Introduction to Corporate Finance. Corporate Finance and the Financial Manager.

Upload

koshicatamangCategory

view

307download

0

1. WHAT IS CORPORATE FINANCE?2. FINANCE IN THE ORGANIZATIONAL

STRUCTURE OF A FIRM2.1 ORGANIZATION OF FINANCE FUNCTION2.2 FINANCIAL MANAGER

3. FINANCE FUNCTIONS3.1 EXECUTIVE FINANCE FUNCTION3.2 ROUTINE FINANCE FUNCTION

4. GOALS OF CORPORATE FINANCE4.1 PROFIT MAXIMIZATION4.2 LIMITATIONS OF PROFIT MAXIMIZATION4.3 WEALTH MAXIMIZATION4.4 LIMITATIONS OF WEALTH MAXIMIZATION

5. CORPORATE FINANCE AND RELATED DISCIPLINES5.1 RELATIONSHIP WITH ECONOMICS5.2 RELATIONSHIP WITH ACCOUNTING

5.3 RELATIONSHIP WITH MATHEMATICS6. THE AGENCY PROBLEM

6.1 AGENCY6.2 AGENCY PROBLEMS BETWEEN SHAREHOLDERS AND

MANAGERS6.3 RESOLVING CONFLICTS BETWEEN SHAREHOLDERS AND MANAGERS6.4 AGENCY PROBLEMS BETWEEN SHAREHOLDERS AND

CREDITORS6.5 RESOLVING CONFLICTS BETWEEN SHAREHOLDERS AND CREDITORS

7. DEVELOPMENT OF CORPORATE FINANCE8. MEET THE TEAM9. REFERENCES

“Corporate Finance is the areaof finance dealing with thesources of funding and the capitalstructure of corporations and theactions that managers take toincrease the value of the firm tothe shareholders, as well as thetools and analysis used to allocatefinancial resources.”- Wikipedia

Corporate Finance is the management of financial resources of a business

entity.

Corporate Finance is not only concerned with financing decision, but also with investment and current management decisions.

Corporate Finance is about..

• The management of finance differs according to the organization

- Small family run firms- Large companies

• Authority – Responsibility relationship among people involved in finance functions in an organization • Division of work• Helps avoid confusions on roles and responsibilities of employees, duplication and overlapping of activities

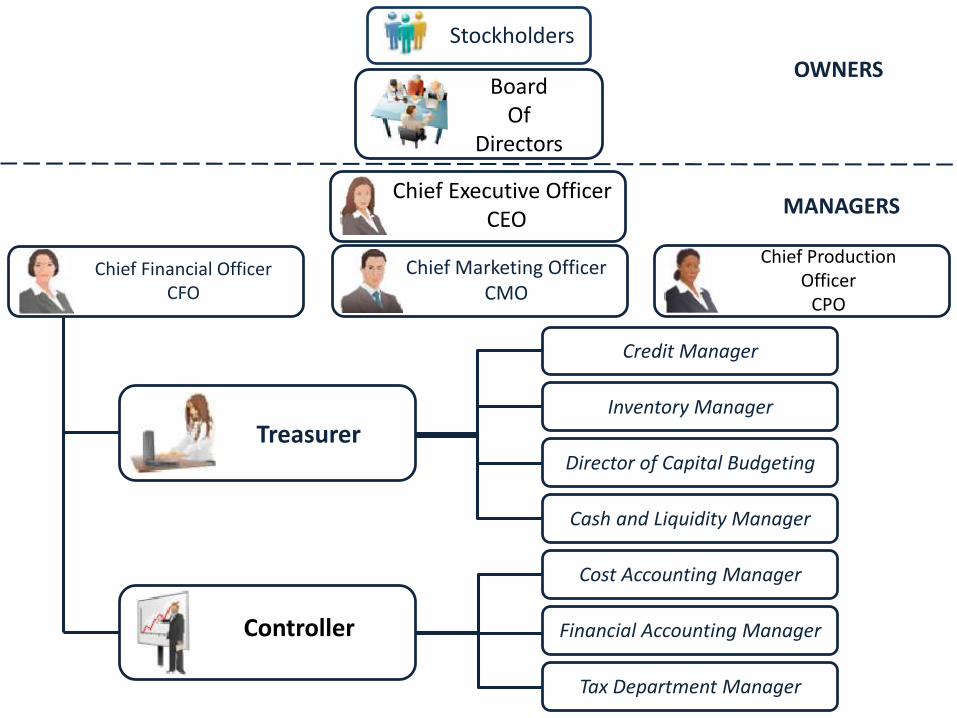

Stockholders

BoardOf

Directors

Chief Executive OfficerCEO

OWNERS

Chief Marketing OfficerCMO

Chief Production Officer

CPO

Chief Financial OfficerCFO

Treasurer

Controller

MANAGERS

Credit Manager

Inventory Manager

Director of Capital Budgeting

Cash and Liquidity Manager

Cost Accounting Manager

Financial Accounting Manager

Tax Department Manager

Also referred to as deputy director or vice – president for finance, treasurer,

controller and other managers working under them

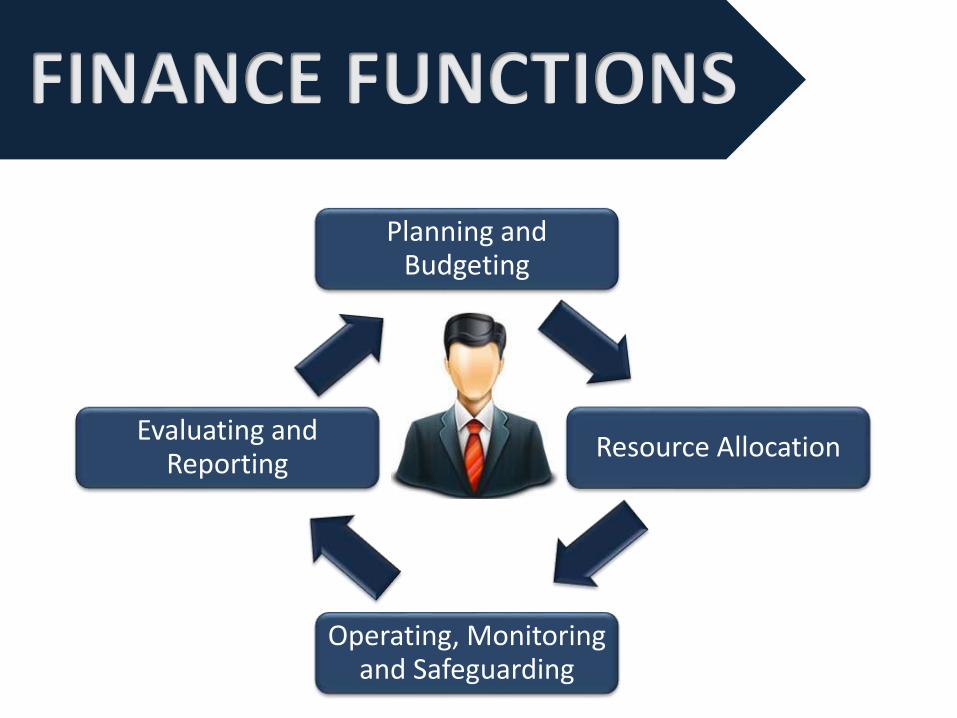

Planning and Budgeting

Resource Allocation

Operating, Monitoring and Safeguarding

Evaluating and Reporting

Also known as collection of fundsapproach, it confines the finance

functions to the procurement funds only and ignores the use of funds.

Comprehensive and universally accepted approach with the procurement of funds and it’s effective utilization.

Investment Decision

Financing Decision

Those which require managerial skills in

their planning, execution and

control

Working Capital Decision

Dividend Decision

Those which require managerial skills in

their planning, execution and

control

Also known as incidental finance functions these are performed for the effective

execution of executive finance functions which

doesn’t require specialized skills. Clerical in nature, this

involves a lot of paper work, cover procedures and

systems.

Goal is an observable and measurable end result having one or more objectives to be achieved within a more or less fixed timeframe.

• Amount and share of national income which is paid to the

owners of business• A situation where output exceeds

input, that is the value created by the use of resources is more than

the total of the input resources• Investment, financing and

dividend policy decisions of a firm should be oriented to the

maximization of profits• A yardstick by which economic

performance can be judged

• Ambiguity- Has no precise connotation and is a vague and ambiguous concept• Timing of Benefit- Ignores the differences in the time pattern of the benefits received from investment proposals or courses of action• Quality of Benefit- ignores the quality aspect of benefits associated with a financial course of action

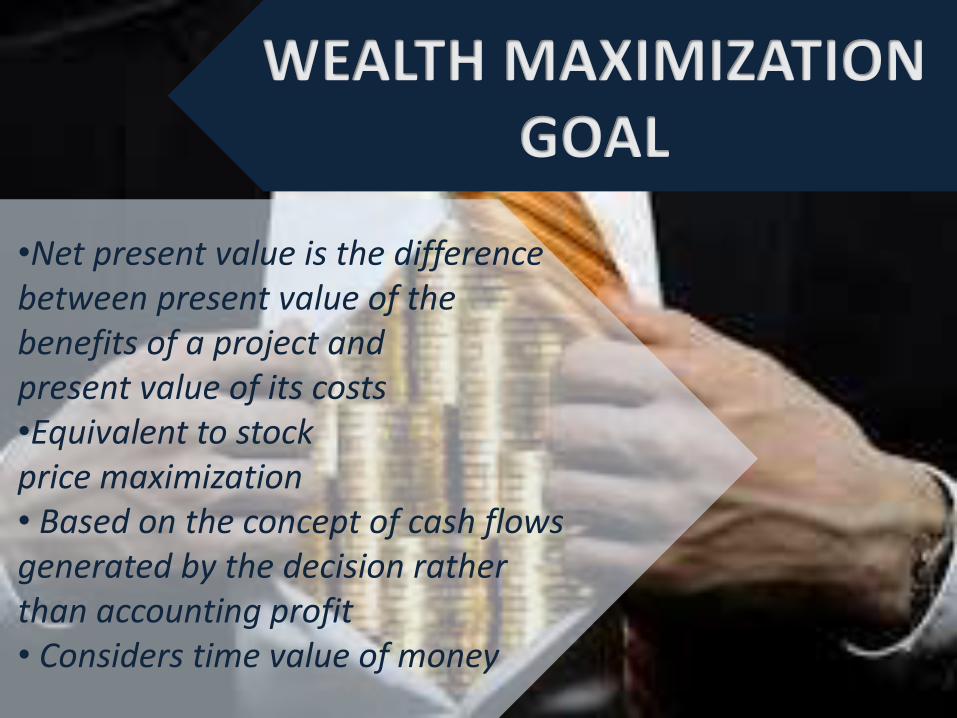

• Also known as value maximization or net present

worth maximization, it is almost universally an accepted goal of a

firm• The managers should take decisions that maximize the

shareholders' wealth or generates a net present value

•Net present value is the difference between present value of the benefits of a project and present value of its costs •Equivalent to stock price maximization • Based on the concept of cash flows generated by the decision rather than accounting profit• Considers time value of money

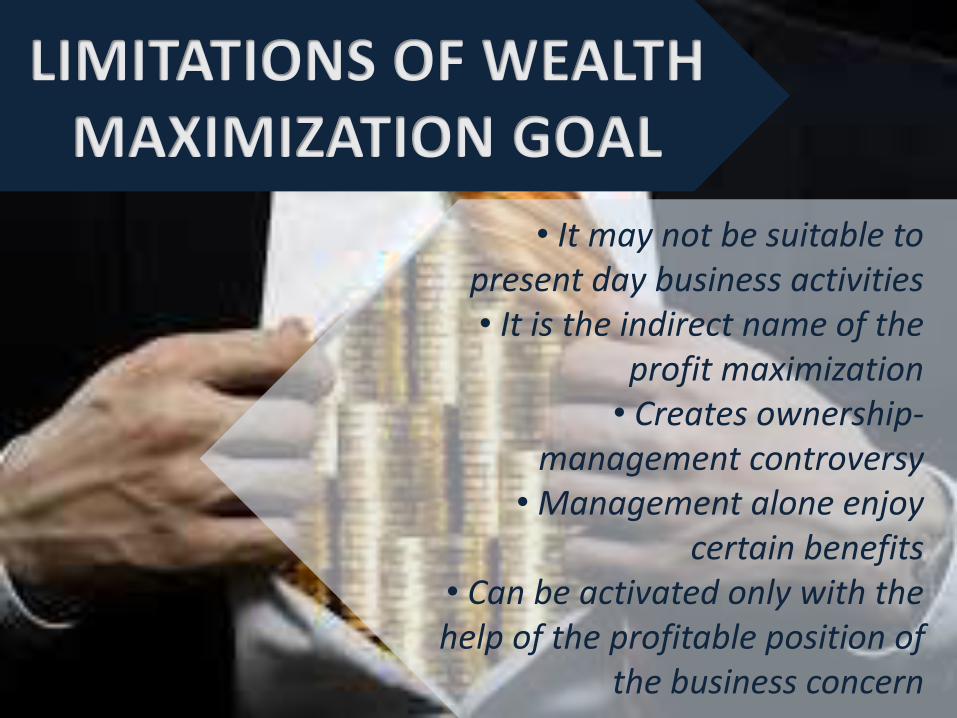

• It may not be suitable to present day business activities• It is the indirect name of the

profit maximization• Creates ownership-

management controversy• Management alone enjoy

certain benefits• Can be activated only with the help of the profitable position of

the business concern

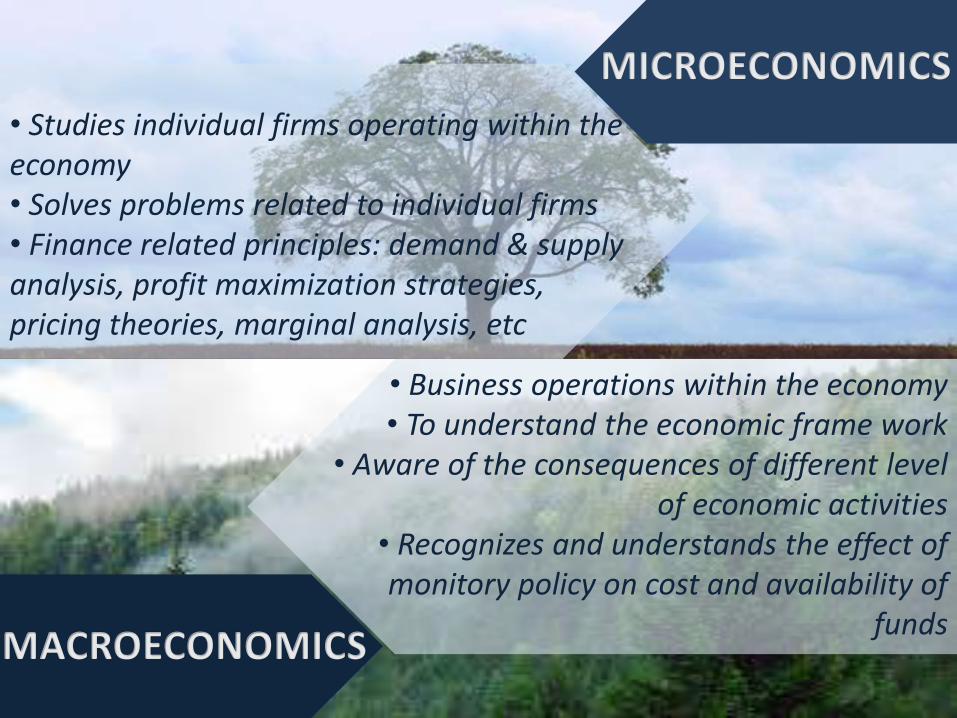

CORPORATE FINANCE AND RELATED DISCIPLINE

• Studies individual firms operating within the economy• Solves problems related to individual firms• Finance related principles: demand & supply analysis, profit maximization strategies, pricing theories, marginal analysis, etc

• Business operations within the economy • To understand the economic frame work

• Aware of the consequences of different level of economic activities

• Recognizes and understands the effect of monitory policy on cost and availability of

funds

• Systematic and comprehensive recording of financial transactions pertaining to a business• Financial manager recasts the statement prepared by accountant and generates additional data and makes decision on analysis

• Finance draws heavily on mathematics and quantitative

techniques.• Useful in complex problem solving

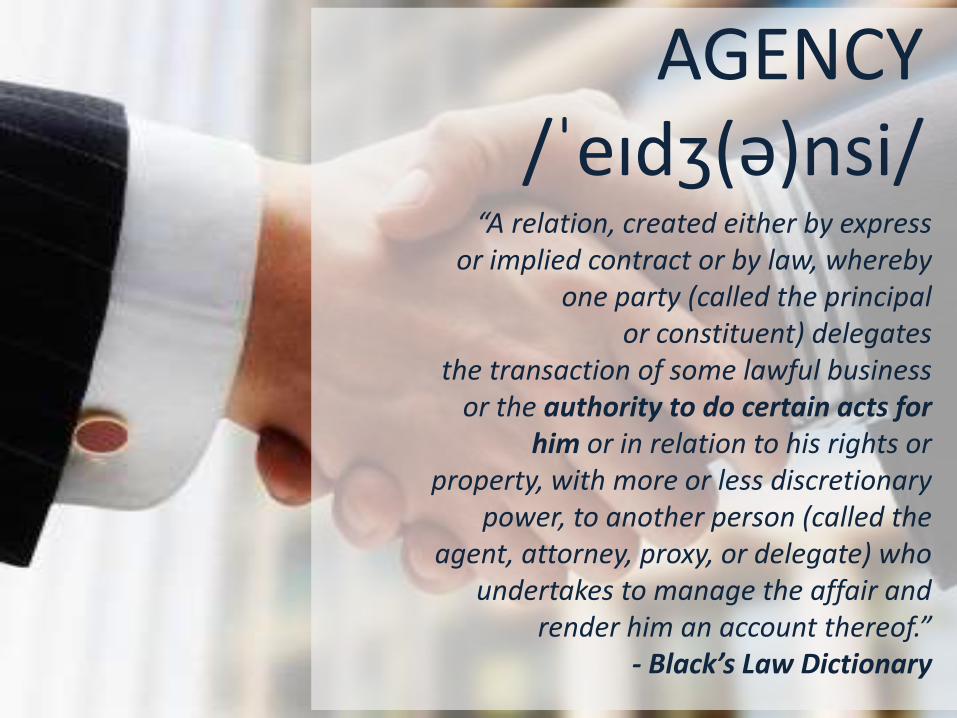

AGENCY /ˈeɪdʒ(ə)nsi/

“A relation, created either by express or implied contract or by law, whereby

one party (called the principal or constituent) delegates

the transaction of some lawful business or the authority to do certain acts for

him or in relation to his rights or property, with more or less discretionary

power, to another person (called the agent, attorney, proxy, or delegate) who

undertakes to manage the affair and render him an account thereof.”

- Black’s Law Dictionary

AGENCY PROBLEM• A problem in determining managerial accountability that arises when delegating authority to managers• Conflict of interest between the principal and the agent, or the shareholder and the manager• Shareholders are at information disadvantage as compared to the managers• It takes considerable time to see the effectiveness of decisions managers can make• Very difficult to evaluate how well the agent has performed because the agent possesses an information advantage over the principal

• In theory, managers should at in the best interest of the shareholders• In practice, managers may maximize their own wealth (in the form o f high salaries and perks) at the cost of shareholders• Buy other companies to expand power, venturing onto fraud, manipulate financial figures to optimize bonuses and stock price related options, etc

RESOLVING CONFLICTS

Managerial Compensation

Direct Intervention By Shareholders

The Threat of Firing

The Threat of Hostile Takeovers

• Shareholders through managers make decisions for shareholders value maximization by ignoring

the interest of creditors• Manager may decide to invest in

a risky project. If the project succeeds, all the benefits goes to

the shareholders and the creditors will receive only the already fixed

low rate of return. However, if the project fails creditors may have to

share the losses as well

RESOLVING CONFLICTS

Compensating Creditors for

Increased Risk

Protective Terms and Conditions for

Creditors

DEVELOPMENT OF CORPORATE FINANCE

1800• Corporate Finance as a part of Economics

1900• Rapid industrialization-new business, expansions, mergers- in the USA and Europe• Shortage of capital due to the absence of capital market• Distrust in financial statements resulting in lack of investors• Birth of finance as a separate discipline

1930THE

GREAT DEPRESSION

• Failure in real market transmits to capital market• Attention shifts from legal control to bankruptcy, reorganization and regulation of capital market

1940• Due to market downfall, focus is shifted from expansion and modernization to survival of firms• Amendments in company’s regulations and setting of accounting standards• Advanced through development of mathematical tools to cash, accounts receivables and fixed assets management

Investor’s increased confidence in

financial statements

1950• Quantitative

method of analyzing financial

problems• Development of

various financial theories

• Efficiency and regulation of

financial markets

21st

CenturyTHE

DIGITALERA

• Technological advancement• Focus on value

maximization• Globalization of

business• Increased use of information and communication

technology• Multinational

companies