Introduction to Financial Engineering Aashish Dhakal Week 4: Bonds.

21

Introduction to Financial Engineering Aashish Dhakal Week 4: Bonds

-

Upload

flora-lewis -

Category

Documents

-

view

229 -

download

1

Transcript of Introduction to Financial Engineering Aashish Dhakal Week 4: Bonds.

Introduction to Financial Engineering

Aashish Dhakal

Week 4: Bonds

Our Plan1. BASIC BOND F EAT URES

2. BOND VAL UATION

3. Z ERO COUPON BONDS

4. Z ERO CURVE & BOOTST RAPPING

5. GILT STRIPPING

Bond Basic Concept

Issuer LenderBOND Certificate

Cash

1. Capital For Business (Issue Price)

1. Regular Interest(Coupon Rate)

2. Redemption price

Basic Bond Features Definition:

A bond is an instrument in which

the issuer promises to repay the lender

the amount borrowed plus interest

over a specified period of time (Hull. 2003).

Maturity or Duration:

is the day when

the debt will cease to exist,

also represents the period to the redemption day.

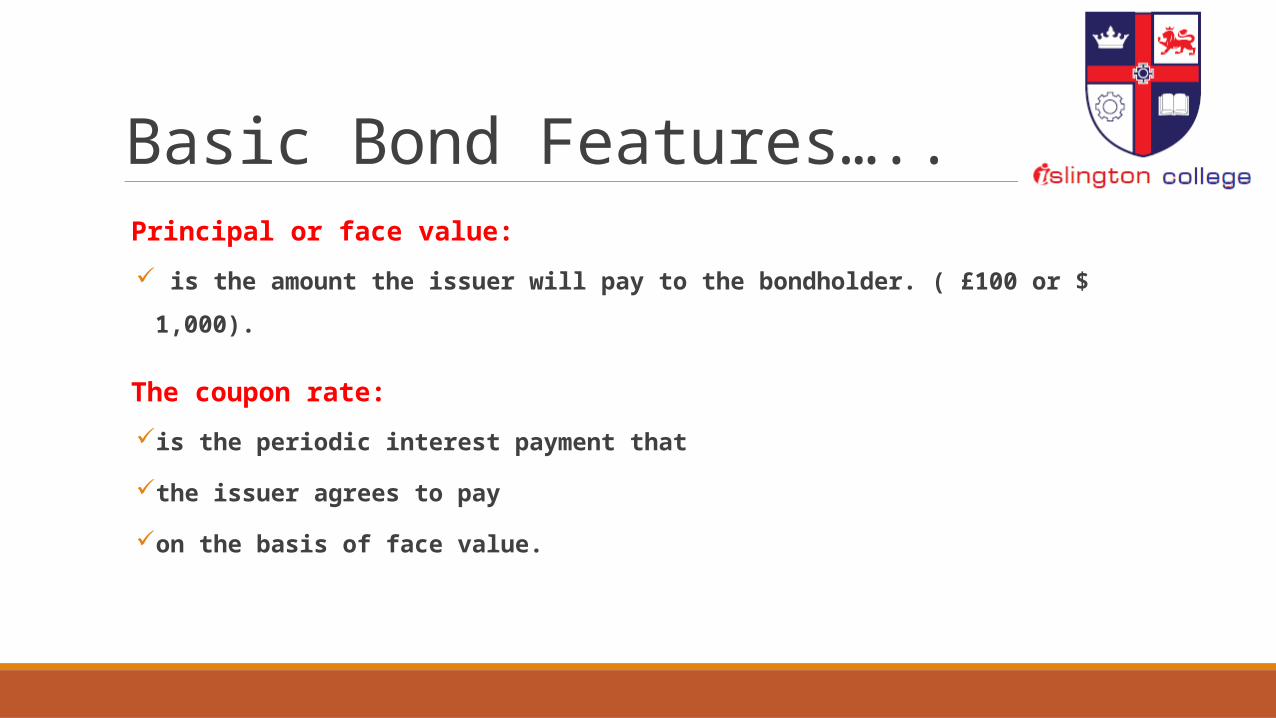

Basic Bond Features….. Principal or face value:

is the amount the issuer will pay to the bondholder. ( £100 or $ 1,000).

The coupon rate:

is the periodic interest payment that

the issuer agrees to pay

on the basis of face value.

Basic Bond Features…..The issuers of the bond can be the governments, corporations or other

institutions.

The holders of the bond are normally investors ( individual or

institutional).

From the bondholder’s prospective, initially there is a cash outflow of X

(e.g. £100 or $ 1,000), then for a coupon bond, there is a positive periodic

cash inflows, in the end the issuer would also return the principle.

Basic Features…. In Summary.Can be issued at, Premium, Par or discount.

Can be redeemed at Premium, Par or discount.

The coupon is applied in face value to arrive at the interest rate.

Interest is payable irrespective of the fortunes of business.

Interest is tax deductibles.

Value of bond means: FAIR MARKET PRICE OF BOND

Fair Market Price :

This is

the PV of

Future cash flows associated with the bond

discounted at the time value of money.

Po =C1

+C1

+ ….. +Cn+M

(1+R) (1+R)^2 (1+R)^n

Bond Valuation….The formula given above makes clear that the price of a financial asset

depends on r and Ci i = 1..n (discount rate). N=time to maturity.

However an important simplification of the formula above is the use of

the same discount rate for all cash flows. In fact this does not take into

account the fact that there are different interest rates for different

maturities. Generally we refer r as the yield rather than discount rate.

Bond ValuationThe “Po” is the current market price of the bond,

“Cn” is the periodic interest rate payment.

“r” is the discounted rate, so-called yield to maturity, it presents the

short term interest,

“M” is the Face Value or Maturity Value,

“n” is the periods of bond life, it could be accounted at an annual, semi-

annual, or quarterly basis.

Bond Valuation…… In coupon bond valuation, we normally assume that the interest rate payment is

made at the end of each period.

SO WHAT WE FIND……

The current market price of the bond equals to

the present value of

the sum of all the future cash flows.

Bond Valuation Example Example 1:

Q)The company plans to issue coupon bonds with 3 years duration. Face value

$1,000, coupon rate 10%, assuming the interest rate is paying semiannually, if

the current market yield is quoted at

(a) 8%,

(b) 10%,

(c) 12%,

How much should be reasonable issuing price respectively? Justify the answer.

Bond Valuation ExampleAnswer:

a) 1052

b) 1000

c) 993

So we Can Conclude……

Case Situation Issued at

A Interest Rate < Coupon rate Premium

B Interest Rate = Coupon rate PAR

C Interest Rate > Coupon rate Discount

Bond Valuation.. BUY/SELL/HOLD

Relationship Valuation Action

AMP < FMP Under Buy

AMP > FMP Over Sell

AMP = FMP Correct Hold

Yield To Maturity A. Current Yield

Current Yield refers to return an investor earns if

invest in the bond at Prevailing market price

Current Yield = (Interest / Market Price) x 100

Coupon rate x Face value

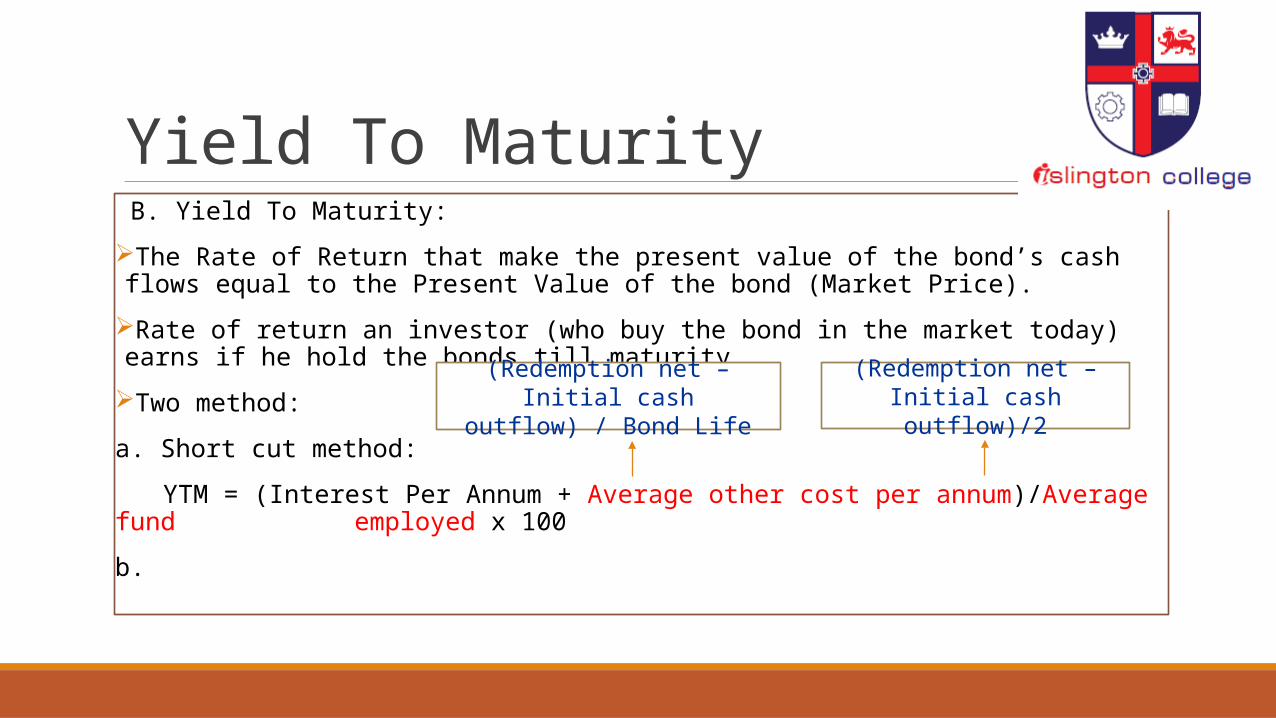

Yield To Maturity B. Yield To Maturity:

The Rate of Return that make the present value of the bond’s cash flows equal to the Present Value of the bond (Market Price).

Rate of return an investor (who buy the bond in the market today) earns if he hold the bonds till maturity.

Two method:

a. Short cut method:

YTM = (Interest Per Annum + Average other cost per annum)/Average fund employed x 100

b.

(Redemption net – Initial cash outflow) / Bond Life

(Redemption net – Initial cash outflow)/2

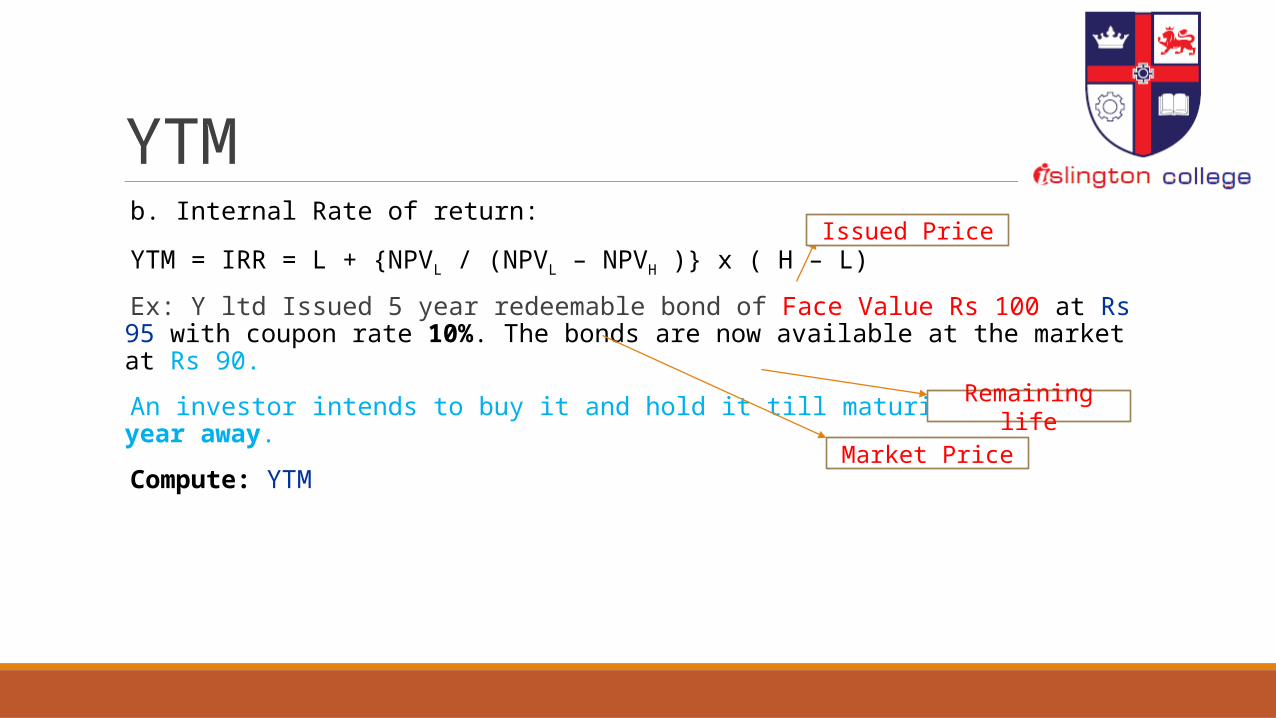

YTM b. Internal Rate of return:

YTM = IRR = L + {NPVL / (NPVL – NPVH )} x ( H – L)

Ex: Y ltd Issued 5 year redeemable bond of Face Value Rs 100 at Rs 95 with coupon rate 10%. The bonds are now available at the market at Rs 90.

An investor intends to buy it and hold it till maturity which is 4 year away.

Compute: YTM

Issued Price

Market Price

Remaining life

YTM…..

So We Have:L = 13%H = 14%H - L = ( 14 - 13 ) = 1%

NPV (L) = 1.08NPV (H) = -1.65NPV (L) - NPV (H) = 1.08 - (-1.65) = 2.73

YTM = L + { NPV (L) / (NPV(L) -NPV (H) )} x (H -L ) = 13 % + ( 1.08 / 2.73 ) x 1% = 13.39 %

Lower Rate (L) 13Higher Rate (H) 14

No of Years 4

Year Invest Interest Cash Flow PVF @ L PV @ L PVF @ H PV @ H0 (90.00) - (90.00) 1.00 (90.00) 1.00 (90.00) 1 - 10.00 10.00 0.88 8.85 0.88 8.77 2 - 10.00 10.00 0.78 7.83 0.77 7.69 3 - 10.00 10.00 0.69 6.93 0.67 6.75 4 100.00 10.00 110.00 0.61 67.47 0.59 65.13

NPV(L) 1.08 NPV(H) (1.65)

Zero Coupon BondDefinition:

Sold at a discount to face value

There is no coupon payment (and so, no reinvestment risk!).

Therefore the bondholders only receive the face value back

at the maturity date

Duration is equal to maturity

Maturity and amount are known

Value : PV of Cash flow

Po = M / ( 1 + r ) ^ n

Yield Curve Yield Curve is a graphical representation of YTM for different maturities period.

Normally, we plot YTM on Y – axis & Maturities period on X – Axis:

87.77.5

76.7

5.95.4

4.64

0

1

2

3

4

5

6

7

8

9

0 2 4 6 8 10 12 14

Maturities

YTM

BEST REGARDS