INTERNATIONAL ARBITRAGE TRANSACTIONS INVOLVING … · table of contents page i. introduction ..... 1

Upload

works-in-gcufCategory

view

2.005download

0

Arbitrage

o types of Arbitrage

o Locational arbitrage

o Triangular arbitrage

o Covered interest

arbitrage

o Interest rate parity

o Simultaneous purchase and sale of commodities or financial instruments in various market to profit from unequal prices without risk.

o arbitrage take benefit from discrepancy in prices they purchase from a place where prices are low and sold where the prices are high.

o arbitrage earn riskless profit

As applied to foreign exchange and international money markets, arbitrage takes three common forms:

o locational arbitrage

o triangular arbitrage

o covered interest arbitrage

is possible when a bank’s buying price (bid price) is higher than another bank’s selling price (ask price) for the same currency.

Example:

Bank C Bid Ask Bank D Bid Ask

NZ$ $.635$.640 NZ$ $.645$.650

Buy NZ$ from Bank C @ $.640, and sell it to Bank D @ $.645. Profit = $.005/NZ$.

o Buy NZ$ from Bank C @ $.640, and sell it to Bank D @ $.645. Profit = $.005/NZ$.

o A person can obtain New Zealand dollars for “Bank A” at the ask price of $.640 and then sell New Zealand dollars to “Bank B” at the bid price of $.645. This represent a “one round trip” transaction in Locational arbitrage.

When the actual cross exchange rate between two currencies differ from spot rate. the process of taking one currency and converting it into another currency only to convert it back to original currency.

Example: Bid Ask

British pound (£) $1.60 $1.61

Malaysian ringgit (MYR) $.200 $.202

£ MYR8.1 MYR8.2

Buy £ @ $1.61, convert @ MYR8.1/£, then sell MYR @ $.200. Profit = $.01/£. (8.1 .2=1.62)

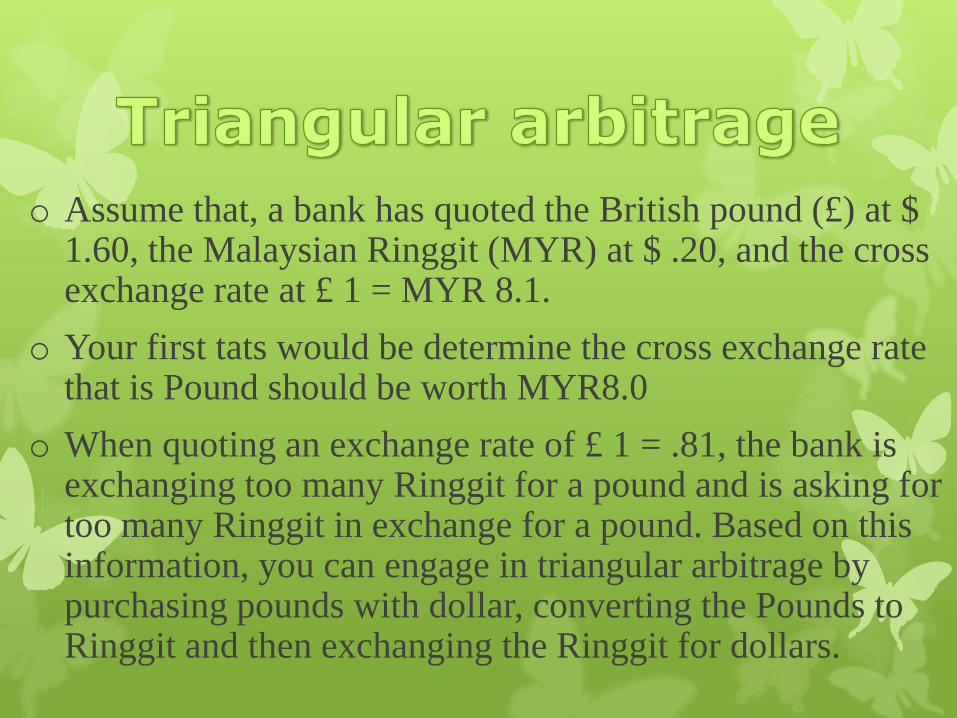

o Assume that, a bank has quoted the British pound (£) at $ 1.60, the Malaysian Ringgit (MYR) at $ .20, and the cross exchange rate at £ 1 = MYR 8.1.

o Your first tats would be determine the cross exchange rate that is Pound should be worth MYR8.0

o When quoting an exchange rate of £ 1 = .81, the bank is exchanging too many Ringgit for a pound and is asking for too many Ringgit in exchange for a pound. Based on this information, you can engage in triangular arbitrage by purchasing pounds with dollar, converting the Pounds to Ringgit and then exchanging the Ringgit for dollars.

o Covered interest arbitrage is the process of capitalizing on the interest rate differential between two countries, while covering for exchange rate risk.

o The logic of the term Covered interest arbitrage become clear when it is broken into two parts; “interest arbitrage” and “covered”.

o Interest arbitrage refers to the process of capitalizing on the difference between interest rates between two countries. On the other hand, Covered refers to hedging your position against exchange rate risk.

o Covered interest arbitrage involving investment dominated in different currencies using forward covered to reduce or eliminate currency risk

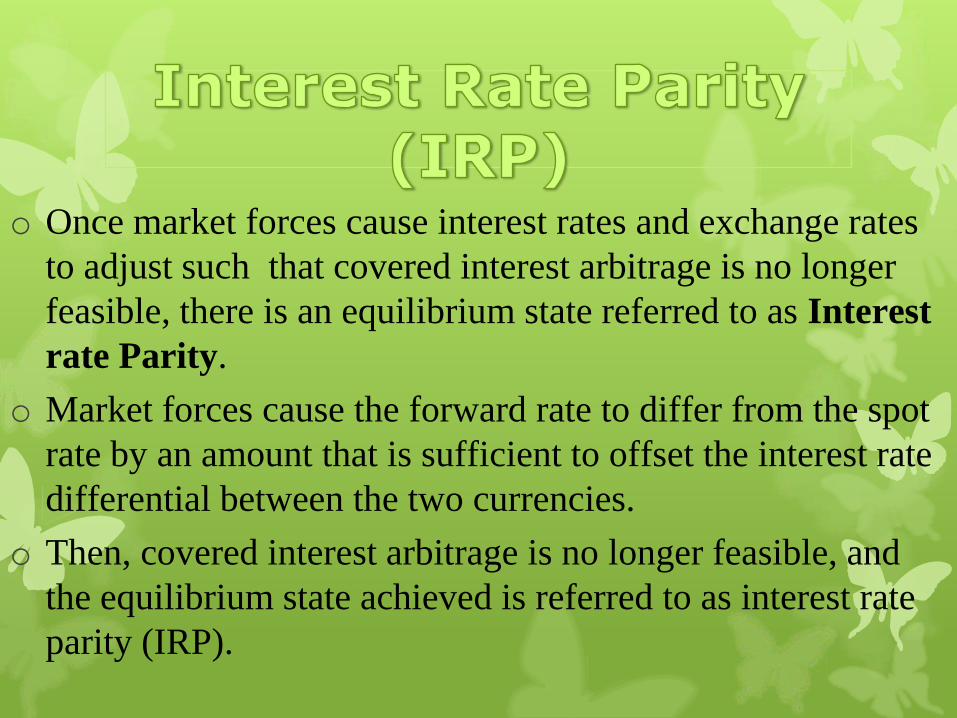

o Once market forces cause interest rates and exchange rates

to adjust such that covered interest arbitrage is no longer

feasible, there is an equilibrium state referred to as Interest

rate Parity.

o Market forces cause the forward rate to differ from the spot

rate by an amount that is sufficient to offset the interest rate

differential between the two currencies.

o Then, covered interest arbitrage is no longer feasible, and

the equilibrium state achieved is referred to as interest rate

parity (IRP).

o When IRP exists, it does not mean both local and foreign investors will earn the same returns.

o What it means is that investors cannot use covered interest arbitrage to achieve higher returns than those achievable in their respective home countries.

oTo test whether IRP exists, collect actual interest rate differentials and forward premiums for various currencies, and plot them on a graph.

o IRP holds when covered interest arbitrage is not possible or worthwhile.

o Various empirical studies indicate that IRP generally holds.

o While there are deviations from IRP, they are often not large enough to make covered interest arbitrage worthwhile.

o This is due to the characteristics of foreign investments, such as transaction costs, political risk, and differential tax laws.

o End-value of a $1 investment in the home country

= 1 + iH

o Equating the two and rearranging terms:

p =(1+iH)

– 1(1+iF)

forward =

(1 + home interest rate) – 1

premium (1 + foreign interest rate)

o The IRP relationship can be rewritten as follows:

F – S = S(1+p) – S = p = (1+iH)– 1 = (iH–iF)

S S (1+iF) (1+iF)

o The approximated form, p iH – iF,

provides a reasonable estimate when the interest rate differential is small.

o Locational arbitrage ensures that quoted exchange rates are similar across banks in different locations.

o Triangular arbitrage ensures that cross exchange rates are set properly.

o Covered interest arbitrage ensures that forward exchange rates are set properly.

o Any discrepancy will trigger arbitrage, which will then eliminate the discrepancy. Arbitrage thus makes the foreign exchange market more orderly.