Internal Revenue Service (IRS) Increases Mileage … Revenue Service (IRS) Increases Mileage Rate to...

16

1 July 2011 TAX ALERTS Contact us at [email protected] Internal Revenue Service (IRS) Increases Mileage Rate to 55.5 Cents per Mile On June 23, 2011, the IRS announced an increase in the optional standard mileage rates for the final six months of 2011. Taxpayers may use the optional standard rates to calculate the deductible costs of operating an automobile for business and other purposes. The rate will increase to 55.5 cents a mile for all business miles driven from July 1, 2011 through December 31, 2011. This is an increase of 4.5 cents from the 51-cent rate in effect for the first six months of 2011, as set forth in Revenue Procedure 2010-51. In recognition of recent gasoline price increases, the IRS made this special adjustment for the final months of 2011. The IRS normally updates the mileage rates once a year in the fall for the next calendar year. "This year's increased gas prices are having a major impact on individual Americans. The IRS is adjusting the standard mileage rates to better reflect the recent increase in gas prices," said IRS Commissioner, Doug Schulman. "We are taking this step so the reimbursement rate will be fair to taxpayers." While gasoline is a significant factor in the mileage figure, other items enter into the calculation of mileage rates, such as depreciation and insurance and other fixed and variable costs. The optional business standard mileage rate is used to compute the deductible costs of operating an automobile for business use in lieu of tracking actual costs. This rate is also used as a benchmark by the federal government and many businesses to reimburse their employees for mileage. The new six-month rate for computing deductible medical or moving expenses will also increase by 4.5 cents to 23.5 cents a mile, up from 19 cents for the first six months of 2011. The rate for providing services for charitable organizations is set by statute, not the IRS, and remains at 14 cents a mile. Taxpayers always have the option of calculating the actual costs of using their vehicles rather than using the standard mileage rates. For more information about this article, please contact us at [email protected] or any of our tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745. www.windes.com Purpose Rates 1/1 through 6/30/11 Rates 7/1 through 12/31/11 Business 51 55.5 Medical/Moving 19 23.5 Charitable 14 14

Transcript of Internal Revenue Service (IRS) Increases Mileage … Revenue Service (IRS) Increases Mileage Rate to...

1

July 2011

TAX ALERTS

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

Internal Revenue Service (IRS) Increases Mileage Rate to 55.5 Cents per Mile

On June 23, 2011, the IRS announced an increase in the optional

standard mileage rates for the final six months of 2011. Taxpayers

may use the optional standard rates to calculate the deductible costs

of operating an automobile for business and other purposes.

The rate will increase to 55.5 cents a mile for all business miles driven

from July 1, 2011 through December 31, 2011. This is an increase of

4.5 cents from the 51-cent rate in effect for the first six months of

2011, as set forth in Revenue Procedure 2010-51. In recognition of

recent gasoline price increases, the IRS made this special adjustment

for the final months of 2011. The IRS normally updates the mileage

rates once a year in the fall for the next calendar year.

"This year's increased gas prices are having a major impact on individual Americans. The IRS is

adjusting the standard mileage rates to better reflect the recent increase in gas prices," said IRS

Commissioner, Doug Schulman. "We are taking this step so the reimbursement rate will be fair to

taxpayers." While gasoline is a significant factor in the mileage figure, other items enter into the

calculation of mileage rates, such as depreciation and insurance and other fixed and variable costs.

The optional business standard mileage rate is used to compute the deductible costs of operating an

automobile for business use in lieu of tracking actual costs. This rate is also used as a benchmark by

the federal government and many businesses to reimburse their employees for mileage.

The new six-month rate for computing deductible medical or moving expenses will also increase by

4.5 cents to 23.5 cents a mile, up from 19 cents for the first six months of 2011. The rate for

providing services for charitable organizations is set by statute, not the IRS, and remains at 14 cents a

mile.

Taxpayers always have the option of calculating the actual costs of using their vehicles rather than

using the standard mileage rates.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

www.windes.com

Purpose Rates 1/1 through 6/30/11 Rates 7/1 through 12/31/11

Business 51 55.5

Medical/Moving 19 23.5

Charitable 14 14

2

Beware of E-Mail Scams about Electronic Federal Tax Payments

Consumers should be aware of a scam e-mail about an electronic

federal tax payment the e-mail claims they tried to make

or which mentions the Electronic Federal Tax Payment System

(EFTPS). The e-mail states that tax payments made by the e-mail

recipient through EFTPS have been rejected. The e-mail then

directs recipients to a bogus link for a transaction report that,

when clicked, downloads malicious software (malware) that

infects the intended victim’s computer. The malware is designed

to send back personal and financial information to the scammer

already contained on the taxpayer's computer or obtained

through capturing keystrokes. The scammer uses this personal

and financial information to commit identity theft.

To avoid malware, the taxpayers should not click on any links, open any attachments, or reply to the

sender for this or any other unsolicited e-mails that they may receive about their tax account that

claims to come from the Internal Revenue Service (IRS) or EFTPS. If the taxpayer responded to this

scam and believes he or she may have become the victim of identity theft, find out what steps can be

taken. The IRS and the Financial Management Service (the Treasury bureau that owns EFTPS) do not

communicate payment information through e-mail. A scam that tricks people into revealing their

personal and financial data is identity theft. A scam that attempts to do this through e-mail is known

as phishing. Find out more about IRS impersonation phishing scams and how to recognize and

report them to the IRS.

EFTPS is a tax payment system that allows individuals and businesses to pay federal taxes

electronically via the Internet or phone. It is committed to taxpayer privacy and uses industry-

leading security practices and technology to protect taxpayer data.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

3

The Internal Revenue Service (IRS) QuickAudit is Getting Quicker

This article is reproduced with permission from Spidell Publishing, Inc.

In fall 2010, the IRS Press Office issued a release explaining how helpful it

was that the IRS would obtain information from the QuickBooks data file

directly, rather than forcing the taxpayers to spend time providing the

needed data, which they may not have possessed the skill set to do. Since

that time, the American Institute of Certified Public Accountants (AICPA)

has become more vocal in their objection to this process. The IRS has

responded to the AICPA and is becoming more aggressive at issuing

information document requests (IDRs) pertaining to QuickBooks.

Information Document Request (IDR)

The IRS is now including a paragraph about QuickBooks and states, "If your

client does not utilize QuickBooks, please have the following available at

the time of our scheduled appointment." Their list includes traditional

items like work papers and other books and records.

The 2011 IDR referencing QuickBooks now includes a three-page document regarding Internal

Revenue Code (IRC) §6001, which substantiates why the IRS is allowed to ask for QuickBooks data

files. It includes Revenue Ruling 71-20 and references IRC of 1954. It is a trip down memory lane,

discussing punch cards and magnetic tapes.

The 2011 QuickBooks paragraph in the IDR asks for an original electronic backup file and it states,

"The copy should not be an altered version of the QuickBooks data… ." In the next sentence, the

IDR states that the "file should include any changes to the data entered after year-end… ." It is

assumed that it meant the IRS wants to have any year-end adjusting journal entries posted into the

file but does not want the file to be modified in any other way.

AICPA letter to the IRS

Patricia A. Thompson, Chair of the AICPA's Tax Executive Committee, sent a letter dated March 29,

2011, to Christopher Wagner, Commissioner of the Small Business/Self-Employed Division of the

IRS. She makes several points in her letter, which will be covered below.

In the Large Business and International Division of the IRS, Thompson notes that a full accounting

system is never turned over to the IRS. The IRS asks for certain information and the taxpayer

provides it. Her comment is that QuickBooks can work in exactly the same manner. She states that

the software file contains information that is not relevant to the tax year issues or issues under audit,

and the file may contain information considered confidential under the law. She believes this is

central to the issue at hand: the IRS audit is usually a limited scope audit, so why should the IRS

require access to all records of all types of the taxpayer for the applicable year? Her letter then

states, "The AICPA believes the taxpayer should have the right to "redact" the software file and turn

over only the data that is responsive and relevant to the examination - but no more." This would be

a huge undertaking for small business, but indicates how varied the opinions are about small business

exams.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

4

IRS QuickAudit is Getting Quicker (continued)

IRS response to the AICPA

On April 20, 2011, Commissioner Wagner responded. The Wagner letter states that, "an exact

copy…be provided to the examiner and not an altered version." This "allows the examiners to

properly consider the integrity and veracity of the … files." In the same paragraph, the QuickBooks

audit trail is discussed without naming it. The paragraph concludes using the phrase, "directly

relevant to the evaluation of the taxpayer's internal controls." The Wagner letter provides

suggestions to the small business under examination:

The taxpayer backs up the "electronic data files" annually. This backup can then

be used by the IRS.

The taxpayer can condense the data other than the period under audit.

The Wagner letter goes on to state that if the examination is expanded, another backup for a

different year will be needed, a backup that does not have condensed data for the next year under

audit. This will happen when the IRS goes to an older year for a second year of examination. This

points out the difficulty in condensing. If the year of audit is 2008, then the taxpayer would condense

through 2007. If the IRS went back to 2007, the taxpayer would not have to take a new backup and

go through the condensing process through 2006.

When the IDR is compared to the IRS letter, the inconsistencies can be seen. A backup at year-end

would not have year-end adjusting journal entries. At least, in 2011, the Wagner letter is asking for a

backup QuickBooks file with a file extension of "QBB," not a working copy with a file extension of

"QBW."

The Wagner letter goes on to address the privacy issue of the IRS getting all of a taxpayer's

accounting system. The letter references IRC §6103 and states the taxpayer's information "is a

matter of the utmost importance to the IRS." While that is the official position of the IRS, it does

not address the misuse of the additional information by the IRS. There are dozens of questions that

can be contemplated pertaining to the IRS possessing the taxpayer's complete file.

Taxpayer's dilemma

It is clear that the subject has not been resolved. The IRS will continue to request QuickBooks data

files, so the small business will have to respond to these requests. Although there has been more

discussion at higher levels, there is no absolute manner to deal with the QuickBooks request. Here

are some alternatives:

1. Provide schedules both in hard copy and in electronic spreadsheet format of all

accounts selected for examination without providing the QuickBooks file. This

is the cleanest and fairest way to provide the IRS with needed information.

2. As soon as the fiscal year-end bank accounts are reconciled, save a copy of the

QuickBooks file in QBW (working copy) format and rename it "Tax Return

Copy - Tax Year 20XX." When the year-end adjustments are received, post

them into this copy as well as the live QuickBooks file the taxpayer is

continuing to use into the new year. If the tax return is selected for the audit,

the data file can be compressed accordingly.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

5

The Internal Revenue Service (IRS) Releases Draft Version of Form 8938 for Foreign Financial Asset Holders

The IRS is seeking comments on the new draft Form 8938, “Statement of Specified Foreign Financial

Assets,” which is available on the IRS's website. Form 8938 will be used by individuals to report an

interest in one or more specified foreign financial assets under the Internal Revenue Code (IRC)

Section 6038D. The form is required to be filed by the taxpayers on or before April 16, 2012 for

the initial year.

Background

For tax years beginning after March 18, 2010, the Hiring Incentives to Restore Employment Act of

2010 (HIRE Act) provides that individuals with an interest in a “specified foreign financial asset”

during the tax year must attach a disclosure statement to their income tax returns for any year in

which the aggregate value of all such assets is greater than $50,000. In addition, to the extent

provided by the IRS in regulations or other guidance, the IRC Section 6038D applies to any domestic

entity formed or availed of for purposes of holding, directly or indirectly, specified foreign financial

assets, in the same manner as though the entity were an individual.

“Specified foreign financial assets” are:

(1) depository or custodial accounts at foreign financial institutions, and

(2) to the extent not held in an account at a financial institution,

(a) stocks or securities issued by foreign persons,

(b) any other financial instrument or contract held for investment that is

issued by, or has, a counterparty that is not a U.S. person, and

(c) any interest in a foreign entity.

IRS QuickAudit is Getting Quicker (continued)

3. If the IRS audit is of a Schedule C taxpayer, the focus is typically on the income

statement. The taxpayer may be able to have reasonably good results with a

compression of the QuickBooks file using QuickBooks tools.

4. If the IRS audit is for a business return and the IRS wants to examine various

balance sheet accounts, such as officer loans or advances, and intercompany

accounts, the taxpayer may want to seek professional assistance in truncating

the QuickBooks file for just the period of the audit.

5. Professional data managers, like in #4 above, can also remove the audit trail of

a QuickBooks file.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

6

IRS Releases Draft Version of Form 8938 (continued)

Recent guidance

In the Notice 2011-55, 2011-29 IRB, the IRS suspended the IRC Section 6038D reporting

requirements until it releases Form 8938. After the new Form 8938 is released in its final form

individuals for whom the filing of Form 8938 was suspended for a tax year will have to attach the

form for the suspended tax year to their next income tax returns required to be filed with IRS.

The Notice 2011-55 further stated that the IRC Section 6501(c)(8) limitations period for tax

assessments for periods for which reporting is required under IRC Section 6038D will not expire

before three years after the date on which the IRS receives Form 8938.

Draft Form

The draft Form 8938 was released on June 22 without instructions. However, the draft form

references the instructions throughout, which indicates that they will likely be issued soon.

Part I of the draft form requires information about foreign deposit and custodial accounts, including

the maximum value of any such account during the tax year. Part II has similar entries for “other

foreign assets,” but notes that specified foreign financial assets that have been otherwise reported on

Forms 3520, 3520-A, 5471, 8621, or 8865, do not have to be included on Form 8938. Part III asks

for a summary of tax items attributable to the accounts and assets reported in Parts I and II, including

associated items such as interest, dividends, and royalties. Part IV requires disclosure of the number

of the filed forms referenced in Part II on which any foreign financial assets that were excepted from

Part II were reported.

Comments on the form must be submitted on the IRS's website within 30 days of the form's June 22

posting date to receive consideration.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

7

Proposed Change to Due Date of Tax Returns

There is a legislative proposal presented to the Internal Revenue Service (IRS)

to change the due dates of various returns (see table below). The proposal

was made because of the problem the tax practitioners have with the late

arriving Schedule K-1 from the partnerships and trusts. If the partnership or

trusts have other Schedules K-1 flowed into their tax returns, their tax

returns cannot be completed and finalized until all the K-1s are received. Due

to the flow of the information from one entity to another, it causes the

delay on the filing process. The IRS has temporarily fixed the problem by

shortening the extension for the partnership and trust returns by one month,

from October 15 to September 15. However, people are still looking for a

better way to fix the problem, which results in the following proposed change

to the various due dates. As of today, this is only a proposal and no one

knows when it will be effective and what will be the final form of the changes.

The information is here to let people be aware of the proposed change.

There is also a bill introduced by a senator to change the due dates of the quarterly estimated tax

payments for corporations in April 2011. There has not been any recent development on this bill

since it is not clear whether this bill will be a revenue loser or gainer. Since the due dates of the

quarterly estimated tax payments are dictated by the due dates of the tax return, if the above change

is implemented, people can expect to see changes in the due dates of the quarterly estimated tax

payments as well.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

CURRENT PROPOSED

Original due

date Extended due

date Original due

date Extended due

date

C Corporation (Form 1120) 3/15 9/15 4/15 10/15

S Corporation (Form 1120S) 3/15 9/15 3/31 9/30

Trust & Estates (Form 1041) 4/15 9/15 4/15 9/30

Partnership (Form 1065) 4/15 9/15 3/15 9/15

Individual (Form 1040) 4/15 10/15 4/15 10/15

Foreign Bank Account Reports (FBAR)

(Form TD F 90-22.1) 6/30 N/A 6/30 10/15

Employee Benefit Plan (Form 5500) 7/31 10/15 7/31 11/15

8

Form 1099-K to Report Merchant Card and Third-Party Network Payments

and Revised Form 1065 for Reporting Payment per

Form 1099-K

Earlier this year, in late February 2011, the Internal Revenue Service (IRS)

released a new Form 1099-K, Merchant Card and Third-Party Payments, and

its instructions, which implement new reporting requirements under the

Regulation Section 1.6050W-1, effective for returns for calendar years

beginning after December 31, 2010. Payment settlement entities may have to

report merchant card payments and third-party network payments on the new

Form 1099-K instead of on Form 1099-MISC.

Background

The “Housing Assistance Tax Act of 2008,” added Internal Revenue Code (IRC) Section 6050W.

After year 2010, it generally requires banks to file an information return with the IRS reporting the

gross amount of credit and debit card payments a merchant receives during the year, along with the

merchant's name, address, and taxpayer identification number (TIN). Similar reporting is also re-

quired for third-party network transactions (e.g., those facilitating online sales).

Specifically, under IRC Section 6050W, any payment settlement entity (PSE) making payment to a

participating payee in settlement of reportable payment transactions (any payment card transaction

and any third-party network transaction) must file a return for each calendar year with the IRS and

furnish a statement to the participating payee, setting out the gross amount of the reportable

payment transactions as well as the name, address, and TIN of the participating payee. A PSE is a

merchant acquiring entity in the case of a payment card transaction and a third-party settlement

organization in the case of a third-party network transaction.

A payment card transaction is any transaction in which a payment card is accepted as payment. A

payment card is defined as any card that is issued pursuant to an agreement or arrangement that

provides for:

(a) one or more issuers of the cards;

(b) a network of persons unrelated to each other and to the issuer, who agree to

accept such cards as payment; and

(c) standards and mechanisms for settling the transactions between the merchant

acquiring entities and the persons who agree to accept the cards as payment.

A third-party network transaction is any transaction that is settled through a third-party payment

network - i.e., generally, an agreement or arrangement that involves the establishment of accounts

with a central organization by a substantial number of persons who are unrelated to the organiza-

tion, provide goods or services, and have agreed to settle transactions for the provision of the goods

or services under the agreement or arrangement. A third-party settlement organization is required

to reort with resect to Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

9

Form 1099-K to Report Merchant Card and Third-Party Network Payments (continued)

to report with respect to third-party network transactions of any participating payee only if

(1) the aggregate amount with respect to the third-party network transactions for the year

that would otherwise be reported exceeds $20,000, and

(2) the aggregate number of the transactions exceeds 200.

Reportable payment transactions subject to information reporting generally are subject to backup

withholding requirements, and failure-to-file penalties apply for noncompliance. Backup withholding

for amounts reportable under IRC Section 6050W applies to amounts paid after December 31, 2011.

In August of 2010, the IRS issued final regulations that provide guidance on the information reporting

requirements, information reporting penalties, and backup withholding requirements for payment

card and third-party network transactions.

New Form 1099-K

The instructions to Form 1099-K provide that every PSE which, in any calendar year, makes one or

more payments in settlement of reportable payment transactions, must file an information return on

Form 1099-K with respect to each participating payee for that calendar year. The instructions

explain that a PSE is a domestic or foreign entity that is a merchant acquiring entity (i.e., a bank or

other organization) that has the contractual obligation to make payments to participating payees in

settlement of payment card transactions, or a third-party settlement organization (i.e., the central

organization that has the contractual obligation to make payments to participating payees of third-

party network transactions). A PSE makes a payment in settlement of a reportable payment

transaction, that is, any payment card or third-party network transaction, if the PSE submits the

instruction to transfer funds to the account of the participating payee to settle the reportable

payment transaction.

If two or more persons qualify as PSEs for the same reportable transaction, the PSE who actually

makes payment must file the return. However, the PSE obligated to file may designate another

person to file the return, including the PSE not making payment, if the parties agree in writing. If the

designated person fails to timely file the return, the party who makes payment is liable for any

applicable penalties under IRC Section 6721 and 6722. If a PSE contracts with an electronic payment

facilitator (EPF) or other third-party payer (TPP) to make payments in settlement of reportable

payment transactions on behalf of the PSE, the facilitator or other third party must file Form 1099-K

in lieu of the PSE.

A PSE enters the gross amount of the total reportable merchant card/third-party network payment

transactions for the calendar year in Box 1 of Form 1099-K. Gross amount means the total dollar

amount of total reportable payment transactions for each participating payee without regard to any

adjustments for credits, cash equivalents, discount amounts, fees, refunded amounts, or any other

amounts. The dollar amount of each transaction is determined on the date of the transaction.

Under IRC Section 6050W(e), a de minimis payment exception applies to a third-party settlement

organization (see discussion above). A PSE enters in Boxes 5a through 5l (which provide a month-by

-month break down) the gross amount of the total reportable payment transactions for each month

of the calendar year. Boxes 2 through 4 are blank, and reserved for future use.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

10

Form 1099-K to Report Merchant Card and Third-Party Network Payments (continued)

The instructions also describe what transactions are not subject to reporting and when a number

of exceptions to the reporting rules apply, including certain payments made by U.S. payers or

middlemen to foreign payees after 2010; payments by U.S. payers to foreign payees prior to 2011;

and payments made by non-U.S. payers or middlemen to foreign payees.

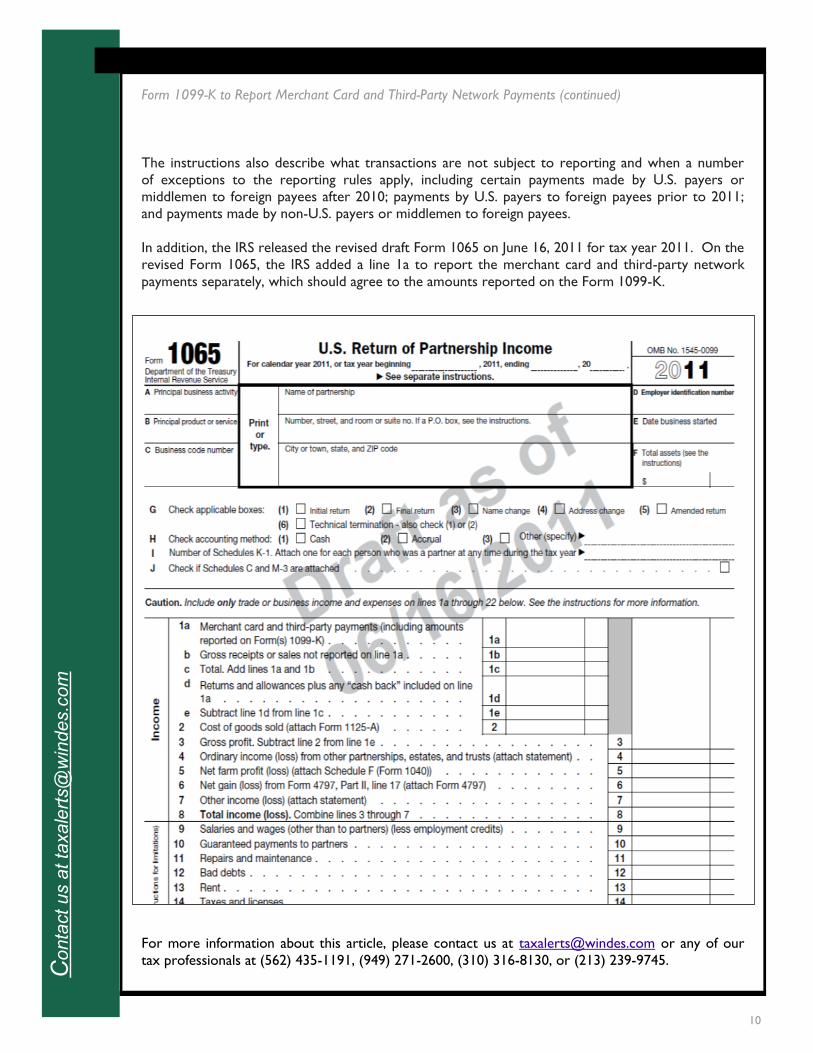

In addition, the IRS released the revised draft Form 1065 on June 16, 2011 for tax year 2011. On the

revised Form 1065, the IRS added a line 1a to report the merchant card and third-party network

payments separately, which should agree to the amounts reported on the Form 1099-K.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

11

California Franchise Tax Board (FTB) Provides Payment Plans and

Offers in Compromise

This article is reproduced with permission from Spidell Publishing, Inc.

If the taxpayers have financial difficulty and cannot pay the taxes owed to the FTB, installment

agreements and offers in compromise are two things that the taxpayers can consider to help them

settle their debts to the FTB.

Installment agreements

If the taxpayers are financially unable to pay the amount owed and cannot borrow from a private

source, they can request to make monthly installment payments. The FTB would like them to pay

the largest amounts they possibly can. Interest and some penalties will continue to accrue until the

balance is paid in full.

Individual installment agreement:

A $20 processing fee will be added to the liability. The approval or denial of the request to make

installment payments is based on the taxpayer's ability to pay and compliance history and is usually

made within 30 to 60 days. The FTB may still file a lien and/or request a financial statement as a

condition to approval. If the request is denied, the taxpayer may request a review within 30 days and

collection action will resume. If the liability is greater than $10,000 and the installment agreement

exceeds 36 months, then the taxpayer will need to certify that he/she has a financial hardship on the

application.

Individual taxpayers may request an installment agreement without providing detailed financial

information if they:

Owe a balance of $25,000 or less;

Agree to pay in 60 months or less; and

Have filed all required personal income tax returns.

Individuals can request an installment agreement online at:

http://www.ftb.ca.gov/online/eIA/Apply_Online.asp

This applies but only if certain conditions are met, such as not having a current wage garnishment or

an existing installment agreement. They can apply online only once in a 12-month period and only

newly assessed liabilities qualify for an online installment agreement. If individuals apply online,

payments must be made by electronic funds withdrawal for at least $25 per month.

If the taxpayers do not meet the requirements for online filing, they can complete and mail FTB 3567

or they can make arrangements by calling the FTB at (800) 689-4776 Monday through Friday from

8am to 5pm.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

12

California FTB Provides Payment Plans and Offers in Compromise (continued)

Business installment agreement:

Businesses may also enter into an installment agreement if they cannot pay the total balance in 90

days due to a financial hardship. The processing fee is $35. The business must file any delinquent tax

returns and complete a financial condition form, and may be required to submit financial documenta-

tion.

The Business may request an arrangement by calling the FTB at (888) 635-0494. The FTB will evalu-

ate whether the account qualifies for an installment arrangement and will specify the amount of pay-

ments and period of time allowed. The FTB can revoke the business's installment arrangement if

new liabilities accrue, payments are dishonored, or the business entity repeatedly fails to make the

installment payments. The FTB may still file a lien and applicable penalties, and fees and interest ac-

crue until the balance is paid.

Offer in Compromise (OIC)

The OIC program is for taxpayers who do not have, and will not have in the foreseeable future, the

money, assets, or means to pay their tax liability. It allows a taxpayer to offer a lesser amount for

payment of a non-disputed final tax liabilities.

The FTB requires taxpayers to establish that the amount offered is the most that they can pay based

on their present assets and income. In addition, the FTB determines whether taxpayers have reason-

able prospects of acquiring additional income or assets that would allow them to satisfy a greater

amount of the liability than the offered amount within a reasonable period (depending on other fac-

tors, five years is usually considered a reasonable period). Furthermore, the FTB must determine

that acceptance of the offer is in the best interest of the State.

The FTB evaluates each case based upon its own unique set of facts and circumstances. Strong con-

sideration is given to present equity in assets, future earning potential, and other considerations such

as age, health, or hardships that could affect future earnings and expenses. This case-by-case ap-

proach gives the FTB the flexibility to appropriately consider all extenuating circumstances to reach a

fair and appropriate decision for the state and the taxpayer.

How to file an OIC

Individuals may use the 4905 PIT or a Multi-Agency Form. Also, the FTB, Board of Equalization

(BOE), and Employment Development Department (EDD) have a single OIC application, Form DE

999CA, Multi-Agency Form for OIC, for individuals. Taxpayers, however, must negotiate each OIC

separately with each agency.

Corporations, partnerships, and limited liability companies must use FTB 4905 BE. No payment is

made with the application. Mail the completed and signed application along with all required docu-

mentation to:

Offer in Compromise Group A453

Franchise Tax Board

P.O. Box 2966

Sacramento, CA 95812-2966

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

13

California FTB Provides Payment Plans and Offers in Compromise (continued)

Offers are reviewed by the FTB within 10 business days of receipt. The taxpayer receives an

acknowledgment letter indicating whether the offer is accepted for processing or rejected. Those

offers accepted for further processing will be assigned to an OIC specialist within 90 days. The OIC

specialist will generally make a determination within 120 days after assignment, although some cases

may take longer if they are unusually complex. The FTB executive officer and chief counsel, jointly,

or their delegates, may approve a compromise for any final tax liability in which the reduction of tax

is $7,500 or less. Reductions above require review by the three-member FTB.

Differences from IRS offers

One of the biggest differences is that the FTB may require the taxpayer to enter into a collateral

agreement (generally for five years), which requires the taxpayer to pay the FTB a percentage of

future earnings that exceed an agreed-upon amount.

This difference, however, may mean that the FTB will be more willing to compromise a liability today

because it is preserving the possibility of collecting additional amounts in the future; whereas, the IRS

would need to permanently write off the amount. A collateral agreement is generally not required if

a taxpayer is on a fixed income or has limited likelihood of increased earnings.

Unlike the IRS, the FTB does not require a nonrefundable payment when making an OIC. The FTB

also does not allow a taxpayer to pay the offered amount in installment payments. The full amount

of the offer must be paid when the offer is accepted.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

FTB OIC Status

The FTB's current acceptance rate is 25.8%

The average accepted offer amount represents approximately 24% of the total liability

and approximately 104% of the original tax amount, including previous credits.

While there is no age limitation for who can submit an OIC, the average age of

taxpayers receiving approval is 57.

The FTB requests a collateral agreement in about 20% of the OICs it approves. Over

the past five years, collateral agreements have collected an annual average of $422,000.

14

Sales Tax Compliance Visits

This article is reproduced with permission from Spidell Publishing, Inc.

Businesses in 19 ZIP codes have received notification since January 1, 2011 of upcoming visits from

Board of Equalization (BOE) specialists as part of the ongoing Statewide Compliance and Outreach

Program (SCOP). If a business is not registered with the BOE, the business will not receive a letter

but it may be subject to a visit.

At their visit, BOE specialists will:

Ask to see the business' licenses;

Check that a seller's permit is displayed (if required); and

Determine whether there are any other licenses or permits needed

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

Zip codes with upcoming SCOP visits

The zip codes below have received notices since January 1 of upcoming visits.

90028 Los Angeles 91502 Burbank 94901 San Rafael

90029 Los Angeles 91746 La Puente 95014 Cupertino

90280 Southgate 92009 Carlsbad 95051 Santa Clara

90638 La Mirada 92056 Oceanside 95054 Santa Clara

90660 Pico Rivera 92260 Palm Desert 95630 Folsom

90701 Artesia 92801 Anaheim 95661 Roseville

90712 Lakewood 92802 Anaheim 95677 Rocklin

90713 Lakewood 93063 Simi Valley 95678 Roseville

91335 Reseda 93065 Simi Valley 95746 Granite Bay

91351 Canyon Country 93103 Santa Barbara 95747 Roseville

91352 Sun Valley 93105 Santa Barbara 95835 Sacramento

91364 Woodland Hills 94080 South San Francisco 95838 Sacramento

91403 Sherman Oaks 94501 Alameda 95841 Sacramento

15

Withholding on Payments from the Government Delayed

This article is reproduced with permission from Spidell Publishing, Inc.

Federal, state, and local governments must withhold federal income tax at the rate of 3% from

payments for goods or services made on or after January 1, 2013. Therefore, if a business is

providing goods or services to California or a local agency, such as a city or county, federal

withholding will be subtracted from certain payments. The withholding requirement was originally

scheduled to take effect January 1, 2012, but the final regulations that were recently released

postponed the start for one year.

The withholding requirement

Withholding will be required on all single payments equal to or greater than $10,000 to individuals,

trusts, estates, partnerships, associations, and corporations. Payments may not be divided into

separate payments of less than $10,000 in order to avoid the withholding requirement, and

withholding is required at the time of payment.

The following payments are not subject to the new withholding requirement:

1. Payments otherwise subject to withholding, such as wages;

2. Payments for retirement benefits or unemployment compensation;

3. Payments subject to backup withholding, if the required backup withholding is actually

performed;

4. Payments for real property;

5. Payments of interest;

6. Payments to other government entities, foreign governments, tax exempt organizations,

or Indian tribes;

7. Public assistance payments made on the basis of need or income. However, assistance

programs based solely on age, such as Medicare, are subject to the requirements;

8. Payments to employees in connection with services, such as retirement plan contributions,

fringe benefits, and expense reimbursements under an accountable plan;

9. Payments received by nonresident aliens and foreign corporations; or

10. Payments in emergency or disaster situations.

The withholding requirement applies to all forms of payment. However, for payment card

transactions, the Internal Revenue Service (IRS) has stated that the withholding requirement will not

apply until further guidance is issued by the IRS, and will not be in effect until 18 months after the

guidance is issued. Payment cards include credit cards, debit cards, stored value cards (gift cards),

and other payment cards.

For more information about this article, please contact us at [email protected] or any of our

tax professionals at (562) 435-1191, (949) 271-2600, (310) 316-8130, or (213) 239-9745.

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

16

Co

nta

ct u

s a

t ta

xa

lert

s@

win

des.c

om

Visit us online at: www.windes.com

Windes & McClaughry is a recognized leader in the field of accounting, assurance, tax, and business consulting services.

Our goal is to exceed your expectations by providing timely, high-quality, and personalized service that is directed at

improving your bottom-line results. Quality and value-added solutions from your accounting firm are essential steps

toward success in today’s marketplace. You can depend on Windes & McClaughry to deliver exceptional client service in

each engagement. For over eighty-five years, we have gone beyond traditional services to provide proactive solutions and

the highest level of capabilities and experience.

Windes & McClaughry’s team approach allows you to benefit from a breadth of technical expertise and extensive

resources. We service a broad range of clients, from high-net-worth individuals and exempt organizations to privately held

businesses and publicly traded companies. We act as business advisors, working with you to set strategies, maximize

efficiencies, minimize taxes, and take your business to the next level.

Orange County Office

18201 Von Karman Avenue

Suite 1060

Irvine, CA 92612

Tel: (949) 271-2600

Headquarters

111 West Ocean Boulevard

Twenty-Second Floor

Long Beach, CA 90802

Tel: (562) 435-1191

South Bay Office

21515 Hawthorne Boulevard

Suite 840

Torrance, CA 90503

Tel: (310) 316-8130

Los Angeles Office

601 South Figueroa Street

Suite 4950

Los Angeles, CA 90017

Tel: (213) 239-9745