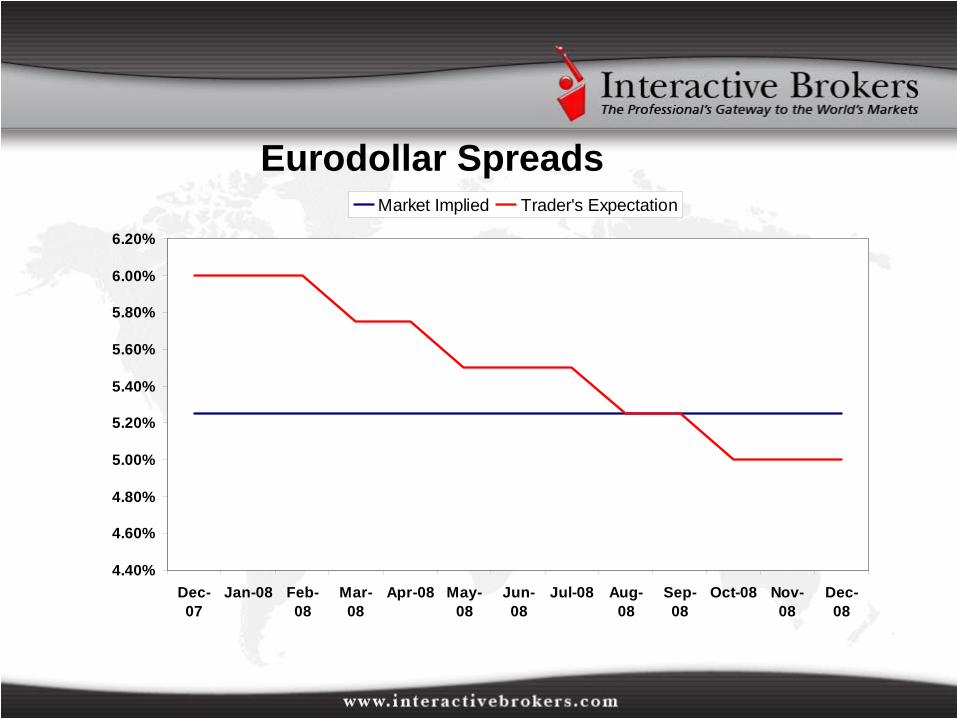

Consider a yield curve across Dec Consider a yield curve across Dec ‘‘07 and Dec 07 and Dec ’’08 08 contracts where both are priced at 94.75 (5.25%)contracts where both are priced at 94.75 (5.25%)Trader expects one Fed hike soon to ice the rate rising Trader expects one Fed hike soon to ice the rate rising cycle cycle Thereafter expects rate market to discount half percent Thereafter expects rate market to discount half percent easing over the course of 12 monthseasing over the course of 12 monthsSees Dec Sees Dec ’’07 falling to 94.50 (5.50%)07 falling to 94.50 (5.50%)Sees Dec Sees Dec ’’08 rising to 95.00 (5.00%)08 rising to 95.00 (5.00%)

Eurodollar Spreads

4.40%

4.60%

4.80%

5.00%

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

Dec-07

Jan-08 Feb-08

Mar-08

Apr-08 May-08

Jun-08

Jul-08 Aug-08

Sep-08

Oct-08 Nov-08

Dec-08

Market Implied Trader's Expectation

Eurodollar Spreads

Trader Trader buysbuys the spread at zero (both futures prices the spread at zero (both futures prices same)same)Sell Dec Sell Dec ’’07 @ 94.7507 @ 94.75Buy Dec Buy Dec ’’08 @ 94.7508 @ 94.75Thereafter the Fed does raise rates sending current Thereafter the Fed does raise rates sending current rates to 5.50% (94.50)rates to 5.50% (94.50)Market anticipates no more and begins to price in a 50 Market anticipates no more and begins to price in a 50 basis point cut sending Dec basis point cut sending Dec ’’08 future to 95.00 (5.00%)08 future to 95.00 (5.00%)

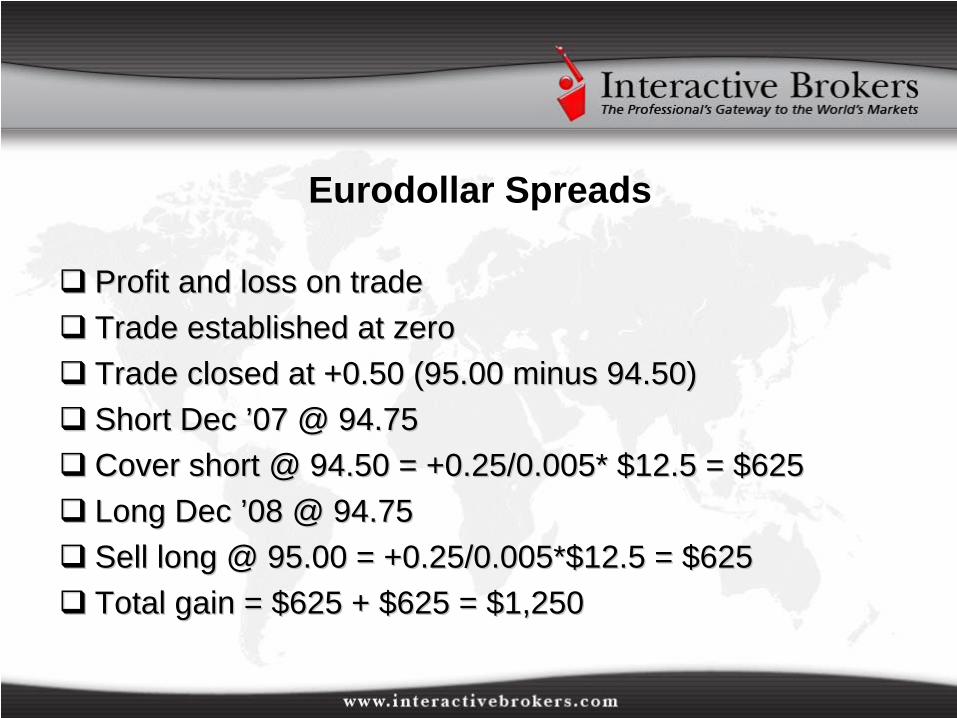

Eurodollar Spreads

Profit and loss on tradeProfit and loss on tradeTrade established at zero Trade established at zero Trade closed at +0.50 (95.00 minus 94.50)Trade closed at +0.50 (95.00 minus 94.50)Short Dec Short Dec ’’07 @ 94.7507 @ 94.75Cover short @ 94.50 = +0.25/0.005* $12.5 = $625Cover short @ 94.50 = +0.25/0.005* $12.5 = $625Long Dec Long Dec ’’08 @ 94.7508 @ 94.75Sell long @ 95.00 = +0.25/0.005*$12.5 = $625Sell long @ 95.00 = +0.25/0.005*$12.5 = $625Total gain = $625 + $625 = $1,250Total gain = $625 + $625 = $1,250

Inter-Market Spreads

In review: buy/sell eurodollar futures hoping to profit from In review: buy/sell eurodollar futures hoping to profit from anticipating interest rate market developmentsanticipating interest rate market developmentsMonitor the yield curveMonitor the yield curvePosition spread trades to benefit from anticipated curve Position spread trades to benefit from anticipated curve movements over time (intramovements over time (intra--market spreads)market spreads)But how to trade American interest rate expectations But how to trade American interest rate expectations versus rate expectations in any other country?versus rate expectations in any other country?InterInter--Market spreads!Market spreads!

Inter-Market Spreads

Theory is similar to intraTheory is similar to intra--market spreads market spreads Buy one currency curve and sell anotherBuy one currency curve and sell anotherWhy?Why?

Anticipate market specific development in one nationAnticipate market specific development in one nationExpect excessive change in inflation profileExpect excessive change in inflation profileNotice a central bank in/out of controlNotice a central bank in/out of controlCurrency related strengthening/weakening impact economy hardCurrency related strengthening/weakening impact economy hard

Inter-Market Spreads

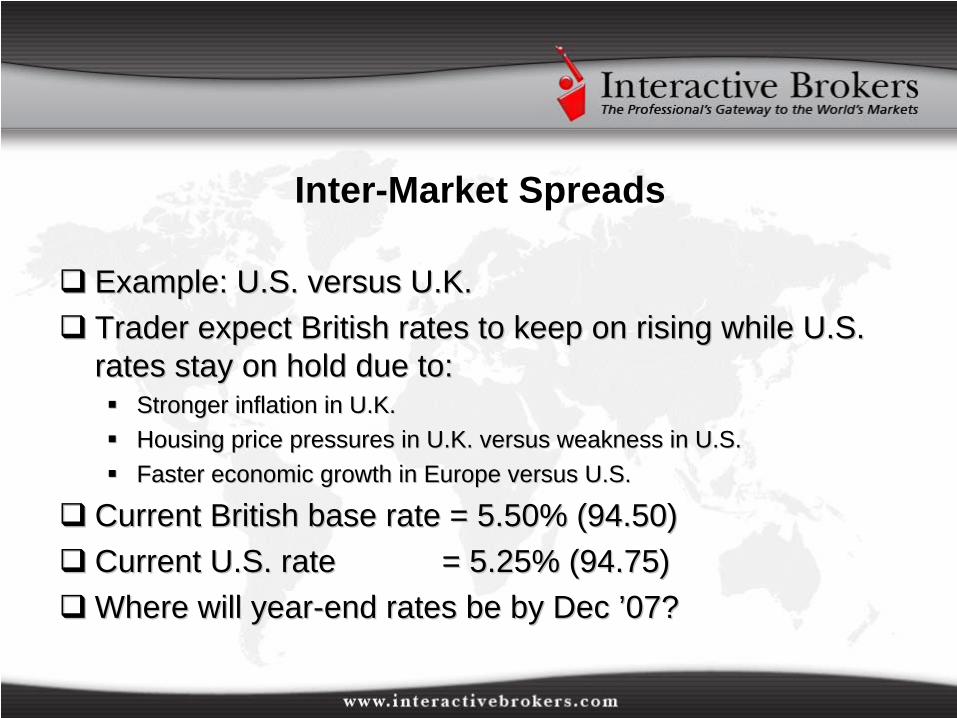

Example: U.S. versus U.K.Example: U.S. versus U.K.Trader expect British rates to keep on rising while U.S. Trader expect British rates to keep on rising while U.S. rates stay on hold due to:rates stay on hold due to:

Stronger inflation in U.K.Stronger inflation in U.K.Housing price pressures in U.K. versus weakness in U.S.Housing price pressures in U.K. versus weakness in U.S.Faster economic growth in Europe versus U.S.Faster economic growth in Europe versus U.S.

Current British base rate = 5.50% (94.50)Current British base rate = 5.50% (94.50)Current U.S. rate Current U.S. rate = 5.25% (94.75)= 5.25% (94.75)Where will yearWhere will year--end rates be by Dec end rates be by Dec ’’07?07?

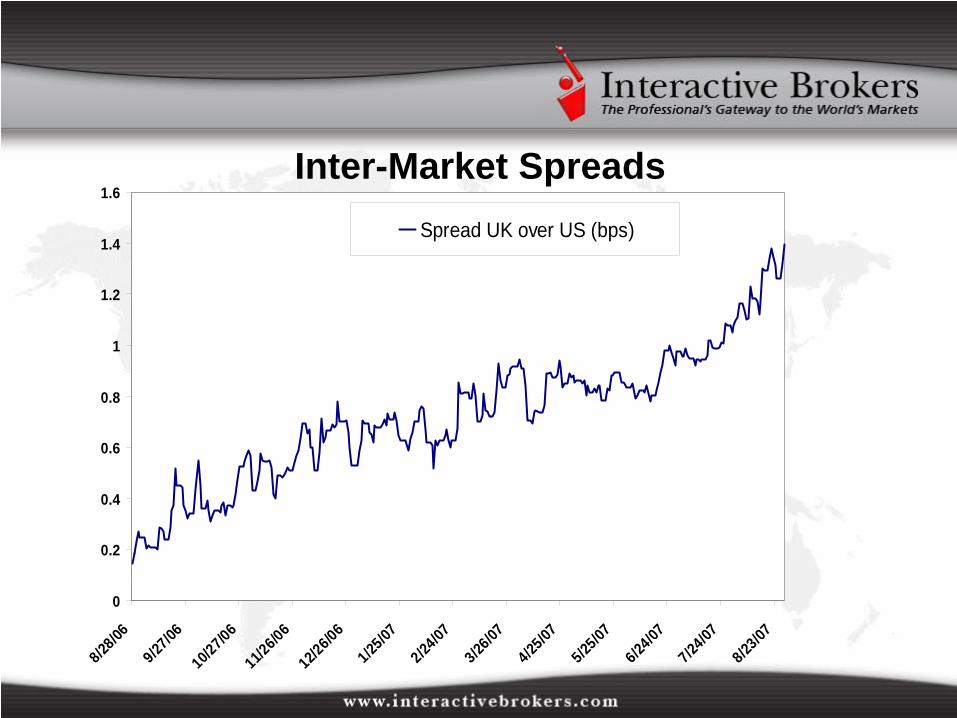

Inter-Market Spreads

More important question is, where are futures now?More important question is, where are futures now?Dec Dec ’’07 307 3--month short sterling @ 93.75 (= 6.25%)month short sterling @ 93.75 (= 6.25%)Dec Dec ’’07 eurodollar future @94.75 (= 5.25%)07 eurodollar future @94.75 (= 5.25%)Official rates are just 0.25% apart in favor of U.K.Official rates are just 0.25% apart in favor of U.K.Expectations are that by year end they will widen to 1%Expectations are that by year end they will widen to 1%What could the trader do?What could the trader do?

Inter-Market Spreads

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

8/28/06

9/27/06

10/27/06

11/26/06

12/26/06

1/25/07

2/24/07

3/26/07

4/25/07

5/25/07

6/24/07

7/24/07

8/23/07

Spread UK over US (bps)

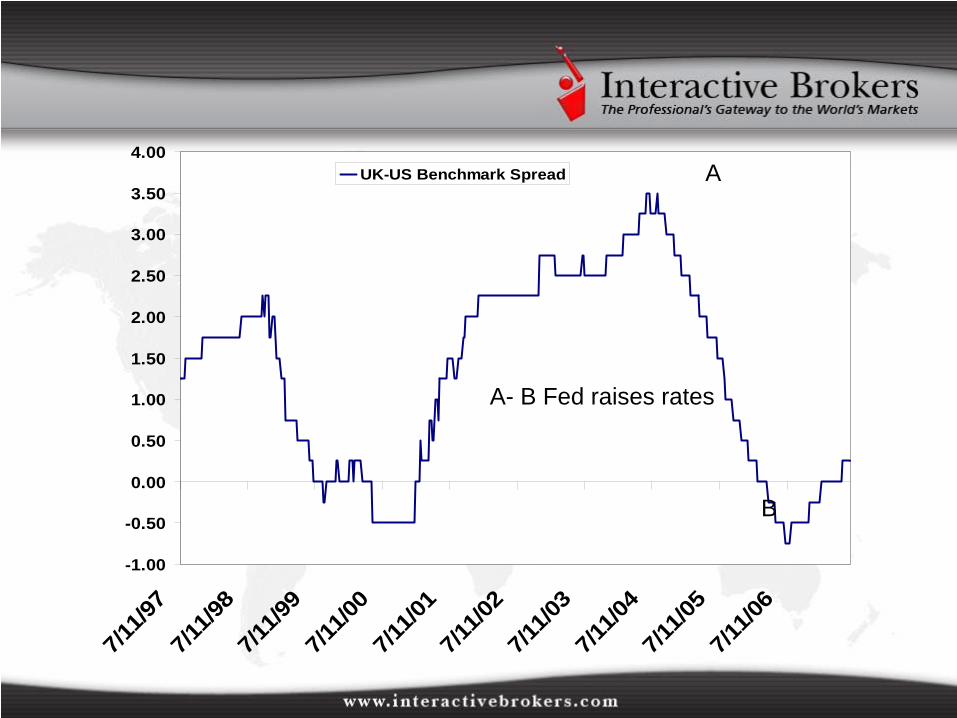

Inter-Market Spreads

Higher inflation rate in U.K. and legacy of weak currencyHigher inflation rate in U.K. and legacy of weak currencyTraditionally higher interest rate economyTraditionally higher interest rate economyFed prepared to move aggressivelyFed prepared to move aggressivelyBut look at historic differential between official ratesBut look at historic differential between official rates……

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

7/11/9

77/1

1/98

7/11/9

97/1

1/00

7/11/0

17/1

1/02

7/11/0

37/1

1/04

7/11/0

57/1

1/06

UK-US Benchmark Spread

A- B Fed raises rates

A

B

Bond Trading

Same principles apply to government debt tradingSame principles apply to government debt tradingVery liquid marketsVery liquid marketsOutright trading and directional tradingOutright trading and directional tradingSpread tradingSpread tradingCan be divorced from CB policyCan be divorced from CB policy

Cash Bond Trading

Focus on futures, but cash bonds are also commonFocus on futures, but cash bonds are also commonMore for mediumMore for medium--long term positioninglong term positioningFocus on incomeFocus on incomeConsider:Consider:

CouponCouponYieldYieldMaturityMaturity

CheapestCheapest--toto--deliver conceptdeliver concept

Locating Ticker Symbols on the Website

Look up icon on TWS toolbarLook up icon on TWS toolbarProduct listing under websiteProduct listing under website

FuturesFutures

Conclusions

Money markets actually more integral to investing Money markets actually more integral to investing than the stock marketsthan the stock marketsPlenty to keep your eye on if you want to venture Plenty to keep your eye on if you want to venture into interest rate tradinginto interest rate trading

Questions?