International Accounting Standards Board (IASB) ACTG 4570/5570.

24

International Accounting Standards Board (IASB) ACTG 4570/5570

-

Upload

kerry-atkinson -

Category

Documents

-

view

233 -

download

5

Transcript of International Accounting Standards Board (IASB) ACTG 4570/5570.

International Accounting Standards Board (IASB)

ACTG 4570/5570

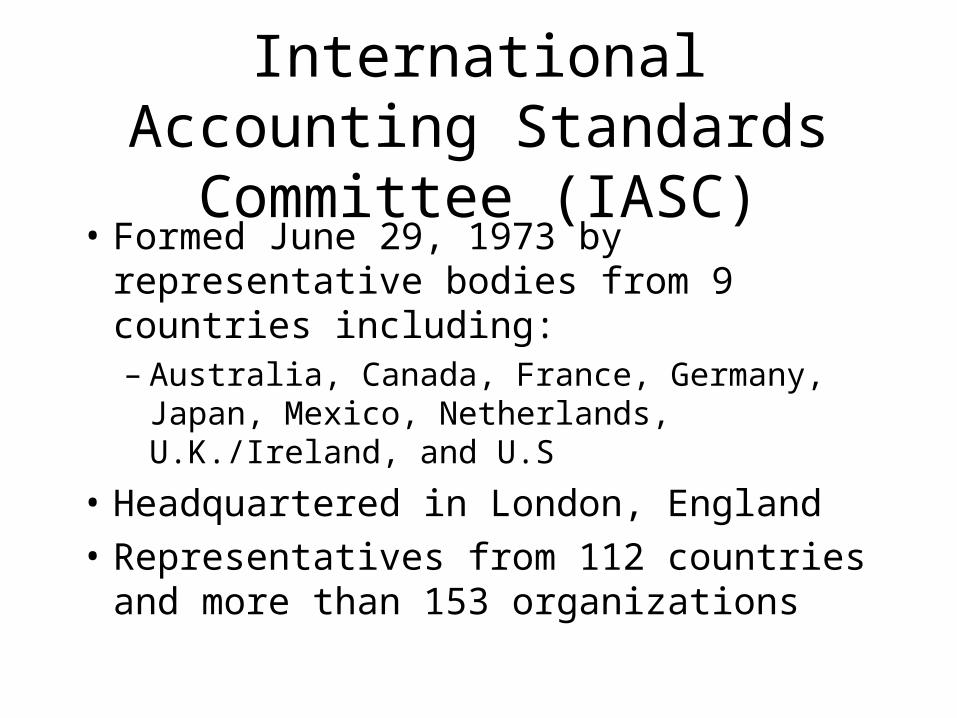

International Accounting Standards Committee (IASC)

• Formed June 29, 1973 by representative bodies from 9 countries including:– Australia, Canada, France, Germany, Japan,

Mexico, Netherlands, U.K./Ireland, and U.S

• Headquartered in London, England

• Representatives from 112 countries and more than 153 organizations

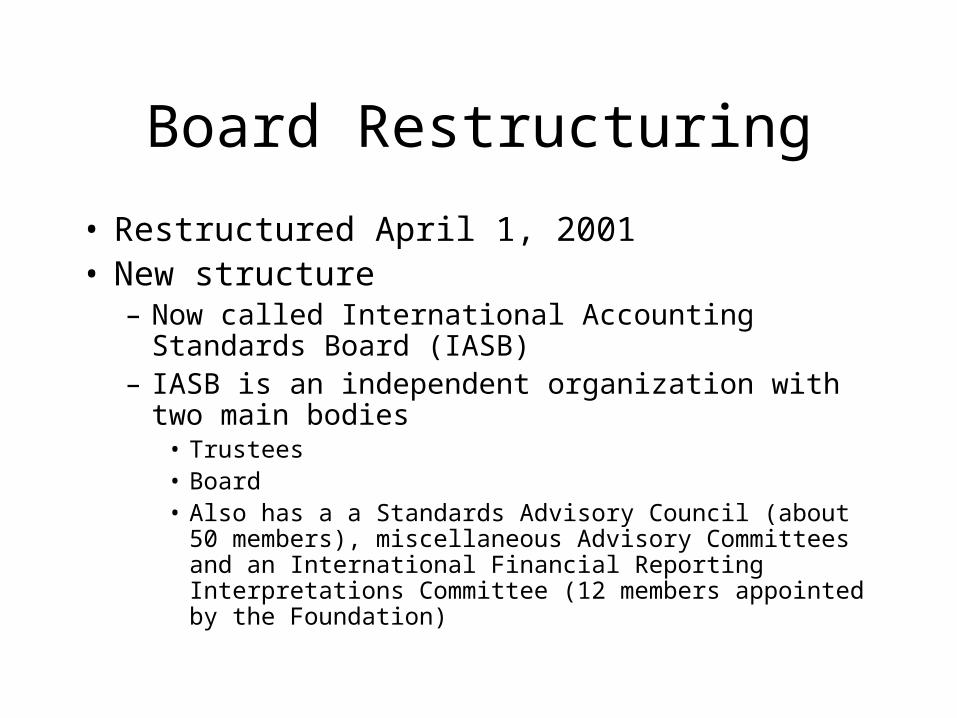

Board Restructuring

• Restructured April 1, 2001• New structure

– Now called International Accounting Standards Board (IASB)

– IASB is an independent organization with two main bodies

• Trustees• Board• Also has a a Standards Advisory Council (about 50 members),

miscellaneous Advisory Committees and an International Financial Reporting Interpretations Committee (12 members appointed by the Foundation)

Board Restructuring

• Trustees– 19 highly respected experienced members– Chairman of trustees is Phil Laskawy, Former

Chairman and CEO of Ernst & Young, New York, USA

– Main duties• Appoint Board, Committee, and Council Members• Exercise oversight of Board• Raise funds

Board Restructuring

• Board– Sole responsibility for setting accounting standards

– 12 full-time, 2 part-time, paid voting members

– Have best available combination of technical skills and international business experience

– First chairman of the new IASC Board• Sir David Tweetie, former U.K. Accounting Standards Board

Chairman

– List of members

Mission Statement

• The International Accounting Standards Board is an independent, privately-funded accounting standard setter based in London, United Kingdom. Board Members come from nine countries and have a variety of functional backgrounds.

• The Board is committed to developing, in the public interest, a single set of high quality, understandable and enforceable global accounting standards that require transparent and comparable information in general purpose financial statements.

• In addition, the Board cooperates with national accounting standard setters to achieve convergence in accounting standards around the world.

Standard Setting Process

• 1. The Board establishes an Advisory Committee to give advice on the issues arising in the project. Consultation with the Advisory Committee and the Standards Advisory Council occurs throughout the project.

• 2. IASB may develop and publish Discussion Documents for public comment.

• 3. Following the receipt and review of comments, IASB would develop and publish an Exposure Draft for public comment

Standard Setting Process

• 4. Following the receipt and review of comments, IASB would issue a final International Financial Reporting Standard.

• 5. Publication of a Standard, Exposure Draft, or final SIC Interpretation requires approval by 8 of the 14 members. Other decisions, including the issuance of a Draft Statement of Principles or a Discussion Paper and agenda decisions, requires a simple majority of the Board Members present at a meeting attended by 50% or more of the board members.

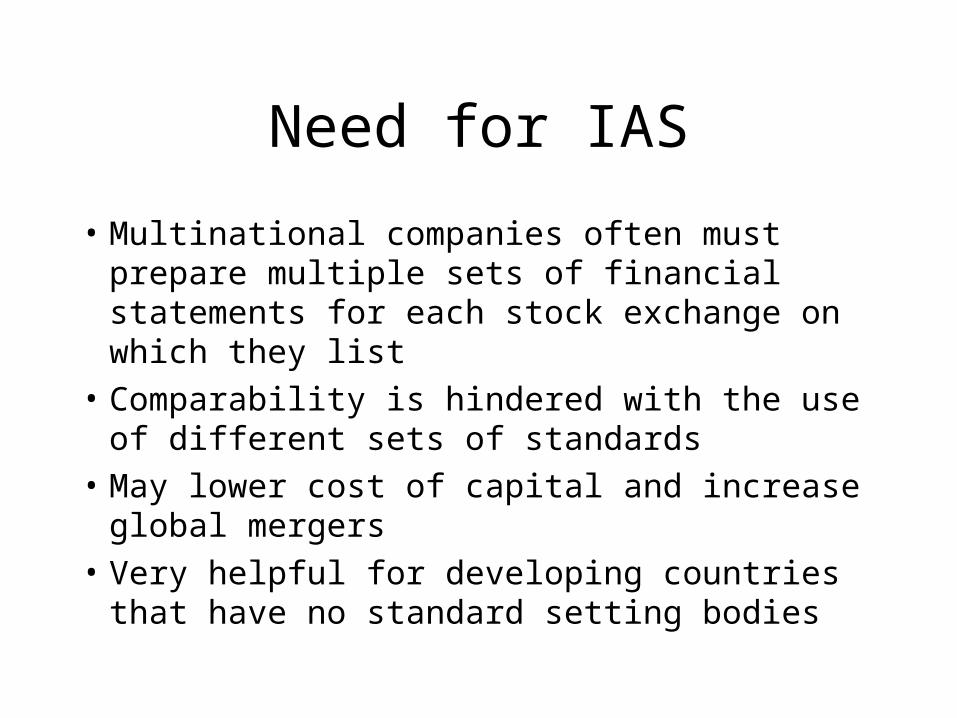

Need for IAS

• Multinational companies often must prepare multiple sets of financial statements for each stock exchange on which they list

• Comparability is hindered with the use of different sets of standards

• May lower cost of capital and increase global mergers

• Very helpful for developing countries that have no standard setting bodies

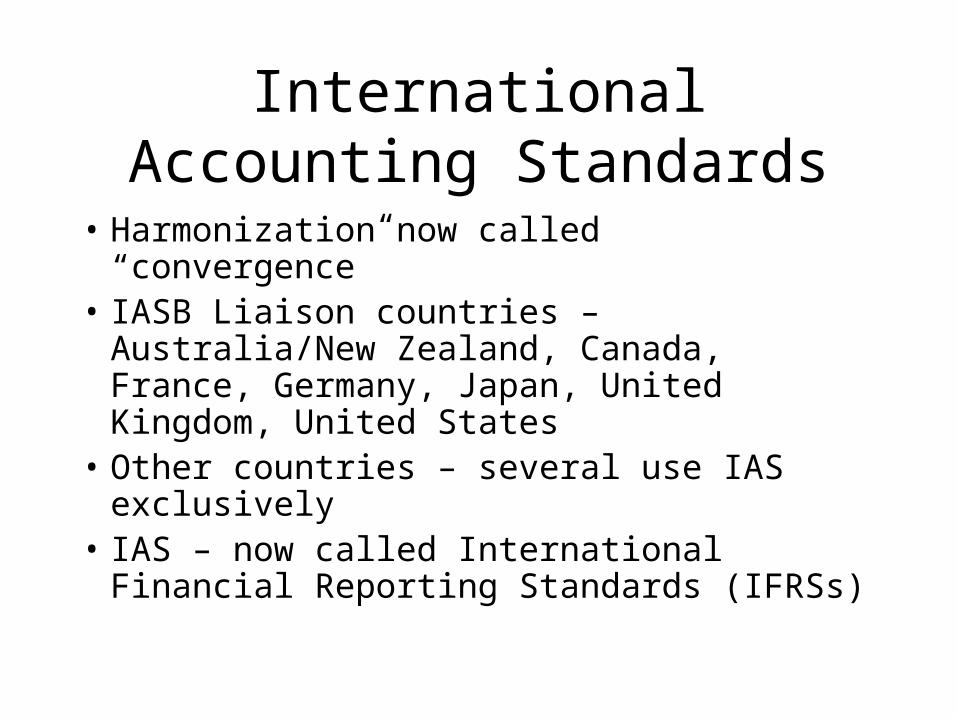

International Accounting Standards

• Harmonization now called “convergence”• IASB Liaison countries – Australia/New

Zealand, Canada, France, Germany, Japan, United Kingdom, United States

• Other countries – several use IAS exclusively

• IAS – now called International Financial Reporting Standards (IFRSs)

Use of IFRS

• European Union – All listed companies must use IFRS beginning January 1, 2005 (NOW!!!!!)

• Those companies in the E.U. trading in the U.S. and now using U.S. GAAP have until 2007 to change to IFRS

• Several other countries (over 100 in total) have changed to IFRS as well – Australia, China, New Zealand, Russia, Switzerland, U.S. SUBSIDIARIES OF ANY OF THESE COUNTRIES!!!!!

• Even Canada in 2007.

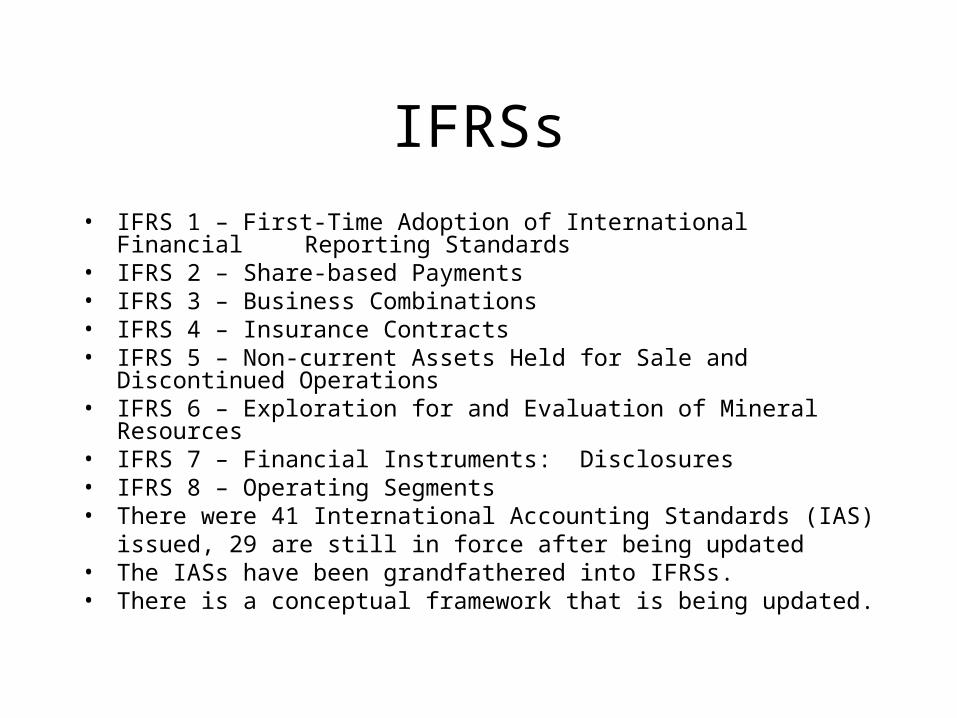

IFRSs

• IFRS 1 – First-Time Adoption of International Financial Reporting Standards

• IFRS 2 – Share-based Payments• IFRS 3 – Business Combinations• IFRS 4 – Insurance Contracts• IFRS 5 – Non-current Assets Held for Sale and

Discontinued Operations• IFRS 6 – Exploration for and Evaluation of Mineral Resources• IFRS 7 – Financial Instruments: Disclosures• IFRS 8 – Operating Segments• There were 41 International Accounting Standards (IAS)

issued, 29 are still in force after being updated• The IASs have been grandfathered into IFRSs.• There is a conceptual framework that is being updated.

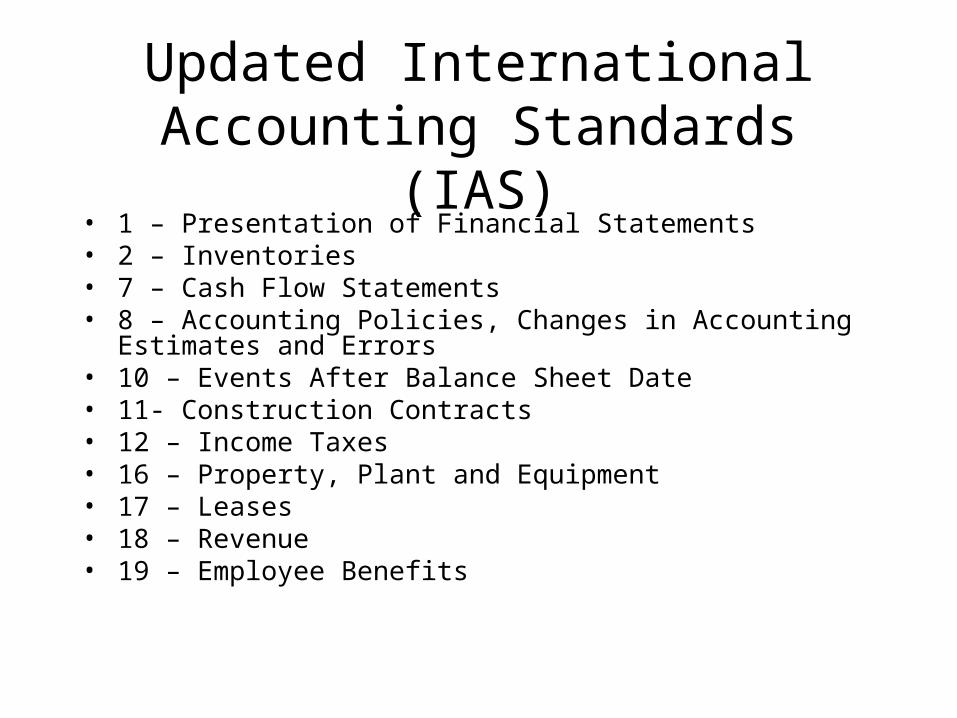

Updated International Accounting Standards (IAS)

• 1 – Presentation of Financial Statements• 2 – Inventories• 7 – Cash Flow Statements• 8 – Accounting Policies, Changes in Accounting Estimates and Errors• 10 – Events After Balance Sheet Date• 11- Construction Contracts• 12 – Income Taxes• 16 – Property, Plant and Equipment• 17 – Leases• 18 – Revenue• 19 – Employee Benefits

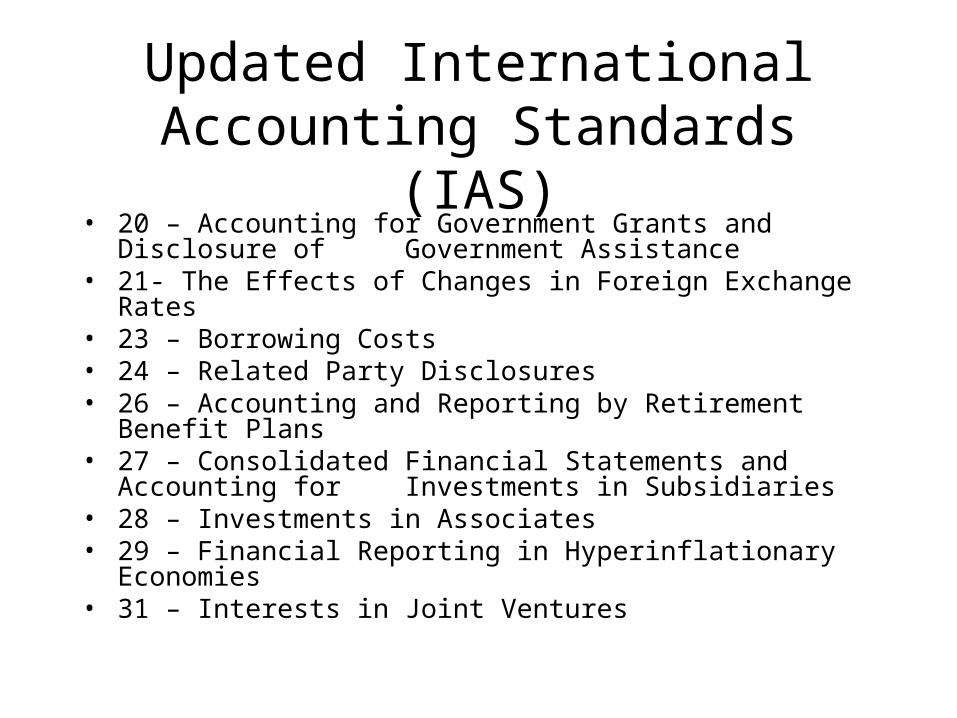

Updated International Accounting Standards (IAS)

• 20 – Accounting for Government Grants and Disclosure of Government Assistance

• 21- The Effects of Changes in Foreign Exchange Rates• 23 – Borrowing Costs• 24 – Related Party Disclosures• 26 – Accounting and Reporting by Retirement Benefit Plans• 27 – Consolidated Financial Statements and Accounting for

Investments in Subsidiaries• 28 – Investments in Associates• 29 – Financial Reporting in Hyperinflationary Economies• 31 – Interests in Joint Ventures

Updated International Accounting Standards (IAS)

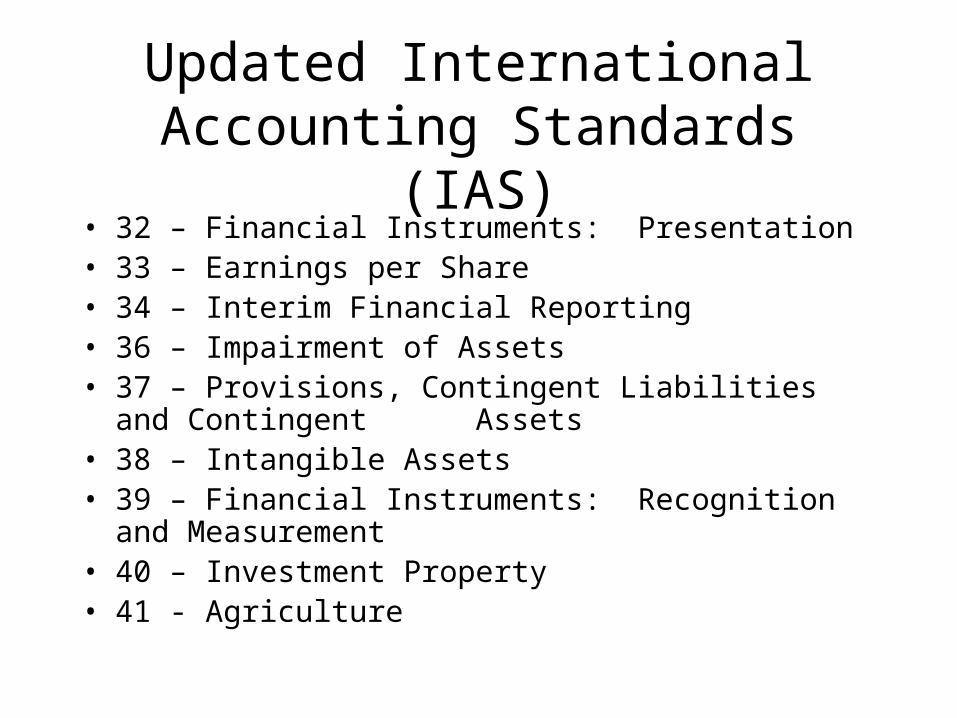

• 32 – Financial Instruments: Presentation • 33 – Earnings per Share• 34 – Interim Financial Reporting • 36 – Impairment of Assets• 37 – Provisions, Contingent Liabilities and Contingent

Assets • 38 – Intangible Assets• 39 – Financial Instruments: Recognition and Measurement• 40 – Investment Property• 41 - Agriculture

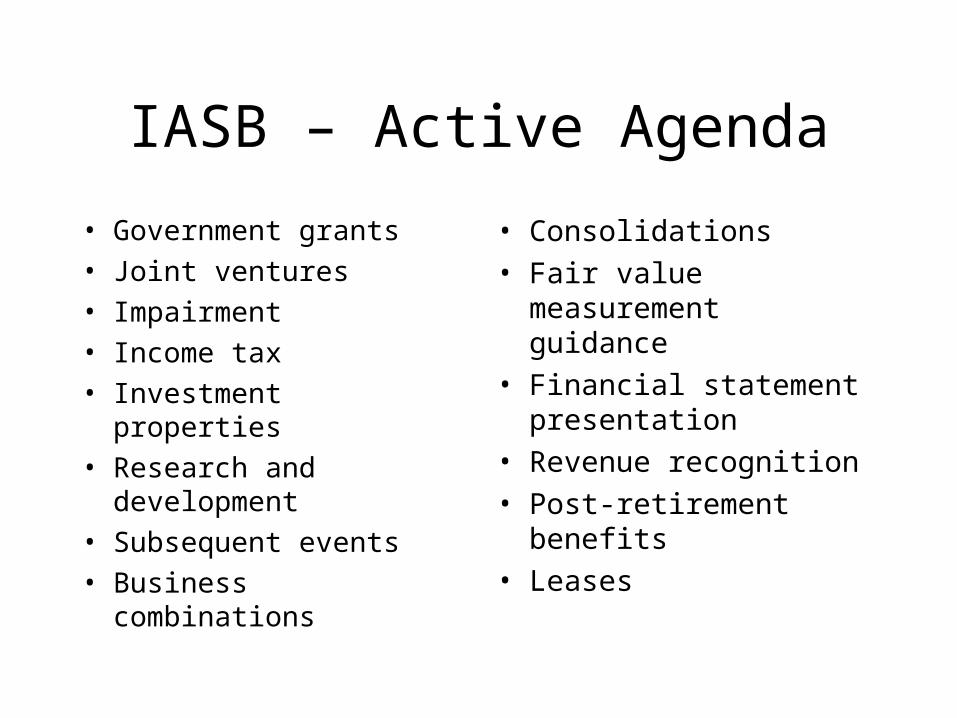

IASB – Active Agenda

• Government grants

• Joint ventures

• Impairment

• Income tax

• Investment properties

• Research and development

• Subsequent events

• Business combinations

• Consolidations

• Fair value measurement guidance

• Financial statement presentation

• Revenue recognition

• Post-retirement benefits

• Leases

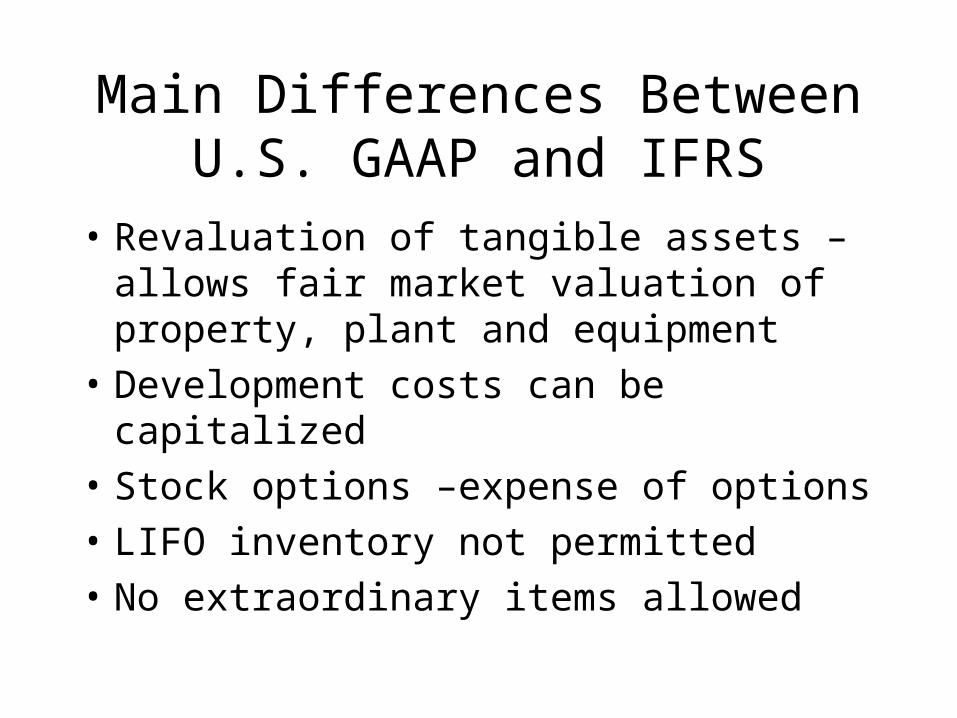

Main Differences Between U.S. GAAP and IFRS

• Revaluation of tangible assets – allows fair market valuation of property, plant and equipment

• Development costs can be capitalized

• Stock options –expense of options

• LIFO inventory not permitted

• No extraordinary items allowed

Differences from U.S. GAAP

• IFRS have no enforceability internationally; only enforceable by local country adopting them.

• IFRSs deemed less rigorous• IFRSs do not cover as many issues as FASB• Board setup

– Too political?– Still too large?– Is it really independent?

• Are constituents biased toward their own national standards?

• Constituents often appear Anti-U.S.

Acceptance of IAS

• Securities and Exchange Commission (SEC) – still requires reconciliation to U.S. GAAP but allows following of IFRS for 3 standards:– IAS 7, IAS 21, IAS 29– SEC Proposal (February 16, 2000)– SEC Proposal (April 21, 2005)

• FASB/IASB Memorandum of Understanding (Norwalk Agreement)– Both pledged to use their best efforts to converge

standards– Coordinate future work programs

SEC Proposal (2/16/00 and 4/21/05)

• The Securities and Exchange Commission (SEC) proposed that foreign companies listing on U.S. stock exchanges be allowed to follow IAS in preparing their financial statements in lieu of using U.S. GAAP.

• Currently there are around 1,230 foreign private issuers from more than 57 countries listing with the SEC.

• What are the implications of this proposal?

Issues for U.S. Proposal

• SEC is proposing IAS (IFRSs) for foreign registrants only; domestic companies must still follow U.S. GAAP

• Should foreign registrants get special privileges?

• Will this cause U.S. companies to be headquartered in a foreign country to take advantage of IFRS rules?

SEC Recent ProposalFirst-time Application of IFRS

• Release 33-8397, March 11, 2004• Permits two year presentation (relief from preparing three

comparative years under IFRS)• Proposal relates to entities that:

– Adopt IFRS on or before 1/1/2007– Comply with all IFRS approved by IASB

• Reconciliation to US GAAP still required but for two years• SEC will evaluate the “quality” of IFRS financial

statements.• SEC Chairman Donaldson gave EU Internal Market

Commissioner a “roadmap” for eliminating the US GAAP reconciliation between now and 2009 at the latest.

Impediments to Convergence

• Resistance to change

• European Economic Union

• Conceptual frameworks?

• No more rigorous than the FASB

• U.S. Congress

Websites

• IASB (www.iasb.org)

• IAS Plus (www.iasplus.com)– Website sponsored by Deloitte– Lists differences between IFRSs and different

country’s GAAP