INTOSAI Privatisation Working Group (PWG) Technical case study Series 1 – Privatisation 5....

25

INTOSAI Privatisation Working Group (PWG) Technical case study Series 1 – Privatisation 5. Protecting the State’s interests following privatisation

-

Upload

loreen-barnett -

Category

Documents

-

view

223 -

download

4

Transcript of INTOSAI Privatisation Working Group (PWG) Technical case study Series 1 – Privatisation 5....

INTOSAI Privatisation Working Group (PWG)

Technical case study Series 1 – Privatisation

5. Protecting the State’s interests following privatisation

2

Summary

Main methods used to protect the state’s interests

• Clawback provisions• Retention of a shareholding• Special or “Golden” shares• Preferential allocation of shares/Stable core of shareholders

List of Acronyms

ECJ – European Court of JusticeEU – European UnionSOE – State Owned Enterprise

Table of Contents

3

Summary

The state can have many reasons for continuing to have an interest in privatised business, including:

– National Interests: national security, international regulations/liabilities.– Economic Interests: protection of the value of a state’s shareholding, protection of employment, a share of profit made when a business is sold on.

Competition law and, where appropriate, economic regulation, may offer sufficient protection. This technical case study examines protection mechanisms specifically developed for privatisations.

The risks associated with methods for protecting state interests include:

– A lower price received at privatisation– Political interference– Deterring foreign investment– Moral hazard– Complaints of unfair competition

4

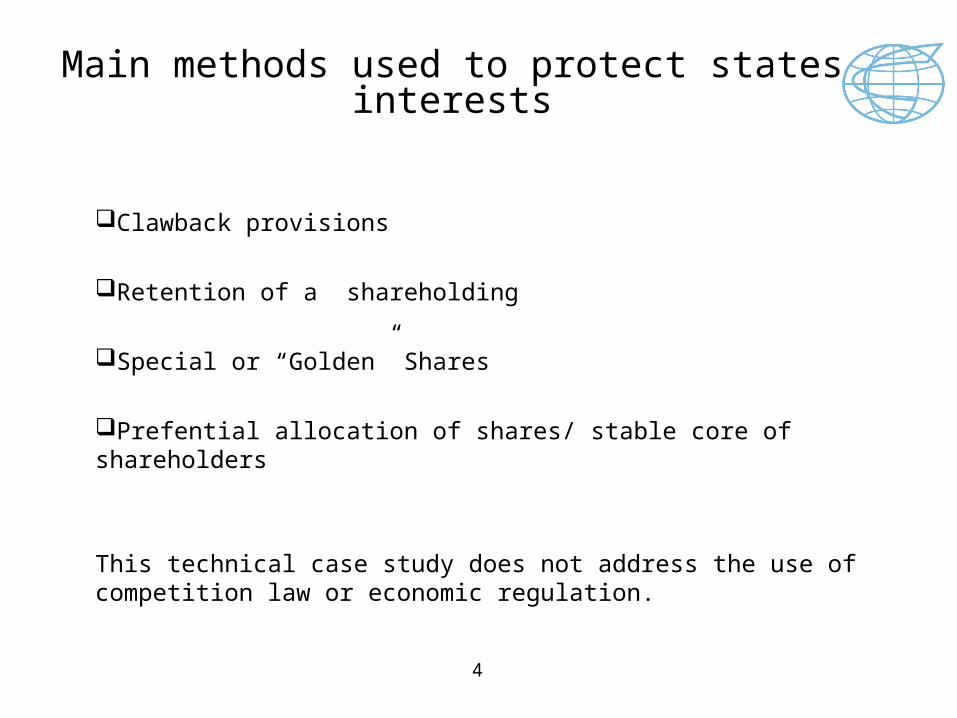

Main methods used to protect states interests

Clawback provisions

Retention of a shareholding

Special or “Golden” Shares

Prefential allocation of shares/ stable core of shareholders

This technical case study does not address the use of competition law or economic regulation.

5

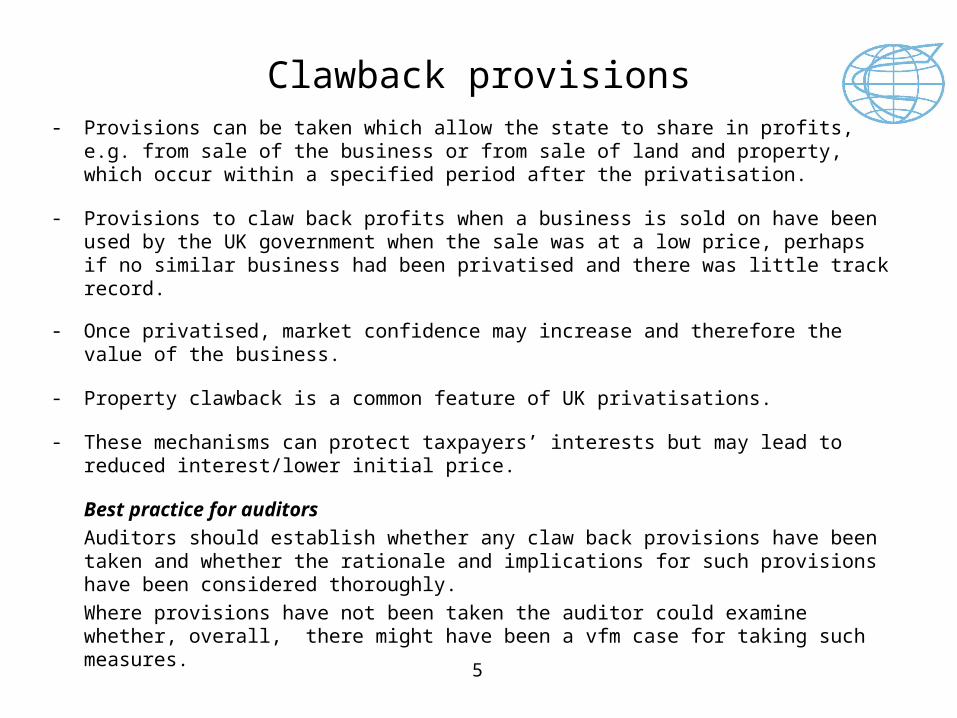

Clawback provisions- Provisions can be taken which allow the state to share in profits, e.g. from sale of the

business or from sale of land and property, which occur within a specified period after the privatisation.

- Provisions to claw back profits when a business is sold on have been used by the UK government when the sale was at a low price, perhaps if no similar business had been privatised and there was little track record.

- Once privatised, market confidence may increase and therefore the value of the business.

- Property clawback is a common feature of UK privatisations.

- These mechanisms can protect taxpayers’ interests but may lead to reduced interest/lower initial price.

Best practice for auditors

Auditors should establish whether any claw back provisions have been taken and whether the rationale and implications for such provisions have been considered thoroughly.

Where provisions have not been taken the auditor could examine whether, overall, there might have been a vfm case for taking such measures.

6

Retention of a Shareholding

Rationale

There could be many reasons for retaining a Government shareholding.

• Sometimes a shareholding is retained specifically to protect national interests.

• Often a shareholding is retained only temporarily:

- if market capacity is not sufficient to allow full privatisation

- for value for money reasons if the expectation is that a better price would be achieved in later sales

- if a strategic partner is used to help prepare the business for full privatisation.

7

Retention of a Shareholding (cont.)

An INTOSAI survey carried out in 2000 looked at 9 states with minority shareholdings. Each state had different objectives that it wished to fulfil, see table.

Pursuing strategic economic goals was an important objective for the majority of the states that retained shareholdings in privatised business.

States’ objectives for retaining minority shareholdings

No. reported (out of 9)

Pursue strategic economic goals 6

Protect the taxpayer’s investments 5

Ensure the business is soundly run on a commercial basis

5

Raise money for the state through the sale of shares

5

Promote growth in employment 4

Obtain taxes and dividends from the efficiency of the private sector

3

Promote shareholding by the general public

3

Increase international investment 2

Other objectives 2

Source: INTOSAI survey 2000

8

Retention of a Shareholding (cont.)

RightsThe State tends to have the same rights as any other minority shareholder (dependent on the proportion of shares held, provisions of shareholder agreements, the Articles of Association of the company, etc.). These include powers to:

Veto major decisions Request the company to be wound up Block a share redemption by the majority shareholder Request certain types of shareholder meeting.

9

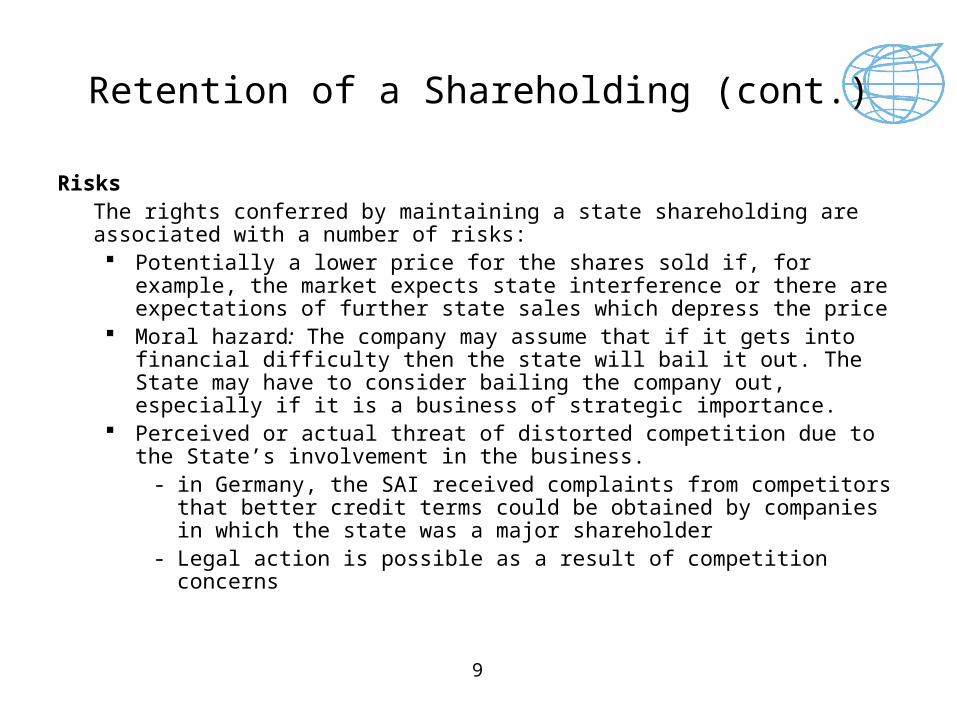

Retention of a Shareholding (cont.)

RisksThe rights conferred by maintaining a state shareholding are associated with a number of risks: Potentially a lower price for the shares sold if, for example, the market expects

state interference or there are expectations of further state sales which depress the price

Moral hazard: The company may assume that if it gets into financial difficulty then the state will bail it out. The State may have to consider bailing the company out, especially if it is a business of strategic importance.

Perceived or actual threat of distorted competition due to the State’s involvement in the business.

- in Germany, the SAI received complaints from competitors that better credit terms could be obtained by companies in which the state was a major shareholder

- Legal action is possible as a result of competition concerns

10

Retention of a Shareholding (cont.)

At the end of 2005, European governments’ ultimate ownership in listed firms was worth €295 billion.

The French government had the largest proportion, with a portfolio value exceeding €118 billion.

There was a high concentration of government ownership in strategic sectors

(see table 1).

Source: Privatization Barometer newsletter, issue 4

Sector Total stake value (bn €)

Utilities 84.73

Telecommunications 67.18

Oil & Gas 66.96

Banking, Finance & Insurance

29.68

Manufacturing & Other Industrials

16.02

Aerospace & Defence 13.95

Transportation Industry 11.43

Trade & Services Industry

3.61

Total 293.57

Table 1 – European governments had almost €300 bn invested in strategic

industries by end 2005.

11

Retention of a Shareholding (cont.)GovernanceResponsibility for the exercise of state ownership rights varies between countries.

There are three main models - the decentralised or sector model, the centralised model and the dual model:

– in the decentralised model responsibility lies with sector ministries.

– in the centralised model responsibility lies with one government body.

– a few countries, such as the Czech Republic, use more than one model.

Reforms are underway in many countries, largely to achieve a centralised model. This is often seen as complementary to privatisation – to strengthen the performance of Government as a shareholder and to improve the incentives on the businesses to be efficient.

12

Retention of a Shareholding (cont.)Organisation and evolution of the ownership function in OECD countries

Source: OECD

13

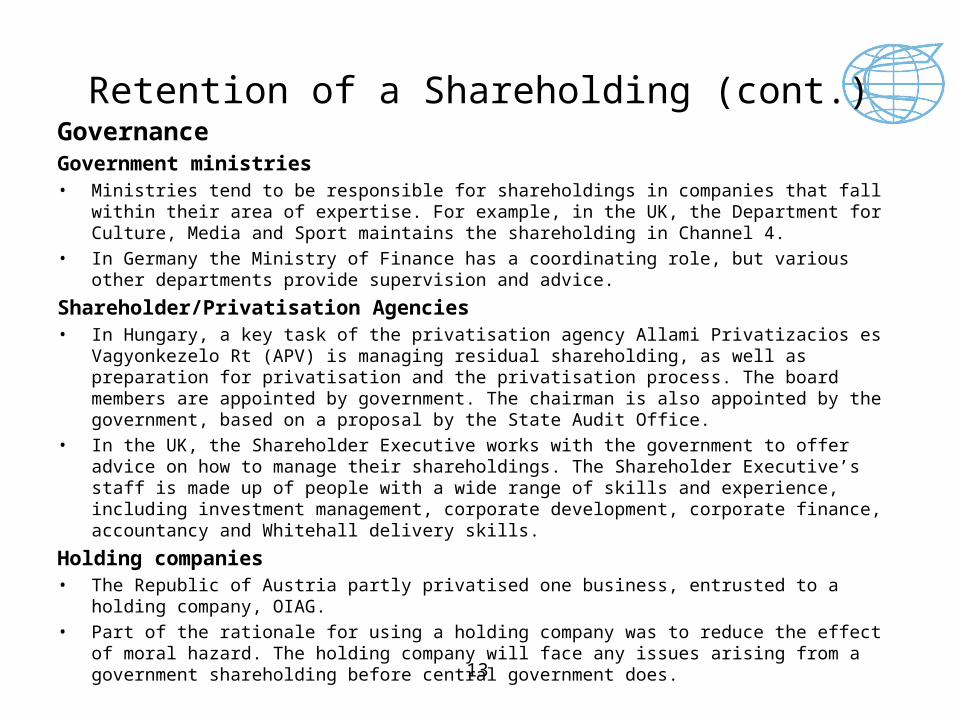

Retention of a Shareholding (cont.)GovernanceGovernment ministries• Ministries tend to be responsible for shareholdings in companies that fall within their area of

expertise. For example, in the UK, the Department for Culture, Media and Sport maintains the shareholding in Channel 4.

• In Germany the Ministry of Finance has a coordinating role, but various other departments provide supervision and advice.

Shareholder/Privatisation Agencies • In Hungary, a key task of the privatisation agency Allami Privatizacios es Vagyonkezelo Rt (APV)

is managing residual shareholding, as well as preparation for privatisation and the privatisation process. The board members are appointed by government. The chairman is also appointed by the government, based on a proposal by the State Audit Office.

• In the UK, the Shareholder Executive works with the government to offer advice on how to manage their shareholdings. The Shareholder Executive’s staff is made up of people with a wide range of skills and experience, including investment management, corporate development, corporate finance, accountancy and Whitehall delivery skills.

Holding companies• The Republic of Austria partly privatised one business, entrusted to a holding company, OIAG.

• Part of the rationale for using a holding company was to reduce the effect of moral hazard. The holding company will face any issues arising from a government shareholding before central government does.

14

Retention of a Shareholding (cont.)

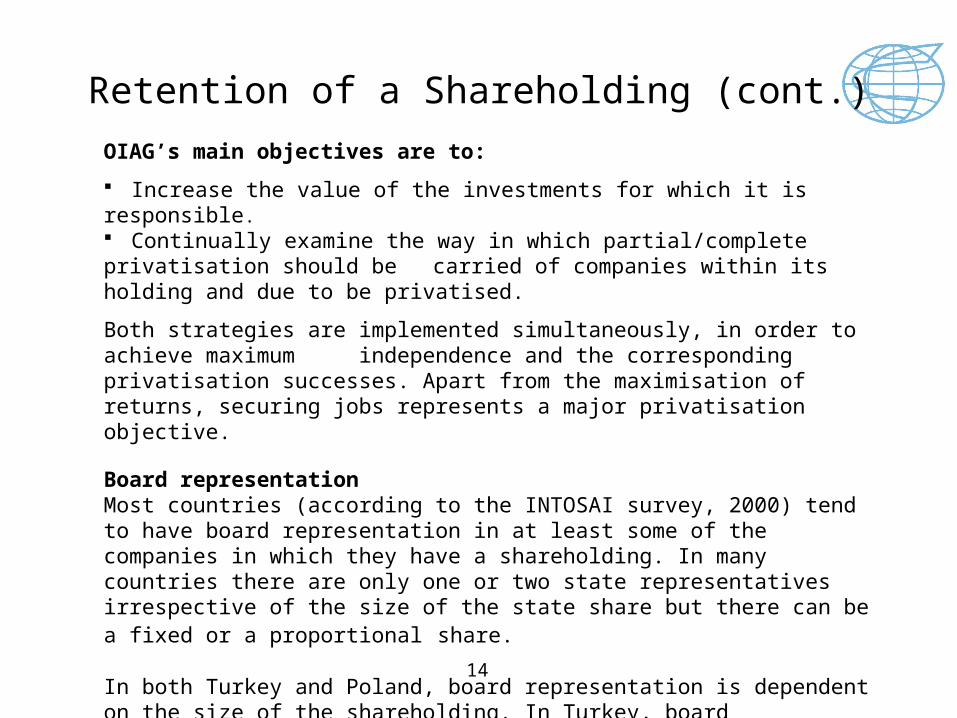

OIAG’s main objectives are to:

Increase the value of the investments for which it is responsible. Continually examine the way in which partial/complete privatisation should be carried of companies within its holding and due to be privatised.

Both strategies are implemented simultaneously, in order to achieve maximum independence and the corresponding privatisation successes. Apart from the maximisation of returns, securing jobs represents a major privatisation objective.

Board representationMost countries (according to the INTOSAI survey, 2000) tend to have board representation in at least some of the companies in which they have a shareholding. In many countries there are only one or two state representatives irrespective of the size of the state share but there can be a fixed or a proportional share.

In both Turkey and Poland, board representation is dependent on the size of the shareholding. In Turkey, board representation is fulfilled by members of a holding company rather than a state ministry. This is done in order to reduce the risk of moral hazard

15

OECD guidelines on corporate governance for state owned entities (SOE)

Use of the OECD guidelines is likely to help mitigate the risks associated with the retention of a state shareholding in a privatised business. The guidelines cover the following main issues:

Transparency of operation

Focus on management of the key risks facing each organisation rather than

imposing standard operational controls across various shareholdings

Empower and professionalise management boards through a clear and consistent ownership policy without interference in the day to day operation of the company

Clear basis and legal framework for obligations relating to general and public service provision when these are to be provided by the SOE

Clearly identified ownership function within government which is accountable to

the Country’s representative bodies

Ensure equal treatment of all minority shareholders, along with establishment of

an effective redress mechanism

Encourage SOE to develop arms length arrangements with its banks and other financial institutions

16

Retention of a Shareholding (cont.)Best Practice for AuditorsAuditors should: Examine the rationale for retaining a state shareholding in privatised business and whether the

stated objectives have been achieved. These objectives should be assessed on a consistent basis from year to year and the results reported in a prominent section of the bodies annual report

Review the terms of reference under which the Governments shareholder teams have set out their relationship with the management team, ensuring that this is clearly understood by all parties and incorporate the risks within the audit strategy. These terms of reference could take the form of a single document (“governance letter” or similar describing the rights and levers held by the shareholder, and how they intend to use them).

Examine whether the corporate governance arrangements associated with the holding are appropriate. In particular the OECD guidelines on corporate governance for state owned entities could be used as a best practice checklist

Review the legislation under which the state’s shareholdings have been held and ensure that the level of review and control which the holdings have been held by shareholding teams is in line with their delegated authority

Where SOE’s have been delegated obligations for general and public service provision which are outside their core business (such as subsidised services), ensure that these services have been provided to the standard and extent instructed under legislation/governing documentation and, where not, evaluate the risks this poses to the enterprise.

17

Special or “Golden” SharesDefinition

• These are special shares, used to retain some control over privatised companies. • They can be held without the government having any other stake in the company.• European Union Treaty rules only allow EU governments to use such powers if there are

strong public interest or strategic service needs due to an European Court of Justice ruling in May 2003 on the free movement of capital within the single European market..

• Special shares may be permanent, where the state has the right to hold the share until it feels it is time to dispose of it, or temporary, losing its powers after a pre-determined period when strong corporate governance may have been established.

– In Poland all golden shares are of a temporary nature and expire when the terms of the buyer’s commitments are fulfilled.

Rationale • The main objective is usually to protect national security, but can also be used to protect

economic interests or to ensure provision of public services. Rights

• As with minority shareholdings, the rights vary from country to country. The powers they confer tend to incorporate at least some of the following:

– The right to block changes in corporate control.– The right to veto decisions in general meetings and influence fundamental company

decisions.– The right to influence and restrict acquisition of shareholdings.– Certain decisions or transactions can only be passed if authorised by the State.– The right to ensure a number of its citizens are represented at Board level.

18

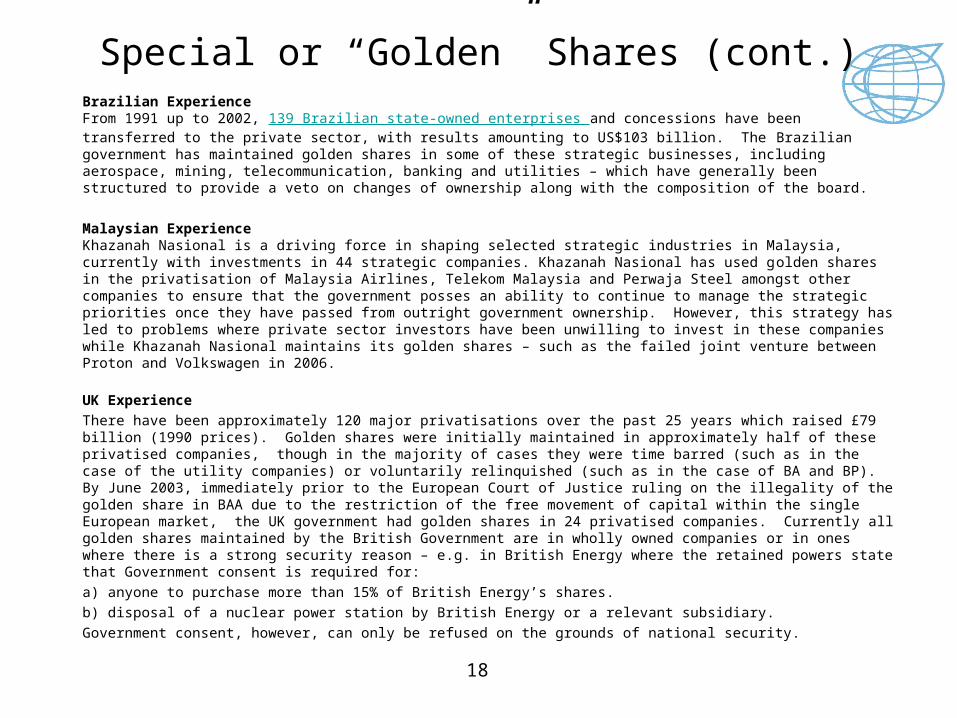

Special or “Golden” Shares (cont.)Brazilian ExperienceFrom 1991 up to 2002, 139 Brazilian state-owned enterprises and concessions have been transferred to the private sector, with results amounting to US$103 billion. The Brazilian government has maintained golden shares in some of these strategic businesses, including aerospace, mining, telecommunication, banking and utilities – which have generally been structured to provide a veto on changes of ownership along with the composition of the board.

Malaysian ExperienceKhazanah Nasional is a driving force in shaping selected strategic industries in Malaysia, currently with investments in 44 strategic companies. Khazanah Nasional has used golden shares in the privatisation of Malaysia Airlines, Telekom Malaysia and Perwaja Steel amongst other companies to ensure that the government posses an ability to continue to manage the strategic priorities once they have passed from outright government ownership. However, this strategy has led to problems where private sector investors have been unwilling to invest in these companies while Khazanah Nasional maintains its golden shares – such as the failed joint venture between Proton and Volkswagen in 2006.

UK Experience

There have been approximately 120 major privatisations over the past 25 years which raised £79 billion (1990 prices). Golden shares were initially maintained in approximately half of these privatised companies, though in the majority of cases they were time barred (such as in the case of the utility companies) or voluntarily relinquished (such as in the case of BA and BP). By June 2003, immediately prior to the European Court of Justice ruling on the illegality of the golden share in BAA due to the restriction of the free movement of capital within the single European market, the UK government had golden shares in 24 privatised companies. Currently all golden shares maintained by the British Government are in wholly owned companies or in ones where there is a strong security reason – e.g. in British Energy where the retained powers state that Government consent is required for:

a) anyone to purchase more than 15% of British Energy’s shares.

b) disposal of a nuclear power station by British Energy or a relevant subsidiary.

Government consent, however, can only be refused on the grounds of national security.

19

Special or “Golden” Shares (cont.)Spanish experience.The Spanish Government has carried out approximately 80 major privatisations over the past 20 years which raised

£25 billion (1990 prices). In common with other Governments, the Spanish Government maintained golden shares in a large number of these firms in order to maintain a veto over their future ownership and strategic direction – an area of particular concern in the telecommunication and utility industries. However, following pressure from the European Court of Justice and the maturing of the former state owned entities, the Spanish Government is in the process of disposing of a number Golden Shares, while allowing others to lapse where they were originally time-barred or reducing their rights.

– In November 2005, the Spanish Government decided to dispose of its golden shares protecting four privatised companies from foreign takeovers, after pressure from the European Union. Golden shares in Telefónica, the former telecommunications monopoly, Endesa, Spain's largest utility, Repsol, an oil and gas group, and Iberia airlines, gave the Spanish government an effective veto over the sale of more than 10 per cent of these companies.

– The Government still has its share in Endesa (which expires in June 2007), but new legislation has been introduced to state that the government cannot veto a takeover by the German utility company E.O.N.

Zambian ExperienceThe Zambian Government has used golden shares as a regulatory tool in a number of joint ventures and partial privatisations in the electricity generation, gas distribution and mining sectors – particularly in the case of joint ventures between it and the private sector.

20

Special or “Golden” Shares (cont.)RisksThe use of golden shares is associated with a number of risks: May lead to a reduced price at privatisation. May deter foreign/private investors due to apprehension over state’s control – such as the

Malaysian experience with the failed joint venture between Proton and Volkswagen in 2006. Other private companies may perceive that the involvement of the state as a shareholder distorts

competition, resulting in legal action/investor uncertainty. Moral hazard: the business and/or its shareholders may feel that the state is obliged to help the

company out of difficulties and act accordingly. Decreased flexibility of the firms in exploiting economies of scale through industry consolidation

where use of the Golden Share prevents bodies building up a controlling influence in the privatised firms

They have an uncertain future: The use of golden shares is becoming more restricted in EU countries. This has resulted from various rulings of the European Court of Justice (ECJ).

In June 2002, the ECJ declared as illegal the Golden Shares held by the French Government in the former state oil company Societe Nationale Elf-Acquitaine. This resulted in a number of infringement cases against the governments of other EU Member States. On 13 May 2003, the ECJ ruled that the UK government was in breach of EU Law by maintaining golden shares in the airport operator BAA.

The ECJ aims to reduce cross-border investments barriers.

21

Special or “Golden” Shares (cont.)

Best Practice for Auditors

Auditors should examine the legal basis for the measures taken. In particular, in EU countries they should observe whether ECJ rulings have been adhered to.

After the recent rulings of the ECJ, there has developed an important divide between those Golden Shares that are permitted and those that are forbidden.Ultimately, Golden Shares are permitted when they can be justified in terms of national security or protecting the general interest. They must be shown to be:

•Non-discriminatory: No nationality is to be discriminated against.•Non-discretionary: The public must be informed with regards to the basis on which a Golden Share right can be exercised.

•Proportional: The restriction in question must be proportionate to the objective pursued.

Auditors should also examine the rationale for the use of Special Shares and whether the objectives have been achieved.

22

Preferential Allocation of Shares/ Stable Core of Shareholders

Rationale for preferential allocation to a group of national investors

There are several possible reasons, including:• To protect businesses against hostile takeover, especially in strategic industries – though this may result in lower proceeds and a lower share price.• To promote a smooth transition from Public to Private ownership.• Initially at least, to ensure that new shareholders meet other objectives such as maintaining national and/or institutional ownership of the company.• Reduced costs in comparison to a full IPO.

Rationale for preferential allocation to employees

There are many reasons for preferential allocation of shares to employees. In the context of protection of state interests it is likely that the state will see a substantial employee holding as helping to protect the business from unwelcome takeover.

The state may attempt to protect its interests by preferentially allocating a proportion of shares to a stable core of shareholders. These shareholders are usually a group of national investors, such as banks and allied industrial groups. Governments may also see the allocation of a substantial proportion of shares to employees as attractive.

23

Preferential Allocation of Shares/Stable Core of Shareholders (cont.) - Case Study

Austrian 46%

North American 24%

European investors 17%

Employees 10%

Rest of world 3%

Table 3 – Shareholders of Voestalpine and diagram of share-price growth

Voestalpine, Austria’s largest steel company, was privatised over a ten year period ending in 2005 with ÖIAG [the state holding group], disposing of its final 15% in August 2005 for €425m.

The sales were carried out in a climate of controversy, with many Austrian voters favouring shares remaining within Austrian hands. As a result, the ÖIAG assembled a network of Austrian investors who already owned around 30% of Voestalpine to bid on the 33% offering in 2003.

As a result Voestalpine’s ownership base has remained in the control of Austrian investors. Its share price post disposal by the government has been strong.

24

Preferential Allocation of Shares/ Stable Core of Shareholders

RisksThere are various risks that come with preferential allocation of shares:

• Can be damaging to good corporate governance as they tend to create exclusive cross-shareholdings.

• May miss the potential for capital market development.

• May burden core shareholders with unproductive assets.

• May deter foreign investors.

• May reduce proceeds raised

25

Preferential Allocation of Shares/ Stable Core of Shareholders (cont.)

Best Practice for Auditors

• Examine the rationale for allocating shares to a stable core of shareholders and whether the objectives have been achieved.

• Where shares that have been allocated preferentially and have been offered at a discount, examine whether the justification and financial implications of this course of action has been suitably communicated to stakeholders.

• Examine the potential consequences of preferential allocation on the interest of other investors, the price achieved and costs.

• Review post deal outcome against deal objectives – e.g. such as maintaining a national shareholding base of the company versus foreign control.