INTERNATIONAL FINANCIAL ACCOUNTING AND REPORTING Elena Kozeltseva PhD, Associate professor Moscow...

58

INTERNATIONAL FINANCIAL ACCOUNTING AND REPORTING Elena Kozeltseva PhD, Associate professor Moscow State University 1 Fudan University School of Economics

-

Upload

preston-bailey -

Category

Documents

-

view

218 -

download

1

Transcript of INTERNATIONAL FINANCIAL ACCOUNTING AND REPORTING Elena Kozeltseva PhD, Associate professor Moscow...

INTERNATIONAL FINANCIAL ACCOUNTING AND REPORTING

Elena Kozeltseva

PhD, Associate professor

Moscow State University

1

Fudan UniversitySchool of Economics

International financial accounting and reporting

Introduction to International Accounting Conceptual Framework Presentation of financial statements Revenue recognition Inventories Property, plant and equipment Intangible assets Provisions Equity Statement of cash flows

2

List of readings1. International Financial Reporting Standards (IFRSs)

2008. – IASCF, 2008.2. Alexander D., Britton A., Jorissen A.International

Financial Reporting and Analysis. – 3rd edition, Thomson Learning, 2007.

3. Alexander D., Nobes C. Financial Accounting. An International Introduction. – Pearson Education Limited, 2001.

4. Keiso D., Weygandt J., Warfield T., Intermediate Accounting.- 12-th ed., John Wiley & Sons, Inc., 2008

Websites:www.iasb.org.ukwww.iasplus.com

3

Accounting is an information system that measures, processes, and communicates financial information about an identifiable economic entity to interested parties for making economic decisions.

Bookkeeping is the means of recording transactions and keeping records.

Introduction to International Accounting

4

USERS OF ACCOUNTING INFORMATION

Those outside the business enterprise

Those who manage a business

With direct financial interest

With indirect financial interest

5

Comparing Financial accounting with Management accounting

Primary users of information

Types of accounting systems

Restrictive guidelines

Units of measurement

Focal point analysis

Frequency of reporting

Degree of reliability

6

Financial accounting standard-setting process

European CommunityAsian & Pacific region AfricaSouth America

National level

International Accounting Standards Committee Foundation (IASCF)International Federation of Accountants (IFAC)International Organization of Securities Commissions (IOSCO)Organization for Economic Cooperation and Development (OECD)

US GAAP (Generally accepted accounting principles)National GAAP

Regional level International

level

7

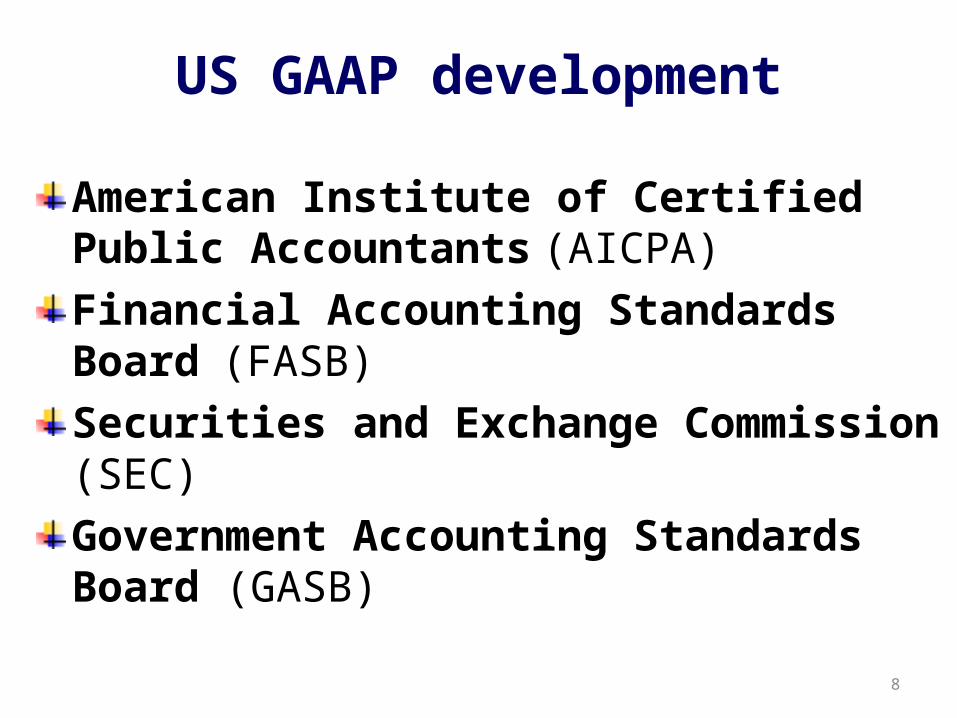

US GAAP development

American Institute of Certified Public Accountants (AICPA)

Financial Accounting Standards Board (FASB)

Securities and Exchange Commission (SEC)

Government Accounting Standards Board (GASB)

8

FASB pronouncements

Statements of Financial Accounting Concepts (SFAC)

Statements of Financial Accounting Standards (SFAS)

Interpretations/Staff positions

Technical Bulletins

Emerging Issues Task Force Statements (EITF)

9

US GAAP hierarchyA FASB

Standards and Interpretations

Accounting Principles Board Opinions

AICPA Accounting Research Bulletins

B FASB technical bulletins

AICPA Industry Audit and Accounting Guides

AICPA

Statements of Positions

C FASB Emerging Issues Task Force Statements

AICPA practice bulletins

D AICPA Accounting Interpretations

FASB Implementation Guides

Widely recognized and prevalent industry practice

10

Financial accounting regulation in Russia

Federal law on accounting

National accounting standards developed and issued by the Ministry of Finance

Normative acts regulating specific accounting issues

Accounting policy

11

Causes of differences between national accounting systems

Provision of finance Legal systems Link between accounting and taxation Accounting profession Cultural differences Geographical position …

12

ACCOUNTING MODELS

Continental European model

Anglo-American model

USAGreat BritainNetherlandsCanadaAustraliaIndiaSouth Africa…

FranceGermanyItalyAustriaBelgium…

13

European accounting directives

14

The Fourth Council Directive 78/660/EEC of 25 July of 1978 on the annual accounts of certain types of companies

The Seventh Council Directive 83/349/EEC of 13 June 1983 on consolidated accounts

…….

ec.europa.eu/internal market/accounting

International Accounting Standards Committee

15

IASC was created in 1973 by agreement between the professional accountancy bodies in nine countries

Australia NetherlandsCanada Great BritainFrance IrelandGermany USAJapan Mexico

(I A S C)

IASB Structure (as a result of structural changes in 2001)

16

IASC Foundation (Trustees)

International AccountingStandards Board (IASB)

International Financial Reporting Interpretations

Committee (IFRIC)

Standards Advisory Council (SAC)

The objectives of the IASC Foundation are:

to develop a single set of high quality, understandable, enforceable and globally accepted international financial reporting standards (IFRSs) through its standard-setting body, the IASB;

to take account of the financial reporting needs of emerging economies and small and medium-sized entities (SMEs); and

to bring about convergence of national accounting standards and IFRSs to high quality solutions.

17www.iasb.org

International Financial Reporting Standards (IFRSs)

18

International Accounting Standards (IAS 1- 41) International Financial Reporting Standards (IFRS 1-8)Interpretations originated by the IFRIC (or its predecessor, the former Standing Interpretations Committee –SIC)

Framework for the Preparation and Presentation of Financial Statements

Standard – setting due process

19

1. Setting the agenda

2. Project planning

3. Development and publication of a discussion paper

4. Development and publication of an exposure draft

5. Development and publication of an IFRS

6. Procedures after an IFRS is issuedIFRSs

Use of IFRS

For 172 jurisdictions for domestic listed companies:

IFRSs not permitted — 33 jurisdictions IFRSs permitted — 25 jurisdictions IFRSs required for some — 5 jurisdictions IFRSs required for all — 90 jurisdictions No stock exchange — 19 jurisdictions

www.iasplus.com

20

Convergence between IFRSs and US GAAP

2002 The “Norwalk Agreement”

2006 Memorandum of Understanding (MoU)

that described a programme to achieve improvements in accounting standards, and substantial convergence between IFRSs and US generally accepted accounting principles (GAAP)

2007 SEC issued its final rule on Acceptance from Foreign Private Issuers of Financial Statements Prepared in Accordance with International Financial Reporting Standards without Reconciliation to US GAAP

21

Harmonization of financial accounting and reporting in Europe

1995 Accounting Harmonization: a new strategy vis-à-vis international harmonization

1998 IAS allowed for consolidated financial statements in several European countries (Germany, France etc.)

1999 EU Financial Reporting Strategy: the way forward. Communication from the Commission to the Council and the European Parliament

2000 Amendments to EU Accounting Directives

19 July 2002

Regulation (EC) No 1660/2002 of the European Parliament and of the Council of 19 July 2002 on the application of international accounting standards

22

IFRSs endorsement mechanism in Europe

I. Legal level

Accounting Regulation Committee – ARC

II. Technical level

European Financial Reporting Advisory Group – EFRAG)

www.efrag.org

23

CONCEPTUAL FRAMEWORK

24

The objective of financial statementsUnderlying assumptionsThe qualitative characteristics that determine

usefulness of information in financial statements

The definition, recognition, and measurement of the elements from which financial statements are constructed

Concepts of capital and capital maintenance

25

Framework for Preparation and Presentation of Financial Statements

Underlying assumptions

26

Accrual basis of accounting

The effects of transactions and other events are recognized when they occur (and not as cash or its equivalent is received or paid), and they are recorded in the accounting records and reported in the financial statements of the periods to which they relate.

Going concern

The financial statements are normally prepared on the assumption that the entity has neither intention nor need to liquidate or curtail materially the scale of its operations, but will continue in operation for the foreseeable future.

Basic principles and concepts (accounting practice)

Double entry Money measure Separate entity/Economic entity Cost principle/Historical cost Periodicity/Accounting period …

27

Qualitative characteristics of financial statements

28

Usefulness of information in financial statements

Relevance Reliability Comparability Understandability

faithfulness

substance over form

neutrality

prudence

completeness

materiality Constraints timeliness

balance between benefit and cost

balance between qualitative

characteristics

Elements of financial statements

29

Assets. An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

Liabilities. Liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

Equity. Equity is the residual interest in the assets of the entity after deducting all its liabilities.

Elements of financial statements

30

Income. Income is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants.

Expenses. Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decrease in equity, other than those relating to distributions to equity participants.

Recognition of the elements of financial statements

it is probable that any future economic benefit associated with the item will flow to or from the entity; and

the item has cost or value that can be measured with reliability.

31

An item that meets the definition of an element should be recognized (i.e., incorporated in the financial statements) if:

Measurement of the elements of financial statements

Historical cost

Current cost

Realizable/Settlement value

Present value32

Measurement of the elements of financial statements

33

Historical cost.Assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given to acquire them at the time of their acquisition.

Liabilities are recorded at the amount of proceeds received in exchange for the obligation, or in some circumstances (for example, income tax), at the amounts of cash or cash equivalents expected to be paid to satisfy the liability in the normal course of business.

Measurement of the elements of financial statements

34

Current cost.Assets are carried at the amount of cash or cash equivalents that would have to be paid if the same or an equivalent asset was acquired currently.

Liabilities are carried at the undiscounted amount of cash or cash equivalents that would be required to settle the obligation currently.

Measurement of the elements of financial statements

35

Realizable (settlement) value.Assets are carried at the amount of cash or cash equivalents that could currently be obtained by selling the asset in an orderly disposal.

Liabilities are carried at their settlement values; that is, the undiscounted amounts of cash or cash equivalents expected to be paid to satisfy the liabilities in the normal course of business.

Measurement of the elements of financial statements

36

Present value.Assets are carried at the present discounted value of the future net cash inflows that the item is expected to generate in the normal course of business.

Liabilities are carried at the present discounted value of the future net cash outflows that are expected to be required to settle the liabilities in the normal course of business.

The basic accounting equation

37

Assets = Liabilities + Owner’s equity

Owner’s equity = Assets – LiabilitiesOwner’s equity2 = Owner’s equity1

+ Revenues

– Expenses

+ Owner’s Investments

– Owner’s Withdrawals

The accounting cycleIdentification and measurement of transactions and other eventsJournalizing (General journal and special journals) Posting (the procedure of transferring journal entries to the ledge accounts)Trial balance preparation (list of all open accounts and their balances)Adjustments (entries made at the end of an accounting period to bring all accounts up to date on an accrual basis)Adjusted trial balancePreparing of financial statementsClosing (nominal accounts)

38

Types of accounts

39

Permanent/ real accounts

assets accounts

liability accounts

owner’s equity accounts

Temporary/nominal accounts

revenue accounts

expense accounts

Statement of financial position

Income statement

General journal Page 1

Date Accounts Titles and Explanation

Ref. Debit Credit

20х7

Jan.30 Telephone expense

Accounts

payable

Received bill for telephone expense

513

212

70

70

40

General Ledger

Accounts payable Account No.212

Date Ref. Debit Credit Balance

Debit Credit

20х7

Jan.30

….

J 1 70 70

41

Types of adjusting entries

Accruals Prepayments

• Accrued revenues Revenues earned but not yet received in cash or recorded.

• Accrued expensesExpenses incurred but not yet paid in cash or recorded.

• Prepaid expenses Expenses paid in cash and recorded as assets before they are used and consumed.

• Prepaid revenues Revenues received in cash and recorded as liabilities before they are earned.

42

IAS 1 Presentation of Financial Statements

43

FINANCIAL STATEMENTS

Complete set of general purpose financial statements

Statement of financial position

Statement of comprehensive income

Statement of changes in equity

Statement of cash flows

Notes, comprising a summary of significant accounting policies and other explanatory notes

44

Overall requirements for the presentation of financial statements

45

Fair presentation and compliance with IFRSs

Going concern

Accrual basis of accounting

Materiality and aggregation

Offsetting

Comparative Information

Consistency of presentation

Frequency of reporting

Presentation of financial statements

Identification of financial statements Financial statements should be clearly identified from other information in the same published document.

Reporting periodFinancial statements should be presented at least annually.

46

• the name of the reporting entity• the separate or consolidated financial statements• the date of the end of the reporting period or the period covered• the presentation currency• the level of rounding used in presenting amounts

Statement of financial position

47

Current/non-current distinction

Current and non-current assets and liabilities

should be classified separately on the face of the statement of financial position

(except in circumstances when a liquidity-based presentation provides more reliable and relevant information)

Current/non-current assets

it expects to realize the asset, or intends to sell or consume it, in its normal operating cycle;

it holds the asset primary for the purpose of trading;

it expects to realize the asset within twelve months after the reporting period; or

the asset is cash or cash equivalent unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period.

48

An entity shall classify an asset as current when:

An entity shall classify all other assets as non-current.

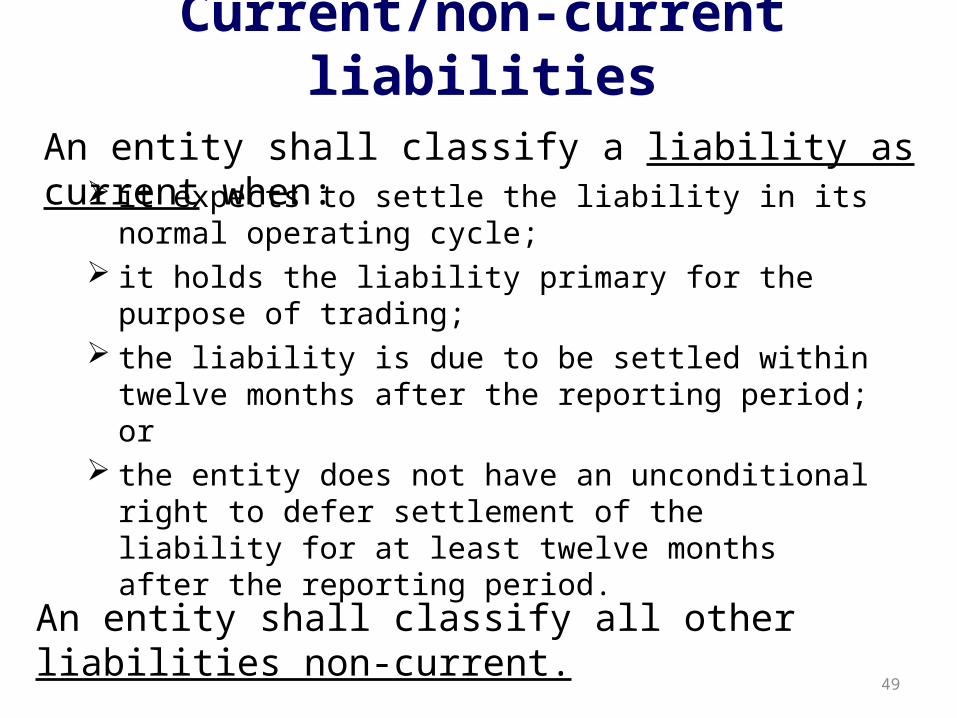

Current/non-current liabilities

it expects to settle the liability in its normal operating cycle;

it holds the liability primary for the purpose of trading;

the liability is due to be settled within twelve months after the reporting period; or

the entity does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting period.

49

An entity shall classify a liability as current when:

An entity shall classify all other liabilities non-current.

The minimum line items that should be included in the statement of financial position

Property, plant and equipmentInvestment propertyIntangible assetsFinancial assets Investments accounted for using the equity methodBiological assetsInventoriesTrade and other receivablesCash and cash equivalentsTrade and other receivables ProvisionsFinancial liabilities Liabilities and assets for current taxDeferred tax liabilities and deferred tax assets Non-controlling interest (presented within equity)Issued capital and reserves

50

Statement of comprehensive income

• in a single statement of comprehensive income, or

• in two statements: a statement displaying components of profit or loss (separate income statement) and a second statement beginning with profit and loss and displaying components of other comprehensive income (statement of comprehensive income).

51

An entity shall present all items of income and expense recognized in the period:

Statement of comprehensive income

52

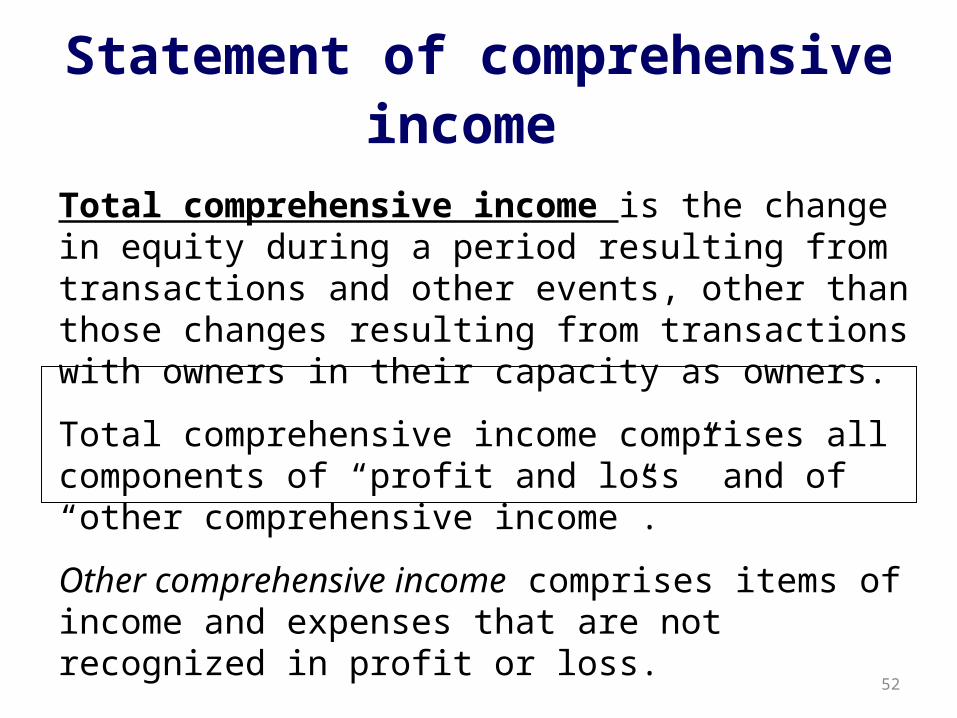

Total comprehensive income is the change in equity during a period resulting from transactions and other events, other than those changes resulting from transactions with owners in their capacity as owners.

Total comprehensive income comprises all components of “profit and loss” and of “other comprehensive income”.

Other comprehensive income comprises items of income and expenses that are not recognized in profit or loss.

Classification of expenses

53

An entity shall present an analysis of expenses recognized in profit or loss using classification based on either their nature or their function within the entity whichever provides information that is reliable and more relevant.

The choice between the function of expense method and the nature of expense method depends on historical and industry factors and the nature of the entity.

Example of classification using the nature of expense method

Revenue Other income Changes in inventories and finished goods and work in progressRaw materials and consumables used Employee benefits expensesDepreciation and amortization expense Other expensesTotal expensesProfit before tax

54

Example of classification using the function of expense method

Revenue

Cost of sales

Gross profit

Other income

Distribution costs

Administrative expenses

Other expenses

Profit before tax55

Statement of changes in equity

• total comprehensive income for the period;• for each component of equity, a reconciliation

between carrying amount at the beginning and at the end of the period, separately disclosing changes resulting from:– profit and loss;– each item of other comprehensive income;– transactions with owners in their capacity as owners.

56

An entity shall present a statement of changes in equity showing in the statement:

Notes

57

The notes shall:

present information about the basis of preparation of the financial statements and other accounting policies used;

disclose the information required by IFRSs that is not presented in the financial statements; and

provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

An entity normally presents notes in the following order..

statement of compliance with IFRSssummary of significant accounting policies

applied, supporting information for items presented in the statement of financial position and of comprehensive income, and in the statement of changes in equity and of cash flows

other disclosures

58