INTERNAL CONTROLS, SYSTEMS AND PROCEDURESintranet.sefa.org.za/Content/Docs/Systems and Procedures -...

125

INTERNAL CONTROLS, SYSTEMS AND PROCEDURES DIRECT LENDING – DUE DILIGENCE

Transcript of INTERNAL CONTROLS, SYSTEMS AND PROCEDURESintranet.sefa.org.za/Content/Docs/Systems and Procedures -...

INTERNAL CONTROLS, SYSTEMS AND PROCEDURES

DIRECT LENDING – DUE DILIGENCE

1

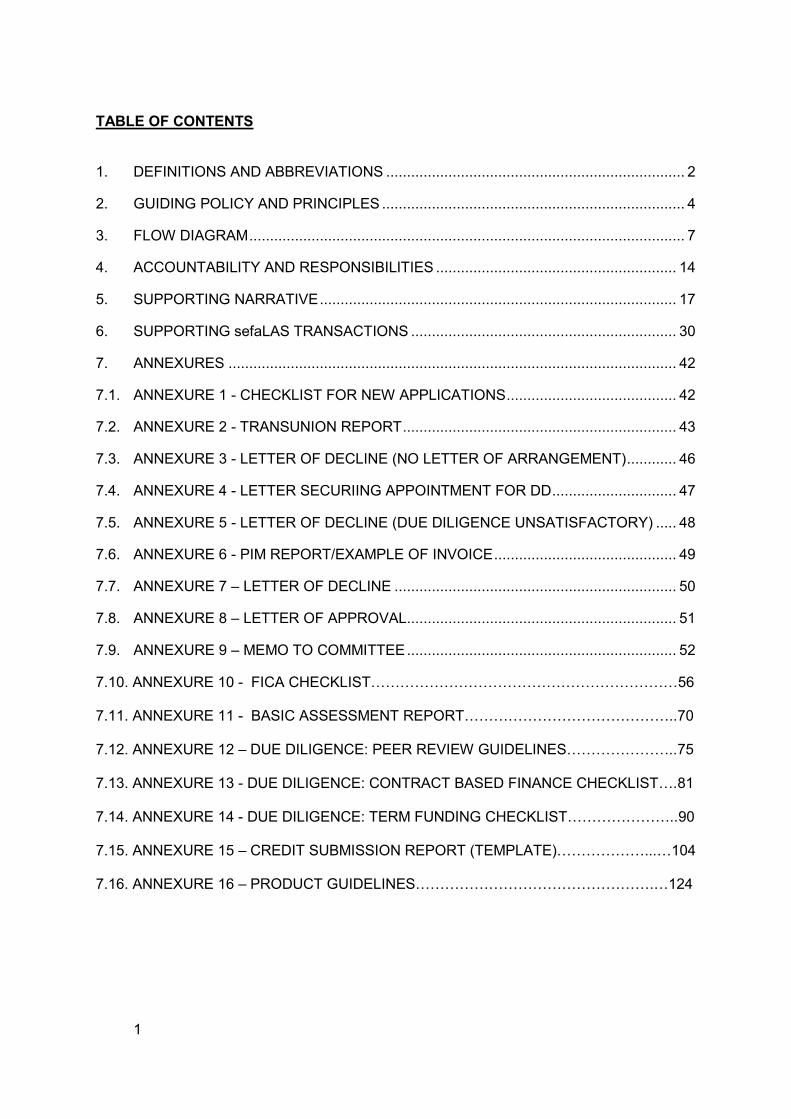

TABLE OF CONTENTS

1. DEFINITIONS AND ABBREVIATIONS ........................................................................ 2

2. GUIDING POLICY AND PRINCIPLES ......................................................................... 4

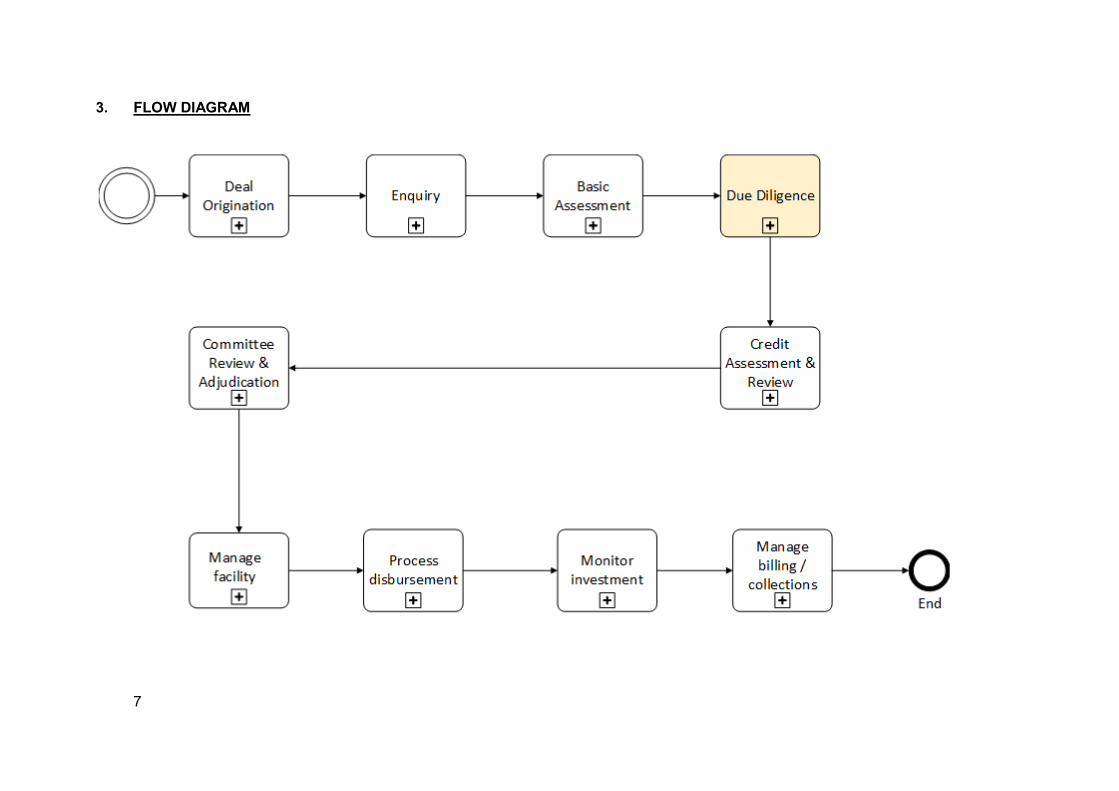

3. FLOW DIAGRAM ......................................................................................................... 7

4. ACCOUNTABILITY AND RESPONSIBILITIES .......................................................... 14

5. SUPPORTING NARRATIVE ...................................................................................... 17

6. SUPPORTING sefaLAS TRANSACTIONS ................................................................ 30

7. ANNEXURES ............................................................................................................ 42

7.1. ANNEXURE 1 - CHECKLIST FOR NEW APPLICATIONS ......................................... 42

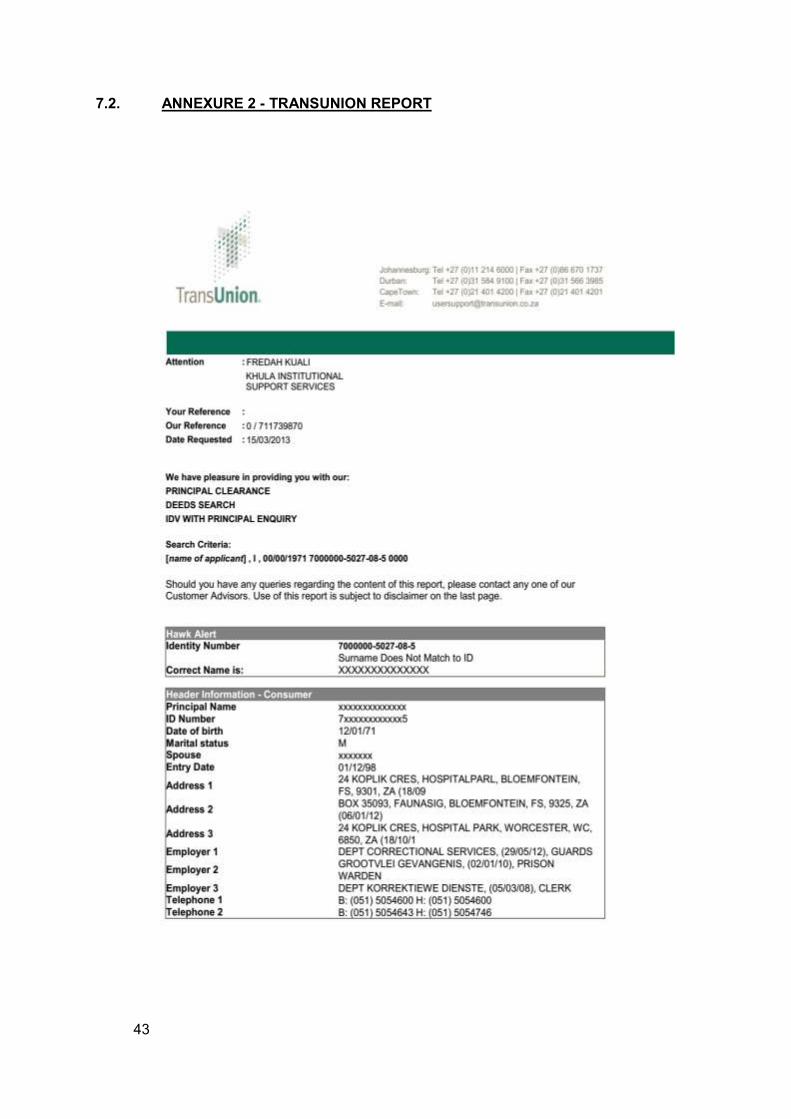

7.2. ANNEXURE 2 - TRANSUNION REPORT .................................................................. 43

7.3. ANNEXURE 3 - LETTER OF DECLINE (NO LETTER OF ARRANGEMENT) ............ 46

7.4. ANNEXURE 4 - LETTER SECURIING APPOINTMENT FOR DD .............................. 47

7.5. ANNEXURE 5 - LETTER OF DECLINE (DUE DILIGENCE UNSATISFACTORY) ..... 48

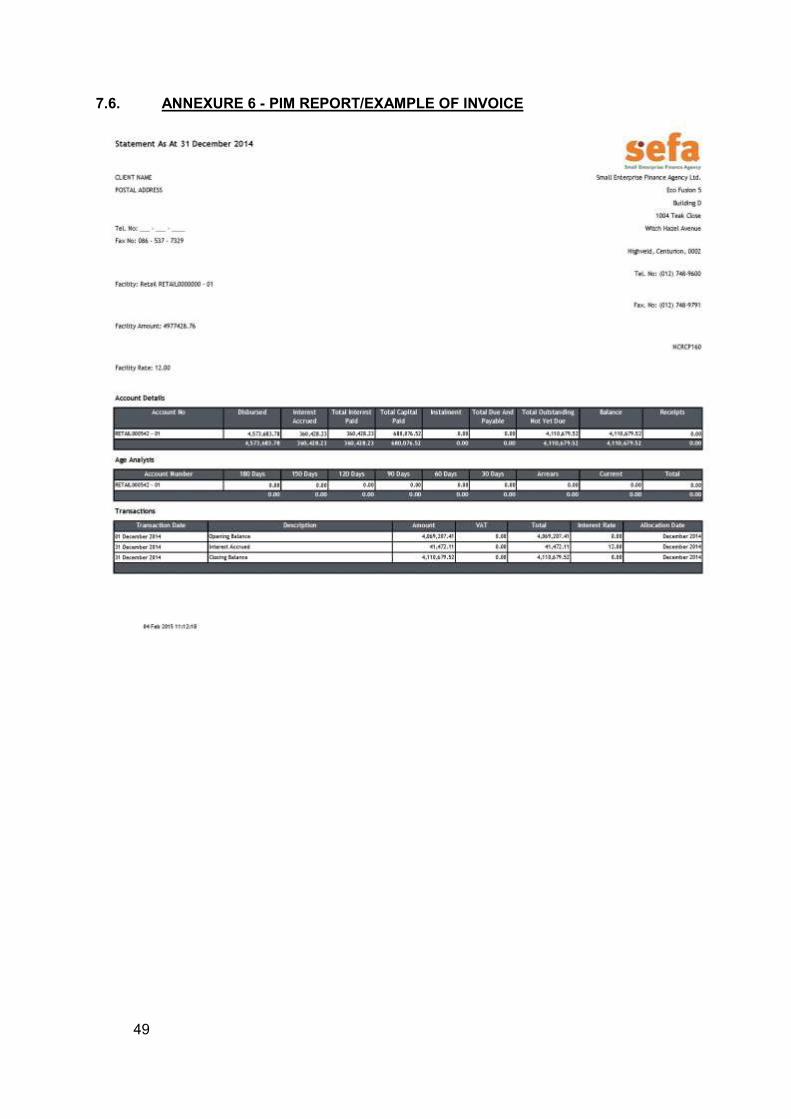

7.6. ANNEXURE 6 - PIM REPORT/EXAMPLE OF INVOICE ............................................ 49

7.7. ANNEXURE 7 – LETTER OF DECLINE .................................................................... 50

7.8. ANNEXURE 8 – LETTER OF APPROVAL................................................................. 51

7.9. ANNEXURE 9 – MEMO TO COMMITTEE ................................................................. 52

7.10. ANNEXURE 10 - FICA CHECKLIST………………………………………………………56

7.11. ANNEXURE 11 - BASIC ASSESSMENT REPORT……………………………………..70

7.12. ANNEXURE 12 – DUE DILIGENCE: PEER REVIEW GUIDELINES…………………..75

7.13. ANNEXURE 13 - DUE DILIGENCE: CONTRACT BASED FINANCE CHECKLIST….81

7.14. ANNEXURE 14 - DUE DILIGENCE: TERM FUNDING CHECKLIST…………………..90

7.15. ANNEXURE 15 – CREDIT SUBMISSION REPORT (TEMPLATE)………………...…104

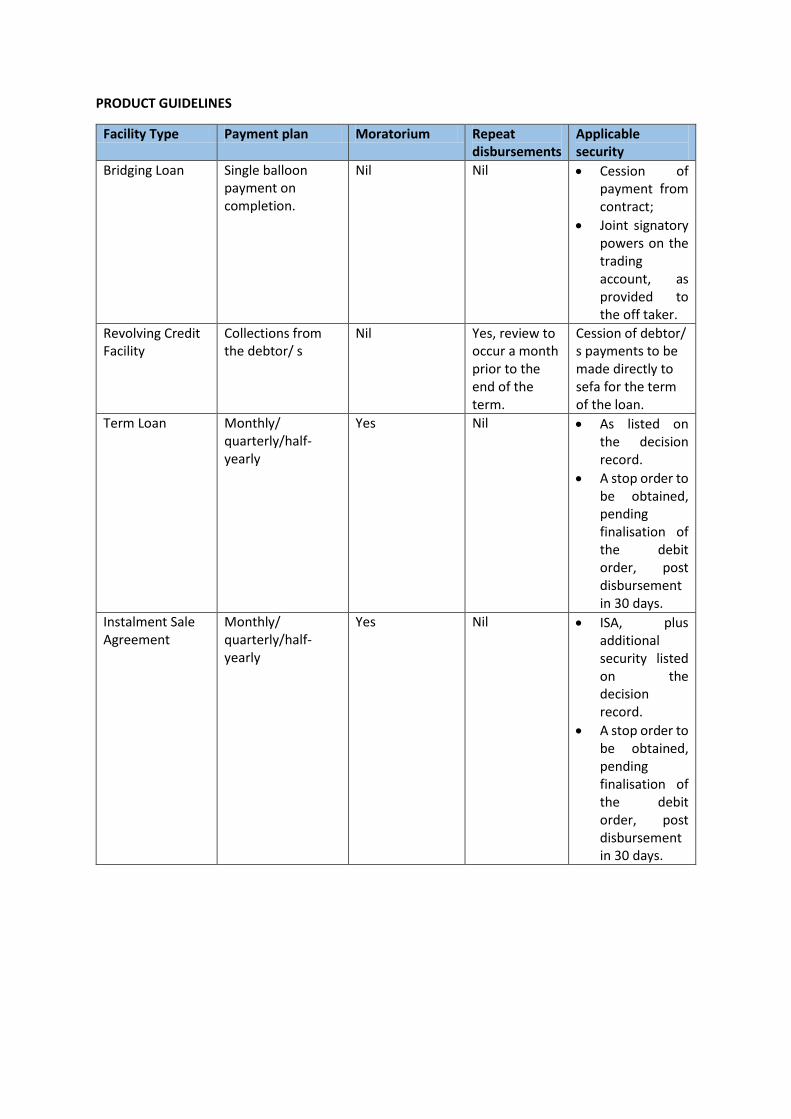

7.16. ANNEXURE 16 – PRODUCT GUIDELINES………………………………………….…124

2

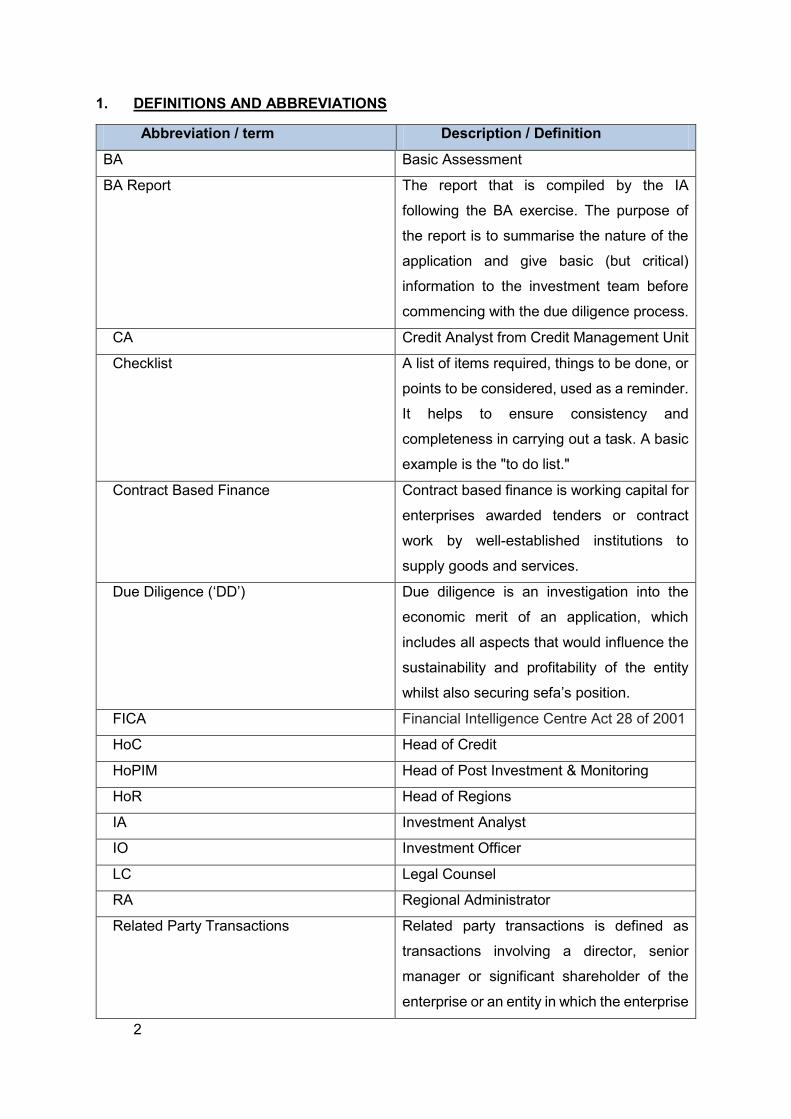

1. DEFINITIONS AND ABBREVIATIONS

Abbreviation / term Description / Definition BA Basic Assessment

BA Report The report that is compiled by the IA

following the BA exercise. The purpose of

the report is to summarise the nature of the

application and give basic (but critical)

information to the investment team before

commencing with the due diligence process.

CA Credit Analyst from Credit Management Unit

Checklist A list of items required, things to be done, or

points to be considered, used as a reminder.

It helps to ensure consistency and

completeness in carrying out a task. A basic

example is the "to do list."

Contract Based Finance Contract based finance is working capital for

enterprises awarded tenders or contract

work by well-established institutions to

supply goods and services.

Due Diligence (‘DD’) Due diligence is an investigation into the

economic merit of an application, which

includes all aspects that would influence the

sustainability and profitability of the entity

whilst also securing sefa’s position.

FICA Financial Intelligence Centre Act 28 of 2001

HoC Head of Credit

HoPIM Head of Post Investment & Monitoring

HoR Head of Regions

IA Investment Analyst

IO Investment Officer

LC Legal Counsel

RA Regional Administrator

Related Party Transactions Related party transactions is defined as

transactions involving a director, senior

manager or significant shareholder of the

enterprise or an entity in which the enterprise

3

has a significant shareholding, as well as a

connected person of any of the

aforementioned persons.

RM Regional Manager

sefaLAS sefa – Loan Administration System

Term Funding Term funding will comprise instalment sale;

revolving credit and term loans.

4

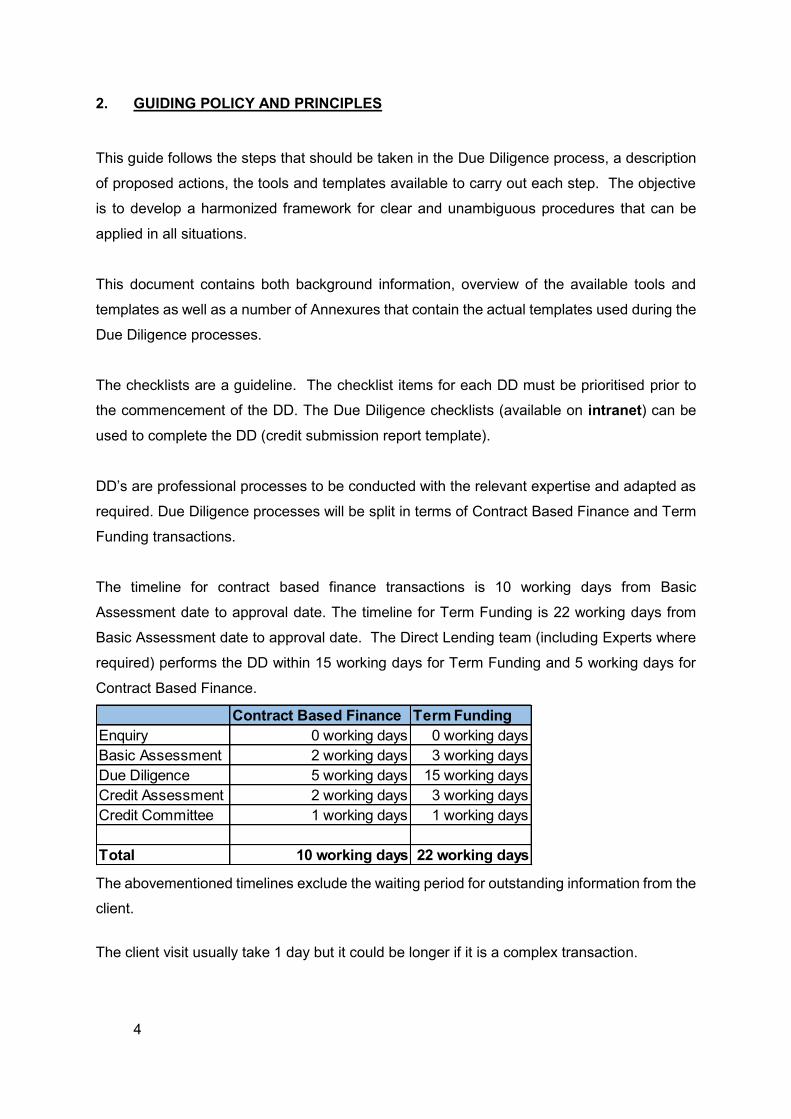

2. GUIDING POLICY AND PRINCIPLES

This guide follows the steps that should be taken in the Due Diligence process, a description

of proposed actions, the tools and templates available to carry out each step. The objective

is to develop a harmonized framework for clear and unambiguous procedures that can be

applied in all situations.

This document contains both background information, overview of the available tools and

templates as well as a number of Annexures that contain the actual templates used during the

Due Diligence processes.

The checklists are a guideline. The checklist items for each DD must be prioritised prior to

the commencement of the DD. The Due Diligence checklists (available on intranet) can be

used to complete the DD (credit submission report template).

DD’s are professional processes to be conducted with the relevant expertise and adapted as

required. Due Diligence processes will be split in terms of Contract Based Finance and Term

Funding transactions.

The timeline for contract based finance transactions is 10 working days from Basic

Assessment date to approval date. The timeline for Term Funding is 22 working days from

Basic Assessment date to approval date. The Direct Lending team (including Experts where

required) performs the DD within 15 working days for Term Funding and 5 working days for

Contract Based Finance.

The abovementioned timelines exclude the waiting period for outstanding information from the

client.

The client visit usually take 1 day but it could be longer if it is a complex transaction.

Contract Based Finance Term Funding Enquiry 0 working days 0 working daysBasic Assessment 2 working days 3 working daysDue Diligence 5 working days 15 working daysCredit Assessment 2 working days 3 working daysCredit Committee 1 working days 1 working days

Total 10 working days 22 working days

5

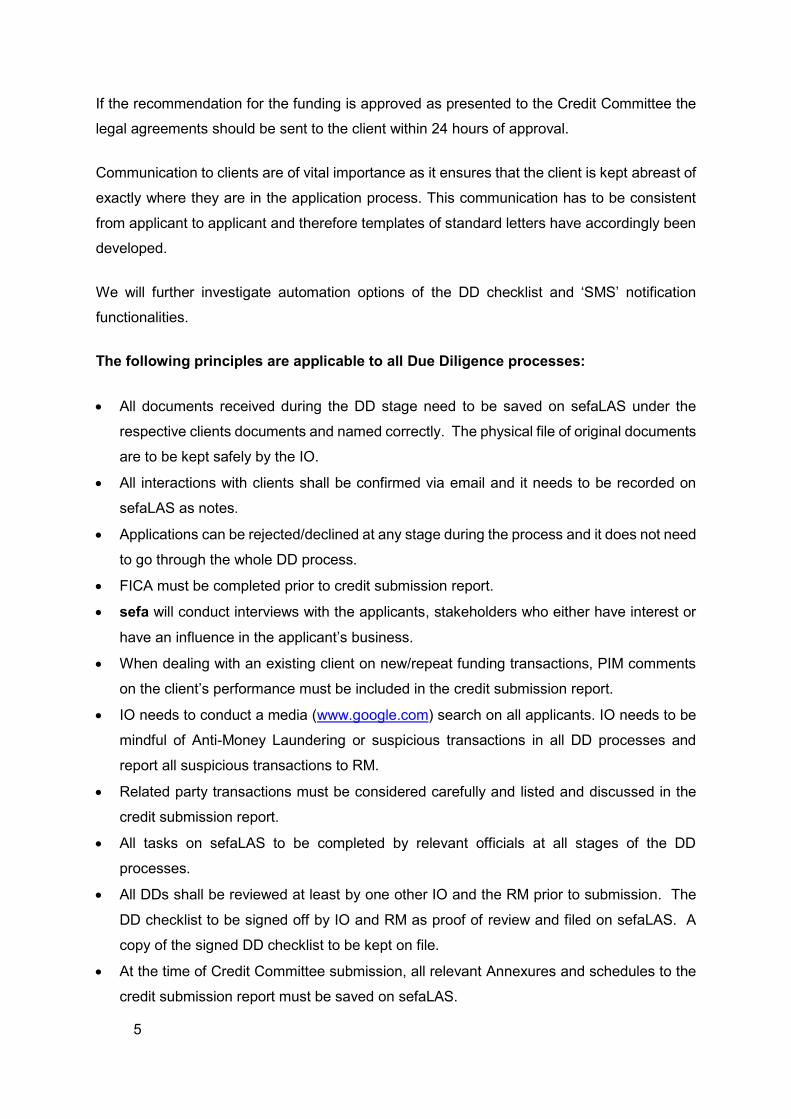

If the recommendation for the funding is approved as presented to the Credit Committee the

legal agreements should be sent to the client within 24 hours of approval.

Communication to clients are of vital importance as it ensures that the client is kept abreast of

exactly where they are in the application process. This communication has to be consistent

from applicant to applicant and therefore templates of standard letters have accordingly been

developed.

We will further investigate automation options of the DD checklist and ‘SMS’ notification

functionalities.

The following principles are applicable to all Due Diligence processes:

All documents received during the DD stage need to be saved on sefaLAS under the

respective clients documents and named correctly. The physical file of original documents

are to be kept safely by the IO.

All interactions with clients shall be confirmed via email and it needs to be recorded on

sefaLAS as notes.

Applications can be rejected/declined at any stage during the process and it does not need

to go through the whole DD process.

FICA must be completed prior to credit submission report.

sefa will conduct interviews with the applicants, stakeholders who either have interest or

have an influence in the applicant’s business.

When dealing with an existing client on new/repeat funding transactions, PIM comments

on the client’s performance must be included in the credit submission report.

IO needs to conduct a media (www.google.com) search on all applicants. IO needs to be

mindful of Anti-Money Laundering or suspicious transactions in all DD processes and

report all suspicious transactions to RM.

Related party transactions must be considered carefully and listed and discussed in the

credit submission report.

All tasks on sefaLAS to be completed by relevant officials at all stages of the DD

processes.

All DDs shall be reviewed at least by one other IO and the RM prior to submission. The

DD checklist to be signed off by IO and RM as proof of review and filed on sefaLAS. A

copy of the signed DD checklist to be kept on file.

At the time of Credit Committee submission, all relevant Annexures and schedules to the

credit submission report must be saved on sefaLAS.

6

sefaLAS needs to be updated with the credit submission report.

The final version of the Excel financial model must be saved on sefaLAS.

When submitting a credit submission report with financials, the actual balance

sheet/income statement and notes must be on separate pages as Annexures. Where

available, all applications should include main page(s) of the Balance Sheet, Income

Statement and Cash Flow Statement.

Requests for information to clients need to be in writing with a cut-off date. The default cut-

off period should be ten (10) working days. If no information is provided before the cut-off

date then the client needs to be informed in writing that his application has been closed,

but he/she is welcome to re-apply in future once the information is available.

The effective dates of the cut-off period will communicated to the client. Five (5) days prior

to the lapse of the cut-off period the client will be reminded in writing in the event that no

response had been received with respect to any request made.

The DD checklist will be used a tool to complete the DD process and for the purposes of

the credit submission report, to guide the officials to successfully conduct the DD

processes.

The RM and IO can agree to exclude certain items, if not applicable, from the DD checklist.

This needs to be signed off by both parties and uploaded on sefaLAS.

Role of Head of Regions

The role of Head of Regions insofar as the due diligence processes will amongst others be as

follows:

To provide assistance on complex transactions and sign them off.

One of the Head of Regions (alternate week) will sit at the committee and identify area(s)

of intervention in terms of quality improvements, policy direction, policy interpretation,

feedback to the Regions on committee proceedings, etc.

To monitor overall turnaround times.

To be involved in deal origination.

To be involved in the negotiation of complex transactions.

7

3. FLOW DIAGRAM

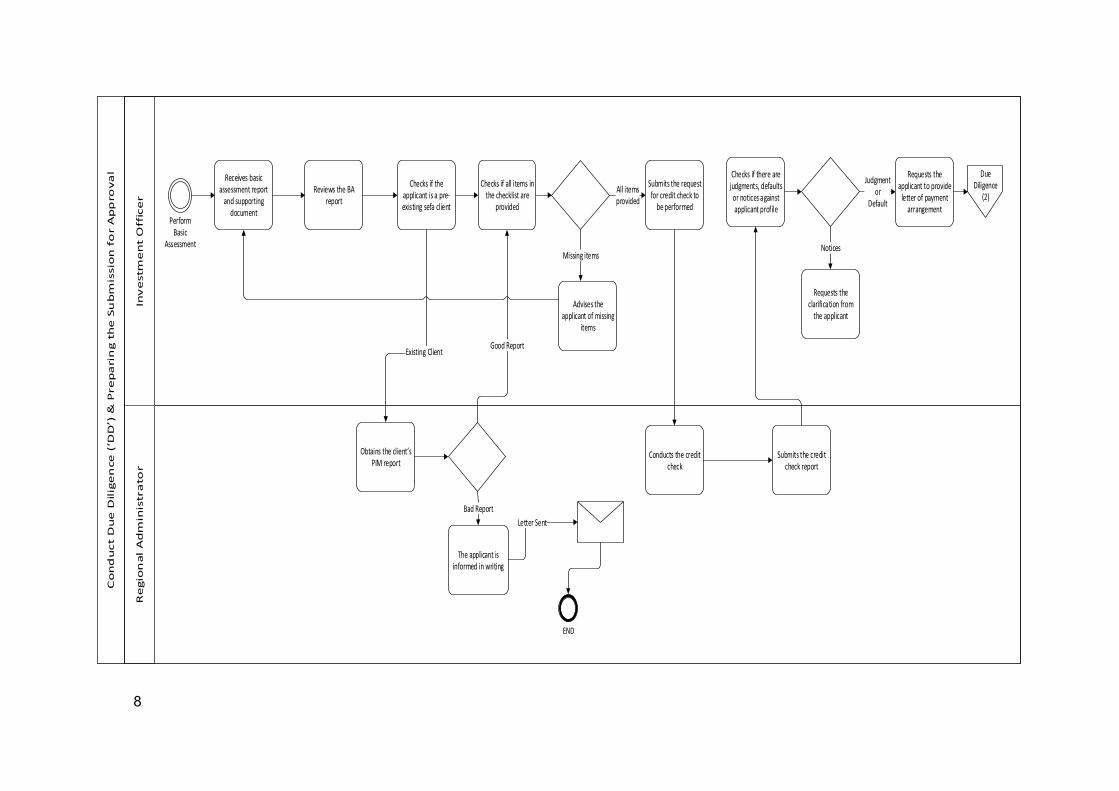

8

Co

nd

uct

Du

e D

ilig

en

ce

( D

D )

& P

re

pa

rin

g t

he

Su

bm

issio

n f

or

Ap

pro

va

l

Inv

estm

en

t O

ffic

er

Re

gio

nal

Ad

min

istr

ato

r

Perform Basic

Assessment

Receives basic assessment report

and supporting document

Reviews the BA report

Checks if all items in the checklist are

provided

All itemsprovided

Submits the request for credit check to

be performed

Missing items

Advises the applicant of missing

items

Conducts the credit check

Submits the credit check report

Checks if there are judgments, defaults or notices against applicant profile

Judgment or

Default

Requests the applicant to provide

letter of payment arrangement

Notices

Requests the clarification from

the applicant

Due Diligence

(2)

Checks if the applicant is a pre-existing sefa client

Obtains the client s PIM report

The applicant is informed in writing

END

Existing Client

Bad Report

Good Report

Letter Sent

9

Co

nd

uct

Du

e D

ilig

en

ce (

DD

) &

Pre

pa

rin

g t

he

Su

bm

issi

on

fo

r A

pp

rova

l

Inv

est

me

nt

Off

ice

rR

egio

nal

Ad

min

istr

ato

rIn

ve

stm

en

t A

naly

st

Letter provided

Checks if the applicant honoured

the arrangement

No letter provided

Application declined

Sends the applicant letter of decline

More than 1 month

Checks the date at which arrangement letter was sent or

acknowledged

Less than 1 month

Not honoured

The Applicant is informed in writing

HonouredSubmits the request

for FICA verifications

Conducts the FICA verifications on the

applicant

Signs off FICA verifications

document and checklist

Provides verifications

document and checklist

Due Diligence

(1)

Due Diligence

(3)

Letter of Decline

10

Cond

uct D

ue D

ilige

nce

( DD

) &

Pre

parin

g th

e Su

bmis

sion

for A

ppro

val

Inve

stm

ent O

ffic

erRe

gion

al

Adm

inist

rato

rIn

vest

men

t An

alys

tRe

gion

al

Man

ager

Hea

d: R

egio

ns

Checks if the applicant is a

politically exposed person (PEP)

PEPapplicant

Notify the Regional Manager and Head

of Regions

Non-PEPapplicant

Invite experts in the field/industry (if

deemed necessary)

Completes the PEP Form

Sends the completed form to

the Head of Regions

Sends to the relevant approval

committee

PEP successfully noted

Arranges for site visit

Arrange for client to visit sefa offices or arrange to visit the intended business

premises

Reviews business plan, historical and/

or projected financials

Due Diligence

(2)

Due Diligence

(4)Conduct client introduction

Prepares Financial Model

11

Cond

uct D

ue D

iligen

ce (

DD )

& Pr

epar

ing t

he Su

bmiss

ion

for A

ppro

val

Inve

stmen

t Offi

cer

Regio

nal

Adm

inist

rato

rIn

vestm

ent

Analy

stRe

giona

l M

anag

erHe

ad: R

egio

nsLe

gal A

dviso

r

Checks the type of required financing (as indicated in the application form)

Contract Based Finance

Performs due diligence in line with

contract financing checklist

Term Funding

Performs due diligence in line with

term funding checklist

Prepares notes/questions for due diligence session

No missinginfo

Checks if there is critical information

that is missing

Requests information in

writing

Info provided

Receives the requested

information

Info notprovided

The applicant is notified in writing

Sends the legal documents for

vetting

Vets the legal documents

Provides the legal report

Receives legal report and reviews

it

Visits the site or meets with the

client

Signs off the due diligence checklist

and sends to RM for sign off

Due Diligence

(3)

Due Diligence

(5)

Invites the expert in the field/industry (if deemed necessary)

END

Letter of Decline

12

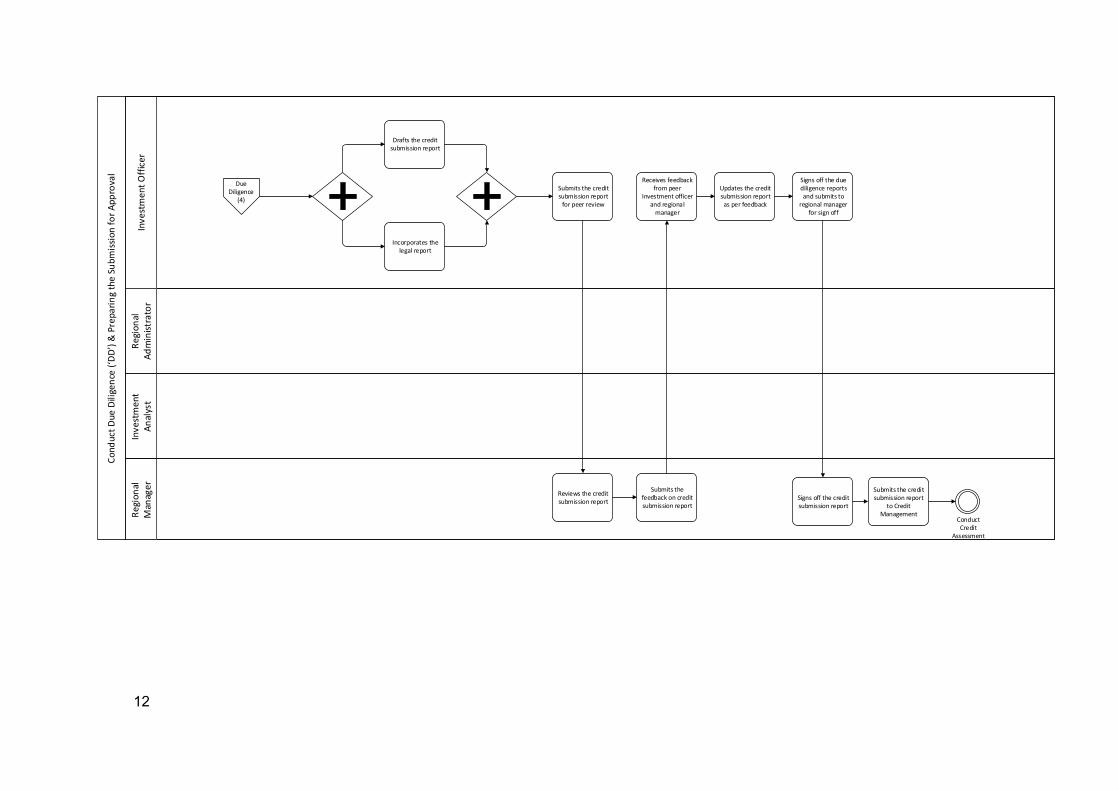

Con

duc

t D

ue D

ilige

nce

( D

D )

& P

rep

arin

g th

e Su

bmis

sion

for

App

rova

l

Inve

stm

ent

Off

icer

Reg

ion

al

Ad

min

istr

ato

rIn

vest

men

t A

nal

yst

Reg

ion

al

Man

ager

Drafts the credit submission report

Incorporates the legal report

Submits the credit submission report

for peer review

Reviews the credit submission report

Submits the feedback on credit submission report

Receives feedback from peer

Investment officer and regional

manager

Updates the credit submission report

as per feedback

Signs off the due diligence reports and submits to

regional manager for sign off

Signs off the credit submission report

Conduct Credit

Assessment

Submits the credit submission report

to Credit Management

Due Diligence

(4)

13

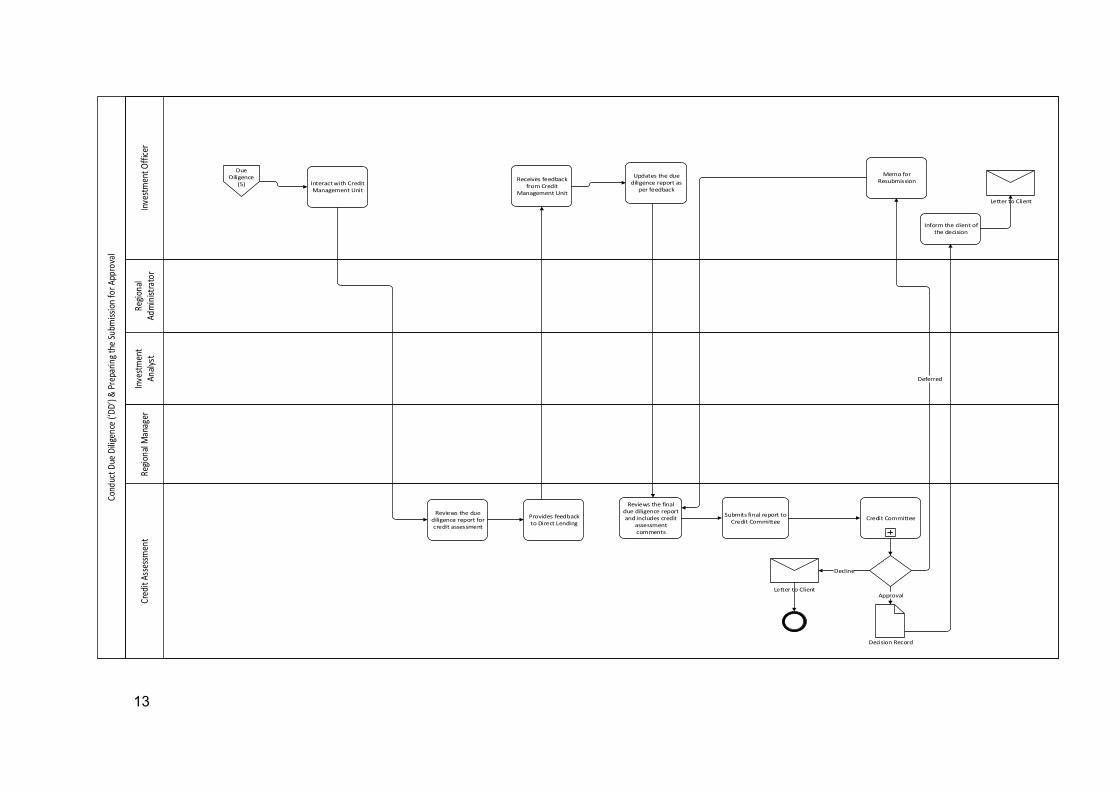

Cond

uct D

ue D

ilige

nce

( DD

) &

Pre

parin

g th

e Su

bmis

sion

for A

ppro

val

Inve

stm

ent O

ffic

erRe

gion

al

Adm

inist

rato

rIn

vest

men

t An

alys

tRe

gion

al M

anag

erCr

edit

Ass

essm

ent

Interact with Credit Management Unit

Receives feedback from Credit

Management Unit

Updates the due diligence report as

per feedback

Due Diligence

(5)

Memo for Resubmission

Deferred

Inform the client of the decision

Letter to Client

Reviews the final due diligence report and includes credit

assessment comments

Reviews the due diligence report for credit assessment

Provides feedback to Direct Lending

Submits final report to Credit Committee

Credit Committee

Decision Record

ApprovalLetter to Client

Decline

14

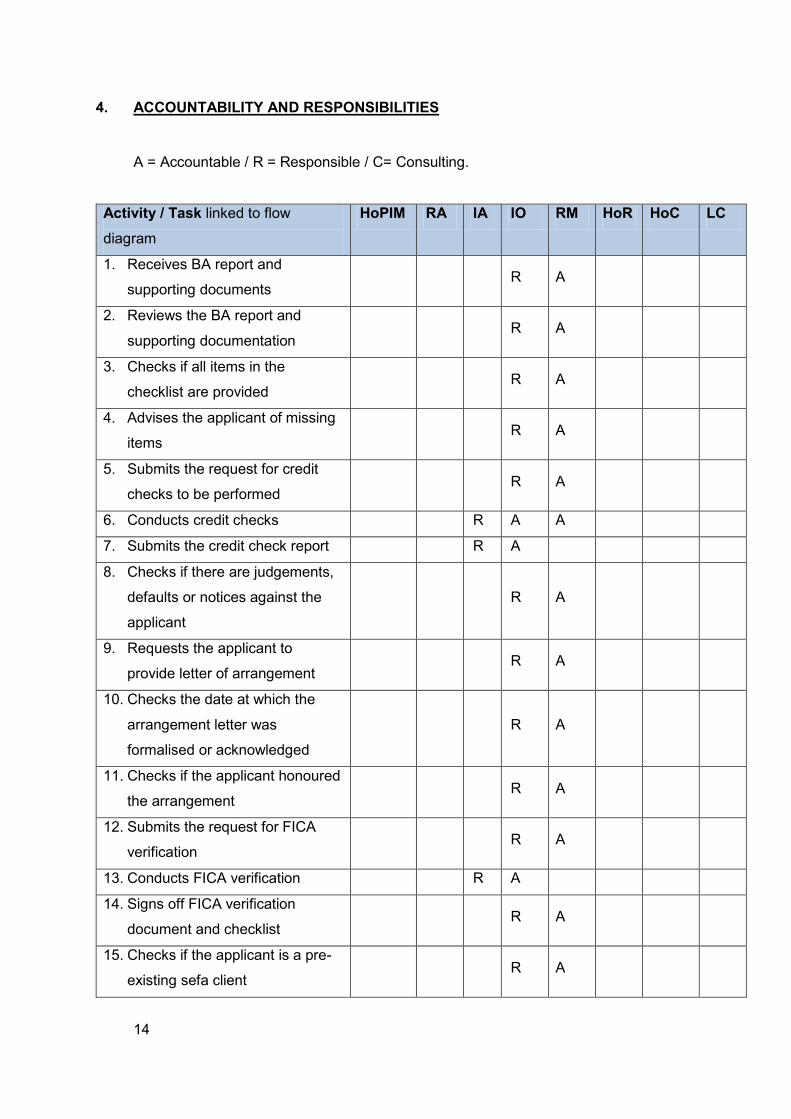

4. ACCOUNTABILITY AND RESPONSIBILITIES

A = Accountable / R = Responsible / C= Consulting.

Activity / Task linked to flow

diagram HoPIM RA IA IO RM HoR HoC LC

1. Receives BA report and

supporting documents R A

2. Reviews the BA report and

supporting documentation R A

3. Checks if all items in the

checklist are provided R A

4. Advises the applicant of missing

items R A

5. Submits the request for credit

checks to be performed R A

6. Conducts credit checks R A A

7. Submits the credit check report R A

8. Checks if there are judgements,

defaults or notices against the

applicant

R A

9. Requests the applicant to

provide letter of arrangement R A

10. Checks the date at which the

arrangement letter was

formalised or acknowledged

R A

11. Checks if the applicant honoured

the arrangement R A

12. Submits the request for FICA

verification R A

13. Conducts FICA verification R A

14. Signs off FICA verification

document and checklist R A

15. Checks if the applicant is a pre-

existing sefa client R A

15

Activity / Task linked to flow

diagram HoPIM RA IA IO RM HoR HoC LC

16. Obtains a PIM report C R A

17. Checks if the applicant is a

Politically Exposed Person

(“PEP”)

R A C

18. Invites experts in the

field/industry (if deemed

necessary)

R A

19. Reviews the business plan,

historical and/or projected

financials

R A

20. Prepares financial model R A

21. Conduct client introduction R A

22. Arranges for site visit R A

23. Checks the type of required

financing R A

24. Performs due diligence in line

with checklist R A

25. Checks if there is critical

information outstanding R A

26. Requests outstanding

information from the applicant in

writing

R A

27. Prepares notes/questions for due

diligence session R A

28. Sends legal documents for

vetting R A C

29. Visits the site or meets with the

applicant R A

30. Sign-off of the Due Diligence

checklist R A

31. Draft credit submission report R A

32. Submits the credit submission

report for Peer Review R A

16

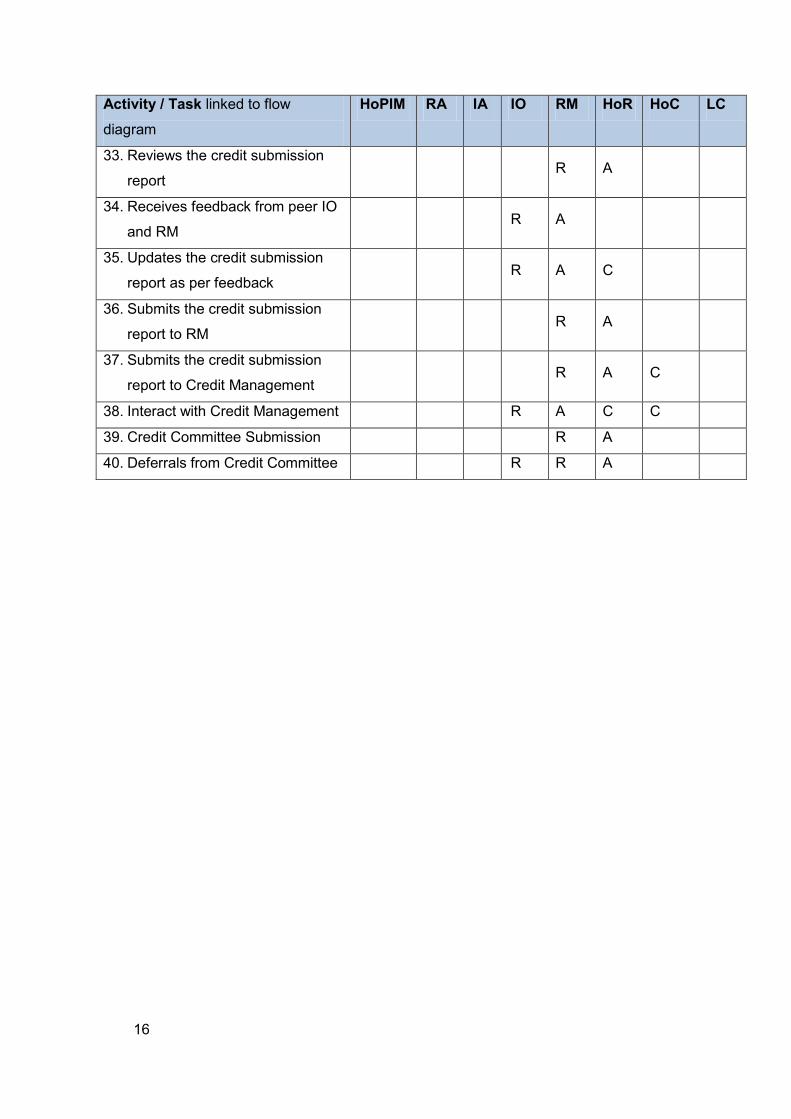

Activity / Task linked to flow

diagram HoPIM RA IA IO RM HoR HoC LC

33. Reviews the credit submission

report R A

34. Receives feedback from peer IO

and RM R A

35. Updates the credit submission

report as per feedback R A C

36. Submits the credit submission

report to RM R A

37. Submits the credit submission

report to Credit Management R A C

38. Interact with Credit Management R A C C

39. Credit Committee Submission R A

40. Deferrals from Credit Committee R R A

17

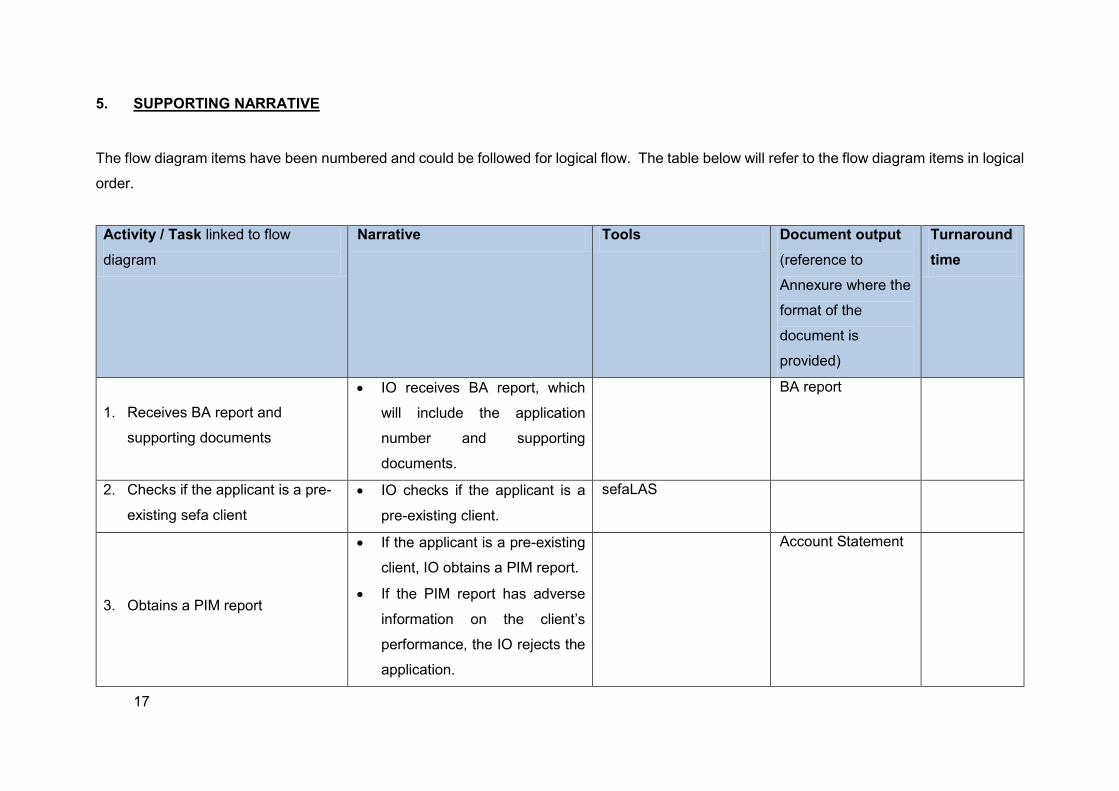

5. SUPPORTING NARRATIVE

The flow diagram items have been numbered and could be followed for logical flow. The table below will refer to the flow diagram items in logical

order.

Activity / Task linked to flow

diagram

Narrative Tools Document output (reference to

Annexure where the

format of the

document is

provided)

Turnaround time

1. Receives BA report and

supporting documents

IO receives BA report, which

will include the application

number and supporting

documents.

BA report

2. Checks if the applicant is a pre-

existing sefa client IO checks if the applicant is a

pre-existing client.

sefaLAS

3. Obtains a PIM report

If the applicant is a pre-existing

client, IO obtains a PIM report.

If the PIM report has adverse

information on the client’s

performance, the IO rejects the

application.

Account Statement

18

If the PIM report has favourable

information, the IO performs the

next step.

4. Reviews the BA report and

supporting documentation IO reviews the report.

5. Checks if all items in the

checklist list are provided

IO checks for missing items

against the checklist.

sefaLAS checklist

New Application

checklist (Annexure

1)

Ticked sefaLAS

checklist

Signed off New

Application

checklist

6. Advises the applicant of missing

items

If there is missing or

outstanding items, IO advises

the applicant.

Cut-off for the applicant to

submit outstanding items is 10

working days.

If the applicant fails to submit

within the specified time,

application is closed.

Notes on sefaLAS

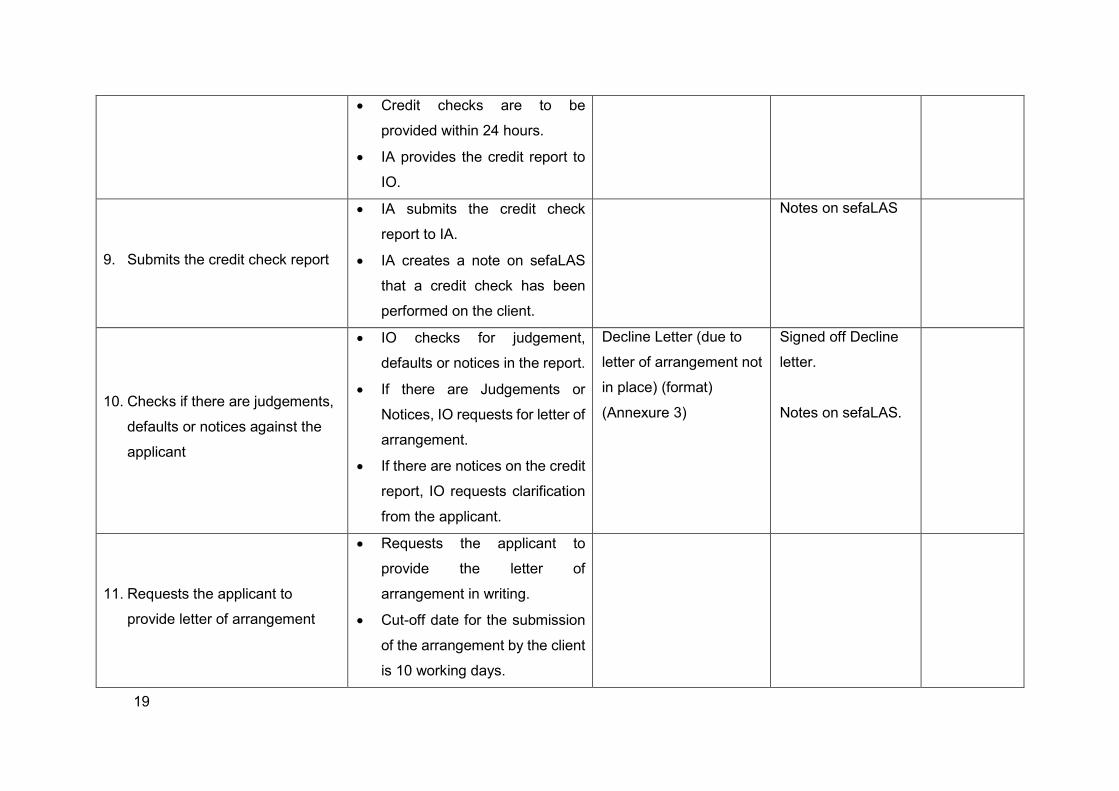

7. Submits the request for credit

checks to be performed IO submits the request for credit

checks to be performed by IA.

8. Conducts credit checks IA conducts the credit checks. www.transunion.co.za TransUnion Report

(Annexure 2)

19

Credit checks are to be

provided within 24 hours.

IA provides the credit report to

IO.

9. Submits the credit check report

IA submits the credit check

report to IA.

IA creates a note on sefaLAS

that a credit check has been

performed on the client.

Notes on sefaLAS

10. Checks if there are judgements,

defaults or notices against the

applicant

IO checks for judgement,

defaults or notices in the report.

If there are Judgements or

Notices, IO requests for letter of

arrangement.

If there are notices on the credit

report, IO requests clarification

from the applicant.

Decline Letter (due to

letter of arrangement not

in place) (format)

(Annexure 3)

Signed off Decline

letter.

Notes on sefaLAS.

11. Requests the applicant to

provide letter of arrangement

Requests the applicant to

provide the letter of

arrangement in writing.

Cut-off date for the submission

of the arrangement by the client

is 10 working days.

20

If the client does not provide a

letter of arrangement within 10

working days, the application is

rejected as unsatisfactory.

IO sends out a letter of decline

to the client.

12. Checks the date at which the

arrangement letter was

formalised or acknowledged

IO checks the date at which the

letter of arrangement was

formalised.

If the letter of arrangement was

formalised less than a month IO

proceeds to the next step.

13. Checks if the applicant honoured

the arrangement

If the letter of arrangement was

formalised more than a month

prior, IO checks if the applicant

honours the arrangement.

If the applicant has not been

honouring the arrangement, IO

declines the application.

14. Submits the request for FICA

verification IO submits a request for FICA

verification to IA.

FICA Checklist

21

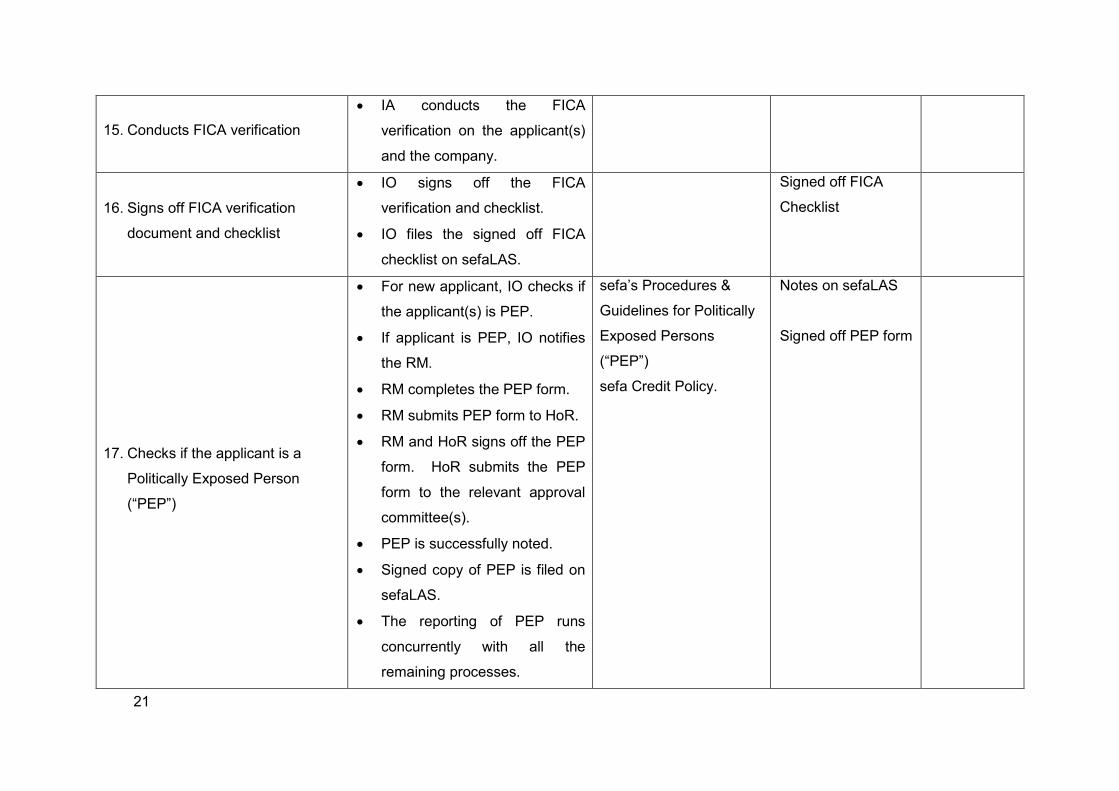

15. Conducts FICA verification IA conducts the FICA

verification on the applicant(s)

and the company.

16. Signs off FICA verification

document and checklist

IO signs off the FICA

verification and checklist.

IO files the signed off FICA

checklist on sefaLAS.

Signed off FICA

Checklist

17. Checks if the applicant is a

Politically Exposed Person

(“PEP”)

For new applicant, IO checks if

the applicant(s) is PEP.

If applicant is PEP, IO notifies

the RM.

RM completes the PEP form.

RM submits PEP form to HoR.

RM and HoR signs off the PEP

form. HoR submits the PEP

form to the relevant approval

committee(s).

PEP is successfully noted.

Signed copy of PEP is filed on

sefaLAS.

The reporting of PEP runs

concurrently with all the

remaining processes.

sefa’s Procedures &

Guidelines for Politically

Exposed Persons

(“PEP”)

sefa Credit Policy.

Notes on sefaLAS

Signed off PEP form

22

18. Invites experts in the

field/industry (if deemed

necessary)

In the event that the transaction

involves specialised fields (e.g.

Agriculture, I.T., Mining), the IO

needs to send an e-mail to RM

and HoR seeking advice on the

transaction (not mandatory).

19. Conduct client introduction

IO introduces himself/herself to

the client for preparation to the

Due Diligence stage.

Letter to secure

appointment for DD with

the client (format)

(Annexure 4)

Notes on sefaLAS

20. Reviews the business plan,

historical and/or projected

financials

IO reviews the business plan,

historical and/or projected

financials and all relevant

industry literature.

21. Prepares financial model

IO prepares the financial model

and make notes on the

variances.

IO prepares questions to be

included in the DD session with

the client

Financial Model Filed Financial

Model on sefaLAS

22. Arranges for site visit For new business or start-up, IO

arranges for the applicant to

visit sefa offices or arranges to

Notes on sefaLAS

23

visit the intended business

premises.

For existing business, IO

arranges for the site visit to the

applicant’s premises.

23. Checks the type of required

financing.

IO checks the type of financing

required (as indicated in the

application form & BA report).

Product Guidelines

24. Performs Due Diligence in line

with checklist

For contract based finance

transactions, IO performs the

due diligence in line with

contract based finance DD

checklist.

For term funding transactions,

IO performs DD in line with term

funding DD checklist.

IO and RM signs off the DD

checklist.

Contract Based Finance

DD checklist

OR

Term Funding DD

checklist

Signed off Contract

Based Finance DD

checklist

OR

Signed off Term

Funding DD

checklist

25. Checks if there is critical

information outstanding

IO checks if there is critical

information missing.

IO requests the information

from the client in writing.

24

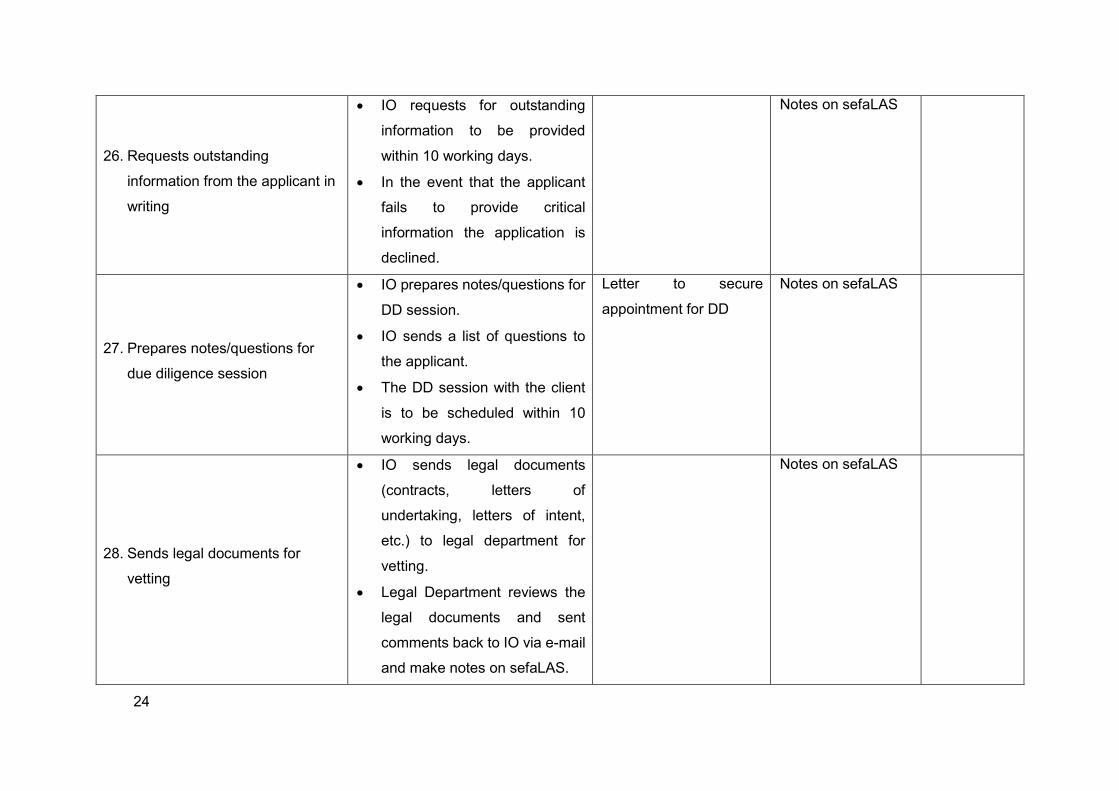

26. Requests outstanding

information from the applicant in

writing

IO requests for outstanding

information to be provided

within 10 working days.

In the event that the applicant

fails to provide critical

information the application is

declined.

Notes on sefaLAS

27. Prepares notes/questions for

due diligence session

IO prepares notes/questions for

DD session.

IO sends a list of questions to

the applicant.

The DD session with the client

is to be scheduled within 10

working days.

Letter to secure

appointment for DD

Notes on sefaLAS

28. Sends legal documents for

vetting

IO sends legal documents

(contracts, letters of

undertaking, letters of intent,

etc.) to legal department for

vetting.

Legal Department reviews the

legal documents and sent

comments back to IO via e-mail

and make notes on sefaLAS.

Notes on sefaLAS

25

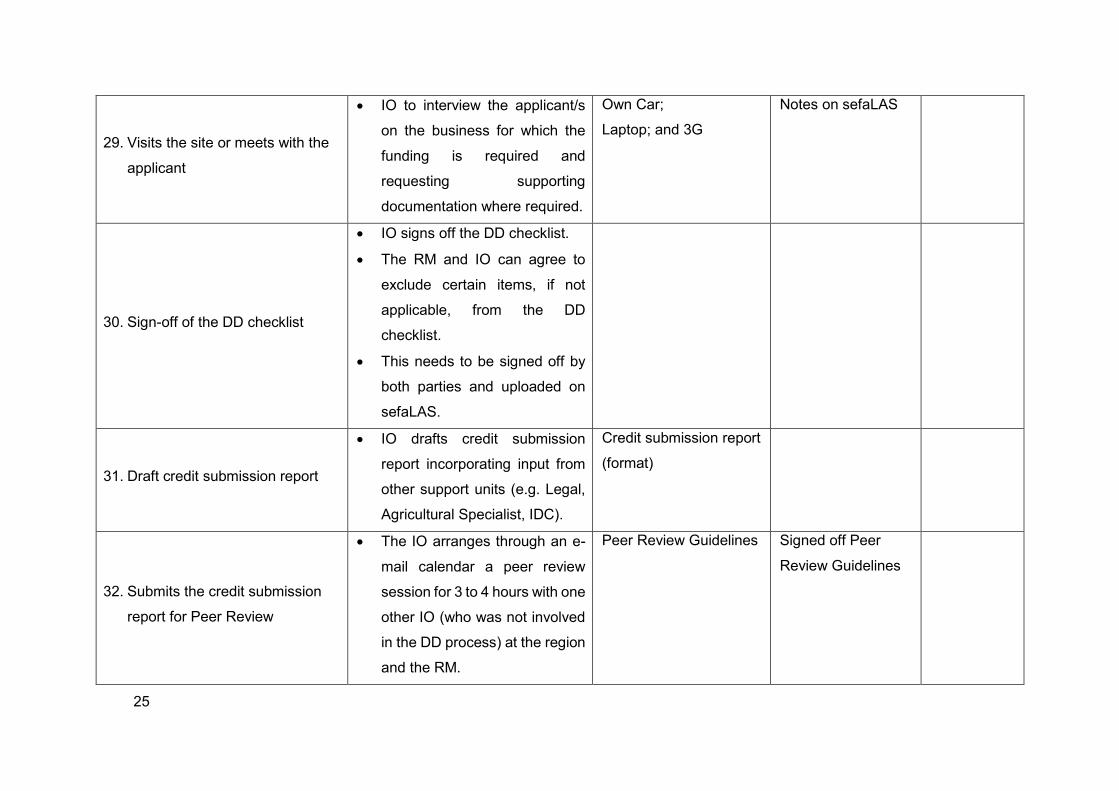

29. Visits the site or meets with the

applicant

IO to interview the applicant/s

on the business for which the

funding is required and

requesting supporting

documentation where required.

Own Car;

Laptop; and 3G

Notes on sefaLAS

30. Sign-off of the DD checklist

IO signs off the DD checklist.

The RM and IO can agree to

exclude certain items, if not

applicable, from the DD

checklist.

This needs to be signed off by

both parties and uploaded on

sefaLAS.

31. Draft credit submission report

IO drafts credit submission

report incorporating input from

other support units (e.g. Legal,

Agricultural Specialist, IDC).

Credit submission report

(format)

32. Submits the credit submission

report for Peer Review

The IO arranges through an e-

mail calendar a peer review

session for 3 to 4 hours with one

other IO (who was not involved

in the DD process) at the region

and the RM.

Peer Review Guidelines Signed off Peer

Review Guidelines

26

33. Reviews the credit submission

report

Peer reviews the credit

submission report in line with

Peer Review Guidelines.

IO and RM signs off the Peer

Review Guidelines.

Signed off Peer

Review Guidelines

and notes

34. Receives feedback from peer IO

and RM

IO receives feedback from peer

review session.

Peer Review

Feedback notes on

sefaLAS

35. Updates the credit submission

report as per feedback

IO updates the credit

submission report as per

feedback.

36. Submits the credit submission

report to RM

IO submits the credit

submission report to RM for

final review.

Credit submission

report on sefaLAS

37. Submits the credit submission

report to Credit Management

Unit

RM submits the credit

submission report to CA at

Credit Management Unit.

Credit submission report

(format)

Credit submission

report on sefaLAS

38. Interact with Credit Management

Unit

CA reviews the credit

submission report.

CA sends risk comments to IO.

IO and RM interacts with CA on

risk issues.

Notes on sefaLAS

27

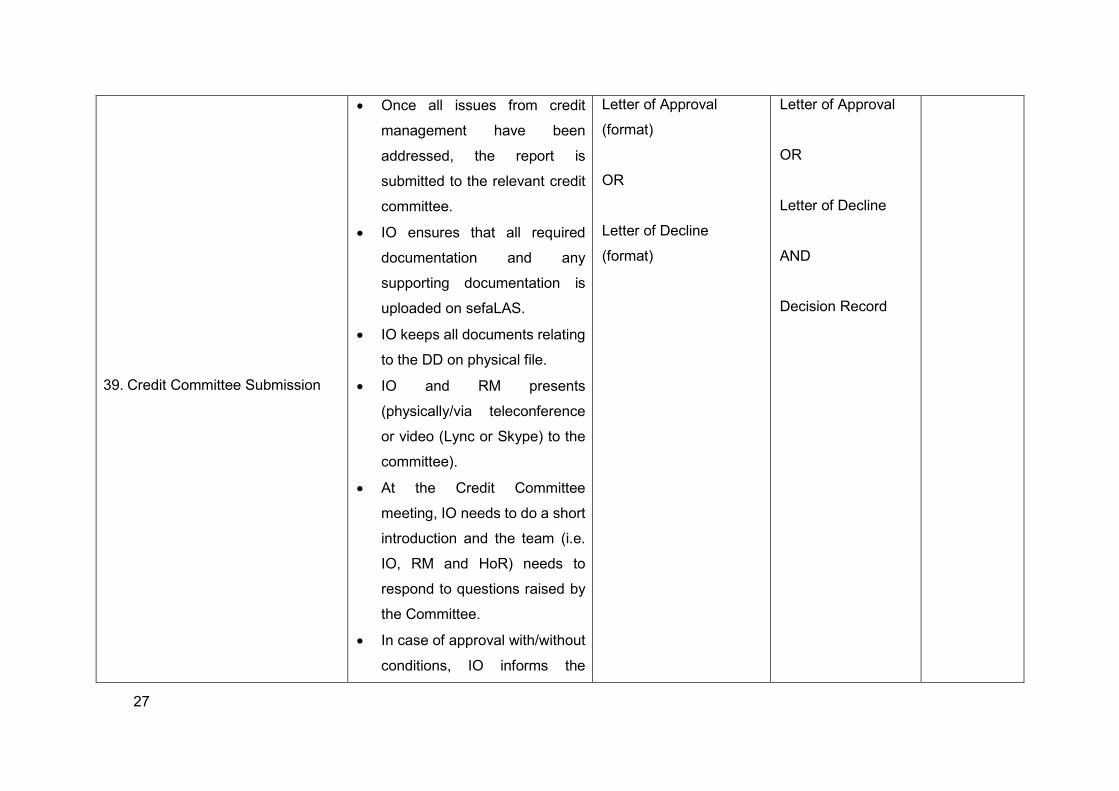

39. Credit Committee Submission

Once all issues from credit

management have been

addressed, the report is

submitted to the relevant credit

committee.

IO ensures that all required

documentation and any

supporting documentation is

uploaded on sefaLAS.

IO keeps all documents relating

to the DD on physical file.

IO and RM presents

(physically/via teleconference

or video (Lync or Skype) to the

committee).

At the Credit Committee

meeting, IO needs to do a short

introduction and the team (i.e.

IO, RM and HoR) needs to

respond to questions raised by

the Committee.

In case of approval with/without

conditions, IO informs the

Letter of Approval

(format)

OR

Letter of Decline

(format)

Letter of Approval

OR

Letter of Decline

AND

Decision Record

28

applicant in writing within 48

hours after the meeting.

In case of approval a decision

record to be signed off by the

latter within2 working days after

the Credit Committee meeting.

IO to inform the successful

applicant in writing of the next

process of signing of legal

documents.

In case of declined application,

IO needs to inform the applicant

in writing of the Credit

Committee decision.

40. Deferrals from Credit Committee

In the event that the deal is

deferred by the committee due

to insufficient information or any

other reason, IO interacts with

client to obtain the missing or

outstanding information or

augment the submission for

submission.

Resubmission Memo

(format)

Notes on sefaLAS

Signed off

Resubmission

Memo

29

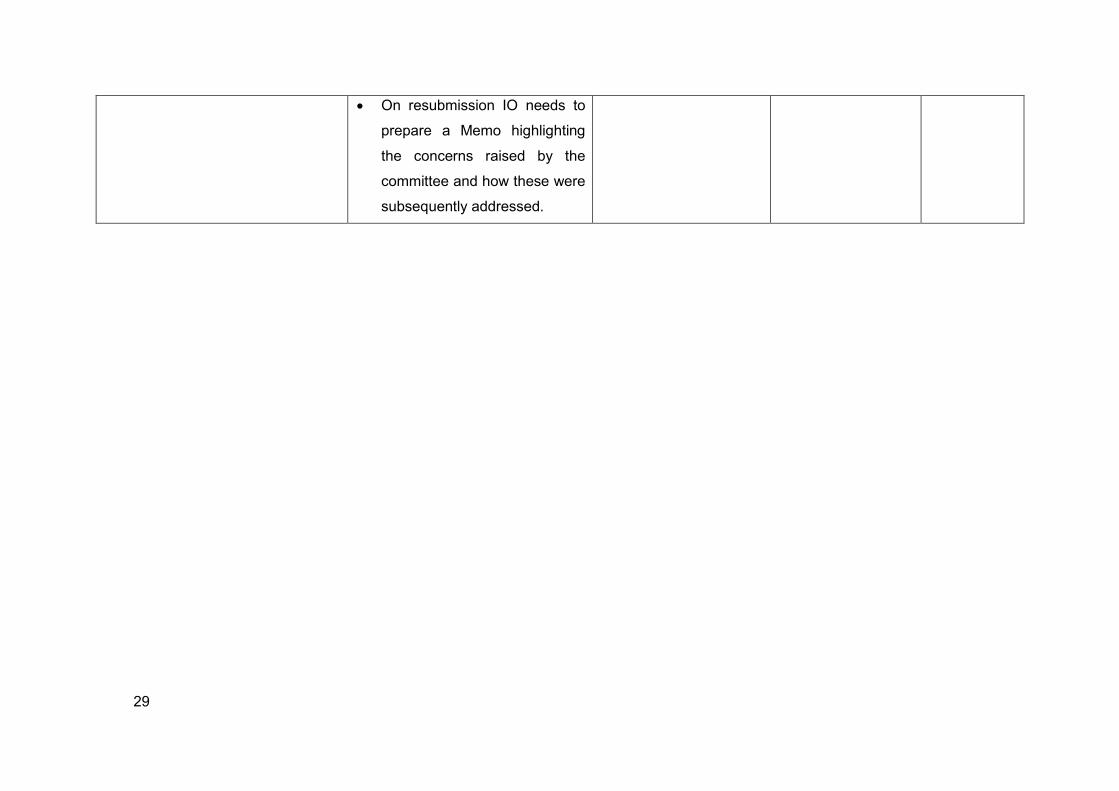

On resubmission IO needs to

prepare a Memo highlighting

the concerns raised by the

committee and how these were

subsequently addressed.

30

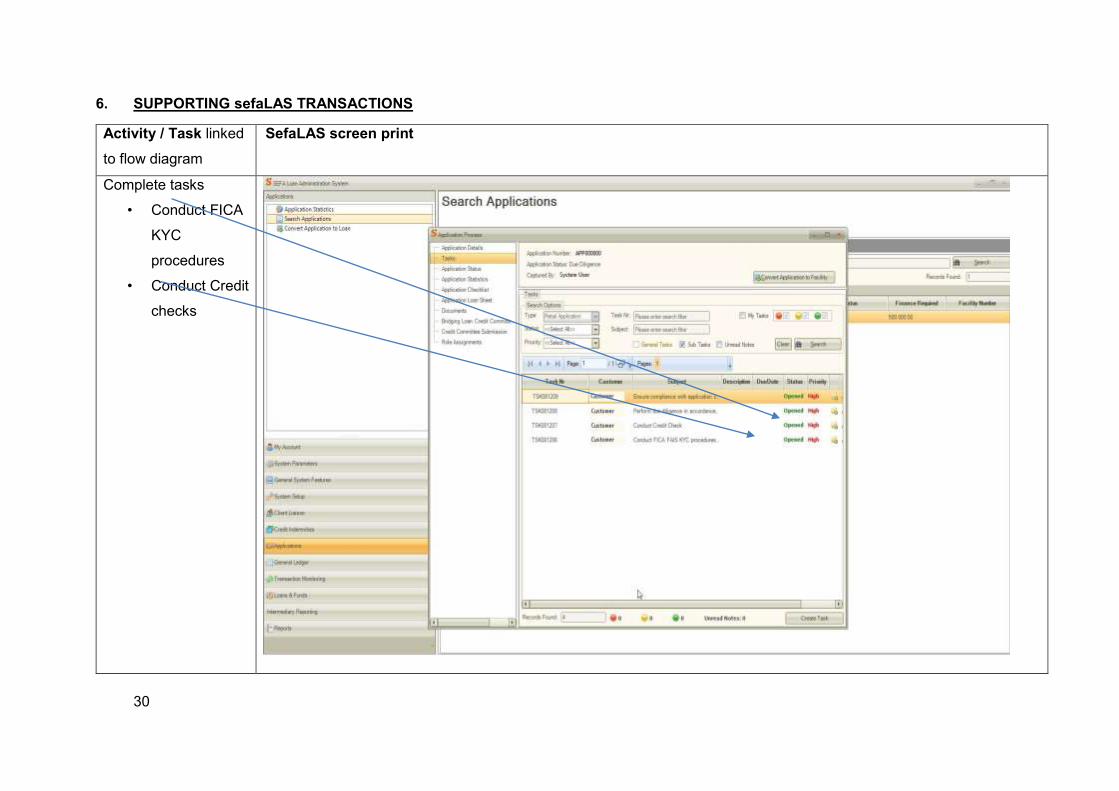

6. SUPPORTING sefaLAS TRANSACTIONS

Activity / Task linked

to flow diagram

SefaLAS screen print

Complete tasks

• Conduct FICA

KYC

procedures

• Conduct Credit

checks

31

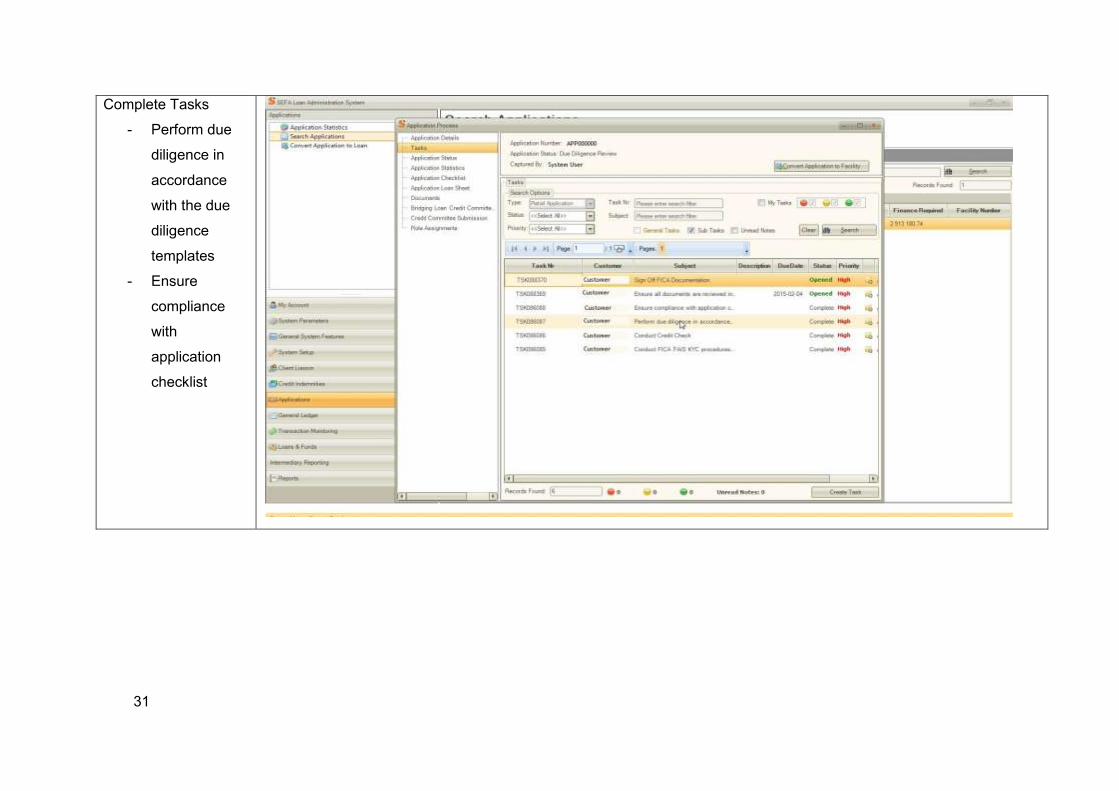

Complete Tasks

- Perform due

diligence in

accordance

with the due

diligence

templates

- Ensure

compliance

with

application

checklist

32

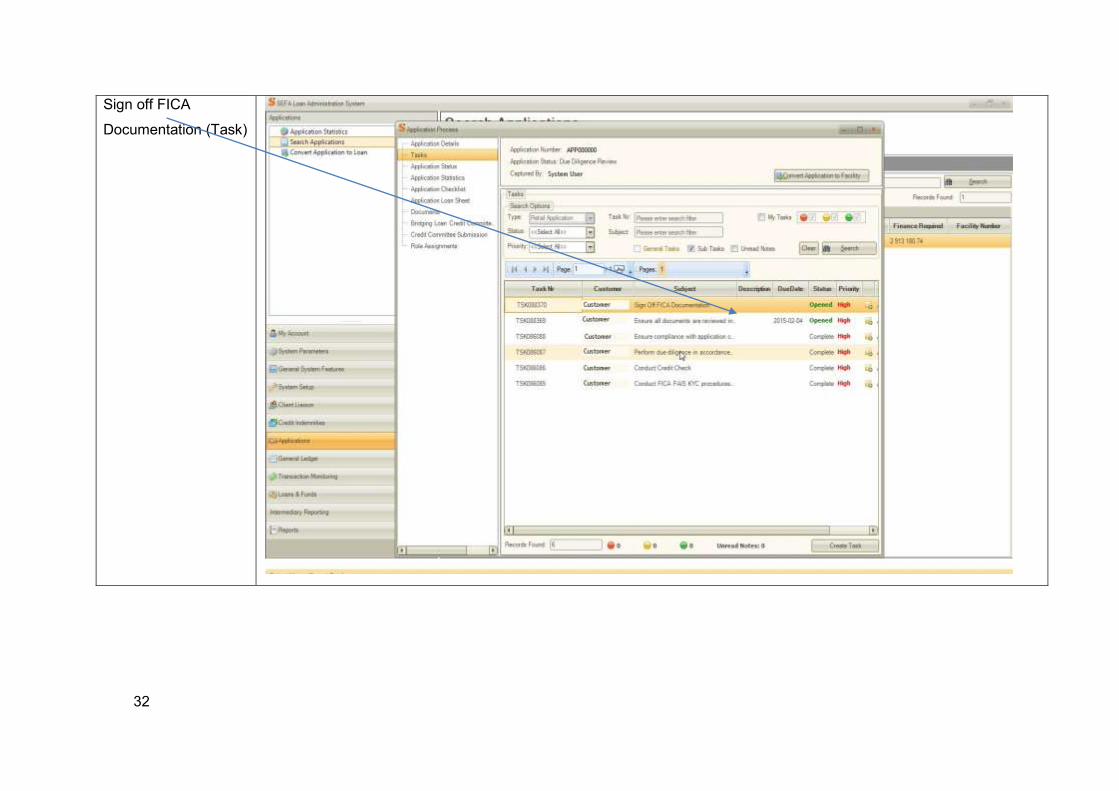

Sign off FICA

Documentation (Task)

33

Due Diligence Status

Change

34

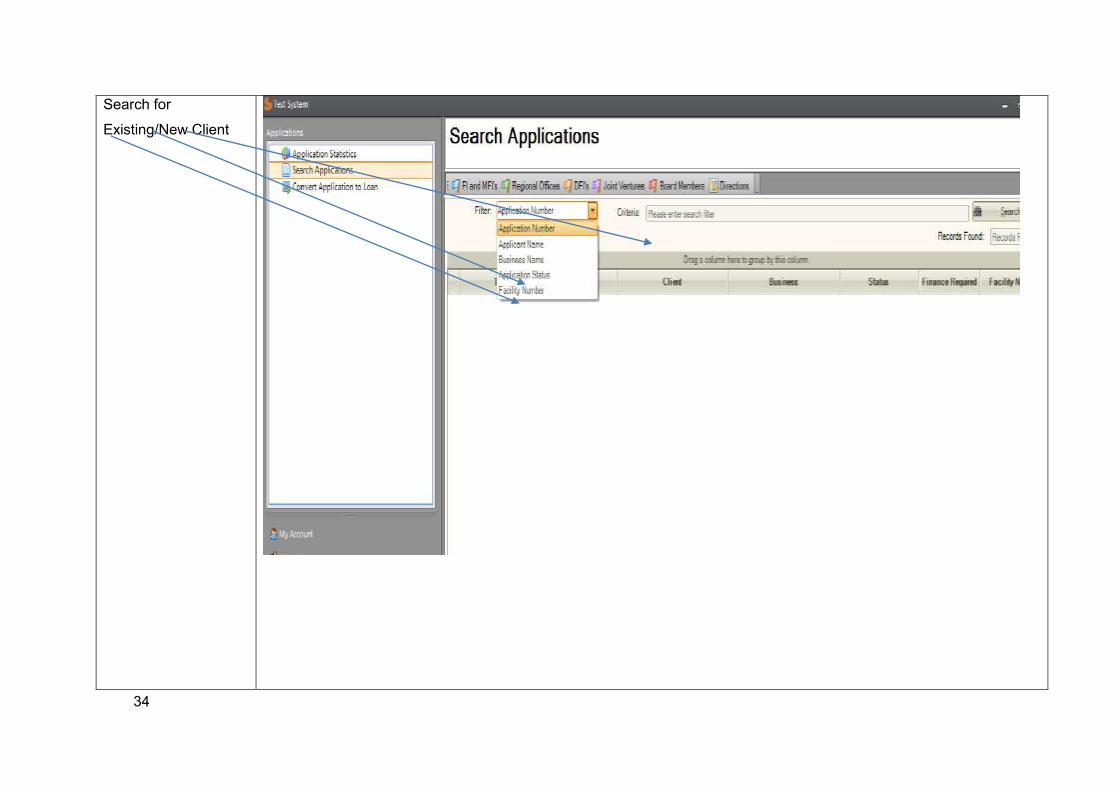

Search for

Existing/New Client

35

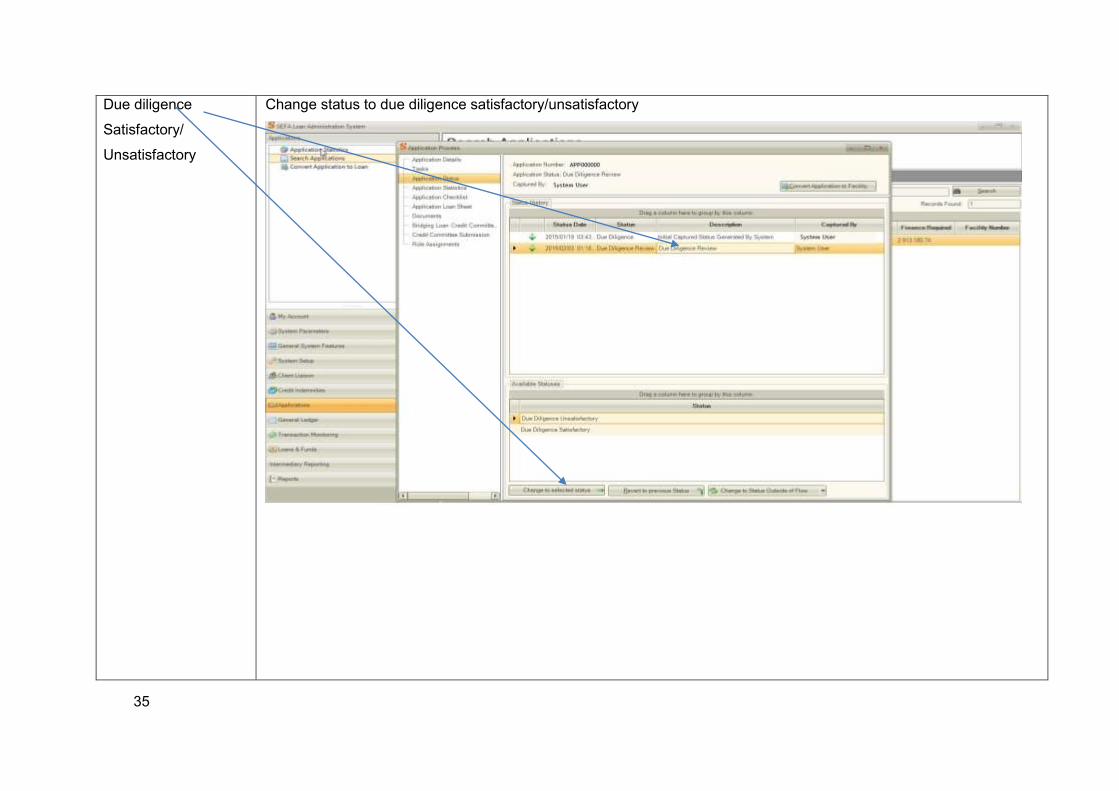

Due diligence

Satisfactory/

Unsatisfactory

Change status to due diligence satisfactory/unsatisfactory

36

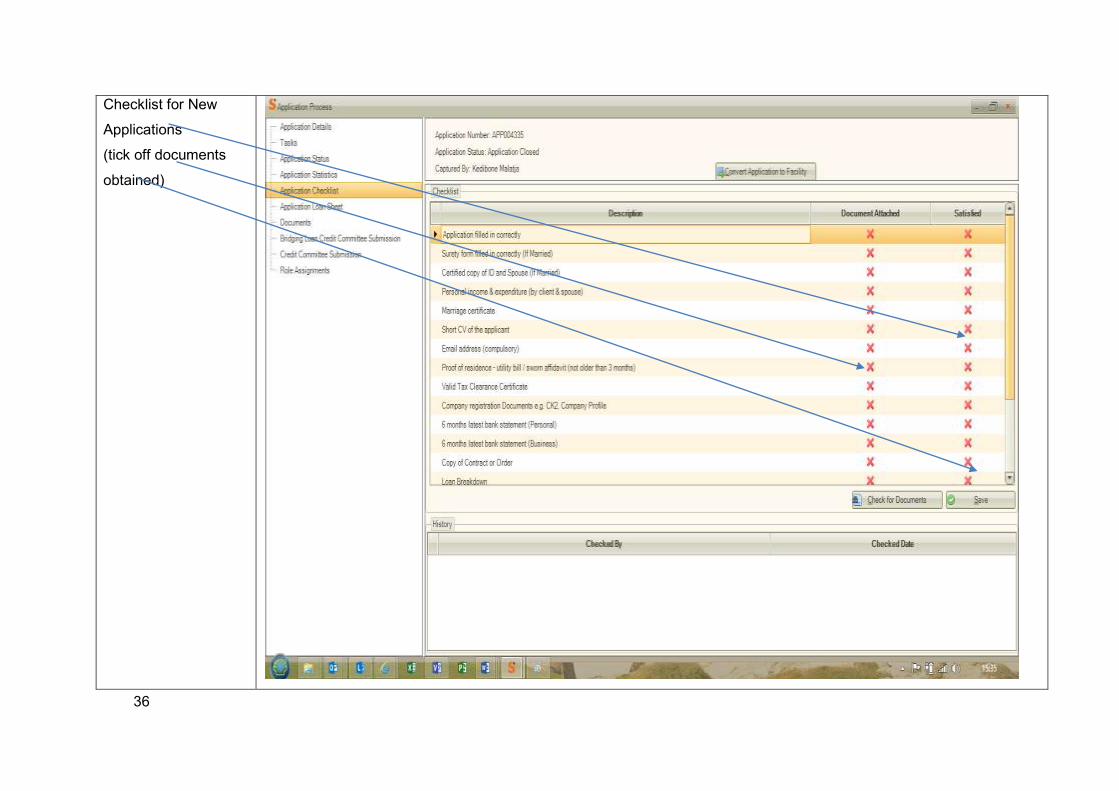

Checklist for New

Applications

(tick off documents

obtained)

37

Deal Summary,

Motivation, Sector,

Finance Required.

38

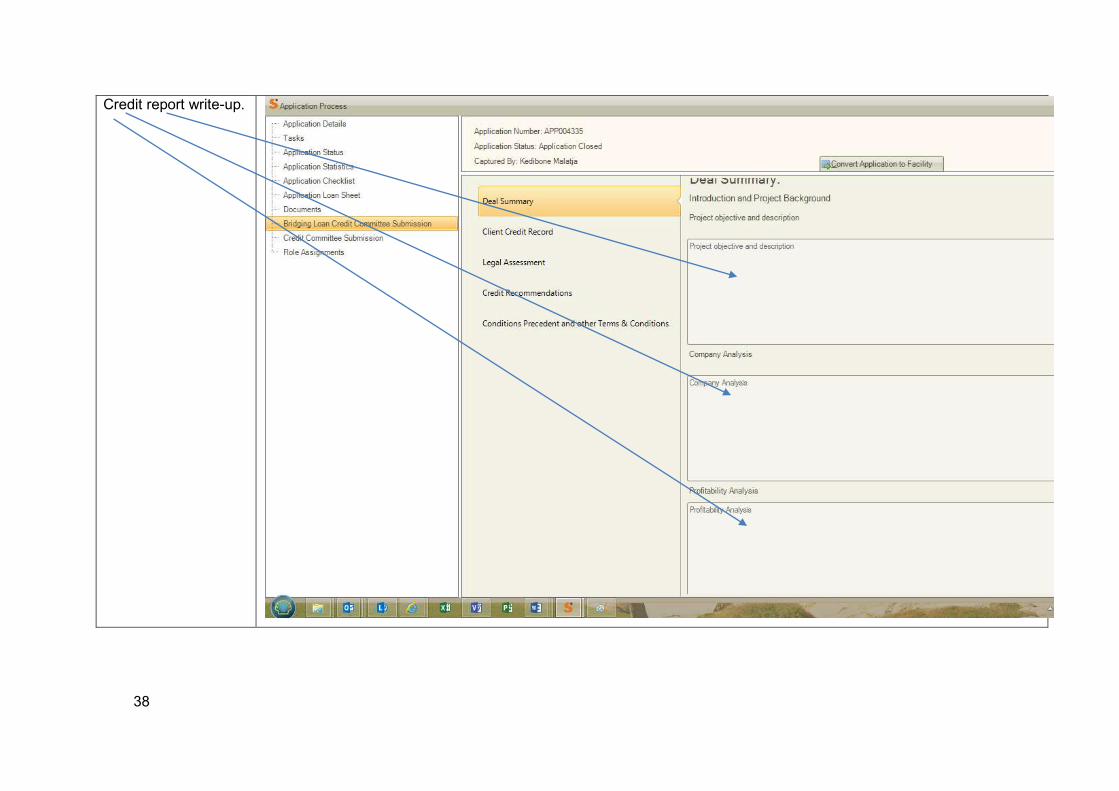

Credit report write-up.

39

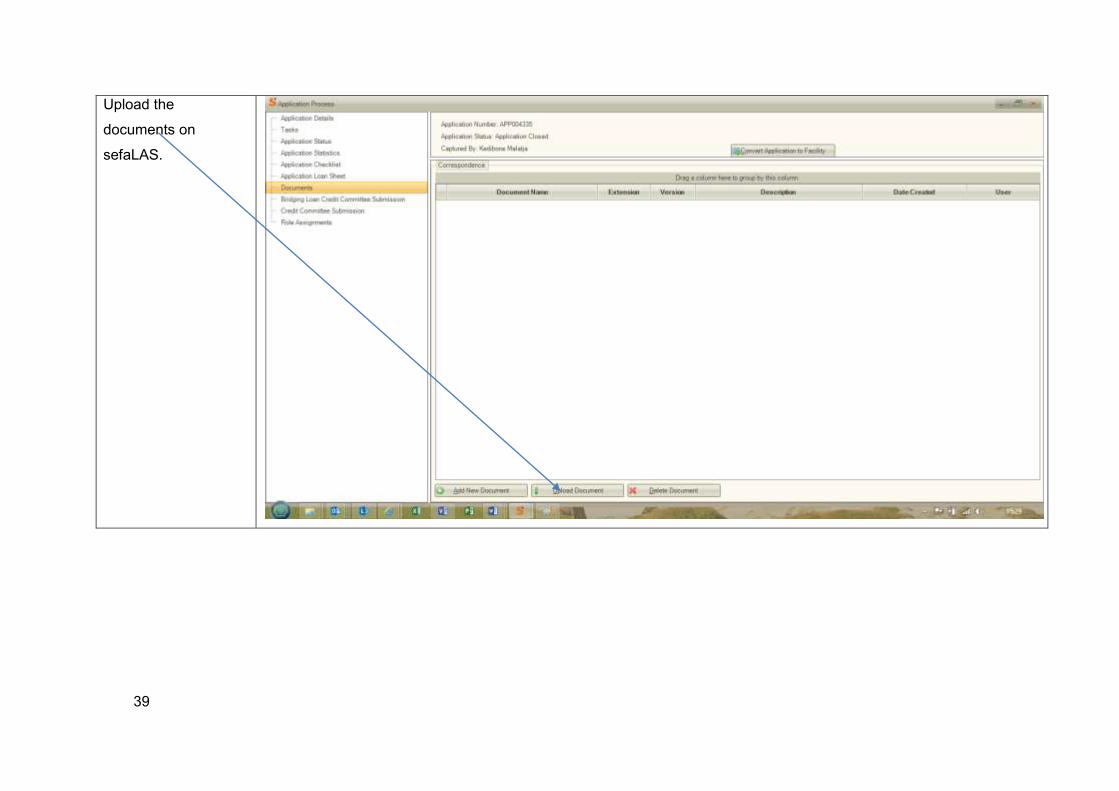

Upload the

documents on

sefaLAS.

40

Update Jobs Created,

Permanent,

Temporary Jobs,

Skilled Jobs, Unskilled

Jobs, Ownership (in

terms of racial

composition),

Provincial

Classification, Age

Group and Inside

NCA or Outside NCA.

41

Create Notes on

sefaLAS for all

interaction with the

client.

42

7. ANNEXURES

7.1. ANNEXURE 1 - CHECKLIST FOR NEW APPLICATIONS

43

7.2. ANNEXURE 2 - TRANSUNION REPORT

44

45

46

7.3. ANNEXURE 3 - LETTER OF DECLINE (NO LETTER OF ARRANGEMENT)

47

7.4. ANNEXURE 4 - LETTER SECURIING APPOINTMENT FOR DD

48

7.5. ANNEXURE 5 - LETTER OF DECLINE (DUE DILIGENCE UNSATISFACTORY)

49

7.6. ANNEXURE 6 - PIM REPORT/EXAMPLE OF INVOICE

50

7.7. ANNEXURE 7 – LETTER OF DECLINE

51

7.8. ANNEXURE 8 – LETTER OF APPROVAL

52

7.9. ANNEXURE 9 – MEMO TO COMMITTEE

53

54

ANNEXURE 10

FICA CHECKLIST

1

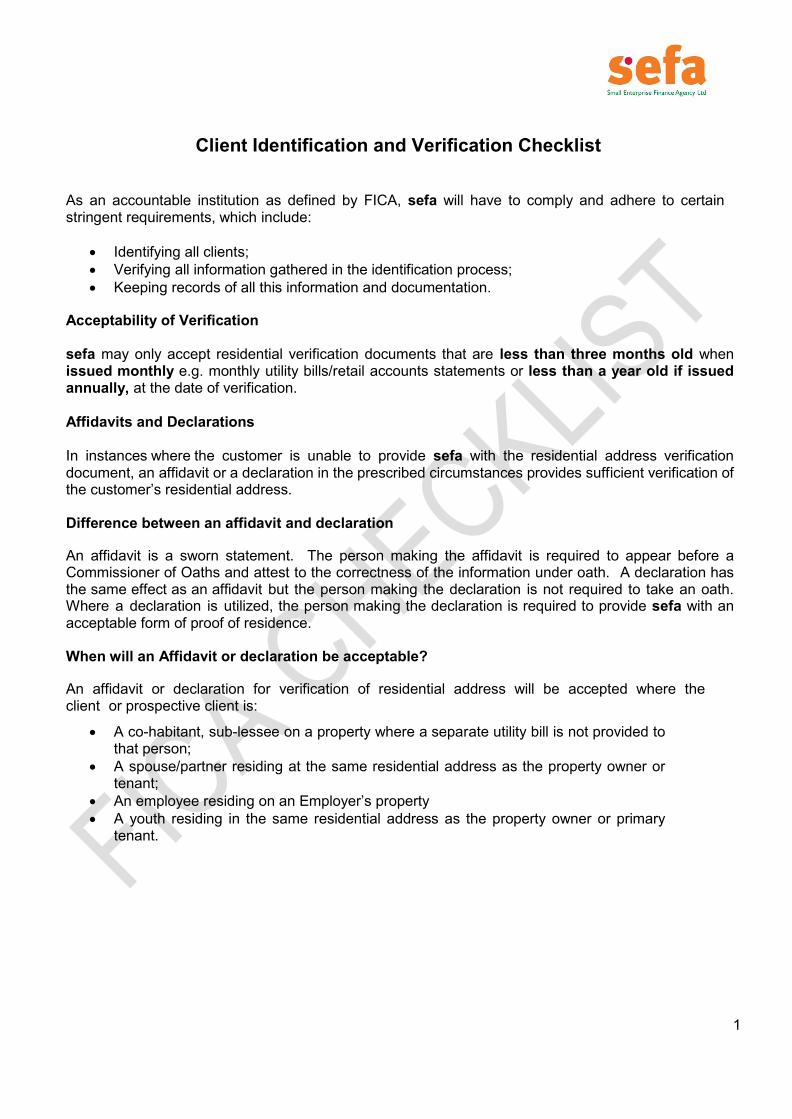

Client Identification and Verification Checklist

As an accountable institution as defined by FICA, sefa will have to comply and adhere to certain stringent requirements, which include:

Identifying all clients; Verifying all information gathered in the identification process; Keeping records of all this information and documentation.

Acceptability of Verification sefa may only accept residential verification documents that are less than three months old when issued monthly e.g. monthly utility bills/retail accounts statements or less than a year old if issued annually, at the date of verification. Affidavits and Declarations In instances where the customer is unable to provide sefa with the residential address verification document, an affidavit or a declaration in the prescribed circumstances provides sufficient verification of the customer’s residential address. Difference between an affidavit and declaration

An affidavit is a sworn statement. The person making the affidavit is required to appear before a Commissioner of Oaths and attest to the correctness of the information under oath. A declaration has the same effect as an affidavit but the person making the declaration is not required to take an oath. Where a declaration is utilized, the person making the declaration is required to provide sefa with an acceptable form of proof of residence. When will an Affidavit or declaration be acceptable?

An affidavit or declaration for verification of residential address will be accepted where the client or prospective client is:

A co-habitant, sub-lessee on a property where a separate utility bill is not provided to that person;

A spouse/partner residing at the same residential address as the property owner or tenant;

An employee residing on an Employer’s property A youth residing in the same residential address as the property owner or primary

tenant.

2

IDENTIFICATION AND VERIFICATION REQUIREMENTS CHECK LIST South African Citizens and Residence Customer type Information required Verification documentation Comments South African citizens and residents

Full name

Date of Birth; and

Identity number

Primary Identification

Green bar-coded identity document.

Residential address Anyone of the following valid documents reflecting the clients’ name and address:

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Account statement from a service provider registered in

terms of the National Credit Act;

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

Valid television licence

Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from another financial institution;

3

Customer type Information required Verification documentation Comments Long/short term insurance policy documents, from another

Financial Service Provider;

Motor Vehicle registration/licence documents;

Municipal council letter;

Body corporate/governing body letter or statement;

Official employer letter for employees resident on the

company/institution premises;

Physical site visit conducted for verification purposes;

Tribal authority letter;

Affidavit to confirm residential address by Co-habitant,

Home Owner or Parent;

Declaration of residential address employer where the

employer resides on the Employer’s property;

Declaration of residential address by co-habitant, home

owner or parent.

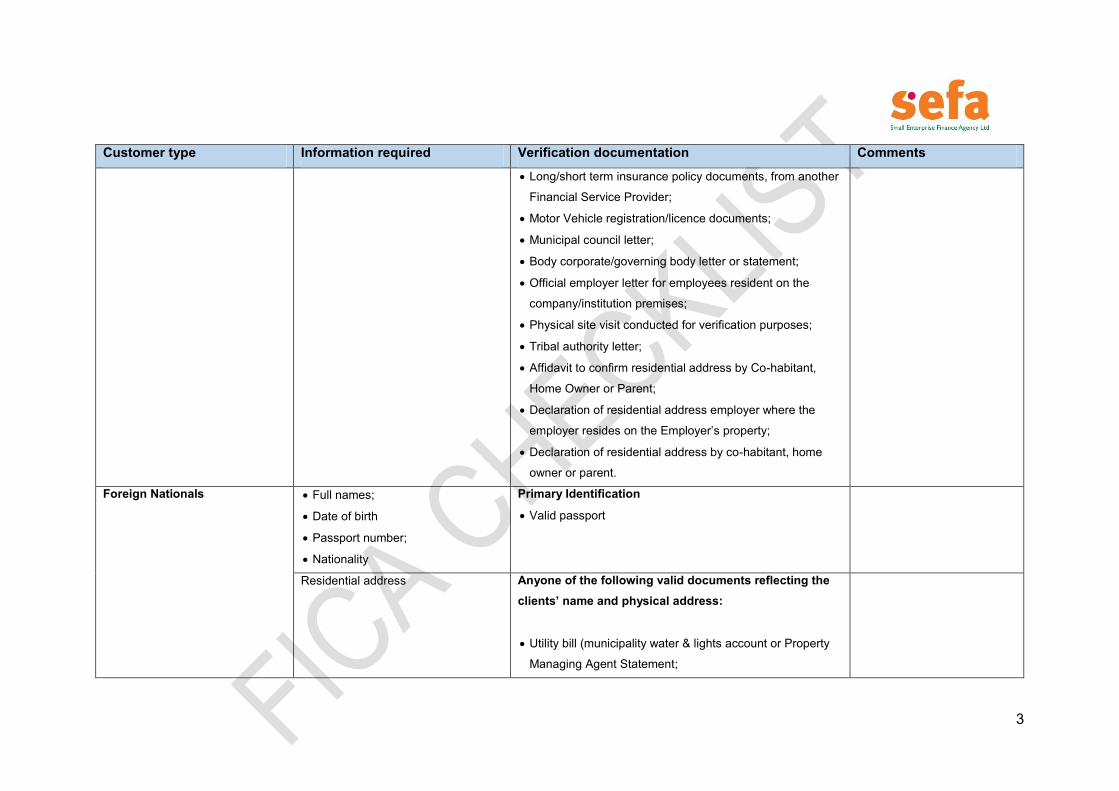

Foreign Nationals Full names;

Date of birth

Passport number;

Nationality

Primary Identification

Valid passport

Residential address

Anyone of the following valid documents reflecting the clients’ name and physical address:

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

4

Customer type Information required Verification documentation Comments Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Account statement from a service provider registered in

terms of the National Credit Act;

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

Valid television licence

Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from another financial institution;

Long/short term insurance policy documents, from another

Financial Service Provider;

Motor Vehicle registration/licence documents;

Municipal council letter;

Body corporate/governing body letter or statement;

Official employer letter for employees resident on the

company/institution premises;

Physical site visit conducted for verification purposes;

Tribal authority letter;

Affidavit to confirm residential address by Co-habitant,

Home Owner or Parent;

5

Customer type Information required Verification documentation Comments Declaration of residential address employer where the

employer resides on the Employer’s property;

Declaration of residential address by co-habitant, home

owner or parent.

Sole traders Full names;

Date of birth

Identity number if a South African

citizen or resident;

Nationality and passport number if

a foreign national.

See requirements in the tables for individuals and Foreign

Nationals.

Residential and business address

(both to be verified by separate

documents);

Business name (operating name)

See requirements in the tables for individuals and Foreign

Nationals.

Close Corporation Registered name;

Name under which the business is

conducted (Trade name);

Registration number;

Registered address

Most recent version of the founding statement and

certificate of Incorporation (form CK1), specifying the

controlling members; OR

Amended founding statement (form CK2),OR

Independently obtained CIPC certificate of confirmation.

The Physical address from which

the Close Corporation operates. If

multiple addresses, the street

address of the office seeking the

business relationship and Head

6

Customer type Information required Verification documentation Comments Office address must be obtained

and verified;

NB: In the event that the business

address and the physical address is

one and the same, then one

document confirming and indicating

as such is acceptable

Full names, date of birth and identify

number (nationality of a foreign

national), residential address and

contact particulars:

Each member;

The mandate officials who are

authorised to establish a business

relationship or enter into transaction

as per resolution

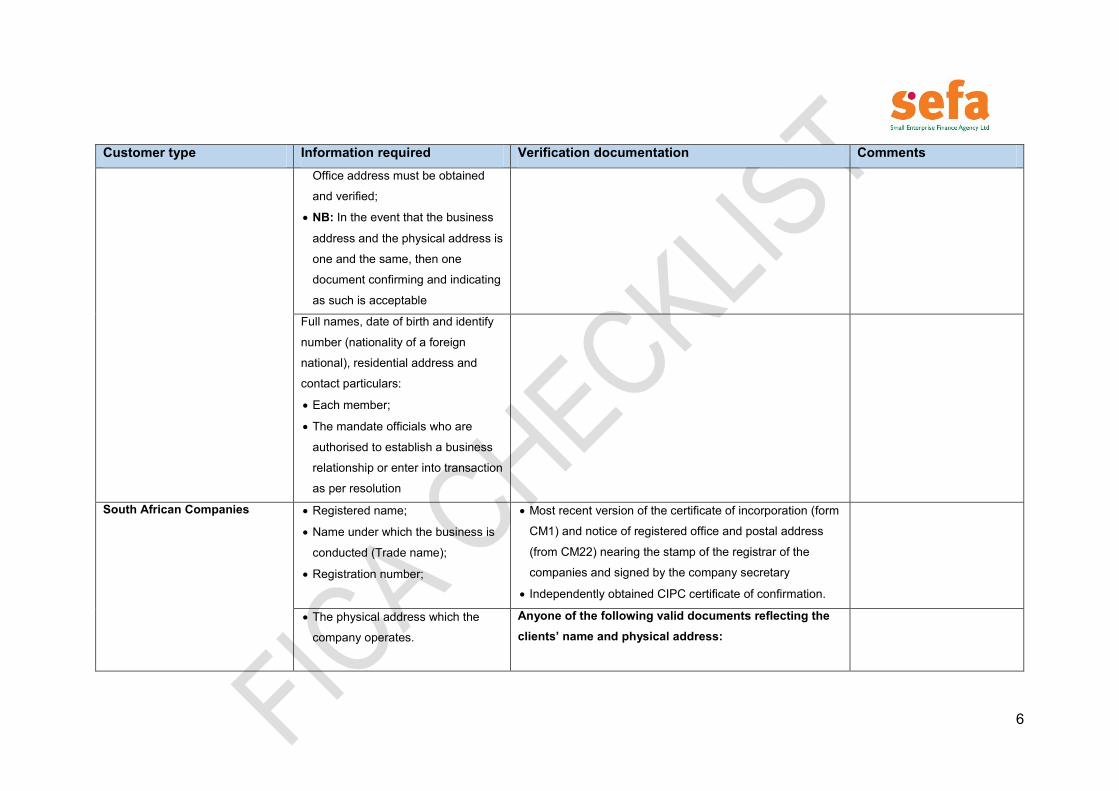

South African Companies Registered name;

Name under which the business is

conducted (Trade name);

Registration number;

Most recent version of the certificate of incorporation (form

CM1) and notice of registered office and postal address

(from CM22) nearing the stamp of the registrar of the

companies and signed by the company secretary

Independently obtained CIPC certificate of confirmation.

The physical address which the

company operates.

Anyone of the following valid documents reflecting the clients’ name and physical address:

7

Customer type Information required Verification documentation Comments If multiple addresses, the street

address of the office seeking

financial assistance.

Head Office address must be

obtained and verified

NB: In the event that the head office address and operational address is one and the same, then one document confirming and indicating as such is acceptable.

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Account statement from a service provider registered in

terms of the National Credit Act;

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

Valid television licence

Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from another financial institution;

Long/short term insurance policy documents, from the

Financial Service Provider;

Attorney/Accountant/Auditor letter on

Attorney/Accountant/Auditor letterhead confirming the

address of the client;

Motor Vehicle registration/licence documents;

Physical site visit conducted for verification purposes;

Tribal authority letter;

Affidavit from an authorised official confirming the

operational address and trading name of the company;

8

Customer type Information required Verification documentation Comments Full names, date of birth and identify

number (nationality of a foreign

national), residential address and

contact particulars of:

The manger/CEO of the company;

The mandate officials authorised to

establish a business relationship or

enter into transaction as per

resolution;

The natural person, legal person,

partnership or trust holding 10% or

more, of the voting rights at a

general meeting of the company.

See requirements in the tables for individuals and Foreign

Nationals – in respect of members and mandate officials.

A resolution/mandate authorising the person as mandate

officials is required.

NB: It is not necessary to verify the residential address and contact particulars of these persons – however it is necessary to obtain and record the information. If a shareholder is not a natural person, the identification and Verification requirements for the entity or the business arrangement into which they fall needs to be applied.

South African Listed Companies

Registered name;

Registration number.

The physical address from which

the company operates; and

If multiple addresses, the street

address of the office seeking the

business relationship; and

The Head Office address must be

obtained

This information need to be verified, only obtained and

recorded.

This information need to be verified, only obtained and

recorded.

9

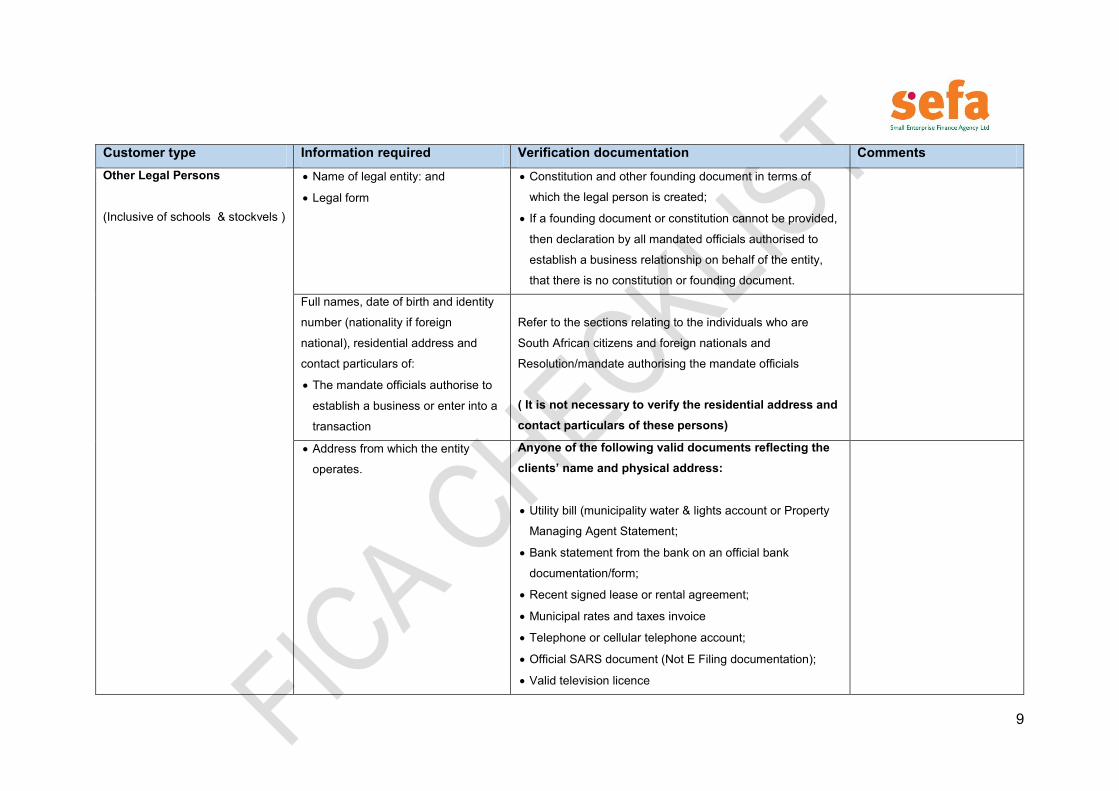

Customer type Information required Verification documentation Comments Other Legal Persons (Inclusive of schools & stockvels )

Name of legal entity: and

Legal form

Constitution and other founding document in terms of

which the legal person is created;

If a founding document or constitution cannot be provided,

then declaration by all mandated officials authorised to

establish a business relationship on behalf of the entity,

that there is no constitution or founding document.

Full names, date of birth and identity

number (nationality if foreign

national), residential address and

contact particulars of:

The mandate officials authorise to

establish a business or enter into a

transaction

Refer to the sections relating to the individuals who are

South African citizens and foreign nationals and

Resolution/mandate authorising the mandate officials

( It is not necessary to verify the residential address and contact particulars of these persons)

Address from which the entity

operates.

Anyone of the following valid documents reflecting the clients’ name and physical address:

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

Valid television licence

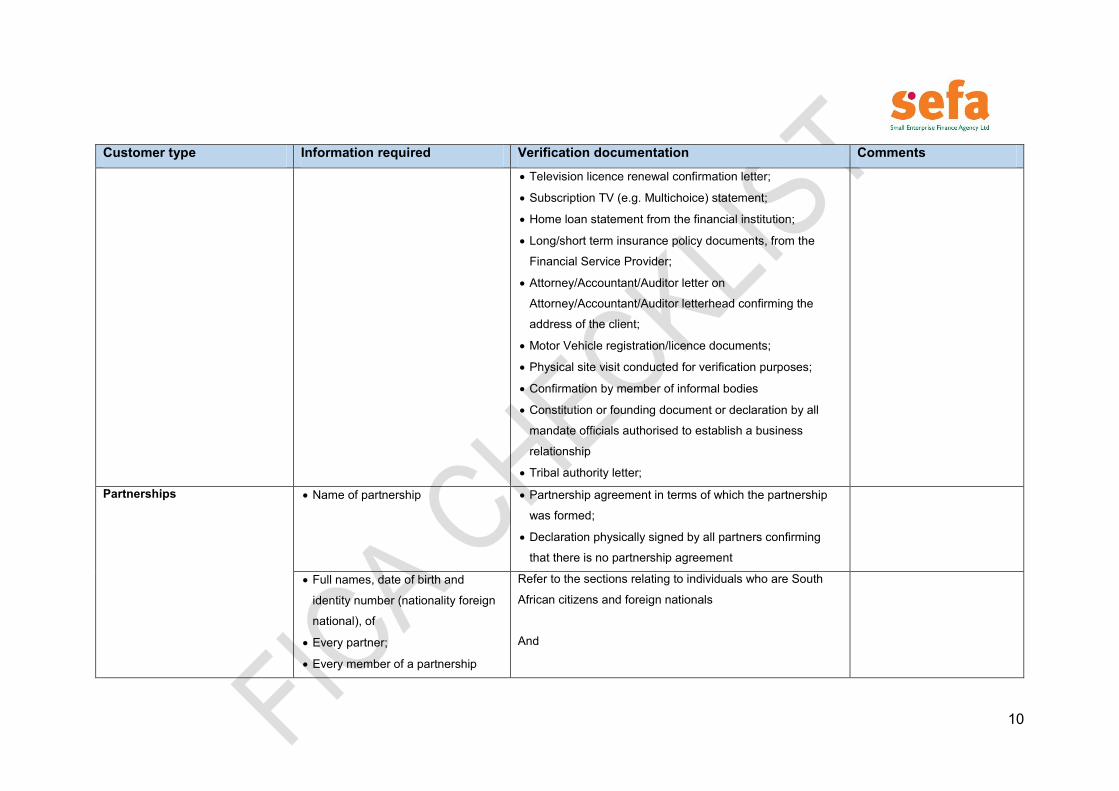

10

Customer type Information required Verification documentation Comments Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from the financial institution;

Long/short term insurance policy documents, from the

Financial Service Provider;

Attorney/Accountant/Auditor letter on

Attorney/Accountant/Auditor letterhead confirming the

address of the client;

Motor Vehicle registration/licence documents;

Physical site visit conducted for verification purposes;

Confirmation by member of informal bodies

Constitution or founding document or declaration by all

mandate officials authorised to establish a business

relationship

Tribal authority letter;

Partnerships Name of partnership Partnership agreement in terms of which the partnership

was formed;

Declaration physically signed by all partners confirming

that there is no partnership agreement

Full names, date of birth and

identity number (nationality foreign

national), of

Every partner;

Every member of a partnership

Refer to the sections relating to individuals who are South

African citizens and foreign nationals

And

11

Customer type Information required Verification documentation Comments The mandated officials who are

authorised to establish a business

relationship or enter into a

transaction; and executive control

over the partnership.

Resolution/mandate authorising the mandate officials

If a partner is not a natural person, the entity must be

identified as per the mandatory information for the category

of client with which it falls

Business address

In the event that the partnership does

not have a business operating

address, the address of at least one

partner must be provided.

Anyone of the following valid documents reflecting the clients’ name and physical address:

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

Valid television licence

Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from the financial institution;

Long/short term insurance policy documents, from the

Financial Service Provider;

12

Customer type Information required Verification documentation Comments Attorney/Accountant/Auditor letter on

Attorney/Accountant/Auditor letterhead confirming the

address of the client;

Motor Vehicle registration/licence documents;

Physical site visit conducted for verification purposes; Trusts Trust name;

Trust number

Address of the Master of the High

Court where the trust is registered;

and

Particulars of names beneficiaries,

details of how the beneficiaries a

determined.

Letter of Authority/Authority by Master (for SA trusts);

Trust Deed; and

Resolution/mandate authorising the mandated officials

where available

Business address

Obtain Residential address

details of:

• Each trustee;

• Founder;

• Each named

beneficiary

• The mandated officials

authorised to establish

a business

Anyone of the following valid documents reflecting the clients’ name and physical address:

Utility bill (municipality water & lights account or Property

Managing Agent Statement;

Bank statement from the bank on an official bank

documentation/form;

Recent signed lease or rental agreement;

Municipal rates and taxes invoice

Telephone or cellular telephone account;

Official SARS document (Not E Filing documentation);

13

Customer type Information required Verification documentation Comments relationship or enter into a

transaction as per

resolution / signing instruction /

application form/mandate

Valid television licence

Television licence renewal confirmation letter;

Subscription TV (e.g. Multichoice) statement;

Home loan statement from the financial institution;

Long/short term insurance policy documents, from the

Financial Service Provider;

Attorney/Accountant/Auditor letter on

Attorney/Accountant/Auditor letterhead confirming the

address of the client;

Motor Vehicle registration/licence documents;

Physical site visit conducted for verification purposes;

The Income Tax registration number An official SARS document

Signature of IO…………………………… Date:…………………………..

Signature of RM……………………………. Date:…………………………….

ANNEXURE 11

BASIC ASSESSMENT REPORT

BASIC ASSESSMENT REPORT

Business Background:

Name of shareholder %age Shareholding Gender BEE Status

Include the following information:

Who owns the company (what is the percentage held by BEE)?

How old is the company?

What does the company do, or what are they intending to do?

Which sector are they operating in?

Who are the strategic partners?

Comment on profitability of the business (i.e. high level on turnover & profits achieved)

Strategic fit to mandate of sefa

Does the business qualify in terms of the sefa’s product and funding criteria:

What product are they applying for (i.e. is it a startup, expansion, etc.)

Do they meet the product financing criteria?

Funding Requirements:

Include the following information

What is the total funding requirement (total value of the project)?

How much is required from sefa? (if less that project value, who are the co-funders)

What is the purpose of the funding?

Proposed transaction structure?

Name of Investment Analyst:

Date: Click here to enter a date. Enquiry Number:

Name of Business:

(as it appears in company registration documents)

Name of Applicant:

Amount:

Product Type: Province: Choose an item.

How much is the applicant putting as contribution?

Source and Application of Funds

Source of Fund Amount Application of Fund

Commercial Viability

Include the following information:

What is the required period of funding?

Can the business repay the loan within at most 5 years (look at projected revenues and

compare to annual required repayment)?

If it’s an acquisition of equity, what is the P/E multiple that the business is being sold/bought

at (is the price negotiable?)

Consideration of competitive position of the project/company

Information on the target market, major competitors and the general norms of the industry

Has the applicant secured supply of key raw materials?

If it is a startup, has the applicant secured a market (i.e. off-take agreements, letters of

intent, etc.)?

If it is a contract, what is the duration of the contract?

Interpretation of the key ratios as per sefa FinModel (Excel) spreadsheet.

Proposed Security

Security type Value Lien

1.

2.

3.

4.

5.

6.

Developmental Impact:

Include the following information:

Number of new jobs that will be created?

Participation by black designated groups (i.e. youth, rural women & people with

disabilities)

Management Experience:

Name Responsibility/Position Qualifications Experience

Include the following information:

Brief biography of the proposed management team.

Will the applicants be operationally involved in the business?

Does management have relevant experience for the chosen business?

Recommendation

Make a recommendation based on the summary of the key points from the discussions above.

ANNEXURE 12

DUE DILIGENCE: PEER REVIEW GUIDELINES

DUE DILIGENCE: PEER REVIEW GUIDELINES

PEER REVIEW GUIDELINES

The condensed credit report submitted to sefa management places great responsibility on IO, RM and

HoR to ensure that the due diligence is thoroughly done, peer reviews are completed and that all

relevant key issues are communicated to the Credit Committees and the Board.

We all make mistakes. Any person no matter how experienced can make an error. In addition to this

there are a number of assumptions made in due diligence. It is therefore of paramount importance

to have somebody who had not been involved in the due diligence processes questioning the

assumptions and approaches.

A peer review offers opportunities for training and skills transfer. It also allows the team member(s)

the opportunity to get comfort on his/her work. It constitutes a form of self-regulation by these

members within the relevant field. It ensures that quality is improved and maintained. It improves

performance, and provide credibility.

It is essential to have a formal process in place for peer review to ensure consistency across all regions.

The RM could either nominate reviewers in the region or he/she will do the reviewing of the due

diligence him/herself. Peer review comments should be indicated in writing on the document being

reviewed. These comments must be placed on sefaLAS under documents and clearly marked due

diligence peer review for future reference.

Guidelines on Technical, Marketing and Financial review have been prepared to assist reviewers with

the process and are contained in the attached annexures.

Annexure A1 – Marketing Peer Review

Annexure A2 – Technical Peer Review

Annexure A3 – Financial Peer Review

Annexure A1

MARKETING PEER REVIEW

The important aspects to a marketing peer review is to ensure that the marketing submission has

logical consistency, makes overall sense, that key issues have been addressed, that the paragraph has

been well written and clearly spells out the issues.

The reviewer should focus on the following:

AREAS OF ASSESSMENT Y/N

1. Does the report seek to illustrate and demonstrate the marketing and sales strategies of the business, customer analysis, competitive analysis and the industry analysis?

2. Reasonability of sales volumes and prices.

3. Projections are well motivated.

4. The logic of the approach to the projections.

5. Marketing of the client has been thought through and is constituent with the projections.

6. Appropriateness of the product mix.

7. Historical sales have no unexplained/unreasonable fluctuations.

8. Appropriateness and adequacy of the marketing costs.

9. Positioning of the product is clear and the product use is understood.

10. Understanding of the product demand, niche, alternative products.

11. Assessment of management’s ability to adhere to projections.

12. Have there been sufficient research done and is the projections and the projections discussions consistent with the research.

13. Were the projections done independently taking into consideration all the available information?

14. Is an understanding of the market displayed?

15. Is analysis of historical sales consistent with projections?

16. Were negative/positive items independently confirmed and are they reflected in the projections and the report?

17. Are negative/positive marketing issues highlighted in the body of the report?

18. Does marketing annexures capture the relevant information?

19. Has support documentation been obtained and stored.

Investment Officer Regional Manager

……………………………….. ………………………………..

Annexure A2

TECHNICAL PEER REVIEW

The review process entails ensuring that the technical submission has logical consistency, makes

overall sense, that the key issues have been addressed and that the correct process of assessment has

been followed.

In this section the reviewer should ensure the manufacturing and production processes, the energy

requirements, quality control and supplier analysis are adequately addressed in the report.

The reviewer should consider that the following key points are adequately addressed:

AREAS OF ASSESSMENT Y/N

1. SITE AND BUILDING

Hire and ownership considerations.

Conflict of interest issues (shareholders are site owners).

Reasonability of sited related costs.

Physical location/

Site relevance to the project or expansion.

Availability of support services.

Environmental issues.

Should a new site and/or building be required, ensure the following issues have also been addressed:

Legalities around land ownership (land claims) and transfer of ownership.

Reasonability of cost estimates (building, site and services).

Have expert services been used for cost estimates where necessary.

2. PROCESS (MANUFACTURING/SERVICE)

The process description contains a logical and consistent description of the conversion of raw materials into products. Key conversion points and parameters such as flow rates, temperatures and pressures should be highlighted.

Applicability of the proposed technology.

Process ownership (Intellectual Property) issues and associated costs (royalties) are addressed.

The value service value chain captures the life cycle wide considerations from sourcing through to customer use, after sales support and on to end life cycle disposition.

Environmental, health and safety are addressed and key issues highlighted (including legal and legislative issues).

3. PROCESS EQUIPMENT

Local/import supply and key forex issues.

Reputable suppliers.

Equipment capacity match with projected requirements.

Reasonability and comprehensiveness of CAPEX cost estimates.

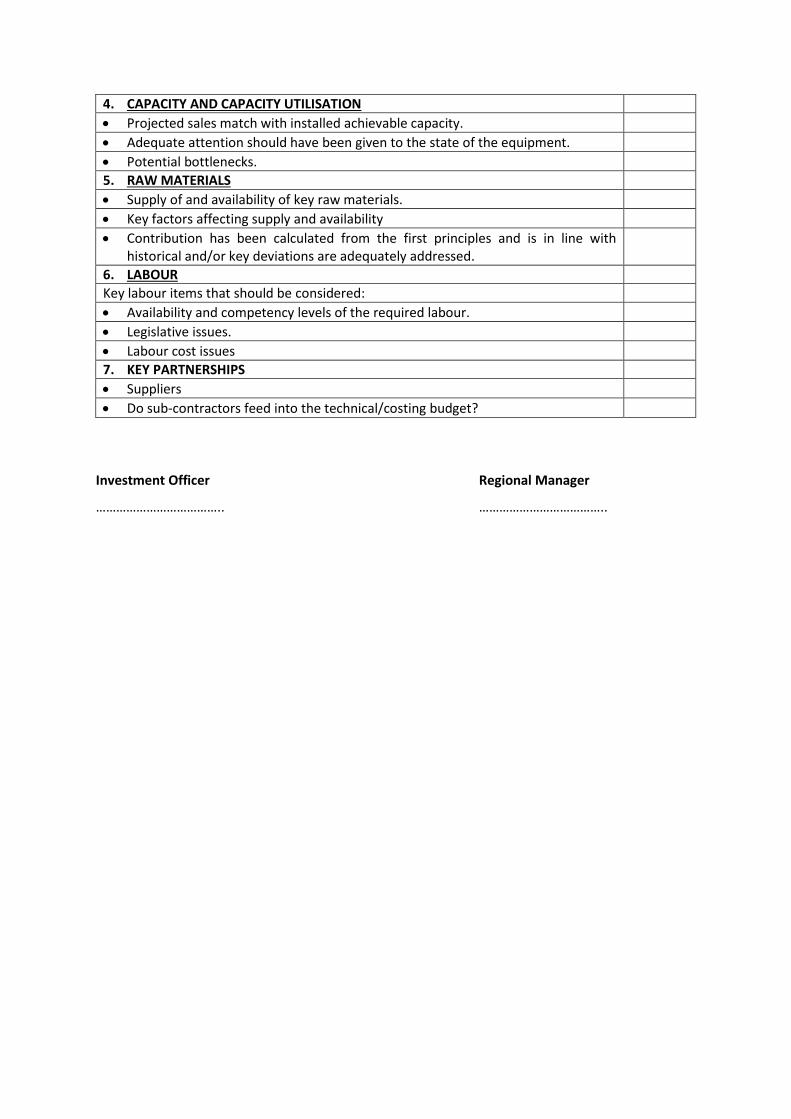

4. CAPACITY AND CAPACITY UTILISATION

Projected sales match with installed achievable capacity.

Adequate attention should have been given to the state of the equipment.

Potential bottlenecks.

5. RAW MATERIALS

Supply of and availability of key raw materials.

Key factors affecting supply and availability

Contribution has been calculated from the first principles and is in line with historical and/or key deviations are adequately addressed.

6. LABOUR

Key labour items that should be considered:

Availability and competency levels of the required labour.

Legislative issues.

Labour cost issues

7. KEY PARTNERSHIPS

Suppliers

Do sub-contractors feed into the technical/costing budget?

Investment Officer Regional Manager

……………………………….. ………………………………..

Annexure A3

FINANCIAL PEER REVIEW

The review process entails checking all financial budget annexures including balance sheet, income

statement, and cash flow projections for both technical correctness and logistical and reasonability of

assumptions. It requires checking of the financial considerations for completeness and correctness.

Technical Correctness:

The reviewer seeks to evaluate if the report demonstrate the financial management, controls and the

analysis of the financial statements and projected financial information is a true reflection of the

information provided by the applicant. The following should be checked:

AREAS OF ASSESSMENT Y/N

Balance Sheet

1. Increases in fixed assets reflect correctly.

2. Accumulated depreciation adds correctly and re-investment correctly applied.

3. Treatment of investment and other long-term assets such as patents and/or, trademarks are treated correctly.

4. Working capital levels compute correctly.

5. Treatment of factored debtors correct.

6. Treatment of other short-term assets – e.g. VAT receivable.

7. Treatment of other short-term liabilities – e.g. VAT payable.

8. Calculation of long-term liabilities.

9. Calculation of short-term portion of long-term liabilities.

10. Treatment of shareholders’ loans and other quasi equity.

11. Treatment of deferred tax.

12. Equity and changes in equity.

13. Peak calculation.

14. Ratio calculations.

Income Statement

1. All line items to be checked for mathematical correctness.

2. Ratio calculations.

3. Treatment of extra-ordinary items

4. Correct application of seasonality.

Cash Flow Statement/Projections

1. Are the assumptions realistic?

2. Accuracy of forecasts against actual for the past 2 years.

3. Treatment of the funds inflow/outflow.

4. All lines should be checked to ensure that assumptions are correctly applied.

Investment Officer Regional Manager

……………………………….. ………………………………..

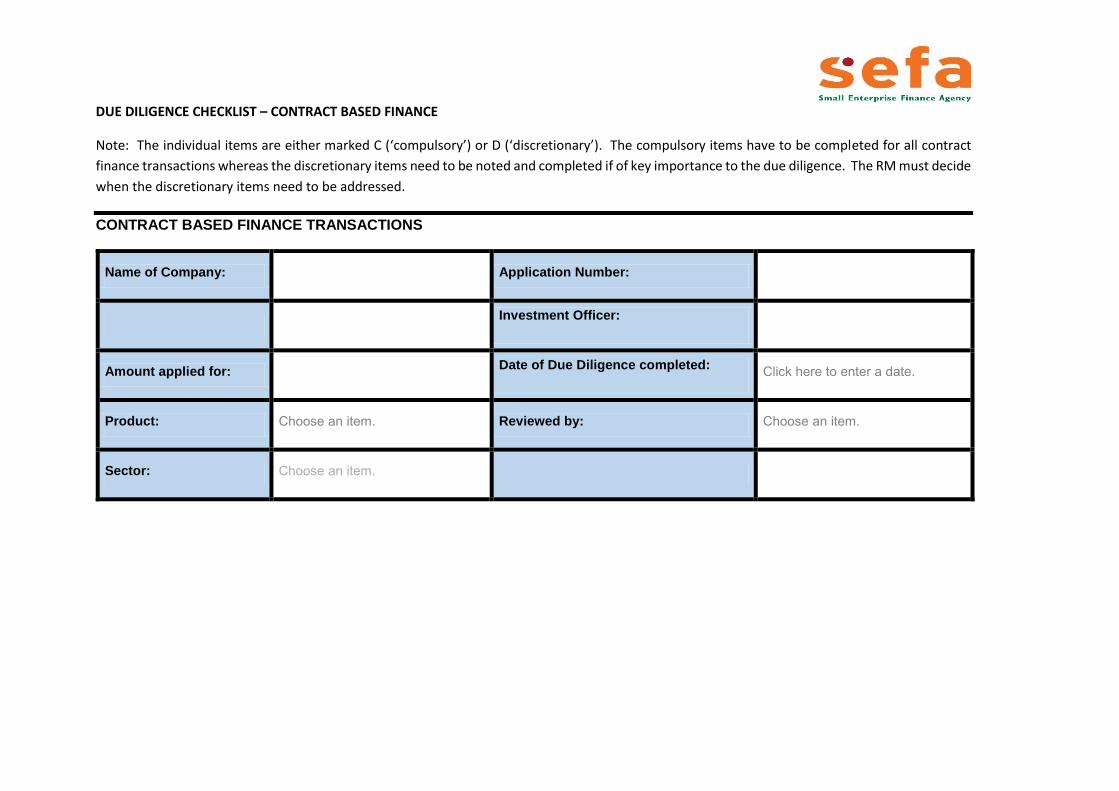

ANNEXURE 13

DUE DILIGENCE: CONTRACT BASED FINANCE

CHECKLIST

DUE DILIGENCE CHECKLIST – CONTRACT BASED FINANCE

Note: The individual items are either marked C (‘compulsory’) or D (‘discretionary’). The compulsory items have to be completed for all contract

finance transactions whereas the discretionary items need to be noted and completed if of key importance to the due diligence. The RM must decide

when the discretionary items need to be addressed.

CONTRACT BASED FINANCE TRANSACTIONS

Name of Company: Application Number:

Investment Officer:

Amount applied for: Date of Due Diligence completed: Click here to enter a date.

Product: Choose an item. Reviewed by: Choose an item.

Sector: Choose an item.

AREA OF ASSESSMENT (C/D) Y/N Comment

1. INSTITUTIONAL & GOVERNANCE DISCIPLINE

Review signed audited Annual Financial Statements for the past two years.

C

Review the auditor’s report for the past 2 years and identify any issues giving rise to concern or qualification.

C

Assess reliability of management accounts and determine

if they are prepared on a consistent basis with that of the Annual Financial Statements.

C

Determine that compliance with internal control with policies and procedures are enforced.

C

Discuss the list/structure of subsidiaries, associated companies and other interests held by the company, target company or any of its directors in other companies or businesses (including JV’s, partnerships, consortiums, or other profit sharing arrangements).

C

Review the following information: - Certified ID copies of all relevant parties in the

transaction - Income Tax & VAT Registration - UIF registration - PAYE, SDL registration - Proof of residence of all relevant parties in the

transaction.

C

2. LEGAL & REGULATORY DISCIPLINE

Peruse contract for all authorising signatures. Check all pages are initialled.

C

Obtain letter of appointment with matching signatures. C

What is the commencement date of the contract? C

What is the completion date of the contract? C

AREA OF ASSESSMENT (C/D) Y/N Comment

Is the applicant the main contractor or a sub-contractor? C

Does the contract allow the main contractor to sub-contract work?

C

What is the percentage of work that is being sub-

contracted? C

Conduct internet search, where the tender was a public tender and published in the newspaper.

C

Conduct background check on National Treasury to verify that the contractor and/or sub-contractor is not blacklisted.

C

Check whether the appeal period has lapsed and whether

there are contractors contesting the award. C

Give background to the awarding of the contract. Unpack purpose for the award e.g. the contract is awarded as part of the government’s poverty alleviation initiatives which includes providing nutrition to schools in rural areas.

C

Detail process followed in awarding the contract. C

Basis of revenue – Based on completion of set milestones per the bill of

quantities. Revenue will be earned on completion of the project. On a monthly basis based on site progress.

C

Does the contract make provision for variations in the value?

C

Is the value fixed for the duration of the contract? C

Highlight penalties applicable under the contract C

Submit detailed project plan with payment terms from the debtors.

C

AREA OF ASSESSMENT (C/D) Y/N Comment

Value of the contract must be matched to the projections. C

Payment terms must match projected cash flow statement. C

Discuss possibility of extending the contract. C

3. TECHNICAL DISCIPLINE

Does the company comply with regulatory standards within the industry they operate in? C

What accreditation is required under the contract e.g. CIDB grading, ISO standards, SABS approval where applicable. C

Obtain list and value of projects previously completed by the company. C

Obtain certificates of completion for previous work done by the company C

Give description of assets required under the contract?

Give description on condition of existing assets that will be used in the execution of the contract.

C

Give profile of key suppliers, their terms and provide a supplier agreement where applicable.

C

List and profile key staff involved in the project. Provide

details on their qualifications, experience and time at the business.

C

Test capacity of the business if the business is currently executing multiple contracts.

C

Are there other contracts underway? C

How have the other contracts been financed? C

AREA OF ASSESSMENT (C/D) Y/N Comment

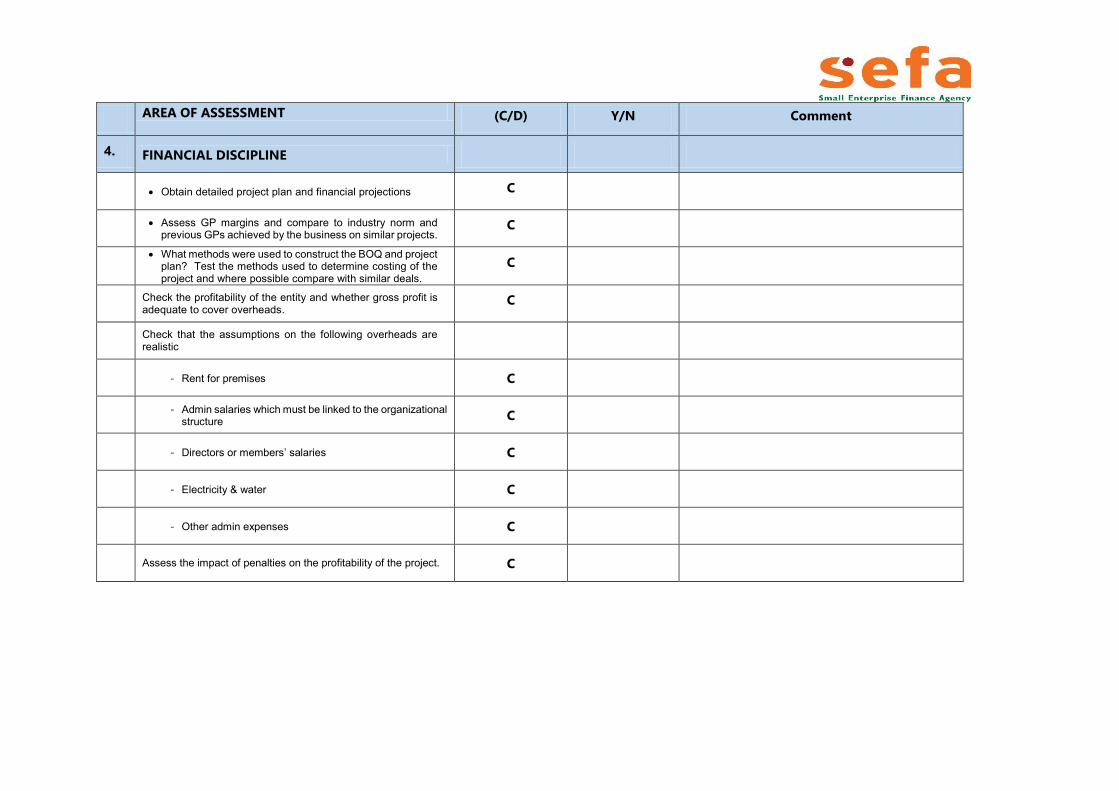

4. FINANCIAL DISCIPLINE

Obtain detailed project plan and financial projections C

Assess GP margins and compare to industry norm and previous GPs achieved by the business on similar projects.

C

What methods were used to construct the BOQ and project

plan? Test the methods used to determine costing of the project and where possible compare with similar deals.

C

Check the profitability of the entity and whether gross profit is adequate to cover overheads.

C

Check that the assumptions on the following overheads are realistic

- Rent for premises C

- Admin salaries which must be linked to the organizational

structure C

- Directors or members’ salaries C

- Electricity & water C

- Other admin expenses C

Assess the impact of penalties on the profitability of the project. C

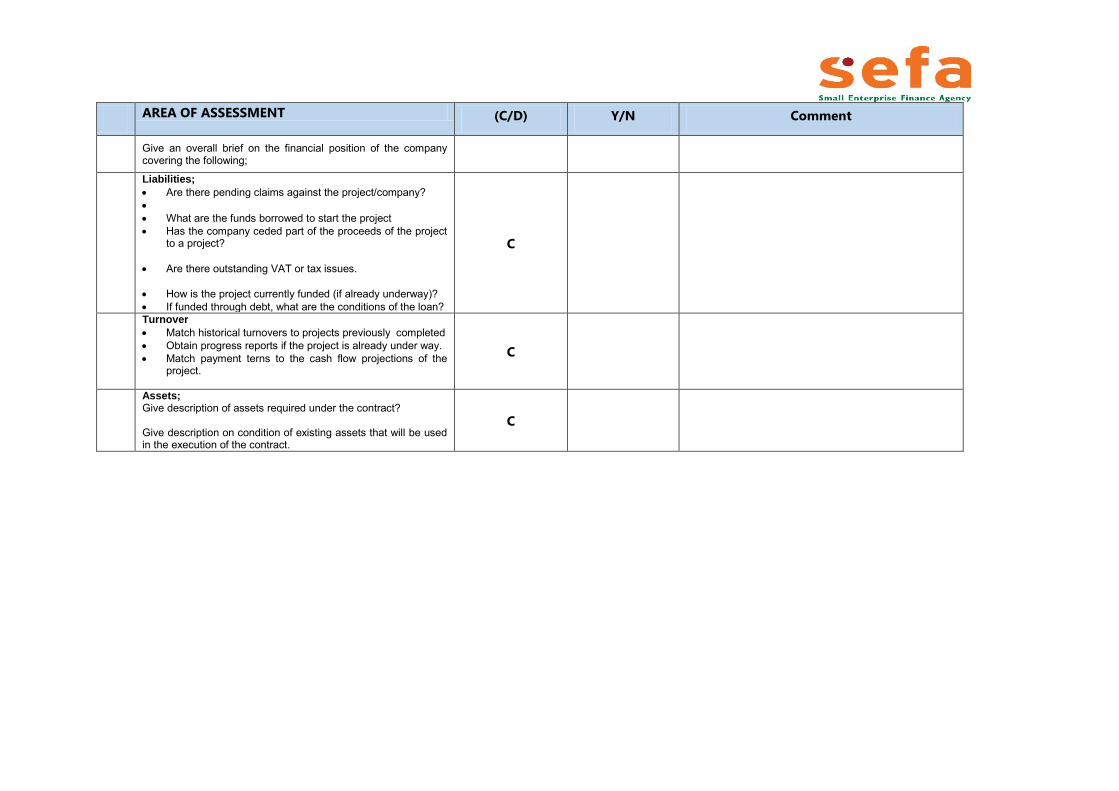

AREA OF ASSESSMENT (C/D) Y/N Comment

Give an overall brief on the financial position of the company covering the following;

Liabilities;

Are there pending claims against the project/company? What are the funds borrowed to start the project Has the company ceded part of the proceeds of the project

to a project? Are there outstanding VAT or tax issues. How is the project currently funded (if already underway)? If funded through debt, what are the conditions of the loan?

C

Turnover

Match historical turnovers to projects previously completed Obtain progress reports if the project is already under way. Match payment terns to the cash flow projections of the

project.

C

Assets; Give description of assets required under the contract? Give description on condition of existing assets that will be used in the execution of the contract.

C

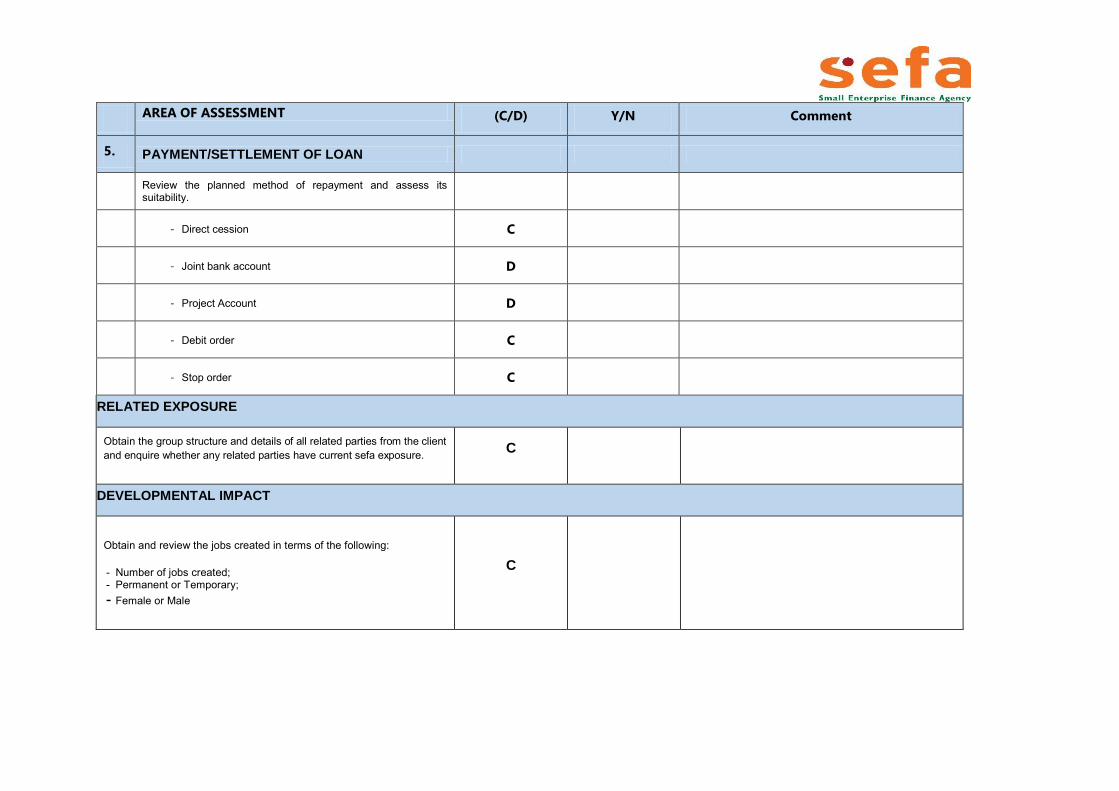

AREA OF ASSESSMENT (C/D) Y/N Comment

5. PAYMENT/SETTLEMENT OF LOAN

Review the planned method of repayment and assess its suitability.

- Direct cession C

- Joint bank account D

- Project Account D

- Debit order C

- Stop order C

RELATED EXPOSURE

Obtain the group structure and details of all related parties from the client and enquire whether any related parties have current sefa exposure. C

DEVELOPMENTAL IMPACT

Obtain and review the jobs created in terms of the following:

- Number of jobs created; - Permanent or Temporary; - Female or Male

C

AREA OF ASSESSMENT (C/D) Y/N Comment

On labour provide the following; No of labour employed; How is the labour sourced; Is there special skills required; Labour rates;

C

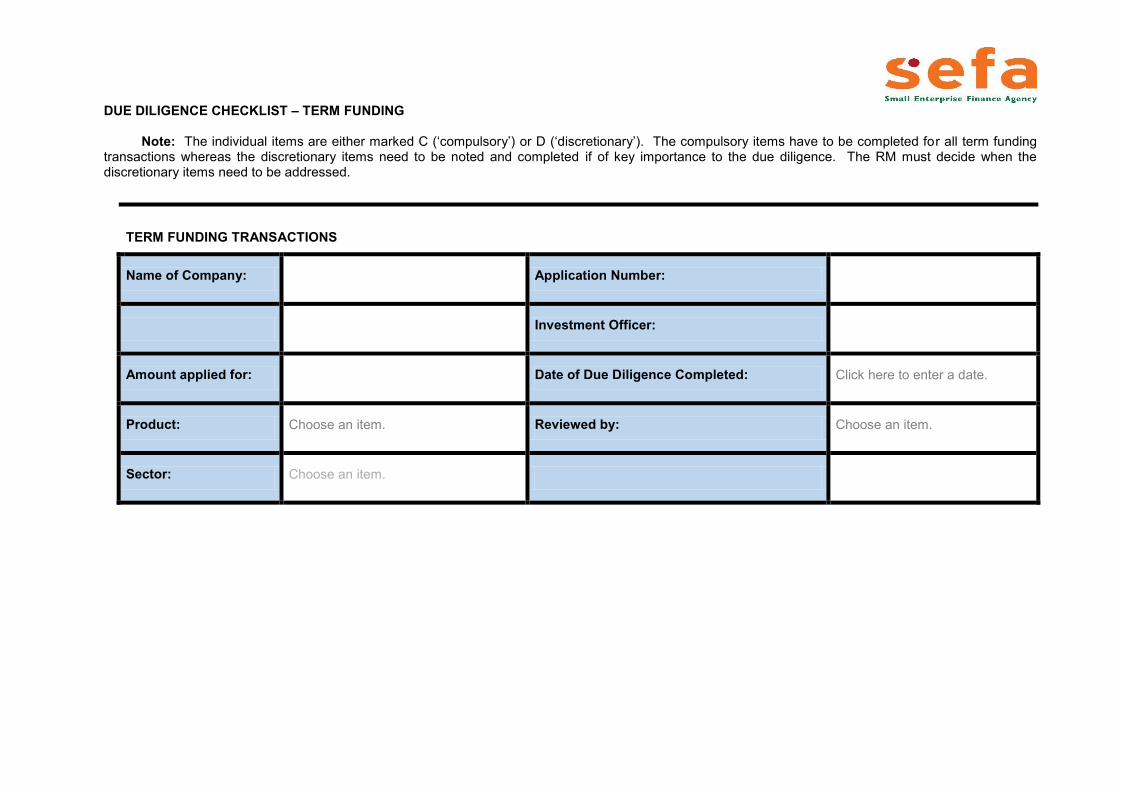

ANNEXURE 14

DUE DILIGENCE: TERM FUNDING CHECKLIST

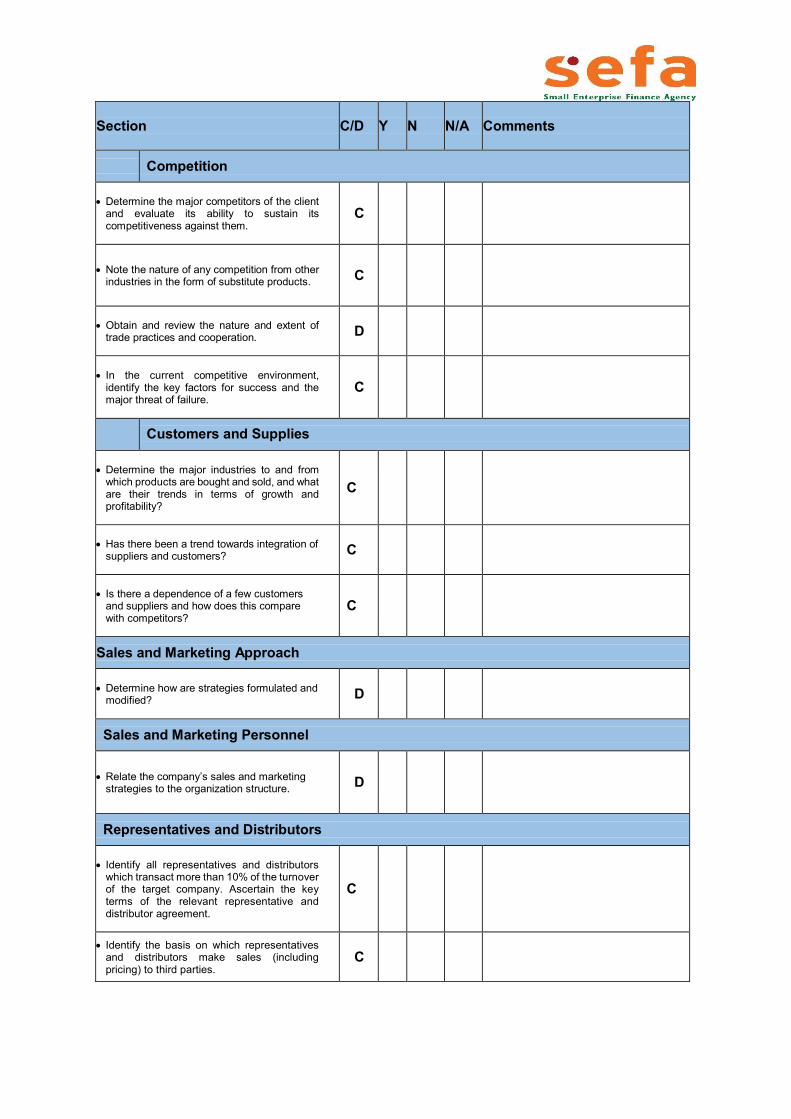

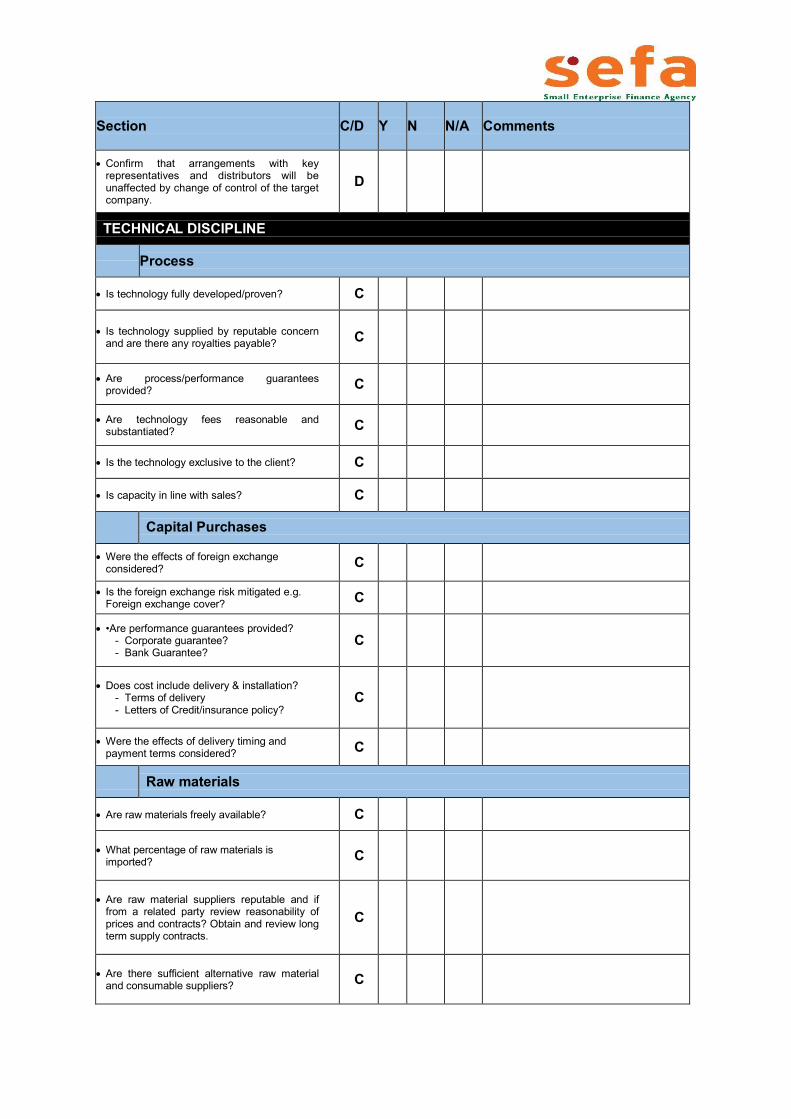

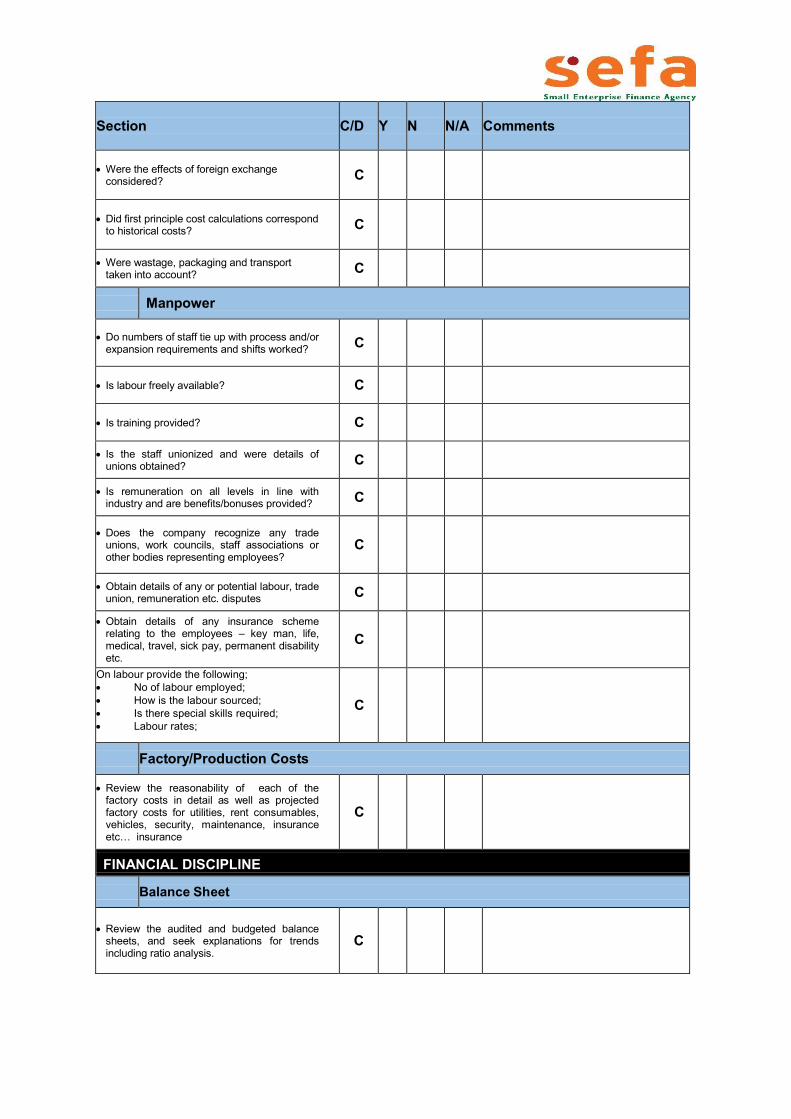

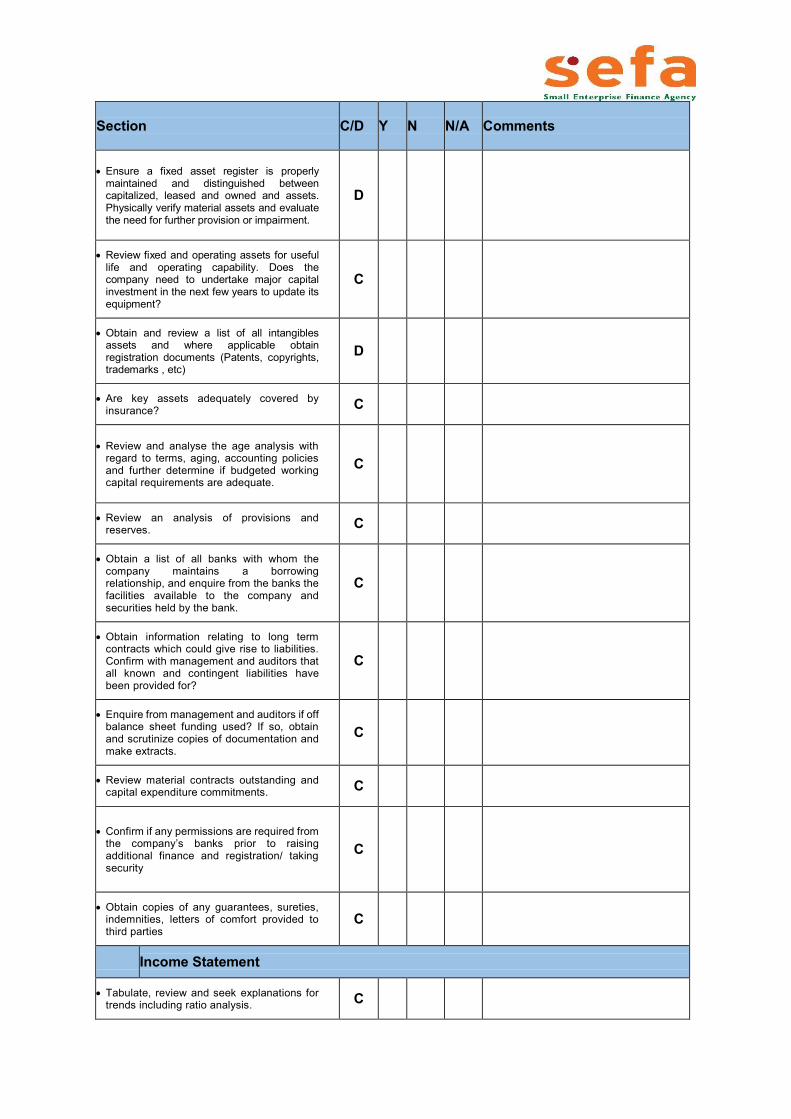

DUE DILIGENCE CHECKLIST – TERM FUNDING

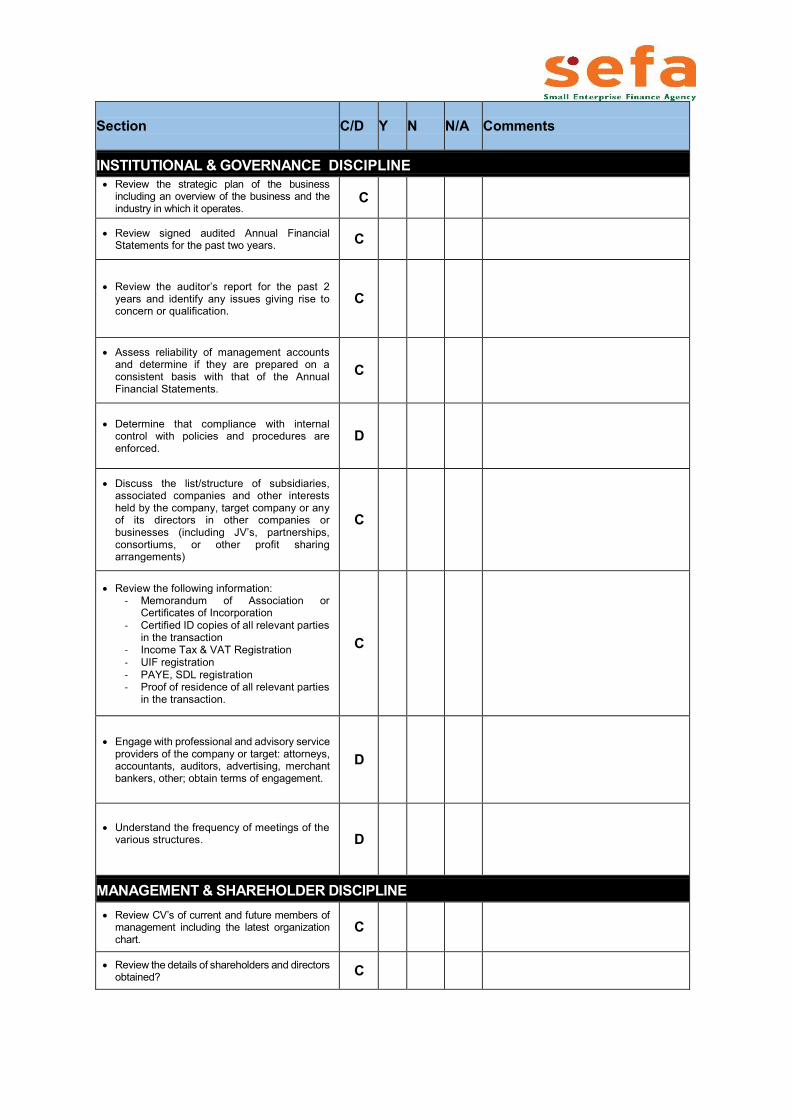

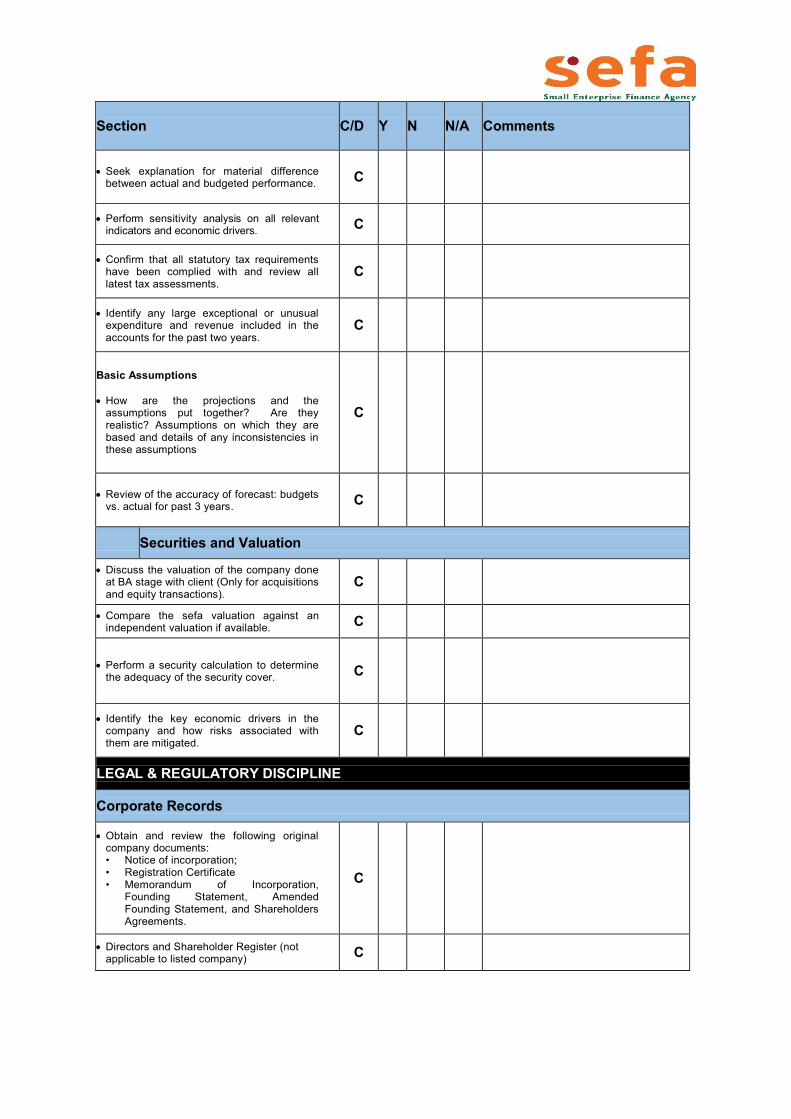

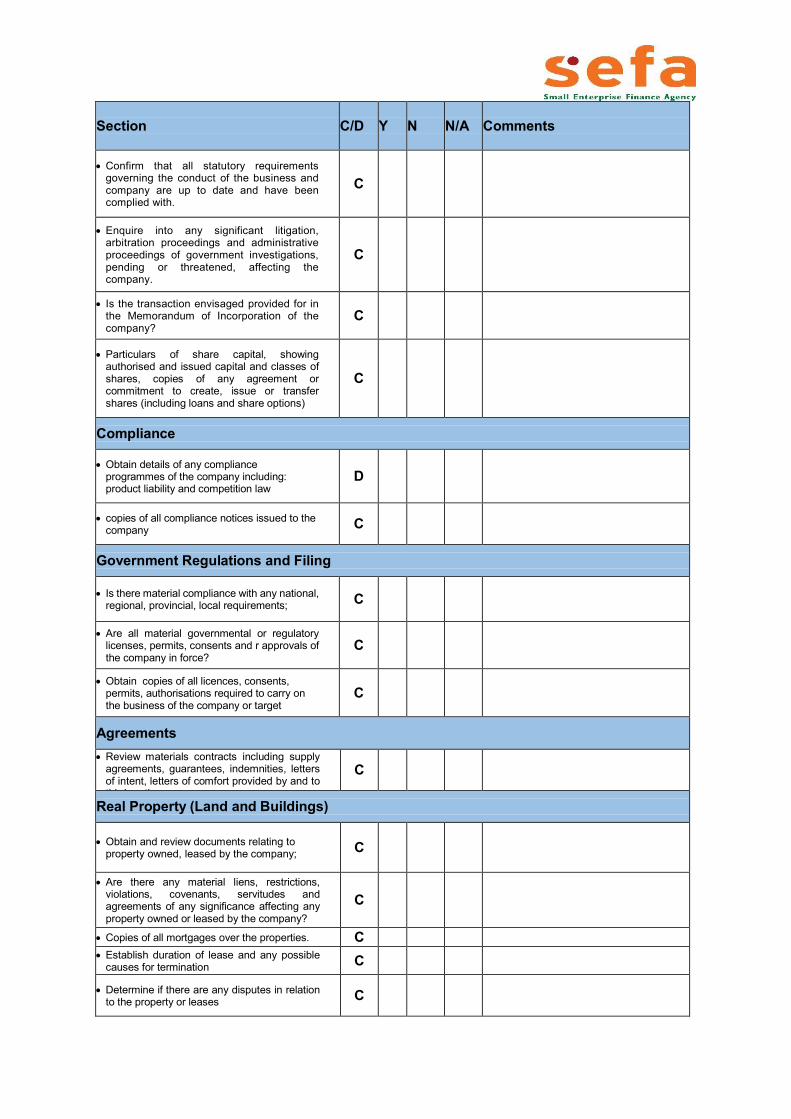

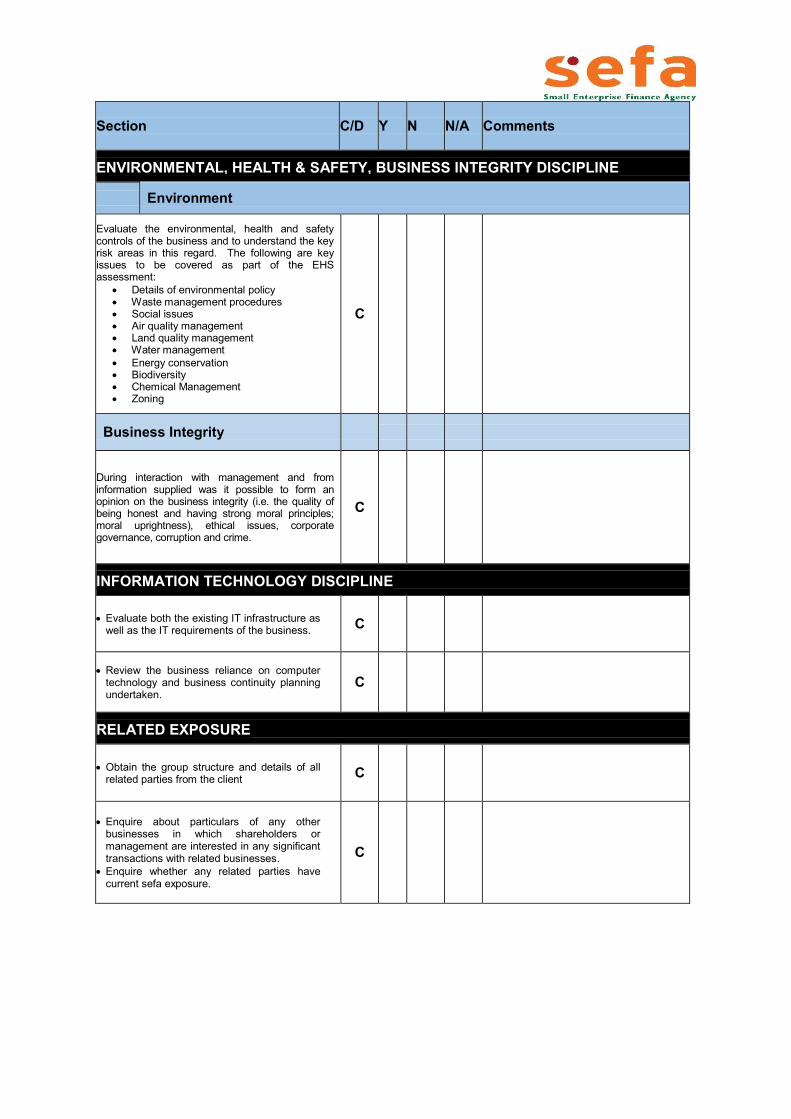

Note: The individual items are either marked C (‘compulsory’) or D (‘discretionary’). The compulsory items have to be completed for all term funding transactions whereas the discretionary items need to be noted and completed if of key importance to the due diligence. The RM must decide when the discretionary items need to be addressed.

TERM FUNDING TRANSACTIONS

Name of Company: Application Number:

Investment Officer:

Amount applied for: Date of Due Diligence Completed: Click here to enter a date.

Product: Choose an item. Reviewed by: Choose an item.

Sector: Choose an item.

DUE DILIGENCE CHECKLIST – TERM FUNDING

CONTENTS:

INSTITUTIONAL & GOVERNANCE DISCLIPLINE

MANAGEMENT & SHAREHOLDER DISCIPLINE

MARKETING DISCIPLINE

TECHNICAL DISCIPLINE

FINANCIAL DISCIPLINE

LEGAL & REGULATORY DISCIPLINE ENVIRONMENTAL, HEALTH & SAFETY, BUSINESS INTEGRITY DISCIPLINE INFORMATION TECHNOLOGY DISCIPLINE

RELATED PARTY EXPOSURE DEVELOPMENTAL IMPACT

Section C/D Y N N/A Comments

INSTITUTIONAL & GOVERNANCE DISCIPLINE Review the strategic plan of the business

including an overview of the business and the industry in which it operates.

C

Review signed audited Annual Financial Statements for the past two years. C

Review the auditor’s report for the past 2 years and identify any issues giving rise to concern or qualification.

C

Assess reliability of management accounts and determine if they are prepared on a consistent basis with that of the Annual Financial Statements.

C

Determine that compliance with internal control with policies and procedures are enforced.

D

Discuss the list/structure of subsidiaries, associated companies and other interests held by the company, target company or any of its directors in other companies or businesses (including JV’s, partnerships, consortiums, or other profit sharing arrangements)

C

Review the following information: - Memorandum of Association or

Certificates of Incorporation - Certified ID copies of all relevant parties

in the transaction - Income Tax & VAT Registration - UIF registration - PAYE, SDL registration - Proof of residence of all relevant parties

in the transaction.

C

Engage with professional and advisory service providers of the company or target: attorneys, accountants, auditors, advertising, merchant bankers, other; obtain terms of engagement.

D

Understand the frequency of meetings of the various structures.

D

MANAGEMENT & SHAREHOLDER DISCIPLINE Review CV’s of current and future members of

management including the latest organization chart.

C

Review the details of shareholders and directors obtained? C

Section C/D Y N N/A Comments

Review the percentage ownership or potential ownership each member of the management team have?

C

Are there any loans to and from management or key shareholders? C

During interaction with management and from information supplied was it possible to form an opinion on the capability of management with regards to general administrative abilities, technical know-how, financial know how, marketing knowledge and human resource management?

C

What changes have there been in the management group in the last three years? C

Have any managerial shortfalls been identified and have these been addressed? C

• Is a succession plan in place? D

Are key man policies required and in place? C

Obtain sworn personal balance sheets of shareholders. C

Review the present salary level of management, any kind of incentive compensation, any employment contracts in place?

C

MARKETING DISCIPLINE

Review industry information to assess the current and potential growth prospects of the market in which the client operates.

C

What does the product do for its users? How does it work? What need does the product fill for its user? Is the need real, created, or imagined?

C

Review the monthly historical sales of existing products (Rand & Volumes) per major product category.

C

Review list of major customers and contact details. C

Status report of potential customers under negotiations and details of key contacts. C

Review monthly budgeted sales (Rand and Volumes) per major product category for the present financial year, including latest management account figures.

C

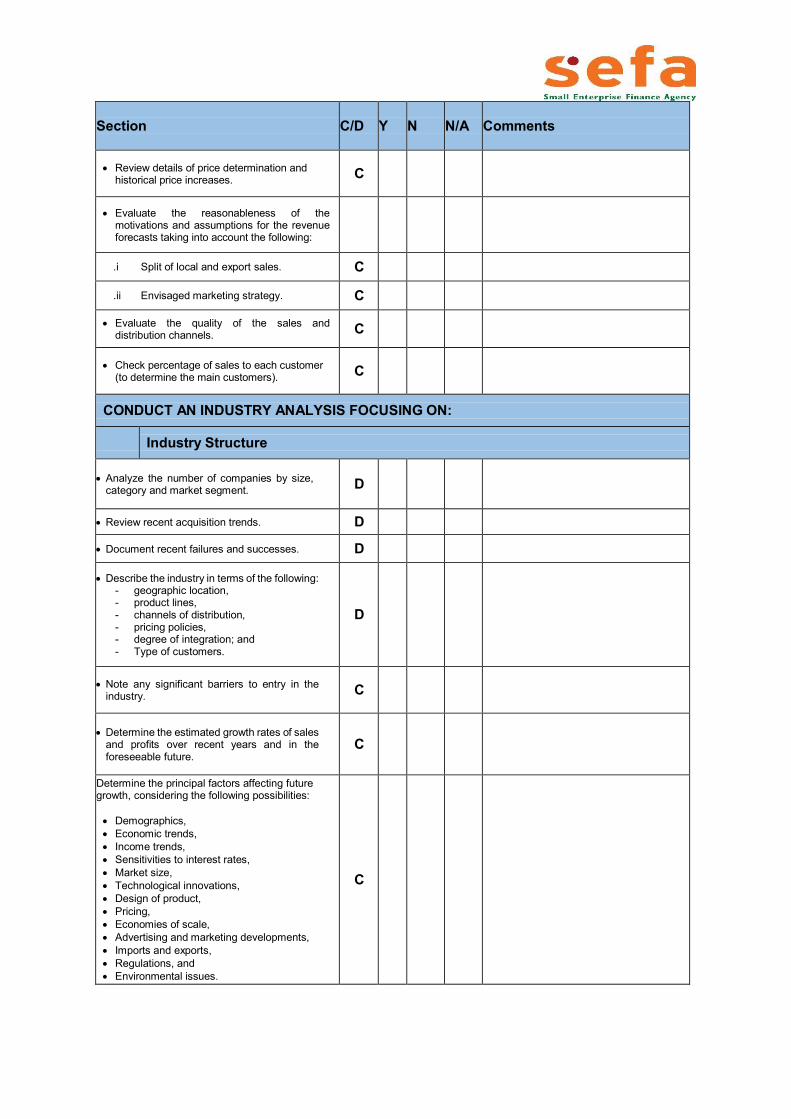

Review list of outstanding orders on hand. C