INTERNATIONAL FINANCE INVESTMENTS & COMMERCE BANK LIMITED

39

PERFORMANCE EVALUATION OF INTERNATIONAL FINANCE INVESTMENTS & COMMERCE BANK LIMITED Executive Summary Banking industry plays very important role in any economy. It has a long history as a service sector. Banks make it easy for people to complete their different monetary transaction and activity. It also creates new opportunity of earnings and help managing business with reliability. Presently there are 49 banks operating in Bangladesh. Among them 30 privet sector commercial banks, 10 foreign commercial banks, 5 specialized banks and 4 nationalized commercial banks. Commercial banks work for profit providing financial services to its clients. Specialized banks are assisting specific sector of the country created by special ordinance by the parliament. Commercial banks of the country are in its third generation growing faster then before and in more competitive environment. In terms of service banks have gained professionalism, efficiency and knowledge with skilled people. In year 2006 country’s privet sector commercial banks witnessed a growth of 31.87% and the operating profit of 28 PCBs out of 30 were TK. 37.04 billion up by 8.95 billion from previous year.

description

Banking industry plays very important role in any economy. It has a long history as a service sector. Banks make it easy for people to complete their different monetary transaction and activity. It also creates new opportunity of earnings and help managing business with reliability.

Transcript of INTERNATIONAL FINANCE INVESTMENTS & COMMERCE BANK LIMITED

PERFORMANCE EVALUATION

OF

INTERNATIONAL FINANCE INVESTMENTS & COMMERCE BANK LIMITED

Executive Summary

Banking industry plays very important role in any economy. It has a long history as a service sector. Banks make it easy for people to complete their different monetary transaction and activity. It also creates new opportunity of earnings and help managing business with reliability.

Presently there are 49 banks operating in Bangladesh. Among them 30 privet sector commercial banks, 10 foreign commercial banks, 5 specialized banks and 4 nationalized commercial banks. Commercial banks work for profit providing financial services to its clients. Specialized banks are assisting specific sector of the country created by special ordinance by the parliament.

Commercial banks of the country are in its third generation growing faster then before and in more competitive environment. In terms of service banks have gained professionalism, efficiency and knowledge with skilled people. In year 2006 country’s privet sector commercial banks witnessed a growth of 31.87%and the operating profit of 28 PCBs out of 30 were TK. 37.04 billion up by 8.95 billion from previous year.

The International Finance Investment & Commerce Bank Ltd. (IFIC Bank Ltd.)is one of the first generation bank of the country. It was set up at the instance of the Government in 1976 as a joint venture between the Government of Bangladesh and sponsors in the private sector with the objective of working as a finance company within the country and setting up joint venture banks/financial institutions abroad. The Government held 49 per cent shares and the rest 51 per cent were held by the sponsors and general public.

In 1983 when the Government allowed banks in the private sector, IFIC was converted into a full-fledged commercial bank. The Government of the People’s Republic of Bangladesh now

holds 35% of the share capital of the Bank. Leading industrialists of the country own 34% of the share capital and the rest is held by the general public.

The performance evaluation of the bank has been completed with the help of financial statements analysis techniques. Beside, the organizational framework & operational detail has been described to gain knowledge about this institution.

IFIC bank Ltd. provides all kinds of banking service and other financial solution. The deposit of the bank grows at 16.8% on an average in last twenty years. The bank earned TK. 1010 million as profit in 2006, and registered a growth of 42.30%.The bank maintains a steady liquidity position in the past years and operating abroad from its early life.

The bank was able to manage its debt, the times interest earned ratio of last four years shows a positive result of 1.12, 1.10, 1.11, 1.13 for 2002, 2003, 2004, and 2005 respectively.

About the report

This report is prepared as a requirement of MBA program as a part of internship of the Department of Finance, University of Dhaka. The report covered the time period from 21 January, 2007 to 07 March, 2007 of 1 month & 15 days.

There are five chapters in the report covering a description of IFIC Bank Ltd. and operational and financial activity. The first chapter deals with the methodology followed in the study and motivation behind the work. Chapter two is devoted to Pallabi branch as I was given placement at this branch as an intern of the bank.

Chapter three covers the profile of IFIC Bank Ltd. in two different perspectives:

a. Organizational and b. operational.

The first section covers IFIC at its organization base describes the departments and their job level also the employee profile.

The operational overviews entitles the bank’s different banking operation such as deposit, loans & advances, international business, information technology and introduction of new product.

Chapter four contains the financial statement analysis of the bank. The Balance sheet & the Profit & loss Account of the bank is analyzed to identify the strength and weakness and compare the performance over the years 2002, 2003, 2004 & 2005.

Chapter five concludes the report containing findings of the study.

The International Finance Investment & Commerce Bank Limited is a full service commercial bank of the Peoples Republic of Bangladesh. For the last two decades there has been a number of reformation in the banking sector of Bangladesh as well as of the global banking system and some new dimensions have evolved to match changes in the world’s flow of economic activity.

In terms of mode of service, reducing time & complicated paper work create significant economies of scale for the banking service as a whole. Bangladesh is also trying to reach that standard of service. The competition and other factor for this alleviation are there in the commercial banking sector. The report tries to portray this effort and identify the limitations there on.

Motivation

IFIC Bank Ltd is serving for a long time, as a commercial bank. From the beginning government and public sponsors comprises its equity structure. The bank has survived the economic crises of the country and demonstrated a sound financial performance. It has also expanded its business outside Bangladesh and is offering almost every newest banking product and service. The bank has a significant share in foreign trade. So I thought as a student of finance IFIC Bank Ltd is the right place to learn more about finance.

Objectives of the study

1. To have an insight of day to day banking operation; and2. To evaluate the financial performance of IFIC Bank Ltd.

Approach and Methodology

The research methodology followed in this report is in accordance with the objectives, requirement and scope of the study. The study has many limitations because of my inability to collect all the related information.

In this report the effort was given to emphasize on an overall performance evaluation of the International Finance Investment & Commerce Bank Limited.

The different techniques used in the analysis are

1. Time series analysis is done with last 20 year’s data of deposits.

2. Ratio and Trend analysis to evaluate financial position. For an example, the burden of debts and the company’s ability to repay them can be best evaluated by comparing I) firm’s debt to its assets and II) the interest it must pay for its funds to the interest it earns from its lending operations.

3. Common size analysis for identifying trends in financial statements. The analysis is useful in comparative evaluation, where all income statements items are divided by sales and all balance sheet items are divided by total assets. The common size income statement shows each item as a percentage of sales and common size balance sheet shows each item as a percentage of total assets.

4. Percentage change analysis, where growth rates are calculated for all income statement items and balance sheet accounts. Percentage change analysis helps to identify exclusively, the influence of any individual item. For an example it will identify if the interest expense decreased or increased the reported income.

5. SWOT analysis, which is a qualitative judgment and represents the Strength, Weakness, and Opportunities and Threats for the company in terms of its financial states, service, client, contribution to the economy, growth and creditworthiness, stated in a brief manner.

Sources of data

1. Library search of IFIC Bank Ltd at the HRD and Research division.2. Annual Report 2003 and Audit report 2005.3. Academic calendar 2006 and 2007.4. Web site of IFIC Bank Ltd., Bangladesh Bank and DSE.

5. Pallabi branch yearly performance evaluation report. 6. Prudential guidelines for Consumer Finance – IFIC Bank Ltd.

Introduction

During 2003 IFIC Bank Ltd. opened six new branches among which Pallabi Branch is one. Pallabi is located in Mirpur of Dhaka and identified as one of the developed area of Mirpur. Pallabi is a residential area with significant amount of commercial activity. Transport facility of the area is satisfactory. Potentiality of the branch is proven through its performance of three years of operation.

On 14 January, 2007 I was given placement as an intern at Pallabi branch of IFIC Bank Ltd. During my intern I have learned how a bank’s operational activities are run. At that time I get introduced with very nice and friendly people working for Pallabi branch, who has co operate me in every way and make my internship a special one.

Pallabi branch Profile:

Inception on: 2003Location: Kashem Chamber (1st and 2nd floor) Commercial plot, 11 Main Road, 03 Section, 07

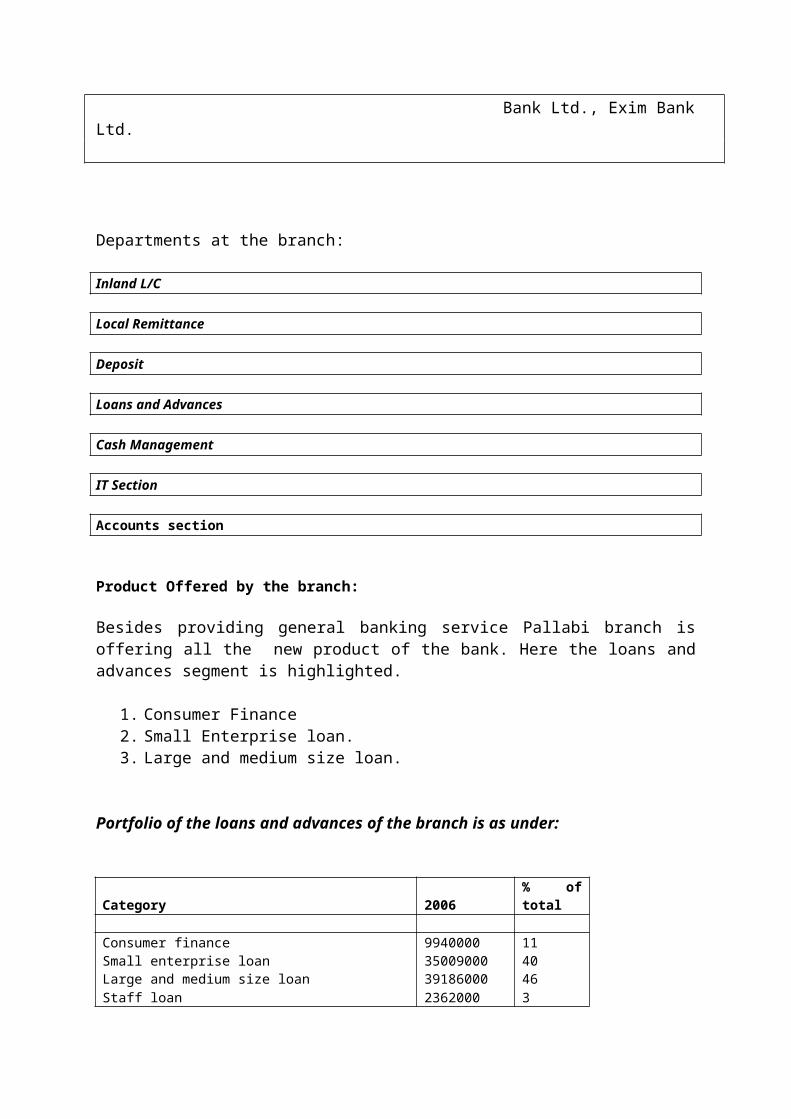

Pallabi, Dhaka.Rival banks in the area: Standard Chartered, Brac bank, One bank Ltd., Eastern Bank Ltd., AB Bank Ltd., Mutual Trust Bank Ltd., Exim Bank Ltd.

Departments at the branch:

Inland L/C

Local Remittance

Deposit

Loans and Advances

Cash Management

IT Section

Accounts section

Product Offered by the branch:

Besides providing general banking service Pallabi branch is offering all the new product of the bank. Here the loans and advances segment is highlighted.

1. Consumer Finance2. Small Enterprise loan.3. Large and medium size loan.

Portfolio of the loans and advances of the branch is as under:

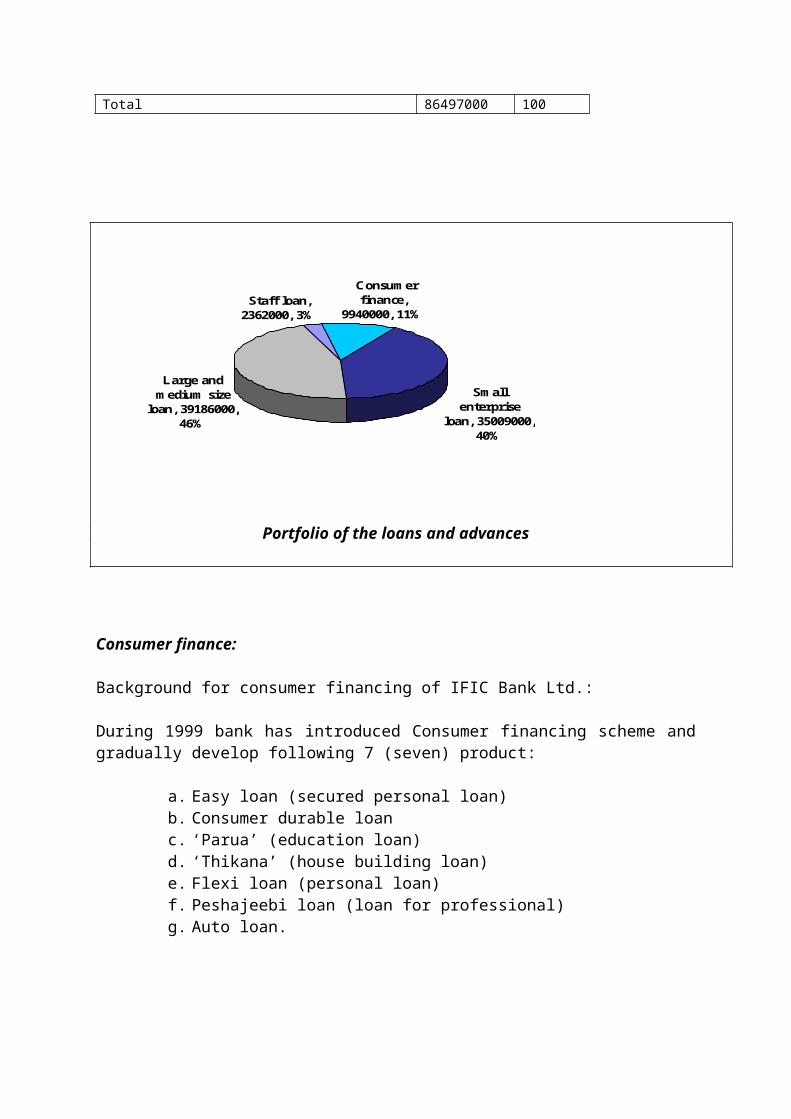

Category 2006 % of total Consumer finance 9940000 11Small enterprise loan 35009000 40Large and medium size loan 39186000 46Staff loan 2362000 3Total 86497000 100

Small enterprise

loan, 35009000, 40%

Consumer finance,

9940000, 11%Staff loan,

2362000, 3%

Large and medium size

loan, 39186000, 46%

Portfolio of the loans and advances

Consumer finance:

Background for consumer financing of IFIC Bank Ltd.:

During 1999 bank has introduced Consumer financing scheme and gradually develop following 7 (seven) product:

a. Easy loan (secured personal loan)b. Consumer durable loanc. ‘Parua’ (education loan)d. ‘Thikana’ (house building loan)e. Flexi loan (personal loan)f. Peshajeebi loan (loan for professional)g. Auto loan.

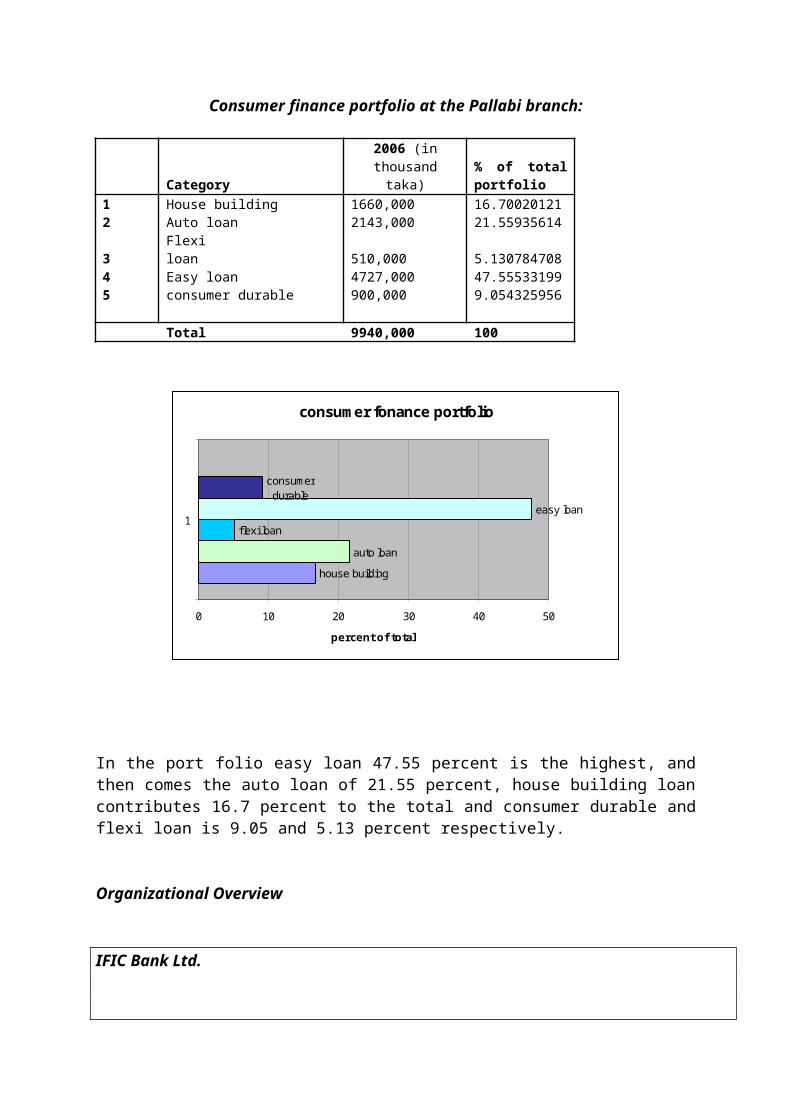

Consumer finance portfolio at the Pallabi branch:

Category 2006 (in thousand

taka)% of total portfolio

1 House building 1660,000 16.700201212 Auto loan 2143,000 21.559356143 Flexi loan 510,000 5.1307847084 Easy loan 4727,000 47.555331995 consumer durable 900,000 9.054325956 Total 9940,000 100

consumer fonance portfolio

house building

auto loan

flexi loan

easy loan

consumer durable

0 10 20 30 40 50

1

percent of total

In the port folio easy loan 47.55 percent is the highest, and then comes the auto loan of 21.55 percent, house building loan contributes 16.7 percent to the total and consumer durable and flexi loan is 9.05 and 5.13 percent respectively.

Organizational Overview

IFIC Bank Ltd.

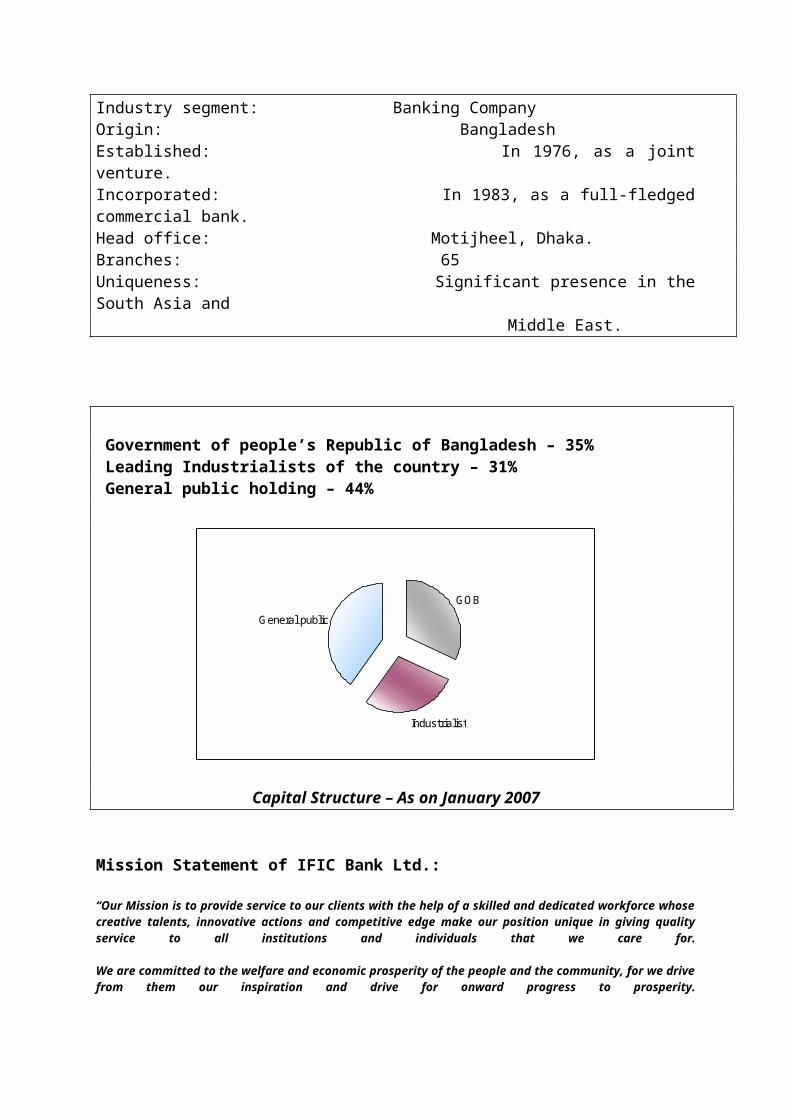

Industry segment: Banking CompanyOrigin: BangladeshEstablished: In 1976, as a joint venture.Incorporated: In 1983, as a full-fledged commercial bank.Head office: Motijheel, Dhaka.Branches: 65Uniqueness: Significant presence in the South Asia and Middle East.

Government of people’s Republic of Bangladesh – 35% Leading Industrialists of the country – 31% General public holding – 44%

General public

Industrialist

GOB

Capital Structure – As on January 2007

Mission Statement of IFIC Bank Ltd.:

“Our Mission is to provide service to our clients with the help of a skilled and dedicated workforce whose creative talents, innovative actions and competitive edge make our position unique in giving quality service to all institutions and individuals that we care for.

We are committed to the welfare and economic prosperity of the people and the community, for we drive from them our inspiration and drive for onward progress to prosperity.

We want to be the leader among banks in Bangladesh and make our indelible mark as an active partner in regional banking operating beyond the national boundary.

In an intensely competitive and complex financial and business environment, we particularly focus on growth and profitability of all concerned.”

Board of Directors:

Thirteen (13) directors designated as under,

Eight represents Sponsors and general public.Four represents the government of Bangladesh who are senior official in the rank and status of joint secretary/ Additional secretary. Managing Director is the ex-officio Director of the board.

Achievements of the bank overtime:

1976 - Established as an Investment and Finance Company under arrangement of joint venture with the Govt. of Bangladesh.

1980 - Commenced operation in Foreign Exchange Business in a limited scale.

1982 - Obtained permission from the Govt. to operate as a commercial Bank.

1983 - Setup its first overseas joint venture (Bank of Maldives) on the Republic of Maldives. - Commenced operation as a full-fledged commercial Bank in Bangladesh.

1985 - Set up a joint venture Exchange Company in the Sultanate of Oman.

1987 - Set up its first overseas branch in Pakistan at Karachi.

1993 - Set up its second overseas branch in Pakistan at Lahore.

1994 - Set up its first joint venture in Nepal for banking operation.

1999 - Set up its second joint venture in Nepal for lease financing.

2003 - Bank celebrated its 20th founding anniversary. - Overseas Branches in Pakistan amalgamated with NDLC, to establish a joint venture Bank: NDLC-IFIC Bank Ltd. subsequently renamed as NIB Bank Ltd.

People at IFIC bank ltd.:

Total number of employee are-2,014. 1,430 are officer 584 are staff.

Percentage of totalNumber of male worker 1739 86.34%Number of female worker 275 13.66%

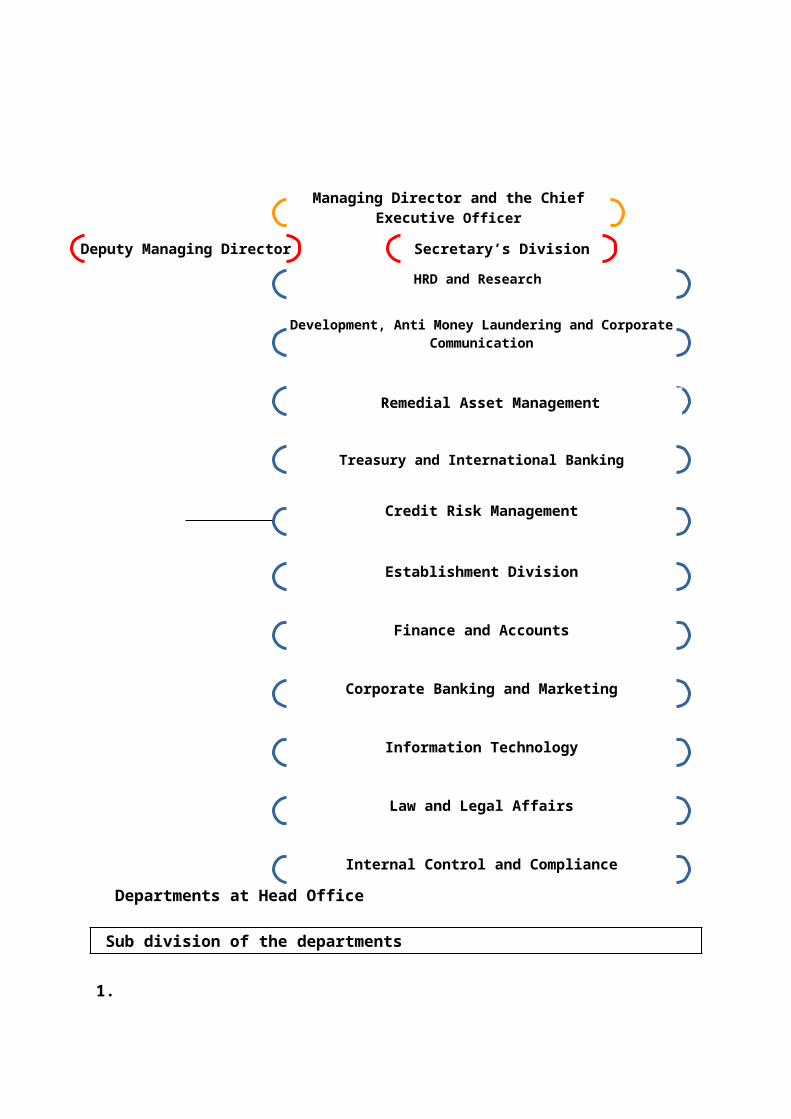

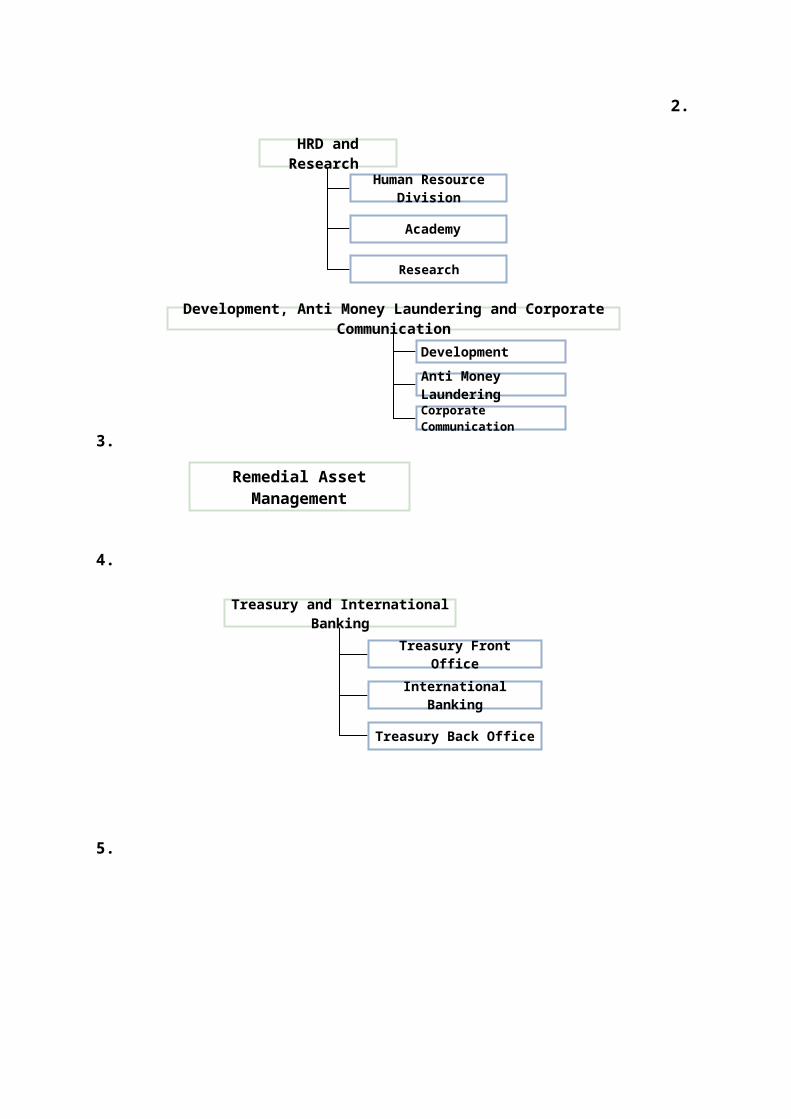

Departments at Head Office

Sub division of the departments

1.

Managing Director and the Chief Executive Officer

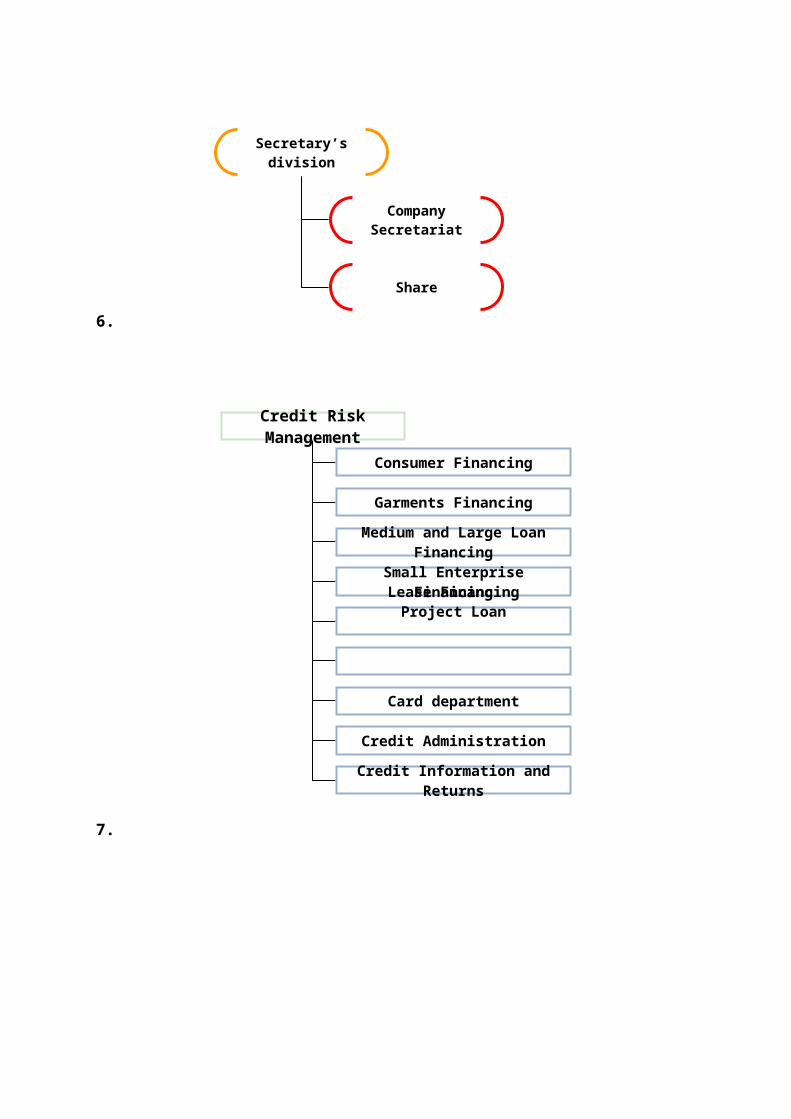

Deputy Managing Director Secretary’s Division

HRD and Research

Development, Anti Money Laundering and Corporate Communication

Treasury and International Banking

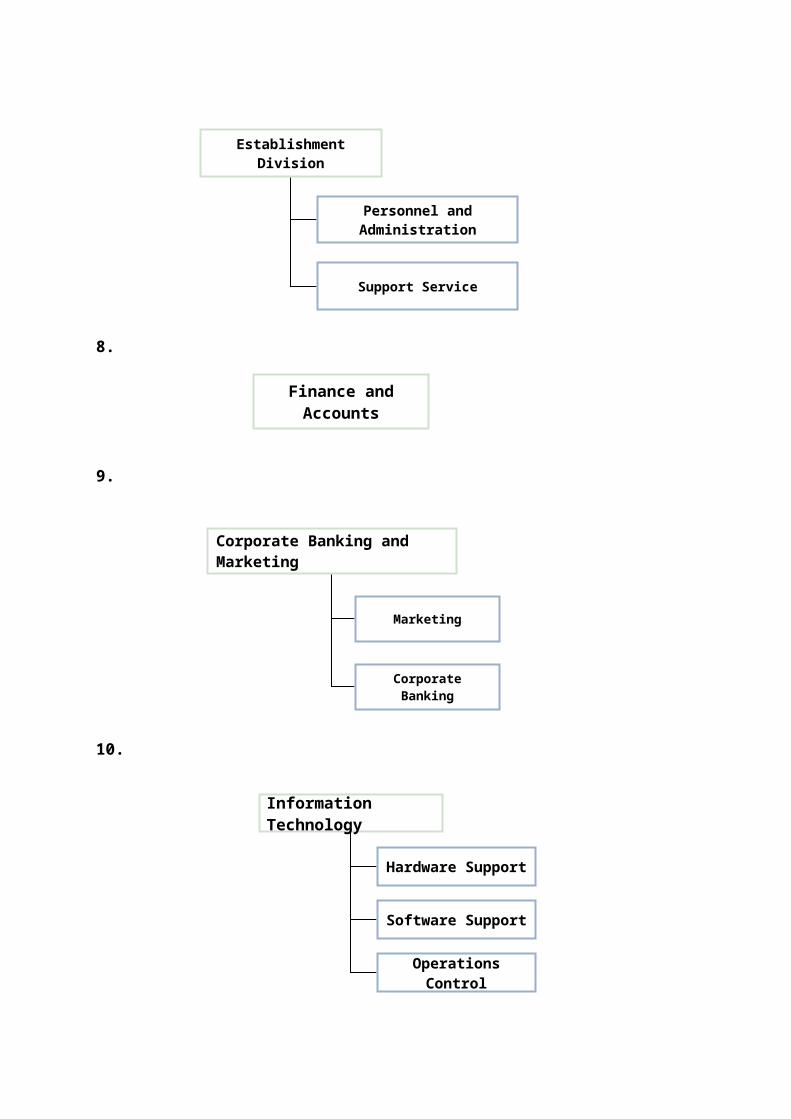

Establishment Division

Finance and Accounts

Corporate Banking and Marketing

Information Technology

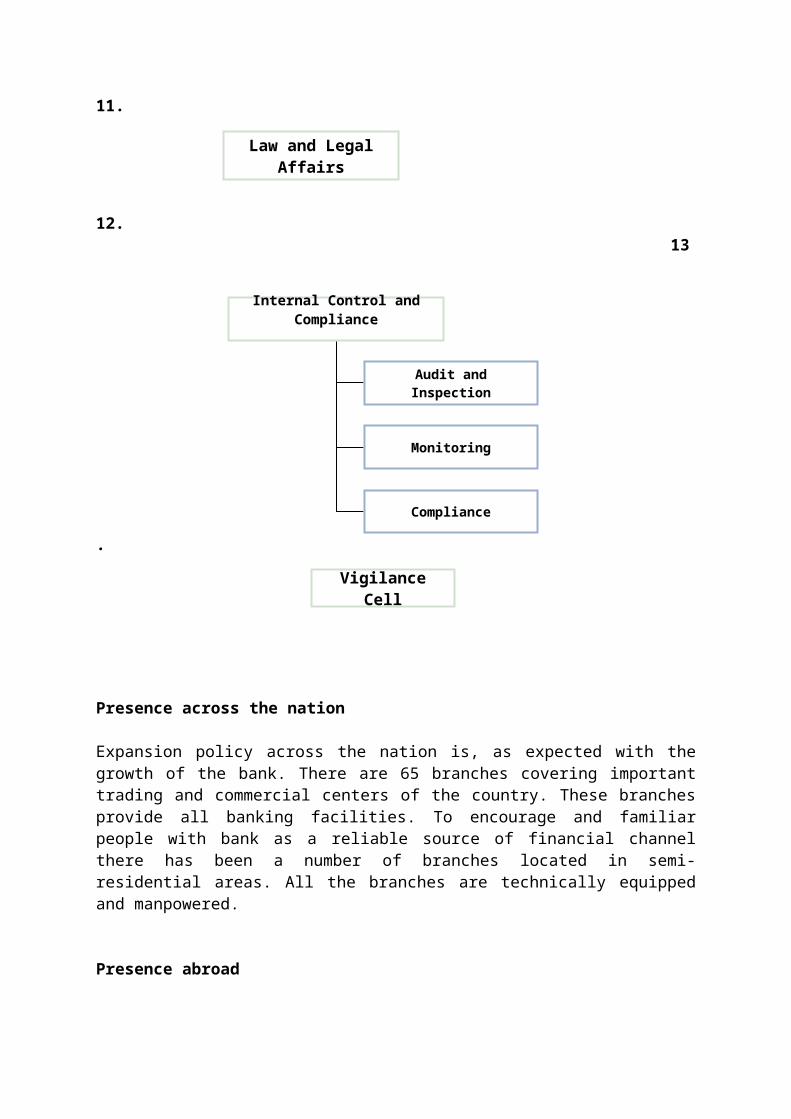

Law and Legal Affairs

Internal Control and Compliance

Remedial Asset Management

Credit Risk Management

2.

3.

4.

5.

HRD and Research

Human Resource Division

Academy

Research

Development, Anti Money Laundering and Corporate Communication

Development

Anti Money Laundering

Corporate Communication

Remedial Asset Management

Treasury and International Banking

Treasury Front Office

International Banking

Treasury Back Office

6.

7.

Secretary’s division

Company Secretariat

Share

Credit Risk Management

Consumer Financing

Garments Financing

Medium and Large Loan Financing

Small Enterprise FinancingLease Financing

Project Loan

Card department

Credit Administration

Credit Information and Returns

8.

9.

10.

11.

Establishment Division

Personnel and Administration

Support Service

Finance and Accounts

Corporate Banking and Marketing

Marketing

Corporate Banking

Information Technology

Hardware Support

Software Support

Operations Control

12.13.

Presence across the nation

Expansion policy across the nation is, as expected with the growth of the bank. There are 65 branches covering important trading and commercial centers of the country. These branches provide all banking facilities. To encourage and familiar people with bank as a reliable source of financial channel there has been a number of branches located in semi-residential areas. All the branches are technically equipped and manpowered.

Presence abroad

IFIC is the first among the banks in the private sector to have operations abroad. In 1983, the Bank set up a joint venture bank in Maldives known as 'Bank of Maldives Limited' (BML) at the request of the Government of the Republic of Maldives. This is the only national bank in that country having branches throughout that country. IFIC Bank managed the affairs of BML from 1983 to 1992. IFIC Bank sold its shares in 1992 to the Government of the Republic of Maldives and handed over the Management of BML to Maldives Government. Presently the bank is operating abroad as under:

Law and Legal Affairs

Internal Control and Compliance

Audit and Inspection

Monitoring

Compliance

Vigilance Cell

1. Oman International Exchange LLC (OIE), is a joint venture between IFIC Bank Ltd. and Oman nationals, was established in 1985 to facilitate remittance by Bangladeshi wage earners in Oman. The company is run by the bank under a management contract.

2. Nepal Bangladesh Bank Ltd. (NB Bank), a joint venture commercial bank with the Nepalese in effect from June 06, 1994. The management interest was withdrawn after expiry of the Technical Service Agreement on 08 April, 2005.

3. Nepal Bangladesh Finance and Leasing Ltd. (NBFLC), a joint venture leasing company started operations on 18 April, 1999.

4. NDLC-IFIC Bank Ltd. was emerged by the amalgamation of the Pakistan operation of IFIC bank ltd. and National Development Leasing Corporation of Pakistan on 03 October, 2003. On 28 November, 2005 the bank was renamed as NIB Bank Ltd. due to revise minimum capital requirements by the State Bank of Pakistan and ownership structure has changed. Presently IFIC Bank Ltd. holds 7.31% share in the bank.

Operational Overview

Credit policy and Portfolio

Credit operation is one of the major tasks for any bank. The diversification and complexity this sector has gained in last 5/10 years that policy in this regard matters. IFIC Bank Ltd. works within the framework of three main objectives in their credit policy and portfolio management. The objectives are:

a. Maintenance and improvement of quality of assets.b. Recovery on-time.c. Building-up efficient customer oriented credit delivery system.

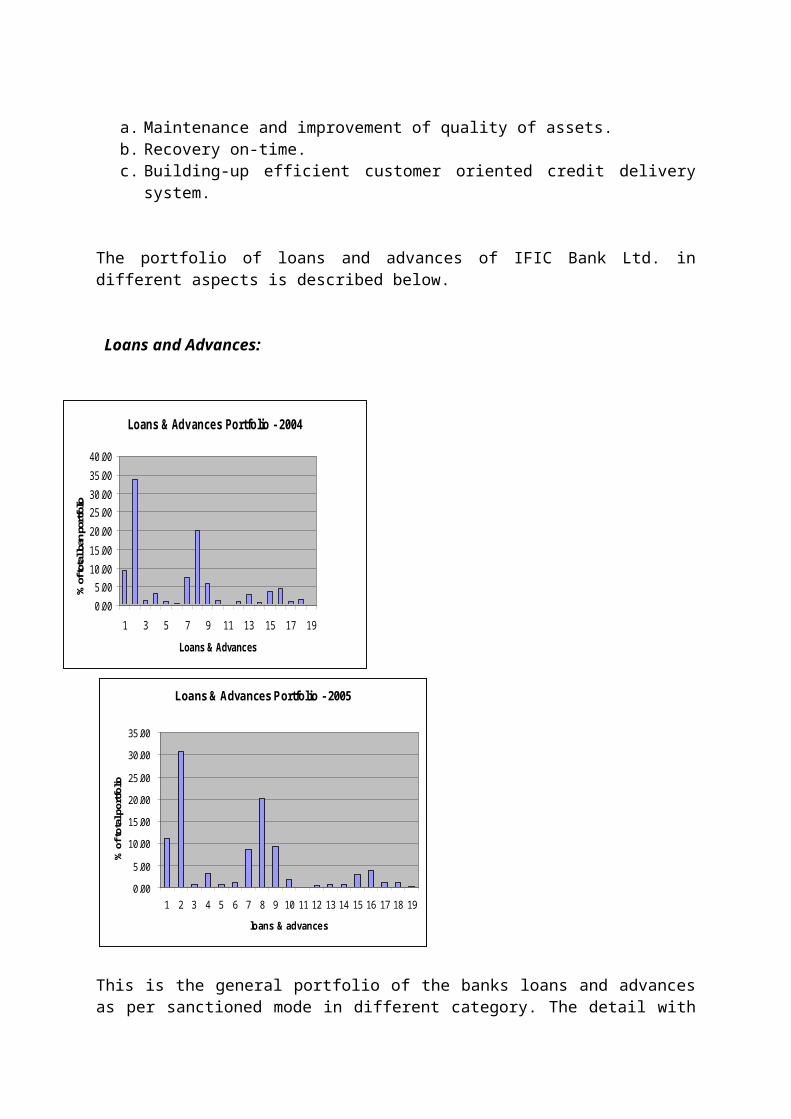

The portfolio of loans and advances of IFIC Bank Ltd. in different aspects is described below.

Loans and Advances:

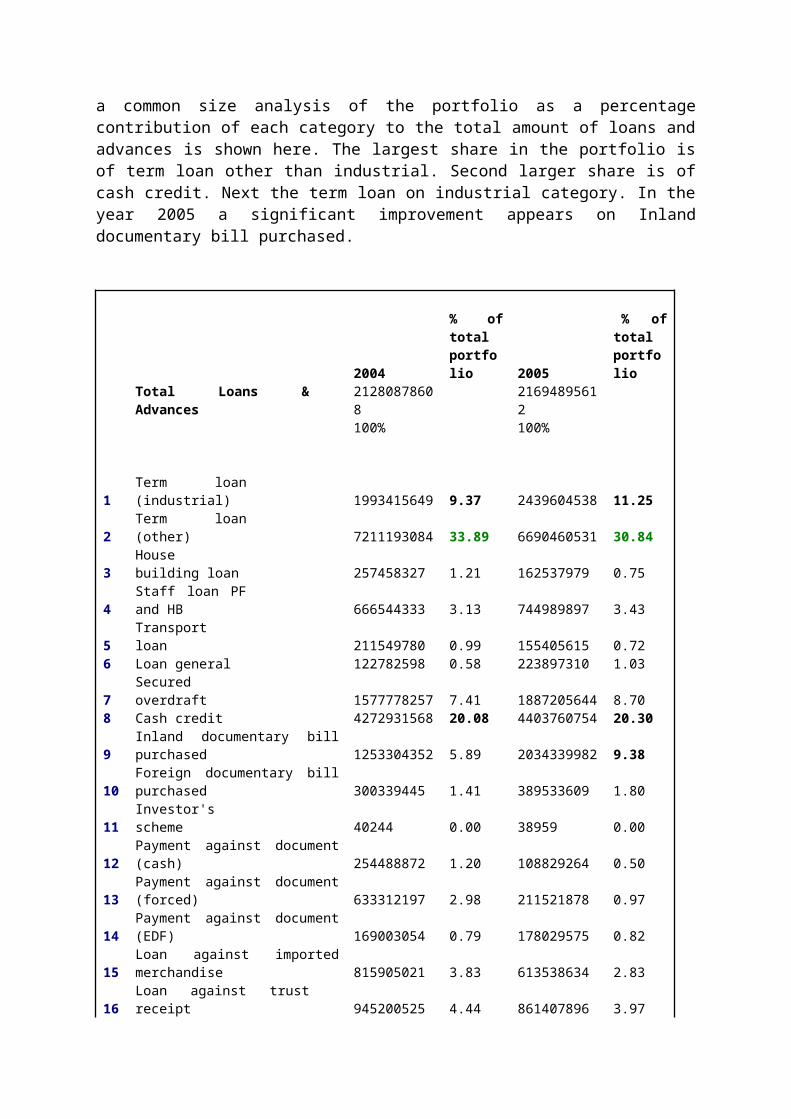

This is the general portfolio of the banks loans and advances as per sanctioned mode in different category. The detail with a common size analysis of the portfolio as a percentage contribution of each category to the total amount of loans and advances is shown here. The largest share in the portfolio is of term loan other than industrial. Second larger share is of cash credit. Next the term loan on industrial category. In the year 2005 a significant improvement appears on Inland documentary bill purchased.

Loans & Advances Portfolio - 2004

0.005.00

10.0015.0020.0025.0030.0035.0040.00

1 3 5 7 9 11 13 15 17 19

Loans & Advances

% o

f tot

al lo

an p

ortfo

lio

2004

% of total portfolio 2005

% of total portfolio

Total Loans & Advances 21280878608 21694895612 100% 100%

1Term loan (industrial) 1993415649 9.37 2439604538 11.25

2 Term loan (other) 7211193084 33.89 6690460531 30.84

3House building loan 257458327 1.21 162537979 0.75

4Staff loan PF and HB 666544333 3.13 744989897 3.43

5 Transport loan 211549780 0.99 155405615 0.72 6 Loan general 122782598 0.58 223897310 1.03 7 Secured overdraft 1577778257 7.41 1887205644 8.70 8 Cash credit 4272931568 20.08 4403760754 20.30 9 Inland documentary bill purchased 1253304352 5.89 2034339982 9.38

10Foreign documentary bill purchased 300339445 1.41 389533609 1.80

11 Investor's scheme 40244 0.00 38959 0.00 12 Payment against document (cash) 254488872 1.20 108829264 0.50

13Payment against document (forced) 633312197 2.98 211521878 0.97

14 Payment against document (EDF) 169003054 0.79 178029575 0.82

15Loan against imported merchandise 815905021 3.83 613538634 2.83

16 Loan against trust receipt 945200525 4.44 861407896 3.97 17 Export cash credit 216039767 1.02 263625024 1.22 18 Consumers' credit scheme 362161586 1.70 282454565 1.30 19 Other loans and advances 17429949 0.08 43713958 0.20

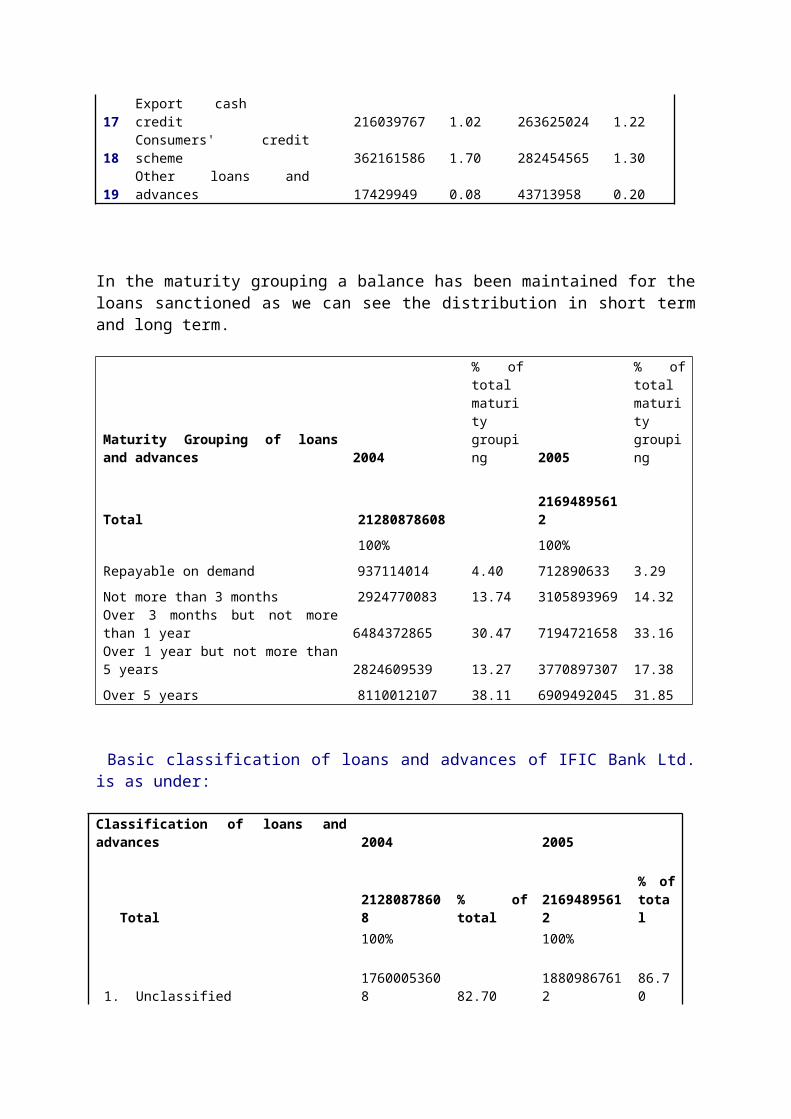

In the maturity grouping a balance has been maintained for the loans sanctioned as we can see the distribution in short term and long term.

Maturity Grouping of loans and advances 2004

% of total maturity grouping 2005

% of total maturity grouping

Total 21280878608 21694895612

100% 100%

Repayable on demand 937114014 4.40 712890633 3.29

Not more than 3 months 2924770083 13.74 3105893969 14.32Over 3 months but not more than 1 year 6484372865 30.47 7194721658 33.16

Over 1 year but not more than 5 years 2824609539 13.27 3770897307 17.38

Over 5 years 8110012107 38.11 6909492045 31.85

Basic classification of loans and advances of IFIC Bank Ltd. is as under:

Classification of loans and advances 2004 2005

Total 21280878608 % of total 21694895612% of total

100% 100% 1. Unclassified 17600053608 82.70 18809867612 86.70 2. Special mention account 0.00 790308000 3.64 3. Substandard 184952000 0.87 89553000 0.41 4. Doubtful 75629000 0.36 52139000 0.24

5. Bad/loss 3420244000 16.07 1953028000 9.00

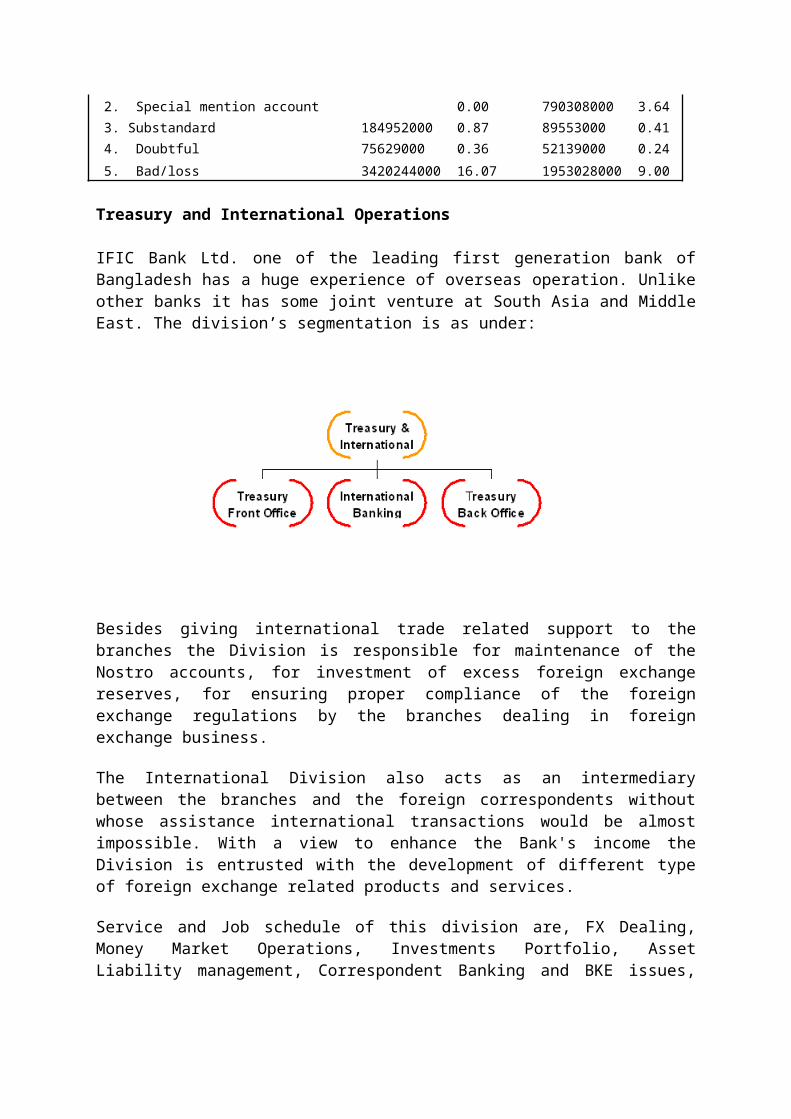

Treasury and International Operations

IFIC Bank Ltd. one of the leading first generation bank of Bangladesh has a huge experience of overseas operation. Unlike other banks it has some joint venture at South Asia and Middle East. The division’s segmentation is as under:

Besides giving international trade related support to the branches the Division is responsible for maintenance of the Nostro accounts, for investment of excess foreign exchange reserves, for ensuring proper compliance of the foreign exchange regulations by the branches dealing in foreign exchange business.

The International Division also acts as an intermediary between the branches and the foreign correspondents without whose assistance international transactions would be almost impossible. With a view to enhance the Bank's income the Division is entrusted with the development of different type of foreign exchange related products and services.

Service and Job schedule of this division are, FX Dealing, Money Market Operations, Investments Portfolio, Asset Liability management, Correspondent Banking and BKE issues, Joint Ventures Operations, Drawing Arrangements, Inward and Outward Foreign Remittance, AD License etc.

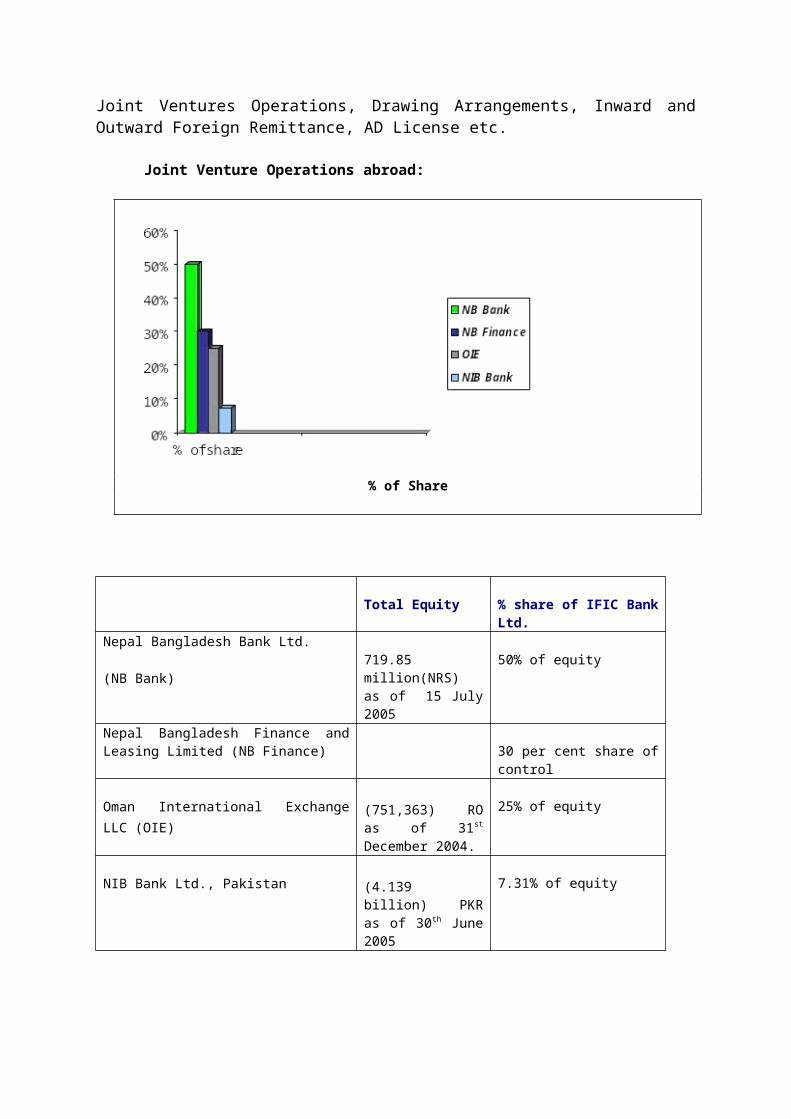

Joint Venture Operations abroad:

% of Share

Total Equity % share of IFIC Bank Ltd.Nepal Bangladesh Bank Ltd.

(NB Bank) 719.85 million(NRS) as of 15 July 2005

50% of equity

Nepal Bangladesh Finance and Leasing Limited (NB Finance) 30 per cent share of

control

Oman International Exchange LLC (OIE) (751,363) RO as of 31st December 2004.

25% of equity

NIB Bank Ltd., Pakistan (4.139 billion) PKR as of 30th June 2005

7.31% of equity

Information technology and online banking:

There are 65 branches across the nation of which 22 are Authorized Dealer (AD) for conducting foreign trade. All the branches are using computerized banking solution. To join the ever competitive technology base banking service IFIC Bank Ltd. now working on the objectives:

a. Achieve better customer relationship management.b. Multi-channel distribution.c. Developing attractive products and services.d. Assured risk management.e. Use of better business intelligence and enhanced image.

To achieve these objectives Project Horizon has been launched. The project is devoted to implement software banking solution solely for IFIC Bank Ltd. featuring real-time, integrated and centralized banking solution. The solution is being provided by Misys International Banking Systems, UK with consulting services.

Five pilot branches have been selected for the first phase implementation. These branches are Gulshan, Motijheel, Narayanganj, Agrabad and Sylhet. In the second phase another 14 AD branches will be provided with the solution.

Some of the success achieved already as Gulshan branch is being facilitated with:

a. Internal and Communication infrastructures.b. Initiation of Roll Out process.c. Conversion and migration of live data.d. Parallel runs with live data and routine reconciliation with the existing process.

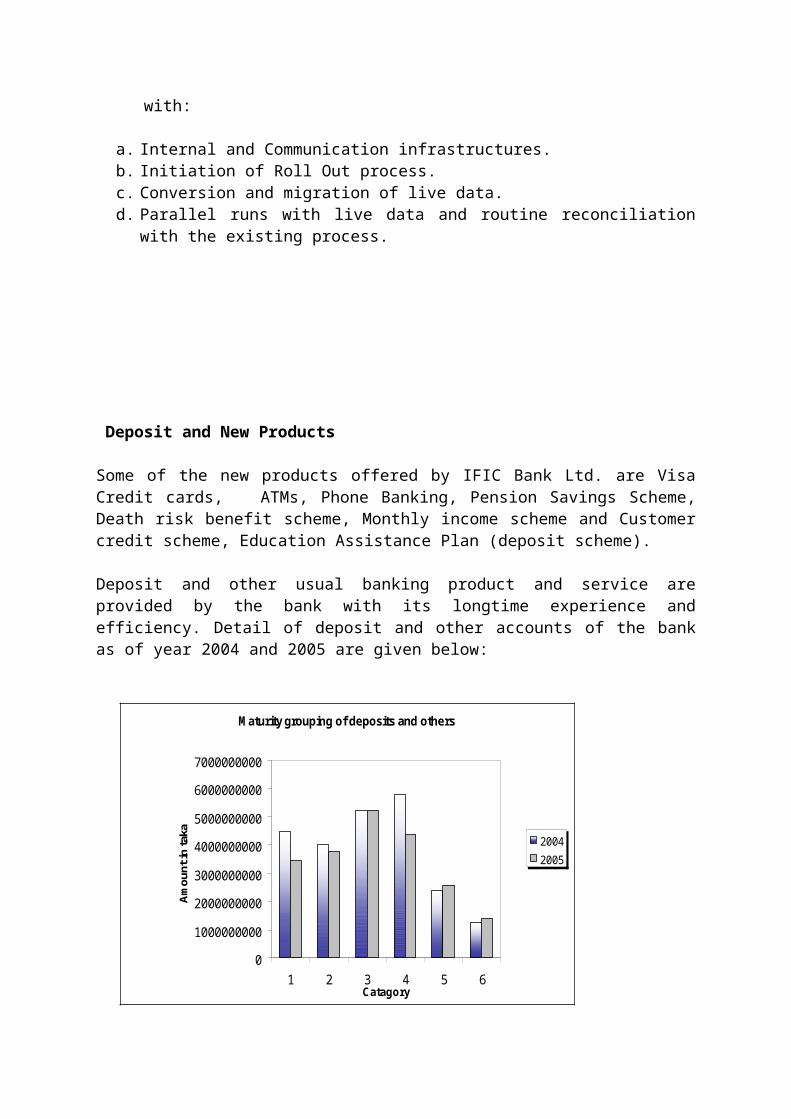

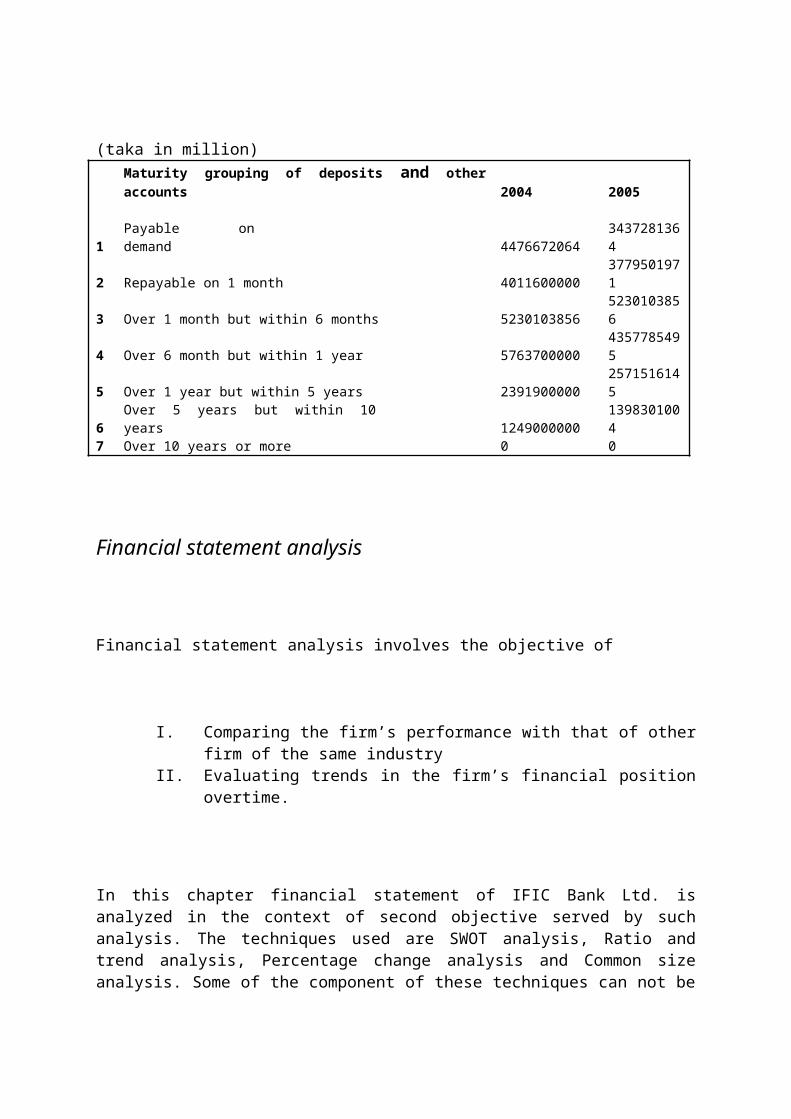

Deposit and New Products Some of the new products offered by IFIC Bank Ltd. are Visa Credit cards, ATMs, Phone Banking, Pension Savings Scheme, Death risk benefit scheme, Monthly income scheme and Customer credit scheme, Education Assistance Plan (deposit scheme). Deposit and other usual banking product and service are provided by the bank with its longtime experience and efficiency. Detail of deposit and other accounts of the bank as of year 2004 and 2005 are given below:

Maturity grouping of deposits and others

0

1000000000

2000000000

3000000000

4000000000

5000000000

6000000000

7000000000

1 2 3 4 5 6Catagory

Am

ount

in ta

ka 20042005

(taka in million) Maturity grouping of deposits and other accounts 2004 2005 1 Payable on demand 4476672064 34372813642 Repayable on 1 month 4011600000 37795019713 Over 1 month but within 6 months 5230103856 52301038564 Over 6 month but within 1 year 5763700000 43577854955 Over 1 year but within 5 years 2391900000 25715161456 Over 5 years but within 10 years 1249000000 13983010047 Over 10 years or more 0 0

Financial statement analysis

Financial statement analysis involves the objective of

I. Comparing the firm’s performance with that of other firm of the same industry

II. Evaluating trends in the firm’s financial position overtime.

In this chapter financial statement of IFIC Bank Ltd. is analyzed in the context of second objective served by such analysis. The techniques used are SWOT analysis, Ratio and trend

analysis, Percentage change analysis and Common size analysis. Some of the component of these techniques can not be covered as nature and criteria of the absence of with specific nature and criteria.

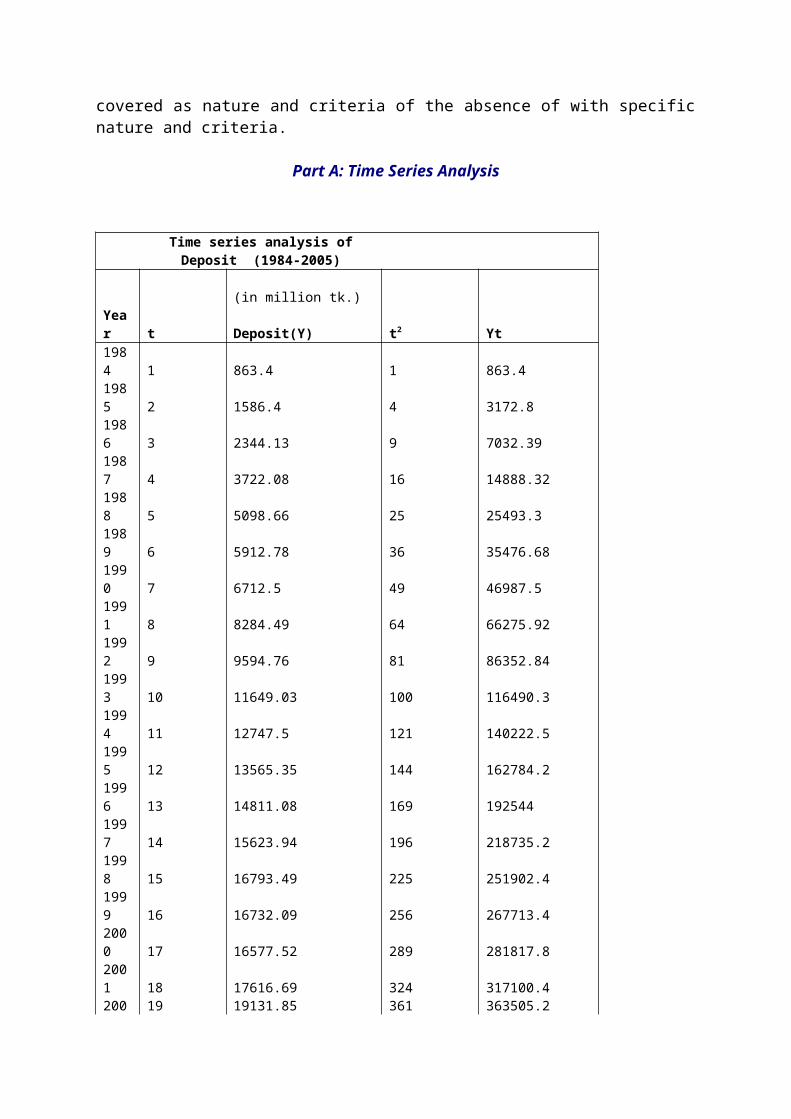

Part A: Time Series Analysis

Time series analysis of Deposit

(1984-2005) (in million tk.) Year t Deposit(Y) t2 Yt1984 1 863.4 1 863.41985 2 1586.4 4 3172.81986 3 2344.13 9 7032.391987 4 3722.08 16 14888.321988 5 5098.66 25 25493.31989 6 5912.78 36 35476.681990 7 6712.5 49 46987.51991 8 8284.49 64 66275.921992 9 9594.76 81 86352.841993 10 11649.03 100 116490.31994 11 12747.5 121 140222.51995 12 13565.35 144 162784.21996 13 14811.08 169 1925441997 14 15623.94 196 218735.21998 15 16793.49 225 251902.41999 16 16732.09 256 267713.42000 17 16577.52 289 281817.82001 18 17616.69 324 317100.42002 19 19131.85 361 363505.22003 20 19798.97 400 395979.42004 21 20774.48 441 436264.12005 22 22505.17 484 495113.7 ∑t =253 ∑Y =262446.36 ∑t2 =3795 ∑Yt = 926716 n = 22 ∑Y*∑t = 66398929.08 (∑t)2 = 64009 t =11.5 Ý= 11929.38

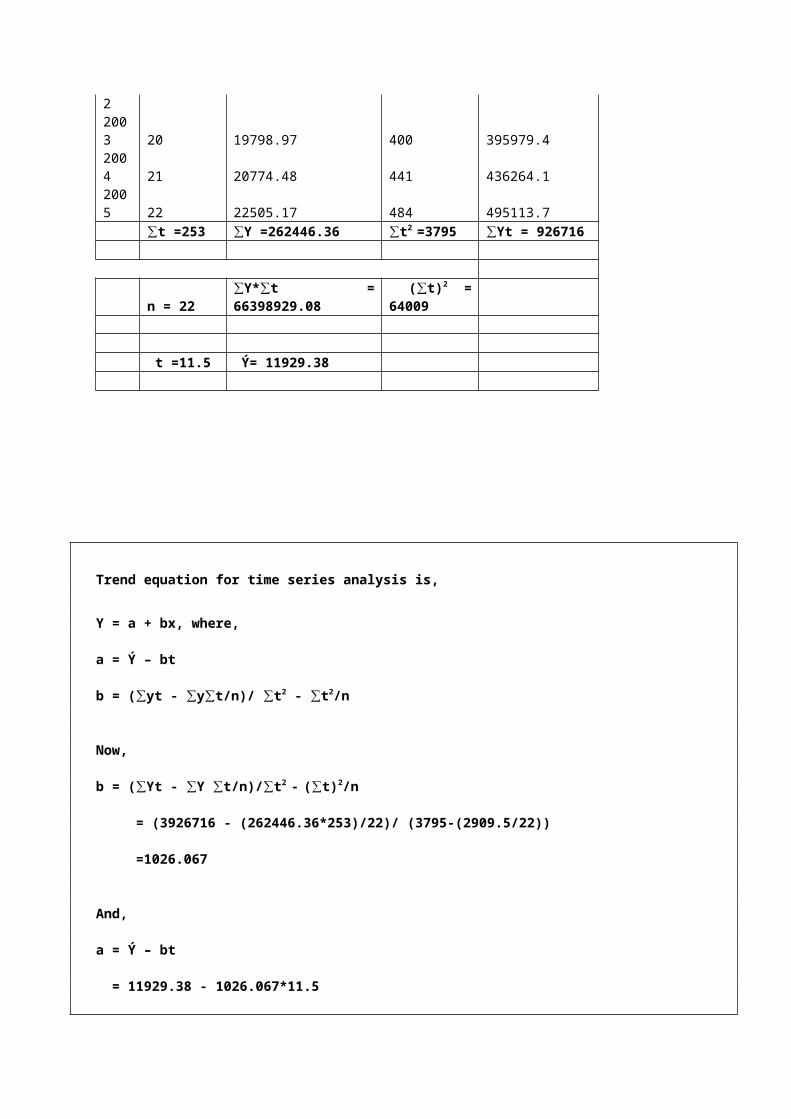

Trend equation for time series analysis is,

Y = a + bx, where,

a = Ý – bt

b = (∑yt - ∑y∑t/n)/ ∑t2 - ∑t2/n

Now, b = (∑Yt - ∑Y ∑t/n)/∑t2 - (∑t)2/n

= (3926716 - (262446.36*253)/22)/ (3795-(2909.5/22))

=1026.067

And,

a = Ý – bt

= 11929.38 - 1026.067*11.5

=129.6056

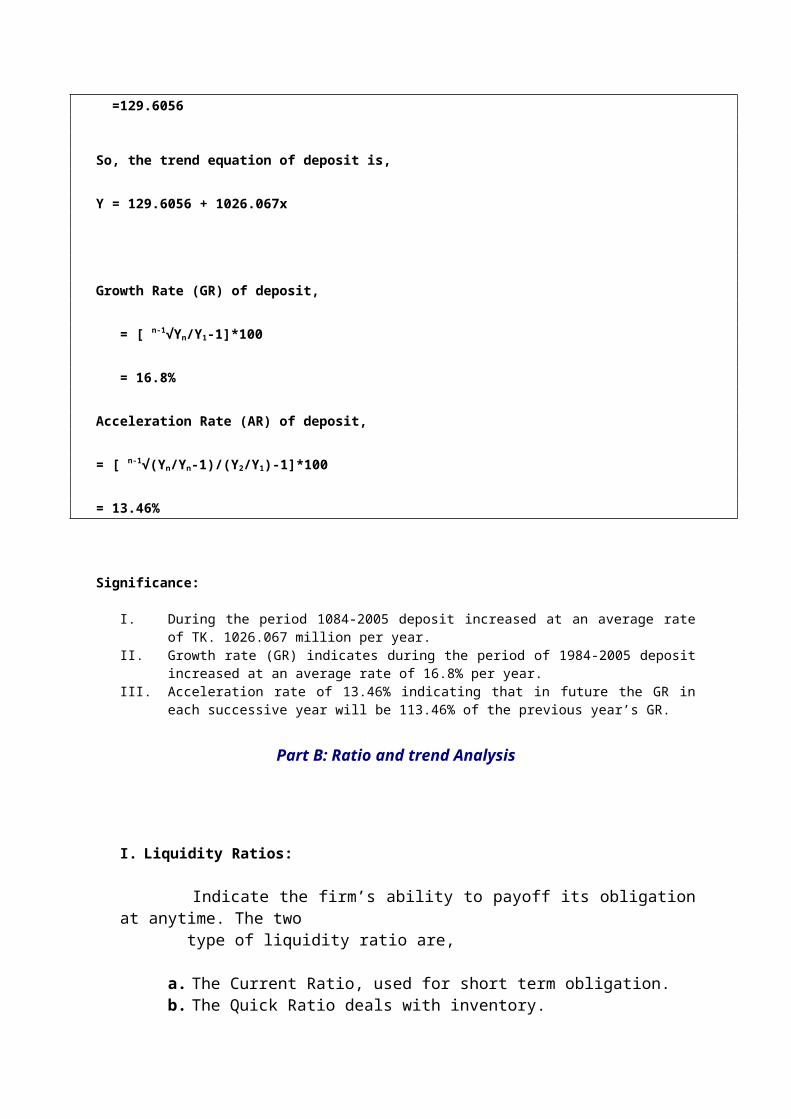

So, the trend equation of deposit is,

Y = 129.6056 + 1026.067x

Growth Rate (GR) of deposit,

= [ n-1√Yn/Y1-1]*100

= 16.8%

Acceleration Rate (AR) of deposit,

= [ n-1√(Yn/Yn-1)/(Y2/Y1)-1]*100

= 13.46%

Significance:

I. During the period 1084-2005 deposit increased at an average rate of TK. 1026.067 million per year.

II. Growth rate (GR) indicates during the period of 1984-2005 deposit increased at an average rate of 16.8% per year.

III. Acceleration rate of 13.46% indicating that in future the GR in each successive year will be 113.46% of the previous year’s GR.

Part B: Ratio and trend Analysis

I. Liquidity Ratios:

Indicate the firm’s ability to payoff its obligation at anytime. The two type of liquidity ratio are,

a. The Current Ratio, used for short term obligation.b. The Quick Ratio deals with inventory.

Here current ratio of IFIC is analyzed:

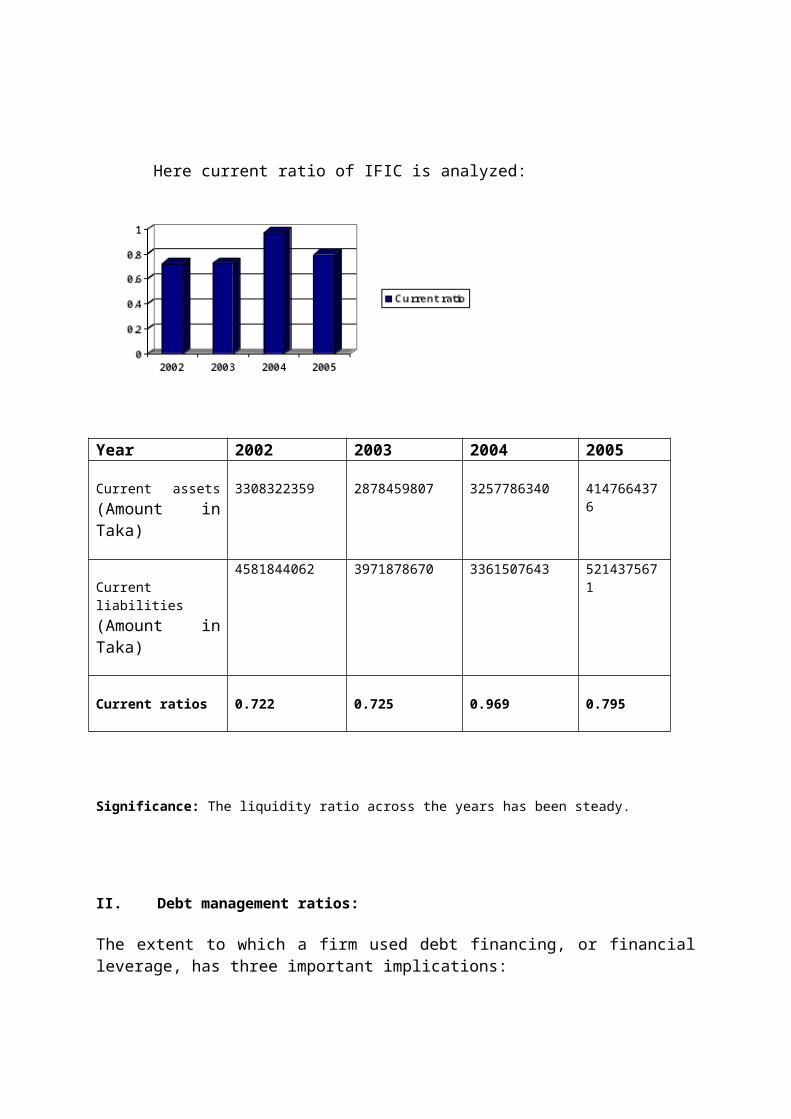

Year 2002 2003 2004 2005

Current assets (Amount in Taka)

3308322359 2878459807 3257786340 4147664376

Current liabilities (Amount in Taka)

4581844062 3971878670 3361507643 5214375671

Current ratios 0.722 0.725 0.969 0.795

Significance: The liquidity ratio across the years has been steady.

II. Debt management ratios:

The extent to which a firm used debt financing, or financial leverage, has three important implications:

a. By raising funds through debt, stockholders can maintain control of a firm without increasing their investment. b. To provide a margin of safety creditors are concerned of the equity or owner supplied fund. The higher the proportion of total capital provided by stockholders, the less the risk faced by creditors. c. If the firm earn more on investments financed with borrowed funds then it pays in interest, the return on the owner’s capital is magnified or ‘leveraged’

So debt management ratios help to figure out how the capital is structured. There are three kinds of debt management ratios, are:

1. Total debt to Total asset; shows how the firm is financed2. Times Interest Earned (TIE); shows ability to pay interest3. EBITDA coverage ratio; shows ability to service debt.

Here TIE ratio of IFIC bank ltd. is analyzed:

Significance: IFIC Bank Ltd. has maintained a steady Times Interest Earned ratio across the years.

Part C: Percentage Change Analysis

Year 2002 2003 2004 2005

EBIT (Amount in Taka)

1232603215 1330269974 1372209463 1332754621

Interest payments (Amount in Taka)

1082888515 1213193960 1241459524 1183216786

TIE ratio 1.12 1.10 1.11 1.13

Percentage change analysis is a technique where growth rates are calculated for all income statement items and balance sheet accounts. Percentage change analysis helps to identify exclusively, the influence of any individual item. For an example through percentage change analysis one can identify if the borrowings decreased or increased the reported assets and liabilities.

Procedure used in Percentage Change Analysis as under:

1. Important major heads and sub heads are selected for analysis.2. Formula used to get, % change is, (yr1-yr0/yr0*100)

Percentage Change Analysis of Profit and Loss Account

2004 (Yr0) 2005 (Yr1) % changeNet interest income 512386365.00 657220774.00 28.27

Total operating income 1445561029.00 1488972882.00 3.00Salaries and allowances 460086709.00 602182622.00 30.88Total operating expense 745311090.00 939435047.00 26.05Profit before provision 700249939.00 549537835.00 -21.52Provision for loans and advances 569500000.00 400000000.00 -29.76Total provision 569500000.00 400000000.00 -29.76

Profit before tax 130749939.00 149537835.00 14.37Provision for tax 58837473.00 67292026.00 14.37Profit after tax 71912466.00 82245809.00 14.37Retained profit brought forward 159339260.00 160399278.00 0.67AppropriationsStatutory reserve 26149988.00 29907567.00 14.37Proposed bonus share 44702460.00 49172706.00 10.00Retained earnings 160399278.00 163564814.00 1.97EPS 17.70 20.24 14.35

Significance:

I. Profit has decreased from previous year.II. Provision has been decreased from previous year.

Percentage Change Analysis of Balance Sheet

2004 (yr0) 2005 (yr1)% change

Cash 2295582386 2146612028 -6.49%Balance with other banks and financial institution 252203954 1011052348 301.00%Money at call at short notice 710000000 990000000 39.44%

Investments 2666288202 2971466388 11.45%Loans and Advances 21280878608 21694895612 1.95%Loans, cash credits, overdrafts, etc. 19727234811 19271022021 -2.31%Bills discounted and purchased 1553643797 2423873591 56.01%Fixed assets including premise, furniture and fixtures 178809339 192758868 7.80%Other assets 1192069538 1194269731 0.19%

Total assets 28575832027 30201054975 5.69%

Liabilities: Borrowing from other banks, financial institutions and agents 95870100 1197380691 1148.96%

Deposits and other accounts 20774489835 22505172064 8.33%Current deposits and other accounts 2884945098 3452927221 19.69%Other liabilities 6489983199 5137405111 -20.84%

Total liabilities 27360343134 28839957866 5.41%Shareholders' equity 1215488893 1361097109 11.98%

Total liabilities and shareholders' equity 28575832027 30201054975 5.69%

Significance:

I. Cash decreased in 2005 then 2004, in compare to other two near cash asset at the top of the balance sheet. On the other hand a portion of liability has decreased, though total liability has increased. One of the important sources of loan portfolio ‘loans, cash credit, overdrafts, etc.’ has decreased.

II. Two huge changes appear in the ‘balance with other banks and financial institution’ of asset side and ‘liabilities: Borrowing from other banks, financial institutions and agents’ of liability and equity side of the balance sheet. It reflects that interbank transaction of the bank has grown at a large scale.

Part D: Common Size Analysis

Common size analysis is a technique of identifying trends in financial statements. Common size analysis is useful in comparative analysis, where all income statements items are divided by sales and all balance sheet items are divided by total assets. Thus a common size income statement shows each item as a percentage of sales, and a common size balance sheet shows each item as a percentage of total assets.

Procedure used for common size analysis as under:1. Important major heads and sub heads are selected for analysis.2. Formula used to get 3. For analyzing profit and loss account all items are divided by Net interest income.

Common Size Analysis of Profit and Loss Account

2004% net interest 2005

% net interest

Net interest income 512386365.00 657220774.00 1.00 1.00

Total operating income 1445561029.00 282.12 1488972882.00 290.60 Salaries and allowances 460086709.00 89.79 602182622.00 117.53 Total operating expense 745311090.00 145.46 939435047.00 183.35 Profit before provision 700249939.00 136.66 549537835.00 107.25 Provision for loans and advances 569500000.00 111.15 400000000.00 78.07 Total provision 569500000.00 111.15 400000000.00 78.07

Profit before tax 130749939.00 25.52 149537835.00 29.18 Provision for tax 58837473.00 11.48 67292026.00 13.13 Profit after tax 71912466.00 14.03 82245809.00 16.05 Retained profit brought forward 159339260.00 31.10 160399278.00 31.30 AppropriationsStatutory reserve 26149988.00 5.10 29907567.00 5.84 Proposed bonus share 44702460.00 8.72 49172706.00 9.60 Retained earnings 160399278.00 31.30 163564814.00 31.92 EPS 17.70 20.24 0.00

Significances: In 2005 interest income contribution to operating profit increased then the previous year.

Common Size Analysis of Balance sheet

2004

% of total asset 2005

% of total asset

Total assets 28575832027 30201054975100% 100%

Cash 2295582386 8.03 2146612028 7.11Balance with other banks and financial institution 252203954 0.88 1011052348 3.34Money at call at short notice 710000000 2.48 990000000 3.28Investments 2666288202 9.33 2971466388 9.84Loans and Advances 21280878608 74.47 21694895612 71.83Loans, cash credits, overdrafts, etc. 19727234811 69.03 19271022021 63.81Bills discounted and purchased 1553643797 5.44 2423873591 8.03Fixed assets including premise, furniture and fixtures 178809339 0.63 192758868 0.64Other assets 1192069538 4.17 1194269731 3.95

Liabilities: Borrowing from other banks, financial institutions and agents 95870100 0.34 1197380691 3.96Deposits and other accounts 20774489835 72.70 22505172064 74.52Current deposits and other accounts 2884945098 10.10 3452927221 11.43Other liabilities 6489983199 22.71 5137405111 17.01

Total liabilities 27360343134 95.74 28839957866 95.49Shareholders' equity 1215488893 4.25 1361097109 4.51

Total liabilities and shareholders' equity 28575832027 100 30201054975 100

Significance: Loans and advances contributes the highest to the total asset of IFIC Bank Ltd.

Part E: SWOT AnalysisStrength

1. Consistent financial performance

2. Strong organize base. 3. Growth in compare to the industry is consistent in year 2006. The operating profit of

28 PCBs out of 30 were tk.37.04 billion, result in a growth of 31.87%. IFIC record an operating profit of tk.1010 million, a growth of 42.30% then the previous year.

Weakness:

1. Internal compliance need to be more sophisticated.2. More concentration should be given to expansion process, not only increase in

number but also support to the existing branches should be given with a view of present competitive environment.

3. IFIC has built a reputation of being one of the larger and better institution their service must be competent in this respect.

Opportunities:

1. Operational and Organizational structure of the bank is really set for better service; there is potentiality for the bank to grow in this aspect.

2. As the bank has experience of business abroad there is scope for expansion and diversification.

Threats:

1. IFIC should be concern of their pros pond of AGM of last 3 years.

Major Findings:

IFIC Bank Ltd, one of the few first generation banks operating and serving the nation for a long time, has so far passed its journey with such a sound financial record all the way.

The study excludes any comparison of the institution with its industry, but it analyzes the performance of year 2005 in compare to year 2004. In this aspect the findings are:

I. The average growth rate of deposit is 16.8 percent for last twenty years.

II. In terms of liquidity and debt service ability IFIC bank ltd. is maintaining a secured position.

III. In compare to year 2004 to 2005 the cash has decreased, the reported income also decreased.

IV. Inter bank transaction increased to a significant extant indicating a more active banking operation.

V. In 2005 loans and advances increased 71.83 percent then 2004.

VI. The interest income increased then 2004 in 2005.

VII. 98% of loans and advances of the total is being treated as ‘good’ in 2004: the figure in 2005 is 97%. The base of this criterion is the quality of security pledged.

VIII. In classification of the loans, unclassified loan amount 82.7% and 86.7% in year 2004 & 2005 respectively.

IX. IFIC Bank Ltd. is having problem in arranging the AGM which has

remained withheld for last three years.

References:

1. Financial Management, Theory and Practice – Eugene F. Brigham and Michael C. Ehrharat. ( 10th edition)

2. Prudential regulations for Consumer finance – IFIC Bank Ltd.3. Auditor’s Report and Accounts of IFIC Bank Ltd., for the year ended December 31,

2005.4. Annual Report, 2003- of IFIC Bank Ltd. 5. Branch manager’s report, 2006 of Pallabi branch of IFIC Bank Ltd.6. Academic Celendar,20067. Academic Celendar, 2007.8. www.ificbank bd.com.9. www.dsebd.org 10. www.bbank.org