International Banking: Reserves, Debt, and Risk © 2011 Cengage Learning. All Rights Reserved. May...

47

International Banking: Reserves, Debt, and Risk © 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password‐protected website for classroom use 1 PowerPoint slides prepared Andreea Chiritescu Eastern Illinois University

-

Upload

braedon-towns -

Category

Documents

-

view

213 -

download

0

Transcript of International Banking: Reserves, Debt, and Risk © 2011 Cengage Learning. All Rights Reserved. May...

1

International Banking:Reserves, Debt, and Risk

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

PowerPoint slides prepared by:Andreea ChiritescuEastern Illinois University

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

2

Nature of International Reserves• International reserves• Enable nations to finance disequilibrium in

their balance-of-payments positions• Deficit: monetary receipts fall short of monetary

payments• Settled with international reserves

• Enable nations to sustain temporary balance-of-payments deficits• Until acceptable adjustment measures can operate

to correct the disequilibrium

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

3

Demand for International Reserves• Demand for international reserves • Depends on• Monetary value of international transactions• Disequilibrium that can arise in balance-of-

payments positions• Contingent on • Speed and strength of the balance-of-payments

adjustment mechanism• Overall institutional framework of the world

economy

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

4

Demand for International Reserves• Demand for international reserves • Exchange-rate flexibility• Automatic adjustment mechanisms that

respond to payments disequilibrium• Economic policies used to bring about

payments equilibrium• International coordination of economic policies

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

5

Demand for International Reserves• Changes in the degree of exchange-rate

flexibility • Inversely related to changes in the quantity of

international reserves demanded• More rapid and flexible exchange-rate

adjustments requires smaller reserves

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

6

When exchange rates are fixed (pegged) by monetary authorities, international reserves are necessary for the financing of payment imbalances and the stabilization of exchange rates. With floating exchange rates, payment imbalances tend to be corrected by market-induced fluctuations in the exchange rate; the need for exchange-rate stabilization and international reserves then disappears.

The demand for international reserves and exchange-rate flexibility

FIGURE 17.1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

7

Demand for International Reserves• Automatic adjustment mechanisms • Prices, interest rates, incomes, and monetary

flows • The more efficient each of these adjustment

mechanisms is• The smaller and more short-lived market

imbalances will be and • The fewer reserves will be needed

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

8

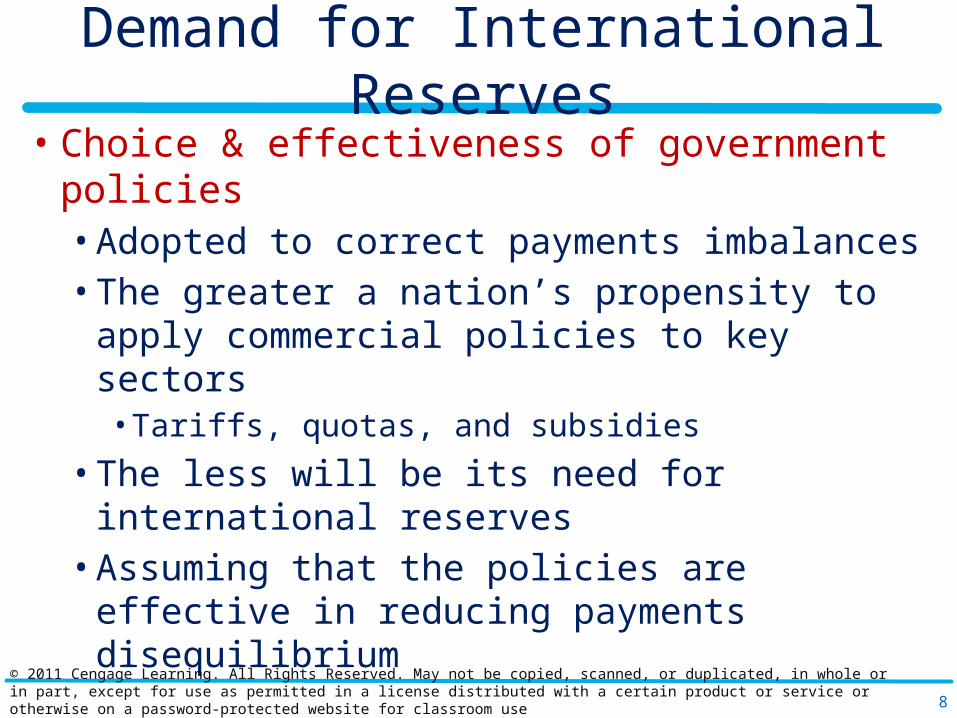

Demand for International Reserves• Choice & effectiveness of government policies• Adopted to correct payments imbalances• The greater a nation’s propensity to apply

commercial policies to key sectors• Tariffs, quotas, and subsidies

• The less will be its need for international reserves• Assuming that the policies are effective in

reducing payments disequilibrium

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

9

Demand for International Reserves• International coordination of economic policies• Goal of economic cooperation: • Reduce the frequency and extent of payment

imbalances• Reduce the demand for international reserves

• Quantity demanded of international reserves• Positively related to the level of world prices

and income

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

10

Supply of International Reserves• Total supply of international reserves• Owned reserves• Gold, acceptable foreign currencies• Special drawing rights (SDRs)

• Borrowed reserves• Lenders:• Foreign nations with excess reserves• Foreign financial institutions• International agencies

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

11

Foreign Currencies• 1800s–1900s, reserve currencies• The U.S. dollar• The UK pound• Trading nations have traditionally been willing

to hold them as international reserve assets• Since World War II, the U.S. dollar has been the

dominant reserve currency

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

12

Foreign Currencies• The U.S. dollar as reserve currency• Early 1950s - a dollar-shortage era• Massive development programs in Europe• Excess demand for the dollars

• Late 1950s, dollar glut• U.S. continued to provide reserves to the world

through its payments deficits• 1960s, liquidity problem• 1970, creation of SDRs as reserve assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

13

International reserves, 2006, all countries (in billions of SDRs*)

TABLE 17.1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

14

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• The United States dollar• Main reserve currency in the world today• Medium of exchange, unit of account, and store of

value• Wealth in dollar-denominated assets • 64% of world’s official foreign exchange reserves• 86% of daily foreign exchange trades

• Other reserve currencies• The euro, the British pound, Japanese yen

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

15

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• Benefits for the U.S.• Americans • Can purchase products at a marginally cheaper rate• Can borrow at lower interest rates for homes and

automobiles• The U.S. government • Can finance larger deficits longer and at lower

interest rates• Can issue debt (securities) in its own currency• Pushing exchange rate risk onto foreign lenders

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

16

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• Concerns • Substantial dollar depreciation• Losing purchasing power

• The U.S. - huge deficits and massive borrowing• Volatility of the dollar• Destabilizing effect that it can have on international

trade and finance

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

17

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• 2009, China - Special Drawing Right (SDR) to replace the dollar• New world reserve currency • Based on a basket of currencies instead of just

the dollar• SDR: euro, yen, pound, and dollar• Expand to include all major currencies

• SDR would be managed by the IMF

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

18

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• Benefits of SDRs• China - cushion any depreciation in the dollar’s

exchange value• Help stabilize the value of China’s holdings of U.S.

Treasury securities• Support aggregate demand in the world• Economic welfare of the world should not

depend on the behavior of a single currency

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

19

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• Benefits of SDRs• Currency risk - diversified through a basket

reserve unit• Enhancing stability and confidence throughout the

world• Equity• U.S. can attract the savings of other countries even

when the interest rates it pays are very low

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

20

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• Potential pitfalls of SDRs• SDR is backed by nothing other than the good

faith and credit of the IMF• Who would determine the “right price” of the

SDR?• Add another step to each international

transaction• Convert local currency into SDRs

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

21

GLOBALIZATIONShould SDRs replace the dollar as the world’s

reserve currency?

• The U.S. and SDRs• Americans would have to pay more for

imported goods• Interest rates on both private and

governmental debt would increase• Increased private cost of borrowing• Weaker consumption, decreased investment, and

slower growth

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

22

Gold• Gold standard, historically• International means of payments• Unit of account• Viable store of value• Overall acceptability

• Monetary role of gold today• Glittering ghost haunting efforts to reform the

international monetary system

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

23

Gold• International gold standard, 1880 to 1914• Values of most national currencies were

anchored in gold• Gold coins circulated• Generally accepted means of payment

• Money supply• Fixed relation to the monetary stock of gold• Growth in monetary gold• Growth in the money supply• At a rate that corresponded to the growth in real

national output

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

24

Gold• U.S. and the gold standard• 1934, the Gold Reserve Act• U.S. government - title to all monetary gold • Required citizens to turn in their private holdings to

the U.S. Treasury• The U.S. dollar - devalued in 1934• Official price of gold was raised from $20.67 to $35

per ounce

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

25

Gold• Gold exchange standard, dollar-gold system• International monetary system as formulated

by the IMF nations• To economize on monetary gold stocks as

international reserves• The U.S – dominant economy• Productive capacity and national wealth

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

26

Gold• Gold exchange standard, dollar-gold system• The United States• Assume the role of world banker• The dollar - chief reserve currency of the

international monetary system• Responsibility for buying and selling gold at a fixed

price to foreign official holders of dollars• The dollar – convertible to gold• All other currencies – pegged to the dollar

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

27

Gold• Gold exchange standard, dollar-gold system• 1968, two-tier gold system• Official tier - central banks could buy and sell gold

for monetary purposes at the official price of $35 per ounce• Private market - gold as a commodity could be

traded at the free-market price

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

28

Gold• Demonetization of gold• August 1971, President Richard Nixon• The United States was suspending its commitment

to buy and sell gold at $35 per ounce• U.S. stock of monetary had declined to $11 billion• Deteriorating U.S. balance-of-payments position

• January 1, 1975• The official price of gold was abolished as the unit

of account for the international monetary system

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

29

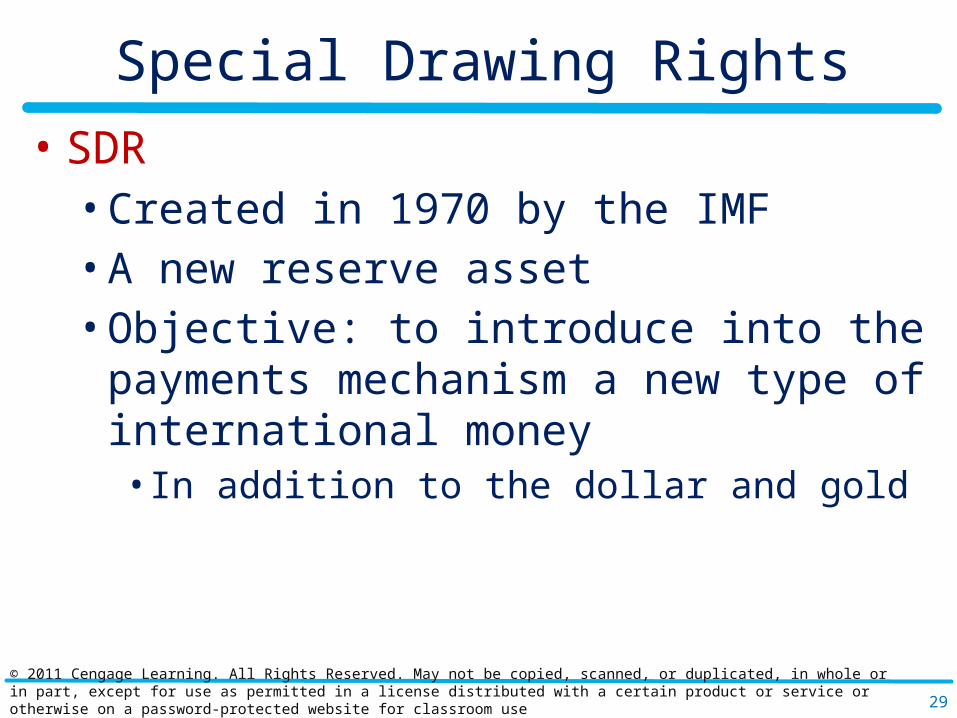

Special Drawing Rights• SDR• Created in 1970 by the IMF• A new reserve asset• Objective: to introduce into the payments

mechanism a new type of international money• In addition to the dollar and gold

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

30

Special Drawing Rights• SDR today• Limited use as a reserve asset• Main function: unit of account of the IMF and

some other international organizations• Some of the IMF’s member nations peg their

currency values to the SDR• Potential claim on the freely usable currencies

of IMF members

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

31

Special Drawing Rights• Value of SDR • Basket of currencies• The U.S. dollar, Japanese yen, UK pound, and the

euro• The weights of the currencies reflect the

amount of exports and imports of these countries during the previous five years

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

32

Facilities for Borrowing Reserves• IMF drawings • The transactions by which the fund makes

foreign-currency loans available• Deficit nations• Do not borrow from the fund• Purchase with their own currency the foreign

currency required to help finance deficits• Reverse the transaction when the balance-of-

payments position improves

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

33

Facilities for Borrowing Reserves• General Arrangements to Borrow, 1962• G-10 agreed to lend the fund up to a maximum

of $6 billion• Do not provide a permanent increase in the

supply of world reserves• Once the loans are repaid, world reserves revert

back to their original levels• World reserves - more flexible and adaptable to

the needs of deficit nations

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

34

Facilities for Borrowing Reserves• Swap arrangements• Bilateral agreements between central banks• Each government provides for an exchange of

currencies to help finance temporary payments disequilibrium• The nation requesting the swap• Expected to use the funds to help ease its

payments deficits and discourage speculative capital outflows• Repay within a stipulated period of time, normally

within 3 to 12 months

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

35

International Lending Risk• Credit risk• Financial• The probability that part or all of the interest or

principal of a loan will not be repaid• The larger the potential for default on a loan• The higher the interest rate that the bank must

charge the borrower

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

36

International Lending Risk• Country risk - Political• Closely related to political developments in a

country• Government’s views concerning international

investments and loans

• Currency risk - Economic• Associated with currency depreciations and

appreciations as well as exchange controls

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

37

The Problem of International Debt• Concern: insufficient international lending • After the oil shocks in 1974–1975 and 1979–

1980• Oil-importing developing nations might not be able

to obtain loans to finance trade deficits• Resulting from the huge increases in the price of oil

• Able to borrow dollars from commercial banks

• 1980s, commercial banks• Part of an international debt problem• Lent so much to developing nations

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

38

The Problem of International Debt• Debt service/export ratio• Indicator of debt burden• Scheduled interest and principal payments as a

percentage of export earnings• Interest rate that the nation pays on its external

debt• Growth in its exports of goods and services

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

39

The Problem of International Debt• A nation has debt-servicing problems because• May have pursued improper macroeconomic

policies that contribute to large balance-of-payments deficits• May have borrowed excessively or on

unfavorable terms• May have been affected by adverse economic

events that it could not control

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

40

The Problem of International Debt• Options for a nation facing debt-servicing

difficulties• Cease repayments on its debt• Service its debt at all costs• Debt rescheduling• Obtain emergency loans from the IMF• Conditionality

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

41

Reducing Bank Exposure to Developing-Nation Debt

• Stability of the international financial system• Threatened when developing nations cannot

meet their debt obligations to foreign banks• Banks - improve their financial position• Increasing their capital base• Setting aside reserves to cover losses• Reducing new loans to debtor nations

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

42

Reducing Bank Exposure to Developing-Nation Debt

• Banks - improve their financial position• Liquidate developing-nation debt • Loan sales to other banks in the secondary market

• Debt buyback• Government of the debtor nation buys the loans

from the commercial bank at a discount• Debt-for-debt swaps• Bank exchanges its loans for securities issued by the

debtor nation’s government • Lower interest rate or discount

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

43

Reducing Bank Exposure to Developing-Nation Debt

• Banks - improve their financial position• Debt/equity swaps• Commercial bank sells its loans at a discount to the

developing-nation government • For local currency, which it then uses to finance an

equity investment in the debtor nation

• Debt reduction• Debt forgiveness

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

44

Debt Reduction and Debt Forgiveness• Debt reduction• Voluntary scheme that lessens the burden on

the debtor nation to service its external debt• Use of negotiated modifications in the terms and

conditions of the contracted debt• Debt reschedulings• Retiming of interest payments• Improved borrowing terms

• Debt/equity swaps• Debt buybacks

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

45

Debt Reduction and Debt Forgiveness• Debt forgiveness• Arrangement that reduces the value of

contractual obligations of the debtor nation• Markdowns of developing-nation debt• Write-offs of developing-nation debt • Abrogation of existing obligations to pay interest

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

46

The Eurodollar Market• Eurodollar market• Eurocurrency market• Financial intermediary• Brings together lenders and borrowers

• Bank deposit liabilities• Time deposits• Denominated in U.S. dollars and other foreign

currencies in banks outside the United States• Transactions in dollars• Three-fourths of the volume of transactions

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password protected website for classroom use‐

47

The Eurodollar Market• Eurodollar market• Eurodollar deposits • Redeposited in other foreign banks, lent to business

enterprises, invested, or retained to improve reserves or overall liquidity• Free of regulation by the host country

• Eurodollars increase the efficiency of international trade and finance• Internationally accepted medium of exchange,

store of value, standard of value