Introduction to Accounting & Business CPA, MBA By Rachelle Agatha, CPA, MBA Slides by Rachelle...

56

Introduction to Accounting & Business By Rachelle Agatha, CPA, MBA Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

-

Upload

charles-tyler -

Category

Documents

-

view

244 -

download

0

Transcript of Introduction to Accounting & Business CPA, MBA By Rachelle Agatha, CPA, MBA Slides by Rachelle...

Introduction to Accounting & Business

By Rachelle Agatha, CPA, MBA

Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

2

2. Summarize the development of accounting principles and relate them to practice.

3. State the accounting equation and define each element of the equation.

After studying this lecture material, you should be able to:

1. Describe the nature of a business and the role of ethics and accounting in business.

3

4. Describe and illustrate how business transactions can be recorded in terms of the resulting change in the basic elements of the accounting equation.

5. Describe the financial statements of a proprietorship and explain how they interrelate.

4

Describe the nature of a business and the

role of ethics and accounting in

business.

Objective 1

5

Proprietorship Partnership Corporation Limited liability

company

Common Forms of Business Organizations

6

Service Merchandiser Manufacturing

Types of Businesses

7

Comprises 70% of business organizations in the United States.

Requires low cost of organizing.

Is limited to financial resources of the owner.

Is used by small businesses.

A proprietorship is owned by one individual and—

8

Comprises 10% of business organizations in the United States.

Combines the skills and resources of more than one person.

A partnership is similar to a proprietorship except that it is owned by two or more individuals and—

9

Generates 90% of the total dollars of business receipts received.

Comprises 20% of the businesses.

A corporation is organized under state or federal statues as a separate legal taxable entity and—

Continued

10

Includes ownership divided into shares of stock, sold to shareholders (stockholders).

Is able to obtain large amounts of resources by issuing stock.

Is used by large businesses.

11

Is a popular alternative to a partnership.

Has tax and liability advantages to the owners.

A limited liability company (LLC) combines attributes of a partnership and a corporation in that it is organized as a corporation. However, a limited liability corporation can elect to be taxed as a partnership and—

12

A business stakeholder is a person or entity

having an interest in the economic

performance and well-being of a business.

13

Capital market stakeholders provide the

major financing for the business in order for the business to begin and

continue its operations.

14

Product or service market stakeholders include customers who purchase the business’s products or services as well as the vendors who

supply inputs to the business.

15

Government stakeholders have an interest in the economic

performance of a business. City, county, state, and

federal governments collect taxes from businesses

within their jurisdiction.

16

Internal stakeholders include individuals

employed by the business. Managers have an incentive to maximize the economic

value of the business. Employees have an interest because their jobs depend

on it.

17

The moral principles that guide the conduct of individuals are called

ethics.

1. Individual character2. Firm culture3. Laws and enforcement

18

Accounting can be defined as an information

system that provides reports to stakeholders

about the economic activities and condition of

a business.

1-1

19

The process by which accounting provides information to business stakeholders is as follows: Identify stakeholders.

Assess stakeholders’ information needs.

Design the accounting information system to meet stakeholders’ needs.

Record economic data about business activities and events.

Prepare accounting reports for stakeholders.

20

21

Financial accounting is primarily concerned with the recording and reporting of economic data and

activities for a business.

Managerial accounting uses both financial accounting and estimated data to aid management in running

day-to-day operations and in planning future operations.

22

Accountants employed by a business firm or a not-for-profit

organization are said to be employed in private accounting.

Accountants and their staff who provide services on a fee basis are

said to be employed in public accounting.

23

Summarize the development of

accounting principles and relate them to

practice.

Objective 2

24

The business entity concept or principle

limits the economic data in the accounting system to data related directly to

the activities of the business.

25

The cost concept or principle is the basis for

entering the exchange price, or cost of an acquisition in

the accounting records.

26

The objectivity concept or principle requires that the accounting

records and reports be based upon objective

evidence.

27

The unit of measure concept or principle requires that economic

data be recorded in dollars.

28

On March 1, Smith's Repair Service extended an offer of $115,000 for land that had been priced for sale at $135,000. On March 15, Smith's Repair Service accepted the seller’s counter-offer of $125,000. On April 1, the land was assessed at a value of $100,000 for property tax purposes. On May 1, Smith's Repair Service was offered $150,000 for the land by a national retail chain. At what value should the land be recorded in Smith Repair Service’s books (general ledger)?

$125,000. Under the cost concept, the land should be recorded at the cost to Smith's Repair Service.

29

State the accounting

equation and define each

element of the equation.

Objective 3

ASSETS = LIABILITIES + OWNERS EQUITY

Slide by Rachelle Agatha, CPA

ACCOUNTING EQUATION

ASSETS LIAB + OE

31

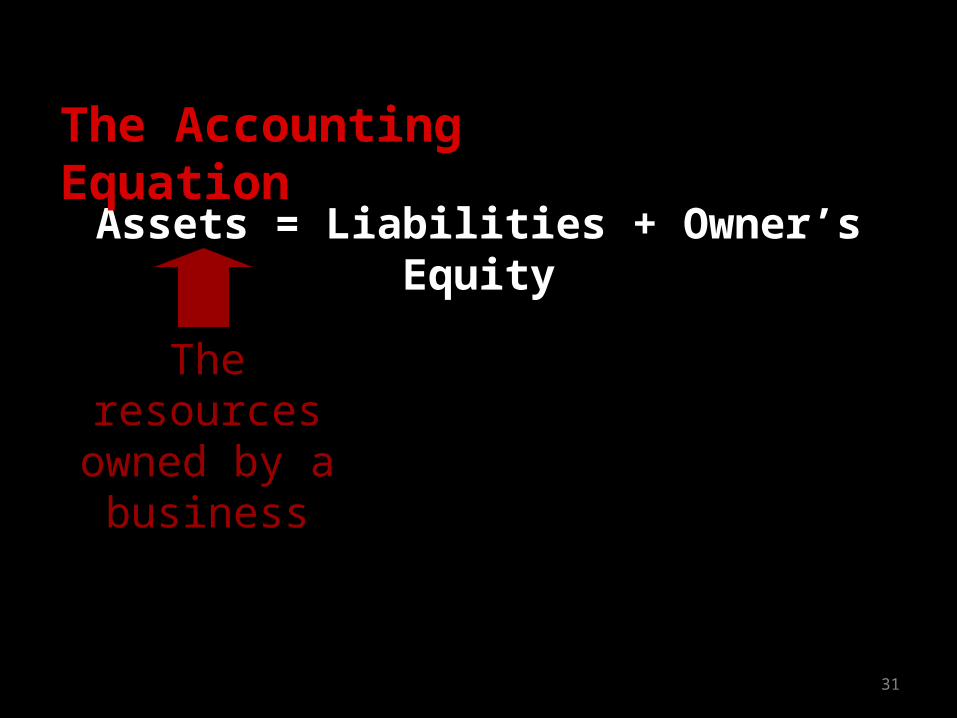

Assets = Liabilities + Owner’s Equity

The resources

owned by a business

The Accounting Equation1-3

32

The rights of the

creditors, which

represent debts of the

business

Assets = Liabilities + Owner’s Equity

The Accounting Equation 1-3

33

The rights of the owners

Assets = Liabilities + Owner’s Equity

The Accounting Equation 1-3

34

Assets = Liabilities + Owner’s Equity

1-3

ASSETS = LIABILITIES + OWNERS EQUITY

850,000$ = 250,000$ + ?(250,000)$ = (250,000)$ +

600,000$ = -$ + ?

850,000$ = 250,000$ + 600,000$

At the end of 12/31/08, Smith's Repair Service had Assets of $850,000 and Liabilities of $250,000. How much equity did Smith's Repair Service have?

35

Describe and illustrate how business

transactions can be recorded in terms of the resulting change in the basic elements of the accounting equation.

Objective 41-4

36

A business transaction is an economic event or condition that directly changes an entity’s

financial condition or directly affects its results of

operations.

1-4

37

.

1-4

= Liab +

Accts. Accts. Gilmore, Gilmore Fees AllCash + Rec. + Supplies = Payable Capital - Drawing + Earned - Exp.

Bal. 24,620$ 2,250$ 380$ 550$ 25,000$ (1,000)$ 6,750$ (4,050)$

27,250 = 550 + 26,700

Assets Owner's Equity

Slide by Rachelle Agatha, CPA

38

.

1-4

Slide by Rachelle Agatha, CPA

+ Initial Capital Investment+ Revenue- Expense- Withdrawls= Ending Equity

Owner's Equity

39

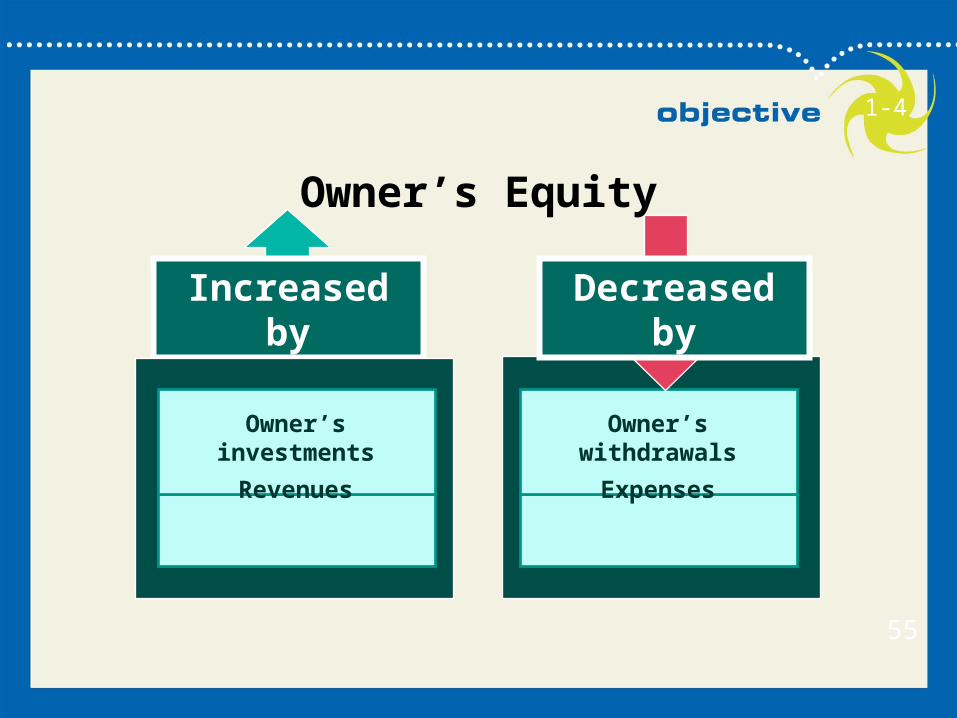

Owner’s withdrawals

Expenses

Decreased by

Owner’s Equity

Increased by

Owner’s investments

Revenues

55

1-4

40

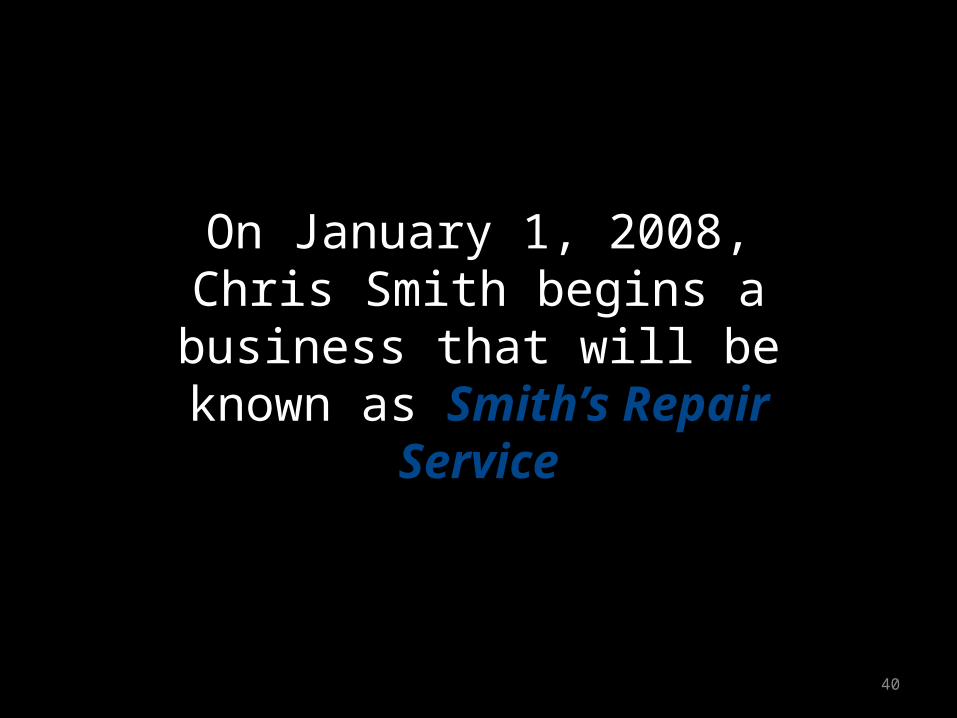

On January 1, 2008, Chris Smith begins a business

that will be known as Smith’s Repair Service

41

Chris Smith invests $25,000 into the business

Assets Owner’s Equity=

=

Chris Clark, Capital

25,000Investment by Chris Clark

Cash25,00

0

42

Describe the financial statements of a

proprietorship and explain how they

interrelate.

Objective 5

1-5

43

Accounting reports, called financial

statements, provide summarized

information to the owner.

1-5

44

The income statement is a summary of the

revenue and expenses for a specific period of

time, such as a month or a year.

45

A statement of owner’s equity is a summary of

the changes in the owner’s equity that have occurred during a specific

period of time.

1-5

46

1-5

Revenue 153,750$ Expenses:

Wages 20,775$ Rent 48,000Depreciation 10,800Supplies 9,375Utilities 1,065Insurance 1,800Miscellaneous 705 92,520

Net income 61,230$

J . Terrier Capital, J anuary 1, 2008 75,000$ Net income 61,230Less: Drawing (15,000)Increase in owner's equity 46,230J Terrier Capital, December 31, 2008 121,230$

For the Year Ended December 31, 2008

For the Year Ended December 31, 2008

Statement of Owner's Equity

San Diego Designer Puppy Store and CoutureIncome Statement

San Diego Designer Puppy Store and Couture

47

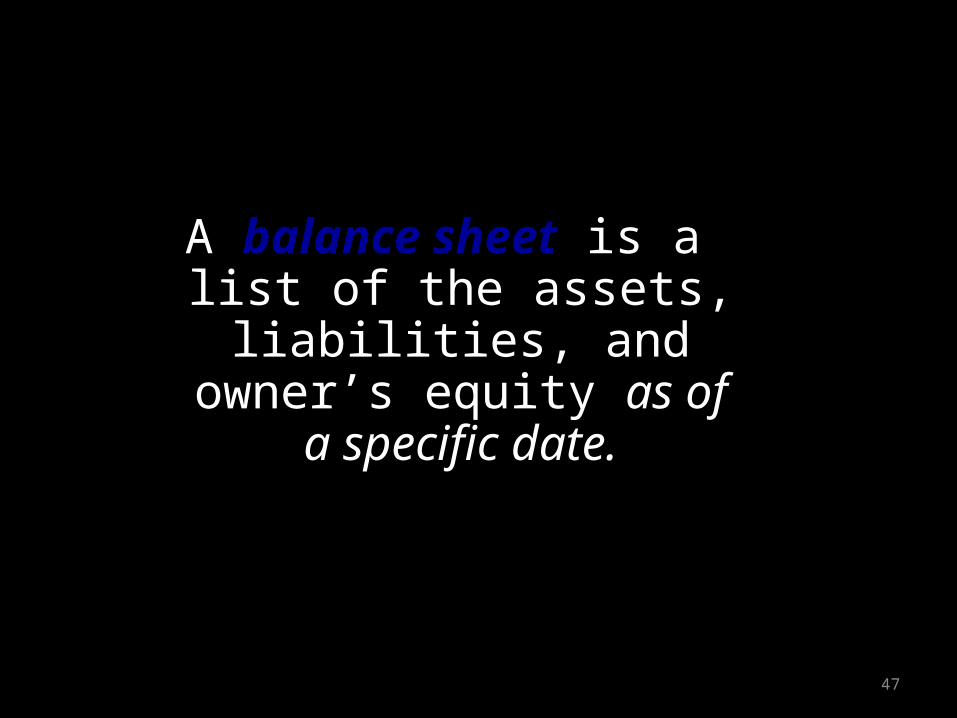

A balance sheet is a list of the assets,

liabilities, and owner’s equity as of a specific

date.

1-5

48

1-5J . Terrier Capital, J anuary 1, 2008 75,000$ Net income 61,230Less: Drawing (15,000)Increase in owner's equity 46,230J Terrier Capital, December 31, 2008 121,230$

Assets Liabilities Cash $12,000 Accounts payable $15,000 Supplies 1,300 Wages payable 4,500 Prepaid insurance 900 Current Liabilities $19,500 Inventory 16,000 Current assets $30,200 Notes Payable 25,000$

Equipment $182,865 Total Liabilities $44,500 Acc. Depreciation 47,335 Fixed assets $135,530 J . Terrier Capital 121,230$

Total Liabilities andTotal assets $165,730 Owner's Equity $165,730

San Diego Designer Puppy Store and CoutureBalance Sheet

December 31, 2008

For the Year Ended December 31, 2008Statement of Owner's Equity

San Diego Designer Puppy Store and Couture

49

A statement of cash flows is a summary of the

cash receipts and payments for a

specific period of time.

1-5

50

The income statement reports the revenues and expenses for a period of time based on the

matching concept. This concept is applied by matching the expenses with the revenue generated during a period by

those expenses.

1-5Income Statement

51

The excess of revenue over the expenses is called net income or

net profit. If the expenses exceed the

revenue, the excess is a net loss.

1-5

52

The statement of owner’s equity reports

the changes in the owner’s equity for a period of time. It is prepared after the income statement.

1-5Statement of Owner’s Equity

53

The balance sheet reports the amounts

of a firm’s assets, liabilities, and

owner’s equity at the end of a specific

period.

1-5Balance Sheet

54

The income statement and the statement of owner’s equity are interrelated.

Net income or net loss appears on both

statements.

1-5Interrelationships Among Financial Statements

55

The statement of owner’s equity and the balance sheet are interrelated.

The owner’s capital at the end of the period on the

statement of owner’s equity also appears on the balance

sheet as owner’s capital.

1-5

56

The balance sheet and the statement of cash flows are interrelated.

The cash on the balance sheet also appears as the end-of-

period cash on the statement of cash flows.

1-5