Internal Audit Report - BoardDocs

27

Page | 1 Internal Audit Report Audit of High School Cash Receipts and Change Funds October 1, 2013 Wayland E. Mueller, CPA, CIA – Internal Auditor Internal Audit No. 2013-3 Kraft Administrative Center, 1359 E. St. Louis St., Springfield, MO 65802 www.springfieldpublicschoolsmo.org

Transcript of Internal Audit Report - BoardDocs

Page | 1

Internal Audit Report

Audit of High School Cash Receipts and Change Funds

October 1, 2013

Wayland E. Mueller, CPA, CIA – Internal Auditor

Internal Audit No. 2013-3

Kraft Administrative Center, 1359 E. St. Louis St., Springfield, MO 65802 www.springfieldpublicschoolsmo.org

Page | 2

TABLE OF CONTENTS TRANSMITTAL LETTER .................................................................................................................................. 3 AUDIT PURPOSE................................................................................................................................................ 4 BACKGROUND .................................................................................................................................................. 4 AUDIT RATING .................................................................................................................................................. 5 AUDIT SCOPE AND METHODOLOGY ............................................................................................................. 5 FINDINGS .............................................................................................................................................................. 6 APPENDIX A: AUDIT RATING DEFINITIONS .............................................................................................. 19 APPENDIX B: BOARD POLICIES RELEVANT TO THIS AUDIT ................................................................. 20 APPENDIX C: TIMELINESS OF REMOTE CAPTURE CHECK DEPOSITS ................................................. 21 APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS ............................................................ 23

We Exist for the Academic Excellence of All Students

Wayland E. Mueller, CPA, CIA – Internal Auditor

KRAFT ADMINISTRATIVE CENTER

1359 E. SAINT LOUIS STREET - SPRINGFIELD, MISSOURI 65802-3409 - TELEPHONE 417/523-0679 Page | 3

TRANSMITTAL LETTER October 1, 2013 Board of Education School District of Springfield R-XII Springfield, Missouri I have completed internal audit number 2013-3, “Audit of High School Cash Receipts and Change Funds.” The purpose of the audit was to examine the cash receipts process and the related controls over change funds at each of the five district high schools, and provide the district with recommendations in order to improve the operational effectiveness, efficiency, and security of these activities. The scope of this audit was limited to the fiscal 2013 cash receipts and change fund activities occurring at the district’s high school finance offices. I conducted this audit in accordance with the standards applicable to performance audits contained in Government Auditing Standards, issued by the Comptroller General of the United States of America. Those standards require that I plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for my findings and conclusions based on the audit objective. I believe that the evidence obtained provides a reasonable basis for my findings and conclusions based on the audit objective. The findings in this report were reviewed by the district’s management, and their responses are included in this report. I appreciated management’s cooperation and assistance throughout this audit. Respectfully submitted,

Wayland E. Mueller, CPA, CIA Internal Auditor

Page | 4

AUDIT PURPOSE In accordance with the Internal Audit Work Plan for fiscal year 2013, as approved by the Board of Education on October 16, 2012, I designed this audit for the purposes of examining the controls over high school cash receipts and change funds. I developed the objective of this audit and my audit procedures based in part on the concerns noted in State Auditor’s Finding No. 2, “Accounting Controls over Cash Receipts and Change Funds,”1 and on other areas I noted during my risk assessment. The objective of this audit was to examine the cash handling procedures at the five district high schools to determine if existing internal controls are properly designed and if these controls are effective in achieving the goals of safeguarding monies collected, properly processing cash receipts, and properly managing change funds.

BACKGROUND The district’s high schools serve as collection points for various types of fees and other revenues. Examples of the types of fees and revenues collected include:

Parking fees Student athletic and activity participation fees Course fees Transcript fees Library fines and lost book fees Student activity fundraisers and dues (clubs, athletics, etc.) Yearbook sales Dance ticket sales Athletic event ticket sales Athletic event concessions sales Cafeteria sales

At each high school various individuals are involved in the collection activities. Eventually, most of the types of revenues listed above are processed for deposit by the school’s finance secretary. Concessions and athletic event ticket revenues are the responsibility of the schools’ concessions managers and ticket managers, respectively. Cafeteria managers are responsible for the cafeteria collections. Concessions, athletic event revenues, and cafeteria collections were not examined in this audit. The district finance department also performs some monitoring activities to aid in the proper recording of the deposits made by each school. The finance department serves as a resource to the high school finance secretaries by providing training and guidance on cash receipting procedures.

1 “Management Advisory Report No. 2012-16,” Missouri State Auditor, < www.auditor.mo.gov>, p.7, accessed on January 14, 2013.

Page | 5

AUDIT RATING The rating system described in Appendix A was used to describe the effectiveness of the high schools’ performance as related to the audit objective. Audit tests were designed to provide a reasonable basis for my rating. Although important new controls have been implemented since the release of the State Audit in March 2012, I believe the findings described later in this report confirm my overall rating of “IMPROVEMENT NEEDED.” Based on my work performed at each high school, I observed a widespread understanding of the importance of proper cash handling procedures, and an adequate level of compliance with policies and procedures. However, I also observed several areas where improvements can be made. These are listed in the “Findings” section of this report.

AUDIT SCOPE AND METHODOLOGY This audit consisted of an examination of the system of internal controls in place to safeguard and appropriately deposit cash collections at the district’s five high schools. Excluded from the scope of this audit were the cafeteria collections, and the concessions and athletic event collections. For the purposes of this audit, “cash” is defined as currency, coins, checks, and money orders. The audit included tests of controls, inquiries of district employees, examinations of receipt books, parking registration forms, bank deposit forms, bank deposit activity records, and other audit procedures considered necessary to form the basis of my conclusions. I conducted the audit in accordance with the standards applicable to performance audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that I plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for my findings and conclusions based on the audit objective. I believe that the evidence obtained provides a reasonable basis for my findings and conclusions based on the audit objective. The audit is considered a performance audit. As defined by Government Auditing Standards, “performance audits provide objective analysis to assist management and those charged with governance and oversight in using the information to improve program performance and operations.”2 For this audit, the program being assessed is the district’s activities involving the management of change funds and the collecting and depositing of cash receipts through the finance office of each high school.

2 “Government Auditing Standards, December 2011 Revision,” U.S. Government Accountability Office (GAO), http://www.gao.gov/assets/590/587281.pdf , p. 17, accessed on January 14, 2013.

Page | 6

FINDINGS Finding 1 – Unauthorized Change Funds

Criteria – All change funds at the high schools should be authorized, monitored, and accounted

for through the district’s centralized accounting function. According to the State Audit, “written policies should be established outlining the procedures for maintaining, using, and accounting for change funds.” 3

Condition – The finance department maintains a list of authorized high school change funds, and the list details the authorized amounts for these change funds. During the course of my audit, I noted unauthorized change funds at Central High School, Kickapoo High School, Hillcrest High School, and Parkview High School. Several of these unauthorized change funds also did not maintain constant balances. All of these change funds were small, with balances less than $100.

Cause – The finance department has done considerable work to develop a list of authorized change funds, and to ensure that this list reconciles to the general ledger. However, some confusion remains at the high school sites concerning the proper management of change funds. As the need, or perceived need, for a change fund is identified by school staff, a common practice is for the site to create one by not depositing all collections as received, but instead retaining a small portion of these collections in a change fund.

Effect – Without proper oversight of change funds, the district is exposed to the risk that change funds will not be appropriately safeguarded from theft and/or misuse.

Recommendation – Management should update the high school site Financial Handbooks and the Administrative Practices and Procedures Manual to include a description of the proper procedures to maintain, use, and account for change funds. Also, at each high school, the building principal should coordinate with the finance secretary and the central office finance department to identify all unauthorized change funds located within their school. Once identified, management should determine if these unauthorized change funds are necessary. Newly identified change funds that are deemed necessary should be added to the approved list of change funds to be monitored by the finance department. All change funds considered unnecessary should be deposited at the district’s bank. Finally, management should perform periodic cash counts of the authorized change funds to provide assurance that these funds are being managed properly.

Management’s Response – Management concurs with the audit recommendations. Processes will be structured as soon as possible to meet these recommendations with a target completion date of January 2, 2014. Management will develop a work team to review the audit recommendations, develop processes for meeting those recommendations, develop/enhance training if needed and make policy recommendations where appropriate. The Financial Handbooks and Administrative Practices and Procedures Manual will be updated based on these recommendations.

3 “Management Advisory Report No. 2012-16,” Missouri State Auditor, < www.auditor.mo.gov>, p.13, accessed on January 14, 2013.

Page | 7

Finding 1 – Unauthorized Change Funds (continued)

Management’s Response (continued) –

At the annual secretary orientation each of the last two years, the Finance Department requested to be notified of all change funds and addressed the proper use of change funds. This will continue to be performed at each annual secretary orientation. Once the work team has completed the review, the Finance Department will send an email to all staff reminding them of proper cash handling procedures and to notify Finance of any change funds.

Page | 8

Finding 2 – Timeliness of Deposits

Criteria – According to Board Policy DG, all funds received by the school district “shall be deposited within 24 hours of receipt.”

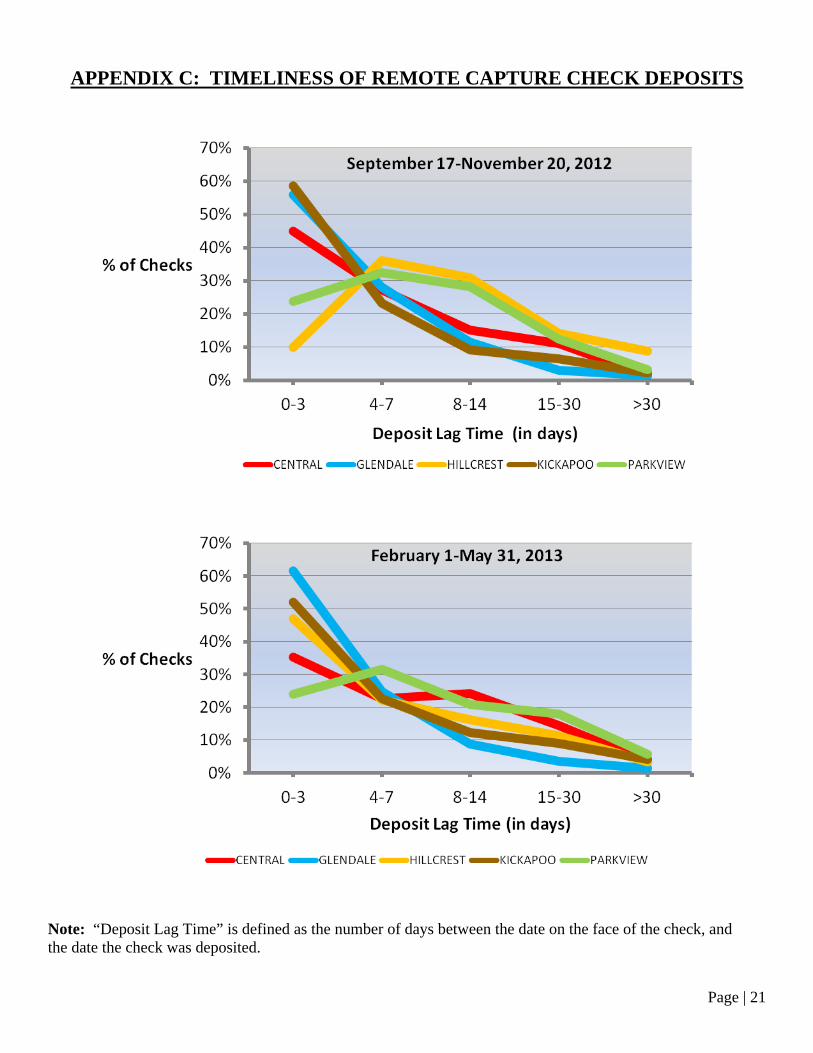

Condition – As evidenced by my review of the deposit activity at the district’s high schools, compliance with Board Policy DG needs improvement. To test the schools’ compliance with the requirement to make timely deposits, I reviewed every remote capture deposit of checks made by the high school finance secretaries for two different time periods during fiscal 2013. The remote deposit capture process allows the schools to scan images of checks directly to the bank for deposit, instead of using the traditional method of sending the checks to the bank with a courier. Since the images of the deposited checks were available to me through online access, I was able to view images of the deposited checks, and compare the dates on the checks to the deposit dates at the bank. The two time periods I selected to examine were: September 17, 2012 through November 20, 2012 (“fall”), and February 1, 2013 through May 31, 2013 (“spring”). During the fall period, 3,768 checks were deposited by the high school finance secretaries using the remote capture process. A total of 3,764 checks were processed using this method during the spring period. The total amount remotely deposited in the fall was $330,828.50, and the total in the spring was $319,945.89. Appendix C contains graphs that illustrate the timeliness of check deposits by each school. The “deposit lag” is calculated as the difference between the date the check was remotely deposited and the date on the check. Some lag time is normal and is due to various factors, some of which include:

travel time of checks given to students who subsequently bring the checks to school timing of deposits after weekends, school holidays, and bank holidays timing of vacation or sick leave used by the finance secretaries

Although some deposit lag is inevitable, many of the delays I noticed could have been prevented by all staff complying with Board Policy DG. Based on my review of the deposits, I noticed that sometimes checks collected away from the finance secretaries’ offices were not turned over to the office on a daily basis. I also noticed instances where the finance secretaries did not make daily deposits. Even though the extent of compliance with Board Policy DG varies from school to school, I believe each school’s compliance with this policy can be improved.

Cause – Cash and checks are collected at the high schools by various individuals located throughout the schools. As a result, the timeliness of deposits depends largely on how quickly club sponsors, coaches, and teachers can turn over their collections to the finance secretary for deposit. Timeliness of deposits also depends on the finance secretaries’ compliance with the requirement to make daily deposits. Achieving widespread compliance requires a commitment to comply with the policy from everyone involved in the cash handling process.

Effect – Cash and/or checks that are held for multiple days before being deposited expose the district to losses due to money being misplaced or stolen. Also, the longer cash is held, the more likely that a deposit error will occur and will not be corrected or detected in a timely manner.

Page | 9

Finding 2 – Timeliness of Deposits (continued) Recommendation – Improving the timeliness of high school deposits will require a coordinated

effort between the finance department, high school administrators, and high school staff. Everyone involved in the cash handling process must be committed to ensuring deposits are made timely. The finance department and the high school administrators must continue to train employees on the importance of timely deposits. High school administrators should consider using compliance with Board Policy DG as one component of their staff’s performance evaluations. Management should also consider establishing deposit lag goals, and use the deposit lag as a monitoring tool. Also, although current staffing levels may not allow for additional monitoring activities, ideally the Finance department would perform site visits to determine compliance with existing policies.

Management’s Response – Management agrees with the comments related to policy compliance and thanks the auditor for recognizing that current staffing levels do not allow for compliance testing. Timeliness of deposits has been a main focus of the annual meetings with secretaries, athletic ticket managers and high school fundraisers. Management will review and, if necessary, revise policy DG to ensure alignment and feasibility. Training and monitoring processes concerning the timeliness of high school deposits will also be reviewed and expectations will be clearly established, documented and communicated. The administration at each high school, working in conjunction with Finance and the site financial secretaries, will be responsible for specifying the methods used for building level oversight of these processes.

Page | 10

Finding 3 – Board-approved Fees

Criteria – Annually, the Board of Education approves a list of fees in accordance with Board Policy JN – Student Fees, Fines, and Charges. To be an effective governance tool, the approved fee list should include all fees.

Condition – The Board-approved fee list is only a partial listing of the fees being paid by the district’s high school students. Although other fees may exist, the fees I noted that are not included on the Board-approved list are:

Course fees Library fines Identification badge replacement fees Transcript fees Graduation DVD sales price

Cause – Creating the annual list of fees and seeking Board approval for these fees is performed by the district’s central office. However, many of the fees are imposed and collected by individuals at the high schools. Due to the decentralized nature of the process, some fees were not identified by the central office and were not included on the annual list for the Board to approve.

Effect – The Board might be unaware of some of the fees that are currently being paid by high school students in the district. Without receiving a complete list of fees, the Board does not have the opportunity to discuss the purpose or need for all of these fees.

Recommendation – Management should implement a process to identify all fees being charged throughout the district, and include all fees on the annual list that is submitted to the Board for approval. A complete list of fees is more useful to the Board and also provides better information to citizens of the district.

Management’s Response – As part of management’s review of Board policies, Policy JN will be reviewed and compliance will be clearly established, documented and communicated. Management will work with Secondary Operations and Educational Services to develop and review/revise a list of all fees. Some fees may be building specific and further discussion will be needed to determine if all fees should go before the Board; in addition, a process for requesting course level fees will be developed. Target completion date is January 2, 2014.

Page | 11

Finding 4 – Parking Permit Fee Structure

Criteria – Annually, the Board of Education approves a list of fees in accordance with Board Policy JN – Student Fees, Fines, and Charges. One of the approved fees is the student parking permit fee. The approved fee for FY 2013 was $35. To promote equal treatment of all high school students throughout the district, the process of charging and collecting parking permit fees should be uniform across all district high schools.

Condition – The student parking permit fee structure differs from one high school to another. All of the high schools consistently charge the Board-approved fee of $35 for routine annual parking permits. However, the parking fee charged for special situations differs from school to school, and the Board-approved fee does not address any special circumstances. The special situations I observed were:

The process of charging a student for a partial-year parking permit was not consistent from school to school. At most schools, if a student requested a permit for only the first semester, that student was only charged a reduced rate of either $17.50 or $15. But at Kickapoo High School, the student was required to pay the entire $35 fee in the first semester. When the first semester was over the student was issued a refund check for $17.50 if the administrators were able to confirm that the student would not be returning for the spring semester.

At Hillcrest in FY 2013, the parking fee was waived for seven student office workers. No other high school issued any parking permits for free.

Students at Hillcrest who also attended Ozarks Technical College (OTC) were charged a

reduced fee of $17.50. The other high schools did not discount the parking permit fee for their students who also attended OTC.

At Parkview and Hillcrest a small number of students were allowed to receive parking

permits without paying the full amount due. For some of these students I found no evidence that the remaining balances were ever paid.

The chart below summarizes the differences in the parking fee structure at each school.

FEE SCENARIO BOARD

APPROVEDCENTRAL GLENDALE HILLCREST KICKAPOO PARKVIEW

Annual fee $ 35.00 $ 35.00 $ 35.00 $ 35.00 $ 35.00 $ 35.00

One-semester fee Not addressed $ 17.50 $ 15.00 $ 15.00 $ 17.50 $ 15.00

OTC students Not addressed $ 35.00 $ 35.00 $ 17.50 $ 35.00 $ 35.00

Replacement tag fee Not addressed $ 1.00 $ 1.00 $ 1.00 $ 1.00 $ 1.00

Waived fees Not addressed No No Yes No No

Cause – The list of fees approved by the Board annually does not address any special circumstances or scenarios that might justify a school to charge a lower parking fee or to waive the fee. Each school has interpreted the approved fee schedule slightly differently to accommodate special circumstances not addressed by the Board-approved fee schedule.

Page | 12

Finding 4 – Parking Permit Fee Structure (continued)

Effect – The different variations of implementing the parking permit fee structure is resulting in students being treated differently from one school to another.

Recommendation – Management should develop a comprehensive parking permit fee schedule to address the scenarios listed in the table above, and all other necessary scenarios that management identifies. If considered necessary by management, the Board of Education should approve the revised parking fee schedule.

Management’s Response – The action to this finding will be incorporated in the actions identified in management’s response to Finding 3. A work group will be formed to address many of the findings within this report. This work group will be charged with developing processes to meet expectations of the audit, revise or develop policy, and address training issues where appropriate. This work group will include representation from Secondary Operations, Finance, administration at all five high schools, financial secretaries and other representative departments when appropriate. Through the work team, management will develop and implement a consistent, district-wide schedule for charging parking fees.

Page | 13

Finding 5 – Parking Permit Fee Reconciliation Process

Criteria – Annually, the finance secretary at each high school completes a form that accounts for all of the parking decals issued to their school from the School Police Services Department (School Police). At the end of each fiscal year, the finance secretary returns all unsold decals to School Police along with the completed reconciliation form. The reconciliation forms recalculate the expected parking fee revenue based on the number of permits sold. For these forms to be useful, the reconciliations should be accurate and appropriately reviewed.

Conditions – I noted mistakes on four of the five completed reconciliation forms for fiscal 2013. Minor mistakes were noted on 3 of the forms, but the form from Parkview High School contained significant inaccuracies. At Parkview High School, based on my review of receipt books, total parking fees collected in FY 2013 were $5,670. However, only $4,924 was recorded in the revenue account and reported on the reconciliation form. Further analysis revealed that $321 of the shortage was due to checks that were collected and deposited, but recorded into the wrong revenue account. I was able to trace $365 of the remaining $425 shortage to a cash deposit on August 6, 2012 that was short. Cash receipts records showed that a total of $490 in cash was collected for parking permits sold on August 1, 2012. However, on August 6, 2012, only $125 was deposited at the bank. The shortage of $365 is unexplained. The total cash shortage of $425 represents 7.5% of the total parking fees collected for the year. The error rate was much smaller at the other four high schools. Without verifying the accuracy of the annual reconciliation form, these errors would not have been detected.

Cause – Although the parking permit reconciliation forms are completed and provided to School Police each year, these forms are only used by School Police to track the decals that were issued to each school. No one matches the expected revenue with the actual fees collected and deposited.

Effect – Without someone independent of the high school finance secretary performing a review of the reconciliation of student parking permits sold to the recorded student parking fee revenue, little assurance exists that the amount of parking fee revenue reflected in the district’s general ledger matches the amount that was actually collected.

Recommendation – Someone other than the high school finance secretaries should perform a review of the reconciliation of the parking permits sold to the parking fee revenue each year. Since the finance secretary performs all duties related to the selling of parking permits, no segregation of duties exists. Since no segregation of duties exists, additional monitoring controls (like a properly monitored reconciliation process) are necessary to provide additional assurance that all fees collected for parking permits have been appropriately deposited and recorded.

Management’s Response – Through the work team described in the response to Finding 4, it will be determined if a process for reconciling and monitoring parking fees can be developed within the existing staffing structure, or if additional staffing is required. This will occur in conjunction with the response to Finding 3.

Page | 14

Finding 6 – Course Fees

Criteria – The process for charging students fees for participating in a course should be transparent, collection efforts should be consistently applied, and these course fees should undergo an appropriate approval process.

Condition – Students enrolled in certain courses are expected to pay a course fee which is intended to fund the purchase of supplemental materials for use in that course. While this practice may be necessary for many courses due to budgetary constraints in the district, the controls over the assessment and collection of these fees are lacking. Current practices allow teachers to impose a course fee without obtaining further administrative approval. In many instances teachers collect these fees in their classrooms. The collected fees are subsequently given to the school’s finance secretary to prepare the bank deposit. To enforce payment of the fees, at some point during each semester, teachers typically provide the finance secretary with a list of the students who have not paid. Then the finance secretary enters these fees as “fines” on the student’s account. Although this process is consistently followed across the five high schools, no standard method exists for establishing, imposing, or collecting course fees. Also, no process is in place to reconcile the fees received and receivable to the expected total fees based on course enrollment.

Cause – The district high schools lack comprehensive approved listings of course fees, and the district lacks a documented and uniform process for approving, charging, and collecting the fees.

Effect – Adequate safeguards have not been implemented to prevent students from being charged unreasonable course fees, to prevent these course fees from being misappropriated, or to ensure the process of enforcing payment of the fees is fair and consistent across the district. Under current practices, course fees are not monitored or approved by anyone other than the same teacher who imposes and collects the fee. Without someone else approving the fee, little assurance exists that the fee is appropriate or necessary. Without someone reconciling the fees collected to the expected fee revenue, little assurance is provided that all fees collected have been appropriately deposited or that the fee has been fairly enforced.

Recommendation – Course fees should be approved annually and a listing of the course fees should be made available for students and parents at each high school. Management and/or the Board of Education should decide who has the authority to approve these fees. Also, a standardized process for all high schools to follow should be developed and documented that addresses:

how fees will be collected how payment of the fees will be enforced how fee revenue will be monitored

Management’s Response – The action to this finding will be incorporated in the actions identified in management’s response to Finding 3. Management will develop monitoring processes to help ensure compliance with Board policy concerning fees, approval, and collection.

Page | 15

Finding 7 – Band Fees

Criteria – Annually, the Board of Education approves a “Band/Drum Corps” participation fee (band fee) that is intended to be charged to all students participating in the high school band programs. The board-approved fee for fiscal 2013 was $25. These fees should be consistently enforced and recorded in the appropriate general ledger accounts.

Condition – Specific revenue accounts have been established in the Incidental Fund (Fund 10) for the high schools to use for the purpose of recording the band fee collections. However, as displayed below, only two of the five high schools have consistently collected the fees and recorded the fees in the appropriate Incidental Fund revenue account.

FY 2010 FY 2011 FY 2012 FY 2013

Central $ 75.00 $ 125.00 $ 75.00 $ 50.00

Glendale 2,025.00 1,925.00 1,225.00 2,100.00

Hillcrest 1,500.00 1,500.00 1,625.00 1,450.00

Kickapoo - - - -

Parkview 350.00 25.00 - 125.00

Band Fee Revenue Recorded in Financial Accounting Software

High School

Based on my review of the district’s general ledger and my discussions with the high school finance secretaries, for at least the past four years, three of the five high schools have either collected the $25 band participation fee and recorded the fee in the wrong revenue account, or these schools have not collected the fee from the band students at all.

Cause – Collection and enforcement of the band fee is performed by each high school. No one at the district has been assigned the responsibility for monitoring the band fee revenue accounts. As a result, no one has addressed the issue that at least three of the high schools have not appropriately managed the band fee collection process.

Effect – The district is exposed to the risk that the high schools are not appropriately enforcing or collecting the Board-approved band fee. The existing control structure does not provide a high level of assurance that the $25 fee is being enforced or recorded properly.

Recommendation – Management should provide clarified instructions to the high school finance secretaries, band directors, and building principals, which clearly indicate which accounts should be used to record the fees received from band students. Management should also monitor compliance with these instructions by performing annual reconciliations of each school’s band fees collected to determine if the total band fee revenue collected is consistent with the expected total band fee revenue based on the size of the band at each school.

Management’s Response – The Finance Department will provide clarified instructions at the annual meetings for secretaries and principals. Management will develop monitoring processes to help ensure compliance with Board policy concerning course fees, approval, and collection. Processes for reconciliation may require additional resources/staff. Finding 7 will be addressed in conjunction with Finding 3.

Page | 16

Finding 8 – Student Activity Account Balances

Criteria – The Student Activity Fund is “used to account for money raised by the students for the students,” and the “purpose of raising and expending activity money is to promote the general welfare, education, and morale of all the students and to finance approved extracurricular and co-curricular activities of student body organizations.” 4 According to Board Policy IGDG, the “management of the funds will be in accordance with good business practices, including sound budgetary and accounting procedures.” One element of “good business practices” includes properly monitoring account balances, and only allowing temporary deficit balances in any individual student activity account. In most instances student activity accounts should end the fiscal year with either a positive balance or a balance of $0.

Condition – As shown in the list of student activity accounts in Appendix D, 54 out of 433 active high school student activity accounts ended FY 2013 with a deficit balance. A deficit balance in a student activity account occurs when a student group (overseen by a club sponsor, coach, etc.) has spent more money than it has collected through fundraisers, events, or student fees. Occasionally some student activity accounts will have circumstances that necessitate incurring a temporary deficit balance. As an example, a school’s drama activity account may develop a temporary deficit balance because many of the expenditures for a school play must occur before the tickets for the play can be sold.

However, student activity accounts with deficit balances year after year are an indication of poor fiscal management of these activities. Particularly troubling is that 26 out of 68 active student activity accounts at Hillcrest High School had deficit balances at June 30, 2013, and 23 of these accounts also had deficit balances at June 30, 2012. In contrast, Glendale High School only had two activity accounts with deficit balances at June 30, 2013, and only one of those accounts also had a deficit balance at June 30, 2012. Glendale had a total of 97 active student activity accounts.

Cause – The methods used to monitor activity account balances varies greatly from one school to another. Activity sponsors (coaches, club sponsors, etc.) are responsible for managing their individual student activity accounts. However, these sponsors do not have access to the financial accounting software that would allow them to monitor their balances on a continuous basis. Instead, the sponsors must rely on the school finance secretaries to keep them informed of their balances. But even with access to timely account balance information, problems with persistent deficit balances will remain unless building administrators become more actively involved in monitoring the accounts.

Effect – If a student activity account is allowed to incur a deficit balance without a definitive plan in place to address the deficit, the likelihood of that account regaining a positive balance in a timely manner is greatly diminished. Naturally, students and parents would rather perform fundraisers to pay for expenses that will have a current benefit for their club, team, or student activity. Performing fundraisers to pay for items purchased years ago is not likely to receive much enthusiasm from students or parents.

4 “Springfield Public Schools Budget Book 2012-2013,” Springfield Public Schools, https://isharesps.org/websitedoc/Finance/FINANCE/BUDGET%20BOOKS/2012-2013%20BUDGETBOOK.pdf, p. 254, accessed on April 10, 2013.

Page | 17

Finding 8 – Student Activity Account Balances (continued)

Recommendation – High school student activity balances need to be monitored more effectively to prevent activity accounts from developing long-term deficit balances. The district’s finance department and the high school building administrators should work together to devise plans to improve the financial condition of activity accounts with deficit balances. Management should also define the types of allowable situations that justify an activity account balance to incur a temporary deficit balance. In most situations a student activity should have sufficient funds available to pay for expenditures in advance of obligating the account’s funds. Only a few exceptions to this practice should be necessary. One option to improve the monitoring of activity account balances would be to provide activity sponsors with access to the district’s accounting software to allow them to view their account balances anytime they desire. Improved access to their account information is one tool that could improve the ability of many activity sponsors to manage their accounts.

Management’s Response – Management will develop general guidelines identifying when it is appropriate for an activity account to have a deficit balance. Once these guidelines have been developed, on a monthly basis, the Finance Department will monitor and prepare a report on student activity accounts with negative balances. The Finance Department will work with the site administrator responsible for activities to develop a plan for achieving a positive account balance by fiscal year end. Excepting reasonable explanations, should the plan not be met, the activity account will subsequently be closed until it is brought to a positive balance.

Page | 18

Finding 9 – Athletic Participation Fees

Criteria – Annually, the Board of Education approves the “Athletics Participation Card” student fee that will be charged to all students participating in high school sports. The Board-approved annual fee for fiscal 2013 was $50.

Condition – At all high schools, the actual athletics participation fee that was charged to students who had been approved for free or reduced lunch was $25. However, the “2012-2013 School Handbook” states that “the athletic participation card fee will be waived upon the request of a parent for those high school students eligible for free and reduced lunch.”

Cause – As mentioned in Finding 4, the Board-approved list of student fees does not address all special situations. One of the special situations excluded from the list is the athletics participation fee structure for those students who have been approved for free or reduced lunches.

Effect – The high school athletics participation fee structure that has been implemented for those students approved for free or reduced lunches does not comply with either the Board-approved fee or the School Handbook.

Recommendation – Management and/or the Board should clarify the athletics participation fee structure to include a description of how the fee will be assessed for those students who have been approved for free or reduced lunches.

Management’s Response – Fees are waived at the middle school level for students qualifying for free-reduced priced lunch. Fees are reduced to $25 for high school students who qualify for free/reduced priced lunch. An editing error resulted in incorrect information in the high school portion of the student handbook. That information has been corrected within the on-line version and processes at the high schools are in compliance with the expectations. We are unable to correct the printed copies for the 2013-2014 school year; however, the handbooks will be corrected for the 2014-2015 edition.

Page | 19

APPENDIX A: AUDIT RATING DEFINITIONS EFFECTIVE – Operational, financial, and compliance controls evaluated are adequate, appropriate, and effective to provide reasonable assurance that risks are being managed and objectives are being met. Any findings of control deficiencies are minor, and the risks associated with these findings are insignificant. IMPROVEMENT NEEDED – Generally, the controls evaluated are adequate, appropriate, and effective to provide reasonable assurance that risks are being managed and objectives are being met. However, findings of control deficiencies, either in design or function, are noted for which the risks associated with these findings are more than inconsequential. Further deterioration in these controls could, but might not, result in failure to adequately prevent a material loss or to ensure functional objectives are met. INEFFECTIVE – Controls evaluated are not adequate, appropriate, or effective to provide reasonable assurance that risks are being managed and objectives are being met. Urgent corrective action is necessary to correct the control deficiencies identified.

Page | 20

APPENDIX B: RELEVANT BOARD POLICIES5

Board Policy Relevance to this Audit

CF - School Building Administration

-Establishes building principals' duty to oversee staff within their building and to ensure that Board policies, rules, and regulations are observed

CH - Policy Implementation -Requires the Superintendent to be responsible for implementing and interpreting Board policies -Grants administrators and supervisors the responsibility for implementing and interpreting policies to staff members under their supervision -Allows the administration to also use staff, student, and parent/guardian handbooks to disseminate policies and regulations

CHA - Administrative Regulations and Procedures

-Requires administrative regulations and procedures to be developed for the purpose of interpreting and implementing policies and legal mandates -Specifies that development of these procedures is the Superintendent's responsibility

CHCA - Approval of Handbooks and Directives

-Authorizes administrators to develop handbooks for the purpose of informing staff about Board policies -Specifies that these handbooks should only contain policies, rules, regulations, and procedures which do not conflict with the intent of Board policies

DFE - Gate Receipts and Admissions

-Requires the Board of Education to determine the admission prices for athletic events -Specifies that building principals are responsible for the proper collection and supervision of admission receipts at school events

DG - Depository of Funds -Requires all funds to be deposited at the official district depository institution within 24 hours of receipt -Requires funds kept overnight in a district building to be kept in a secure place

DI - Fiscal Accounting and Reporting/Accounting System

-Requires the Superintendent to be responsible for receiving and properly accounting for all funds of the district

DM - Cash in School Buildings -Requires all moneys collected within the district's schools to be prudently safeguarded IGDF - Fundraising Activities -Requires school fundraising activities to be approved in advance by the school principal

-Requires school booster club fundraising activities to be approved in advance by the school principal

IGDG - Student Activities Funds Management

-Places all student activities funds under the jurisdiction of the superintendent and building principals -Specifies that the management of the funds will be in accordance with good business practices, and the funds will be expended to benefit students currently enrolled in school

JHFD - Student Automobile/Vehicle Use

-Specifies that high school students are required to pay a fee to park on school parking lots

JN - Student Fees, Fines, and Charges

-Requires the Superintendent to submit annually to the Board of Education a schedule of fees to be charged students for the Board to approve -Requires students to pay for school property they have lost or damaged

5 Springfield Public Schools, <https://isharesps.org/websitedoc/CommunityRelations/Board/allpolicies.pdf>, accessed on March 12, 2013.

Page | 21

APPENDIX C: TIMELINESS OF REMOTE CAPTURE CHECK DEPOSITS

Note: “Deposit Lag Time” is defined as the number of days between the date on the face of the check, and the date the check was deposited.

Page | 22

APPENDIX C: TIMELINESS OF REMOTE CAPTURE CHECK DEPOSITS

Page | 23

APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS

STUDENT ACTIVITY ACCOUNTBalance

6/30/2013

Balance

6/30/2012STUDENT ACTIVITY ACCOUNT

Balance

6/30/2013

Balance

6/30/2012

SCHOLARSHIP $33,199.50 $24,960.16 MU ALPHA THETA $363.50 $368.50

CHEERLEADING 11,556.60 9,028.93 DECA 311.47 98.24

PRE-INTERNATIONAL BACCALAUREATE 10,905.90 12,244.87 ORCHESTRA 282.65 928.71

DRUM CORPS 9,027.84 6,891.46 ATTENDANCE INCENTIVE 273.10 473.10

ACTIVITY-GENERAL 7,188.14 7,167.90 FRESHMAN ACTIVITY 261.25 504.72

STUDENT ACTIVITIES-ENGLISH DEP 6,656.98 4,223.94 AGAINST DESTRUCTIVE DECISIONS 257.51 457.51

YEARBOOK 6,044.72 7,619.03 STUDENT ACTIVITIES-WORLD LANG 254.01 63.17

MEDIA CLUB 5,494.06 5,402.66 SPECIAL ED LIFE SKILLS 240.23 212.00

TRANSITION CLUB 5,101.74 4,133.00 MCBRIDE ACCOUNT 223.60 173.55

CHOIR 4,480.88 3,352.09 TENNIS 199.96 247.72

QUILL & SCROLL 4,422.96 1,750.60 GSA 197.40 193.10

STUDENT COUNCIL 3,640.98 25.22 GIRLS GOLF 177.02 177.02

STUDENT ACTIVITIES-BUSINESS ED 3,275.08 2,039.47 SCIENCE CLUB 172.96 1,003.73

CONCESSIONS 3,117.67 2,367.04 MODEL U.N. 170.29 170.29

FOOTBALL 3,038.24 4,352.21 KEY CLUB 147.33 (23.60)

JUNIOR ACTIVITY 2,755.20 380.23 FTA CLUB 145.00 250.00

SMART DOG STUDIOS 2,561.69 2,514.25 LINK 127.36 29.00

NEWSPAPER 2,381.10 1,862.71 SOCCER 112.71 66.61

FOUNDATION 2,380.74 2,412.19 CROSS COUNTRY 107.24 165.65

GIRLS SWIMMING 2,209.64 2,430.94 SALSA CLUB 106.99 0.00

SOPHOMORE ACTIVITY 2,140.15 2,216.74 SPANISH CLUB 91.68 (893.75)

FINE ARTS 1,994.50 382.48 GIRLS SOCCER 87.76 296.96

BASE-ST. JOHNS 1,880.35 1,965.53 ACTION & INNOVATION CLUB 81.19 10.00

DRAMATICS 1,828.41 146.61 FELLOWSHIP OF CHRISTIAN ATHLETES 73.55 73.55

FBLA CLUB 1,640.27 2,231.40 GIRLS BASKETBALL 67.61 144.51

GIRLS TENNIS 1,635.00 1,635.00 AFRICAN AMERICAN ACAD ACHIEVERS 47.97 41.67

LIBRARY 1,628.12 1,148.19 JUSTICE IN ACTION 35.58 135.58

SCIENCE COPIER 1,573.43 21,373.05 HISTORY CLUB 28.02 (136.73)

FCCLA CLUB 1,499.70 1,021.68 GOLF 17.60 (108.45)

FRIENDS OF CENTRAL 1,400.60 1,293.10 BASE-COX NORTH 15.33 414.88

GIRLS 4 GOOD 1,387.40 928.35 STAT CLUB 13.21 13.21

SENIOR ACTIVITY 1,299.71 1,537.50 FRENCH CLUB 12.00 0.00

COMMUNITY FOUNDATION 1,175.71 4,499.12 PEER MEDIATION 6.84 (60.71)

NERD CLUB 974.41 846.91 NATIONAL ART HONOR SOCIETY 6.10 6.10

SPEECH CLUB 909.36 2,408.29 RELAY FOR LIFE 0.00 0.00

TRANSCRIPT FEES 875.48 627.09 YOUTH EMPOWERMENT PROJECT 0.00 500.00

PROJECT GRADUATION 857.37 1,201.31 SHOPPE 17 COFFEE 0.00 374.60

I.D. TAGS 811.81 711.09 WRESTLING (63.71) (133.80)

NATIONAL HONOR SOCIETY 727.62 652.90 INTERNATIONAL CLUB (203.59) 267.87

STUDENT ACTIVITIES-MATH 705.35 550.10 ATHLETICS (255.75) 1,652.52

RESTORE CENTRAL 700.64 700.64 BASEBALL (277.71) (173.86)

IB THEATER-ISTA TAPS 691.53 0.00 ART CLUB (433.94) (532.91)

TRACK 643.49 643.49 SOFTBALL (680.99) 5.21

SWIMMING 533.56 872.25 BAND (718.18) (992.79)

CHESS CLUB 501.41 501.41 DANCE TEAM (1,746.48) (4,809.75)

STUDENT ACTIVITIES-TECH ED 490.01 12.17 BASKETBALL (5,091.95) (5,324.95)

VOLLEYBALL 384.69 113.38 TOTAL COMBINED BALANCE 155,573.46$ 151,706.66$

Source: The above balances were obtained from the district's general ledger accounting software.

CENTRAL HIGH SCHOOL

Page | 24

APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS

STUDENT ACTIVITY ACCOUNTBalance

6/30/2013

Balance

6/30/2012STUDENT ACTIVITY ACCOUNT

Balance

6/30/2013

Balance

6/30/2012

QUILL & SCROLL $14,428.44 $20,235.26 FUNCTION JUNCTION $270.59 $104.06

SENIOR ACTIVITY 13,798.44 13,841.90 FACS DUAL CREDIT 244.21 567.62

CHEERLEADING 12,220.23 12,092.56 PROJECT GRADUATION 239.90 (239.00)

STUDENT ACTIVITIES-ENGLISH 10,657.27 16,741.91 GUIDANCE FUND 231.47 341.47

CONCESSIONS 6,885.09 5,031.72 AUDITORIUM ACTIVITY 225.00 225.00

STUDENT COUNCIL 6,765.14 7,423.18 STUDENT 2 STUDENT 194.02 214.81

SPEECH CLUB 6,195.95 2,843.34 FOOTBALL 192.02 205.19

DECA 5,909.17 6,795.03 GOLF-GIRLS 171.49 0.00

I.D. TAGS 5,668.59 5,177.42 DRAMATICS 162.57 585.58

ACTIVITY-GENERAL 5,406.60 6,576.72 ANCHOR-GIRLS SERVICE SOCIETY 135.44 53.00

LIBRARY 4,950.50 3,872.25 FTA CLUB 134.97 140.20

WORLD LANGUAGE CLUB 4,726.76 4,203.11 DIVERSITY & CULTURE CLUB 101.77 0.00

STUDENT ACTIVITIES-HISTORY 4,052.75 5,897.62 ART CLUB-SCULPTURE 96.61 473.22

FOREIGN LANGUAGE DEPT 3,938.71 7,187.23 SOFTBALL 92.73 684.54

STUDENT ACTIVITIES-BUSINESS ED 3,898.92 3,477.96 YOUTH AGAINST CANCER 85.72 12.58

NEWSPAPER ADS 3,864.32 15,270.96 SWIMMING 82.96 199.50

FIN ARTS-PRODUCTIONS 3,848.48 4,508.51 FACS IS 80.00 541.82

THE NEST 3,669.83 1,952.00 SPECIAL ED-GHS 74.07 25.32

STUDENT ACTIVITIES-MATH 2,290.53 1,731.76 PLTW LAB 66.39 0.00

FIELD TRIPS-MARINE BIOLOGY 2,262.44 1,682.09 BAND 65.23 1,361.47

A+ ACTIVITY 2,189.73 2,082.90 FACS IN 64.94 332.02

SCIENCE DUAL CREDIT-CR 1,797.76 1,797.76 SCIENCE DUAL ENROLL-JL 61.84 0.00

MEDIA CLUB 1,710.22 967.35 PEER MEDIATION 47.32 2.32

SCIENCE DUAL CREDIT-MP 1,682.03 1,308.07 SOCCER-GIRLS 41.24 (1,382.54)

WRESTLING 1,660.50 76.68 ART CLUB 39.04 32.00

ORCHESTRA 1,598.53 7.16 AGAINST DRIVING DRUNK 37.37 37.37

FELLOWSHIP OF CHRISTIAN ATHLETES 1,503.96 41.65 FOUNDATION SUPPORT 37.21 1,356.84

NATIONAL HONOR SOCIETY 1,365.25 2,477.80 ART FUNDAMENTALS 30.68 90.44

ART DEPARTMENT 1,353.63 1,577.36 GHS ATHLETICS PROGRAMS 25.00 0.00

CHOIR 1,301.89 (5,485.69) FACS CA 22.43 96.08

FOUNDATION COLLEGE FEES 1,277.05 1,296.00 YONKE'S SCIENCE GRANTS 15.90 0.00

ANCHOR-BOYS SERVICE SOCIETY 1,259.14 1,059.14 SPECIAL ED-BASE 11.28 11.28

VENDING 1,044.98 4,496.78 OUTDOORS CLUB 10.00 10.00

TRACK 894.90 221.28 GHS GARDEN GRANT 7.38 58.83

THE GREEN SQUAD 880.89 779.15 TENNIS 3.60 3.60

FUTURE FALCONS 843.29 613.32 SOCCER 1.00 0.00

FALCON TECHNOLOGY FUND 801.00 657.12 BASKETBALL 0.78 330.78

CROSS COUNTRY 681.43 371.31 GIRLS BASKETBALL 0.64 50.64

LIFT-A-THON 550.00 0.00 CRIMINAL JUSTICE CLUB 0.09 0.00

VOLLEYBALL 523.15 689.08 YEARBOOK 0.00 7,524.28

FACS PROSTART 518.73 155.09 TRANSCRIPT FEES 0.00 0.00

CHARACTER COUNCIL 499.22 624.72 FRESHMAN TRANSITION 0.00 2,441.06

SCIENCE DUAL ENROLL-KM 484.00 140.32 GOLF-BOYS 0.00 236.49

MCBRIDE ACCOUNT 459.53 369.77 STUDENT ACTIVITIES-TECHNOLOGY 0.00 17.67

ACADEMIC TEAM 442.07 447.07 LIBRARY HIGH DEF GRANT 0.00 687.88

FALCON FUND 429.94 961.68 SCIENCE OLYMPIAD 0.00 0.00

FBLA CLUB 383.69 383.48 BASEBALL (384.59) 124.87

SCIENCE DUAL CREDIT-FF 356.87 466.87 DANCE TEAM (540.30) (1,190.97)

FCCLA CLUB 341.25 15.15 TOTAL COMBINED BALANCE $156,752.80 $181,508.22

Source: The above balances were obtained from the district's general ledger accounting software.

GLENDALE HIGH SCHOOL

Page | 25

APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS

STUDENT ACTIVITY ACCOUNTBalance

6/30/2013

Balance

6/30/2012STUDENT ACTIVITY ACCOUNT

Balance

6/30/2013

Balance

6/30/2012

MARKET ON THE HILL $22,088.33 $0.00 FRENCH CLUB $161.14 $112.36

STUDENT ACTIVITIES-SCIENCE 19,277.04 16,453.44 TECHNOLOGY CLUB 113.36 190.36

I.D. TAGS 18,196.68 12,507.88 BASE-COX 103.30 46.30

ART 10,123.67 11,478.88 DANCE/POM POM 92.64 (1,185.17)

SPECIAL ED 9,274.02 10,551.10 BASE-SWI 71.43 417.93

MEDIA 7,200.14 (2,063.55) SHOPPE 17 COFFEE 68.16 0.00

STUDENT ACTIVITIES-MATH 4,407.41 2,529.47 KEY CLUB 36.71 143.29

STUDENT ACTIVITIES-ENGLISH 3,370.71 2,785.11 GRANTS 3.34 (67.71)

DESIGN CLASS 3,244.08 2,461.08 FOUNDATION SUPPORT (44.01) 0.00

PRESS CLUB 3,232.19 1,000.89 FTA CLUB (50.00) (50.00)

FRESHMAN ACTIVITY 3,000.00 3,000.00 FELLOWSHIP OF CHRISTIAN ATHLETES (206.50) (192.67)

VOLLEYBALL 2,881.39 6,008.70 ACADEMIC TEAM (330.22) (370.22)

ACTIVITY-GENERAL 2,805.60 558.32 DRUM CORPS (346.82) (346.82)

NEWSPAPER 2,507.20 2,507.20 SOCCER (374.61) 168.61

NATIONAL HONOR SOCIETY 2,489.33 2,334.75 BASEBALL (392.99) 124.81

SENIOR ACTIVITY 2,472.06 1,827.99 GIRLS ATHLETICS (443.42) (917.08)

DECA 2,403.73 992.56 WRESTLING (1,298.56) (345.51)

STUDENT ACTIVITIES-HISTORY 2,381.74 1,161.67 ORCHESTRA (1,464.80) (1,482.67)

HORNET FOUNDATION 2,206.13 4,071.23 SOFTBALL (1,687.96) (1,485.67)

A+ ACTIVITY 2,197.85 4,784.89 FOOTBALL (1,770.92) (1,860.56)

FOUNDATION SUPPORT 1,941.96 3,779.76 TENNIS (1,868.06) (1,550.26)

ATHLETICS 1,871.02 1,192.62 BASE-OZARKS HOSPITAL (2,223.58) (1,934.17)

FCCLA CLUB 1,737.64 3,381.74 FBLA CLUB (2,346.69) (2,347.97)

SWIMMING 732.85 944.85 ATHLETICS-BOYS GOLF (3,325.77) (2,577.77)

GERTRUDE MCBRIDE ACCOUNT 695.63 595.63 YEARBOOK (4,151.55) (2,941.43)

SOS CLUB 659.91 659.91 JROTC (4,907.50) (4,542.73)

SPANISH CLUB 551.61 551.61 CHEERLEADING (5,057.58) (11,038.28)

TRACK 534.79 1,223.94 SPEECH CLUB (5,201.30) (3,155.66)

STUDENT COUNCIL 383.68 (1,904.47) DRAMATICS (5,276.51) (6,214.83)

LIBRARY 344.14 53.30 BAND (6,016.55) (2,821.03)

GIRLS BASKETBALL 286.41 (533.08) FINE ARTS (6,542.90) (5,124.55)

S.A.D.D. 283.60 300.72 CHOIR (8,603.82) (9,353.94)

PROJECT GRADUATION 189.61 305.61 CONCESSIONS (9,697.74) (10,176.22)

DIVERSITY CLUB 183.96 183.96 BASKETBALL (9,734.28) (9,583.85)

TOTAL COMBINED BALANCE 53,441.55$ 15,224.60$

Source: The above balances were obtained from the district's general ledger accounting software.

HILLCREST HIGH SCHOOL

Page | 26

APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS

STUDENT ACTIVITY ACCOUNTBalance

6/30/2013

Balance

6/30/2012STUDENT ACTIVITY ACCOUNT

Balance

6/30/2013

Balance

6/30/2012

TEACHERS SUPPLIES $25,775.71 $22,725.46 ACADEMIC TEAM $517.13 $192.11

SCIENCE CLUB 14,022.49 12,341.10 TENNIS-BOYS 450.57 0.00

TECHNOLOGY EQUIPMENT 13,520.35 10,378.11 FTA CLUB 440.50 482.87

STUDENT ACTIVITIES-MATH 11,983.64 9,895.02 AGAINST DRIVING DRUNK 440.03 (100.74)

I.D. TAGS 10,532.01 9,731.19 FOOTBALL 380.84 1,932.58

ACTIVITY-GENERAL 9,953.60 (623.32) PEP CLUB 380.00 236.00

LIBRARY 9,526.36 8,164.42 TRANSITION 351.41 477.38

CONCESSIONS 8,821.91 7,403.08 KIDS BEAT TV 300.00 300.00

VENDING 7,673.10 7,673.10 JAPANESE CLUB 274.74 77.90

SENIOR ACTIVITY 7,327.50 7,465.45 LETTERMAN'S CLUB 270.24 270.24

HISTORY CLUB 6,385.80 1,663.88 GIRLS BASKETBALL 215.52 215.52

PRESS CLUB 6,380.14 3,857.97 SPECIAL ED 196.09 196.09

STUDENT COUNCIL 6,261.41 8,337.17 A+ ACTIVITY 190.41 180.41

FINE ARTS 5,501.17 2,160.13 GIRLS 4 GOOD 189.84 176.00

FOREIGN LANGUAGE CLUB 4,867.94 1,675.49 YOUTH ALIVE 180.37 180.37

SPEECH CLUB 4,563.73 3,588.59 SCHOLARSHIP FUND 159.21 150.25

YOUTH GOVERNMENT 4,494.70 2,421.54 HIV/AIDS PEER EDUCATION 141.45 141.45

CHEERLEADING 4,398.91 14,645.66 CHIEF FUND 129.46 239.11

WORK EXPERIENCE-TRANSITION 4,303.44 19,191.97 DIVERSITY CLUB 111.92 112.89

YEARBOOK 3,997.41 9,358.88 CHESS CLUB 110.01 110.01

ART CLUB 3,274.34 2,462.20 GOLF 105.79 105.79

STUDENT ACTIVITIES-ENGLISH 3,142.39 1,441.03 INVISIBLE CHILDREN 101.00 101.00

TENNIS-GIRLS 2,552.87 4,665.42 PING PONG CLUB 100.00 0.00

H & R DUAL CREDIT 1,832.65 0.00 BASKETBALL 87.50 64.50

KEY CLUB 1,507.39 664.64 BIKES, BOARDS, & BLADES CLUB 74.54 155.00

NATIONAL HONOR SOCIETY 1,505.52 1,287.98 WRESTLING 72.31 72.31

FOUNDATION COLLEGE FEES 1,200.00 1,200.00 CARD CLUB 66.18 66.18

GIRLS' ATHLETIC CLUB 1,193.05 528.99 LIFE SKILLS II 46.22 46.22

BAND 1,147.39 3,444.28 SHELBY'S CLUB 25.07 3,380.07

STUDENT RECOGNITION 1,132.81 (812.79) FCCLA CLUB 22.68 (33.72)

MEDIA CLUB 1,045.95 3,462.33 FELLOWSHIP OF CHRISTIAN ATHLETES 15.24 95.24

ORCHESTRA 1,042.99 222.18 KICKAPOO U 8.55 0.00

MCBRIDE ACCOUNT 1,027.98 268.36 PEER MEDIATORS 0.00 0.00

DRAMATICS 888.13 420.21 INDUSTRIAL TECHNOLOGY 0.00 0.00

BASEBALL 876.95 1,049.13 SWIMMING-GIRLS 0.00 (341.51)

COLORGUARD 859.03 (51.15) FRENCH CLUB (5.57) (26.93)

FOUNDATION 844.33 (76.81) TECHNOLOGY CLUB (28.05) 378.73

DANCE TEAM 843.86 (2,772.98) PHYSICS CLUB (111.17) (167.02)

SWIMMING-BOYS 838.70 653.70 TUTORING (222.73) (222.73)

DECA 837.63 (320.77) SOCCER (416.60) 84.70

BASE 737.66 25.29 FBLA CLUB (528.21) 1,253.36

SPANISH CLUB 680.43 290.90 TRACK (881.98) 168.04

PROJECT GRADUATION 629.46 109.81 CHOIR (1,362.00) (499.48)

TOTAL COMBINED BALANCE 202,531.34$ 190,467.03$

Source: The above balances were obtained from the district's general ledger accounting software.

KICKAPOO HIGH SCHOOL

Page | 27

APPENDIX D: HIGH SCHOOL STUDENT ACTIVITY ACCOUNTS

STUDENT ACTIVITY ACCOUNTBalance

6/30/2013

Balance

6/30/2012STUDENT ACTIVITY ACCOUNT

Balance

6/30/2013

Balance

6/30/2012

PEP CLUB $19,976.07 $8,132.40 TEACHER SUPPORT-COALITION $480.00 ($461.54)

SCIENCE DEPARTMENT 15,977.44 10,572.18 FRESHMAN ACTIVITY 463.36 83.10

YEARBOOK 15,686.29 18,409.68 MATH CLUB 451.32 449.62

QUILL & SCROLL 8,810.01 6,881.28 TRACK 445.11 44.70

LASSIES 8,629.85 (800.00) NATIONAL HONOR SOCIETY 437.77 500.50

STUDENT ACTIVITIES-ENGLISH 5,917.03 6,757.93 HISTORY CLUB 433.50 897.50

HISTORY DEPARTMENT 3,889.96 3,398.68 WRESTLING 432.26 721.33

TECHNOLOGY 3,563.26 586.14 CROSS COUNTRY 422.27 0.00

STUDENT COUNCIL 3,499.97 4,535.24 SOFTBALL 412.20 378.20

SPECIAL ED 3,174.74 3,312.92 SWIMMING 372.81 (369.92)

GIRLS BASKETBALL 2,601.20 2,875.95 BASEBALL 366.06 43.49 STUDENT ACTIVITIES-WORLD LANGUAGES

2,593.03 2,593.03 SOPHOMORE ACTIVITY 355.15 979.02

WORLD LANGUAGE CLUB 2,303.64 1,140.80 PROJECT GRADUATION 316.13 (335.77)

VOLLEYBALL 2,231.20 2,217.85 HELPING INTERNATIONAL PEOPLE 278.02 219.30

ART DEPARTMENT 2,185.18 1,940.12 TICKET TO RIDE 266.39 0.00

FCCLA CLUB 2,182.21 2,869.56 EVENTS-PHS 255.95 982.57

BAND 1,884.58 389.11 STUDENT ACTIVITIES-TECH ED 254.36 425.36

TRANSCRIPT FEES 1,658.25 630.02 FBLA CLUB 201.07 (210.82)

NEWSPAPER 1,553.01 1,383.01 SPANISH CLUB 169.67 554.61

ART CLUB 1,401.70 2,436.41 STUDENT ACTIVITIES-BUSINESS ED 132.95 829.29

FOOTBALL 1,321.00 208.09 CONCESSIONS 128.73 6,781.63

BASKETBALL 1,276.06 717.19 MCBRIDE ACCOUNT 117.04 5.02

AER 1,223.03 1,238.21 PING PONG CLUB 100.95 100.95

TESTING & ENTRY FEES 1,221.84 1,031.84 FUTURE EDUCATORS OF AMERICA 87.78 (812.22)

ART EQUIPMENT 1,190.13 165.13 GERMAN CLUB 61.20 61.20

LIBRARY 1,149.00 399.63 BLACK AWARENESS 45.17 45.17

FRESHMAN FOCUS 1,135.28 752.24 GIRLS GOLF 17.94 17.94

GREEN TEAM 1,057.33 1,232.25 GIRLS TENNIS 10.64 10.64

JUNIOR ACTIVITY 1,054.35 674.18 GOLF 8.85 8.85

ORCHESTRA 1,025.47 445.18 SENIOR ACTIVITY 0.00 1,841.52

FOUNDATION 1,000.00 0.00 MEDIA CLUB 0.00 0.00

CHOIR 910.89 (490.70) MEDIA SUPPLIES 0.00 100.01

DECA 896.53 (3,672.30) STUDENT ACTIVITIES-MATH 0.00 (220.68)

ACADEMIC BOWLING 875.14 578.73 SOCCER-GIRLS 0.00 (262.30)

ASL CLUB 866.67 391.00 GIRLS SWIMMING 0.00 1,021.93

BASE 830.17 205.50 BROADCAST JOURNALISM (9.99) (597.06)

TARGET CLUB 771.81 613.78 FRENCH CLUB (381.45) (21.45)

KEY CLUB 715.67 496.44 ACTIVITY-GENERAL (548.14) (703.54)

YOUTH AGAINST CANCER 579.31 2,019.00 TENNIS (716.61) (27.66)

MUSIC HONOR SOCIETY 576.38 842.65 COLORGUARD (749.59) (594.79)

UNDERGROUND CLUB 572.84 503.84 DEBATE CLUB (787.86) (5,930.11)

SCIENCE CLUB 544.57 544.57 W.A.V.E. (794.27) (1,737.23)

SOCCER-BOYS 542.87 363.87 CHEERLEADING (2,909.01) 4,614.67

DANCE 494.28 170.78 DRAMATICS (11,238.77) 565.01

A+/SAT 480.49 221.32 TOTAL COMBINED BALANCE 121,418.69$ 99,912.77$

Source: The above balances were obtained from the district's general ledger accounting software.

PARKVIEW HIGH SCHOOL