Introduction 6.2 Methodology 6.2.1 Statistical Analysis 6.2.2 Financial Analysis...

55

166 6 : Capital Budgeting and Selected Variables 6.1 Introduction 6.2 Methodology 6.2.1 Statistical Analysis 6.2.2 Financial Analysis 6.3 Conclusion

Transcript of Introduction 6.2 Methodology 6.2.1 Statistical Analysis 6.2.2 Financial Analysis...

166

6 : Capita l Budget ing and Selected Variables

6.1

Introduction

6.2 Methodology

6.2.1 Statistical Analysis

6.2.2 Financial Analysis

6.3 Conclusion

167

Chapter 6 : Capital Budgeting and Selected Variables

6.1 Introduction:

The objective of the data analysis of the companies hereafter is to measure the extent of

relationship the investment decisions in plant and machinery of the company and sales

have in explaining the variation in its operating income.

6.2 Methodology:

6.2.1 Statistical Analysis:

A linear regression analysis1 of the financial data of the company for the last five years

(for some companies four years and for one company three years due to unavailability of

data) has been carried out using a statistical SPSS program.

To understand the significance of capital budgeting decisions, operating income of the

firm has been used as dependent variable to develop a best possible regression model with

Plant and Machinery (P&M) and Sales as independent variables. These variables have

been selected since capital budgeting practices are maximum used for investment in plant

and machinery. Thus the researcher has attempted to use a linear regression model, to

understand how these variables are significant in explaining the variation in the operating

income of the company.

The following tables give the results generated by SPSS programme.

1. Table 6.1… Descriptive Statistics showing Mean and Standard Deviation for the

variables selected.

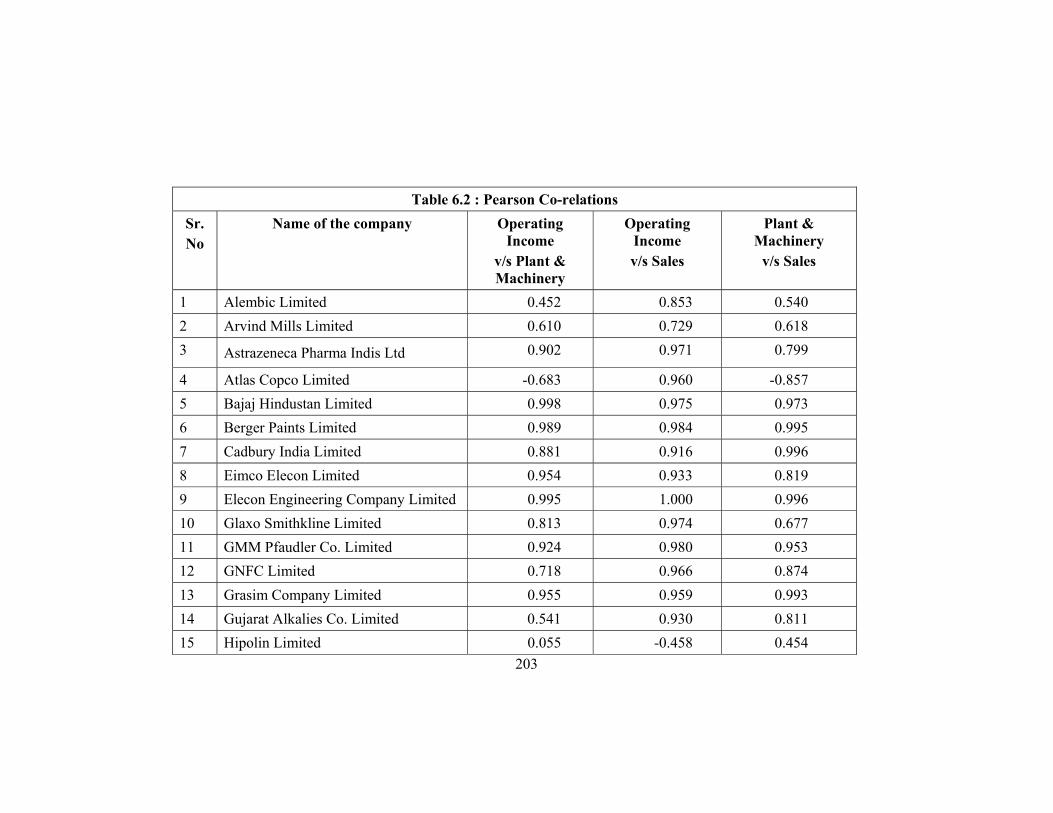

2. Table 6.2… Pearson's Co-relations showing the strength of the relation between

the variables.

1 Regression analysis is a general process of predicting one variable from another by statistical means, using available data. Our goal in carrying out regression analysis is to develop a statistical model that can be used to predict the values of independent variables.

168

3. Table 6.3… Statistical data showing various Beta (β ) co-efficient for the

variables selected, value of R2, and p values for the estimated

model.

On carrying out regression analysis for the financial data available, following linear

regression model have been used, which checks the significance of investment in Plant

and Machinery and Sales of the company have in explaining the operating income of the

company.

iXXY εβββ +⋅+⋅+= 22110

Where, Y = Dependent Variable, Operating income in our study

0β = A Constant term i.e. the intercept value for the straight line Model.

1β = Beta Co-efficient for 1X variable,

1X = variable 1X , Plant and Machinery (P&M) in our study

2β = Beta Co-efficient for the 2X variable

2X = variable 2X , Sales in our study

ε = Estimate for error, measures the variability, or scatter of the

Observed values around the regression line.

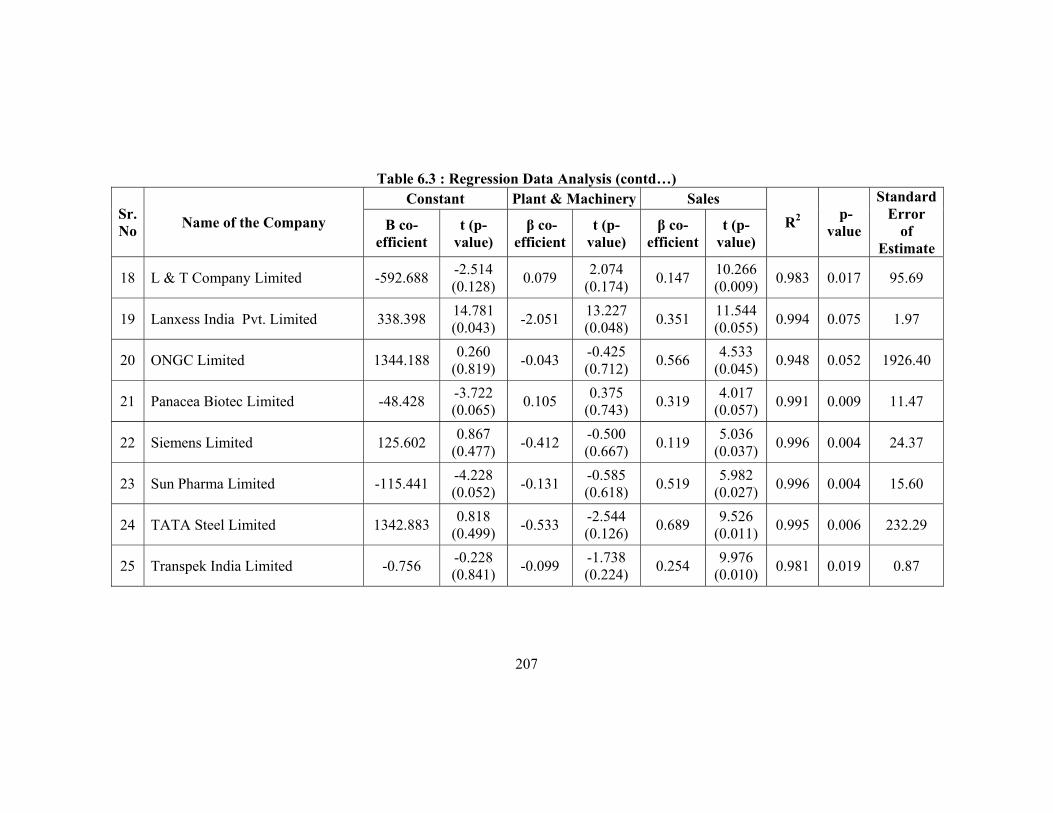

Table 6.3, gives values of β co-efficient and standard estimate of error values for each

company. The regression model that would be derived by reading the values of the co-

efficient from the table 6.3, is provided below for one of the company, GMM Pfaudler

Limited :

169

Operating Income = -3.399 -0.166 P&M + 0.252 Sales + ε 2

Similar model can be estimated for other companies under study through the values of co-

efficient available in Table 6.3.

Further, it would be necessary to check how well the regression model explains the

variation of the dependent variable Y. The co-efficient of determination (R2) 3 is the

primary way to measure the extent, or strength, of the association that exists between two

variables, 1X and 2X . Table 6.3 gives the value of R2 for each company.

The Co-efficient of Determination value R2 for the above regression model of GMM

Pfaudler Limited is 0.962, which denotes that almost 96 % variation in operating income

is explained by the two variables P&M and Sales. In other words, it can be said that the

capital budgeting decisions for Plant and Machinery and the growth in sales together

explains almost 96% variation in the operating income achieved by the company.

As seen in Table 6.3, the R2 for almost 90 % of the companies is around 95 %. Thus, it can be

said that capital budgeting decisions leading to investment in plant and machinery and sales

together influence almost 95 % variation in the operating income of a company.

Further, to support that the regression model achieved is fully significant, t-test and F

ratio along with p-value4 have been evaluated for each company and the values are

provided in Table 6.3.

For, GMM Pfaudler Limited F-statistic is 25.448 together with a 0.038 p value, which

is less than 5 % conventional level, suggests that the model estimated as a whole is fully

significant in explaining the variation in operating income resulting from decisions taken

for investment in Plant and Machinery and growth in sales.

2 Estimating equations are not perfect predictors. The values of operating income derived through the model are only an estimate. Even so, the regression gives us a rough idea of what to expect for the coming year. 3 Co-efficient of determination ( R2) measures the strength of the linear relationship between two variables. The value of R2 is equal to +1 whenever the regression model is perfect estimator. Thus an R2 value close to 1 indicates a strong correlation between the variables. 4 P-value, i.e. Probability value is the largest significance level at which we would accept the hypothesis. Thus, a p-value of model if within significance level of 0.05 denotes that the regression model as a whole is highly (95 %) significant.

170

Also through Pearson’s correlation5 analysis as shown in Table 6.2, it can be seen that the

variables Plant and Machinery, Sales and Operating Income are also significantly

correlated to each other.

It would be appropriate at this point to make a note that the researcher has limited the

analysis to estimate a linear model only. However in some cases where the model is not

significant, further analysis can be carried out to estimate a more significant model, which

may be a non-linear model or curvilinear model or any other. The focus of this research is

on evaluating the practices of the Capital Budgeting for evaluation of investment

proposals in the corporate sector in India and not on identifying the relevant model for

understanding the relationship between these variables.

6.2.2 Financial Analysis:

Further, the analysis has also been carried out using ratio analysis. The following ratios

have been calculated to identify the need and relevance of capital budgeting decisions for

the firms under study.

1. Total Assets Efficiency Ratio

2. Net Profit Margin

3. Earning Power Ratio

4. Fixed Asset Efficiency Ratio

5. Plant & Machinery Turnover Ratio

6. Plant & Machinery to Gross Fixed Asset Ratio

5 Pearson correlation indicates the strength and direction of a linear relationship between two random variables. In general statistical usage, correlation or co-relation refers to the departure of two variables from independence. The correlation is 1 in the case of an increasing linear relationship, −1 in the case of a decreasing linear relationship, and some value in between in all other cases, indicating the degree of linear dependence between the variables. The closer the coefficient is to either −1 or 1, the stronger the correlation between the variables.

171

The total assets efficiency ratio, the fixed asset efficiency ratio and the plant & machinery

turnover ratio explain how efficiently firms are using its assets particularly plant and

machinery which is useful for production and ultimate sales (income) for the firm.

Addition in plant and machinery/fixed assets require the exercise of capital budgeting. An

improvement in the efficiency ratio indicates effective use of firm’s assets. The Du Pont

Company began to use a particular approach to ratio analysis to evaluate the firm’s

effectiveness in 1919. One variation of this Du Pont approach has special relevance to

understanding a firm’s ROI. According to the approach, when we multiply the net profit

margin of the firm by the total asset turnover, we obtain the return on investment (ROI) or

earning power on total assets. Neither the net profit margin nor the total asset turnover

ratio by itself provides an adequate measure of overall effectiveness. The net profit

margin ignores the utilization of assets, and the total asset turnover ratio ignores

profitability on sales. The return on investment (ROI) or earning power resolves these

shortcomings. An improvement in the earning power of the firm will result if there is an

increase in turnover on assets, an increase in the net profit margin, or both.6

The following are the results of the analysis carried out for various companies under

study.

6 Van Horne James C. and Wachowicz, Jr. John M.,Fundamentals of Financial Management (Eleventh Ed.), Prentice Hall of India Private Limited, 2002,pg. 147

172

1. Alembic Limited:

The decreasing efficiency ratio calculated below indicates that the assets of the company

are underutilized over a period of last five years. The company’s total investment in plant

and machinery is also reducing year by year. The plant & machinery turnover ratio has

reduced in the year 2004, 2005, and 2006 but it has improved in the year 2007. Thus, the

improvement in net profit margin and earning power ratio indicate that the increase is due

to some other reasons rather than asset efficiency.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.08 1.09 0.90 0.95 0.79

Net Profit Margin (%) 100×

SalesPAT

5.56% 5.09% 9.08% 11.78% 9.78%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 5.99% 5.54% 8.15% 11.14% 7.69%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 1.56 1.40 1.14 1.26 1.28

Plant & Machinery Turnover Ratio (times)

MachineryPlantSales

& 1.84 1.63 1.49 1.69 1.90

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

84.71% 86.06% 76.43% 74.59% 67.43%

173

2. Arvind Mills Ltd.

It can be seen that the assets of the company are underutilized over a period of last five

years as the ratio is decreasing and it is significantly less than 1. The company’s total

investment in plant and machinery has also significantly decreased in the year 2007 in

comparison to the year 2003 to 2006 but the plant and machinery turnover ratio has

improved over a period of five years except in the year 2004 and 2006. The net profit

margin has slightly improved in 2005 and 2006 compared to 2004, however, compared to

2003 it is not healthy. In last year of analysis i.e. 2007 it is lowest. This is mainly because

of substantial increase in material consumption cost and sales expenses. Thus, if we put

all these observations together it indicates that the company need to apply sound

techniques of capital budgeting which can help in taking right decision for fixed assets

investment and in turn increasing sales and income.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.58 0.49 0.53 0.44 0.49

Net Profit Margin (%) 100×

SalesPAT

8.33% 6.64% 7.48% 7.83% 6.46%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 4.87% 3.27% 3.93% 3.46% 3.16%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 0.76 0.70 0.77 0.71 0.64

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

1.22 1.12 1.24 1.11 1.31

Plant & Machinery to GFA Ratio (%) 100&

×AssetsGrossFixed

MachineryPlant62.29% 62.78% 61.88% 64.19% 48.99%

174

3. Astrazeneca Pharma India Ltd.

The company is generally investing more than 50% in plant and machinery out of its total

investment in fixed assets. The asset efficiency ratio is decreasing over a period of four

years except in the year 2005 but the gross fixed assets efficiency ratio and the plant and

machinery turnover ratio has improved continuously indicating use of sound capital

budgeting techniques. This is reflected in terms of increase in net profit margin and

earning power but both the ratios are slightly decreased in the year 2004 though the fixed

asset efficiency ratio is increasing in that year also which may be due to decrease in sales.

Ratio Formula 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales

1.34 1.26 1.38 1.21

Net Profit Margin (%) 100×

SalesPAT

12.50% 12.21% 17.47% 16.60%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 16.80% 15.38% 24.08% 20.05%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 3.03 3.10 3.32 3.70

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 4.97 5.03 5.46 6.63

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

61.00% 61.54% 60.71% 55.79%

175

4. Atlas Copco (India) Ltd.

There is a slight decrease in the asset efficiency ratio in the year 2004. The asset

utilization of the company is moderately improving over a period of last four years. The

company’s proportionate investment in plant and machinery is substantially less from the

year 2004 onwards and it has major investment in intangible asset of the company in

these years. Thus almost three times increase in plant and machinery turnover ratio may

be due to decreasing investment in plant and machinery. The poor asset utilization has

been reflected in terms of decrease in net profit margin and earning power ratio.

Ratio Formula 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.41 1.13 1.50 1.50

Net Profit Margin (%) 100×

SalesPAT

10.42% 5.26% 8.17% 9.00%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 14.64% 5.93% 12.27% 13.48%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

4.32 2.31 3.11 3.64

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

7.98 11.89 16.41 22.86

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

54.12% 19.46% 18.96% 15.94%

176

5. Bajaj Hindusthan Ltd.

The efficiency ratios calculated below indicate that the assets of the company are under

utilized substantially over a period of five years. The company is usually investing in

plant and machinery more than 50% except in the year 2005 and 2006. The fixed asset

efficiency ratio is decreasing significantly indicating that increase in investment in fixed

asset is more than increase in sales. The net profit margin and earning power ratio have

substantially increased except in the year 2007 where both these ratios have decreased.

This is due to other income and reduction in employee cost and other administrative cost.

It is observed that this improvement has no link with asset utilization of the company. But

the earning power ratio of the company would have improved further if the company

would have used sound capital budgeting techniques for its investment in fixed assets

especially plant and machinery.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 2.48 1.24 0.92 0.69 0.45

Net Profit Margin (%) 100×

SalesPAT

1.00% 6.19% 11.57% 15.74% 12.50%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 2.48% 7.67% 10.65% 10.84% 5.61%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.86 0.78 0.41 0.36 0.48

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 2.92 1.40 1.05 0.92 0.76

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

63.58% 55.74% 39.22% 38.56% 63.08%

177

6. Berger Paints India Ltd.

The asset efficiency ratio has decreased continuously over a period of five years. The

fixed asset efficiency ratio is also decreasing year by year but which has increased in the

year 2007. The company is investing more than fifty percent in plant and machinery and

the plant and machinery turnover ratio is fluctuating during this period requiring sound

capital budgeting decisions. The earning power ratio of the firm has also improved

moderately indicating significance of asset efficiency and net profit margin.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 2.20 2.16 2.18 2.12 2.10

Net Profit Margin (%) 100×

SalesPAT

4.99% 5.71% 5.49% 6.27% 6.26%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 11.00% 12.32% 11.95% 13.31% 13.14%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

4.97 4.90 4.74 4.73 5.13

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 9.30 9.41 9.32 8.85 9.37

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

53.48% 52.08% 50.85% 53.42% 54.76%

178

7. Cadbury India Limited

The efficiency ratio calculated has reduced from the year 2003 onwards except in the year

2006 where it has slightly improved indicating little improvement in the use of assets.

Even the fixed asset efficiency ratio has also decreased continuously over the years.

Though the investment in plant and machinery of the total investment in gross fixed

assets has reduced, the plant and machinery turnover ratio is continuously improving

which indicates that the company has used sound capital budgeting techniques at least for

investment in plant and machinery. One can even observe a small increase in Net Profit

Margin and earning power ratio also.

Ratio Formula 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.63 1.54 1.52 1.63

Net Profit Margin (%) 100×

SalesPAT

5.52% 5.22% 4.57% 5.98%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 8.97% 8.02% 6.96% 9.78%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

2.47 2.39 2.37 2.24

Plant & Machinery Turnover Ratio (times) MachineryPlant

Sales&

3.14 3.19 3.28 3.46

Plant & Machinery to GFA Ratio (%) 100&

×AssetsGrossFixed

MachineryPlant 78.41% 74.73% 72.20% 64.80%

179

8. Eimco Elecon Company Limited

It can be seen that the company is investing more than eighty percent in plant and

machinery out of its total investment in fixed assets but the assets of the company are

underutilized over a period of last five years as the asset efficiency ratio and plant and

machinery turnover ratio is continuously decreasing. The earning power ratio has slightly

reduced in the year 2006 in comparison to year 2003 but still it has again increased in the

year 2007. This would have increased further if the company would have taken care of its

asset utilization through sound capital budgeting decisions which enable the company to

make appropriate investment in fixed assets.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.87 0.65 0.60 0.57 0.69

Net Profit Margin (%) 100×

SalesPAT

6.05% 8.77% 8.94% 8.94% 8.93%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 5.27% 5.71% 5.32% 5.11% 6.14%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.76 1.31 1.29 1.04 1.10

Plant & Machinery Turnover Ratio (times)

MachineryPlantSales

& 2.05 1.49 1.47 1.18 1.24

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

85.93% 87.87% 87.25% 88.75% 89.21%

180

9. Elecon Engineering Company Ltd

It can be seen that the total assets and gross fixed assets efficiency ratio is improving over

a period of five years except in the year 2004 where asset efficiency ratio is slightly

reducing indicating that the company’s assets are effectively utililized. The net profit and

earning power ratio has also been significantly improved over five years period which is

the result of sound capital budgeting decisions because almost eighty percent of the total

fixed assets investment is in plant and machinery requiring capital budgeting exercise.

There is a considerable increase in the plant and machinery turnover ratio also.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.92 0.76 0.95 0.94 1.13

Net Profit Margin (%) 100×

SalesPAT

0.95% 1.16% 3.04% 5.50% 6.52%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 0.88% 0.88% 2.88% 5.19% 7.36%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.23 1.25 1.86 2.38 3.35

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 1.57 1.57 2.32 3.07 4.18

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

78.58% 79.27% 80.20% 77.51% 80.13%

181

10. Glaxo Smithkline Limited

The efficiency ratio calculated below is decreasing from the year 2003 onwards except in

the year 2004 where it has moderately improved. The fixed asset efficiency ratio and the

plant & machinery turnover ratio are improving over a period of four years which means

that decrease in total asset utilization ratio is due to higher component of current assets.

However, the earning power ratio has decreased in comparison to the year 2003.

Ratio Formula 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.29 1.32 0.99 0.99

Net Profit Margin (%) 100×

SalesPAT

8.37% 7.41% 9.81% 10.26%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 10.79% 9.79% 9.76% 10.12%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.86 1.96 2.11 2.34

Plant & Machinery Turnover Ratio (times) MachineryPlant

Sales&

3.01 3.22 3.86 4.25

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

61.64% 60.71% 54.67% 55.07%

182

11. GMM Pfaudler Limited

The asset efficiency ratio has improved in the years 2004, 2005 and 2006 however; it has

slightly decreased in the year 2007. But fixed assets efficiency ratio has been

continuously increased with earning power ratio indicating increase in sales and effective

utilization of fixed assets. The company has made three-fifth of its investment in plant

and machinery of the total investment in GFA and the plant and machinery turnover ratio

has continuously increased over a period of five years indicating that the company is

using its plant and machinery efficiently.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.87 0.93 0.92 1.07 0.93

Net Profit Margin (%) 100×

SalesPAT

4.05% 9.27% 8.41% 10.67% 9.41%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 3.53% 8.65% 7.73% 11.37% 8.78%

Fixed Asset Efficiency Ratio (times) AssetsGrossFixed

Sales 1.51 1.66 1.86 2.28 2.47

Plant & Machinery Turnover Ratio (times)

MachineryPlantSales

& 2.40 2.69 2.81 3.46 3.69

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

63.05% 61.75% 66.15% 65.81% 66.96%

183

12. Gujarat Narmada Valley Fertilizers Company Ltd. (GNFC)

The asset efficiency ratio, the fixed asset efficiency ratio and the plant and machinery

turnover ratio are improving over a period of five years. The net profit margin has

improved year by year after 2003, which is doubled by 2005 is because of better asset

utilization as shown by asset efficiency ratio and addition in plant and machinery which

has lead to more production, more sales and higher profit. It indicates that the assets of

the company are properly utilized.

Ratios Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.70 0.74 0.82 0.92 0.87

Net Profit Margin (%) 100×

SalesPAT

5.78% 7.52% 11.8% 12.9% 11.02%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit

Margin 4.02% 5.53% 9.69% 11.81% 9.64%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 0.70 0.74 0.89 1.05 1.10

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

&

0.75 0.80 0.99 1.15 1.21

Plant & Machinery to GFA Ratio (%)

AssetsGrossFixedMachineryPlant &

93.41% 93.05% 90.43% 91.44% 90.74%

184

13. Grasim Industries Ltd.

It can be seen that the total assets utilization as well as fixed assets utilization of the

company has been moderately improved over a period of last five years as the ratio is

improving and it is very much close to one. The plant & machinery turnover ratio is also

improving during this period. The net profit margin and earning power of the company

has been improved significantly which indicates effective assets utilization as well as

increase in the sales of the company.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.82 0.84 0.89 0.87 0.85

Net Profit Margin (%) 100×

SalesPAT

6.77% 12.70% 12.28% 11.27% 15.96%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 5.56% 10.66% 10.94% 9.75% 13.64%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 0.97 1.06 1.19 1.19 1.21

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 1.20 1.30 1.48 1.52 1.74

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

81.04% 81.12% 80.22% 78.59% 69.20%

185

14. Gujarat Alkalies & Chemicals Limited (GACL)

The company is making more than eighty percent investment in plant and machinery. It

can be seen that the assets of the company are effectively utilized as the efficiency ratios

are improving over a period of last five years. The plant and machinery turnover ratio is

also improving during this period indicating sound capital budgeting decisions. The

significant improvement in earning power ratio indicates both effective utilization of

assets as well as increase in sales.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.48 0.52 0.71 0.66 0.67

Net Profit Margin (%) 100×

SalesPAT

3.67% 7.77% 13.76% 18.08% 15.13%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 1.77% 4.06% 9.80% 11.98% 10.20%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

0.47 0.50 0.63 0.59 0.61

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 0.51 0.54 0.68 0.70 0.68

Plant & Machinery to GFA Ratio (%) AssetsGrossFixed

MachineryPlant &

93.80% 93.74% 91.98% 84.27% 88.95%

186

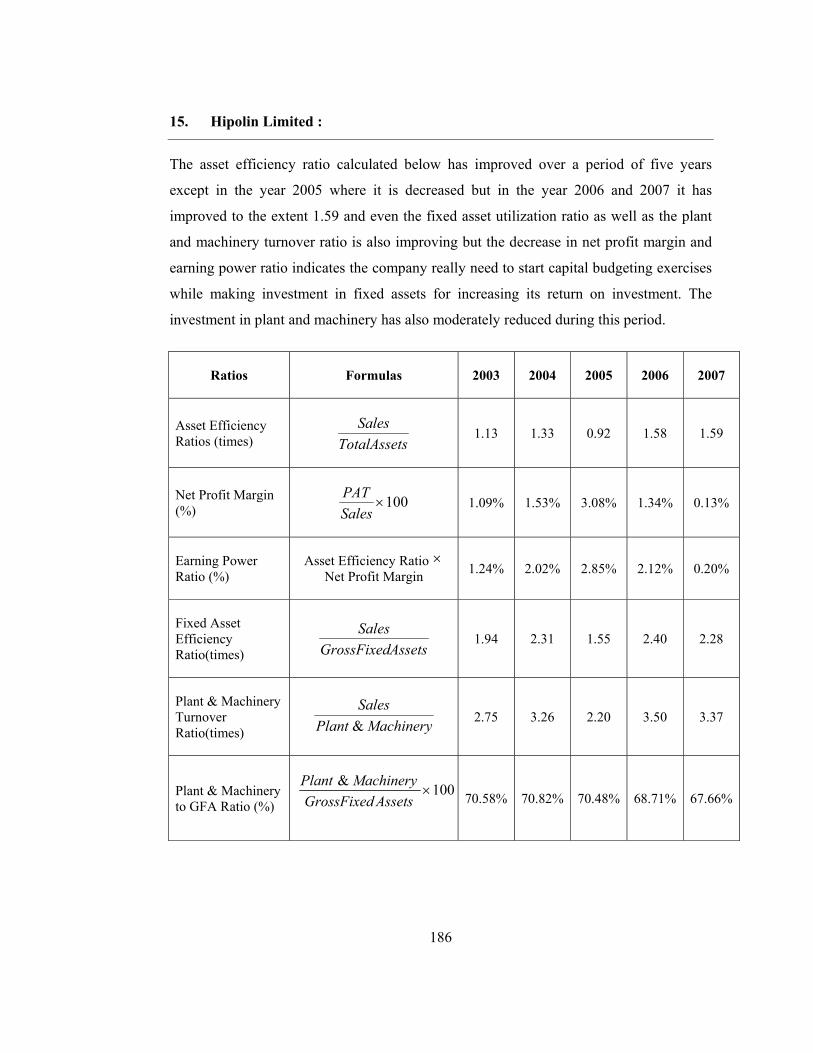

15. Hipolin Limited :

The asset efficiency ratio calculated below has improved over a period of five years

except in the year 2005 where it is decreased but in the year 2006 and 2007 it has

improved to the extent 1.59 and even the fixed asset utilization ratio as well as the plant

and machinery turnover ratio is also improving but the decrease in net profit margin and

earning power ratio indicates the company really need to start capital budgeting exercises

while making investment in fixed assets for increasing its return on investment. The

investment in plant and machinery has also moderately reduced during this period.

Ratios Formulas 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.13 1.33 0.92 1.58 1.59

Net Profit Margin (%) 100×

SalesPAT

1.09% 1.53% 3.08% 1.34% 0.13%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 1.24% 2.02% 2.85% 2.12% 0.20%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.94 2.31 1.55 2.40 2.28

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

2.75 3.26 2.20 3.50 3.37

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

70.58% 70.82% 70.48% 68.71% 67.66%

187

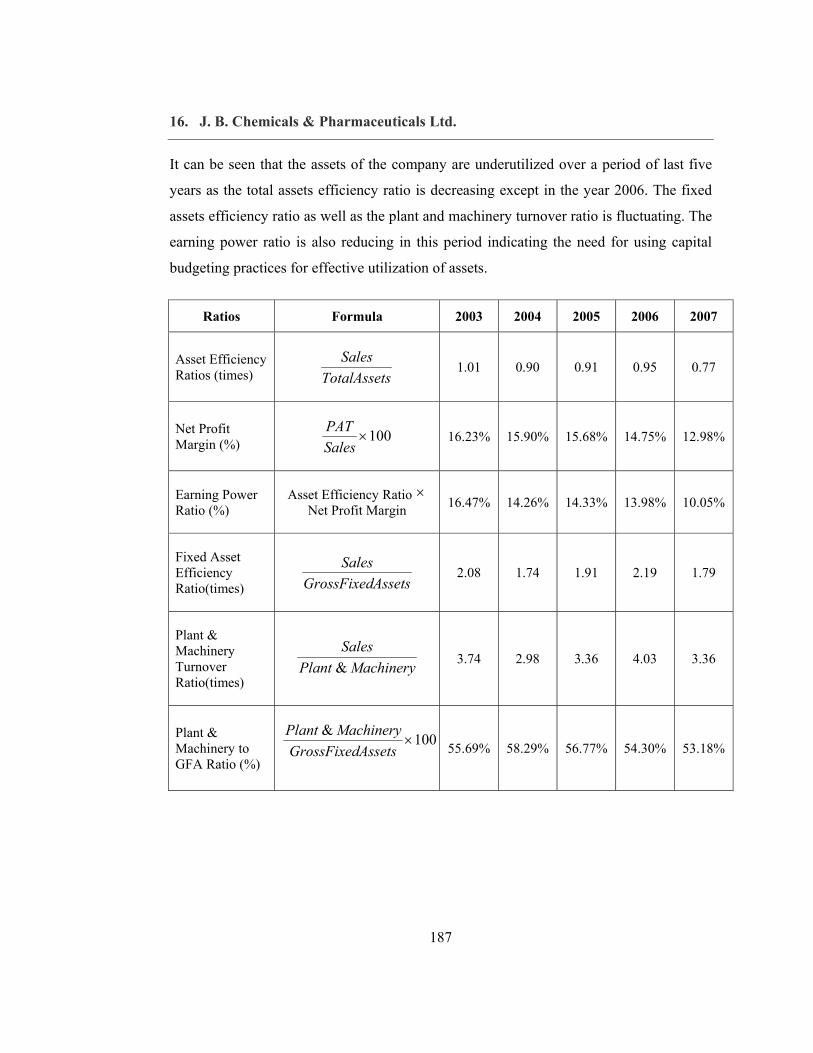

16. J. B. Chemicals & Pharmaceuticals Ltd.

It can be seen that the assets of the company are underutilized over a period of last five

years as the total assets efficiency ratio is decreasing except in the year 2006. The fixed

assets efficiency ratio as well as the plant and machinery turnover ratio is fluctuating. The

earning power ratio is also reducing in this period indicating the need for using capital

budgeting practices for effective utilization of assets.

Ratios Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.01 0.90 0.91 0.95 0.77

Net Profit Margin (%) 100×

SalesPAT

16.23% 15.90% 15.68% 14.75% 12.98%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 16.47% 14.26% 14.33% 13.98% 10.05%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

2.08 1.74 1.91 2.19 1.79

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 3.74 2.98 3.36 4.03 3.36

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

55.69% 58.29% 56.77% 54.30% 53.18%

188

17. KSB Pumps Ltd.

The company is investing almost seventy percent in plant and machinery of its total

investment in gross fixed assets. The efficiency ratio has improved over a period of four

years except in the year 2006 where it is slightly reduced indicating that the total assets

including fixed assets of the company and especially plant and machinery are properly

utilized. This has even reflected in the increase of earning power ratio also.

Ratio Formula 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.24 1.39 1.42 1.30

Net Profit Margin (%) 100×

SalesPAT

6.96% 9.22% 9.50% 11.18%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 8.66% 12.78% 13.51% 14.54%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 1.89 2.24 2.57 2.49

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 2.51 3.01 3.36 3.57

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

75.51% 74.39% 76.52% 69.68%

189

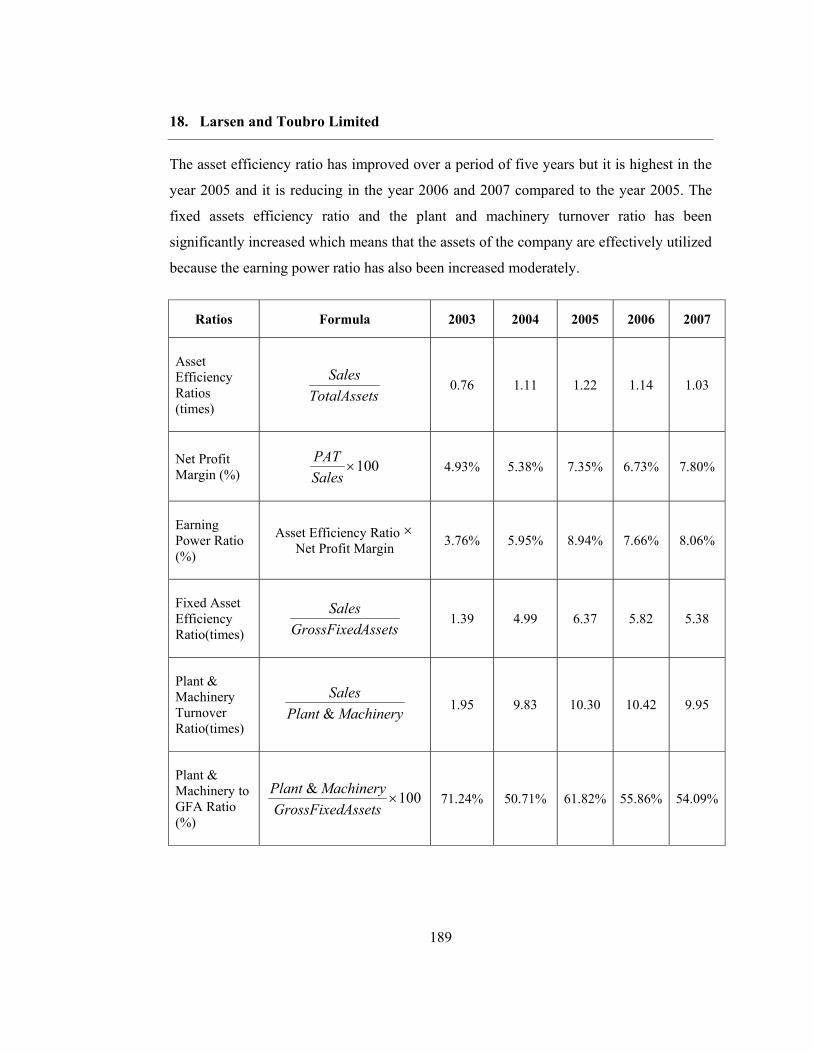

18. Larsen and Toubro Limited

The asset efficiency ratio has improved over a period of five years but it is highest in the

year 2005 and it is reducing in the year 2006 and 2007 compared to the year 2005. The

fixed assets efficiency ratio and the plant and machinery turnover ratio has been

significantly increased which means that the assets of the company are effectively utilized

because the earning power ratio has also been increased moderately.

Ratios Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times)

sTotalAssetSales

0.76 1.11 1.22 1.14 1.03

Net Profit Margin (%) 100×

SalesPAT

4.93% 5.38% 7.35% 6.73% 7.80%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 3.76% 5.95% 8.94% 7.66% 8.06%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.39 4.99 6.37 5.82 5.38

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 1.95 9.83 10.30 10.42 9.95

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

71.24% 50.71% 61.82% 55.86% 54.09%

190

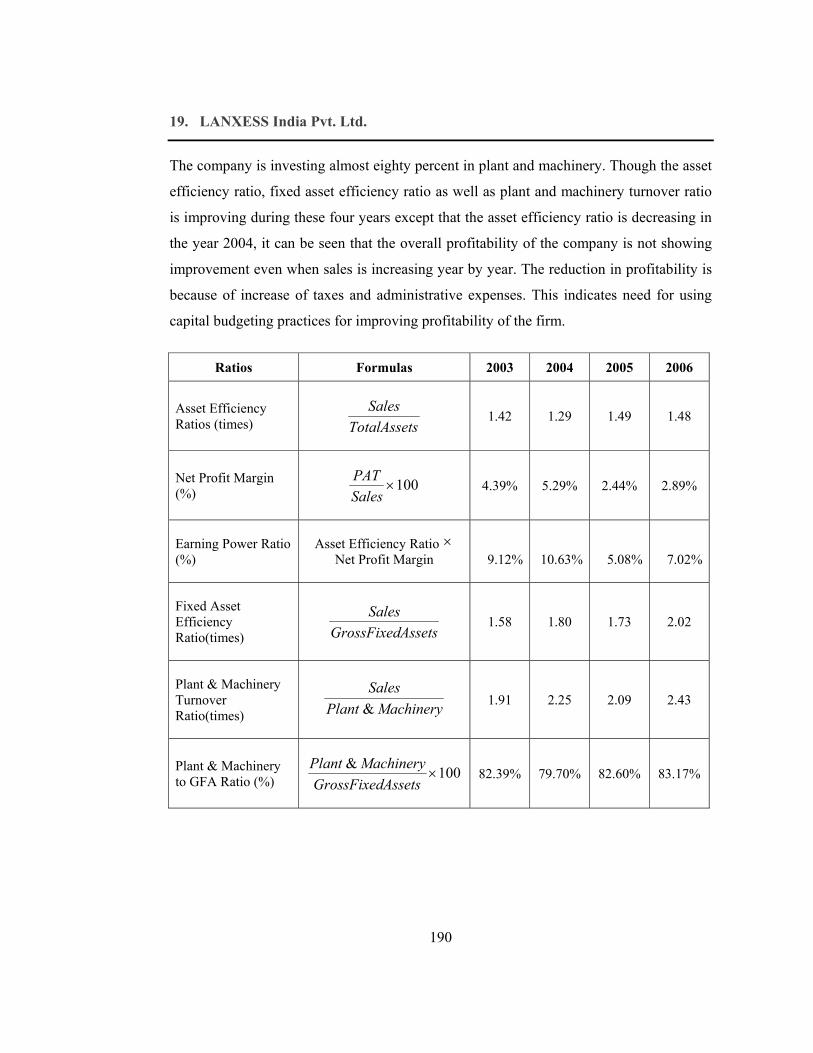

19. LANXESS India Pvt. Ltd.

The company is investing almost eighty percent in plant and machinery. Though the asset

efficiency ratio, fixed asset efficiency ratio as well as plant and machinery turnover ratio

is improving during these four years except that the asset efficiency ratio is decreasing in

the year 2004, it can be seen that the overall profitability of the company is not showing

improvement even when sales is increasing year by year. The reduction in profitability is

because of increase of taxes and administrative expenses. This indicates need for using

capital budgeting practices for improving profitability of the firm.

Ratios Formulas 2003 2004 2005 2006

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.42 1.29 1.49 1.48

Net Profit Margin (%) 100×

SalesPAT

4.39% 5.29% 2.44% 2.89%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 9.12% 10.63% 5.08% 7.02%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.58 1.80 1.73 2.02

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

1.91 2.25 2.09 2.43

Plant & Machinery to GFA Ratio (%) 100&

×AssetsGrossFixed

MachineryPlant82.39% 79.70% 82.60% 83.17%

191

20. Oil and Natural Gas Company Limited (ONGC)

The company is making huge investment in plant and machinery. But the efficiency ratio

has decreased over a period of five years which means that the assets of the company are

not effectively utilized and the fixed assets efficiency ratio and the plant and machinery

turnover ratio has been slightly increased in comparison to the year 2003. The same

observation can be made for earning power ratio also and the net profit ratio has been

decreased year by year except in the year 2006 where it is slightly increased.

Ratios Formulas 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times)

sTotalAssetSales

0.51 0.41 0.49 0.44 0.44

Net Profit Margin (%) 100×

SalesPAT

29.84% 26.19% 27.71% 28.98% 26.21%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 15.25% 10.79% 13.67% 12.62% 11.43%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

0.60 0.50 0.48 0.61 0.66

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 0.65 0.53 0.53 0.68 0.76

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

93.43% 93.85% 91.34% 89.63% 87.69%

192

21. Panacea Biotec Limited :

The investment in plant and machinery has been increased significantly over a period of

five years but the asset efficiency is decreased during this period. It can be seen that the

company’s net profit ratio is showing substantial increase particularly in the year 2006

and 2007. This is mainly because of high increase in profit margin due to increase in sales

and decrease in expenses. This increase is not supported by asset utilization indicating the

need for capital budgeting exercise.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.97 0.62 0.72 0.54 0.81

Net Profit Margin (%) 100×

SalesPAT

7.45% 6.01% 8.87% 11.11% 17.42%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 7.23% 3.72% 6.35% 6.00% 14.10%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

2.24 1.85 1.77 1.80 1.66

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 8.03 3.53 3.80 4.90 3.84

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

27.91% 52.23% 46.62% 36.76% 43.36%

193

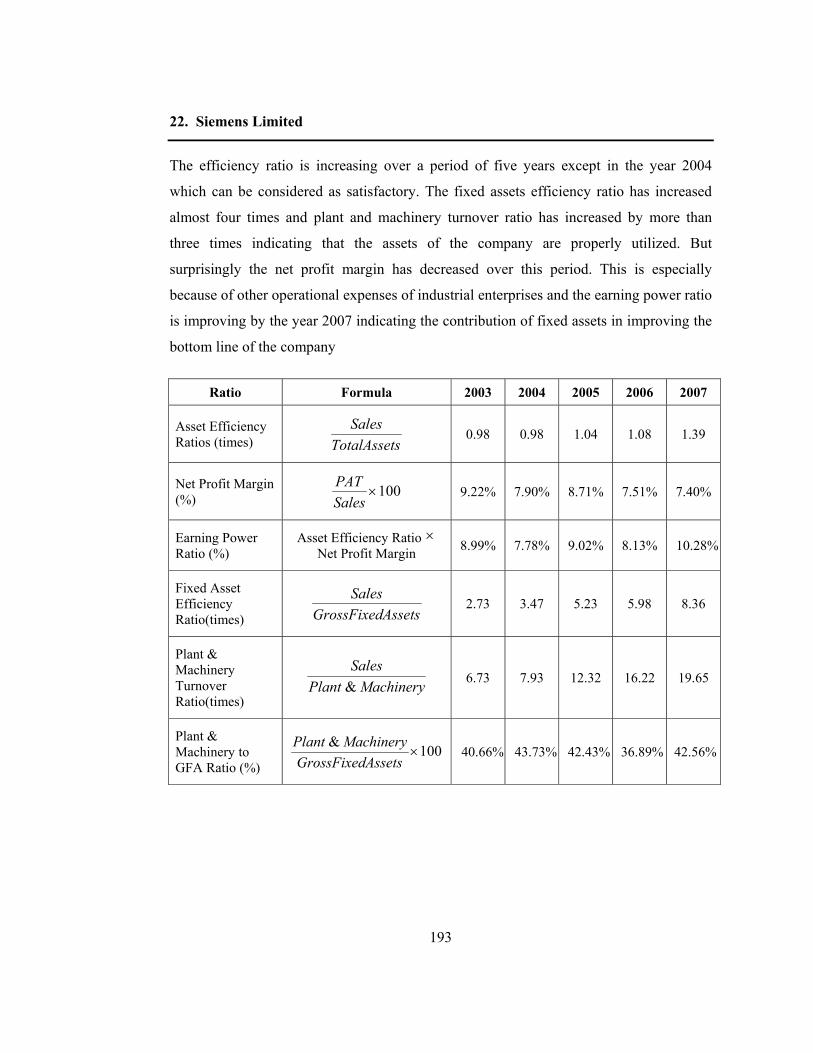

22. Siemens Limited

The efficiency ratio is increasing over a period of five years except in the year 2004

which can be considered as satisfactory. The fixed assets efficiency ratio has increased

almost four times and plant and machinery turnover ratio has increased by more than

three times indicating that the assets of the company are properly utilized. But

surprisingly the net profit margin has decreased over this period. This is especially

because of other operational expenses of industrial enterprises and the earning power ratio

is improving by the year 2007 indicating the contribution of fixed assets in improving the

bottom line of the company

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.98 0.98 1.04 1.08 1.39

Net Profit Margin (%) 100×

SalesPAT

9.22% 7.90% 8.71% 7.51% 7.40%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 8.99% 7.78% 9.02% 8.13% 10.28%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

2.73 3.47 5.23 5.98 8.36

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 6.73 7.93 12.32 16.22 19.65

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

40.66% 43.73% 42.43% 36.89% 42.56%

194

23. Sun Pharmaceuticals Limited :

Though the fixed asset efficiency ratio is moderately improving in the year 2007 in

comparison to year 2003, the overall asset efficiency ratio and plant and machinery

turnover ratio is decreasing. It can be seen that the company is having lesser asset

efficiency ratio because sales and income are increasing but at the same time there is

substantial increase in fixed assets year by year. Profitability ratio is higher only because

of other income but the earning power ratio is decreasing due to poor asset utilization.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.91 0.62 0.32 0.38 0.44

Net Profit Margin (%) 100×

SalesPAT

29.30% 26.95% 29.34% 34.09% 36.52%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 26.55% 16.75% 9.49% 12.79% 16.24%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

1.94 1.67 1.58 1.75 1.98

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 3.92 3.04 2.74 2.81 3.01

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

49.40% 54.79% 57.79% 62.10% 65.62%

195

24. Tata Steel Limited

The efficiency ratio calculated below has improved over a period of five years except in

the year 2007 which means that the assets of the company are properly utilized even the

fixed assets efficiency ratio has been improved over five years indicating effective

utilization of fixed asset where more than eighty percent investment has taken place in

plant and machinery. The plant and machinery turnover ratio has also increased during

this period. This has been reflected in terms of substantial increase in net profit margin

and earning power ratio.

Ratios Formulas 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times)

sTotalAssetSales

0.74 0.86 0.95 0.89 0.62

Net Profit Margin (%) 100×

SalesPAT

10.34% 14.65% 21.89% 20.47% 21.36%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 7.63% 12.53% 20.81% 18.21% 13.15%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

0.79 0.90 1.06 1.04 1.07

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 0.90 1.06 1.36 1.27 1.42

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

88.14% 84.42% 78.04% 82.16% 75.67%

196

25. Transpek Industries Limited

The total assets and fixed assets efficiency ratio calculated below has improved over a

period of five years except in the year 2007 which means that the assets of the company

are properly utilized. The same observation can be made for plant and machinery turnover

ratio. This can be observed in the increase of the earning power ratio of the firm. This is

not possible without taking effective capital budgeting decisions because the company is

making more than 75% investment in plant and machinery out of its total investments in

gross fixed assets.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 0.51 0.73 0.93 0.91 0.86

Net Profit Margin (%) 100×

SalesPAT

-6.91% 4.13% 6.92% 5.83% 5.23%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin -3.50% 3.03% 6.41% 5.28% 4.48%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 0.69 0.85 1.15 1.10 0.96

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

0.77 1.00 1.52 1.44 1.24

Plant & Machinery to GFA Ratio (%) AssetsGrossFixed

MachineryPlant & 88.59% 85.32% 75.61% 76.62% 77.21%

197

26. Vadilal Enterprises Limited:

The company is investing almost ninety percent in plant and machinery. It can be seen

that the assets of the company are underutilized over a period of last five years as the ratio

is decreasing except in year 2004. The fixed assets efficiency ratio is decreasing every

year except 2004 and even net profit margin and earning power ratio of the company is

also not very impressive. All these put together, the company need to focus more on asset

utilization by taking sound capital budgeting decisions at the time of investment in the

fixed assets.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 2.47 2.72 2.42 2.40 2.41

Net Profit Margin (%) 100×

SalesPAT

(0.02%) (0.80%) 0.36% 0.23% 0.23%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin (0.05%) (2.17%) 0.86% 0.55% 0.55%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales 3.80 3.81 3.52 3.64 3.59

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 4.27 4.24 3.90 4.04 3.93

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

88.97% 89.84% 90.26% 90.07% 91.21%

198

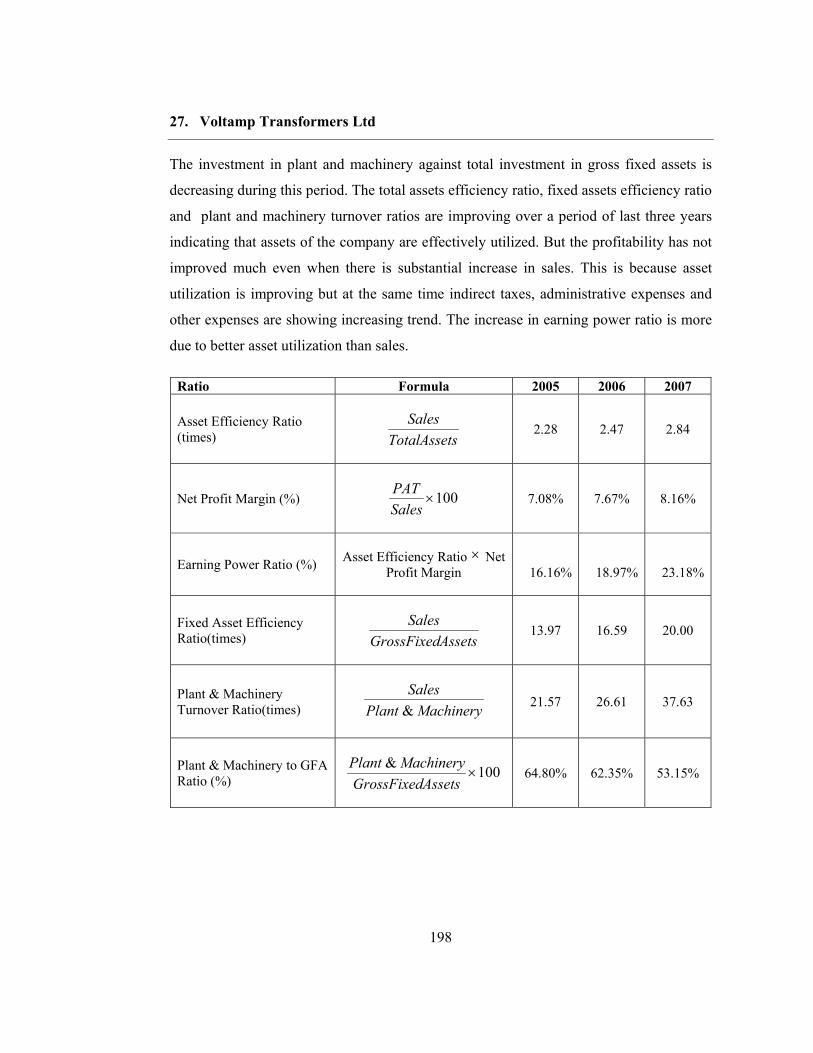

27. Voltamp Transformers Ltd

The investment in plant and machinery against total investment in gross fixed assets is

decreasing during this period. The total assets efficiency ratio, fixed assets efficiency ratio

and plant and machinery turnover ratios are improving over a period of last three years

indicating that assets of the company are effectively utilized. But the profitability has not

improved much even when there is substantial increase in sales. This is because asset

utilization is improving but at the same time indirect taxes, administrative expenses and

other expenses are showing increasing trend. The increase in earning power ratio is more

due to better asset utilization than sales.

Ratio Formula 2005 2006 2007

Asset Efficiency Ratio (times) sTotalAsset

Sales 2.28 2.47 2.84

Net Profit Margin (%) 100×SalesPAT

7.08% 7.67% 8.16%

Earning Power Ratio (%) Asset Efficiency Ratio × Net Profit Margin 16.16% 18.97% 23.18%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

13.97 16.59 20.00

Plant & Machinery Turnover Ratio(times) MachineryPlant

Sales&

21.57 26.61 37.63

Plant & Machinery to GFA Ratio (%) 100&

×AssetsGrossFixed

MachineryPlant 64.80% 62.35% 53.15%

199

28. Wipro Limited

The asset efficiency ratio calculated below indicates that the ratio is marginally improving

over a period of last five years. The earning power ratio has improved negligibly is a

matter of concern because it indicates ineffective utilization of assets. The plant and

machinery turnover ratio has improved in this period but it has not reflected in terms of

significant increase in the profitability of the firm. The sound capital budgeting decision

would have improved fixed asset efficiency and in turn earning power ratio of the firm.

Ratio Formula 2003 2004 2005 2006 2007

Asset Efficiency Ratios (times) sTotalAsset

Sales 1.00 0.98 1.09 1.08 1.03

Net Profit Margin (%) 100×

SalesPAT

20.08% 17.62% 20.54% 19.69% 20.66%

Earning Power Ratio (%)

Asset Efficiency Ratio × Net Profit Margin 19.99% 17.31% 22.43% 21.25% 21.33%

Fixed Asset Efficiency Ratio(times) AssetsGrossFixed

Sales

3.22 3.52 3.61 3.45 3.26

Plant & Machinery Turnover Ratio(times)

MachineryPlantSales

& 5.94 7.10 7.66 7.63 7.79

Plant & Machinery to GFA Ratio (%)

100&×

AssetsGrossFixedMachineryPlant

54.24% 49.67% 47.19% 45.19% 41.78%

200

Conclusion:

As seen, in most cases since the co-efficient of relation R2 is significant (i.e. near to 1), it

can be stated that the variables plant and machinery and sales are exhaustive enough to

explain the variation in operating income of the company. Thus, our findings, through the

above analysis it can be stated that proper usage of capital budgeting techniques lead to

accurate decision for investment in fixed assets and hence better operating income

through the better capital budgeting practices. Further, in cases where R2 is not significant

(i.e. near to 1), future research can be carried out to find more significant / relevant

model.

The financial analysis reveals that the companies which use capital budgeting techniques

wisely have better asset-efficiency ratio and the plant and machinery turnover ratio and

ultimately a good earning power ratio. Further, Table 6.4 to 6.9 reveals that all the

companies are using more than one techniques of capital budgeting for evaluating the

various projects under consideration. Almost all the companies are using pay back period

method to evaluate the project from liquidity point of view and at the same time all the

companies are using at least one of the DCF techniques to assess the profitability of the

projects. This reflects the confidence level in any single method for decision-making.

Hence results of all methods are calibrated and decisions are taken.

201

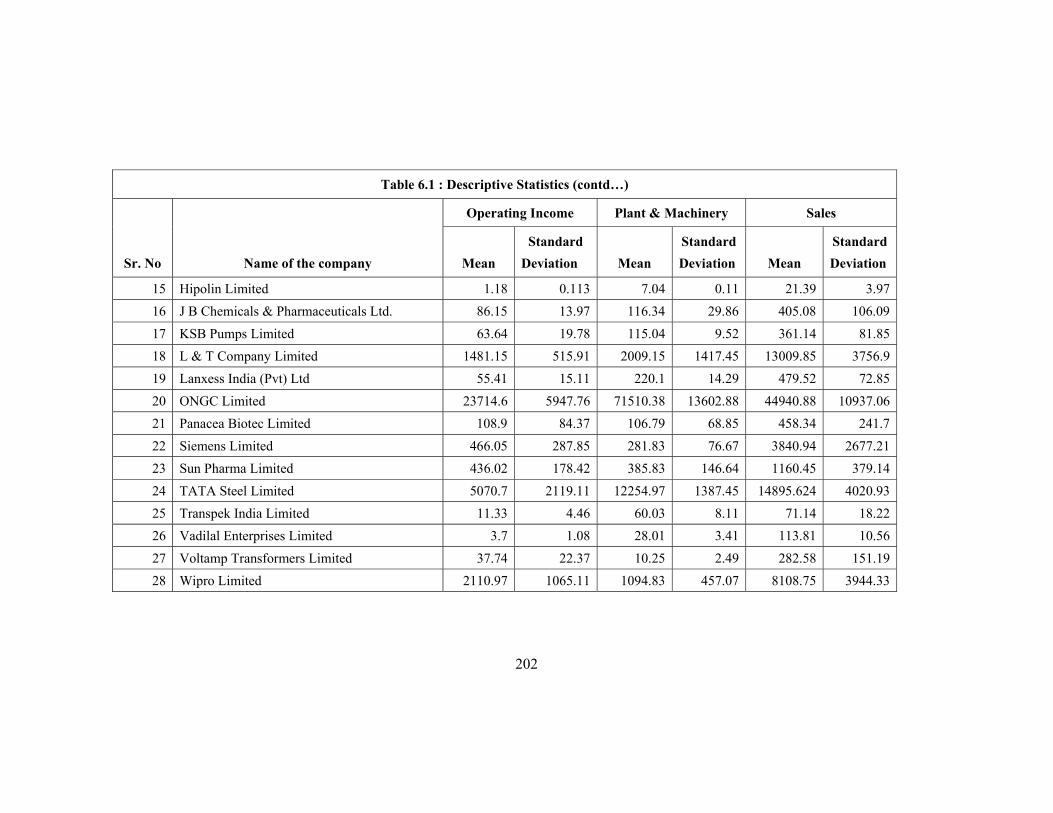

Table 6.1 : Descriptive Statistics

Sr. No Name of the company

Operating Income Plant & Machinery Sales

Mean Standard

Deviation Mean Standard Deviation Mean

Standard Deviation

1 Alembic Limited 102.522 21.71 368.69 34.55 628.74 65.86

2 Arvind Mills Limited 381.64 36.34 1364.89 75.49 1637.24 149.48

3 Astrazeneca Pharma Indis Ltd 61.07 17.76 42.69 2.55 236.78 43.42

4 Atlas Copco Limited 89.75 40.2 37.57 2.33 545.71 208.66

5 Bajaj Hindustan Limited 172.73 159.24 805.68 737.23 806.03 437.75

6 Berger Paints Limited 95.57 26.67 104.86 29.35 967.88 264.79

7 Cadbury India Limited 118.75 19.46 294.84 30.76 967.13 142.84

8 Eimco Elecon Limited 19.68 4.23 64.02 16.18 90.79 7.17

9 Elecon Engineering Company Limited 49.98 42.24 148.14 35.62 408.34 276.24

10 Glaxo Smithkline Limited 194.7 35.82 295.77 10.76 1057.25 140.96

11 GMM Pfaudler Co. Limited 14.75 6.9 29.88 4.9 91.81 29.9512 GNFC Limited 446.9 144.74 2054.33 223.58 2033 610.913 Grasim Company Limited 1694.18 608.05 4934.99 376.87 7212.02 1609.7

14 Gujarat Alkalies Co. Limited 348.04 92.86 1586.44 122.59 990.37 197.64

202

Table 6.1 : Descriptive Statistics (contd…)

Sr. No Name of the company

Operating Income Plant & Machinery Sales

Mean Standard

Deviation Mean Standard Deviation Mean

Standard Deviation

15 Hipolin Limited 1.18 0.113 7.04 0.11 21.39 3.9716 J B Chemicals & Pharmaceuticals Ltd. 86.15 13.97 116.34 29.86 405.08 106.0917 KSB Pumps Limited 63.64 19.78 115.04 9.52 361.14 81.8518 L & T Company Limited 1481.15 515.91 2009.15 1417.45 13009.85 3756.919 Lanxess India (Pvt) Ltd 55.41 15.11 220.1 14.29 479.52 72.8520 ONGC Limited 23714.6 5947.76 71510.38 13602.88 44940.88 10937.0621 Panacea Biotec Limited 108.9 84.37 106.79 68.85 458.34 241.722 Siemens Limited 466.05 287.85 281.83 76.67 3840.94 2677.2123 Sun Pharma Limited 436.02 178.42 385.83 146.64 1160.45 379.1424 TATA Steel Limited 5070.7 2119.11 12254.97 1387.45 14895.624 4020.9325 Transpek India Limited 11.33 4.46 60.03 8.11 71.14 18.2226 Vadilal Enterprises Limited 3.7 1.08 28.01 3.41 113.81 10.5627 Voltamp Transformers Limited 37.74 22.37 10.25 2.49 282.58 151.1928 Wipro Limited 2110.97 1065.11 1094.83 457.07 8108.75 3944.33

203

Table 6.2 : Pearson Co-relations

Sr. No

Name of the company Operating Income

v/s Plant & Machinery

Operating Income v/s Sales

Plant & Machinery

v/s Sales

1 Alembic Limited 0.452 0.853 0.540 2 Arvind Mills Limited 0.610 0.729 0.618 3 Astrazeneca Pharma Indis Ltd 0.902 0.971 0.799

4 Atlas Copco Limited -0.683 0.960 -0.857 5 Bajaj Hindustan Limited 0.998 0.975 0.973 6 Berger Paints Limited 0.989 0.984 0.995 7 Cadbury India Limited 0.881 0.916 0.996 8 Eimco Elecon Limited 0.954 0.933 0.819 9 Elecon Engineering Company Limited 0.995 1.000 0.996 10 Glaxo Smithkline Limited 0.813 0.974 0.677 11 GMM Pfaudler Co. Limited 0.924 0.980 0.953 12 GNFC Limited 0.718 0.966 0.874 13 Grasim Company Limited 0.955 0.959 0.993 14 Gujarat Alkalies Co. Limited 0.541 0.930 0.811 15 Hipolin Limited 0.055 -0.458 0.454

204

Table 6.2 : Pearson Co-relations Sr. No

Name of the company Operating Income

v/s Plant & Machinery

Operating Income v/s Sales

Plant & Machinery

v/s Sales

16 J B Chemicals & Pharmaceuticals Ltd. 0.862 0.985 0.907 17 KSB Pumps Limited 0.989 0.995 0.990 18 L & T Company Limited -0.276 0.973 -0.460 19 Lanxess India (Pvt) Ltd -0.487 0.029 0.858 20 ONGC Limited 0.639 0.971 0.708 21 Panacea Biotec Limited 0.957 0.995 0.954 22 Siemens Limited 0.975 0.998 0.981 23 Sun Pharma Limited 0.963 0.998 0.971 24 TATA Steel Limited 0.849 0.987 0.917 25 Transpek India Limited 0.175 0.976 0.342 26 Vadilal Enterprises Limited 0.760 0.596 0.965 27 Voltamp Transformers Limited 0.909 0.996 0.942 28 Wipro Limited 0.996 0.998 0.996

205

Table 6.3 : Regression Data Analysis

Sr. No Name of the Company

Constant Plant & Machinery Sales R2 p-

value

Standard Error

of Estimate

B co-efficient

t (p-value)

β co-efficient

t (p-value)

β co-efficient

t (p-value)

1 Alembic Limited -72.873 -0.784 (0.515) -0.007 -0.026

(0.981) 0.283 1.961 (0.189) 0.728 0.272 16.01

2 Arvind Mills Limited -14.732 -0.048 (0.966) 0.124 0.44

(0.703) 0.138 0.968 (0.436) 0.573 0.427 33.59

3 Astrazeneca Pharma India Limited -109.727 -2.561

(0.237) 2.431 1.855 (0.315) 0.283 3.674

(0.169) 0.987 0.113 3.48

4 Atlas Copco Limited -400.072 -4.063 (0.154) 9.088 3.961

(0.157) 0.272 10.617 (0.060) 0.995 0.068 4.77

5 Bajaj Hindustan Limited -9.784 -0.384 (0.738) 0.201 4.891

(0.039) 0.026 0.376 (0.743) 0.996 0.004 13.97

6 Berger Paints Limited 1.195 0.111 (0.922) 0.841 0.873

(0.476) 0.006 0.06 (0.957) 0.978 0.022 5.66

7 Cadbury India Limited 235.041 2.141

(0.278) -2.713 -2.203

(0.271) 0.707 2.666 (0.228) 0.972 0.166 5.60

8 Eimco Elecon Limited -14.674 -2.025 (0.180) 0.15 3.250

(0.083) 0.273 2.616 (0.120) 0.979 0.021 0.86

206

Table 6.3 : Regression Data Analysis (contd…)

Sr. No Name of the Company

Constant Plant & Machinery Sales R2 p-

value

Standard Error

of Estimate

B co-efficient

t (p-value)

β co-efficient

t (p-value)

β co-efficient

t (p-value)

9 Elecon Engineering Company Limited -5.254 -0.195

(0.864) -0.075 -0.267 (0.815) 0.162 4.479

(0.046) 0.999 0.001 1.78

10 Glaxo Smithkline Limited 262.845 -1.868 (0.313) -0.941 -2.379

(0.253) 0.199 6.587 (0.096) 0.992 0.087 5.42

11 GMM Pfuadler Company Limited -3.399 -0.325 (0.776) -0.166 -0.258

(0.820) 0.252 2.398 (0.139) 0.962 0.038 1.90

12 GNFC Limited 465.054 22.091 (0.002) -0.344 -23.765

(0..002) 0.339 63.933 (0.00) 1.000 0.000 3.15

13 Grasim Company Limited -1777.72 -0.194 (0.864) 0.264 0.094

(0.934) 0.301 0.458 (0.692) 0.920 0.080 242.89

14 Gujarat Alkalies & Chemicals Ltd 429.287 9.502 (0.011) -0.472 -12.00

(0.007) 0.675 27.631 (0.001) 0.998 0.002 5.65

15 Hipolin Limited -0.848 -0.182 (0.872)

0.339 0.498

(0.668) -0.017

-0.915 (0.457)

0.291 0.703 0.133

16 J B Chemicals & Pharmaceuticals Ltd. 34.696 5.458

(0.032) -0.082 -0.658 (0.578) 0.151 4.293

(0.05) 0.975 0.025 3.14

17 KSB Pumps Limited -47.664 -0.464 (0.723) 0.333 0.239

(0.851) 0.202 1.247 (0.430) 0.991 0.092 3.17

207

Table 6.3 : Regression Data Analysis (contd…)

Sr. No Name of the Company

Constant Plant & Machinery Sales R2 p-

value

Standard Error

of Estimate

B co-efficient

t (p-value)

β co-efficient

t (p-value)

β co-efficient

t (p-value)

18 L & T Company Limited -592.688 -2.514 (0.128) 0.079 2.074

(0.174) 0.147 10.266 (0.009) 0.983 0.017 95.69

19 Lanxess India Pvt. Limited 338.398 14.781 (0.043) -2.051 13.227

(0.048) 0.351 11.544 (0.055) 0.994 0.075 1.97

20 ONGC Limited 1344.188 0.260 (0.819) -0.043 -0.425

(0.712) 0.566 4.533 (0.045) 0.948 0.052 1926.40

21 Panacea Biotec Limited -48.428 -3.722 (0.065) 0.105 0.375

(0.743) 0.319 4.017 (0.057) 0.991 0.009 11.47

22 Siemens Limited 125.602 0.867 (0.477) -0.412 -0.500

(0.667) 0.119 5.036 (0.037) 0.996 0.004 24.37

23 Sun Pharma Limited -115.441 -4.228 (0.052) -0.131 -0.585

(0.618) 0.519 5.982 (0.027) 0.996 0.004 15.60

24 TATA Steel Limited 1342.883 0.818 (0.499) -0.533 -2.544

(0.126) 0.689 9.526 (0.011) 0.995 0.006 232.29

25 Transpek India Limited -0.756 -0.228 (0.841) -0.099 -1.738

(0.224) 0.254 9.976 (0.010) 0.981 0.019 0.87

208

Table 6.3 : Regression Data Analysis (contd…)

Sr. No Name of the Company

Constant Plant & Machinery Sales R2 p-

value

Standard Error

of Estimate

B co-efficient

t (p-value)

β co-efficient

t (p-value)

β co-efficient

t (p-value)

26 Vadilal Enterprises Limted 3.079 0.769 (0.522) 0.852 2.59

(0.122) -0.204 -1.925 (0.194) 0.852 0.148 0.59

27 Voltamp Tansformers Limited 9.60 6.041

(0.104) -2.305

-8.860 (0.072)

0.183 42.688 (0.015)

1.00 0.010 0.378

27 Wipro Limited -182.78 -0.841 (0.489) 0.688 0.578

(0.622) 0.19 1.378 (0.302) 0.996 0.004 95.63

209

Table 6. 4 : Asset Efficiency Ratio

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

1 Alembic Limited 1.08 1.09 0.90 0.95 0.79 NPV / PBP / PI

2 Arvind Mills Limited 0.58 0.49 0.53 0.44 0.49 IRR / NPV /PBP

3 Astrazeneca Pharma Indis Ltd 1.34 1.26 1.38 1.21 PBP / NPV

4 Atlas Copco (India) Limited 1.41 1.13 1.50 1.50 PBP / NPV

5 Bajaj Hindusthan Limited 2.48 1.24 0.92 0.69 0.45 IRR / NPV

6 Berger Paints India Limited 2.20 2.16 2.18 2.12 2.10 IRR / PBP / NPV

7 Cadbury India Limited 1.63 1.54 1.52 1.63 NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 0.87 0.65 0.60 0.57 0.69 NPV /IRR/ PBP

9 Elecon Engg Co. Limited 0.92 0.76 0.95 0.94 1.13 IRR / PBP / NPV

10 Glaxo Smithkline Limited 1.29 1.32 0.99 0.99 NPV / IRR /PBP

11 GMM Pfaudler Limited 0.87 0.93 0.92 1.07 0.93 NPV / PBP

12 GNFC Limited 0.70 0.74 0.82 0.92 0.87 PBP / NPV / IRR

13 Grasim Industires Limited 0.82 0.84 0.89 0.87 0.85 IRR / NPV

14 Gujarat Alkalies Co. Limited 0.48 0.52 0.71 0.66 0.67 IRR /PBP

210

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

15 Hipolin Limited 1.13 1.33 0.92 1.58 1.59 na-

16 J B Chemicals & Pharmaceuticals Ltd. 1.01 0.90 0.91 0.95 0.77 IRR / PBP / NPV

17 KSB Pumps Limited 1.24 1.39 1.42 1.30 PBP / NPV

18 L&T Limited 0.76 1.11 1.22 1.14 1.03 NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 1.42 1.29 1.49 1.48 PBP / NPV / IRR

20 ONGC Limited 0.51 0.41 0.49 0.44 0.44 IRR / PBP /NPV

21 Panacea Biotec Limtied 0.97 0.62 0.72 0.54 0.81 IRR / NPV / PBP

22 Siemens Limited 0.98 0.98 1.04 1.08 1.39 IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 0.91 0.62 0.32 0.38 0.44 IRR /PBP

24 TATA Steel Limited 0.74 0.86 0.95 0.89 0.62 IRR / PBP / NPV

25 Transpek Industires Limited 0.51 0.73 0.93 0.91 0.86 IRR / NPV / ARR

26 Vadilal Enterprises Limited 2.47 2.72 2.42 2.40 2.41 IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 2.21 2.28 2.47 2.84 PBP / PI

28 Wipro Limited 1.00 0.98 1.09 1.08 1.03 IRR / NPV

211

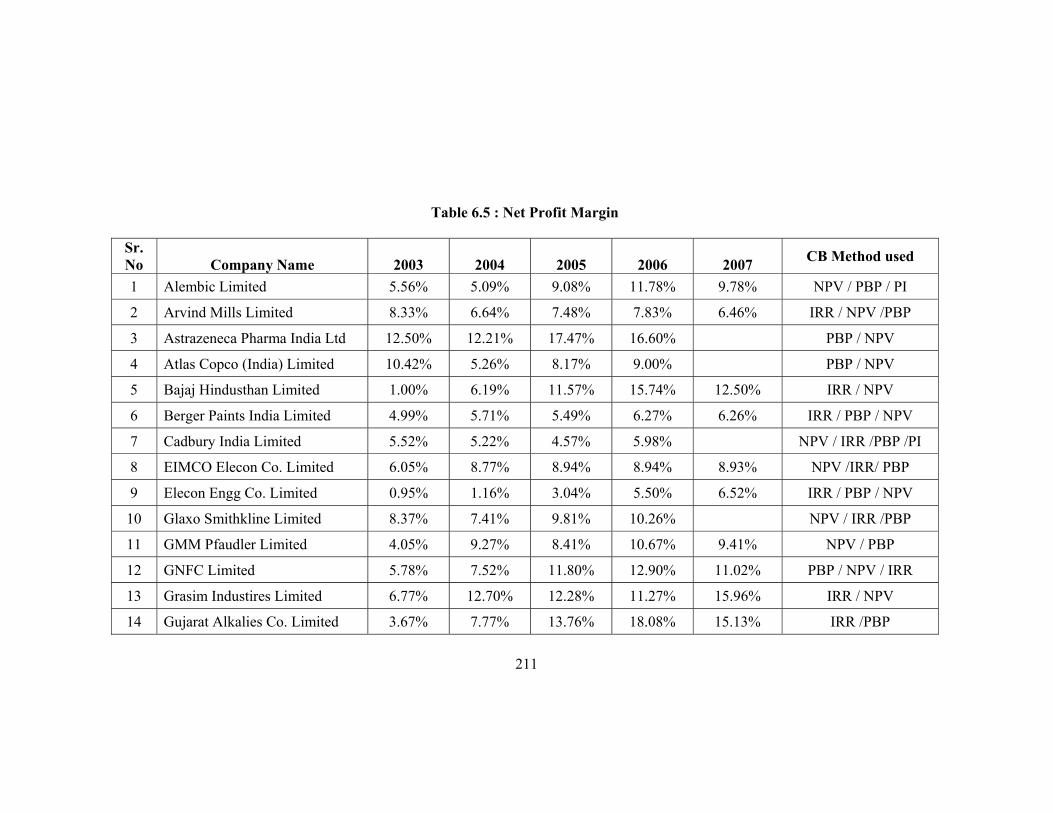

Table 6.5 : Net Profit Margin

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

1 Alembic Limited 5.56% 5.09% 9.08% 11.78% 9.78% NPV / PBP / PI

2 Arvind Mills Limited 8.33% 6.64% 7.48% 7.83% 6.46% IRR / NPV /PBP

3 Astrazeneca Pharma India Ltd 12.50% 12.21% 17.47% 16.60% PBP / NPV

4 Atlas Copco (India) Limited 10.42% 5.26% 8.17% 9.00% PBP / NPV

5 Bajaj Hindusthan Limited 1.00% 6.19% 11.57% 15.74% 12.50% IRR / NPV

6 Berger Paints India Limited 4.99% 5.71% 5.49% 6.27% 6.26% IRR / PBP / NPV

7 Cadbury India Limited 5.52% 5.22% 4.57% 5.98% NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 6.05% 8.77% 8.94% 8.94% 8.93% NPV /IRR/ PBP

9 Elecon Engg Co. Limited 0.95% 1.16% 3.04% 5.50% 6.52% IRR / PBP / NPV

10 Glaxo Smithkline Limited 8.37% 7.41% 9.81% 10.26% NPV / IRR /PBP

11 GMM Pfaudler Limited 4.05% 9.27% 8.41% 10.67% 9.41% NPV / PBP

12 GNFC Limited 5.78% 7.52% 11.80% 12.90% 11.02% PBP / NPV / IRR

13 Grasim Industires Limited 6.77% 12.70% 12.28% 11.27% 15.96% IRR / NPV

14 Gujarat Alkalies Co. Limited 3.67% 7.77% 13.76% 18.08% 15.13% IRR /PBP

212

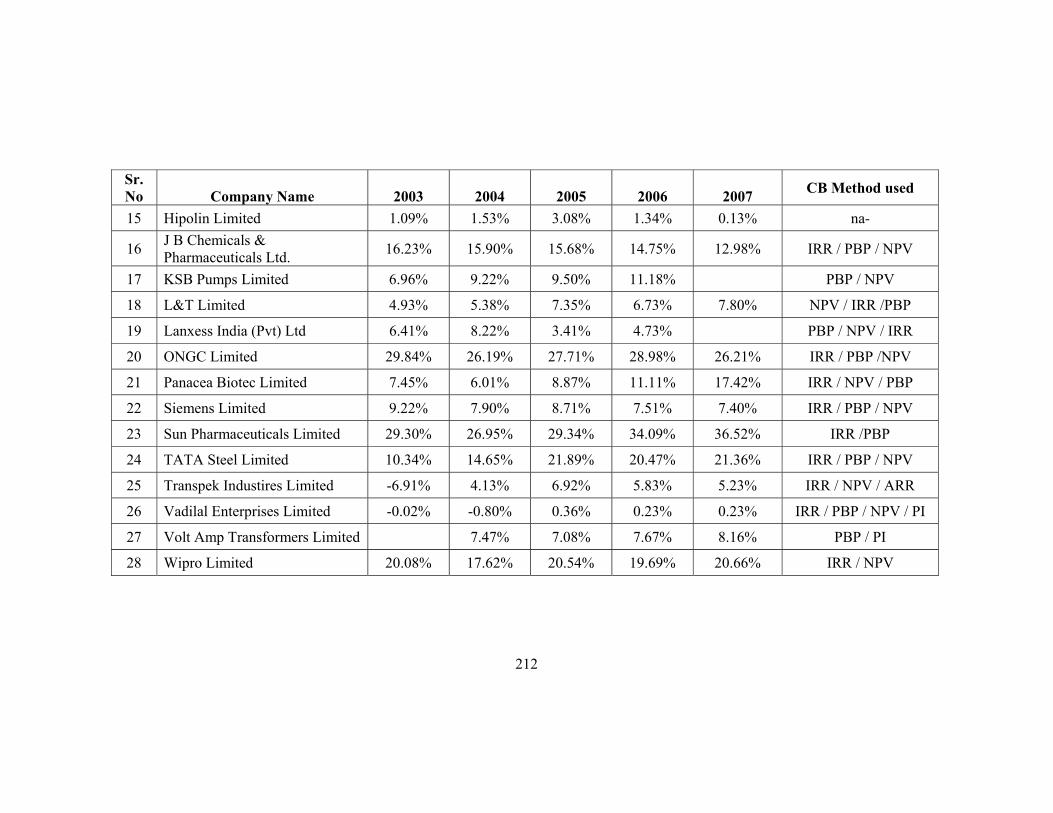

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

15 Hipolin Limited 1.09% 1.53% 3.08% 1.34% 0.13% na-

16 J B Chemicals & Pharmaceuticals Ltd. 16.23% 15.90% 15.68% 14.75% 12.98% IRR / PBP / NPV

17 KSB Pumps Limited 6.96% 9.22% 9.50% 11.18% PBP / NPV

18 L&T Limited 4.93% 5.38% 7.35% 6.73% 7.80% NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 6.41% 8.22% 3.41% 4.73% PBP / NPV / IRR

20 ONGC Limited 29.84% 26.19% 27.71% 28.98% 26.21% IRR / PBP /NPV

21 Panacea Biotec Limited 7.45% 6.01% 8.87% 11.11% 17.42% IRR / NPV / PBP

22 Siemens Limited 9.22% 7.90% 8.71% 7.51% 7.40% IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 29.30% 26.95% 29.34% 34.09% 36.52% IRR /PBP

24 TATA Steel Limited 10.34% 14.65% 21.89% 20.47% 21.36% IRR / PBP / NPV

25 Transpek Industires Limited -6.91% 4.13% 6.92% 5.83% 5.23% IRR / NPV / ARR

26 Vadilal Enterprises Limited -0.02% -0.80% 0.36% 0.23% 0.23% IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 7.47% 7.08% 7.67% 8.16% PBP / PI

28 Wipro Limited 20.08% 17.62% 20.54% 19.69% 20.66% IRR / NPV

213

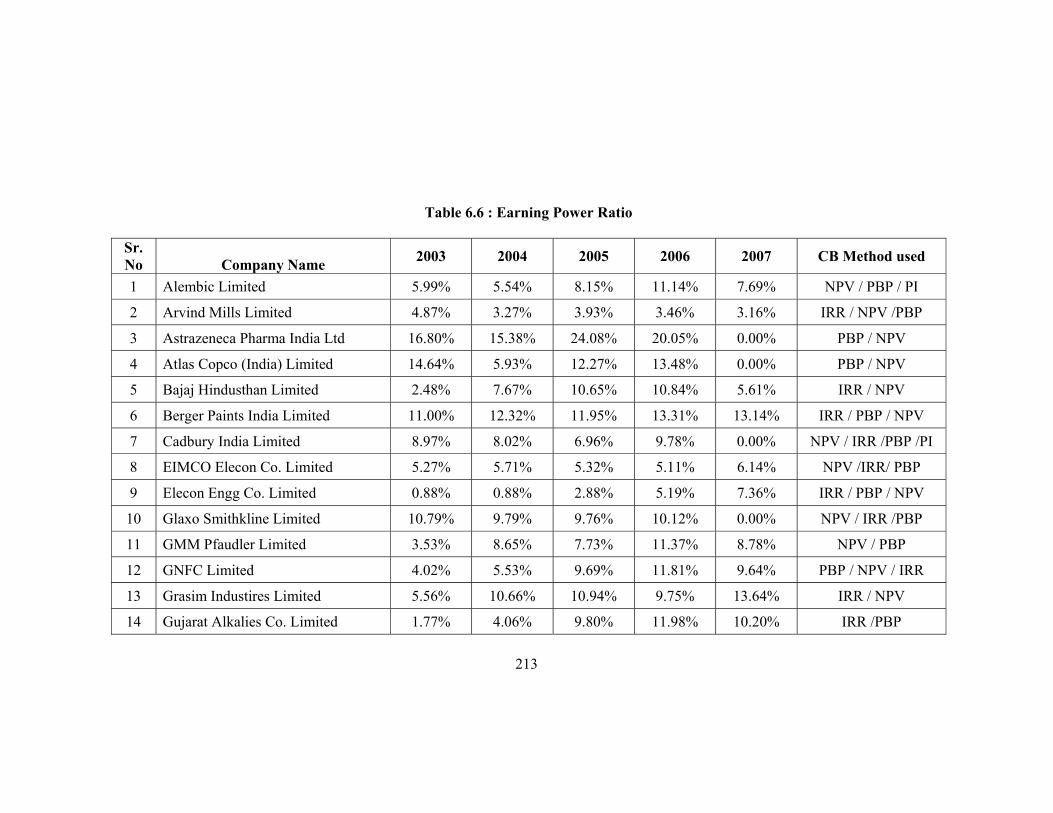

Table 6.6 : Earning Power Ratio

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

1 Alembic Limited 5.99% 5.54% 8.15% 11.14% 7.69% NPV / PBP / PI

2 Arvind Mills Limited 4.87% 3.27% 3.93% 3.46% 3.16% IRR / NPV /PBP

3 Astrazeneca Pharma India Ltd 16.80% 15.38% 24.08% 20.05% 0.00% PBP / NPV

4 Atlas Copco (India) Limited 14.64% 5.93% 12.27% 13.48% 0.00% PBP / NPV

5 Bajaj Hindusthan Limited 2.48% 7.67% 10.65% 10.84% 5.61% IRR / NPV

6 Berger Paints India Limited 11.00% 12.32% 11.95% 13.31% 13.14% IRR / PBP / NPV

7 Cadbury India Limited 8.97% 8.02% 6.96% 9.78% 0.00% NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 5.27% 5.71% 5.32% 5.11% 6.14% NPV /IRR/ PBP

9 Elecon Engg Co. Limited 0.88% 0.88% 2.88% 5.19% 7.36% IRR / PBP / NPV

10 Glaxo Smithkline Limited 10.79% 9.79% 9.76% 10.12% 0.00% NPV / IRR /PBP

11 GMM Pfaudler Limited 3.53% 8.65% 7.73% 11.37% 8.78% NPV / PBP

12 GNFC Limited 4.02% 5.53% 9.69% 11.81% 9.64% PBP / NPV / IRR

13 Grasim Industires Limited 5.56% 10.66% 10.94% 9.75% 13.64% IRR / NPV

14 Gujarat Alkalies Co. Limited 1.77% 4.06% 9.80% 11.98% 10.20% IRR /PBP

214

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

15 Hipolin Limited 1.24% 2.02% 2.85% 2.12% 0.20% na-

16 J B Chemicals & Pharmaceuticals Ltd. 16.47% 14.26% 14.33% 13.98% 10.05% IRR / PBP / NPV

17 KSB Pumps Limited 8.66% 12.78% 13.51% 14.54% 0.00% PBP / NPV

18 L&T Limited 3.76% 5.95% 8.94% 7.66% 8.06% NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 9.12% 10.63% 5.08% 7.02% 0.00% PBP / NPV / IRR

20 ONGC Limited 15.25% 10.79% 13.67% 12.62% 11.43% IRR / PBP /NPV

21 Panacea Biotec Limtied 7.23% 3.72% 6.35% 6.00% 14.10% IRR / NPV / PBP

22 Siemens Limited 8.99% 7.78% 9.02% 8.13% 10.28% IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 26.55% 16.75% 9.49% 12.79% 16.24% IRR /PBP

24 TATA Steel Limited 7.63% 12.53% 20.81% 18.21% 13.15% IRR / PBP / NPV

25 Transpek Industires Limited -3.50% 3.03% 6.41% 5.28% 4.48% IRR / NPV / ARR

26 Vadilal Enterprises Limited -0.05% -2.17% 0.86% 0.55% 0.55% IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 0.00% 16.50% 16.16% 18.97% 23.18% PBP / PI

28 Wipro Limited 19.99% 17.31% 22.43% 21.25% 21.33% IRR / NPV

215

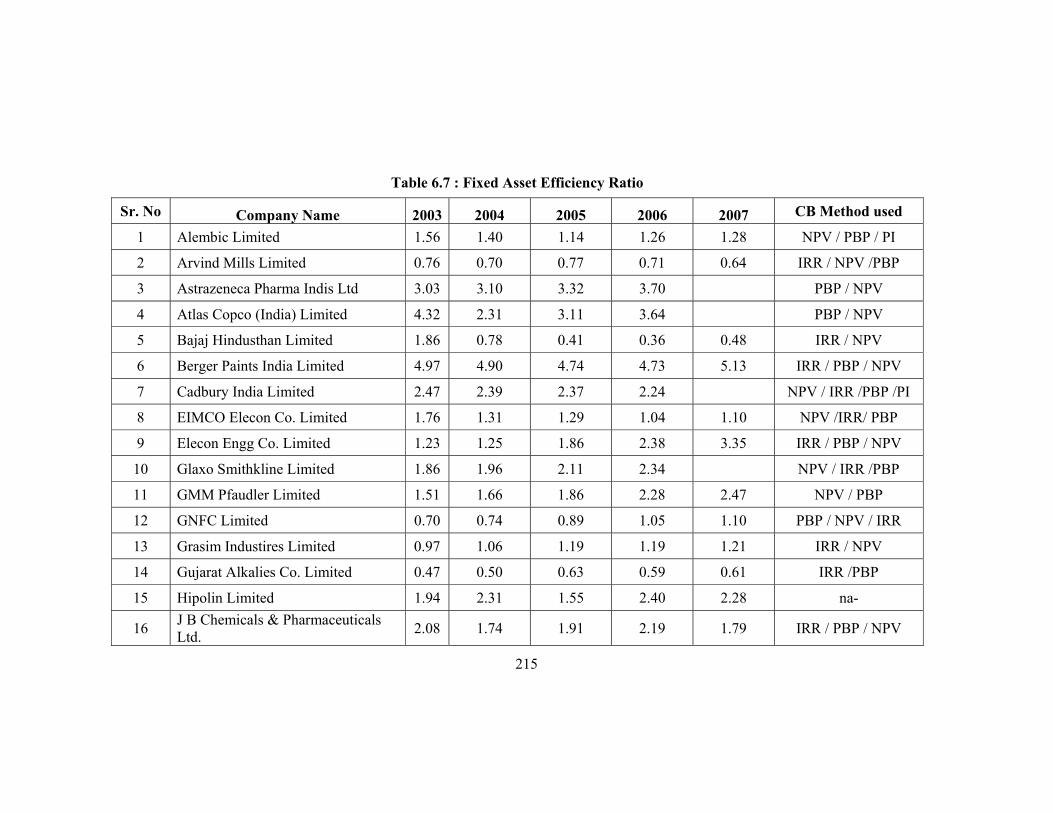

Table 6.7 : Fixed Asset Efficiency Ratio

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

1 Alembic Limited 1.56 1.40 1.14 1.26 1.28 NPV / PBP / PI

2 Arvind Mills Limited 0.76 0.70 0.77 0.71 0.64 IRR / NPV /PBP

3 Astrazeneca Pharma Indis Ltd 3.03 3.10 3.32 3.70 PBP / NPV

4 Atlas Copco (India) Limited 4.32 2.31 3.11 3.64 PBP / NPV

5 Bajaj Hindusthan Limited 1.86 0.78 0.41 0.36 0.48 IRR / NPV

6 Berger Paints India Limited 4.97 4.90 4.74 4.73 5.13 IRR / PBP / NPV

7 Cadbury India Limited 2.47 2.39 2.37 2.24 NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 1.76 1.31 1.29 1.04 1.10 NPV /IRR/ PBP

9 Elecon Engg Co. Limited 1.23 1.25 1.86 2.38 3.35 IRR / PBP / NPV

10 Glaxo Smithkline Limited 1.86 1.96 2.11 2.34 NPV / IRR /PBP

11 GMM Pfaudler Limited 1.51 1.66 1.86 2.28 2.47 NPV / PBP

12 GNFC Limited 0.70 0.74 0.89 1.05 1.10 PBP / NPV / IRR

13 Grasim Industires Limited 0.97 1.06 1.19 1.19 1.21 IRR / NPV

14 Gujarat Alkalies Co. Limited 0.47 0.50 0.63 0.59 0.61 IRR /PBP

15 Hipolin Limited 1.94 2.31 1.55 2.40 2.28 na-

16 J B Chemicals & Pharmaceuticals Ltd. 2.08 1.74 1.91 2.19 1.79 IRR / PBP / NPV

216

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

17 KSB Pumps Limited 1.89 2.24 2.57 2.49 PBP / NPV

18 L&T Limited 1.39 4.99 6.37 5.82 5.38 NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 1.58 1.80 1.73 2.02 PBP / NPV / IRR

20 ONGC Limited 0.60 0.50 0.48 0.61 0.66 IRR / PBP /NPV

21 Panacea Biotec Limtied 2.24 1.85 1.77 1.80 1.66 IRR / NPV / PBP

22 Siemens Limited 2.73 3.47 5.23 5.98 8.36 IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 1.94 1.67 1.58 1.75 1.98 IRR /PBP

24 TATA Steel Limited 0.79 0.90 1.06 1.04 1.07 IRR / PBP / NPV

25 Transpek Industires Limited 0.69 0.85 1.15 1.10 0.96 IRR / NPV / ARR

26 Vadilal Enterprises Limited 3.80 3.81 3.52 3.64 3.59 IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 11.30 13.97 16.59 20.00 PBP / PI

28 Wipro Limited 3.22 3.52 3.61 3.45 3.26 IRR / NPV

217

Table 6.8 : Plant & Machinery Turnover Ratio

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

1 Alembic Limited 1.84 1.63 1.49 1.69 1.90 NPV / PBP / PI

2 Arvind Mills Limited 1.22 1.12 1.24 1.11 1.31 IRR / NPV /PBP

3 Astrazeneca Pharma Indis Ltd 4.97 5.03 5.46 6.63 PBP / NPV

4 Atlas Copco (India) Limited 7.98 11.89 16.41 22.86 PBP / NPV

5 Bajaj Hindusthan Limited 2.92 1.40 1.05 0.92 0.76 IRR / NPV

6 Berger Paints India Limited 9.30 9.41 9.32 8.85 9.37 IRR / PBP / NPV

7 Cadbury India Limited 3.14 3.19 3.28 3.46 NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 2.05 1.49 1.47 1.18 1.24 NPV /IRR/ PBP

9 Elecon Engg Co. Limited 1.57 1.57 2.32 3.07 4.18 IRR / PBP / NPV

10 Glaxo Smithkline Limited 3.01 3.22 3.86 4.25 NPV / IRR /PBP

11 GMM Pfaudler Limited 2.40 2.69 2.81 3.46 3.69 NPV / PBP

12 GNFC Limited 0.75 0.80 0.99 1.15 1.21 PBP / NPV / IRR

13 Grasim Industires Limited 1.20 1.30 1.48 1.52 1.74 IRR / NPV

14 Gujarat Alkalies Co. Limited 0.51 0.54 0.68 0.70 0.68 IRR /PBP

218

Sr. No Company Name 2003 2004 2005 2006 2007 CB Method used

15 Hipolin Limited 2.75 3.26 2.20 3.50 3.37 na-

16 J B Chemicals & Pharmaceuticals Ltd. 3.74 2.98 3.36 4.03 3.36 IRR / PBP / NPV

17 KSB Pumps Limited 2.51 3.01 3.36 3.57 3.32 PBP / NPV

18 L&T Limited 1.95 9.83 10.30 10.42 9.95 NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 1.91 2.25 2.09 2.43 PBP / NPV / IRR

20 ONGC Limited 0.65 0.53 0.53 0.68 0.76 IRR / PBP /NPV

21 Panacea Biotec Limited 8.03 3.53 3.80 4.90 3.84 IRR / NPV / PBP

22 Siemens Limited 6.73 7.93 12.32 16.22 19.65 IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 3.92 3.04 2.74 2.81 3.01 IRR /PBP

24 TATA Steel Limited 0.90 1.06 1.36 1.27 1.42 IRR / PBP / NPV

25 Transpek Industries Limited 0.77 1.00 1.52 1.44 1.24 IRR / NPV / ARR

26 Vadilal Enterprises Limited 4.27 4.24 3.90 4.04 3.93 IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 19.02 21.57 26.61 37.63 PBP / PI

28 Wipro Limited 5.94 7.10 7.66 7.63 7.79 IRR / NPV

219

Table 6.9 : Plant & Machinery to GFA Ratio

Sr. No Company Name Mar 2003 Mar 2004 Mar 2005 Mar 2006 Mar 2007 CB Method used

1 Alembic Limited 84.71% 86.06% 76.43% 74.59% 67.43% NPV / PBP / PI

2 Arvind Mills Limited 62.29% 62.78% 61.88% 64.19% 48.99% IRR / NPV /PBP

3 Astrazeneca Pharma Indis Ltd 61.00% 61.54% 60.71% 55.79% PBP / NPV

4 Atlas Copco (India) Limited 54.12% 19.46% 18.96% 15.94% PBP / NPV

5 Bajaj Hindusthan Limited 63.58% 55.74% 39.22% 38.56% 63.08% IRR / NPV

6 Berger Paints India Limited 53.48% 52.08% 50.85% 53.42% 54.76% IRR / PBP / NPV

7 Cadbury India Limited 78.41% 74.73% 72.20% 64.80% NPV / IRR /PBP /PI

8 EIMCO Elecon Co. Limited 85.93% 87.87% 87.25% 88.75% 89.21% NPV /IRR/ PBP

9 Elecon Engg Co. Limited 78.58% 79.27% 80.20% 77.51% 80.13% IRR / PBP / NPV

10 Glaxo Smithkline Limited 61.64% 60.71% 54.67% 55.07% NPV / IRR /PBP

11 GMM Pfaudler Limited 63.05% 61.75% 66.15% 65.81% 66.96% NPV / PBP

12 GNFC Limited 93.41% 93.05% 90.43% 91.44% 90.74% PBP / NPV / IRR

13 Grasim Industires Limited 81.04% 81.12% 80.22% 78.59% 69.20% IRR / NPV

14 Gujarat Alkalies Co. Limited 93.80% 93.74% 91.98% 84.27% 88.95% IRR /PBP

220

Sr. No Company Name Mar 2003 Mar 2004 Mar 2005 Mar 2006 Mar 2007 CB Method used

15 Hipolin Limited 70.58% 70.82% 70.48% 68.71% 67.66% na-

16 J B Chemicals & Pharmaceuticals Ltd. 55.69% 58.29% 56.77% 54.30% 53.18% IRR / PBP / NPV

17 KSB Pumps Limited 75.51% 74.39% 76.52% 69.68% PBP / NPV

18 L&T Limited 71.24% 50.71% 61.82% 55.86% 54.09% NPV / IRR /PBP

19 Lanxess India (Pvt) Ltd 82.39% 79.70% 82.60% 83.17% PBP / NPV / IRR

20 ONGC Limited 93.43% 93.85% 91.34% 89.63% 87.69% IRR / PBP /NPV

21 Panacea Biotec Limtied 27.91% 52.23% 46.62% 36.76% 43.36% IRR / NPV / PBP

22 Siemens Limited 40.66% 43.73% 42.43% 36.89% 42.56% IRR / PBP / NPV

23 Sun Pharmaceuticals Limited 49.40% 54.79% 57.79% 62.10% 65.62% IRR /PBP

24 TATA Steel Limited 88.14% 84.42% 78.04% 82.16% 75.67% IRR / PBP / NPV

25 Transpek Industires Limited 88.59% 85.32% 75.61% 76.62% 77.21% IRR / NPV / ARR

26 Vadilal Enterprises Limited 88.97% 89.84% 90.26% 90.07% 91.21% IRR / PBP / NPV / PI

27 Volt Amp Transformers Limited 59.44% 64.80% 62.35% 53.15% PBP / PI

28 Wipro Limited 54.24% 49.67% 47.19% 45.19% 41.78% IRR / NPV