Introducing Africa GreenCo April 2017 - Startseite ... · Introducing Africa GreenCo April 2017 Ana...

19

Introducing Africa GreenCo April 2017 Ana Hajduka (Founder & CEO) [email protected] Cathy Oxby (Commercial Director) [email protected]

Transcript of Introducing Africa GreenCo April 2017 - Startseite ... · Introducing Africa GreenCo April 2017 Ana...

Introducing Africa GreenCo

April 2017

Ana Hajduka (Founder & CEO)

Cathy Oxby (Commercial Director)

GreenCo Partners

Grant Support Provided By:

Supported By:

Financial Advisor:

Overview of Africa’s Need and Current Reality

Public

funds

insufficient.

Private

Sector

investment

required

Reality

• Current funding

US$4.6bn p.a. (50%

public sector)

• Only 59 IPPs >5MW in

SSA (excl. RSA)

• 1990 to 2013, only 24.85

GW in SSA (RSA = 9.2

GW)

• AfDB: 160GW

by 2025

• COP 21/AREI:

300GW by 2030

• AfDB: US$60

- 90bn p.a.

The current power purchase paradigm

� Long term bilateral contracts between power producers and

utilities

� Many utilities cash constrained / depend on government for

budgetary support

� Without a creditworthy counterparty or a liquid power market,

developers and lenders require sovereign and/or Development

Finance Institution (DFI) guarantees

� This project-by-project approach is unsustainable:

– DFI resources are insufficient to address Africa’s funding need of

$60-90bn p.a. to achieve universal access by 2025

– Credit enhancement of projects on a one-off basis adds cost and

delays

– Requiring governments to provide guarantees shifts the

creditworthiness issue to the sovereign level

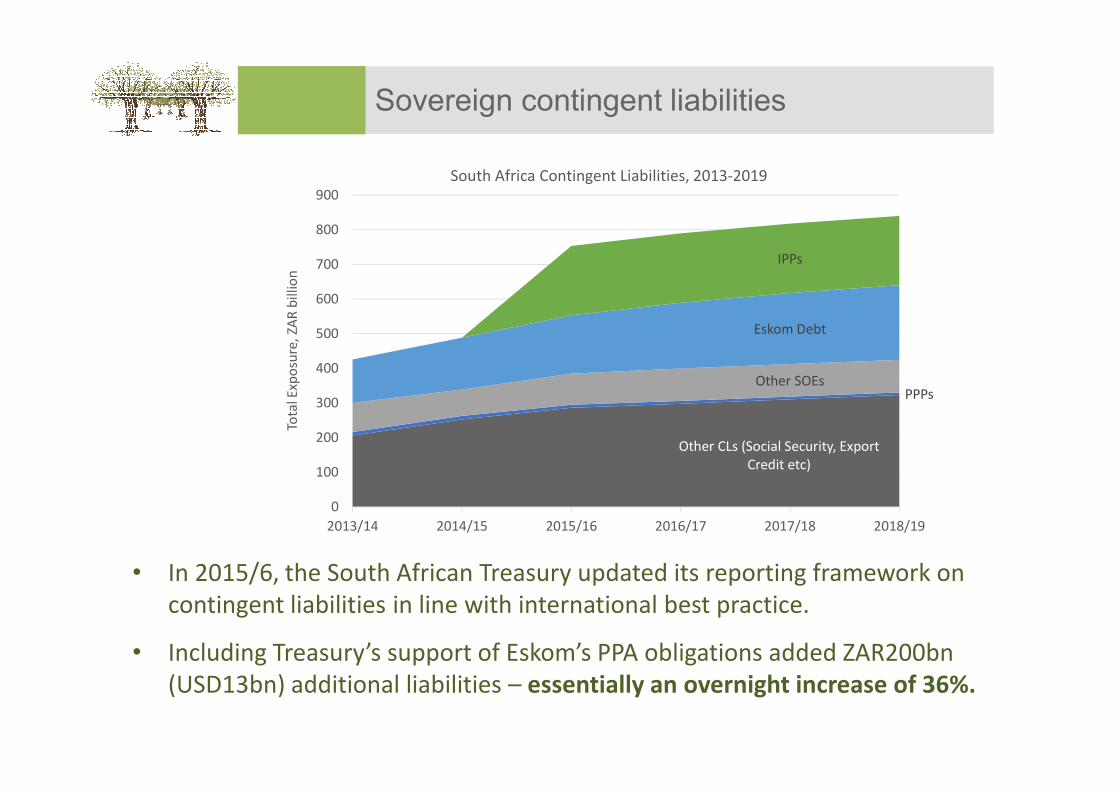

Sovereign contingent liabilities

Other CLs (Social Security, Export

Credit etc)

PPPsOther SOEs

Eskom Debt

IPPs

0

100

200

300

400

500

600

700

800

900

2013/14 2014/15 2015/16 2016/17 2017/18 2018/19

Tota

l Exp

osu

re,

ZAR

bil

lion

South Africa Contingent Liabilities, 2013-2019

• In 2015/6, the South African Treasury updated its reporting framework on

contingent liabilities in line with international best practice.

• Including Treasury’s support of Eskom’s PPA obligations added ZAR200bn

(USD13bn) additional liabilities – essentially an overnight increase of 36%.

Moving away from long-term liabilities – the role

of Regional Electricity Markets

There is already substantial cross-border power trading activity through long term fixed

contracts and short term competitive power markets

� Bilateral contracts dominate

– 18+ contracts in 2015

– 8m MWh traded in 2015

– 94% market share in 2014-15, falling to 80-85% market share in 2016

� Active competitive market

– DAM, IDM and now FPM

– 50-100,000MWh / $3.5-5m traded per month

– Deficit: only 20% of buy orders, and 70% of supply orders transacted

– SAPP forecast 10% growth y-o-y

Ap

r 1

3

Jun

13

Au

g 1

3

Okt

13

De

z 1

3

Feb

14

Ap

r 1

4

Jun

14

Au

g 1

4

Okt

14

De

z 1

4

Feb

15

Ap

r 1

5

Jun

15

Au

g 1

5

Okt

15

De

z 1

5

Feb

16

Ap

r 1

6

0

20

40

60

80

100

120

140

Tra

nsa

cte

d v

olu

me

MW

hT

au

sen

de

SAPP Competitive Trading Activity

No. Supplier Buyer Capacity (MW)

1 HCB Eskom 1600

2 Eskom MOTRACO 950

3 ZESA NamPower 150-80

4 Aggreko ZESCO 148-40

5 Aggreko NamPower 108

6 APR BPC 70 + 35

7 Eskom BPC 300

8 Eskom NamPower As required

9 EDM BPC 50

10 HCB ZESA 150

11 Eskom LEC As required

12 Eskom SEC As required

13 EDM SEC As required

14 EDM ZESCO 150

15 HCB Eskom 250

16 Eskom ZESCO 300

17 Karpowership ZESCO 100 + 300

18 ZESCO NamPower 50

Precedent: Power Trading Corporation of India

Purchased electricity from

independent power projects

(IPPs)

Purchased electricity from

independent power projects

(IPPs)

Sold to State Electricity

Boards, regional utilities &

industrial users

Sold to State Electricity

Boards, regional utilities &

industrial users

Creditworthy one-stop-shop

for IPPs, reducing risk and therefore

tariff

Creditworthy one-stop-shop

for IPPs, reducing risk and therefore

tariff

Diversified risk through

portfolio approach

Diversified risk through

portfolio approach

Provided route to market for surplus power and in case of

default

Provided route to market for surplus power and in case of

default

Helped develop a liquid power market in India

and neighbouring

countries

Helped develop a liquid power market in India

and neighbouring

countries

Attracted private sector investment in IPPs and PTC

itself

Attracted private sector investment in IPPs and PTC

itself

Evolved from creditworthy intermediary

to power trader

Evolved from creditworthy intermediary

to power trader

What is Africa GreenCo?

AND

Intermediary

Creditworthy

Offtaker

Power Pool Participant

(Trader)

o A catalyst to unlock private sector investment in renewable energy

generation projects

o Representing a paradigm shift in the cooperation with international

partners

o A public-private partnership entity

Africa Green Regional Energy: Efficient, New and Creditworthy Offtaker

A Principal in the Market

Host Government

and other investors

AFRICA

GREENCOIPP

PPA

Investors

(& Lenders)

Offtaker End UsersPSA

Host

Government

� Interposed between IPPs and Offtakers

� Creditworthy and independently managed

� Reducing the perceived risk of the project for investors

� Increase the number of bankable projects

� Crowding in commercial capital, including local institutional investors

� Improving the availability and cost of capital

� Technical and legal capacity and framework to execute transactions more efficiently

Operating on a Portfolio Basis

AFRICA

GREENCOInvestors IPP

Capital Utility 2 End Users

PPA PSA Power

Utility 1 End UsersPSA

Power

Private

Offtaker

Industrial

UserPSA Power

IPP

IPP

PPA

PPA

InvestorsCapital

InvestorsCapital

� Achieving structural risk mitigation

� An aggregator and diversifier of risks

� Addressing the inefficiencies of the ‘single buyer, single seller’ model

� Channeling Donor / DFI / MDB willingness to take sovereign risk

Trade

SAPP

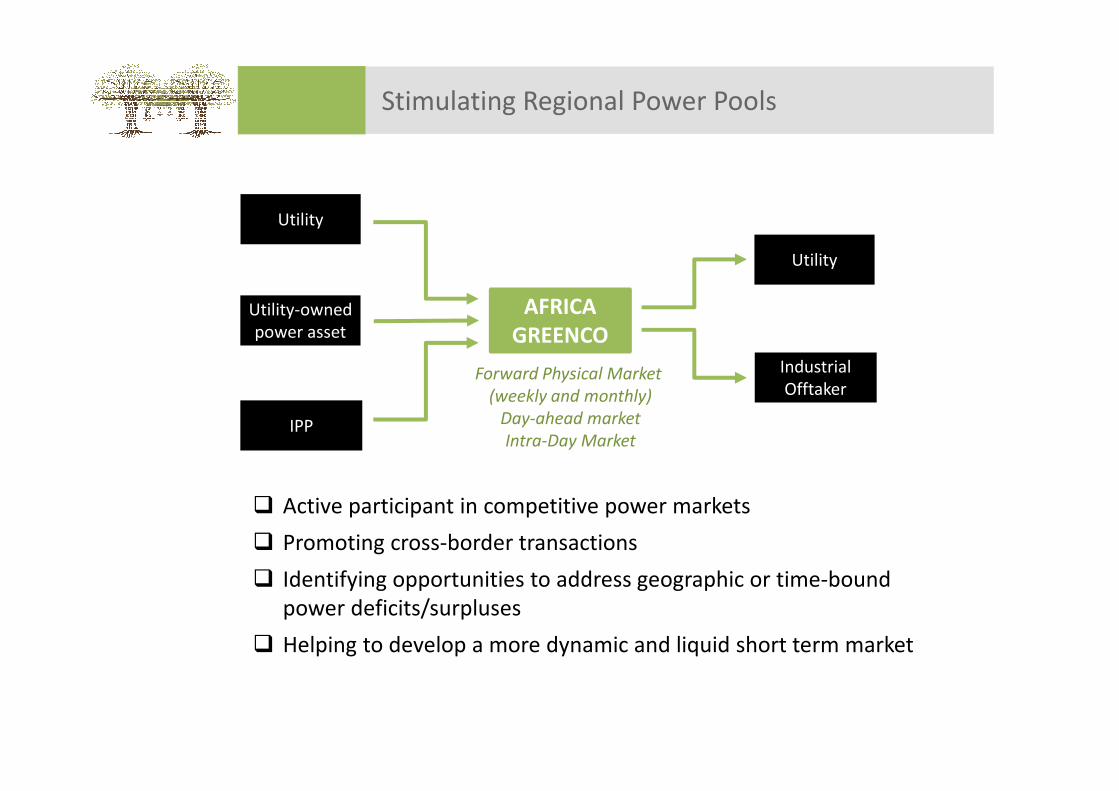

Stimulating Regional Power Pools

AFRICA

GREENCO

IPP

Utility-owned

power asset

Utility

Industrial

Offtaker

Utility

Forward Physical Market

(weekly and monthly)

Day-ahead market

Intra-Day Market

� Active participant in competitive power markets

� Promoting cross-border transactions

� Identifying opportunities to address geographic or time-bound

power deficits/surpluses

� Helping to develop a more dynamic and liquid short term market

Mitigating payment default

AFRICA

GREENCOInvestors IPP

Capital Offtaker 1 End Users

PPA PSA Power

Offtaker 2 End Users

PSA Power

Default on PSA

� Better placed to manage payment default

� Portfolio approach reduces reliance on any single offtaker

� No Government guarantee of utility’s power purchase obligations

� Government retains responsibility for political risks which Africa GreenCo

cannot mitigate

� Risks also mitigated through Africa GreenCo ownership structure

Converting a contingent liability into an asset

13

� Government support of National Utility under bilateral structures

� Government support of National Utility under Africa GreenCo structure

14

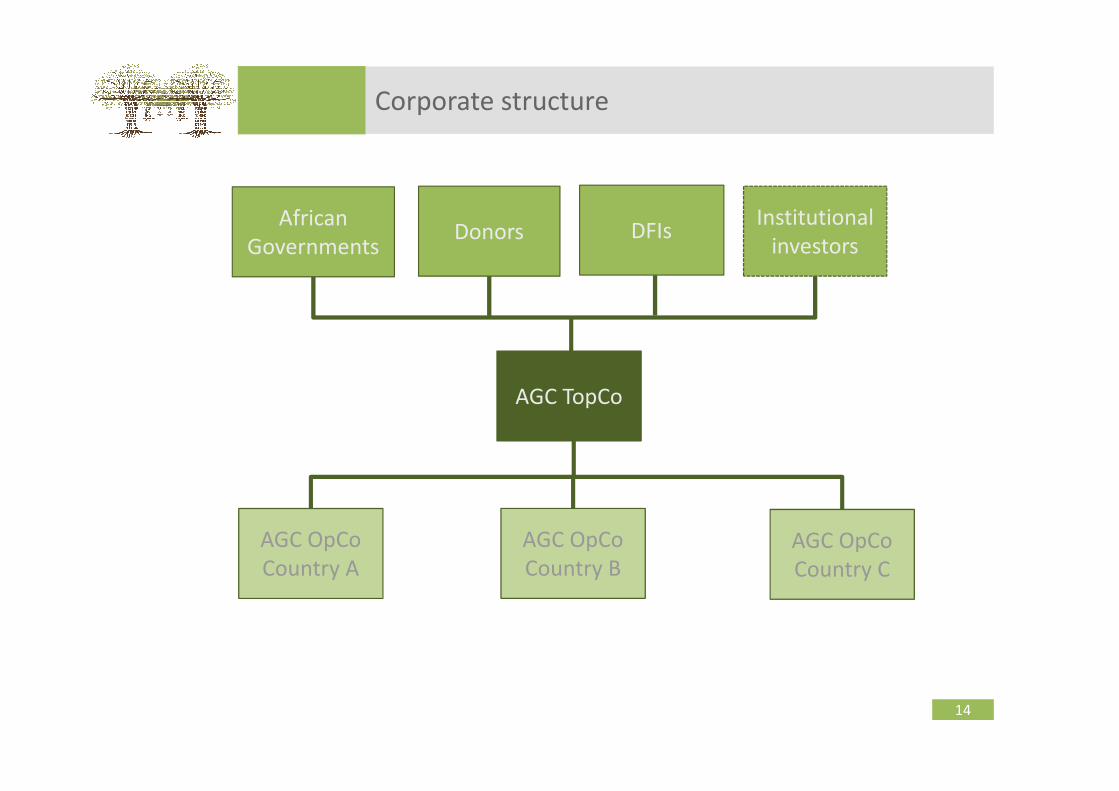

Corporate structure

DFIsInstitutional

investorsDonors

AGC TopCo

AGC OpCo

Country B

African

Governments

AGC OpCo

Country A

AGC OpCo

Country C

Tranched capital structure

� Drivers of tranched structure:

– Ensuring African political and financial ownership of the concept

– Creating a strong capital base through donor, DFI and host government

engagement

– Attracting different types of investor over time

Equity

Liquidity

Facility

Donors

DFIs

MDBs

Host Gvmts

3 years

aggregate PPA

payments1 year PSA payments

from national utility

Equal to

outstanding

debt under

GreenCo’s

PPA

portfolio + 6

months’ PPA

payments

Uncovered Excess

Value of PPA

Evolving Structure and Investors

LIQUIDITY

MDBs/DFIs

EQUITY

African Governments

Int’l Donors

Foundations

LIQUIDITY

International Capital Markets

Insurance and Re-insurance

…

Rating

Structuring

STAGE 1: PILOT

STAGE 2: GROWTH

CAPITAL

African public sector

African institutional investors

Int’l institutional investors

� Host governments/anchor

investors

� Initial deal flow

� Proof of concept

� Greater leverage

� Broader local ownership/buy in

� Financial sustainability

Current Status

Feasibility Study

Proof of Concept

Scale

- COMPLETE

- Based upon hypothetical portfolio of projects

- Includes financial structuring and technical analysis

- Broad industry support obtained (including SADC,

RERA, SAPP, KfW, DBSA, )

- Proof of concept expected in Zambia

- Leverage existing market infrastructure

- Complement parallel initiatives

- Expand capital base to support growing portfolio

- Replicate initial transaction, tailoring strategy to new

markets

Implementation

Plan- Establish a concrete pipeline of projects within SADC

- Detailed technical and regulatory review

- Further develop legal and regulatory structure

- Prepare financial structure & business plan

18

Next Steps Timeline

19

Thank You