INTERNATIONAL AND DOMESTIC TRANSFER PRICING. HISTORY Chapter X of the Income Tax Act, 1961 was...

37

INTERNATIONAL AND DOMESTIC TRANSFER PRICING

-

Upload

sibyl-sullivan -

Category

Documents

-

view

218 -

download

1

Transcript of INTERNATIONAL AND DOMESTIC TRANSFER PRICING. HISTORY Chapter X of the Income Tax Act, 1961 was...

INTERNATIONAL AND DOMESTIC

TRANSFER PRICING

HISTORY

Chapter X of the Income Tax Act, 1961 was amended by the Finance Act, 2001 for introducing the elaborate transfer pricing regime to the tax laws.

The provisions introduced the concepts of:

Associated Enterprises.

Arm’s Length Pricing [original concepts used, “fair market value” –40 A (2), market value –80 IA (7), “more than ordinary profits” –80 IA (11)].

International Transaction.

Uncontrolled Transaction.

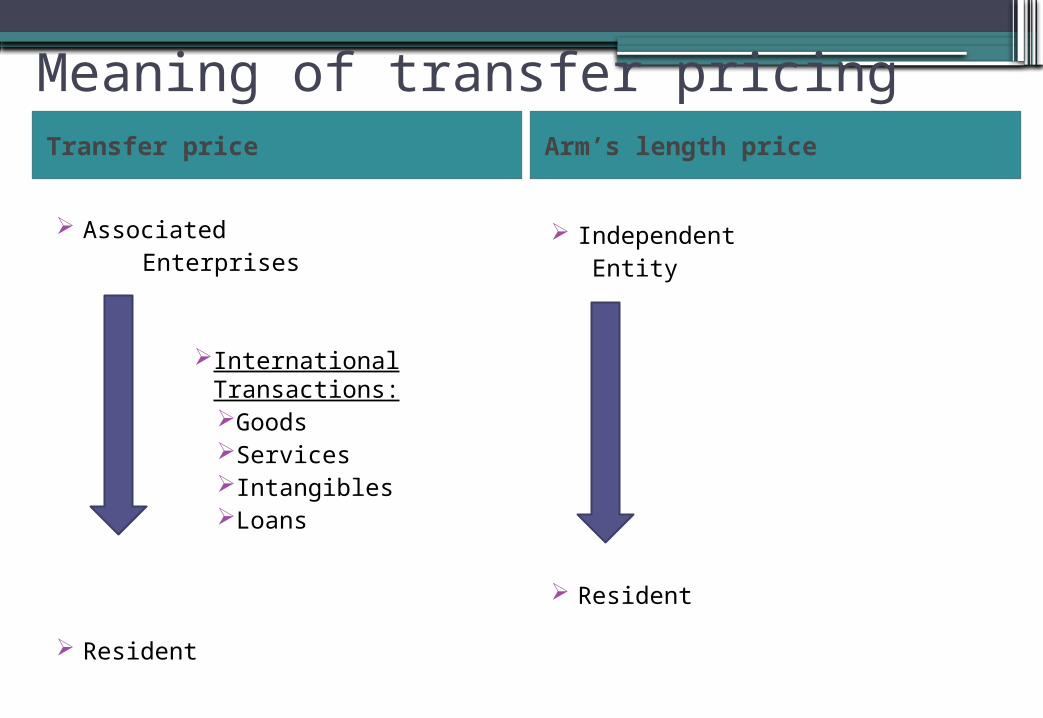

Meaning of transfer pricingTransfer price Arm’s length price

Associated Enterprises

International Transactions:GoodsServicesIntangiblesLoans

Resident

Independent Entity

Resident

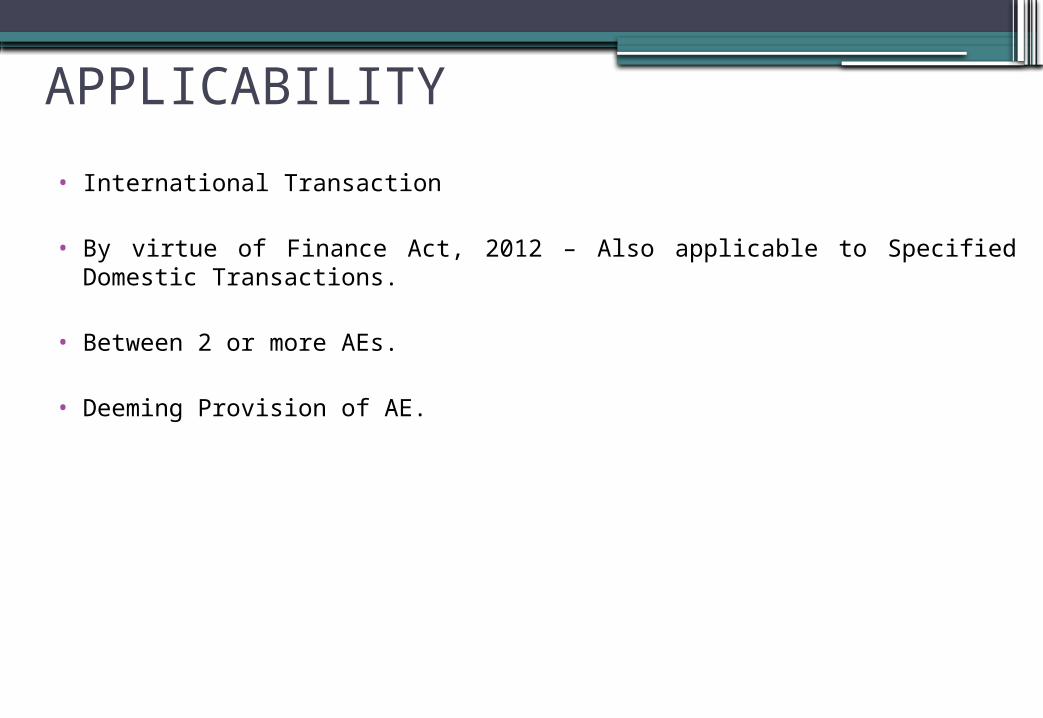

APPLICABILITY

• International Transaction

• By virtue of Finance Act, 2012 – Also applicable to Specified Domestic Transactions.

• Between 2 or more AEs.

• Deeming Provision of AE.

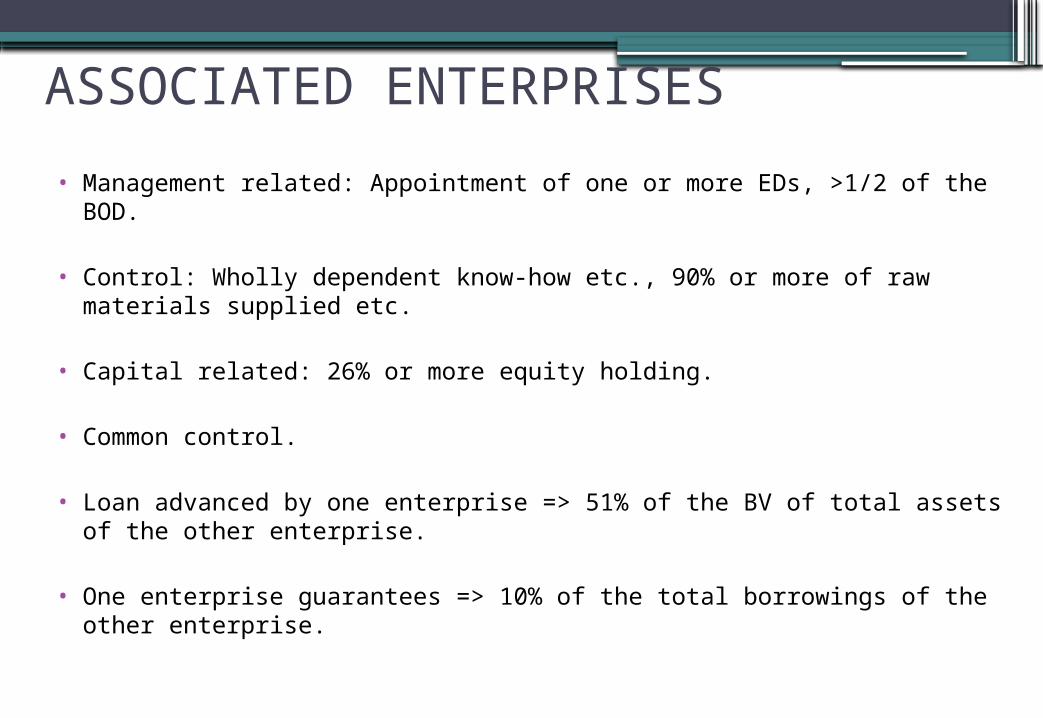

ASSOCIATED ENTERPRISES

• Management related: Appointment of one or more EDs, >1/2 of the BOD.

• Control: Wholly dependent know-how etc., 90% or more of raw materials supplied etc.

• Capital related: 26% or more equity holding.

• Common control.

• Loan advanced by one enterprise => 51% of the BV of total assets of the other enterprise.

• One enterprise guarantees => 10% of the total borrowings of the other enterprise.

INTERNATIONAL TRANSACTION• "transaction" includes an arrangement, understanding or action in concert,

—

whether or not such arrangement, understanding or action is formal or in writing; or

whether or not such arrangement, understanding or action is intended to be enforceable by legal proceeding.

• Transaction relates to:▫ Purchase, sale or lease;

▫ Provision of services;

▫ Lending or borrowing of money;

▫ Any other transaction having a bearing on the profits, income, losses or assets of such enterprises;

▫ Cost sharing agreements or arrangements.

DEEMED INTERNATIONAL TRANSACTION

Susbidiary

Outside India AE

---------------------------------------------------------------------------------------------------------------------------------

India

Relevant Transaction

C - Non AE

B - India

A - USA

Prior arrangement related to the relevant transaction

The terms of the relevant transaction are determined in substance by A – USA.

Deemed International Transaction

KEY DEFINITIONS• Arm’s Length Price:

The price which is applied or proposed to be applied in a transaction between persons other than AEs, in uncontrolled conditions.

• Uncontrolled transaction:

Uncontrolled transaction means a transaction between enterprises other than AEs, whether resident or non-resident.

MOST APPROPRIATE METHOD

• The arm's length price in relation to an international transaction [or specified domestic transaction] shall be determined by any of the following methods, being the most appropriate method:

(a) comparable uncontrolled price method;

(b) resale price method;

(c) cost plus method;

(d) profit split method;

(e) transactional net margin method;

(f) such other method as may be prescribed by the Board.

CUP METHODCOMPARABILITY FACTORS:

• Strong similarity of products and services;

• Functions;

• Volume;

• Contractual terms;

• Economic conditions;

• Geography of markets.

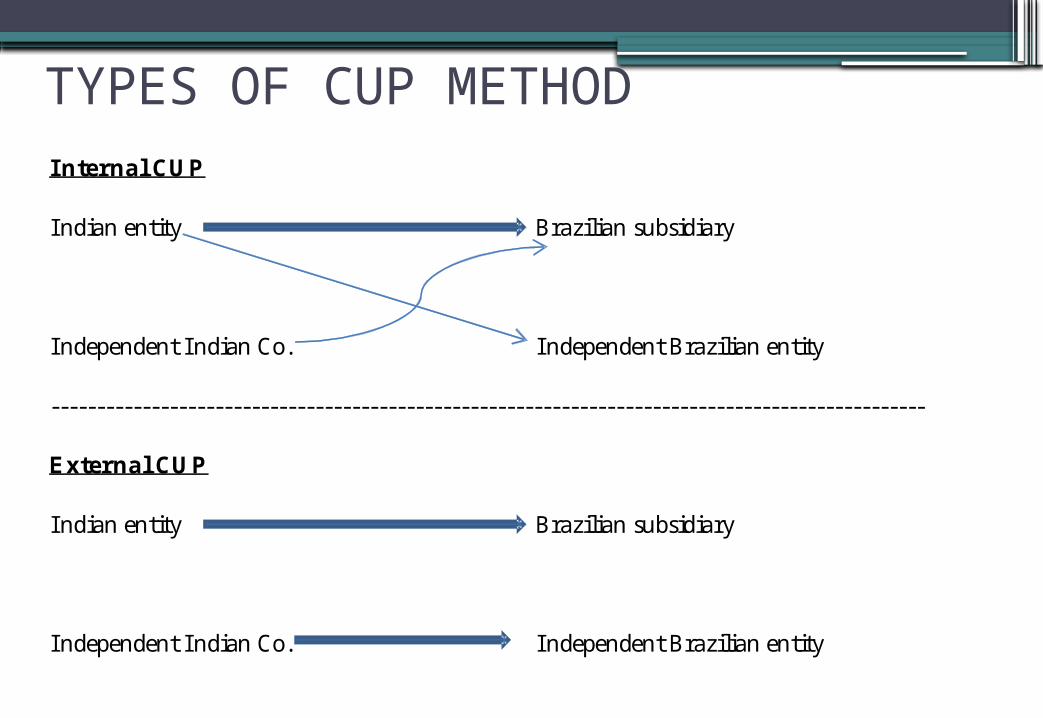

TYPES OF CUP METHODInternal CUP

Indian entity Brazilian subsidiary

Independent Indian Co. Independent Brazilian entity

------------------------------------------------------------------------------------------------

External CUP

Indian entity Brazilian subsidiary

Independent Indian Co. Independent Brazilian entity

CUP METHOD: ExamplesA Co. R Co. (Independent Third Party)

Susbidiary

Outside India AE

---------------------------------------------------------------------------------------------------------------------------------

India B Co. S Co.(Independent Third Party)

In this case, factors to be taken into consideration before applying CUP method are:* whether this is the only comparable;* effect of brand;

If above factors are material, reasonable and accurate adjustments are required for applying CUP.

Sells branded coffee beans

Sells coffee beans Factors such as:

* Quality of beans;

* Quantity of beans;

* Time of sale;

And other assumptions remain same.

RESALE PRICE METHOD (RPM)• Used in case of purchase of goods or services from related parties for

resale to unrelated parties without substantial value addition.

• Price reduced by normal gross margin earned by unrelated party for same or similar products or services.

• Need for similarity of functions performed and risks undertaken.

• Gross margin used as the PLI.

• Generally used for marketing operations of finished products, where distributor does not perform significant value addition to the product.

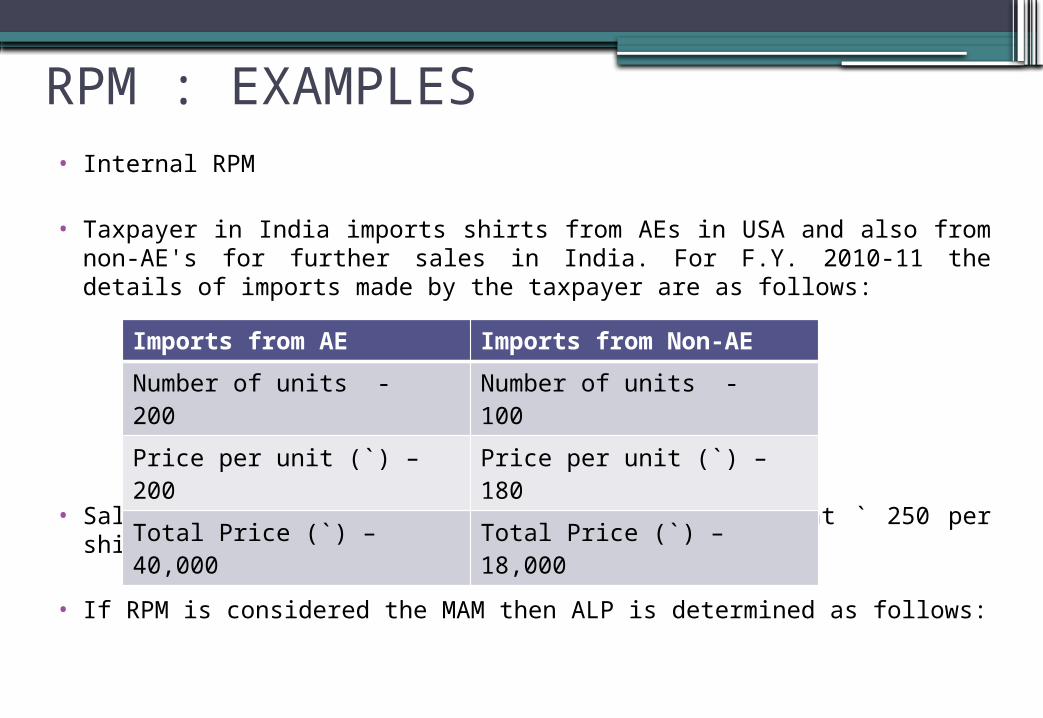

RPM : EXAMPLES• Internal RPM

• Taxpayer in India imports shirts from AEs in USA and also from non-AE's for further sales in India. For F.Y. 2010-11 the details of imports made by the taxpayer are as follows:

• Sale price to third party customers in India is at ` 250 per shirt.

• If RPM is considered the MAM then ALP is determined as follows:

Imports from AE Imports from Non-AE

Number of units - 200 Number of units - 100

Price per unit (`) – 200 Price per unit (`) – 180

Total Price (`) – 40,000 Total Price (`) – 18,000

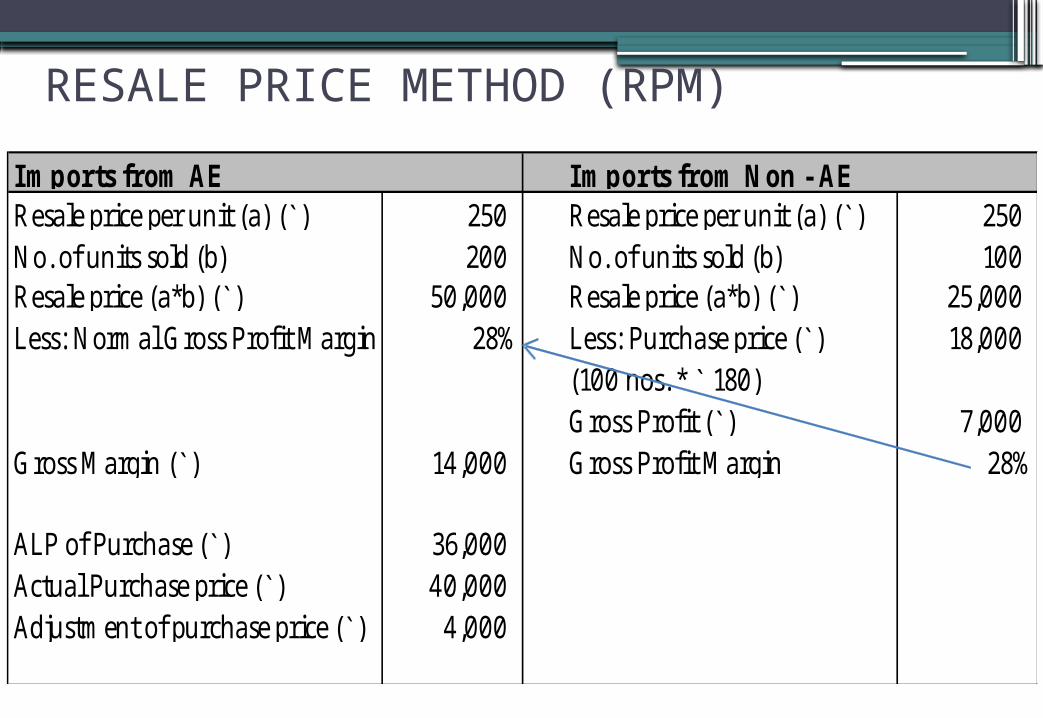

RESALE PRICE METHOD (RPM)

Resale price per unit (a) (`) 250 Resale price per unit (a) (`) 250 No. of units sold (b) 200 No. of units sold (b) 100 Resale price (a*b) (`) 50,000 Resale price (a*b) (`) 25,000

28% Less: Purchase price (`) 18,000 (100 nos. * ̀ 180)Gross Profit (`) 7,000

Gross Margin (`) 14,000 Gross Profit Margin 28%

ALP of Purchase (`) 36,000 Actual Purchase price (`) 40,000 Adjustment of purchase price (`) 4,000

Less: Normal Gross Profit Margin

Imports from AE Imports from Non - AE

COST PLUS METHOD (CPM)• Method using the costs incurred in a controlled transaction for property

or services provided to an associate purchaser.

• An appropriate cost plus mark-up is added to the above cost in light of the FAR.

• More appropriate to transactions like provision of services, transfer of semi-finished goods, long-term buy/sell arrangement.

• Tolerant to product differences as compared to CUP method:

ALP = Direct + Indirect cost of production + GP mark-up of entity selling goods to AE.

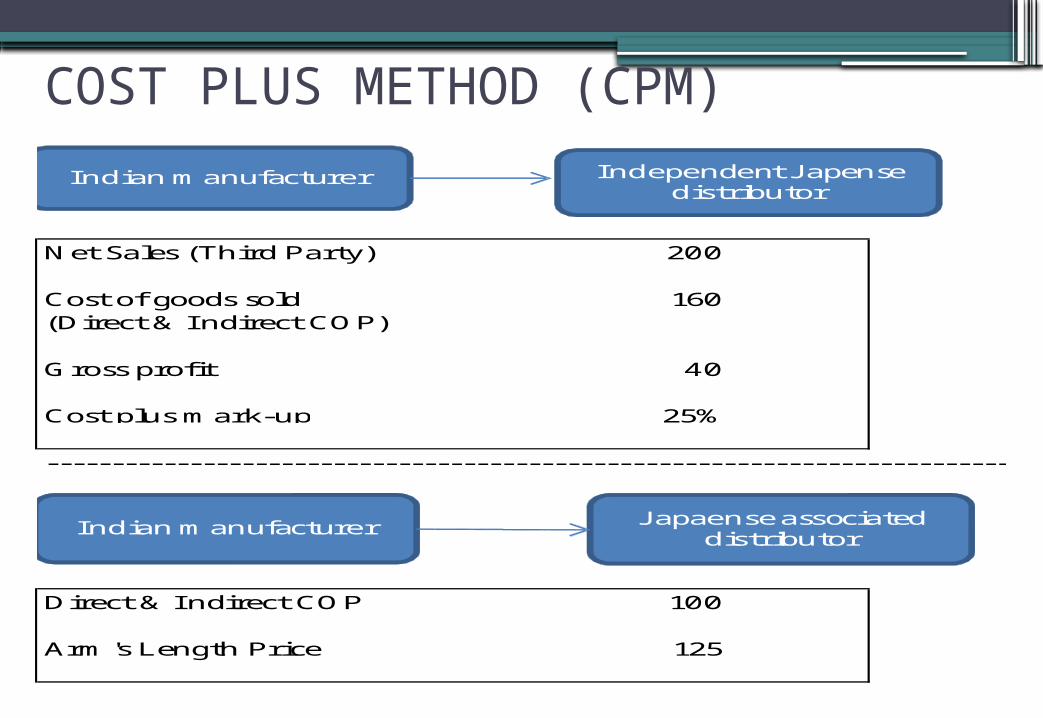

COST PLUS METHOD (CPM)

Net Sales (Third Party) 200

Cost of goods sold 160(Direct & Indirect COP)

Gross profit 40

Cost plus mark-up 25%

---------------------------------------------------------------------------

Direct & Indirect COP 100

Arm's Length Price 125

Indian manufacturer Independent Japensedistributor

Indian manufacturer Japaenseassociated distributor

CPM: Practical issues and challenges• Focuses on GP margins, which are heavily influenced by the scope,

intensity of functions and accounting methods.

• Requires high level of comparability between the tested party and the comparables in terms of functions performed.

• Relatively difficult to apply in loss situation.

• Difference in the cost base may require adjustment for proper comparability.

Inadequate data to compute the gross margins accurately. This is because under Indian GAAP,

companies reporting financial statements are not required to compute the gross margin

separately.

Profit Split Method (PSM)• Only method for which Rules have prescribed the types of transaction to

which it may be applicable:

▫ Integrated services provided by more than one enterprise.▫ Multiple inter-related transactions, which cannot be separately

evaluated.▫ Transfer of unique intangibles.

▫ Applied in cases where:

Both entities have unique intangibles.

Operations of both the entities are so integrated that identifying the tested party is very difficult.

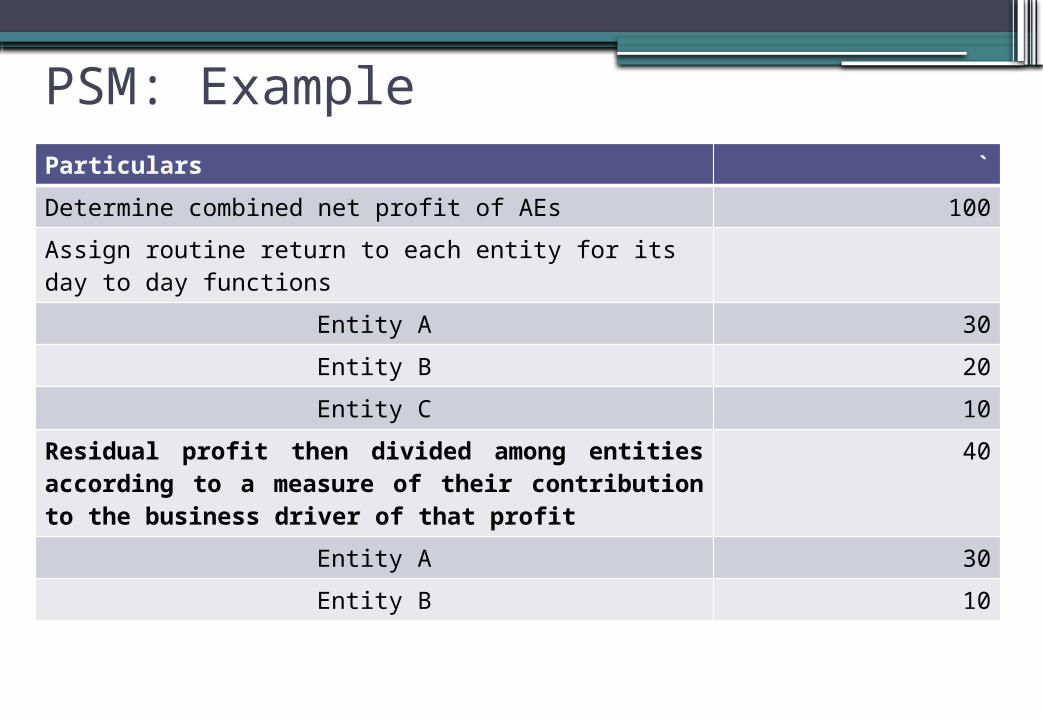

PSM: ExampleParticulars `

Determine combined net profit of AEs 100

Assign routine return to each entity for its day to day functions

Entity A 30

Entity B 20

Entity C 10

Residual profit then divided among entities according to a measure of their contribution to the business driver of that profit

40

Entity A 30

Entity B 10

Transactional Net Margin Method (TNMM)

▫ Most frequently used and practical method.

▫ Comparison at operating margin level.

▫ Broad level of similarity of functions, assets and risks.

▫ Selection of the right comparables and PLI are critical factors.

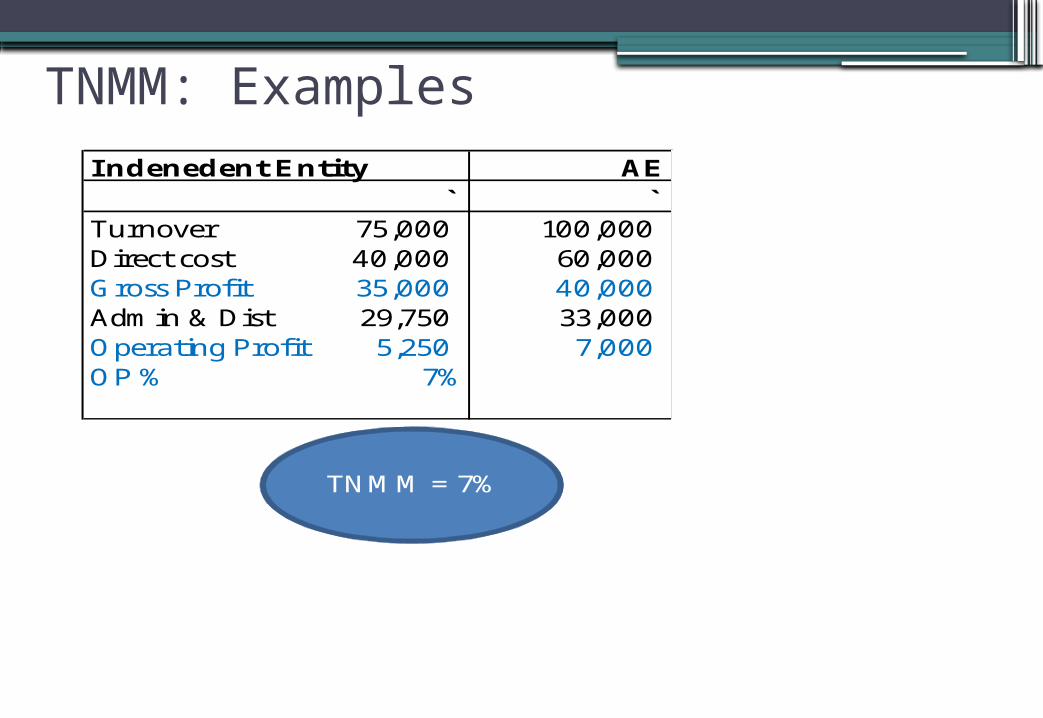

TNMM: ExamplesIndenedent Entity AE

` `Turnover 75,000 100,000 Direct cost 40,000 60,000 Gross Profit 35,000 40,000 Admin & Dist 29,750 33,000 Operating Profit 5,250 7,000 OP % 7%

TNMM = 7%

TNMM: Practical issues and challenges▫ Aggregations v/s Transactional analysis.

▫ Segmental v/s Entity.

▫ Internal TNMM v/s External TNMM.

▫ Lack of availability of data at the time of undertaking transaction / documentation.

6th Method▫ Rule 10AB.

▫ For the purposes of clause (f) of sub-section (1) of section 92C, the other

method for determination of the arms' length price in relation to an

international transaction shall be any method which takes into account

the price which has been charged or paid, or would have been charged or

paid, for the same or similar uncontrolled transaction, with or between

non-associated enterprises, under similar circumstances, considering all

the relevant facts.

6th Method - Observation▫ Other method can be used for following transactions:

Valuation of intangible property.

Valuation of shares.

Reimbursements.

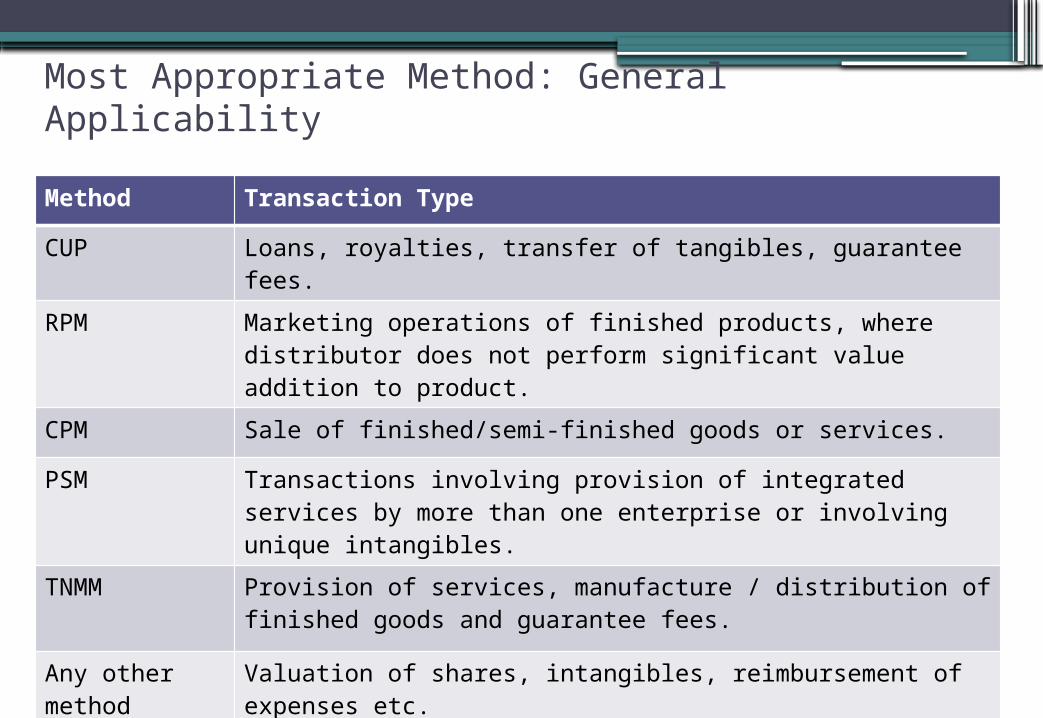

Most Appropriate Method: General Applicability

Method Transaction Type

CUP Loans, royalties, transfer of tangibles, guarantee fees.

RPM Marketing operations of finished products, where distributor does not perform significant value addition to product.

CPM Sale of finished/semi-finished goods or services.

PSM Transactions involving provision of integrated services by more than one enterprise or involving unique intangibles.

TNMM Provision of services, manufacture / distribution of finished goods and guarantee fees.

Any other method

Valuation of shares, intangibles, reimbursement of expenses etc.

DocumentationEntity related Price related Transaction related

i) Profile of industry i) Transaction terms i) Agreements

ii) Profile of group ii) FAR analysis ii) Invoices

iii) Profile of Indian entity iii) Economic analysis iii) Pricing related correspondence(letters, emails etc)

iv) Profile of Aes iv) Forecasts, budgets, estimates

Contemporaneous documentationrequirement

Documents to be retained for 8 years from the end of the relevant A.Y.

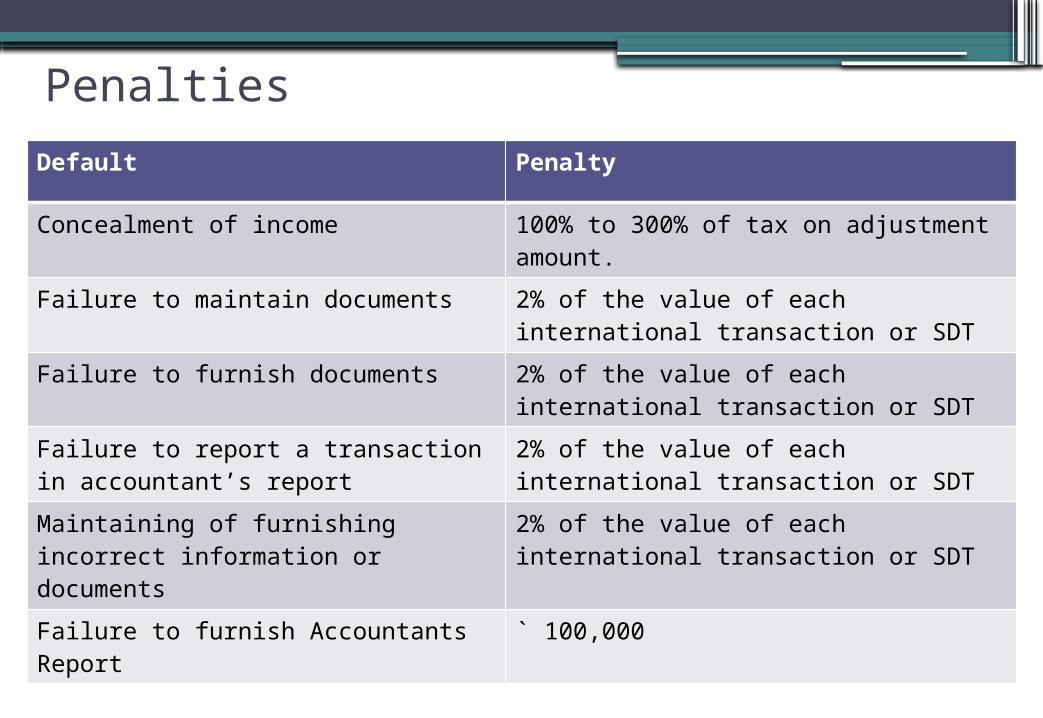

PenaltiesDefault Penalty

Concealment of income 100% to 300% of tax on adjustment amount.

Failure to maintain documents 2% of the value of each international transaction or SDT

Failure to furnish documents 2% of the value of each international transaction or SDT

Failure to report a transaction in accountant’s report

2% of the value of each international transaction or SDT

Maintaining of furnishing incorrect information or documents

2% of the value of each international transaction or SDT

Failure to furnish Accountants Report

` 100,000

TRANSFER PRICINGSPECIFIED DOMESTIC TRANSACTIONS

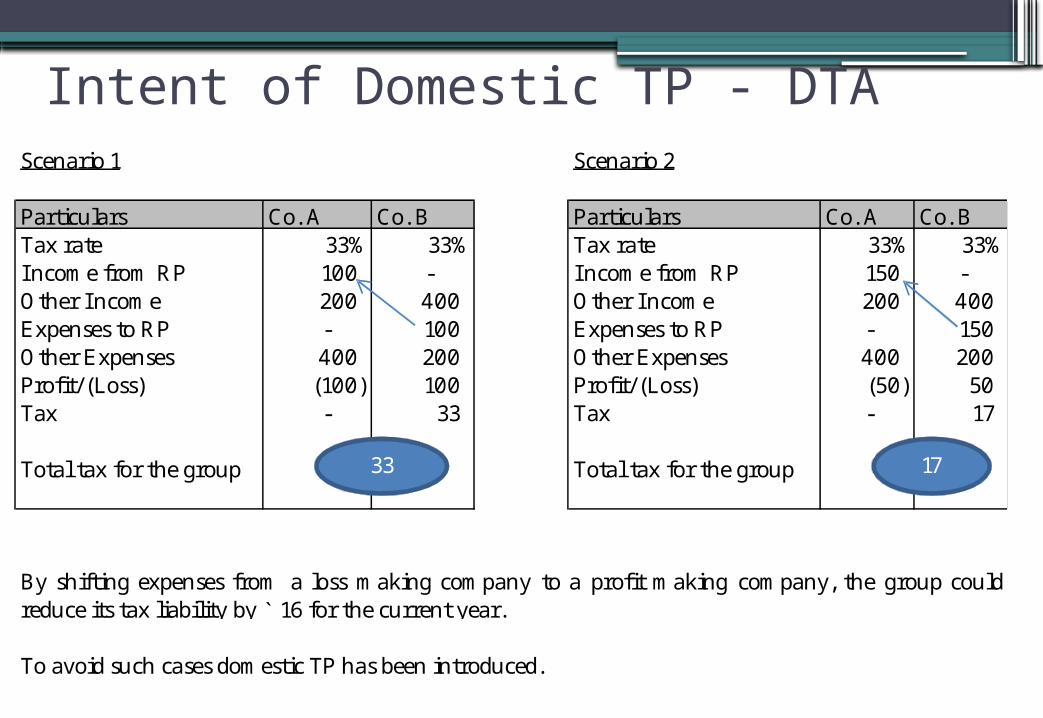

Intent of Domestic TP - DTAScenario 1 Scenario 2

Particulars Co. A Co. B Particulars Co. A Co. BTax rate 33% 33% Tax rate 33% 33%Income from RP 100 - Income from RP 150 - Other Income 200 400 Other Income 200 400 Expenses to RP - 100 Expenses to RP - 150 Other Expenses 400 200 Other Expenses 400 200 Profit/ (Loss) (100) 100 Profit/ (Loss) (50) 50 Tax - 33 Tax - 17

Total tax for the group Total tax for the group

To avoid such cases domestic TP has been introduced.

By shifting expenses from a loss making company to a profit making company, the group couldreduce its tax liability by ̀ 16 for the current year.

33 17

Intent of Domestic TP – DTA & Tax Holiday Unit

Scenario 1 Scenario 2

Particulars THU DTA Particulars THU DTATax rate 0% 33% Tax rate 0% 33%Income from RP 200 - Income from RP 325 - Other Income 300 700 Other Income 300 700 Expenses to RP - 200 Expenses to RP - 325 Other Expenses 350 200 Other Expenses 350 200 Profit/ (Loss) 150 300 Profit/ (Loss) 275 175 Tax - 99 Tax - 58

Total tax for the group Total tax for the group

To avoid such cases domestic TP has been introduced.

By shifting expenses from a DTA to a tax holiday unit, the group could reduce its tax liability by` 43 for the current year.

99 58

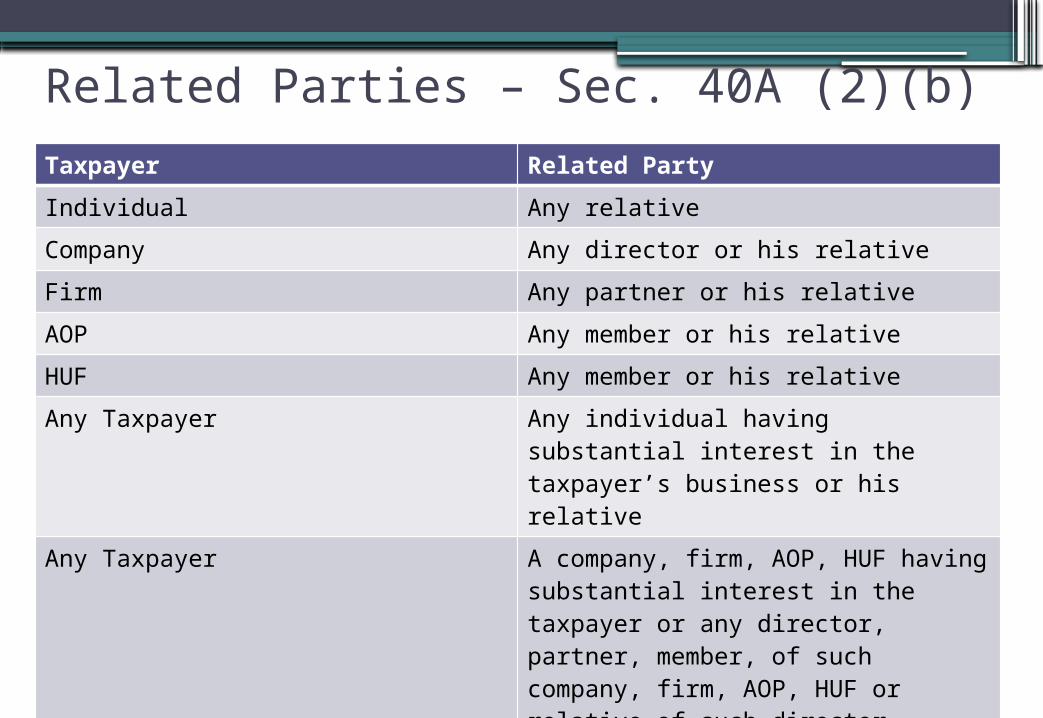

Related Parties – Sec. 40A (2)(b)Taxpayer Related Party

Individual Any relative

Company Any director or his relative

Firm Any partner or his relative

AOP Any member or his relative

HUF Any member or his relative

Any Taxpayer Any individual having substantial interest in the taxpayer’s business or his relative

Any Taxpayer A company, firm, AOP, HUF having substantial interest in the taxpayer or any director, partner, member, of such company, firm, AOP, HUF or relative of such director, partner or member

SDT: Issues which may arise…• Whether provisions will be applicable if both assessee are falling under

same tax bracket?

• In case of upward adjustment – whether benefit of corresponding adjustment is available?

• If TPO accepts the ALP of the domestic transaction whether AO can still trigger business expediency and benefit test?

• Can AO step into shoes of businessman?

• What is the impact of capital expenditure transactions?

Transfer Pricing Process

Identification of Comparable Transactions

Identification of Intra Group transactions

FAR Analysis

Identification of Comparable Transactions

Establishingcomparability,

adjustment for material differences

Selection of Most AppropriateMethod Determination of ALP

Adjustments

Documentation

Return Filing

Documentation is the key

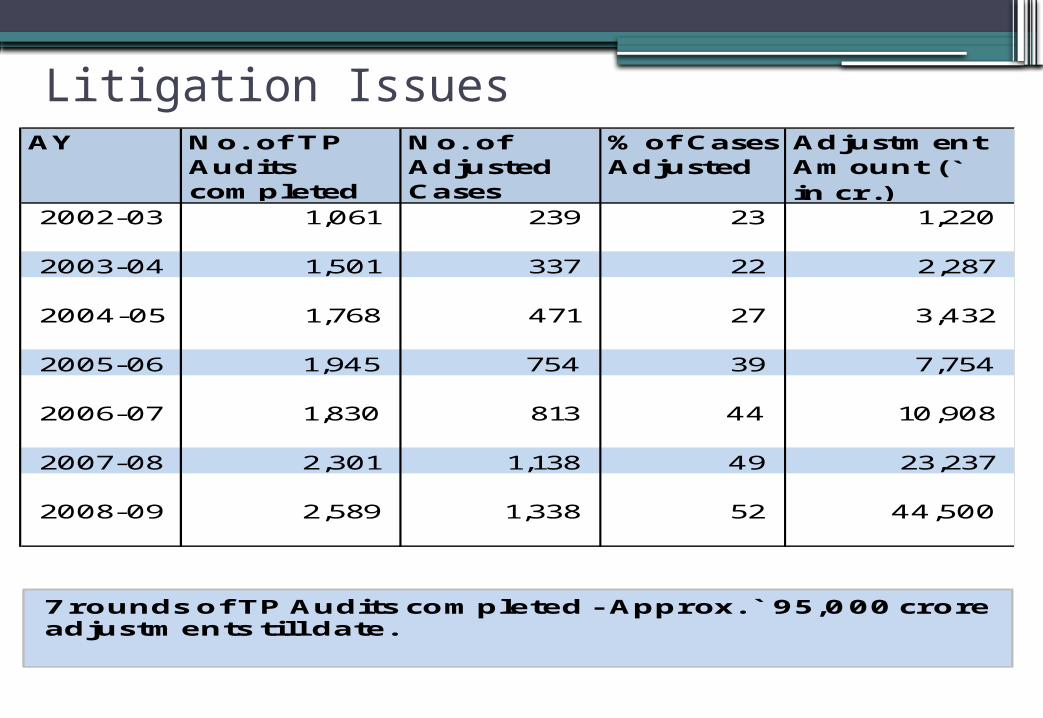

Litigation IssuesAY No. of TP

Audits completed

No. of Adjusted Cases

% of Cases Adjusted

Adjustment Amount (` in cr.)

2002-03 1,061 239 23 1,220

2003-04 1,501 337 22 2,287

2004-05 1,768 471 27 3,432

2005-06 1,945 754 39 7,754

2006-07 1,830 813 44 10,908

2007-08 2,301 1,138 49 23,237

2008-09 2,589 1,338 52 44,500

7 rounds of TP Audits completed - Approx. ̀ 95,000 crore adjustments till date.

![THE CHHATTISGARH MUNICIPALITIES ACT, 1961 [Act No. 37 of ... · THE CHHATTISGARH MUNICIPALITIES ACT, 1961 [Act No. 37 of 1961] [20th November, 1961] Chapter I - PRELIMINARY Section](https://static.fdocuments.in/doc/165x107/5ed3fd1c8d46b66d2263399d/the-chhattisgarh-municipalities-act-1961-act-no-37-of-the-chhattisgarh-municipalities.jpg)

![INCOME-TAX ACT, 1961 - International Center for Not-for ... · INCOME-TAX ACT, 1961 * [43 OF 1961] [AS AMENDED BY FINANCE ACT, 2008] ... that revenue derived from land shall not include](https://static.fdocuments.in/doc/165x107/5af0e50e7f8b9a8b4c8e114d/income-tax-act-1961-international-center-for-not-for-act-1961-43-of-1961.jpg)

![INCOME-TAX ACT, 1961€¦ · INCOME-TAX ACT, 1961 * [43 OF 1961] [AS AMENDED BY FINANCE ACT, 2008] An Act to consolidate and amend the law relating to income-tax and super-tax BE](https://static.fdocuments.in/doc/165x107/6097f37f4534cb51153b4a4c/income-tax-act-1961-income-tax-act-1961-43-of-1961-as-amended-by-finance.jpg)